Since the great 2007 financial crisis, many companies have been coping to recapture their former glory. The healthcare industry is not spared of this struggle.

This makes the continuous growth of Merck (MRK) all the more impressive, with the company reaching $195 billion in market capitalization and sustaining its rise for over 130 years.

Curiously, Merck’s share price is still in the mid-$70s.

Meanwhile, other large-cap biopharmaceutical companies that offer similar products and services are trading higher.

For instance, the share price for Abiomed (ABMD) is over $330 while Illumina (ILMN) is nearly $400, and Align Technology (ALGN) is at a whopping $600.

Like Merck, investors gravitate towards Abiomed, Illumina, and Align because of their capacity to generate long-term sustainable revenues and boost earnings.

Notably, though, none of them hold the same depth or even breadth of products and services that Merck offers.

Recently, Merck disclosed some of its initiatives to boost the company’s earnings in the near- and long term.

One of the most visible efforts is its collaboration with Johnson & Johnson (JNJ) to help with the manufacturing of JNJ-78436735, in which Merck received federal funding.

While JNJ is one of the biggest healthcare companies across the globe, with a market capitalization of roughly $425 billion, joining forces with Merck will substantially boost its vaccine manufacturing capacity.

For context, JNJ’s goal prior to Merck’s help is to deliver 100 million doses by the end of the second quarter of 2021.

With Merck’s assistance, JNJ can now realistically manufacture up to 3 billion doses in 2022 alone.

This means that JNJ can implement a massive vaccination drive in the next two years since its manufacturing capacity ensures that it can deliver shots to over one-third of the population.

This is obviously good news for everyone as it means that the virus will be contained, but the enhanced manufacturing capacity also means profit accretion for both JNJ and Merck.

This partnership with JNJ is possibly a key factor in Merck’s move to invest heavily in the vaccine business.

Merck recently announced its plans to allocate $20 billion to expand its global vaccine manufacturing network from 2021 to 2024. This would mean an annual investment of $5 billion.

Part of this global vaccine plan is Merck’s acquisition of Pandion Therapeutics (PAND) in 2020.

Another recent initiative of the company is its joint effort with Gilead Sciences (GILD) to develop long-lasting HIV treatments.

Gilead will be in charge of the US market, while Merck will handle the EU and the rest of the international markets.

For starters, the companies will focus on a combination of Merck’s Islatravir and Gilead’s Lenacapavir to create a long-lasting and well-tolerate HIV treatment.

Outside these partnerships, Merck has been working on strengthening its oncology segment.

In fact, its top-selling drug, Keytruda, can be used to medicate an extensive range of indications, which include colorectal, esophageal, and even lung cancers.

At this point, Keytruda is generating north of $16 billion in sales every year and exhibiting roughly 30% growth annually.

Since the drug continues to gain approvals for additional indications, it looks like its growth runway is definitely far from over.

Keytruda is poised to reach $24 billion in annual sales in a few years’ time, which puts it on track to become the best-selling drug in the world by 2023.

Although Keytruda will be under patent protection until 2028, Merck remains active in expanding its oncology pipeline.

By then, Merck is projected to have multiple immunotherapy staples in its portfolio not only derived from its own R&D but also via partnerships like its 2020 collaboration with Alkermes (ALKS) to work on an ovarian cancer study and Immunovaccine (IMV) to cooperate on a blood cancer study.

The total oncology market is estimated to be $200 billion annually, with over 30 million cases projected to be added by 2040.

Overall, Merck is a well-oiled company that continues to deliver good results thanks to strategic acquisitions and partnerships neatly tied up together in a particular domain.

While its rival biotechnology and pharmaceutical companies become hot properties in the market and pose higher price tags, Merck silently moves forward in the shadows of sustainability and familiarity.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-13 14:00:492021-04-19 23:11:39Mega Cap Pharma Up for Grabs

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-13 10:29:532021-04-13 10:29:53Trade Alert - (TSM) April 13, 2021 - SELL-TAKE PROFITS

Now that technology stocks have returned from the grave, it is time to increase our exposure to the sector. After all, we are two weeks into a rally that could last until the rest of the year.

It was the stabilization of interest rates that did the trick. While ten-year US Treasury yields (TLT) were soaring from 0.89% to 1.76%, tech stocks smelled like three-day-old sushi left in the sun.

