Mad Hedge Technology Letter

May 24, 2018

Fiat Lux

Featured Trade:

(MICRON'S BLOCKBUSTER SHARE BUYBACK)

(MU), (AMZN), (NFLX), (AAPL), (SWKS), (QRVO), (CRUS), (NVDA), (AMD)

Mad Hedge Technology Letter

May 24, 2018

Fiat Lux

Featured Trade:

(MICRON'S BLOCKBUSTER SHARE BUYBACK)

(MU), (AMZN), (NFLX), (AAPL), (SWKS), (QRVO), (CRUS), (NVDA), (AMD)

The Amazon (AMZN) and Netflix (NFLX) model is not the only technology business model out there.

Micron (MU) has amply proved that.

Bulls were dancing in the streets when Micron announced a blockbuster share buyback of $10 billion starting in September.

This is all from a company that lost $276 million in 2016.

The buyback is an overwhelmingly bullish premonition for the chip sector that should be the lynchpin to any serious portfolio.

The news keeps getting better.

Micron struck a deal with Intel to produce chips used in flash drives and cameras. Every additional contract is a feather in its cap.

The share repurchase adds up to about 16% of its market value and meshes nicely with its choreographed road map to return 50% of free cash flow to shareholders.

Tech's weighting in the S&P has increased 3X in the past 10 years.

To put tech's strength into perspective, I will roll off a few numbers for you.

The whole American technology sector is worth $7.3 trillion, and emerging markets and European stocks are worth $5 trillion each.

Tech is not going away anytime soon and will command a higher percentage of the S&P moving forward and a higher multiple.

The $5 billion in profit Micron earned in 2017 was just the start and sequential earnings beats are part of their secret sauce and a big reason why this name has been one of the cornerstones of the Mad Hedge Technology Letter portfolio since its inception as well as the first recommendation at $41 on February 1.

Did I mention the stock is dirt cheap at a forward PE multiple of just 6 and that is after a 35% rise in the share price so far this year?

What's more, putting ZTE back into business is a de-facto green light for chip companies to continue sales to Chinese tech companies.

China consumed 38% of semiconductor chips in 2017 and is building 19 new semiconductor fabrication plants (FAB) in an attempt to become self-sufficient.

This is part of its 2025 plan to jack up chip production from less than 20% of global share in 2015 to 70% in 2025.

This is unlikely to happen.

If it was up to them, China would dump cheap chips to every corner of the globe, but the problem is the lack of innovation.

This is hugely bullish for Micron, which extracts half of its revenue from China. It is on cruise control as long as China's nascent chip industry trails miles behind them.

At Micron's investor day, CFO David Zinsner elaborated that the mammoth buyback was because the stock price is "attractive" now and further appreciation is imminent.

Apparently, management was in two camps on the capital allocation program.

The two choices were offering shareholders a dividend or buying back shares.

Management chose share repurchases but continued to say dividends will be "phased in."

This is a company that is not short on cash.

The free cash flow generation capabilities will result in a meaningful dividend sooner than later for Micron, which is executing at optimal levels while its end markets are extrapolating by the day.

As it stands today, Micron is in the midst of taking its 2017 total revenue of about $20 billion and turning it into a $30 billion business by the end of 2018.

Growth - Check. Accelerating Revenue - Check. Margins - Check. Earnings beat - Check. Guidance hike - Check.

The overall chips market is as healthy as ever and data from IDC shows total revenues should grow 7.7% in 2018 after a torrid 2017, which saw a 24% bump in revenues.

The road map for 2019 is murkier with signs of a slowdown because of the nature of semi-conductor production cycles. However, these marginal prognostications have proved to be red herrings time and time again.

Each red herring has offered a glorious buying opportunity and there will be more to come.

Consolidation has been rampant in the chip industry and shows no signs of abating.

Almost two-thirds of total chip revenue comes from the largest 10 chip companies.

This trend has been inching up from 2015 when the top 10 comprised 53% in 2016 and 56% in 2017.

If your gut can't tell you what to buy, go with the bigger chip company with a diversified revenue stream.

The smaller players simply do not have the cash to splurge on cutting-edge R&D to keep up with the jump in innovation.

The leading innovator in the tech space is Nvidia, which has traded back up to the $250 resistance level and has fierce support at $200.

Nvidia is head and shoulders the most innovative chip company in the world.

The innovation is occurring amid a big push into autonomous vehicle technology.

Some of the new generation products from Nvidia have been worked on diligently for the past 10 years, and billions and billions of dollars have been thrown at it.

