Featured Trade: (WHY THE JANUARY NONFARM PAYROLL WAS A BIG DEAL), (IWM), (DXJ), (HEDJ), (FXE), (FXY), (THE BIPOLAR ECONOMY), (TESTIMONIAL)

iShares Russell 2000 (IWM) WisdomTree Japan Hedged Equity ETF (DXJ) WisdomTree Europe Hedged Equity ETF (HEDJ) CurrencyShares Euro ETF (FXE) CurrencyShares Japanese Yen ETF (FXY)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-10 01:07:512015-02-10 01:07:51February 10, 2015

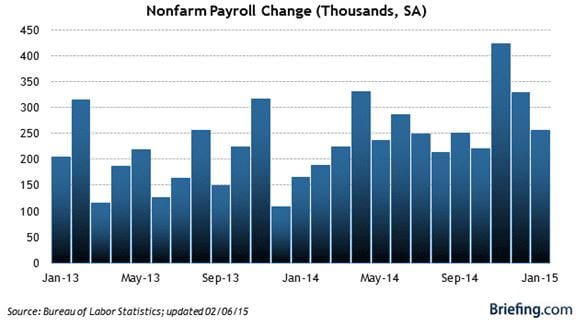

Economists were blown away by the January nonfarm payroll numbers, announced on Friday.

Some 257,000 jobs were added the previous month, holding the headline unemployment figure at 5.7%. Far more important were the revisions for earlier months, which saw December increased to a robust 329,000 and November bumped up to a breathtaking 423,000.

These numbers are almost back to ?normal.? Are ?normal? interest rates to follow?

All told, the January report, the revisions and the additions to the work force means that 703,000 jobs were added to the economy, taking the year on year increase to a positively boom time 3 million. The last quarter has seen the fastest jobs growth rate since 1997. Yikes!

A major part of the new jobs were in retail, proof that our windfall tax cut in the form of falling gasoline prices is finally kicking in.

Needless to say, this is all a bit of a game changer.

It totally vindicates the high-end forecasts for the US economy of 3% plus I made in my New Year forecasts (click here for my ?2015 Annual Asset Class Review?).

The data confirms my thesis that investors are substantially underestimating the strength of the US economy. Furthermore, they have yet to understand the enormously positive impact of cheap energy prices.

It also means that the bull market in stocks is alive and well. It is only resting.

To understand why, let me highlight the major points brought to the fore by the Bureau of Labor Statistics report.

1) The US Economy Has Entered a Self Sustaining Recovery

The trend line for many economic data points are now moving so convincingly upward that they can no longer be treated as statistical anomalies. Nor can they be ascribed to temporary artificial overstimulation by the Federal Reserve in the form of quantitative easing.

Count on Treasury Secretary, Jack Lew, to announce ?mission accomplished? when he address congress later on this week (click here for my one-on-one with Jack, ?Riding With the Treasury Secretary?).

My bet is that this is not our last blockbuster revision. Next to come will be the Q4 GDP, from the just reported flaccid 2.6% annual rate back towards the red hot 5% seen in Q3.

2) The Date for the Next Fed Rate Hike has Been Moved Up

The bond market certainly believed this last week, giving up 9 full points in a couple of days, taking yields from 2.62% to 2.92% in a heartbeat.

I still think this is a 2016 story. The pernicious effects of deflation are still advancing, not retreating, and are not exactly an argument for raising interest rates. But there is no doubt that the desire among the Fed governors to return rates to normal levels is growing, especially if the impact on the economy will be minimal. So call the next rate rise an early, rather than a later, 2016 eventuality.

3) The Strong Dollar is Becoming a Factor With Earnings

The Euro (FXE) has depreciated 31% against the dollar from its 2008 peak, and the yen (FXY) 38% from its 2011 apex. Yet the impact on corporate earnings so far has been marginal at best.

Where will it really start to hurt?

When these currencies approach my final targets of 87 cents and 150, or down another 22% and 18%. It is safe to say that a strong dollar will command an increasing amount of our attention going forward.

