Global Market Comments

October 18, 2024

Fiat Lux

Featured Trade:

(HOW TO FIND A GREAT OPTIONS TRADE)

Global Market Comments

October 18, 2024

Fiat Lux

Featured Trade:

(HOW TO FIND A GREAT OPTIONS TRADE)

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Mad Hedge Biotech and Healthcare Letter

October 17, 2024

Fiat Lux

Featured Trade:

(NO TEARS HERE)

(JNJ)

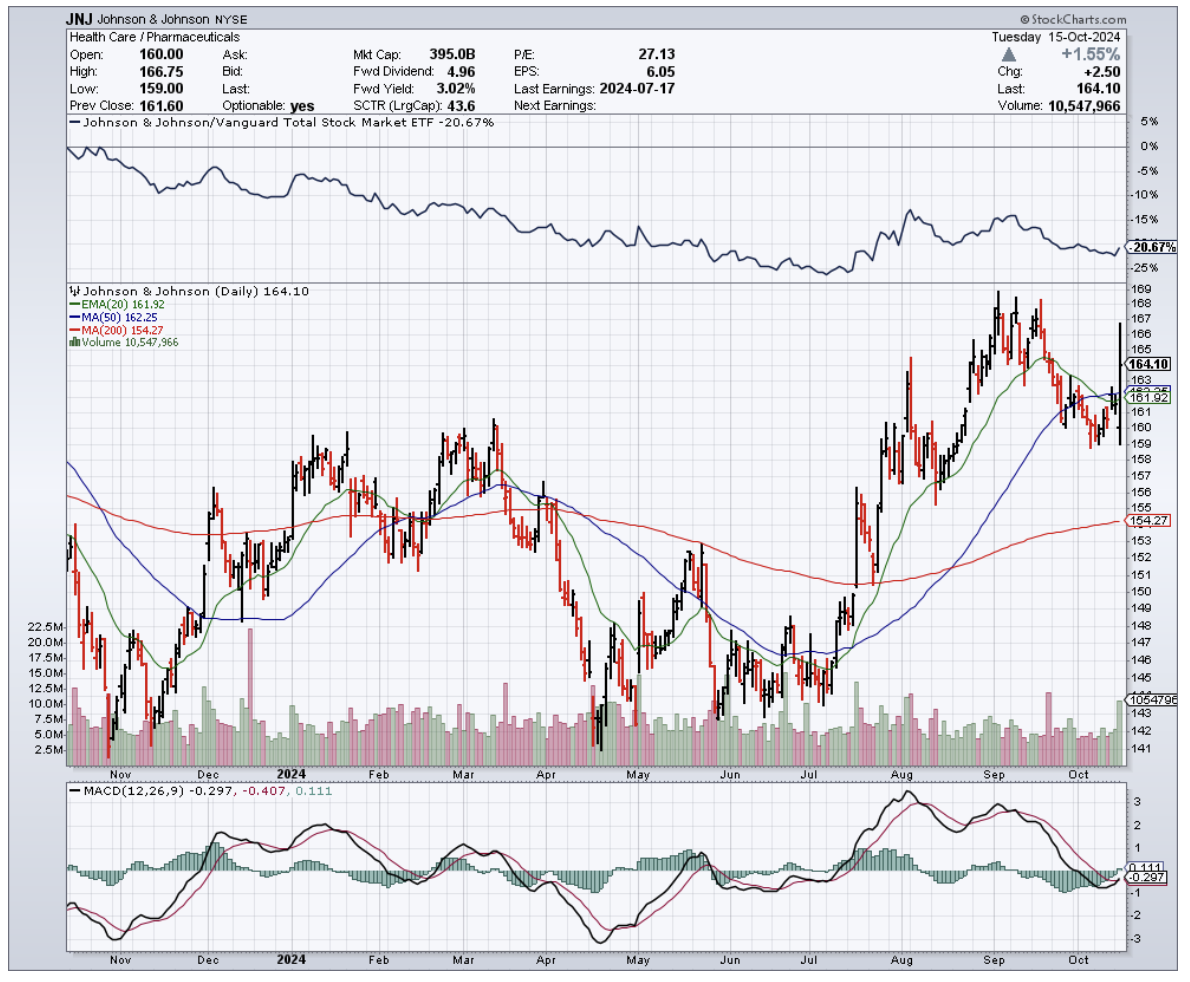

If you've been following my adventures in the market jungle for any length of time, you know I've got a nose for opportunity that'd make a bloodhound jealous. Well, folks, that nose is twitching something fierce, and it's pointed straight at Johnson & Johnson (JNJ).

Now, I know what you're thinking: "John, J&J? Aren't they as exciting as watching paint dry?" Before you dismiss this company, let me tell you—this isn't your grandma's Band-Aid shop anymore.

First off, let's talk about their pharmaceutical arm. It's not just flexing; it's practically bench-pressing the competition with one hand tied behind its back. I'm talking about a lineup that includes immunology juggernauts like Stelara and Tremfya, and cancer-fighting dynamos such as Darzalex and Erleada.

But here's the kicker—they've got over 40 late-stage clinical trials cooking. That's no mere pipeline; it's a veritable gusher of potential blockbusters.

The surprises from J&J don't end there. They recently spun off their consumer health unit faster than you can say "No more tears." Why? To zero in on their real money-makers: pharmaceuticals and medical devices. It's like watching a prizefighter shed weight before a title bout—leaner, meaner, and ready to deliver a knockout punch to the market.

Speaking of punches, J&J has been on an acquisition spree that'd make a Silicon Valley startup blush. On October 9th, they snatched up V-Wave for a cool $1.7 billion, adding to their previous grabs of Abiomed ($16.6 billion in 2022) and Shockwave Medical ($13.1 billion in 2024). And if you think they're splurging just for the heck of it, think again. This triple play gives J&J a solid foothold in the $60 billion cardiovascular device market, which is growing at a heart-racing 8% annually.