Now that rates have fallen back to 1.64%, tech stocks have caught on fire. Rates didn’t really have to go down, just stop going up at 100 miles per hour.

Markets are now pricing in the end of the pandemic. So, I have been dusting off some of my favorite trades for a decade ago, when we were dealing with similar levels of panic, despair, and desperation.

Suddenly, the (ROM) came to mind.

The (ROM) is the ProShares Ultra Technology ETF, a 2X long in the top technology shares. It holds the fastest growing, cream of the cream of corporate America which you want to hide behind the radiator and keep forever.

Quality is on sale now and here is where you want to be loading the boat. The $683 million market cap (ROM) even pays a modest 0.17% dividend.

(ROM)’s ten largest holdings include:

Microsoft (MSFT)

Apple (AAPL)

Facebook (FB)

Alphabet (GOOGL)

Intel (INTC)

Cisco (CSCO)

Adobe (ADBE)

NVIDIA (NVDA)

Salesforce (CRM)

Oracle (ORCL)

The major (ROM) holdings, like Apple, Amazon, and Facebook (FB) have gone virtually nowhere for eight months. Yet, their earnings have continued to grow at a feverish 20% annual rate. The stocks were just exhausted and needed a time-out.

The great thing about the (ROM) is that it is one of the most volatile ETFs in the market. Over the past two weeks, the (ROM) has rocketed 20%. From the March 2020 bottom, it has rocketed from $20 to $86.

I’d like a piece of that!

It gets better. The (ROM) HAS OPTIONS. That effectively increases your technology leverage from 2:1 to 20:1 with defined limited risk (you can’t lose any more than you put in).

I’ll give you an example.

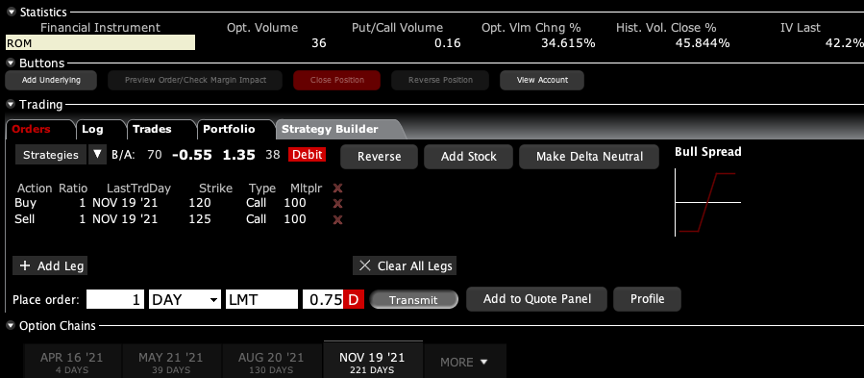

The longest expiration for which (ROM) options are currently trading is November 19, 2021, or six months out. (ROM) is currently trading at $85.03. You can buy the (ROM) November 19 $120-$125 call spread for $0.75.

If tech stocks rise by 23% by November and the (ROM) soars by 47%, then the value of your call spread increases from $0.75 to $5.00, or 466%.

You can engineer yourself closer to the money spreads requiring less prolific moves in tech stocks that will still bring in triple-digit returns,

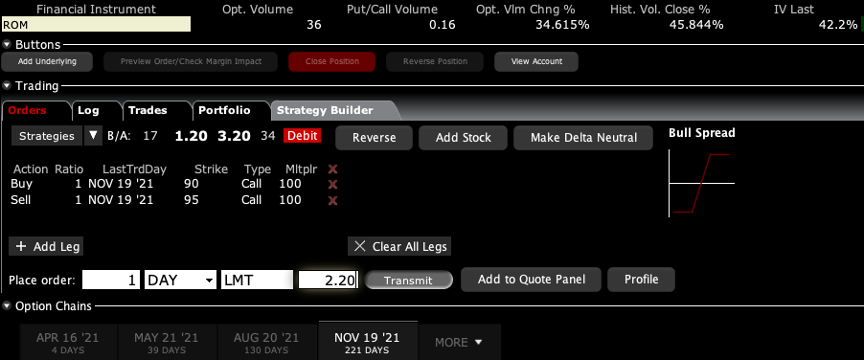

For example, the (ROM) November $90-$95 vertical bull call spreads cost $2.20 and requires only a 5.9% rise in tech stocks, or an 11.8% increase in the (ROM) to appreciate to $5.00 for a gain of 127% in six months.

