Global Market Comments

March 28, 2019

Fiat Lux

Featured Trade:

(JOIN US AT THE MAD HEDGE LAKE TAHOE, NEVADA, CONFERENCE, OCTOBER 25-26, 2019)

(THE REBIRTH OF THE MASTER LIMITED PARTNERSHIP),

(USO), (AMLP), (FPL), (MLPS), (MLPX)

Global Market Comments

March 28, 2019

Fiat Lux

Featured Trade:

(JOIN US AT THE MAD HEDGE LAKE TAHOE, NEVADA, CONFERENCE, OCTOBER 25-26, 2019)

(THE REBIRTH OF THE MASTER LIMITED PARTNERSHIP),

(USO), (AMLP), (FPL), (MLPS), (MLPX)

Global Market Comments

March 27, 2019

Fiat Lux

Featured Trade:

(JUMP ON THE VERTEX BANDWAGON),

(VRTX), (CRSP),

(MAD HEDGE FUND TRADER CELEBRATES ITS 11-YEAR ANNIVERSARY)

The biotech industry has at least 500 stocks listed on the market today. These companies range from huge biotech firms with several blockbuster drugs to humble money-losing startups still on the lookout for their first big break.

Among these companies, Vertex Pharmaceuticals Incorporated (VRTX) presents a compelling case that could attract investors.

Recent developments on Vertex's triple-combination treatment for cystic fibrosis (CF) have been predicted to spur the company's revenues this year in a major way. If the results of the studies turn out successful, then Vertex is on the verge of becoming the sole treatment provider to at least 90% of the people suffering from this severe genetic condition. That’s a nice monopoly to have.

While the recent developments have yet to aggressively show its effect in Vertex stock, the company has already recorded an impressive 160% growth since 2017 and this is anticipated to go higher in the years to come.

At present, the annual revenue of Vertex is recorded as $3 billion, while major competitors like Pfizer has $53.4 billion, Bristol-Myers Squibb has $22.6 billion, and Novartis has $51 billion. In order words, there is plenty of room to grow.

Just how far can Vertex shares go?

Let's take a look at previous reports on the company. Its December 2018 financial report reveals that its earnings per share jumped by 113% year-over-year to $1.3. Its quarterly revenues increased by 40% and reached $869.44 million -- a gigantic 39.7% leap from the $622.63 million it achieved during the same period in the previous year.

While the March 2019 EPS for this company is anticipated to go down to $0.68 compared to the $0.76 recorded the same period last year, its 2020 EPS is projected to get a 49.46% boost. With that estimate, Vertex is expected to reach its long-term annual earnings growth rate of 53.86%.

How can investors be sure that Vertex continues with its remarkable progress?

The company's moves in the past months have been quite promising. A major factor that could guarantee its success is its dominance in the CF market. At the moment, Vertex has three approved CF drugs available in the market: Kalydeco, Orkambi, and Symdeko.

Of these three, two are already considered as blockbuster products while Symdeko is poised to hit the $1 billion yearly sales mark this year.

Another promising reason to invest in Vertex is its move to expand the addressable CF market it currently covers. If the company succeeds in cornering the market for treating younger patients, then its target population will increase from 39,000 to 44,000.

Vertex is also working towards gaining approval for a triple-drug combo this year. The biotech company projects an additional 24,000 patients globally to benefit from this triple-drug regimen.

Should all these plans fall into place, Vertex would see a 75% expansion on its addressable CF market in the years to come.

Although CF has been the focus of Vertex in the previous years, the company also intends to widen its scope and plans to conduct early-stage clinical studies for at least two new diseases this year.

This move would prove to be beneficial in the long-term considering the decision of AbbVie Inc (ABBV) to join the triple-drug CF race. So far, AbbVie has a long way to go before it can catch up with Vertex's progress in this arena especially since the latter practically has a monopoly as it alone offers the drugs that can treat the underlying causes of CF.

