My friend and esteemed colleague, Mad Day Trader Jim Parker, spent the weekend perusing hundreds of long term charts. He was assembling a short list of attractive names to buy after the next major sell off.

I am not talking about a modest 4% decline. Even a textbook 10% won?t get his attention. I?m talking about the kind of gut churning, rip your face off, time to change the shorts panic that you only see in your worst nightmares.

Keep in mind that Jim is a technical and momentum analyst. He doesn?t know the CEO?s, hasn?t done the channel checks, nor has he gone through the balance sheets and income statements with a fine tooth comb. That is my job.

These are picks that are simply interesting on a chart basis only. Here they are, with ticker symbols included. For specific upside targets, please contact Jim directly.

BUY (KITE) Kite Pharmaceuticals

BUY (PCYC) Pharmacyclics, Inc.

BUY (AGN) Allergan

BUY (ACT) Actavis

BUY (PANW) Palo Alto Networks

BUY (GS) Goldman Sachs

BUY?(BRKA) Berkshire Hathaway

BUY?(SMH) Market Vectors Semiconductors Index

BUY?(MMM) 3M Co.

BUY?(DIS) Walt Disney Co.

BUY?(SWKS) Skyworks Solutions

BUY?(LNG) Cheniere Energy

Keep in mind that companies with great fundamentals often have fantastic charts as well. This is why you often have researchers and technicians frequently making identical recommendations.

One approach might be to trade around these over time, but only from the long side. Another might be to enter deep out-of-the-money limit orders to buy in case we get a mini flash crash in your favorite name.

While the Diary of a Mad Hedge Fund Trader focuses on investments over a one week to six-month time frame, Mad Day Trader will exploit money-making opportunities over a brief ten minute to three day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points.

The Diary of a Mad Hedge Fund Trader is written by me, John Thomas, who you may have met during my recent series of conferences in the southern hemisphere.

I use a combination of deep, long term fundamental research, technical analysis and a global network of contacts to generate great investment ideas. The target holding period can be anywhere from three days to six months, although if something fortuitously doubles in a day, I don?t need to be told twice to take a profit (yes, this happens sometimes).

Last year, I issued some 200 Trade Alerts, of which 80% were profitable.

The Mad Day Trader is a separate, but complimentary service run by my Chicago based friend, Jim Parker. He uses a dozen proprietary short-term technical and momentum indicators he developed himself to generate buy and sell signals.

These will be sent to you by email for immediate execution. During normal trading conditions, you should receive three to five alerts and updates a day. The target holding period can be anywhere from a few minutes to three days.

Jim issues far more alerts and updates than I, possibly as many as 1,000 a year. He also uses far tighter stop loss limits, given the short-term nature of his strategy. The goal is to keep losses miniscule so you can always live to fight another day.

You will receive the same instructions for order execution, like ticker symbols, entry and exit points, targets, stop losses, and regular real time updates, as you do from the Mad Hedge Fund Trader. At the end of each day, a separate short-term model portfolio will be posted on the website for both strategies.

Jim Parker is a 40-year veteran of the wild and wooly trading pits in Chicago. Suffice it to say, Jim knows which end of a stock to hold up. I have followed his work for yonks, and can?t imagine a better partner in the serious business of making money for you, the reader.

Together, the?Mad Hedge Fund Trader?and the?May Day Trader?comprise?Mad Hedge Fund Trader PRO, which is for sale on my website for $4,500 a year.

You can upgrade your existing Global Trading Dispatch service, to include the Mad Day Trader. For more information, please call my loyal assistant, Nancy, in Florida at 888-716-1115 or 813-388-2904, or email her directly at?support@madhedgefundtrader.com.

00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-23 01:04:462015-01-23 01:04:4612 Stocks to Buy at the Bottom

After a prolonged, four year hibernation, it appears that the gold bulls are at long last back.

Long considered nut cases, crackpots and the wearers of tin hats, lovers of the barbarous relic have just enjoyed the first decent trading month in a very long time.

The question for the rest of us is whether there is something real and sustainable going on here, or whether the current rally will end with yet another whimper, to be sold into.

To find the answer, you?ll have to read until the end of this story.

Let me recite all the reasons that perma bulls used to buy the yellow metal.

1) Obama is a socialist and is going to nationalize everything in sight, prompting a massive flight of capital that will send the US dollar crashing.

2) Hyperinflation is imminent and the return of ruinous double digit price hikes will send investors fleeing into the precious metals and other hard assets, the last true store of value.

3) The Federal Reserve?s aggressive monetary expansion through quantitative easing will destroy the economy and the dollar, triggering an endless bid for gold, the only true currency.

4) To protect a collapsing greenback, the Fed will ratchet up interest rates, causing foreigners to dump the half of our national debt they own, causing the bond market to crash.

5) Taxes will skyrocket to pay for the new entitlement state, the government?s budget deficit will explode, and burying a sack of gold coins in your backyard is the only safe way to protect your assets.

6) A wholesale flight out of paper assets of all kind will cause the stock market to crash. Remember those Dow 3,000 forecasts?

7) Misguided government policies and oppressive regulation will bring the Armageddon, and you will need gold coins to bribe the border guards to get out of the country. You can also sew them into the lining of your jacket to start a new life abroad, presumably under an assumed name.

