The real shocker today in the Fed?s announcement is that it may increase monetary easing from here. As if we haven?t had enough already, with the US and Japan throwing in a combined $170 billion a month worth of monetary stimulus!

More easing means that the America?s central bank thinks the global economy is even weaker than you and I realize. Yikes! Man the lifeboats, pass out the parachutes, and tighten your seatbelts! This is bad for commodities and even worse for precious metals, especially gold.

The barbarous relic has managed an impressive $155 rally off its $1,325 bottom made two weeks ago. This is one of the sharpest and fastest moves up in the yellow metal in history. It has been largely achieved through massive buying of physical coins in India and the US, as well as short covering in the futures markets and the ETF (GLD). The disappearance of margin calls has also been a major help.

The heavy hand of the China slowdown is still with us. So I am more than happy to buy the SPDR Gold Trust Shares June, 2013 $150-$155 in-the-money bear put spread. The big attraction here is that I have a generous $97 safety cushion over the next six weeks before I lose money on this trade.

You can thank the sky high implied volatilities on the (GLD) puts for getting such a great deal on this spread. Just for the sake of comparison, the implied on the (GLD) $150 puts you just sold short is 18.2%, some 30% higher than the 14% front month implied on the Volatility Index on the S&P 500. If you don?t understand why this is important, please buy the book, Options for the Beginner and Beyond, at Amazon by clicking the title or the book cover below.

Time To Grab a Second Handful

https://www.madhedgefundtrader.com/wp-content/uploads/2013/04/Gold-Nuggets.jpg414617Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-05-02 10:12:202013-05-02 10:12:20Selling Gold Again

What would happen if I recommended a stock that had no profits, was cash flow negative, and had a net worth of negative $44 trillion? Chances are, you would cancel your subscription, demand a refund, de-friend me from you Facebook account, and delete my email address from your address book.

Yet that is precisely what my former colleague at Morgan Stanley did, technology guru Mary Meeker. Now a partner at venture capital giant Kleiner Perkins, Mary has brought her formidable analytical talents to bear on analyzing the United States of America as a stand alone corporation. The bottom line: the challenges are so great they would daunt the best turnaround expert. But our problems are not hopeless or unsolvable.

The US government was a miniscule affair until the Great Depression and WWII, when it exploded in size. Since 1965 when Lyndon Johnson?s ?Great Society? began, GDP rose by 2.7 times, while entitlement spending leapt by 11.1 times. If current trends continue, the Congressional Budget Office says that entitlements and interest payments will exceed all federal revenues by 2025.

Of course, the biggest problem is with health care spending, which will see no solution until health care costs are somehow capped. Despite spending more than any other nation, we get one of the worst results, with lagging quality of life, life spans, and infant mortality. Some 28% of Medicare spending is devoted to a recipient?s final year of life. Somewhere, there are emergency room cardiologists making a fortune off of this.

Social Security is an easier fix. Since it started in 1935, life expectancy has risen by 26% to 78, while the retirement age is up only 3% to 68. Any reforms have to involve raising the retirement age to at least 70, and means testing recipients.

The solutions to our other problems are simple, but require political suicide for those making the case. For example, you could eliminate all tax deductions, including those for home mortgage deductions, charitable contributions, IRA contributions, dependents, and medical expenses, and raise $1 trillion a year. That would wipe out the current budget deficit in one fell swoop.

Mary reminds us that government spending on technology laid the foundations of our modern economy. If the old ARPNET had not been funded during the sixties, Google, Yahoo, EBay, Facebook, Cisco, and Oracle would be missing today. Global Positioning Systems (GPS) was also invented by and is still run by the government and has been another great wellspring of profits.

There are a few gaping holes in Mary?s ?thought experiment?. I doubt she knows that the Treasury Department carries the value of America?s gold reserves, the world?s largest at 8,965 tons worth $414 billion, at only $32 an ounce, versus an actual market price of $1,445.

Nor is she aware that our ten aircraft carriers are valued at $1 each, against an actual cost of $5 billion in today?s dollars. And what is Yosemite worth on the open market, or Yellowstone, or the Grand Canyon? These all render her net worth calculations meaningless.

Mary expounds at length on her analysis, in her book entitled USA Inc. which you can buy at Amazon by clicking on the title or the book cover below.

Worth More Than a Dollar?