So, what does V-Wave bring to a giant like J&J? It's not just another cog in the medical machine. V-Wave is developing innovative treatment options for heart failure patients. Their device has already snagged the FDA's breakthrough device designation in 2019 and Europe's CE mark in 2020. For J&J, this means they can hit the ground running, spreading V-Wave's Ventura Interatrial Shunt across the globe faster than you can say "cardiovascular revolution."

As for their Q3 results? Let's just say J&J didn't settle for merely meeting expectations—they exceeded them. We're looking at a 5.4% adjusted operational revenue growth, with their cardiovascular business shooting up 26.5% year-over-year.

Now, I'm no fortune teller—if I were, I'd be writing this from my private island—but I'd bet my favorite Bloomberg terminal that their cardiovascular business is going to keep pumping life into J&J's MedTech segment. With more folks lining up for cardiovascular procedures than a Black Friday sale, J&J is poised to ride this wave like a pro surfer at Pipeline.

Of course, it's not all sunshine and rainbows. Their China business is facing more headwinds than a kite in a hurricane, thanks to an anti-corruption campaign that's thrown a monkey wrench into their marketing machine.

But hey, this is J&J we're talking about—a company that's been around since Grover Cleveland was in the White House. They've seen tougher times than this and come out swinging.

So, what's the bottom line? I'm slapping a "Buy" rating on this stock, with a fair value of $195 per share. For those of you looking for a stock that combines the stability of a mountain with the growth potential of a tech startup, J&J might just be your golden ticket.

Now, if you'll excuse me, I've got a sudden urge to go check my own blood pressure after all this excitement.

P.S. If J&J ever decides to venture into stem cell therapy for aging knees, you can bet I'll be first in line. These well-worn joints have a few more mountains to climb!