Needless to say, it didn?t exactly pan out that way. The end-of-the-world scenarios that one regularly heard at Money Shows, Hard Asset Conferences, and other dubious sources of investment advice all proved to be so much bunk.

I know, because I was a regular speaker on this circuit. I alone, a voice in the darkness, begged people to buy stocks at the beginning of the greatest bull markets of all time, which was then, only just getting started.

Eventually, I ruffled too many feathers with my politically incorrect views, and they stopped inviting me back. I think it was my call that rare earths (REMX) were a bubble that was going to collapse was the weighty stick that finally broke the camel?s back.

So, here we are, five years later. The Dow Average has gone from 7,000 to 18,000. The dollar has blasted through to a 12 year high against the Euro (FXE). The deficit has fallen by 75%. Gold has plummeted from $1,920 to $1,100. And no one has apologized to me, telling me that I was right all along, despite the fact that I am from California.

Welcome to the investment business.

Except that now, gold is worth another look. It has rallied a robust $200 off the bottom in a mere two months. Some of the most frenetic action was seen in the gold miners (GDX), where shares soared by as much as 50%. Even mainstay Barrick Gold (ABX) managed a 30% revival.

The gold bulls are now looking for their last clean shirt, sending suits out to the dry cleaners, and polishing their shoes for the first time in ages, about to hit the road to deliver almost forgotten sales pitches once again.

The news flow has certainly been gold friendly in recent weeks. Technical analysts were the first to raise the clarion call, noting that a string of bad news failed to push gold to new lows. Charts started putting in the rounding, triple bottoms that these folks love to see.

The New Year stampede into bonds gave it another healthy push. One of the long time arguments against the barbarous relic is that it pays no yield or dividend, and therefore has an opportunity cost.

Well guess what? With ten year paper now paying a scant 0.40% in Germany, 0.19% in Japan, and an eye popping -0.04% in Switzerland, nothing else pays a yield anymore either. That means the opportunity cost of owning precious metals has disappeared.

Then a genuine black swan appeared out of nowhere, improving gold?s prospects. The Swiss National Bank?s doffing of its cap against the Euro (FXE) ignited an instant 20% revaluation of the Swiss franc (FXF).

In addition to wiping out a number of hedge funds and foreign exchange brokers around the world, they shattered confidence in the central bank. And if you can?t hide in the Swiss franc, where can you?

This all accounts for the $200 move we have just witnessed.

So now what?

From here, the picture gets a little murky.

Certainly, none of the traditional arguments in favor of gold ownership are anywhere to be seen. There is no inflation. In fact, deflation is accelerating.

The dollar seems destined to get stronger, not weaker. There is no capital flight from the US taking place. Rather, foreigners are throwing money at the US with both hands, escaping their own collapsing economies and currencies.

And once global bond markets top out, which has to be soon, the opportunity cost of gold ownership returns with a vengeance. You would think that with bond yields near zero we are close to the bottom, but I have been wrong on this so far.

All of which adds up to the likelihood that the present gold rally is getting long in the tooth, and probably only has another $50-$100 to go, from which it will return to the dustbin of history, and possibly new lows.

I am not a perma bear on gold. There is no need to dig up your remaining coins and dump them on the market, especially now that the IRS has a mandatory withholding tax on all gold sales. I do believe that when inflation returns in the 2020?s, the bull market for gold will return for real.

You can expect newly enriched emerging market central banks to raise their gold ownership to western levels, a goal that will require them to buy thousands of tons on the open market.

Gold still earns a permanent bid in countries with untradeable currencies, weak banks, and acquisitive governments, like China and India, still the world?s largest buyers.

Remember, too, that they are not making gold anymore, and that all of the world?s easily accessible deposits have already been mined. The breakeven cost of opening new mines is thought to be around $1,400 an ounce, so don?t expect any new sources of supply anytime soon.

These are the factors which I think will take gold to the $3,000 handle by the end of the 2020?s, which means there is quite an attractive annualized return to be had jumping in at these levels. Clearly, that?s what many of today?s institutional buyers are thinking.

Sure, you could hold back and try to buy the next bottom. Oh, really? How good were you at calling the last low, and the one before that?

Certainly, incrementally scaling in around this neighborhood makes imminent sense for those with a long-term horizon, deep pockets and a big backyard.

Oops!

https://www.madhedgefundtrader.com/wp-content/uploads/2014/07/John-Thomas-Gold-e1455831491219.jpg297400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-22 10:51:162015-01-22 10:51:16Is the Bull Market in Gold Back?

I?ve just spent the entire morning on the phone, and it?s clear that thousands of individuals, hedge funds and brokers have just been wiped out as a result of The Swiss National Bank?s surprise move to remove its cap against the Euro.

This is a black swan on steroids.

And it hasn?t just been Swiss franc positions that have been bedeviling traders. You can add to the list bonds, energy, and this week, financial stocks as well. All of a sudden, the world seems to have gone mad.

The great flaw in the management of big brokers and hedge funds is that they base their risk models on historic data. It is rare to see a foreign currency move more than 1% against the US dollar in a day. You might see that one-day a year.

Risk models, and margin requirements, are therefore based on this assumption. To bomb proof themselves, margin departments might require clients to post collateral assuming that a 2% or even a 3% move in a currency will happen tomorrow.