This is the argument for investing in small cap US stocks (IWM), where the currency exposure is minimal. Hedge European (HEDJ) and Japanese (DXJ) stocks start to look pretty good too.

4) Wages May Finally Be Rising

The biggest structural impediment facing the US economy has been wage inequality, where virtually all of the benefits of growth accrue to the risk investors of the 1% at the expense of the working class. Hyper accelerating technology and dreadfully imbalanced tax policies are to blame.

January brought us an increase in wages that was miniscule, incremental and modest at best, but it was an increase nonetheless. Average hourly earnings fell by 5 cents in December and then rose by 12 cents the following month.

If this continues, consumer spending will see a big revival, giving us yet another leg to a rising stock market, and creating a win-win situation for all.

One can only hope.

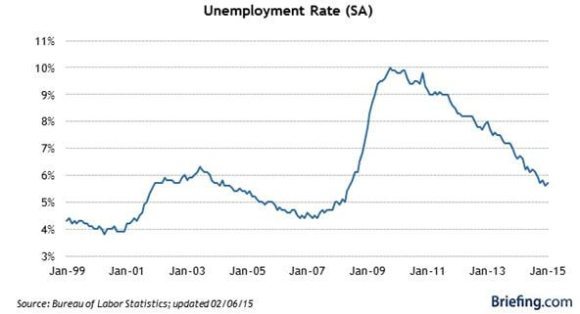

5) More Americans Are Looking for Work

The really amazing thing about the January numbers that they occurred in the face of a large increase in the work force. The participation rate, which has been plummeting for a decade, rose smartly. Long-term U-6 unemployment stayed high, but is down a quarter from peak levels.

To me, this is all a warm up for my ?Golden Age? in the 2020?s. The best is yet to come.

Suddenly, the Line is Getting Shorter

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Unemployment-Line-e1423518746703.jpg257400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-10 01:06:492015-02-10 01:06:49Why the January Nonfarm Payroll Was a Big Deal

Featured Trade: (THE 12 NEW TRADING RULES FOR 2015), (AN ENVIRONMENTAL ACTIVISTS TAKE ON THE MARKETS), (DBA), (MOO), (PHO), (FIW) (FRIDAY, APRIL 3 HONOLULU, HAWAII STRATEGY LUNCHEON)

PowerShares DB Agriculture ETF (DBA) Market Vectors Agribusiness ETF (MOO) PowerShares Water Resources ETF (PHO) First Trust ISE Water ETF (FIW)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-09 01:06:262015-02-09 01:06:26February 9, 2015

1) Dump all hubris, pretentions and stubbornness. It will only cost you money.

2) The market is always right, even if all the prices appear wrong.

3) Only buy the puke outs and sell the euphoria. Do anything in the middle, and you will get whipsawed.

4) Outright calls and puts are offering a better risk/reward right now than bull and bear vertical call and put spreads, which have a built in short volatility element. It is also better to buy stocks and ETF?s outright with a tight stop loss. This won?t last forever.

5) If you do trade spreads, you can no longer run them into expiration. If you have a nice profit take it, don?t hang on to the last 30 basis points, even if it means paying more commission. The world could end three times, and then recover three times, before the monthly expiration date rolls around.

6) Tighten up your stop loss limits. Not losing money is the key to winning in this market. There is nothing worse than having to dig yourself out of a hole. Don?t run hemorrhaging losses, like the (TBT) from $57.56 down to $43.11. It will get easy again some day.

7) Buy every foreign crisis and sell every recovery. It really makes no difference to assets here in the US.

8) Several asset classes are becoming untradeable for long periods (bonds, oil, ags). Stay away and stick to the asset classes that are working (stocks, foreign exchange).

9) Keep positions small. The doubled volatility will make up for your reduced risk. This is not the time to get greedy and bet the ranch.

10) Turn off the TV and just look at your screens and data. Public entertainers have no idea what the market is going to do, especially if their last job was sports reporting. Their job is to get you to watch the ads for General Motors and TD Ameritrade.