Vertex's collaboration with CRISPR Therapeutics (CRSP) on gene-editing treatments, which aim to treat rare blood disorders beta-thalassemia and sickle cell disease, is yet another promising development for the company.

All in all, Vertex is a good biotech stock to invest in today. However, its plans are not foolproof.

There remains the risk that its pipeline candidates fail at clinical trials or that the company loses its bids for regulatory approvals. Nonetheless, it's a promising stock to add to your portfolio especially since the company has more than doubled its stock in the past two years.

High risk, high gain. Welcome to the world of biotech stocks.

The Diary of a Mad Hedge Fund Trader is now celebrating its 11th year of publication.

During this time, I have religiously pumped out 1,500 words a day, or eight double-spaced typed pages, of original, independent-minded, hard-hitting, and often wickedly funny research.

I’ve been covering stocks, bonds, commodities, energy, precious metals, real estate, and agricultural products.

You’ve been kept up on my travels around the world and listened in on my conversations with those who drive the financial markets.

I also occasionally opine on politics, but only when it has a direct market impact, such as with the recent administration's economic and trade policies.

The site now contains over 11 million words or 13 times the length of Tolstoy’s epic War and Peace.

Unfortunately, it feels like I have written on every possible topic at least 100 times over.

So, I am reaching out to you, the reader, to suggest new areas of research that I may have missed until now which you believe justify further investigation.

Please send any and all ideas directly to me at support@madhedgefundtrader.com/, and put “RESEARCH IDEA” in the subject line.

The great thing about running an online business is that I can evolve it to meet your needs on a daily basis.

Many of the new products and services that I have introduced since 2008 have come at your suggestion. That has enabled me to improve the product’s quality to your benefit.

This originally started out as a daily email to my hedge fund investors giving them an update on fast market-moving events. That was at a time when the financial markets were in free fall and the end of the world seemed near.

Here’s a good trading rule of thumb: Usually, the world doesn’t end. History doesn’t repeat itself, but it certainly rhymes.

The daily emails gave me the scalability that I so desperately needed. Today’s global mega enterprise grew from there. Today, the Diary of a Mad Hedge Fund Trader and its Global Trading Dispatch is read in over 140 countries by 24,000 followers.

I’m weak in North Korea and Mali, in both cases due to the lack of electricity. But that may change.

If you want to read my first pitiful attempt at a post, please click here for my February 1, 2008 post.

It urged readers to buy gold at $950 (it soared to $1,920), and buy the Euro at $1.50 (it went to $1.60).

Now you know why this letter has become so outrageously popular.

Unfortunately, I also recommended that they sell bonds short. I wasn’t wrong on that one, just early, about eight years too early.

I always get asked how long will I keep doing this?

The government tells me that the latest I can start drawing down on my retirement funds and Social Security is 70. That’s some three years off for me.

Given the absolute blast I have doing this job, that is highly unlikely. Take a look at the testimonials I get only an almost daily basis and you’ll see why this business is so hard to walk away from (click here for those).

In the end, you are going to have to pry my cold dead fingers off of this keyboard to get me to give up.

Fiat Lux (let there be light).

Global Market Comments

March 26, 2019

Fiat Lux

Featured Trade:

(WHY I’M SELLING SHORT TESLA SHARES),

(TSLA)

The news is out that new Tesla (TSLA) new car registrations in the major states are falling off a cliff. California, New York, and even Texas are the major culprits.

The company says the ramp up in mass production of the Tesla 3 is the main reason, and that car registrations, in any case, are a deep lagging indicator. (No kidding! I bought a Model X P100D in Nevada in November and it is still not registered).

Analysts say it is because the electric car subsidy was chopped in half by the Trump administration this year from $7,500 to $3,750 per vehicle, and it is going to zero next year, thus demolishing the Tesla 3 market for entry-level low-end buyers. They also point to the company’s fragile financial condition which could be going bankrupt at any time.