Remember too that a 2X ETF can cover a lot of ground in a very short time in a new bull market.

It has since done exactly that.

The harder I work, the luckier I get

To learn more about (ROM), please click here for their website.

The Way Forward is Clear

https://www.madhedgefundtrader.com/wp-content/uploads/2020/03/arrow-e1617635474186.png450338Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-13 10:04:352021-04-13 11:14:55Revisiting the ROM

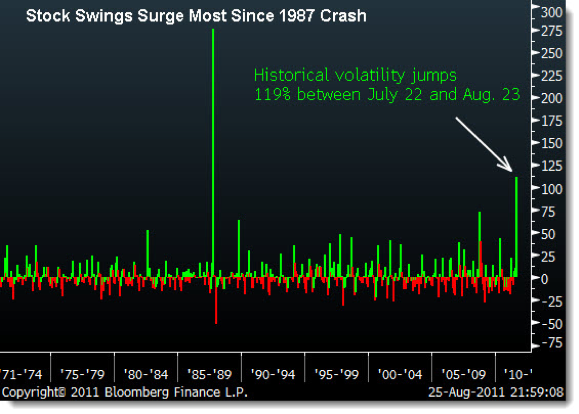

When the Dow crashed 514 points in a single day a few years ago, the market lost a staggering $850 billion in market capitalization. High frequency traders were possibly responsible for half of this move, but generated a mere $65 million in profits, some 7/1,000’s of a percent of the total loss.

Are market authorities and regulators being penny-wise but pound-foolish?

The carnage the HF traders are causing is triggering a rising cry from market participants to ban the despised strategy. Many are calling for the return of the “short sale test tick rule”, or SEC Rule 17 CFR 240.10a-1, otherwise known as the “uptick rule”, which permits traders to execute short sales only if the previous trade caused an uptick in prices.

The rule was created eons ago to prevent the sort of cascading, snowballing selling that we are seeing today. It was repealed on July 6, 2007. Check out a chart of the volatility that ensued and it will make your hair on the back of your neck raise.

Those unfamiliar with how algorithmic trading works, see it as something akin to illegal front running. “Co-location” of mainframes with exchange computers, or having them in adjacent rooms, gives them another head start over the rest of us.

Much of the trading sees HF traders battling each other and involves what used to be called “spoofing”, the placing of large, out-of-the-market orders with no intention of execution.

Needless to say, if you or I tried any of these shenanigans, the SEC would lock us up in the can so fast it would make your head spin.

Many accuse exchange authorities of a conflict of interest, allowing members to reap sizeable custody fees from HF traders, while the rest of us get taken to the cleaners. Co-location fees run in the hundreds of thousands of dollars per customer per month. This is happening while traditional revenue sources, like proprietary trading, are disappearing, thanks to Dodd-Frank. There is no doubt that the volatility is driving the retail investor from the market.

In fact, HF trading has been around since the nineties, back when the uptick rule was still in place and co-location was a term out of Star Trek. But it was small potatoes then, confined to a few niche players like Renaissance, and certainly lacked the firepower to engineer 500-point market swings.

The big problem with this solution is that HF trading now accounts for up to 70% of the daily trading volume. Ban them, and the market volatility will shrink back to double-digit trading ranges that will put us all asleep.

The diminished liquidity might make it difficult for the 800-pound gorillas of the market, like Fidelity and CalPERS, to execute trades, further frightening end investors from equities. It is possible that we have become so addicted to the crack cocaine that HF traders provide us that we can’t live without it?

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/Stock-Swing.png414579John Thomashttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngJohn Thomas2021-04-13 10:02:152021-04-13 11:14:26Bring Back the Uptick Rule!

Beyond Meat (BYND) will most likely retrace back to $90 from its current share price of $130.

The pandemic was a nightmare for most food companies and for the ones that deliver products to restaurants, it was a catastrophe.

BYNDs net revenues of $101.9 million in the fourth quarter of 2020, an increase of 3.5% compared to the fourth quarter of 2019, were in line with expectations of atrocious numbers.

Growth companies are expected to grow 40% year over year each quarter and in a year where many tech companies experienced 5 years of digital transformation in 1, BYNDs performance was quite pitiful.

It could have been worse for BYND.