11) As the bull market in stocks enters its sixth year, too many traders, analysts and strategists have become complacent. You are going to have to work for your crust of bread this year. This is an earnings, technology and productivity driven bull, not a QE driven one.

12) It is clear that more money was allocated to high frequency traders this year. That is driving the new, breakneck volatility, increasing stop outs. A sneeze now generates a 250-point intraday move. It is no coincidence that they announced this week the end of pit trading in Chicago. The traders all retired, or went off to programming school. Get used it.

Better change your password to, from 12345 to DKFGGIDKFOKBJGELXPEVJBKDLKFBBJFCJCKVLBKGTY69!, and hope that the 69 doesn?t give you away.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/03/John-Thomas1-e1421097493926.jpg355400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-09 01:05:022015-02-09 01:05:02The 12 New Trading Rules for 2015

Featured Trade: (TRADING DEVOID OF THE THOUGHT PROCESS), (SPY), (INDU), (TLT), (USO), (GOING BACK INTO GILEAD SCINECES), (GILD), (ON EXECUTING TRADE ALERTS)

SPDR S&P 500 ETF (SPY) Dow Jones Industrial Average ($INDU) iShares 20+ Year Treasury Bond (TLT) United States Oil ETF (USO) Gilead Sciences Inc. (GILD)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-05 09:37:262015-02-05 09:37:26February 5, 2015

This is a stock that could double by the end of 2015. Buy a great performing stock in the top performing sector on a 10% dip.

The stock has over reacted to an earnings report that was fantastic; but carried conservative forward guidance, based on expected future pricing pressure on its blockbuster Hepatitis C drugs, Sovaldi and Harvini.

I am giving a nod to the current high risk, high volatility environment and being very cautious here buy going with strike prices for the options that are well below the 200-day moving average. A very short, 11 trading day expiration gives us some extra protection.

This position should be able to weather some pretty fierce storms.

If you want to be more aggressive and take a longer view, buy the (GILD) April, 2015 $110 calls at $2.20 or better. If we break to a new all time high by the April 17 expiration, as I expect, you could score a 3-5 bagger for these options.

If you don?t do options, just buy the shares and sit on them for the rest of the year.

I spoke to a friend of mine who works for a health care venture capital firm, and I thought I?d pass through a few tidbits.

Gilead Sciences (GILD) is basking in the glow of the most profitable drug launch in history. Its treatment for hepatitis C, launched in 2013, inhibits the RNA polymerase that the hepatitis C virus (HCV) uses to replicate its RNA. It traders? parlance, it kills the bug.

(GILD) has taken in $5.7 billion in sales of this drug during the first half of 2014, and could sell as much as $10-$12 billion for the full year.

The drug is so revolutionary, that it on the scale of medical miracles of decades past, such as Salk vaccine immunizations for polio and penicillin treatments for bacterial infections. So far, Gilead has cured a breathtaking 90% of patients.

Now the company is using various drug combinations that produce even higher success rates with fewer side effects, and may be expended to treat other life threatening diseases. These could take Hepatitis C drug sales as high as $15-$18 billion in 2015.

A big controversy has been its immense cost, which works out to $84,000-$135,000 per patient. This has become a bigger issue with the advent of Obamacare, now that the government is picking up much of the tab.

But, that?s a bargain compared to full treatment of the disease, which can run as high as $350,000 per patient. That is, unless you don?t care if you die.

Partly in response to these complaints, the company is making the drug available at deep discounts in 91 emerging nations that account for 50% of all Hepatitis C cases globally. What it loses on margins there it will make back in volume.

With any luck, we may see hepatitis C wiped out in my lifetime, as I have already seen with smallpox (I saw some of the last few live cases in kids in Nepal in 1976).

All of this makes the stock appear a bargain at its current $99.01 price. At a multiple of a subterranean 11X earnings, the stock should hit $140 next year.

You all know that health care is one of my three core industries to bet on for the long term (there others are energy and technology).

The short-term driver of the share price for (GILD) is obviously whether the health care sector is in, or out of vogue. But for the long term Gilead looks like a good bet to me.

And I don?t even have hepatitis, or Ebola.