For whatever reason, I believe that the shares will break two-year support on the charts and plunge to new lows. At the very least, Tesla shares are capped for the time being.

I, therefore, sold short Tesla shares yesterday.

As much as this looks like a great short-term trade, I love Tesla long term and see it as a potential ten bagger from current price levels. Tesla will become the world’s largest car company within a decade and become the first car company with a $1 trillion market valuation.

As long as I have been following Tesla since the early venture capital days, it has been going bankrupt. It was going bankrupt during the move in the share price from $16.50 to $394, and it is going bankrupt today.

When I pulled up to the Fremont factory last week, I couldn’t believe what I found. There was a version 3 supercharger that would top up my battery at the staggering rate of 1,000 miles an hour!

That meant that with 50 miles of range left on my 300-mile range Model X battery, I could get a full charge in 15 minutes! The electric power was coming down the cable so fast that it had to be liquid-cooled.

I pinched myself to make sure I hadn’t fallen into a Star Trek movie. The V3 supercharger will soon be available across the country. No other car company is close to achieving something like this.

The fact is that I have been subjected to an unrelenting torrent of bad news, rumors, and envy since I first bought the shares at $16.50 ten years ago. This is the most despised company in the universe and regularly sits among the top five companies with the greatest short interest, often above 25%.

But I guess this is what happens when you take on big oil, the Detroit big three, the advertising industry, labor unions, and the entire Republican party all at once. By my calculation, Tesla is a disruptive threat to about 50% of the US GDP all at once.

I ignore them all and just look at the numbers. Here they are.

1) Tesla has increased its total production from 125 when I bought my first Model S1 in 2009 to 245,519 in 2018. It should hit 500,000 by the end of this year when the Shanghai factory comes online. They have gone from employing 100 people to 50,000.

2) With the completion of the Sparks, NV Gigafactory, battery prices are collapsing and are now 50% cheaper per mile than any other competitor, 4.1 miles per kWh versus 2.5 miles.

3) Tesla’s costs for batteries have cratered from $1,000 per kWh ten years ago to $100 per kWh today and are expected to drop to $75 per kWh in a few years. Below $100 per kWh Teslas are cheaper to run than conventional gasoline-powered cars, even without the tax subsidy.

4) Tesla now makes half the lithium batteries in the world, and that figure is growing by 50% a year.

5) Tesla’s vast national charger network will soon become the country’s largest electric power utility and that will also become an enormous money-spinner. They just raised prices to 30 cents per kWh versus a cost of 5 cents. Assuming that 5 million cars buy a 70-kWh charge three times a week, that works out to a $13.65 billion a year profit.

6) Anyone who actually reads Tesla’s balance sheet can see that the company is now spinning off $1 billion in free cash flow. It is investing in new plant and equipment at a prodigious rate.

7) With a market capitalization of $44.5 billion, Tesla just trails General Motors (GM) at $51 billion, but surpasses Ford Motors at $34 billion, and therefore can raise new capital to finance its hyper-growth any time it wants.

More product at high prices at a prodigiously falling cost sounds like a pretty good business model to me. Oh, and climate change is about to become the top political issue for the 2020 presidential election. Who is the big winner in that case?

Tesla.

Global Market Comments

March 25, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR GAME CHANGER)

(SPY), (TLT), (BIIB), (GOOG), (BA), (AAPL), (VIX), (USO)

“When the facts change, I change. What do you do sir?” is a famous quote from the great economist John Maynard Keynes which I keep taped to the top of my monitor and constantly refer to.

The facts certainly changed on Wednesday when the Federal Reserve announced a change in the facts for the ages. Not only did governor Jay Powell announce that there would be no further rate increases in 2019.

He also indicated that the Fed would end its balance sheet unwind much earlier than expected. That has the effect of injecting $2.7 trillion into the US financial system and is the equivalent of two surprise interest rate CUTS.