How About $32 an Ounce?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/Gold-Bars.jpg232288Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-05-02 10:04:392013-05-02 10:04:39Is USA Inc. a ?SELL?

My current scenario for global equities has them selling off over the summer, then a rebounding led by emerging markets starting sometime in the fall. In that case, you want to start building short lists of high growth countries to pile into, once the turn comes.

I would be including Columbia on any such list. It enjoys that sweet spot of being an oil exporting emerging country whose shipments hit an all-time high of 884,000 barrels a day, about half the quantity that Libya once shipped. The quality of the government has improved dramatically over the last decade. It is a narco state no more, although public and investors? perceptions lag deeply. The country has seen upgrades by leading credit agencies. Billionaire Carlos Slim, the world?s richest man, has recently been seen as a major investor.

The country also enjoys one of the world?s most favorable demographic pyramids. A young, upwardly mobile workforce is producing a rising tide of consumers and a burgeoning middle class, while expensive seniors requiring social services and medical care are few and far between.

Columbia was the world?s best performing equity market in 2010, bringing in gains of over 100%. That was how the country ETF (GXG) performed. Is history about to repeat itself?

Like most emerging stock markets this year (EEM), Columbia has been beaten like a red headed step child. That makes it a prime target for a rotation, should another leg to the ?RISK ON? market develop later in the year, as I expect. They also make great coffee. Just ask Juan Valdez.

Juan Valdez is Setting Up for a Buy

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/Juan-Valdez.jpg415549Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-05-02 09:54:262013-05-02 09:54:26Columbia is Popping Up on My Radar

Featured Trade: (MAY 1 GLOBAL STRATEGY WEBINAR), (OLD TECH?S BIG COMEBACK), (AAPL), (MSFT), (INTC), (HPQ), (XLK), (AMAT), (GET READY FOR YOUR NEXT BIG TAX HIT)

Apple Inc. (AAPL)

Microsoft Corporation (MSFT)

Intel Corporation (INTC)

Hewlett-Packard Company (HPQ)

Technology Select Sector SPDR (XLK)

Applied Materials, Inc. (AMAT)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-05-01 09:30:212013-05-01 09:30:21May 1, 2013

Apple blew away the bears today with the issuance of $17 billion in bonds, the largest such corporate debt issue in history. Spread over two, five, ten, and 30 years, the deal was oversubscribed by more than 3:1, with $40 billion in demand left unfilled.

Foreign investors took down a major part of the deal, which explains Deutsche Bank?s senior role in the syndicate. The yield on the ten-year bonds came in at 2.40%, a mere 70 basis points over equivalent US Treasury paper.

The mega deal, dubbed ?iBonds? by traders, underlies the tremendous shortage of high-grade fixed income securities worldwide. Since 2007, the amount of double ?A? or better rated paper has declined by 60%, thanks to widespread downgrades inspired by the newfound religion of the ratings agencies.

As I never tire of pointing out at my strategy luncheons and lectures, the principal sin of governments is not that they are borrowing too much money, but not enough. This has given us a global bond shortage that has taken returns to insanely low levels. Look no further than the ten-year yield of 1.68% in the US, 1.20 % in Germany, and a pitiful 0.60% in Japan.

The issue also highlights the sudden fascination of all things Apple since its better than expected calendar Q1 earnings report last week, with $43 billion in revenues spinning off $9.5 billion in profits. Since then, we learned that the richest man in Russia, Alisher Usmanov, soaked up some $100 million of stock close to the $392 bottom. This is a man who?s proven track record of market timing is uncanny.

It doesn?t require a lot of imagination to figure out what this deal is all about. With $145 billion in cash on the balance sheet, why borrow another $17 billion? The reality is that this is a way of repatriating, through the back door and tax-free, some of the estimated $100 billion in cash the company has parked in offshore bank accounts.

What will it do with the money? How about buying back $17 billion worth of stock? Buy borrowing at 2.4% and retiring 3.2% dividend stock, the yield pick up on the transaction comes to $136 million a year. That goes straight to the bottom line. The deal reminds me of the kind of financial engineering that dominated Japanese finance during the late 1980?s. When I was a director of Morgan Stanley, I signed many of these multi billion dollar deals as a co-manager.

It wasn?t just Apple that has returned from the grave, which saw its stock rise by 14% since last week?s two year low. Look at many of the old tech warhorses, like Microsoft (MSFT), Applied Materials (AMAT), Hewlett Packard (HPQ), and Intel (INTC), which have blasted forth from long moribund levels in recent weeks.