Time for Another Dose of Gilead Sciences

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/Sovaldi-Pills.jpg298367Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-05 09:31:422015-02-05 09:31:42Going Back Into Gilead Sciences

Featured Trade: (SOLAR STOCKS GET A JOLT), (SCTY), (SUNE), (SPWR), (TAN), (IS THE REAL ESTATE MARKET CATCHING COLD?), (ITB), (KBE)

SolarCity Corporation (SCTY) SunEdison, Inc. (SUNE) SunPower Corporation (SPWR) Guggenheim Solar ETF (TAN) iShares US Home Construction (ITB) SPDR S&P Bank ETF (KBE)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-04 01:05:502015-02-04 01:05:50February 4, 2015

The blockbuster for me in President Obama?s budget speech on Monday was his suggestion that the 30% alternative energy investment tax credit be made permanent. All solar stocks, including front-runners Solar City (SCTY), Sun Edison (SUNE), and SunPower (SPWR), rocketed on the news.

Now slated to expire at the end of 2017, the tax break is credited with igniting a solar building boom in recent years. Solar panels are becoming commonplace on roofs in better off residential neighborhoods across the country.

They are becoming so pervasive that they are changing the market for electricity beyond all recognition in lead states like California. The afternoon demand spike, once a regular feature of power management, is rapidly disappearing as consumers now sell excess peak electricity back to utilities at favorable rates.

Of course, this is all wishful thinking on the part of Obama, who couldn?t get a Republican led congress to agree with him on what day it is. Still, it has been outlined a priority with the administration, and could be a bargaining chip used in some broader tax compromise with the opposition.

And where President Obama mail fail, a future President Hillary may succeed.

Indeed, there has recently been an onslaught of good news showering the solar industry. China has announced a 43% increase in its installed solar base, an increase of 15 gigawatts. At the very least, this will divert cheap Chinese made panels from flooding the US market, the recent punitive import duty notwithstanding.

A 15% rally in the price of oil over the past three trading days has also provided a major assist. Solar actually has nothing to do with the price of oil. Its main competitor is the retail cost of electricity, which is driven by future capital spending budgets of local utilities. That has costs rising as far as the eye can see, as the industry replaces aging, 100 year old infrastructure.

The market sees it otherwise, which lumps all energy firms in the same category, be they oil, fracking, natural gas, coal, or even nuclear. Whether it makes sense or not, solar stocks are still tarred by the price of oil. Check out the charts below, and you find a correlation that is almost perfect.

The great irony in the president?s proposal is that solar is now profitable even without the tax breaks. They just provide the juice to accelerate widespread solar adoption.

I think solar is one of a handful of industries that could generate a tenfold return over the coming decade. Costs are plummeting, profit margins are expanding, and the overall market size is growing by leaps and bounds.

The fact that you can buy them now 40% off of their recent peaks is a gift. A $30 recovery in the price of oil could bring a 40% recovery in the shares of the oil majors. It could deliver a ten bagger for solar companies.

Let me pass on a little tidbit I picked up from Solar City a few weeks ago. By the end of this year, used Tesla Model S-1 batteries will become available in large numbers for the first time, including my own. (SCTY) plans to offer these for sale to their customers as backup batteries for home use. One battery can store three days worth of normal power consumption. This would make customers totally independent of the power grid.

No mention has been made of prices. My guess is that since these lithium ion batteries cost $30,000 new, a second hand one should come out at $10,000. These will still have 80% of their original capacity, not enough for a long-range car, but plenty for home storage.

For more depth on Solar City, please refer to my recent piece,?Loading the Boat with Solar City? by clicking here.

Meet the New Bull Market

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Solar-Panel-Installation-e1423003212602.jpg238400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-04 01:04:262015-02-04 01:04:26Solar Stocks Get a Jolt

I used to begin my pieces about residential real estate talking about the broker I found hanging from the showerhead at an open house.

That didn?t really happen. But from 2008-2012 conditions were so dire that it could have.

