When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-15 13:23:332019-07-15 13:23:33Trade Alert - (TLT) July 15, 2019 - BUY

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.Read more

https://www.madhedgefundtrader.com/wp-content/uploads/2016/02/Alert-e1457452190575.jpg135150Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-15 10:50:392019-07-15 10:50:39Trade Alert - (FXA) July 15, 2019 - BUY

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to the six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-15 10:09:082019-07-15 10:09:08July 15, 2019 - MDT Alert (QCOM)

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.Read more

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-15 09:20:022019-07-15 09:20:02July 15, 2019 - MDT Pro Tips A.M.

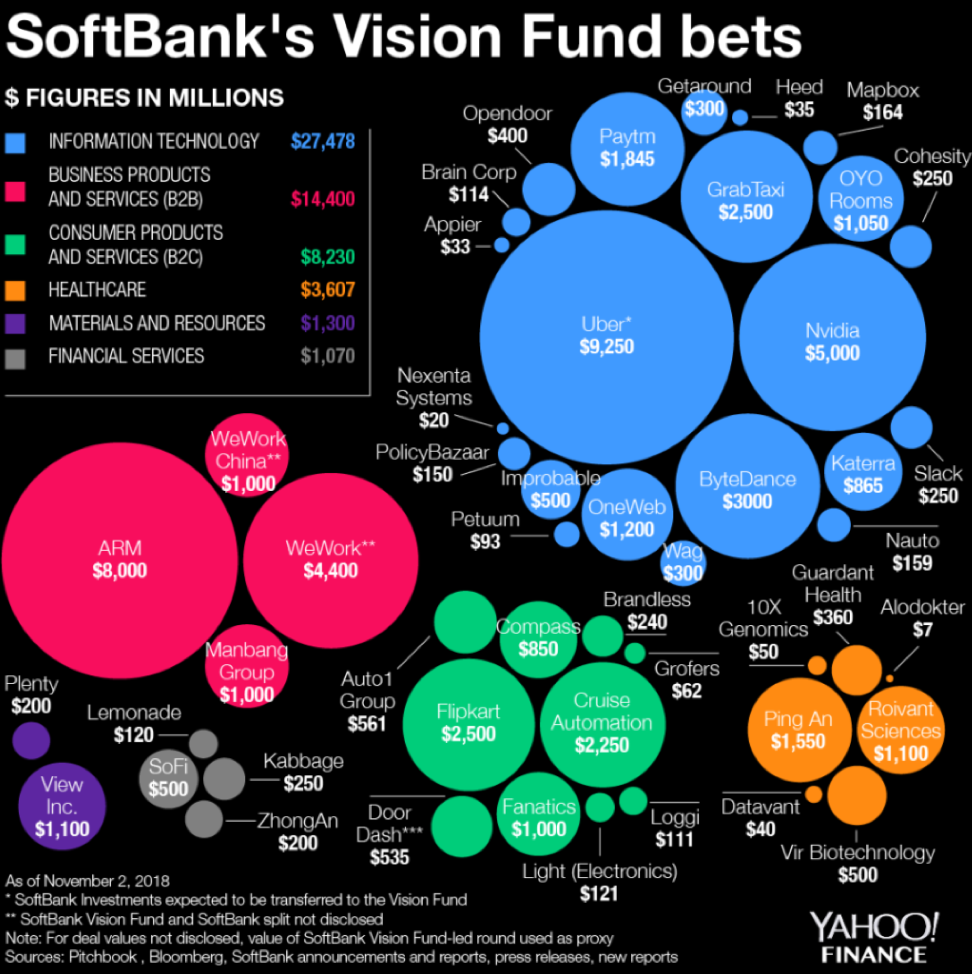

The man with the 300-year vision - Softbank’s Masayoshi Son.

He is the sole force exerting stultifying pressure on the venture capitalists of Silicon Valley.

What a ride it has been so far.

His $100 billion SoftBank Vision Fund has put the Sand Hill Road faithful in a tizzy – utterly revolutionizing an industry and showing who the true power resides with.

He has even gone so far as to double down on his exploits by claiming that he will raise additional $100 billion fund every few years and spend $50 billion per year.

This capital logically would flow into what he knows best – technology and the best technology money can buy.