Even with an ultra conservative 3% margin requirement, a house would only be protected by a move in the underlying of 33%. Any move greater than that, the customer account is completely wiped out, leaving the broker on the hook for the balance of the loss if they can?t get clients to pony up more money.

Of course, US based brokers can always sue their former clients and get their money back that way. But that is a three-year process. Just ask anyone who went through the whole MF Global disaster.

As a former broker myself, I can tell you that clients wiped out by margin calls have a bad habit of disappearing, changing their names and moving to unpronounceable countries to bury the paper trail, or move beyond the reach of extradition treaties. So good luck with that one.

After speaking to several foreign exchange traders, it seems that the first tick after the SNB?s announcement was up a staggering 40% from the last print. The world had stop loss orders to sell Euros as market, and this was the fill they got.

It gets worse. Some brokers, particularly small, undercapitalized foreign ones, were only demanding 0.5% margin or less. These guys are toast, but it may take weeks to find out exactly who.

The news services this morning are ablaze with such losses. Citibank (C) has admitted to a $150 million hickey. Very conservative Interactive Brokers has fessed up to a $120 million hit. FXCM is thought to be out $225 million. All of a sudden, foreign exchange brokers everywhere are for sale at fire sale prices.

These aren?t just some interesting, entertaining and colorful market anecdotes that I?m providing you. The debacle is so severe that it has cast a black cloud over all asset classes.

You see this in the sharply diminished trading volumes in all instruments, from stocks, to options, to futures contracts and exchange traded funds.

If you have just heard of a colleague or a counterparty who has just gone under, trading any of the recent straight line one way moves, guess what? You don?t go out and bet the ranch.

Your risk appetite has been diminished for weeks, if not months. In fact, you may not want to trade at all. This is not good for markets of any description.

I have been through many of these. The best thing to do is to shrink your book, hedge up what?s left, and put your more aggressive tendencies on hold. You may have noticed that the model portfolio for my Trade Alert service has just done exactly that.

Come back only when it?s safe to play, and the markets gets easy again.

Watch Out, They Can Bite

https://www.madhedgefundtrader.com/wp-content/uploads/2014/03/John-Thoms-Black-Swans-e1413901799656.jpg337400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-20 01:06:132015-01-20 01:06:13The Year of the Black Swan

It was one of those moves that appeared so gigantic and so unreal that you had to blink, while checking the cables on the back of your computer and your broadband connection.

The Swiss franc has just skyrocketed by 17% against the dollar in one tick.

First the bad news: the rent on my summer chalet in Zermatt, Switzerland had just risen by 17%.

And the good news? Holders of the ProShares Ultra Short Euro ETF (EUO), which I have been pounding the table on for the past seven months, just instantly appreciated by nearly 10%.

In a market that rarely sees moves of more than 1% a day, 17% is positively earth shaking, if not unbelievable.

A quick scan of my Bloomberg revealed that the Swiss National Bank had eliminated its cap against the Euro. Until now, the central bank had been buying Euros and selling Swiss francs to keep its own currency from appreciating.

This was to subsidize domestic exports of machinery, watches, cheese, and chocolate with an artificially undervalued currency.

The SNB?s move essentially converts the country to a free float with its currency, hence the sudden revaluation. Switzerland has thus run up the white flag in the currency wars, the inevitable outcome for small countries in this game.

One wonders why the Swiss made the move. Their emergency action immediately knocked 10% off the value of the Swiss stock market (which is 40% banks), and 20% off some single names.

I was kind of pissed when I heard the news. Usually I get a heads up from someone in a remote mountain phone booth when something is up in Switzerland. Not this time. There wasn?t even any indication that they were thinking of such a desperate act. Even IMF Director, Christine Lagarde, confessed a total absence of advance notice.

Apparently, the Swiss knew that eliminating the cap would have such an enormous market impact that they could not risk any leaks whatsoever.

This removes the world?s largest buyer of Euro?s (FXE) from the market, so the beleaguered currency immediately went into free fall. The last time I checked, the (FXE) had hit a 12 year low at $114, and the (EUO) was pawing at an all time high.

My prediction of parity for the Euro against the greenback, made only a few weeks ago in my 2015 Annual Asset Review (click here) were greeted as the ravings of a Mad man. Now it looks entirely doable, sooner than later.

The Germans have to be thinking ?There but for the grace of God go I?. If the European Community?s largest member exited the Euro, which has been widely speculated, the new Deutschmark would instantly get hit with a 20% appreciation, then another, and another.

Your low end, entry level Mercedes would see its price jump from $40,000 to $80,000. Kiss the German economy goodbye. Political extremism to follow.

There was another big beneficiary of the Swiss action today. Gold (GLD) had its best day in years, at one point popping a gob smacking $40. After losing its way for years, the flight to safety bid finally found the barbarous relic.

It seems there is nowhere else to hide.

By the way, the rent on my Swiss chalet may not be going up that much. My landlord has already emailed me that whatever increase I suffer in the currency will be offset by a decline in the cost in local currency terms.

It seems that the almost complete disappearance of Russians from the European tourism market during the coming summer, thanks to the oil induced collapse of their economy, is emerging as a major drag on Alpine luxury rentals.