Which raises an interesting possibility. What if the long predicted selloff in May does a no show? What if, instead of the usual 10%-25% swan dive, we only get the 2.5% that has been the pattern for 2013? The possibilities boggle the mind.

In that case where will the money flood into next? Stocks that have been going up like a rocket for the past eight months, or shares that have either fallen like a stone during this time, or barely budged? Stocks that are trading at double the market multiple, or at half the market multiple? Hmmmm. Let me think about this one.

There are two major categories of the latter, commodity related shares and technology ones. China is still slowing, placing a monkey on the back of most commodities related companies. So I vote for technology, which by the way, is the cheapest it has ever been on an earnings multiple basis.

In that case, the strength in old tech will develop into far more than a one-week wonder. It could provide the rocket fuel that will power the major indexes for the rest of the year. That would take the S&P 500 up to 1,700 where it can flaunt a glitzy earnings multiple of 17.

Don?t get too giddy. This is definitely a best-case scenario. But then lately, the best-case scenarios have been happening, thanks to the reflationary efforts of our friend, Ben Bernanke.

That would be fantastic news for Apple?s long-suffering shareholders. Now that its stock has clearly broken through the 50-day moving average on the upside, the eventual target of this leg could be as high as the 200-day moving average at $541. One can only hope.

Old Tech is Rising From the Dead

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/Dracula.jpg268337Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-05-01 09:26:212013-05-01 09:26:21Old Tech?s Big Comeback

No matter what anyone promises you today, this week, or this year, your taxes are going up. I don?t care if you are still licking your wounds from the January 1 payroll tax rise, or the federal tax hike for millionaires, which in my case took my rate up from 35% to 39.6%. At least the capital gains tax is still a steal at 20%.

At $1.3 trillion, the budget deficit is so enormous that bringing it into balance merely through spending cuts is a mathematical impossibility. Chopping funding for Planned Parenthood and National Public Radio just isn?t going to do it.

If you own your own home, work for a large company, save for your retirement, earn money from capital gains, and toss in a check when they pass the dish around at church every Sunday, you are the biggest beneficiary of the current tax system. Therefore, you are about to take a big hit. Check out the target list below, and the tax revenues the death of these tax breaks will raise:

$264 billion- Should those without health care subsidize those who receive it for free from their employers? This is the amount raised by taxing company provided health insurance as regular income. Think large banks and oil companies.

$100 billion- Should renters be subsidizing homeowners? Kiss that home mortgage interest deduction on loans under $1 million goodbye. Ditto for the real estate market as a whole. The more aggressive version of this has the ceiling on deductions dropping to $500,000.

$100 billion- End the tax deductibility of charitable contributions. Should those who don?t go to church subsidize those who do? Universities, churches, and political fund raising go begging.

$52 billion- Should those without savings subsidize those salting away money for retirement. This is the argument that will be made to end tax deductibility of 401k contributions.

$39 billion- Savings on taxes exempted by the step up in the cost bases for investments inherited by surviving spouses. She doesn?t need that McMansion anyway.

$36 billion- Tax capital gains as regular income. This won?t affect you if you never sell and let your heirs sort out the mess.

$31 billion- Stop special tax treatment of dividend incomes.

Please note that these most draconian measures only raise $586 billion a year, a mere 45% of last year?s deficit. Without raising tax rates, the remaining $714 billion will have to come from cutting Medicare, Medicaid, Social Security, and Defense spending. In any case, I think it will be politically impossible to get any of these changes through the current congress. An energy tax and a national value added tax are also on the table.

None of these hikes would be necessary if the economy grew at a 4% real rate instead of 3%. This is why tax rates in emerging countries are so low. But I believe that America?s long-term growth rate is falling, not rising, and that our budget problems are going to get worse, not better. What happens if interest rates rise for the world?s largest borrower? Oops.