Lately, Son said it best of the performance of the Vision Fund saying, “Results have actually been too good.”

So good that after this June, Son changed his schedule to spend 3% of his time on his telecom business down from 97% before June.

His telecommunications business in Japan has turned into a footnote.

It was just recently that Son’s tech investments eclipsed his legacy communications company.

Son vies to rinse and repeat this strategy to the horror of other venture capitalists.

The bottomless pit of capital he brings to the table predictably raises the prices for everyone in the tech investment world.

Son’s capital warfare strategy revolves around one main trope – Artificial Intelligence.

He also strictly selects industry leaders which have a high chance of dominating their field of expertise.

Geographically speaking, the fund has pinpointed America and China as the best sources of companies. India takes in the bronze medal.

His eyes have been squarely set on Silicon Valley for quite some time and his record speaks for himself scooping up stakes in power players such as Uber, WeWork, Slack, and GM (GM) Cruise.

Other stakes in Chinese firms he’s picked up are China’s Uber Didi Chuxing, China’s GrubHub (GRUB) Ele.me and the first digital insurer in China named Zhongan International costing him $500 million.

Other notable deals done are its sale of Flipkart to Walmart (WMT) for $4 billion giving SoftBank a $1.5 billion or 60% profit on the $2.5 billion position.

In 2016, the entire venture capitalist industry registered $75.3 billion in capital allocation according to the National Venture Capital Association.

This one company is rivalling that same spending power by itself.

Its smallest deal isn’t even small at $100 million, baffling the local players forcing them to scurry back to the drawing board.

The reverberation has been intense and far-reaching in Silicon Valley with former stalwarts such as Kleiner Perkins Caufield & Byers breaking up, outmaneuvered by this fresh newcomer with unlimited capital.

Let me remind you that it was once considered standard to cautiously wade into investment with several millions.

Venture capitalists would take stock of the progress and reassess if they wanted to delve in some more.

There was no bazooka strategy then.

SoftBank has promised boatloads of capital up front even overpaying in some cases in order to set the new market price.

Conveniently, Son stations himself nearby at a nine-acre estate in Woodside, California complete with an Italianate mansion he bought for $117.5 million in 2012.

It was one of the most expensive properties ever purchased in the state of California, even topping Hostess Brands owner Daren Metropoulos, who bought the Playboy Mansion from Hugh Hefner in 2016 for $100 million.

If you think Son is posh – he is not. He only fits himself out in the Japanese budget clothing brand Uniqlo. He just needed a comfortable place to stay and he hates hotels.

SoftBank hopes to cash in on its $4.4 billion investment in WeWork, an American office space-share company, proclaiming that WeWork would be his “next Alibaba.”

The company plans to shortly go public.

Son continued to say that WeWork is “something completely new that uses technology to build and network communities.”

Other additions to SoftBank’s dazzling array of unicorns is Bytedance, a start-up whose algorithms have fueled shot form video content app TikTok.

The deal values the company at $75 billion.

They have been able to insulate themselves from local industry giants Tencent and Alibaba.

Son has revealed that the Vision Fund’s annual rate of return has been 44%.

Cherry-picking off the top of the heap from the best artificial intelligence companies in the world is the secret recipe to outperforming your competitors.

At the same time, aggressively throwing money at these companies has effectively frozen out any resemblance of competition. Once the competition is frozen out, the value of these investments explodes, swiftly super-charged by rapidly expanding growth drivers.

How can you compete with a man who is willing to pay $300 million for a dog walking app?

This genius strategy has made the founder of SoftBank the most powerful businessman in the world.

Son owns the future and will have the largest say on how the world and economies evolve going forward.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/Softbank-CEO-2.png539472Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-15 08:02:532019-08-19 16:09:35How SoftBank is Taking Over the US Venture Capital Business

"We are unicorn hunters." - Said Founder and CEO of SoftBank Masayoshi Son

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/masayoshi.png424362MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2019-07-15 08:00:222019-08-19 16:09:43July 15, 2019 - Quote of the Day

(LAST CHANCE TO ATTEND THE FRIDAY, JULY 19 ZERMATT, SWITZERLAND STRATEGY SEMINAR)

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR HERE COMES YOUR NEXT HEART ATTACK),

(INDU), (SPY), (TLT), (GLD), (FXA), (USO)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-15 01:06:032019-07-14 22:01:51July 15, 2019

Come join me for the Mad Hedge Fund Trader’s Global Strategy Seminar, which I will be conducting high in the Alps in Zermatt, Switzerland. You can meet me at 2:00 PM on Friday, July 19, 2019.

