Mad Hedge Biotech and Healthcare Letter

December 30, 2021

Fiat Lux

Featured Trade:

(“WHOLE-PERSON CARE” IS THE FUTURE OF HEALTHCARE)

(TDOC), (PFE), (BNTX), (MRNA)

Mad Hedge Biotech and Healthcare Letter

December 30, 2021

Fiat Lux

Featured Trade:

(“WHOLE-PERSON CARE” IS THE FUTURE OF HEALTHCARE)

(TDOC), (PFE), (BNTX), (MRNA)

Alongside the likes of Pfizer (PFE), BioNTech (BNTX), and Moderna (MRNA), another name stood out during the pandemic: Teladoc (TDOC).

This telehealth company was one of the biggest breakout stars amid the worst periods of the COVID-19 pandemic, with its shares skyrocketing 138%—a feat sustained throughout 2020.

However, Teladoc’s narrative faltered in 2021.

The change wasn’t in terms of the company’s financial future. If anything, the company had been consistent in recording increasing revenues and visits. Teladoc actually even boosted its earnings guidance this year.

Despite all these, the stock fell by roughly 50%.

Looking at the reasons for this baffling fall, it became evident that investors started to fret over the gradual reopening of the economy and the return of people to offices.

They believed that these would result in patients abandoning virtual health consultations and opting to go back to their doctor’s clinics.

As far as we can see, though, that has not happened yet.

Moreover, the recent events and predictions about the future all but guarantee that these fears are baseless. Now, this raises the question of whether or not Teladoc is set to rebound in 2022.

It’s sort of obvious that the company has been moving alongside the COVID-19 headlines, but this doesn’t necessarily mean that Teladoc’s long-term plans depend heavily on the pandemic.

The vital thing we need to understand is that telehealth is here to stay. The pandemic merely accelerated the adoption of this groundbreaking technology.

There’s actually a widespread misunderstanding of Teladoc’s goal over the long term. Some investors seem to assume that the company aims to replace physical healthcare services.

This is extremely far from the truth.

What Teladoc wants to do is simply provide a complementary platform for the physical system.

That is, the company aims to virtualize all the things that can be virtualized and serve as the front door to the actual physical care.

Doing so will offer a more convenient option for patients and for the entire healthcare industry because this new and improved system can generate savings and better allocate resources in one of the most woefully managed and inefficient sectors across the globe.

Our current traditional healthcare system is extremely fragmented. Patients visit an average of 19 doctors in their lifetime, and every new doctor typically necessitates a new practice, a new professional relationship, and another set of medical records.

To get rid of the stress, prevent “wasting time” in waiting rooms, and sometimes receive unsatisfying experiences, which can even lead to unresolved or undetected health issues, Teladoc has come up with a comprehensive system.

It built Primary360, which it dubbed as the “whole-person care” platform.

The idea behind “whole-person care” is to bring all the services, including mental health, primary healthcare, and even treatments for chronic conditions, in one virtual package. This can then be easily accessed via the patient’s phone.

Teladoc integrates data and analytics to develop personalized healthcare experiences for its users, which became even more accurate and comprehensive thanks to its $18.5 billion acquisition of Livongo.

Another advantage in acquiring Livongo is its ability to work with AI.

Virtual care has the ability to offer more proactive solutions as opposed to reactive treatments.

Having a massive set of data, Teladoc can provide proactive measures to manage or prevent symptoms instead of mitigating them when they manifest.

After all, what would patients want more?

Their doctors informing them that they have a high risk of a heart attack in the following month if they fail to receive treatment or wait until it actually happens?

Wearables, such as smartwatches and Oura rings, can send data to Teladoc, which can then be used to prevent these kinds of health crises from arising.

Aside from Livongo, Teladoc has also acquired BetterHelp in 2015 for $4.5 million to form part of its “whole-person care” platform.

This acquisition, which has been on track to rake in $100 million in revenue in 2021, is geared towards mental health services.

Teladoc’s earnings reports in 2021 have been reassuring. In the third quarter, for instance, the company’s revenue skyrocketed 81% while patient visits rose 37% to reach over 3.9 million.

Meanwhile, the company estimates the “whole-person care” to be worth roughly $75 billion within its current client base.

Moreover, the National Labor Alliance of Health Care Coalitions, the largest organization of labor groups, announced that it will make Teladoc’s complete set of services available to all its members.

For context, these members pay for the health services of over 6 million individuals.

Going back to the question of whether Teladoc shares will bounce back in 2022, I think it’s clear that it can easily recover given its current trajectory.

In 2020, the telehealth industry was valued at $62.45 billion. By 2030, the telemedicine segment worldwide is projected to reach more than $431 billion.

Meanwhile, the compound annual growth rate (CAGR) from 2021 until 2030 is estimated to be at 26%.