The loss they experienced in the food service channel was difficult, but sales were partly made up by growth in net revenues in the fourth quarter driven by a 7% increase in volumes sold largely aided by the retail (this is what they call eating BYND burgers at home) channel.

Q4 retail channel sales were up a full 85% year over year, which helped mitigate the 54% year-over-year decline in Foodservice.

The pandemic’s damaging effect was large on supplying places including amusement parks, sports arenas, academic institutions, hotels, corporate catering services, and others.

The 85% uptick in retail growth couldn’t compensate for the drop off in food service channels much like Uber and the Uber Eats conundrum.

Households continued to buy BYND products, and they bought them more frequently.

On average, they're spending more per household on non-meat products.

Another silver lining is in international retail, they saw a sequential acceleration of growth from Q3 to Q4.

International retail net revenues increased 139% year over year, driven mainly by distribution gains in Canada, including in the club stores, where they had no presence in the prior year.

As 2021 develops, we will see a flip in numbers as consumers start to visit their favorite eateries and are less inclined to grill BYND burgers on the patio grill.

This only injects more uncertainty into the numbers for BYNDs management and the headway they made in the retail channel could be mostly given back.

Naturally, BYND burgers just isn’t that software program that is essential, and the business of food tech is still fighting with the business of normal food like real meat such as cow-based beef and pig-based pork.

Many software programs simply do not have to duel with their analog selves which is why any sort of meaningful investments into a company like BYND is illogical.

Anyone who loves eating plant-based burgers should eat these protein-based burgers and leave the stock alone.

What’s on the horizon for BYND?

One word – competition.

Impossible Foods Inc. is planning to go public in the next year and is exploring either an initial public offering or a merger in a SPAC deal.

This would value the company at around $10 billion.

Once a hard-to-find item available at only expensive, trendy eateries, Impossible products are now on menus at national chains including Burger King.

Fast-food chains have fared significantly better than independent restaurants since the pandemic began, giving Impossible an added boost.

It has also been growing its grocery presence, cutting its suggested retail prices by 20% at U.S. grocery stores in February in its ongoing push to compete with real beef.

BYNDs management downplayed pandemic pressures to the business as “transitory”, but the problem with that is they are transiting right into fierce competition who have signaled willingness to enter into a price war against them.

Others like Kroger (KR) have bigger pockets and will have used the pandemic to plot their path against BYND.

Basically, what I am saying is that the first-mover advantage has disappeared forever, an unfortunate consequence for BYNDs future trajectory, and I don’t see a lot of upside to underlying shares in the short term.

In the short-medium term, Beyond Meat will first, need to rejuvenate their foodservice business and prove to investors that covid didn’t just knock it out.

Second, there is no guarantee that BYNDs food service will come back right away, this could be a hard slog for a few years to reach 2019 numbers and that’s still an if.

And third, they will need to prove they are better than Impossible Foods and the rest of them while most likely lowering the prices of their product.

Unluckily, the pandemic didn’t deliver 5 years of innovation in 1 year for BYND and there are more questions than answers moving forward.

Outside the internet, the presence of numerous physical inputs has the chance to go haywire which is why I sometimes believe the bore of buying Microsoft or Alphabet until death isn’t such a bad idea.

Investors might want to keep their tech investors from ever exposing themselves to real-world problems even if I think Uber is a great investment for 2021.

I would recommend investors to avoid this crowded space of food tech and let them cudgel each other down to zero. Whoever wins in the end might be worth a flier.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/beyond-meat.png320772Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-12 14:02:562021-04-13 19:37:59Should I Buy The Beyond Meat Dip?

“An asteroid or a supervolcano could certainly destroy us, but we also face risks the dinosaurs never saw: An engineered virus, nuclear war, inadvertent creation of a micro black hole, or some as-yet-unknown technology could spell the end of us.” – Said Founder and CEO of Tesla Elon Musk

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/elon-musk.png410438Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-12 14:00:522021-04-12 15:04:41April 12, 2021 - Quote of the Day

Her name is Goldilocks. The neighbors have been sneaking peeks at her through the curtains at night and raising their eyebrows because she is slightly older than my kids, or about 50 years younger than me.

I have no complaints. Suddenly, the world looks a brighter place, I’m getting up earlier in the morning, and there is a definite spring in my step. My doctor asks me what I’ve been taking lately.

It helps a lot too that the value of my stock portfolio is going up every day.