Of course, we could adopt Mary Meeker?s suggestion in her paper on USA, Inc. and eliminate all deductions, raising about $1 trillion a year. That would involve shrinking the Internal Revenue Code from the current 71,000 pages to a single page, and moving to a flat tax system. The mass unemployment of one million CPA?s and 106,000 internal revenue agents alone would be worth the price.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/IRS-Emblem-plus.jpg321461Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-05-01 09:22:262013-05-01 09:22:26Get Ready for Your Next Big Tax Hit

Featured Trade: (TRADE ALERT SERVICE POSTS TWO YEAR 90% PROFIT), (MAY 8 LAS VEGAS STRATEGY LUNCHEON), (IT?S OFFICIAL: THERE?S NOTHING TO DO), ?(SPY), (TLT), (JNK), (DINNER WITH ELIOT SPITZER)

SPDR S&P 500 (SPY)

iShares Barclays 20+ Year Treas Bond (TLT)

SPDR Barclays High Yield Bond (JNK)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-04-30 09:46:592013-04-30 09:46:59April 30, 2013

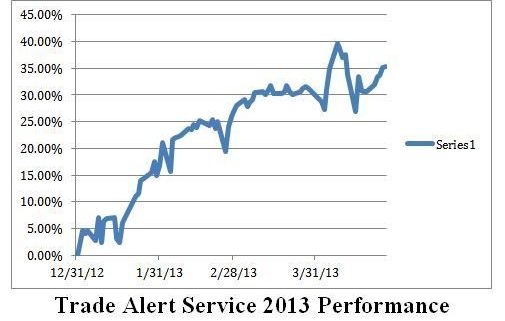

The Trade Alert Service of the Mad Hedge Fund Trader has posted a 90.6% profit since the inception of the service 30 months ago. That compares to a modest 21% return for the Dow average during the same period. This raises the average annualized return for the service to 36.2%, elevating it to the absolute apex of hedge fund ranks.

My bet that the stock markets would continue to grind up to new all time highs in the face of complete disbelief and multiple international shocks paid off big time, as I continued to initiate new long positions in the S&P. After steering readers away from gold (GLD) all year, I then caught the bottom and rode a $74 rally on the way back up. Every short position in the yen has been a money maker. I even managed to cover a brief short in the Treasury bond market for a small profit.

Trade Alerts that I wrote up, but never sent, worked. That?s because I have been 100% invested for the entire year in long stock/short positions. However, followers of my biweekly strategy webinars caught my drift and benefited from the thinking, and many did these trades on their own. These included shorts in the Treasury bond market, (TLT), the Euro (FXE), (EUO), and the British pound (FXB).

Sometimes the best trades are the ones you don?t do. I have been able to dodge the bullets that have been killing off other hedge funds, including those in (USO) and commodities (CORN), (CU). The average hedge fund is up only 4% in 2013, as their short positions in the lowest quality companies have easily outpaced their longs on the upside.

All told, the last 35 of the 42 trade alerts issued by the Trade Alert Service in 2013 were profitable, a success rate of 83%. The year-to-date profit stands at a stunning 35.5%.

Global Trading Dispatch, my highly innovative and successful trade-mentoring program, earned a net return for readers of 40.17% in 2011 and 14.87% in 2012. The service includes my Trade Alert Service, daily newsletter, real-time trading portfolio, an enormous trading idea database, and live biweekly strategy webinars. To subscribe, please go to my website at www.madhedgefundtrader.com, find the ?Global Trading Dispatch? box on the right, and click on the lime green ?SUBSCRIBE NOW? button.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/04/TA-Since-2013.jpg342505Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-04-30 09:46:032013-04-30 09:46:03Trade Alert Service Posts Two Year 90% Profit

Come join me for lunch at the Mad Hedge Fund Trader?s Global Strategy Update, which I will be conducting in Las Vegas, Nevada on Wednesday, May 8, 2013. An excellent meal will be followed by a wide-ranging discussion and an extended question and answer period.

I?ll be giving you my up to date view on stocks, bonds, currencies, commodities, precious metals, and real estate. I will also explain how I have been able to deliver a blowout 40% return since the November, 2012 market bottom. And to keep you in suspense, I?ll be throwing a few surprises out there too. Tickets are available for $179.

I?ll be arriving at 11:00 and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets. The PowerPoint presentation will be emailed to you three days before the event.

The lunch will be held at a major Las Vegas hotel on the Strip, the details will be emailed with your purchase confirmation. Please make your own hotel reservations, as business there is booming.

I look forward to meeting you, and thank you for supporting my research. To purchase tickets for the luncheons, please go to my online store.

https://www.madhedgefundtrader.com/wp-content/uploads/2012/08/las-vegas-welcome-sign.jpg487325Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-04-30 09:41:312013-04-30 09:41:31May 8 Las Vegas Strategy Luncheon

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.