That?s the way it is in the currency world. What you make in one pocket, gets picked out of the other.

That Bratwurst is Suddenly More Expensive

https://www.madhedgefundtrader.com/wp-content/uploads/2015/01/John-Thomas-Switzerland.jpg391291Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-16 01:04:172015-01-16 01:04:17Swiss Surprise Rattles Markets

Mad Day Trader Jim Parker is expecting the first quarter of 2015 to offer plenty of volatility and loads of great trading opportunities. He thinks the scariest moves may already be behind us.

After a ferocious week of decidedly ?RISK OFF? markets, the sweet spots going forward will be of the ?RISK ON? variety. Sector leadership could change daily, with a brutal rotation, depending on whether the price of oil is up, down, or sideways.

The market is paying the price of having pulled forward too much performance from 2015 back into the final month of 2014, when we all watched the December melt up slack jawed.

Jim is a 40-year veteran of the financial markets and has long made a living as an independent trader in the pits at the Chicago Mercantile Exchange. He worked his way up from a junior floor runner to advisor to some of the world?s largest hedge funds. We are lucky to have him on our team and gain access to his experience, knowledge and expertise.

Jim uses a dozen proprietary short-term technical and momentum indicators to generate buy and sell signals. Below are his specific views for the new quarter according to each asset class.

Stocks

The S&P 500 (SPY) and NASDAQ have met all of Jim?s short-term downside targets, and a sustainable move up from here is in the cards. But if NASDAQ breaks 4,100 to the downside, all bets are off.

His favorite sector is health care (XLV), which seems immune to all troubles, and may have already seen its low for the year. Jim is also enamored with technology stocks (XLK).

The coming year will be a great one for single stock pickers. Priceline (PCLN) is a great short, dragged down by the weak Euro, where they get much of their business. Ford Motors (F) probably bottomed yesterday, and is a good offsetting long.

Bonds

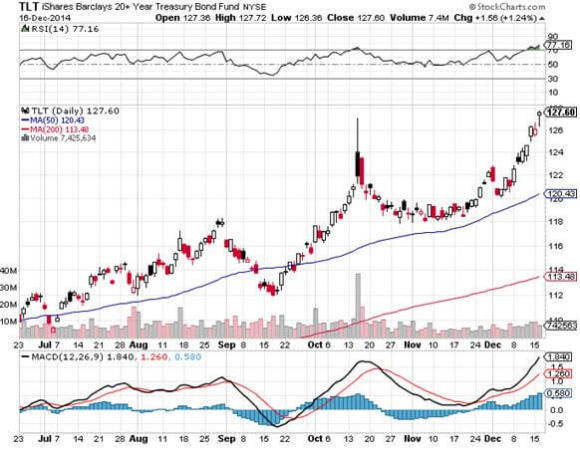

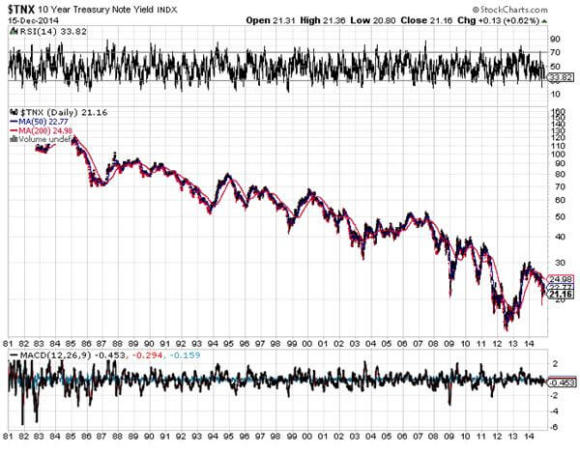

Jim is not inclined to stand in front of a moving train, so he likes the Treasury bond market (TLT), (TBT). He thinks the 30-year yield could reach an eye popping 2.25%. A break there is worth another 10 basis points. Bonds are getting a strong push from a flight to safety, huge US capital inflows, and an endlessly strong dollar.

Foreign Currencies

A short position in the Euro (FXE), (EUO) is the no brainer here. The problem is one of good new entry points. Real traders always have trouble selling into a free fall. But you might see profit taking as we approach $1.16 in the cash market.

The Aussie (FXA) is being dragged down by the commodity collapse and an indifferent government. The British pound (FXB) is has yet to recover from the erosion of confidence ignited by the Scotland independence vote and has further mud splattered upon it by the weak Euro.

Precious Metals

GOLD (GLD) could be in a good range pivoting off of the recent $1,140 bottom. The gold miners (GDX) present the best opportunity at catching some volatility. The barbarous relic is pulling up the price of silver (SLV) as well. Buy the hard breaks, and then take quick profits. In a deflationary world, there is no long-term trade here. It is a real field of broken dreams.

Energy

Jim is not willing to catch a falling knife in the oil space (USO). He has too few fingers as it is. It has become too difficult to trade, as the algorithms are now in charge, and a lot of gap moves take place in the overnight markets. Don?t bother with fundamentals as they are irrelevant. No one really knows where the bottom in oil is.

Agriculturals

Jim is friendly to the ags (CORN), (SOYB), (DBA), but only on sudden pullbacks. However, there are no new immediate signals here. So he is just going to wait. The next directional guidance will come with the big USDA report at the end of January. The ags are further clouded by a murky international picture, with the collapse of the Russian ruble allowing the rogue nation to undercut prices on the international market.