That is clearly not the case any more. The market has been on fire for the past three years. Private equity firms put a floor under the markets by pouring in massive amounts of cash. Once they chewed through a backlog of foreclosed homes, it was off to the races.

The gains in the lead markets have been nothing less than stunning. San Francisco saw prices rocket by 33% last year, floated by a tidal wave of technology IPO money. A home in Fog City is now 40% more expensive than the last peak in 2007.

If you want to work for a startup, you better count on spending some time in a garage, to live, not to work, as rents are now so stratospheric. Even the basket case states of Florida, Arizona, and Nevada have bounced back, although they are still well off their highs.

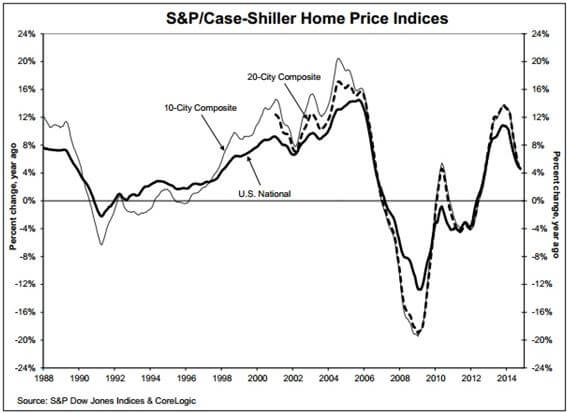

The S&P 500 Case Shiller Real Estate Index has been moving up in nearly a straight line since 2009. That is, until six months ago, when a noticeable softening began (it?s always published on a three month lag, as the market is so fragmented).

The most recent report said that homes were appreciating at a modest 4.7% year on year rate, a much slower rate than in the past. Given the onslaught of other negative data in recent months, you have to ask if the party is now over for homeowners.

It would be easy to blame the weather, last winter being one of the worst on record. My friends in Chicago threw empty beer cans at the TV sets whenever the weatherman appeared, for good reason. You can?t visit an open house if it is buried in snow and black ice has closed the roads. However, you have to ask if there is more going on here. We also learned today that the national homeownership rate has fallen to 68.4%, a new 19 year low, according to the US Census Bureau. It would be easy to ascribe this as just one more effect of concentration of wealth at the top. But more thoughtful analysis is deserved here.

Talk to kids today, and it quickly becomes clear that homeownership is not the priority that it was for earlier generations. And who would blame them. For most of their lives, house prices have gone down, not up. For them, that cute little house with the white picket fence belies tales of financial distress, bankruptcy and foreclosure. So what?s the big rush?

A lot of twenty somethings would rather just spend their money and rent, not own. Many in the San Francisco Bay Area prefer to invest their savings in their own start-ups in the hope of making it big someday.

It?s not like banks want to lend to them anyway. In the aftermath of the Great Recession, banks now have far more stringent lending standards than in the past. You can blame both the new regulation in Dodd Frank and the banks? own desire to pare back risk.

Some 70% of graduating students today do so with outstanding student loan balances. Debts of $100,000 or more are common, and heaven help you if you want to go to graduate school. Needless to say, they don?t exactly make ideal mortgage candidates. We may b losing an entire generation of homebuyers.

I don?t think we are headed for another real estate crash. More likely, it will go to sleep for a while in a prolonged sideways move. Interest rates are still at ultra low levels and will remain so for a long time, providing a floor under current prices. The big killings are long gone. That was a 2012 trade.

The stock market has been telling us as much. The iShares Dow Jones US Home Construction ETF (ITB) has led the market retreat this year, paring back 12.7%. Banks have also taken it in the shorts, thanks to the drying up of new mortgage originations, the SPDR KBW Bank Index ETF (KBE), giving back 12% during the same time frame.

Happy days will return to housing once more. But we may have to wait until the 2020?s, when a gigantic demographic tail wind, returning inflation and rising wages all kick in at the same time.

Some of those nascent start-ups may also be going public by then, adding more fuel to the fire.

Is Housing Cooling Off?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/04/House-Fire.jpg305456Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-04 01:03:002015-02-04 01:03:00Is the Real Estate Market Catching Cold?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.