Global Market Comments

October 17, 2024

Fiat Lux

Featured Trade:

(FRIDAY OCTOBER 25 SALT LAKE CITY UTAH STRATEGY LUNCHEON)

(THIS IS NOT YOUR FATHER’S NUCLEAR POWER PLANT)

(SMR), (MSFT), (GOOGL), (AMZN)

Come join me for the Mad Hedge Fund Trader’s Global Strategy Luncheon, which I will be conducting high in the western desert in Salt Lake City, Utah at the foot of the Rocky Mountains. The event begins at 12:00 noon on Friday, January 31, 2025.

A three-course meal will be provided and an open discussion on the crucial issues facing investors today will take place. The dress is business casual.

I’ll be giving you my up-to-date view on stocks, bonds, foreign currencies, commodities, precious metals, energy, China, and real estate. And to keep you in suspense, I’ll be throwing a few surprises out there too. Tickets are available for $276.

I’ll be arriving early and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The event will be held in a private room at a downtown Salt Lake City restaurant, the details of which will be emailed directly to you with your confirmation.

I look forward to meeting you, and thank you for supporting my research.

To purchase tickets for this luncheon, please click here.

A 35% move-up in one day certainly gets one’s attention. The move was prompted by Microsoft’s (MSFT), Google (GOOGL), and Amazon’s (AMZN) move into the nuclear industry to supply electricity for AI data centers over the past two weeks.

Building on my early career at the Atomic Energy Commission in the 1970’s, I have been covering this company since 2012, and it has been a long and windy road. In one shot, they have solved the dozen problems that held the industry back in the 1950’s.

But thanks to Three Mile Island, Chernobyl, and Fukushima, nuclear had the kiss of death on it, making it impossible for the company to raise capital. The Company finally went public in May 2022 at $10.55 with major backing from Bill Gates, with the ticker symbol of (SMR) for “small modular reactor.”

Then, it rallied 60% when it obtained its first order. It then crashed to $1.80 in 2023 when that single order was canceled. It has doubled since September 1, when the new nuclear movement gained traction.

Nuscale’s design eliminates the risk of a meltdown by refining uranium into small pellets and then encasing them with five layers of zirconium. The heat generated is enough to boil water but not go supercritical. The cost of huge billion-dollar containment structures is eliminated by putting the plants underground.

Below, find my original 2012 research piece.

“On my recent trip to Oregon, I met with venture capital investors in NuScale Power, which is trailblazing the brave new world of “new” nuclear. Their technology has been pioneered by Dr. Jose Reyes, dean of the School of Engineering at Oregon State University in Corvallis.

This is definitely not your father’s nuclear power plant. The company has applied for design certification with the Nuclear Regulatory Commission for a mini-light water reactor with a passive cooling system rated at 45 megawatts. The idea is to site a dozen of these together, which in aggregate can generate 540 Megawatts, little more than half the size of the old 1-gigawatt monsters.

Running a dozen small reactors instead of one big one makes for vastly easier operation and maintenance, as individual units can be brought on and offline as needed. Small size also eliminates the need for gargantuan, expensive containment structures.

This power source runs at night when solar and wind plants are offline. Modular design makes mass production of these units economical. Once certification, approval, permitting, and construction are complete, we can expect to see the NuScale plants running by 2018.

After all, if something similar works in nuclear-powered submarines and aircraft carriers, why not in industrial zones on the outskirts of town? For more on NuScale’s innovative efforts, visit their website by clicking here.”

While the stock has already had a great run from the bottom up tenfold, it's probably not too late to buy. This could be another Nvidia-type situation.

![]()

![]()

My Old Jeep

Mad Hedge Technology Letter

October 16, 2024

Fiat Lux

Featured Trade:

(THE CHIP TRADE IS STILL IN-TACT)

(ASML)

Computer chip equipment maker ASML said they will cut 2025 financial guidance, citing weakness in markets other than AI and delayed orders.

This triggered a steep sell-off in many chip names, and I view this as a healthy event.