The shocking move opens the way for stocks to trade up to new all-time high, with or without a China trade deal. Only the resumption of all-out hostilities, like the imposition of new across the board 25% tariffs, would pee on this parade.

As if we didn’t have enough to discount into the market in one shot. I held publication of this letter until Sunday night when we could learn more about the conclusion of the Mueller Report. There was no collusion with Russia and there will be no obstruction of justice prosecution.

However, the report did not end the president’s legal woes as it opened up a dozen new lines of investigation that will go on for years. The market could care less.

At the beginning of the year, I listed my “Five Surprises for 2019”. They were:

*The government shutdown ended and the Fed makes no move to raise interest rates

*The Chinese trade war ends

*The US makes no moves to impeach the Trump, focusing on domestic issues instead

*Britain votes to rejoin Europe

*The Mueller investigation concludes that he has an unpaid parking ticket in

NY from 1974 and that’s it

Notice that three of five predictions listed in red have already come true and the remaining two could transpire in coming weeks or months. All of the above are HUGELY risk positive and have triggered a MONSTER Global STOCK RALLY

Make hay while the sun shines because what always follows a higher high? A lower low.

The Fed eased again by cutting short their balance sheet unwind and ending quantitative tightening early. It amounts to two surprise interest rate cuts and is hugely “RISK ON”. New highs in stocks beckon. This is a game changer.

Bonds soared and rates crashed taking ten-year US Treasury bond yields down to an eye-popping 2.42%, still reacting to the Wednesday Fed comments. This is the final nail in the bond bear market as global quantitative easing comes back with a vengeance. German ten years bonds turn negative for the first time since 2016.

Interest rates inverted with short term rates higher than long term ones for the first time since 2008. That means a recession starts in a year and the stock market starts discounting that in three months.

Interest rates are now the big driver and everything else like the economy, valuations, and earnings are meaningless. Foreign interest rates falling faster than ours making US assets the most attractive in the world. BUY EVERYTHING, including stocks AND bonds.

Biogen blew up canceling their phase three trials for the Alzheimer drug Aducanumab. This is the worst-case scenario for a biotech drug and the stock is down a staggering 30%. Some $12 billion in prospective income is down the toilet. Avoid (BIIB) until the dust settles.

Europe fined Google $1.7 billion, in the third major penalty in three years. Clearly, there’s a “not invented here” mentality going on. It's sofa change to the giant search company. Buy (GOOG) on the dip.

More headaches for Boeing came down the pike. What can go wrong with a company that has grounded its largest selling product? Answer: they get criminally prosecuted. That was the unhappy news that hit Boeing (BA), knocking another $7 off the shares. It can’t get any worse than this, can it? Buy this dip in (BA).

Indonesia canceled a massive 737 order for 49 planes, slapping the stock on the face for $9. Apparently, they are unwilling to wait for the software fix. Buy the dip in (BA).

Oil prices hit a new four-month high at $58 a barrel as OPEC production caps work and Venezuela melts down. At a certain point, high energy prices are going to hurt the economy. Buy (USO) on dips.

The CBOE suspended bitcoin futures due to low volume and weak demand. It could be a fatal blow for the troubled cryptocurrency. Avoid bitcoin and all other cryptos. They’re a Ponzi scheme.

Equity weightings hit a 2 ½ year low as professional institutional money managers sell into the rally. They are overweight long defensive REITs and short European stocks. Watch out for the reversal.

December stock sellers are now March buyers. Expect this to lead to a higher high, then a lower low. Volatility is coiling. Don’t forget to sit down when the music stops playing.

Volatility hits a six-month low with the $12 handle revisited once again down from $30. (VIX) could get back to $9 before this is all over. Avoid (VIX) as the time decay will kill you.

Weak factory orders crush the market, down 450 points at the low. Terrible economic data is not new these days. But it ain’t over yet. Buy the dip.