An open discussion on the crucial issues facing investors today will take place. Coffee, tea, and schnapps will be made available, but no food. You are welcome to attend in your mountain climbing gear, if necessary. One year, a guest descended from the Matterhorn summit to attend.

I’ll be giving you my up to date view on stocks, bonds, foreign currencies, commodities, precious metals, energy, and real estate. And to keep you in suspense, I’ll be throwing a few surprises out there too. Tickets are available for $241.

I’ll be arriving early and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The event will be held at a central Zermatt hotel with a great Matterhorn view, the details of which will be emailed directly to you with your confirmation. Zermatt is 5,276 feet (1,608 meters) above sea level so make sure you’re in shape.

I look forward to meeting you and thank you for supporting my research. To purchase tickets for this seminar, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/05/zermatt.png445593Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-15 01:04:592019-10-16 16:41:17SOLD OUT - July 19 Zermatt, Switzerland Strategy Seminar

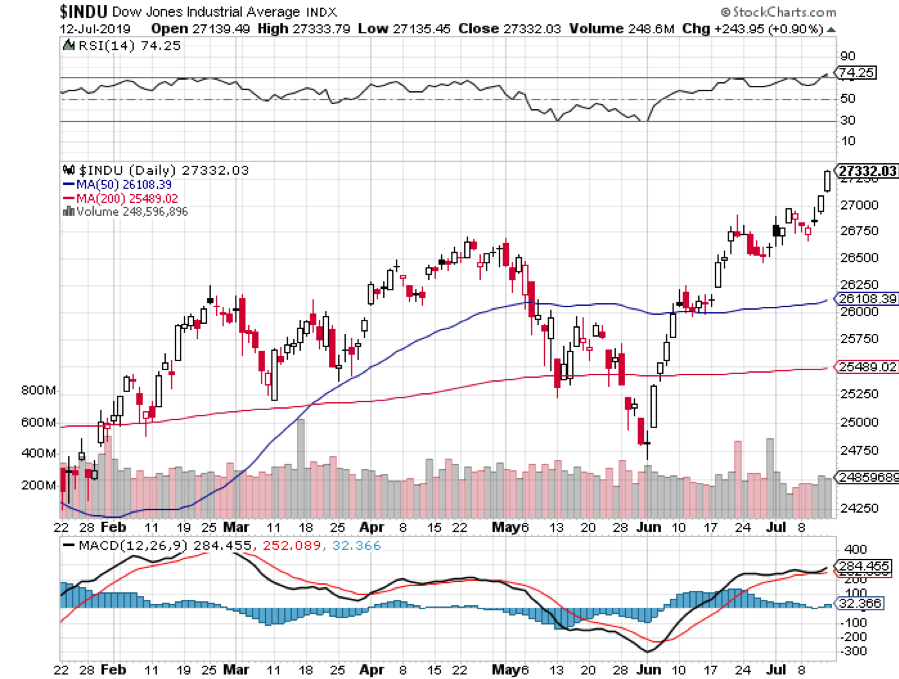

Sitting on a remote Alpine mountaintop this morning, this being Switzerland one with ample WIFI, I turned on my screen for the first time in four weeks and almost had a heart attack.

Risk markets everywhere have gone up almost every day since I left San Francisco in June, taking the major indexes up to new all time highs. They are doing this in the face of slowing global economies, falling earnings growth, and rising energy prices and inflation. Even the respected Atlanta Fed has a Q2 GDP growth forecast of a dismal 1.4%.

Did I mention that the US government is about to run out of money again in September, inviting another shut down?

In the old days the Federal Reserve used to be the sober chaperone at the party, making sure things didn’t get out of hand. Today, they are the devilish frat boy surreptitiously pouring 200 proof ethanol into the punch bowel, much as I used to do at Chemistry Department parties at UCLA during the early 1970s. The problem was that everyone else was doing the same thing, leading to some prodigious hangovers.