Chips used for this technology are forecasted to grow 9.6% per year from 2017-2022.

Another death knell for the legacy computer industry sees chips for computers declining 4% during 2017-2022, which is why investors need to avoid legacy companies like the plague, such as IBM and Oracle because the secular declines will result in nasty headlines down the road.

Half way into 2018, and there is still a dire shortage of DRAM chips.

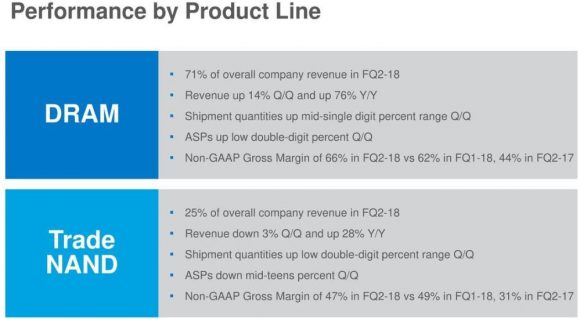

Micron's DRAM segments make up 71% of its total revenue, and the 76% YOY increase in sales underscores the relentless fascination for DRAM chips.

Another superstar, Advanced Micro Devices (AMD), has been drinking the innovation Kool-Aid with Nvidia (NVDA).

Reviews of its next-generation Epyc and Ryzen technology have been positive; the Epyc processors have been found to outperform Intel's chips.

The enhanced products on offer at AMD are some of the reasons revenue is growing 40% per year.

AMD and Nvidia have happily cornered the GPU market and are led by two game-changing CEOs.

It is smart for investors to focus on the highest quality chip names with the best innovation because this setup is most conducive to winning the most lucrative chip contracts.

Smaller players are more reliant on just a few contracts. Therefore, the threat of losing half of revenue on one announcement exposes smaller chip companies to brutal sell-offs.

The smaller chip companies that supply chips to Apple (AAPL) accept this as a time-honored tradition.

Avoid these companies whose share prices suffer most from poor analyst downgrades of the end product.

Cirrus Logic (CRUS), Skyworks Solutions (SWKS), and Qorvo Inc. (QRVO) are small cap chip companies entirely reliant on Apple come hell or high water.

Let the next guy buy them.

Stick with the tried and tested likes of Nvidia, AMD, and Micron because John Thomas told you so.

_________________________________________________________________________________________________

Quote of the Day

"Bitcoin will do to banks what email did to the postal industry." - said Swedish IT entrepreneur and founder of the Swedish Pirate Party Rick Falkvinge.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Global Market Comments

May 23, 2018

Fiat Lux

Featured Trade:

(MONDAY, JULY 16, 2018, PARIS, FRANCE, GLOBAL STRATEGY LUNCHEON),

(WHY I'M SELLING SHORT THE STOCK MARKET),

(SPY), (TLT),

(TESTING TESLA'S SELF-DRIVING TECHNOLOGY),

(TSLA)

Come join me for lunch at the Mad Hedge Fund Trader's Global Strategy Luncheon, which I will be conducting in Paris, France, on Monday, July 16, 2018. A three-course lunch will be followed by an extended question-and-answer period.

I'll be giving you my up-to-date view on stocks, bonds, foreign currencies, commodities, precious metals, energy, and real estate. And to keep you in suspense, I'll be throwing a few surprises out there, too. Enough charts, tables, graphs, and statistics will be thrown at you to keep your ears ringing for a week. Tickets are available for $259.

I'll be arriving early and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and discuss the financial markets.

The lunch will be held at a restaurant in a four-star hotel in the City of Light's central Opera district that was a favorite of Ernest Hemingway's, the details of which will be emailed to you with your purchase confirmation.

I look forward to meeting you and thank you for supporting my research.

To purchase tickets for the luncheon, please click here.

All good things must come to an end, and I think the latest rally in stocks has just about run out of steam.

Up 12 out of 14 days, and the stock market is starting to reach a point of exhaustion. The S&P 500 (SPY) is now at the top end of a four-month trading range.

In addition, we are now well into a seasonally negative period for stocks, the six months when the total return on indexes is zero. The summer slowdown is upon us, and the declining trading volume is screaming at us loud and clear.

Please note that for the past months, stocks have been rising on small volume and falling on big volume. That is classic late cycle market action and is increasingly making me afraid of my own shadow.

We have just had an onslaught of surprise good news that took us up this high, thus giving us a fabulous short side entry point.