Volatility

Volatility (VIX), (VXX) is probably going to peak out her soon in the $23-$25 range. The next week or so will tell for sure. A lot hangs on Friday?s December nonfarm payroll report. Every trader out there remembers that the last three visits to this level were all great shorts. However, the next bottom will be higher, probably around the $16 handle.

If you are not already getting Jim?s dynamite Mad Day Trader service, please get yourself the unfair advantage you deserve. Just email Nancy in customer support at support@madhedgefundtrader.com and ask for the $1,500 a year upgrade to your existing Global Trading Dispatch service.

Volatility Weekly

Volatility Monthly

Euro to the Dollar

https://www.madhedgefundtrader.com/wp-content/uploads/2015/01/Volatility-Weekly.jpg325579Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-08 09:44:082015-01-08 09:44:08Mad Day Trader Jim Parker?s Q1, 2015 Views

After the market closes every night, I usually don a 60 pound backpack and climb the 2,000 foot mountain in my back yard.

To pass the time, I listen to audio books on financial and historical topics, about 200 a year (I?ve really got President Grover Cleveland nailed!). That?s if the howling packs of coyotes don?t bother me too much.

I also engage in mental calisthenics, engaging in complex mathematical calculations. How many grains of sand would you have to pile up to reach from the earth to the moon? How many matchsticks to circle the earth?

For last night?s exercise, I decided to quantify the impact of this year?s oil price crash on the global economy.

The world is currently consuming about 92 million barrels a day of Texas tea, or 33.6 billion barrels a year. In May, at the $107.50 high, that much oil cost $3.6 trillion. At today?s $53.60 low you could buy that quantity of oil for a bargain $1.8 trillion.

Buy a barrel of crude, and you get one for free!

This means that $1.8 trillion has suddenly been taken out of the pockets of oil producers, and put into the pockets of oil consumers. Over the medium term, this is fantastic news for oil consumers. But for the short term, things could get very scary.

$1.8 trillion is a lot of money. If you had that amount in hundred dollar bills, it would rise to 180 million inches, 15 million feet, or 2,840 miles, or 1.2% of the way to the moon (another mental exercise).

The global financial system cannot move this amount of money around on short notice without causing some pretty severe disruptions.

For a start, there is suddenly a lot less demand for dollars with which to buy oil. This has triggered short covering rallies in the long beleaguered Japanese Yen (FXY) and the Euro (FXE), which are just now backing off of long downtrends. The fundamentals for these currencies are still dire. But the short term trend now appears to be an upward one.

The US Federal Reserve certainly sees the oil crash as an enormously deflationary event. The use of energy is so widespread that it feeds into the cost of everything. That firmly takes the chance of any interest rate rise off the table for 2015. The Treasury bond market (TLT) has figured this out and launched on a monster rally.

Traders are also afraid that the disinflationary disease will spread, so they have been taking down the price of virtually all other hard commodities as well, like coal (KOL), iron ore (BHP), and copper (CU). For more depth on this, see yesterday?s piece on ?The End of the Commodity Super Cycle?.

The precipitous fall in energy investments everywhere will be felt principally in the 15 US states involved in energy production (Texas, Oklahoma, Louisiana, and North Dakota, etc.). So, the consumers in the other 35 states should be thrilled.

However, the plunge in energy stocks is getting so severe, that it is dragging down everything else with it. ALL shares are effectively oil shares right now. In fact, all asset classes are now moving tic for tic with the price of oil.

Throw on top of that the systemic risk presented by the ongoing collapse of the Russian economy. The Ruble has now fallen a staggering 70% in six months, and there is panic buying of everything going on in Moscow stores. The means that the dollar denominated debt owed by local firms has just risen by 70%. Any foreign banks holding this debt are now probably regretting ever watching the film, Dr. Zhivago.

Russian interest rates were just skyrocketed from 10.50% to 17%. The Russian stock market (RSX) is the world?s worst performing bourse this year. How do you spell ?depression? in the Cyrillic alphabet?

And guess what the new Russian currency is?

IPhone 6.0?s, of which Apple is now totally sold out in Alexander Putin?s domain!

Thankfully, this is more of a European than an American problem. But nobody likes systemic risks, especially going into illiquid yearend trading conditions. It?s a classic case of being careful what you wish for.

Of the $1.8 trillion today, about $430 billion is shifting between American pockets. That amounts to a hefty 2.5% of GDP.

Money spent on oil is burned. However, money spent by newly enriched consumers has a multiplier effect. Spend a dollar at Wal-Mart, and the company has to hire more workers, who then have more money to spend, and so on. So a shifting of funds of this magnitude will probably add 1% to U.S. economic growth next year.

Unfortunately, we will lose a piece of this from the obvious slowdown in housing. Deflation means that home prices will stagnate, or even fall. This is a major portion of the US economy which, for the most part, has been missing in action for most of this recovery.

Ultimately, cheap energy as far as the eye can see is a key element of my ?Golden Age? scenario for the 2020?s (click here for ?Get Ready for the Coming Golden Age? ).

But you may have to get there by riding a roller coaster first.