I don’t know how long Goldilocks will stay. The longer the better as far as I am concerned. After all, I’m a widower twice over, so anyone and anything is fair game. But two or three months is reasonable and possibly until the end of 2021.

That’s the way it is with these May-December relationships, or so my billionaire friends tell me, who all sport trophy wives 30 years younger.

At my age, there are no long-term consequences to anything because there is no long-term. I don’t even buy green bananas.

I have been expecting exactly this month’s melt-up for months and have been positioning both you and me to take maximum advantage. I am making all my pension fund and 401k contributions early this year to get the money into the stock market as fast as possible.

So far so good.

More money piled into stocks over the past five months than over the previous 12 years. And this pace is set to continue. Those who sold a year ago are buying back. $2 trillion in savings enforced by the pandemic are also going into stocks. And after all, there is nothing else to buy.

If all this sounds great, it’s about to get a lot better. Europe and Asia are still missing in action, thanks to a slower vaccine rollout. When they rejoin the global economy in the fall, it will further throw gasoline on the fire. Exports will boom.

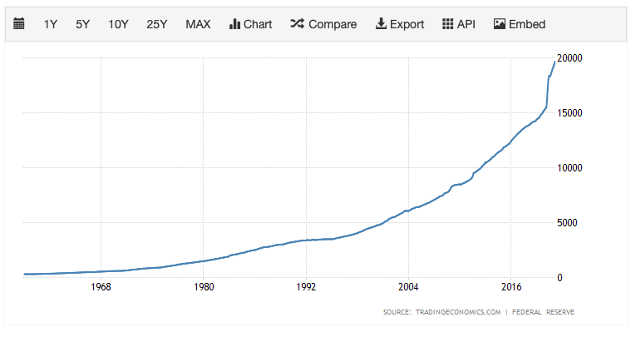

The money supply is growing at an astonishing 26% annual rate, thanks to QE forever and massive government spending. That’s the fastest rate on record. In ten years, a PhD will write a paper on how much of this ended up in the stock market. Today, I can tell you it is quite a lot.

In the meantime, make hay while the sun shines. What am I supposed to talk to about with Goldilocks at night anyway?

Do you suppose she trades stocks?

50 Years of Money Supply Growth is Going Vertical

A face-ripping rally is on for April, or so says Strategas founder Lee. A Volatility Index with a $17 handle is sending a very strong signal that you should be loading up on energy, industrials, consumer discretionary, and travel-related stocks. Avoid “stay at home” stocks like Covid-19, which are extremely overcrowded. I’m using dips to go 100% long.

It’s all about infrastructure, 24/7 for the next three months, or until the $2.3 trillion spending package is passed. It might have to take a haircut first. Biden has set a July 4 target to close thousands of deals and horse-trading. With the S&P 500 breaking out above $4,000 and the financial markets drowning in cash, the plan could be worth another 10% of market upside. Would your district like a new bridge? Maybe a freeway upgrade? The possibilities boggle the mind.

US Manufacturing hits a 37-year high in March, driven by massive new orders front-running the global economic recovery. The Institute for Supply Management publishes a closely followed index that leaped from 60.8 to 64.7. Buy before the $10 trillion hits the market.

US Services Industry hits record high, with the Institute of Supply Management Index soaring from 55.3 to 63.7 in March. The ending of Covid-19 restrictions was the major factor. Roaring Twenties here we come!

US Job Openings are red-hot, coming in at 7.4 million compared to an expected 7 million, according to the JOLTS report. It’s the best report in 15 months. It's a confirmation of the ballistic March Nonfarm Payroll report out on Friday.

US Auto Sales surge in Q1, shaking off the 2020 Great Recession. It’s a solid data point for the recovery, despite a global chip shortage. General Motors (GM) was up 4%, thanks to recovering Escalade sales, and strong demand is expected for the rest of 2021. Toyota (TM) was up 22% and Fiat Chrysler 5%. “Pent-up demand” is a term you’re going to hear a lot this year. The Economic boom will run through 2023, says JP Morgan chairman Jamie Diamond, one of the best managers in the country. In his letter to shareholders, he says 10% of his workforce will work permanently from home. Zoom (ZM) is here to stay. Fintech is a serious threat to legacy banks, which is why we love Square (SQ) and PayPal (PYPL). Keep buying (JPM) on dips. Interest rates will rise for years, but not fast enough to kill the bull market.