That would include a China trade war temporarily going on hold, the administration's free pass for Iran sanctions busting for the multinational Chinese telecom company ZTE, and Micron Technology's (MU) announcement of a $10 billion share buyback. Good news tends to happen in three's, and on the third one you sell.

So, a shot on the short side is reasonable here. However, doing ANY trade with the Volatility Index (VIX) down here at the $12 handle is a bit of a stretch. But I have only sent out one Trade Alert so far in May, and my traders are starving for fresh red meat.

I am not turning bearish, nor do I expect a recession to strike imminently. That will take place in late 2019 at the earliest. I'm just executing a short-term trade here to keep from being bored to death.

It is all just a matter of numbers. The American labor force is currently growing at 0.5% a year, while productivity is expanding by 1.5%. Add them together and that gives you 2% annual trend growth. Add in a 2% inflation rate and you get a 4% nominal GDP growth rate.

That growth rate means the Fed funds overnight interest rate should be 2.5%, a full 1% above the present 1.5%, so four more 25 basis point Fed rate hikes are a sure thing. It will get to 2.5% in a year.

Similarly, a 4% nominal growth rate historically brings you a 4% 10-year U.S. Treasury bond yield versus the current 3.07%, so we have another year to get to 4% as well.

That means our short strategy in the (TLT) is alive and well, we're just waiting for a better entry point. A 4% Treasury bond targets $98 on the downside in the (TLT), or down another $19 from today's close.

With a price earnings multiple 17X and an assumed earnings per share of $155, that puts the fair value for the S&P 500 of $2,720, or exactly where it is right now.

So the stock market isn't expensive, rich, or euphoric. Nor is it at bargain basement throwing the baby out with the bathwater cheap. It is dead in the middle.

And bull markets never end with fair valuation; they end with valuation upside blowouts. We dallied there at the end of January, but only for a few days. We may not see those high numbers again until the end of 2018.

And here's the bad news. Trading conditions could remain like this for another five months, until the November midterm congressional elections.

Just thought you'd like to know.

Mad Hedge Technology Letter

May 23, 2018

Fiat Lux

Featured Trade:

(WHY THE BIG DEAL OVER ZTE?),

(MU), (QCOM), (INTC), (AAPL), (SWKS), (TXN), (BIDU), (BABA)

"If a cop follows you for 500 miles, you're going to get a ticket," said Oracle of Omaha Warren Buffett, in reference to Bank of America's many legal problems.

Here's the conundrum.

Beyond cutting-edge technology, there's nothing that China WANTS OR NEEDS to buy from the U.S. China's largest imports are in energy and foodstuffs, both globally traded commodities.

China is playing the long game because it can.

Earlier this year, China altered its constitution to remove term limits and any obstacle that would hinder Chairman Xi to serve indefinitely.

If it's two, four, eight or 10 years, no problem, China will wait it out.

As it stands, China is enjoying the status quo, which is a robust economic trajectory of 6.7% economic growth YOY and at that rate will leapfrog America as the biggest economy in the world by 2030.

China does not need handouts.

It already has its mooncake and is eating it.

The Chinese are also betting that Donald Trump fades away with the passage of time, possibly soon, and that a vastly different administration will enter the fray with an entirely different strategy.

The indefinite "hold" pattern is a polite way to say we surrender.

ZTE Corporation is a Chinese telecommunications equipment manufacturer and low-end smartphone maker based in Shenzhen, China.

This seemingly innocuous company is ground zero for the U.S. vs China trade practice dispute.

The U.S. Department of Commerce banned American tech companies from selling components to ZTE for seven years, crippling its supply chain after violating sanctions against Iran and North Korea.

ZTE uses about 30% of American components to produce its smorgasbord of telecom equipment and down-market cell phones.

What most people do not know is that ZTE is the fourth most prevalent smartphone in America, only behind Apple, Samsung, and LG, commanding a 12.2% market share, and its phones require an array of American made silicon parts.

In 2017, the company shipped more than 20 million phones to the United States.

The ruling effectively put ZTE out of business because the lack of components shelved production.

Low-end smartphones account for almost one-third of total revenue.

ZTE could very well have survived with a direct hit to its consumer phone business, but the decision to ban components made the telecom equipment division inoperable.

This segment accounts for a heavy 58.2% of revenue. Therefore, disrupting ZTE's supply chain would effectively take down more than 91% of its business for a company that employs 75,000 employees in over 160 countries.