The Mad Hedge Fund Trader was up slightly on the week. That’s fine, given the horrific 450 point meltdown the market suffered on Friday. We might have closed unchanged on the day but for rumors that the Mueller Report would be imminently released.

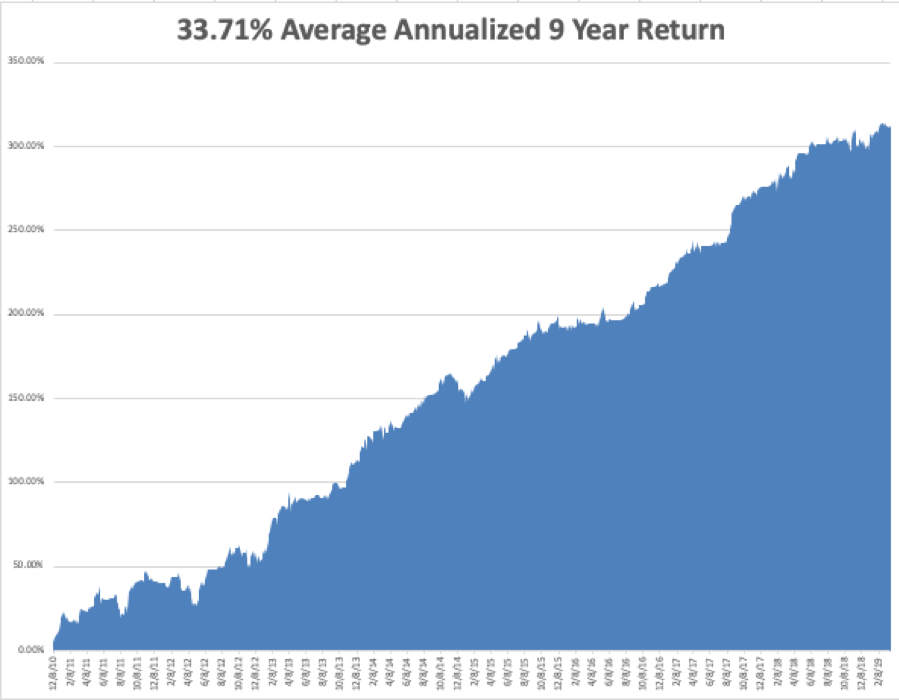

March is still negative, down -1.54%. My 2019 year to date return retreated to +11.74%, boosting my trailing one-year return back up to +24.86%.

My nine-year return recovered to +311.88%. The average annualized return appreciated to +33.71%. I am now 40% in cash, 40% long and 20% short, and my entire portfolio expires at the April 18 option expiration day in 14 trading days.

The Mad Hedge Technology Letter used the weakness to scale back into positions in Microsoft (MSFT), Alphabet (GOOGL), and PayPal (PYPL), which are clearly going to new highs.

The coming week will be a big one for data from the real estate industry.

On Monday, March 25, Apple will take another great leap into services, probably announcing a new video streaming service to compete with Netflix and Walt Disney.

On Tuesday, March 26, 9:00 AM EST, we get a new Case Shiller CoreLogic National Home Price index which will almost certainly show a decline.

On Wednesday, March 27 at 8:30 AM, we get new Trade Deficit figures for January which have lately become a big deal.

Thursday, March 28 at 8:30 AM EST, the Weekly Jobless Claims are announced. We also then get another revision for Q4 GDP which will likely come down.

On Friday, March 29 at 10:00 AM, we get February New Home Sales. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’m praying that it stops snowing in the High Sierras long enough for me to get over Donner Pass and spend the spring at Lake Tahoe. We are at 50 feet for the season, the second highest on record.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 22, 2019

Fiat Lux

Featured Trade:

(I HAVE AN OPENING FOR THE MAD HEDGE FUND TRADER CONCIERGE SERVICE),

(MARCH 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(BA), (FCX), (IWM), (JNJ), (FXB), (VIX), (JPM)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader March 20 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What do you make of the Fed’s move today in interest rates?