Oil at $53?

https://www.madhedgefundtrader.com/wp-content/uploads/2011/12/roller_coaster_monks-e1479779374563.jpg306300Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-17 09:42:222014-12-17 09:42:22Why All Shares Are Now Oil Shares

When the Trade Alerts quit working. I stop sending them out. That?s my trading strategy right now. It?s as simple as that.

So when I received a dozen emails this morning asking if it is time to double up on Linn Energy (LINE), I shot back ?Not yet!? There is no point until oil puts in a convincing bottom, and that may be 2015 business.

Traders have been watching in complete awe the rapid decent the price of Linn Energy, which is emerging as the most despised asset of 2014, after commodity producer Russia (RSX).

But it is becoming increasingly apparent that the collapse of prices for the many commodities is part of a much larger, longer-term macro trend.

(LINN) is doing the best impersonation of a company going chapter 11 I have ever seen, without actually going through with it. Only last Thursday, it paid out a dividend, which at today?s low, works out to a mind numbing 30% yield.

I tried calling the company, but they aren?t picking up, as they are inundated with inquires from investors. Search the Internet, and you find absolutely nothing. What you do find are the following reasons not to buy Linn Energy today:

1) Falling oil revenue is causing Venezuela to go bankrupt. 2) Large layoffs have started in the US oil industry. 3) The Houston real estate industry has gone zero bid. 4) Midwestern banks are either calling in oil patch loans, or not renewing them. 5) Hedge Funds have gone catatonic, their hands tied until new investor funds come in during the New Year. 6) Every oil storage facility in the world is now filled to the brim, including many of the largest tankers.

Let me tell you how insanely cheap (LINN) has gotten. In 2009, when the financial system was imploding and the global economy was thought to be entering a prolonged Great Depression, oil dropped to $30, and (LINN) to $7.50. Today, the US economy is booming, interest rates are scraping the bottom, employment is at an eight year high, and (LINE) hit $9.70, down $70 in six months.

Go figure.

My colleague, Mad Day Trader, Jim Parker, says this could all end on Thursday, when the front month oil futures contract expires. It could.

It isn?t just the oil that is hurting. So are the rest of the precious and semi precious metals (SLV), (PPLT), (PALL), base metals (CU), (BHP), oil (USO), and food (CORN), (WEAT), (SOYB), (DBA).

Many senior hedge fund managers are now implementing strategies assuming that the commodity super cycle, which ran like a horse with the bit between its teeth for ten years, is over, done, and kaput.

Former George Soros partner, hedge fund legend Paul Tudor Jones, has been leading the intellectual charge since last year for this concept. Many major funds have joined him.

Launching at the end of 2001, when gold, silver, copper, iron ore, and other base metals, hit bottom after a 21 year bear market, it is looking like the sector reached a multi decade peak in 2011.

Commodities have long been a leading source of profits for investors of every persuasion. During the 1970?s, when president Richard Nixon took the US off of the gold standard and inflation soared into double digits, commodities were everybody?s best friend. Then, Federal Reserve governor, Paul Volker, killed them off en masse by raising the federal funds rate up to a nosebleed 18.5%.

Commodities died a long slow and painful death. I joined Morgan Stanley about that time with the mandate to build an international equities business from scratch. In those days, the most commonly traded foreign securities were gold stocks. For years, I watched long-suffering clients buy every dip until they no longer ceased to exist.

The managing director responsible for covering the copper industry was steadily moved to ever smaller offices, first near the elevators, then the men?s room, and finally out of the building completely. He retired early when the industry consolidated into just two companies, and there was no one left to cover. It was heartbreaking to watch. Warning: we could be in for a repeat.

After two decades of downsizing, rationalization, and bankruptcies, the supply of most commodities shrank to a shadow of its former self by 2000. Then, China suddenly showed up as a voracious consumer of everything. It was off to the races, and hedge fund managers were sent scurrying to look up long forgotten ticker symbols and futures contracts.

By then commodities promoters, especially the gold bugs, had become a pretty scruffy lot. They would show up at conferences with dirt under their fingernails, wearing threadbare shirts and suits that looked like they came from the Salvation Army. As prices steadily rose, the Brioni suits started making appearances, followed by Turnbull & Asser shirts and Gucci loafers.

There was a crucial aspect of the bull case for commodities that made it particularly compelling. While you can simply create more stocks and bonds by running a printing press, or these days, creating digital entries on excel spreadsheets, that is definitely not the case with commodities. To discover deposits, raise the capital, get permits and licenses, pay the bribes, build the infrastructure, and dig the mines and pits for most commodities, takes 5-15 years.

So while demand may soar, supply comes on at a snail pace. Because these markets were so illiquid, a 1% rise in demand would easily crease price hikes of 50%, 100%, and more. That is exactly what happened. Gold soared from $250 to $1,922. This is what a hedge fund manager will tell us is the perfect asymmetric trade. Silver rocketed from $2 to $50. Copper leapt from 80 cents a pound to $4.50. Everyone instantly became commodities experts. An underweight position in the sector left most managers in the dust.

Some 14 years later and now what are we seeing? Many of the gigantic projects that started showing up on drawing boards in 2001 are coming on stream. In the meantime, slowing economic growth in China means their appetite has become less than endless.