Upon news of ZTE's imminent demise, the administration made a U-turn on its initial decision stating "too many jobs in China lost."

The reversal made America look bad.

It shows that America is being dictated to and not the other way around.

When did it become the responsibility of the American administration to fill Chinese jobs for a company that is a threat to national security?

The Chinese refused to continue talks with the visiting delegation until the ZTE situation was addressed.

Treasury Secretary Steve Mnuchin and company were able to "continue" the talks then were politely shown the door.

Bending the rules for ZTE should have never been a prerequisite for talks, stressing the lack of firepower in the administration's holster.

However, stranding the delegation in Chinese hotel rooms for days waiting in limbo, without offering an audience, would have caused even more humiliation and anguish for the administration.

China is not interested in buying much from America, but one thing it needs -- and needs in droves -- are chips.

Long term, this ZTE ban is great for China.

I believe China will use this episode to rile up the nationalistic rhetoric and make it a point to wean itself from American chips.

However, for the time being, American chips are the most valuable import America can offer China, and that won't change for the foreseeable future.

The numbers back me up.

Micron (MU) earns more than $10 billion in revenue from China, which makes up over 51% of its total revenue.

Qualcomm (QCOM), mainly through its lucrative licensing division, makes more than $14.5 billion from its Chinese revenue, which comprises over 65% of revenue.

Texas Instruments (TXN) earns more than 44% of revenue from China, and almost a quarter of Intel's (INTC) revenue is derived from its China operations.

The biggest name embedded in China is Apple (AAPL), which earned almost $45 billion in sales last year. Its China revenue is three times larger than any other American company.

In less than a decade, China has caught up.

China now has adequate local smartphone substitutes through Huawei, Oppo, Vivo, and Xiaomi phones.

Skyworks Solutions (SWKS), a chip company reliant on iPhone contracts, is most levered toward the Chinese market capturing almost 83% of revenue from China.

You would think these chips would be the first on the chopping block in a trade war. However, you are wrong.

China needs all the chips it can get because there is no alternative.

Stopping the inflow of chips is another way of stopping China from doing business and developing technology.

The Chinese economy has been led by the powerful BATs of Baidu (BIDU), Tencent, and Alibaba (BABA) occupying the same prominent role the American FANGs hold in the American economy.

They are not interested in digging their own grave.

To execute the 2025 plan to become the world leaders in advanced technology, they need chips that power all modern electronic devices.

The most likely scenario is that China maintains development using American chips for the time being and slowly pivots to the Korean chip sector, which is vulnerable to Chinese political pressure.

Remember that South Koreans have two of the three biggest chip companies in the world in Samsung and SK Hynix. China has used economic coercion to get what it wants from Korea in the past or to prove a point.

Korean multinational companies, shortly after the Terminal High Altitude Area Defense (THAAD) installation on the Korean peninsula, were penalized by the Chinese government shutting down mainland Korean stores, temporarily banning Chinese tourism in South Korea, and blocking K-pop stars from performing in the lucrative Chinese market.

The Chinese communist government can turn the screws when it wants and how it wants.

Therefore, the next battleground for tech could migrate to South Korean chip companies as China is on a mission to suck up as much high-grade tech ingenuity as possible while it can.

China has some easy targets to whack down if the administration forces it into a corner with a knife to its throat.

Non-tech companies are ripe for massacre because they do not produce chips.

Companies such as Procter & Gamble, Starbucks, McDonald's, and Nike could be replaced by a Chinese imitation in a jiffy.

Apple is the 800-pound gorilla in the room.

An attack on Apple would hyper-accelerate tension between two leaders to the highest it's ever been and would be the straw that breaks the camel's back.

Technology has transformed the world.

Technology also has been adopted by nations as a critical component to national security.

Nothing has changed fundamentally, and nothing will.

China will become the biggest economy in the world by 2030.

China will kick the proverbial can down the road because it can. It never has to cooperate with America again.

Contrary to expectations, American chip companies are untouchable, and investors won't see Micron suddenly losing half its revenue over this trade war.

Until China can produce higher quality chips, it will lap up as much of Uncle Sam's chips until it can force transfer the chip technology from the Koreans.

American chip companies can breathe a sigh of relief.

_________________________________________________________________________________________________

Quote of the Day

"If we go to work at 8 a.m. and go home at 5 p.m., this is not a high-tech company and Alibaba will never be successful. If we have that kind of 8-to-5 spirit, then we should just go and do something else." - said Alibaba founder and executive chairman Jack Ma.