Given Teladoc’s pioneering status, the company may even surpass the expectations from the industry. At a target 2022 revenue of $2.6 billion and $4 billion by 2024, the company’s projected CAGR is at 25% to 30% in the next three years.

Undeniably, Teladoc has fallen out of favor this year. However, the company is far from underperforming.

In fact, it has been doing an excellent job at sticking to its long-term objectives.

Looking at its low valuation at the moment, Teladoc holds the potential to become a highly rewarding venture for long-term investors who are capable of focusing on the fundamentals instead of the short-term noise.

Mad Hedge Bitcoin Letter

December 30, 2021

Fiat Lux

Featured Trade:

(CRYPTO PASSIVE INCOME THE RIGHT WAY)

(CELSIUS NETWORK), (BTC), (ETH), (SNX), (CEL), (LINK), (UNI), (AAVE)

So global yields are in the toilet today?

Savings accounts don’t do what they used to do, do they?

How about we try out a certificate of deposit (CD) to harvest some cash?

Are there simply no other interest-bearing vehicles one can park capital in and gain a healthy return?

I would say you are right, but then I would be the fool here and I am certainly not in that line of work.

I will tell you — there is an elixir to the anathema!

Enter Celsius.

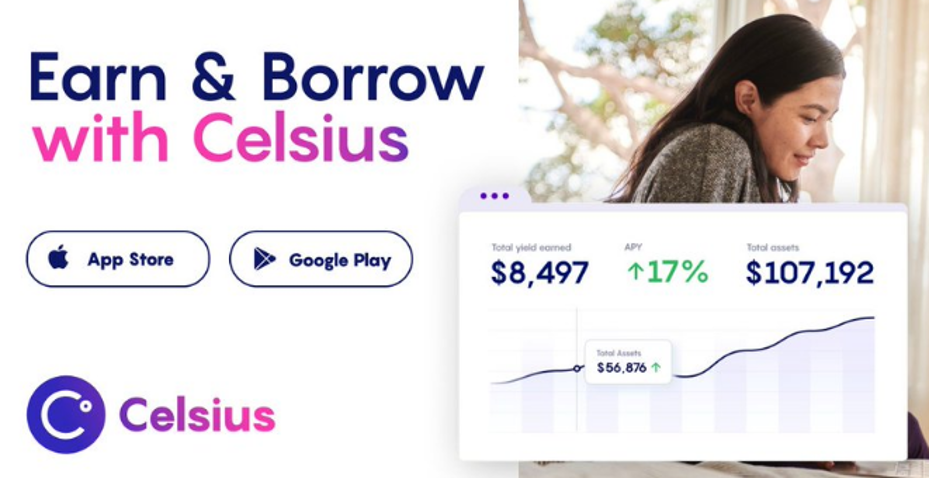

Celsius is a crypto-based financial service hoping to disrupt traditional financial services.

They offer cryptocurrency savings accounts that yield high annual interest rates up to 17% annually. They do this by lending cryptocurrency out to institutional and retail traders who seek to leverage their positions.

Since these platforms require collateral to receive a loan, investors can be sure that the loan will be paid back one way or another.

While these rates are floating interest rates, meaning they can change with the market, they’re relatively stable month-over-month.

These loans are over-collateralized, which means the risk of default is lower than it would be for a standard loan. To this day there has never been a default for any coin on this specific cryptocurrency lending platform.

How Do Celsius Make Money?

Celsius primarily generates revenue through its crypto lending service. The company lends assets to users at a higher interest rate than it pays them for storing their assets on the platform.

Celsius has more cryptocurrencies available for interest-bearing accounts, including BTC, ETH, SNX, CEL, LINK, UNI, and AAVE to name a few.

Payouts and Withdrawals

Celsius users can withdraw their funds at any time without incurring additional fees. Those who wish to withdraw over $50,000 with a single transaction need to wait 24 to 48 hours for it to process. The company makes its weekly interest payments on Mondays.

Let the compound interest payments pile up all while exposed to minimal market risk.

Celsius confirms its holdings of $20,366,621,718 in cryptocurrency assets as of August 13, 2021.

In less than one year, Celsius has grown its total asset holdings from $1 billion to over $20 billion.

Do you want to be part of this 20X growth story?

As part of its Proof of Community (POC) and rewards explorer, Celsius provides real-time data about its assets, loans, users, and rewards paid.

This asset growth trajectory is parabolic with Celsius confirming it is adding close to $1B a month in new assets, as the company trends towards the number one position in total asset holdings in the crypto industry.

For years the traditional banking business has conditioned us naïve folk to accept steep fees and no yield earnings on holdings as the status quo.

I will tell you right now that it’s a load of garbage and nobody should accept these pitiful offers from dinosaur banks.

There is so much more out there that we can access now because of crypto.