IMF predicts 6.0% Global Growth for 2021, the highest in 40 years. China will grow at 8.4%. It’s a big improvement since their January prediction. The $1.9 trillion US Rescue is stimulating not just America’s economy, but that of the entire world. Expect a downgrade to the 3% handle in 2022, which is still the best in a decade.

Fed Minutes say Ultra Dove Policy to Continue, so say the minutes from the March meeting. Rates won’t be raised on forecasts, predictions, or crystal balls, but hard historic data. That’s another way of saying no rate hikes until you see the whites of inflation’s eyes. $120 billion of monthly bond buys will continue indefinitely. Bonds dropped $1.25 on the news. Sell all (TLT) rallies in serious size. It’s still THE trade of 2021.

Disneyland in LA to open April 30 after a one-year hiatus. It’s time to dust off those mouse ears. The last time the Mouse House was closed this long, antiwar protesters took to Tom Sawyer’s Island and raised the Vietcong flag (I was there). Some 10,000 cast members have been recalled. Only 15% capacity will be allowed to California residents only. The new Avengers Campus will open on June 4. The company is about to make back the 25% of revenues it lost last year, but with a much lower cost base. Buy (DIS) on dips.

Was that inflation? The Producer Price Index jumped by 1.0% in March compared to an expected 0.40%. It’s the second hot month in a row. Basically, the price of everything went up. The YOY rate is an astonishing 4.04% a near-decade high. If it looks like a duck and quacks like a duck….Stocks didn’t like it….for about 15 minutes.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 5.80% gain during the first nine days of April on the heels of a spectacular 20.60% profit in March.

It was a very busy week for trade alerts, with five new positions. Sensing an uncontrolled market melt-up for the entire month piled on aggressive long in Visa (V), JP Morgan (JPM), and Microsoft (MSFT). I also poured on a large short position in bonds (TLT) with a distant May expiration.

My now large Tesla (TSLA) long expires in 4 trading days. Half of my even larger short in the bond market (TLT) also expires then.

That leaves me 100% invested for the sixth time since last summer. Make hay while the sun shines.

My 2021 year-to-date performance soared to 49.89%. The Dow Average is up 11.60% so far in 2021.

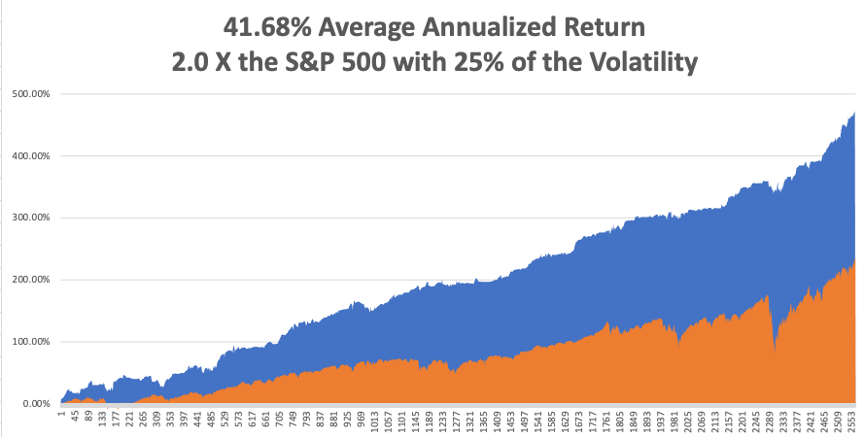

That brings my 11-year total return to 472.44%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 41.68%, the highest in the industry.