Supply and demand fell out of balance. The infinitesimal change in demand that delivered red-hot price gains in the 2000?s is now producing equally impressive price declines. And therein lies the problem. Click here for my piece on the mothballing of brand new Australian iron ore projects, ?BHP Cuts Bode Ill for the Global Economy?.

But this time it may be different. In my discussions with the senior Chinese leadership over the years, there has been one recurring theme. They would love to have America?s service economy.

I always tell them that they have a real beef with their ancient ancestors. When they migrated out of Africa 50,000 years ago, they stopped moving the people exactly where the natural resources aren?t. If they had only continued a little farther across the Bering Straights to North America, they would be drowning in resources, as we are in the US.

By upgrading their economy from a manufacturing, to a services based economy, the Chinese will substantially change the makeup of their GDP growth. Added value will come in the form of intellectual capital, which creates patents, trademarks, copyrights, and brands. The raw material is brainpower, which China already has plenty of.

There will no longer be any need to import massive amounts of commodities from abroad. If I am right, this would explain why prices for many commodities have fallen further that a Middle Kingdom economy growing at a 7.5% annual rate would suggest. This is the heart of the argument that the commodities super cycle is over.

If so, the implications for global assets prices are huge. It is great news for equities, especially for big commod

ity importing countries like the US, Japan, and Europe. This may be why we are seeing such straight line, one way moves up in global equity markets this year.

It is very bad news for commodity exporting countries, like Australia, South America, and the Middle East. This is why a large short position in the Australian dollar is a core position in Tudor-Jones? portfolio. Take a look at the chart for Aussie against the US dollar (FXA) since 2013, and it looks like it has come down with a severe case of Montezuma?s revenge.

The Aussie could hit 80 cents, and eventually 75 cents to the greenback before the crying ends. Australians better pay for their foreign vacations fast before prices go through the roof. It also explains why the route has carried on across such a broad, seemingly unconnected range of commodities.

In the end, my friend at Morgan Stanley had the last laugh.

When the commodity super cycle began, there was almost no one around still working who knew the industry as he did. He was hired by a big hedge fund and earned a $25 million performance bonus in the first year out. And he ended up with the biggest damn office in the whole company, a corner one with a spectacular view of midtown Manhattan.

He is now retired for good, working on his short game at Pebble Beach.

Good for you, John.

Not as Shiny as it Once Was

https://www.madhedgefundtrader.com/wp-content/uploads/2014/12/Gold-Coins.jpg391380Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-16 01:03:502014-12-16 01:03:50End of the Commodity Super Cycle

The continuing collapse in oil prices has finally spilled over into the real world, at its worst knocking 290 points off of the Dow Average yesterday.

Traders who grew accustomed to a market that went up like clockwork every day were in for a rude awakening. Is the positive case for equities coming to an end?

Is the bull dead?

Not yet. All we are seeing is a normal 5%-7% correction in a long-term uptrend. It?s really all about the numbers, as it always is.

American companies are still on tract to increase earnings by 10% in 2015, and S&P 500 earnings are set to reach $130. Technology and innovation are hyper accelerating. Our energy costs have been cut in half, creating a giant tax cut. The world still wants to send its money here.

Goldilocks is still alive and well, just momentarily hiding under the bed.

Yes, it?s another buying opportunity.

This time, however, it?s different.

Oil has gone down so fast, some $46, or 43% in a scant six months that it has set the cat among the pigeons within the producing countries. The decline has been so precipitous that the budgets of oil producing countries from Saudi Arabia, to Russia, to Norway, have taken a real walloping. What else would you expect when your principal revenue source suddenly halves?

The plunge caught the producers totally by surprise. So to meet budget shortfalls, they are having to raise cash from their sovereign wealth funds. Some 15 of the world?s 20 largest sovereign wealth funds are run by oil producing countries.

To raise money, they are having to sell off investments, primarily stocks, and especially energy stocks. That is one of the few industries they actually understand.

This all means that the selling should dry up going into yearend, once budgetary requirements are met. If the price of oil stabilizes here at $61, or heaven forbid, starts to rise, then their selling of stocks completely ceases.

The bull market returns.

After suffering through a Trade Alert drought that has lasted more than a month, there are finally some nice trades setting up. I?m thinking specifically about the S&P 500 (SPY), energy (OXY), (XOM) and Solar stocks (SCTY), (FSLR), (VSLR), and even a chance to get back into the front-runners, technology (XLK) and biotech (BBH). Europe is also finally starting to look enticing.

Watch this space.

Goldilocks is Still Alive and Well

https://www.madhedgefundtrader.com/wp-content/uploads/2014/12/Goldilocks.jpg340151Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-11 09:39:482014-12-11 09:39:48Oil Grinch KO?s Christmas Rally

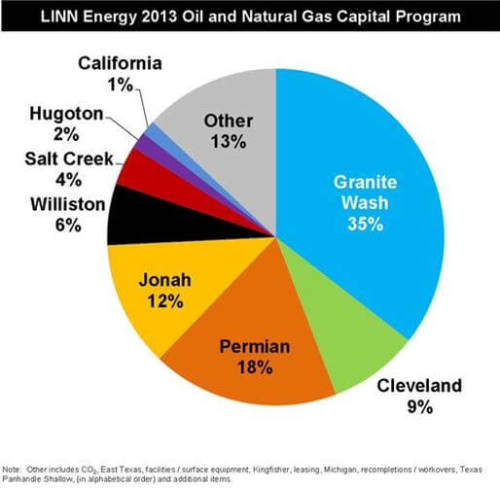

After the catastrophic 25% fall in the units of Linn Energy (LINE) over the past three days, I thought I?d better take another look at the company. The company?s units have now crashed by an eye popping 55% since the May $31 high.