We are bombarded with so much robust news from the chip sector that it is hard for investors to catch their breath before the next spike higher in underlying shares.

Once in a while, it is highly positive to recalibrate momentum and allow the stock to settle.

Chips are definitely boom-and-bust stocks, and we are right in the middle of the boom. and I wouldn’t be too worried for other chip companies as we head into earnings.

This is a great chance to buy the dip in many of the best of class.

Europe's most valuable technology company, ASML, as an essential supplier to chipmakers, is not in question. But doubts have emerged over short-term sales and, for the longer term, whether it can continue to outgrow the overall market.

ASML's dominance of the market for lithography tools needed to create circuitry triggered the stock to all-time highs before this recent weakness.

After the health crisis of the early 2020’s, customers stopped overbuying, which reduced demand.

Now, ASML said some customers had announced delays of new plants and upgrades, including makers of the logic chips used in smartphones, PCs, and other devices.

Manufacturers that make the memory chips that go into them also plan fewer expansions, meaning they can rely on existing equipment for longer.

That's especially the case for an upstream equipment supplier highly reliant on the spending plans of its manufacturing customers.

It’s highly likely that Taiwan Semiconductor was the company who decided to cut back on business with ASML.

TSMC has been spending rather low capex numbers so far this year, and they may do so again next year because their overall (plant) utilization is not as good as their sales numbers suggest.

Among ASML customers that make logic chips, Intel said in August it would cut capital spending by $10 billion in 2025, while Samsung has said it faces challenges at the factory it is building in Texas.

Roughly a quarter of chipmakers' spending on tools goes to ASML, though some analysts say changes in chip-making techniques could lead that to be lower.

Management also said that customer delays are also a negotiating tactic that may force pricing concessions from ASML, squeezing margins.

Ultimately, this is a temporary demand adjustment after years of outperformance, and I would allow the seasonality to work itself through the system.

I see no threat to the overall business model of ASML, and if bad news on ASML triggers hits to other great chip stocks, I would look at some short-term bull call spreads on strong chip stocks in the US.

At the very least, if you don’t buy the dip, don’t take the other side of the trade because, more often than not, this type of price action sets up a “rip your face off” rally to the upside.

(A DISRUPTIVE MODEL COULD CHALLENGE THE BANKS)

October 16, 2024

Hello everyone

The big banks are in control, and nothing could shift their dominance, right?

Well, it might be time for a re-think of that notion.

In banking, the most potent disruptive model is coming from a group called ‘Revolut’ and it has just moved a step closer to getting an Australian banking license.

It’s just got a banking license in the UK, which means an Australian license now looks like a sure thing.

In fact, it is already making some serious inroads in the local market; the company has signed up 720,000 customers already in Australia and has transaction volumes annualized at an estimated $1bn.

Overseas, there are approximately 45 million very happy customers who have left the old banking players behind.

Revolut’s big chief, 40-year-old Russian-born Nikolay Stornosky, says he aims for the group to become the “Amazon of banking”.

So, why is Revolut such a big deal?

It began as a card service competing with operators like Western Union and quickly built up an overseas network of customers who found it faster and cheaper than traditional banks.

Revolut’s headquarters are in London. Its big breakthrough came when it got an EU license. More recently, the Bank of England license confirmed its status as a fully-fledged financial juggernaut, and it can now do everything from mortgages to deposits.

According to Matt Baxby, Chief Executive of Australian Operations, Revolut in Australia is growing at 100% a year, and that’s with a very low profile.

One outstanding feature is the security feature. It offers a once-off card number for any payment.

We are all aware of some of the trepidations we have when traveling and handing over our card numbers. Once a fraudulent operation has your number, you are in big trouble. Revolut’s “disposable card” regenerates your number after each use: problem quickly solved.

Revolut is currently estimated to be worth about $45bn off the back of a recent share sell-down, making it about one-fifth the size of CBA.

QI CORNER

SOMETHING TO THINK ABOUT

Cheers

Jacquie