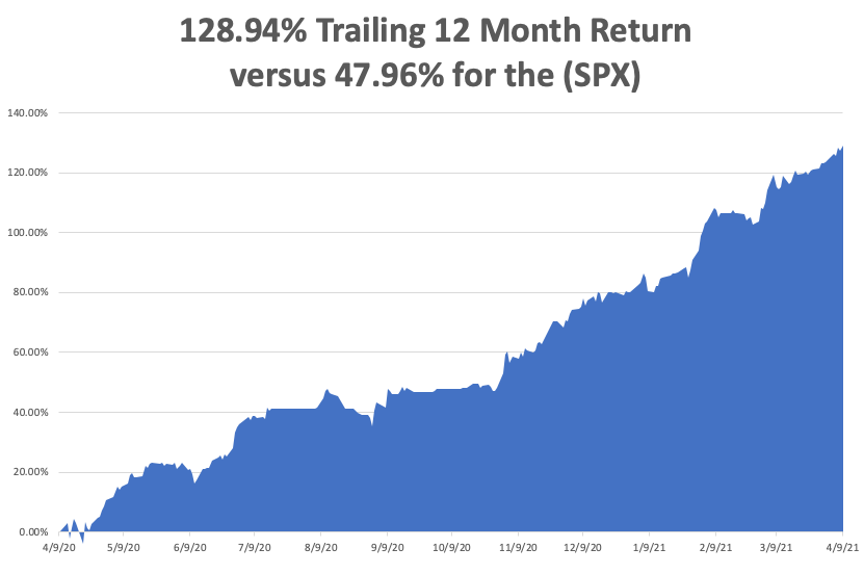

My trailing one-year return exploded to positively eye-popping 128.94%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives. Every time I think these numbers can’t be topped, that increases by another 10% during the following two weeks.

We need to keep an eye on the number of US Coronavirus cases at 30.6million and deaths topping 563,000, which you can find here.

The coming week will be dull on the data front.

On Monday, April 12, at 11:00 AM, the US Consumer Inflation Expectations for March is released.

On Tuesday, April 13, at 8:30 AM, US Core Inflation for March is published.

On Wednesday, April 14 at 2:00 PM, the Federal Reserve Beige Book is out. On Thursday, April 15 at 8:30 AM, the Weekly Jobless Claims are printed. We also learn US Retail Sales for March.

On Friday, April 16 at 8:30 AM, we get the Housing Starts for March. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, the whole Archegos blow-up reminds me that there are always a lot of con men out there willing to take your money. As PT Barnum once said, “There is a sucker born every minute.”

I’ll tell you about the closest call I have ever had with one of these guys.

In the early 2000s, I was heavily involved in developing a new, untried, untested, and even dubious natural gas extraction method called “fracking.” Only a tiny handful of wildcatters were even trying it.

Fracking involved sending dynamite down old, depleted wells, fracturing the rock 3,000 feet down, and then capturing the newly freed up natural gas. If successful, it meant that every depleted well in the country could be reopened to produce the same, or more gas than it ever had before. America’s gas reserves would have doubled overnight.

A Swiss banker friend introduced me to “Arnold” of Amarillo, Texas who claimed fracking success and was looking for new investors to expand his operations. I flew out to the Lone Star state to inspect his wells, which were flaring copious amount of natural gas.

Told him I would invest when the prospectus was available. But just to be sure, I hired a private detective, a retired FBI man, to check him out. After all, Texas is notorious for fleecing wannabe energy investors, especially those from California.

After six weeks, I heard nothing, so late on a Friday afternoon, I ordered $3 million sent to Arnold’s Amarillo bank from my offshore fund in Bermuda. Then I went out for a hike. Later that day, I checked my voice mail and there was an urgent message from my FBI friend:

“Don’t send the money!”

It turns out that Arnold had been convicted of check fraud back in the sixties and had been involved in a long series of scams ever since. But I had already sent the money!

I knew my fund administrator belonged to a certain golf club in Bermuda. So, I got up at 3:00 AM, called the club Starting Desk and managed to get him on the line. He said I had missed the 3:00 PM Fed wire deadline on Friday and the money would go out first thing Monday morning. I told him to be at the bank at 9:00 AM when the doors opened and stop the wire at all costs.

He succeeded, and that cost me a bottle of Dom Perignon Champaign, which fortunately in Bermuda is tax-free.

It turned out that Arnold’s operating well was actually a second-hand drilling rig he rented with a propane tank buried underneath that was flaring the gas. He refilled the tank every night to keep sucking in victims. My Swiss banker friend went bust because he put all his clients into the same project.

I ended up making a fortune in fracking anyway with much more reliable partners. No one had heard of it, so I bought old wells for pennies on the dollar and returned them to full production. Then gas prices soared from $2/MM BTU to $17. America’s gas reserves didn’t double, they went up ten times.

I sold my fracking business in 2007 for a huge profit to start the Diary of a Mad Hedge Fund Trader.

It is all a reminder that if it is too good to be true, it usually is.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-8.png422564Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-12 09:02:542021-04-12 14:11:44The Market Outlook for the Week Ahead, or The Melt Up is On!

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.