The units have been trading as if the company is imminently going bankrupt. The contradiction is that it clearly isn?t. This is basically a healthy company that is undergoing some volatility typical for the sector.

Is this logical or rational?

No, not at all. But when a real panic hits, you sell first, and ask questions later. That has clearly been happening in the oil patch for the past month.

At the $14 low on Monday, the units were yielding a spectacular 20.7% annualized. This is not some imaginary pie in the sky estimate. This is what the actual $0.24 monthly cash payout announced by the company as recently as December 1 works out to for holders of record as of Thursday, December 11.

Nor are these spectacular yields based on some wild leveraged bets in the financial markets. (LINE) is predominantly a natural gas company, a commodity which has seen its price go largely unchanged for the past two years, hovering above $3.50. And much of its production has already been hedged against any downside risk with offsetting positions in the futures market.

I always try to use every loss as a learning opportunity, or the lesson goes wasted, and is doomed to repetition.

The reasons above were why I shot out a quick Trade Alert last week to buy (LINN) at $16.67. It was an uncharacteristically cautious position for me. But calling bottoms in major trends is always a risky enterprise, so I went small, very small. I bought the underlying units, not the options, and then in unleveraged form.

Initially things went great, rocketing 13% right out the door. Short term, smart traders, like Mad Day Trader Jim Parker, then put in tight stop losses below. That way, he was playing with the house?s money in any further upside, and is assured against loss during any rapid reversal.

I, unfortunately was too slow to do so, and had to bear the cost of the sudden 25% drop. Remember, being right 80% of the time means that I am wrong 20% of the time. But with only a 10% position, my loss never exceeded 1.60% of my total portfolio, something I can live with, and ride out until any recovery.

My guess is that many (LINE) holders violated my ?Sleep at night rule,? lured by the hefty dividend payout into owning too many units.

Once burned, twice forewarned.

My advice to you now is ?Hang on.? You?ve already taken the hit. Don?t bail here and miss the recovery, which will probably begin in earnest next year.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/12/LINN-Energy.jpg313361Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-10 01:05:142014-12-10 01:05:14Update on Linn Energy (LINE)

Finally, the economy is starting to deliver the blockbuster numbers that I have been predicting all year.

The 321,000 gain in the November nonfarm payroll on Friday wasn?t just good, they were fantastic, truly of boom time proportions. It was the best report in nearly three years. The headline unemployment rate stayed at 5.8%, a seven year low.

It vindicates my ultra bullish view for the US economy of a robust 4% GDP growth rate in 2015. It also makes my own out-of-consensus $2,100 yearend target for the S&P 500 a chip shot (everybody and his brother?s target now, but certainly out-of-consensus last January).

There has been a steady drip, drip of data warning that something big was headed our way for the last several months. November auto sales a 17 million annualized rate was a key piece of the puzzle, as consumers cashed in on cheap gas prices to buy low mileage, high profit margin SUV?s. The Chrysler Jeep Cherokee, a piece of crap car if there ever was one, saw sales rocket by a mind-boggling 60%!

It reaffirms my view that the 40% collapse in the price of energy since June is not worth the 10% improvement in stock indexes we have seen so far. It justifies at least a double, probably to be spread over the next three years.

It also looks like Santa Claus will be working overtime this Christmas. Retailers are reporting a vast improvement over last year?s weather compromised sales results. A standout figure in the payroll report was the 50,000 jobs added by the sector. This is much more than just a seasonal influence, as FedEx and UPS pile on new workers.

The market impact was predictable. Treasury bond yields (TLT) spiked 10 basis points, the biggest one-day gain in four years. My position in the short Treasury ETF (TBT) saw a nice pop. Unloved gold (GLD) got slaughtered, again, cratering $25.

Stocks (SPY) didn?t see any big moves, and simply failed to give up their recent humongous gains once again. A major exception was the financials (XLF), egged on by diving bond prices. My long in Bank of America (BAC) saw another new high for the year.

All in all, it was another good day for followers of the Mad Hedge Fund Trader.

To understand how overwhelmingly positive the report was, you have to dive into the weeds. Average hourly earnings were up the most in 17 months. The September payroll report was revised upward from 256,000 to 271,000, while October was boosted from 214,000 to 243,000.

Professional and business services led the pack, up a whopping 86,000. There are serious, non minimum wage jobs. Job gains have averaged an impressive 278,000 over the last three months.

The broader U-6 unemployment rate fell to 11.4%, down from 12.7% a year ago. Most importantly, wage growth is accelerating, and hours worked are at a new cyclical high.

In view of these impressive numbers, it is unlikely that we will see any substantial pullback in share prices for the rest of 2014. For that, we will have to wait until 2015.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/12/Rosie-the-Riverter.jpg353306Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-12-08 09:28:162014-12-08 09:28:16The November Nonfarm Payroll Report is a Game Changer

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.