A: By cutting short their balance sheet unwind early and ending quantitative tightening (QT) early, it amounts to two surprise interest rate cuts and is hugely “RISK ON”. In effect, they are injecting $2.7 trillion in new cash into the financial system. New highs in stocks beckon, and technology stocks will lead. This is a game changer. In a heartbeat, the world has moved from QT to QE, and we already know what that means for socks. They go up.

Q: Why buy Boeing shares (BA) ahead of a global recession?

A: It’s an 18-day bet that I’ve made in the options market. The US economic data is already indicating recession. The data will continue to worsen and that will continue until we go into a recession. But that’s not happening in 18 trading days. Also, we’re getting into Boeing down 20% from the top so our risk is minimal.

Q: Why are we in an open Russell 2000 (IWM) short position?

A: We now have three long positions— 40% on the long side with the Freeport McMoRan (FCX) double position. It’s always nice to have something on the other side to hedge sudden 145-point declines like we have today. Ideally, you want to be hedged at all times. But it’s hard to fund good companies to sell short in a bull market.

Q: Do you need some euphoria to get the Volatility Index (VIX) to the $30-$60 level?

A: No, you don’t need euphoria. You need fear and panic. The (VIX) is a good “fear index” in that it rises when markets are crashing and falling when markets are slowly rising. And for that reason, I’m not buying (VIX) right now. With a sideways to slowly rising market, we could see the $9 handle again before this move is over.

Q: What should be the exit on the Russell 2000 (IWM)?

A: One choice is taking 80% of the maximum profit when you hit it—that’s where the risk-reward tips against you if you keep the position. The other option is to be greedy and run it all the way into expiration, taking the full profit. It depends on your risk tolerance. Remember, we hit the 80% profit three times in March only to stop out of positions for a loss. The market just doesn’t seem to want to let you take the whole 100%.

Q: Why are all your expirations on April 18?

A: That’s when the monthly options expire; therefore, they have the most liquidity of any other option expiration. If you go with the weeklies before or after the monthlies, the liquidity declines dramatically, which can be very frustrating. Since I used to cover only the largest clients, we could only trade in monthlies because we needed the size.

Q: Will Johnson and Johnson (JNJ) survive all those talcum powder lawsuits?

A: They’ve been going on for 10 years—you’d think they’d know by now if they have asbestos in their talcum powder or not. I highly doubt this will get anywhere; they’ll probably win everything on appeal.

Q: What do you anticipate on Brexit?

A: I think eventually Brexit will fail; we’ll have a referendum which will get voted down, Britain will rejoin Europe, and the British pound (FXB) will go to $1.65 to the dollar where it was when Brexit hit three years ago, up from $1.29 today. It would be economic suicide for Britain to leave Europe, as they would have to compete against Europe, the US, and China alone, and they are slowly figuring that out. Demographic change alone over three years would guarantee that another referendum fails.

Q: My partner owns JP Morgan (JPM). Do you still say banks are not a good place to be?

A: Yes. Fintech is eating their lunch. If they couldn't go up with interest rates moving up in the right direction, they certainly won’t be doing better now that interest rates are going down. Legacy banks are the new buggy whip industry.

Q: Why are commodities (FCX) increasing with a coming recession?

A: They are a hard asset and do better in inflation. Also, they’re stimulating their economy in China and we aren't—commodities do better in that situation as China is the world’s largest buyer of commodities, as do all Chinese investments.

Q: Would you buy Biogen (BIIB) on the dip? Its down 30% today.

A: Canceling their advanced phase three trials for the Alzheimer drug Aducanumab is the worst-case scenario for a biotech company. Some $12 billion in prospective income is down the toilet and many years of R&D costs are a complete write-off. Avoid (BIIB) until the dust settles.