Another pint made it into the heady brew on Wednesday when Fed governor Jay Powell erred dovishly in his Humphrey Hawkins testimony in from of congress. It was enough to ignite the latest 500-point rally in the Dow (INDU).

The bullishness was confirmed by my own algorithmically driven Mad Hedge Market Timing Index, which reached a three-month high at 65. We have rallied an awesome 45 points from the 20 level in only six weeks and are now a mere 10 points away from solid “SELL” territory.

The end result of all this has been to bring forward my yearend target for the S&P 500 (SPY) of the low 3,000s to, like well, now. And if H1 has been one giant love best, how does that bode for H2?

A frightening convergence of events is setting up. Just when the Fed announces its interest rate decision on July 31, companies will be announcing earnings disappointments AND my Market Timing Index will be hitting the high seventies.

It all sets up what we traders call “an asymmetric risk/reward.” Good news will bring small incremental gain while even a small disappointment will serve up a horrendous sell off. Fed funds futures are now indicating a 100% of a 25-basis point rate cut on the 31st, and see overnight rates plunging to only 1.75% by yearend end. Hence the heart problems mentioned above.

So as much as you may despise, loathe, and hurl epitaphs at me, I am not going to tell you to buy the stock market today. Your last chance to do that was the final week of May.

The quality trade these days is clearly in other asset classes, like bonds (TLT), foreign exchange (FXA), gold (GLD), and energy (USO). My only exceptions will be “BUYS” in any bombed out high-quality single names I can find.

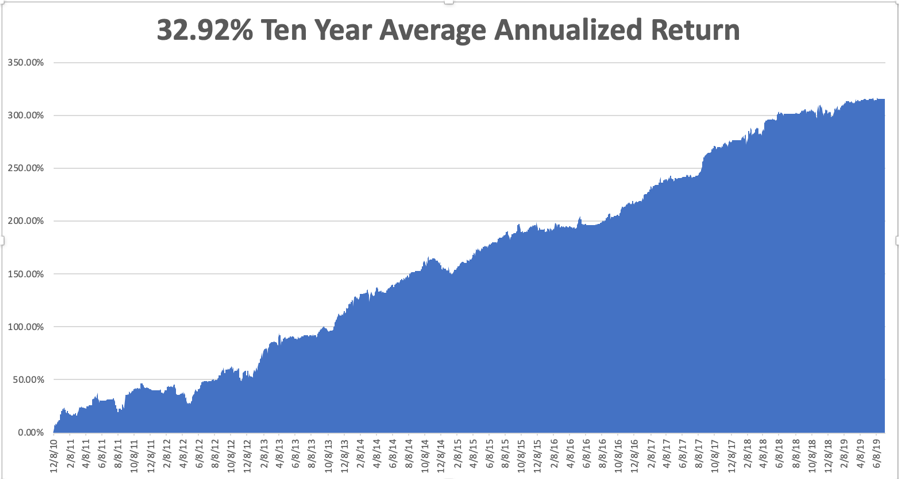

As I have been out of the market, my Global Trading Dispatch has been flat ling at up 15.38% year-to-date and has earned precisely 0% so far in July. My trailing one-year declined to +14.2%.

My ten-year profit fell back to +32.92%.With the markets now in the process of peaking out for the short term I am now 100% in cash with Global Trading Dispatch and 100% cash in the Mad Hedge Tech Letter.

The coming week will be a fairly sedentary one on the data front after last week’s fireworks.

On Monday, July 15 at 9:30 AM EST, New York’s Empire State Manufacturing Index is released.

On Tuesday, July 16 8:30 AM EST, the June US Retail Sales are out.

On Wednesday, July 17 at 8:30 AM EST, June Housing Starts are published.

On Thursday, July 18 at 8:30 AM EST, the Weekly Jobless Claims are printed. We also get the Philadelphia Fed Manufacturing Index.

On Friday, July 19 at 8:30 AM EST, we get the University of Michigan Consumer Sentiment Index. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I am how on my usual summer schedule. I’ll be getting up early every morning to climb an Alpine peak. Then I’ll be riveted to my screen by 3:30 PM when the US markets open, scouring the world for good Trade Alerts.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Market Timing Index

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-8.png422564Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-15 01:02:042019-07-14 22:02:55The Market Outlook for the Week Ahead, or Here Comes Your Next Heart Attack

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.