With that failing model ripe for disruption, Celsius was built to give consumers what banks never could — a community-oriented platform that provides income and financial independence and it delivers it with a bang.

At the start, Celsius had set a goal to bring the next 100 million people into crypto. Today, they have over 950,000 users worldwide.

Celsius has even just launched its crypto-backed lending service in California following regulatory approval.

The California expansion enables the firm to enlarge its footprint in one of the fintech capitals of the world — California.

The firm claims that it now is "one of the most accessible and affordable lenders in California."

The loans can be issued in both United States dollars and stable coins, the minimum loan value is $500, the process is instant, does not need proof of income or credit check.

You are not dreaming — this is the real deal.

Wake up to fresh crypto interest payment receivables on Monday morning easily convertible into fiat currency.

Participate in one of the most unique crypto deals in the world.

To check out this deal of a lifetime, click here to visit their website.

“Cryptocurrencies may hold long-term promise, particularly if the innovations promote a faster, more secure and more efficient payment system.” – Said 14th Chair of the US Federal Reserve, from 2006 to 2014 Ben Bernanke

Global Market Comments

December 30, 2021

Fiat Lux

Featured Trade:

(DINNER WITH DAVID POGUE),

(TSLA)

Mad Hedge Technology Letter

December 29, 2021

Fiat Lux

Featured Trade:

(AUTOMATION AND BANKING)

(SQ), (PYPL), (APPL), (AMZN)

Automation is taking place at warp speed displacing employees from all walks of life.

According to a recent report, the U.S. financial industry will depose of 200,000 workers in the next decade because of automating efficiencies.

Yes, humans are going the way of the dodo bird and banking will effectively become algorithms working for a handful of executives and engineers.

The x-factor in this equation is the direct capital of $150 billion annually that banks spend on technological development in-house which is higher than any other industry.

Welcome to the world of lower cost, shedding wage bills, and boosting performance rates.

We forget to realize that employee compensation eats up 50% of bank expenses.

The 200,000 job trimmings would result in 10% of the U.S. bank jobs getting axed.

The hyped-up “golden age of banking” should deliver extraordinary savings and premium services to the customer at no extra cost.

This iteration of mobile and online banking has delivered functionality that no generation of customers has ever seen.

The most gutted part of banking jobs will naturally occur in the call centers because they are the low-hanging fruit for the automated chatbots.

A few years ago, chatbots were suboptimal, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers are unaware they are communicating with an artificially engineered algorithm.

The wholesale integration of automating the back-office staff isn’t the end of it, the front office will experience a 30% drop in numbers sullying the predated ideology that front office staff are irreplaceable heavy hitters.

Front-office staff has already felt the brunt of downsizing with purges carried out from 2018 representing an eighth year of continuous decline.

Front-office traders and brokers are being replaced by software engineers as banks follow the wider trend of every company transitioning into a tech company.

The infusion of artificial intelligence will lower mortgage processing costs by 30% and the accumulation of hordes of data will advance the marketing effort into a smart, multi-pronged, hybrid cloud-based and hyper-targeted strategy.

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash of 2001 until the sub-prime crisis of 2008 adding around half a million jobs on top of the 1.5 million that existed then.

After the subsidies wear off from the pandemic, I do believe that the banking sector will quietly put in the call to trim even more.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

This type of human hiring will likely never be seen again in the U.S. financial industry.

Recomposing banks through automation is crucial to surviving as fintech companies like PayPal and Square are chomping at the bit and even tech companies like Amazon and Apple have started tinkering with new financial products.

And if you thought that this phenomenon was limited to the U.S., think again, Europe is by far the biggest culprit by already laying off 63,036 employees in 2019, more than 10x higher the number of U.S. financial job losses and that has continued in 2020 and 2021.

In a sign of the times, the European outlook has turned demonstrably negative with Deutsche Bank announcing layoffs of 40,000 employees through 2023 as it scales down its investment banking business.

Germany banks are also passing on the burden of negative interest rates to their clients.

A recent survey by Deutsche Bundesbank shows that 58% of banks are charging all savers negative interest rates while others only target wealthy and corporate clients.

If the U.S. dips into negatives rates in the future, expect the same nasty effect on job force cuts that Europe has experienced.

Either way, don’t tell your kid to get into banking, because they will most likely be feeding on scraps at that point.

THE LAST STAGE OF HUMAN-FACING BANK SERVICES IS NOW!

Global Market Comments

December 29, 2021

Fiat Lux

Featured Trade:

(MY OLD PAL, LEONARDO FIBONACCI),

(TESTIMONIAL)

Mad Hedge Biotech and Healthcare Letter

December 28, 2021

Fiat Lux

Featured Trade:

(ANOTHER VICTIM OF OVERBLOWN FEARS)

(BMY), (PFE), (BNTX), (MRNA), (MRK)