There is no doubt that old tech is back with a vengeance.

Look at the trifecta of blockbuster earnings reports from Microsoft (MSFT), Amazon (AMZN), and Alphabet (GOOGL) recently, and you can reach no other conclusion.

The Microsoft turnaround in particular has been amazing.

PCs, and the software to run them were so 1990s.

After the Dotcom bust in 2000, Microsoft was dead money for years.

Founder Bill Gates retired in 2008. CEO Steve Ballmer finally got the message in 2013, and retired to pay through the nose, some $2 billion, for the basketball team, the LA Clippers.

Succeeding operating systems offered little that was new, and they fell woefully behind the technology curve.

Even I gave away my own machines years ago to switch to Apple devices. These virus immune machines are perfect for a small business like mine, as they seamlessly integrate and all talk to each other.

When the company brought out the Windows Phone in 2010, three years after Apple, people in Silicon Valley laughed.

Long given up for dead as a trading and investment vehicle, the shares have been on a tear in 2015.

The stock is hitting a new all time high FOR THE FIRST TIME IN 15 YEARS!

Satya Nadella, who took over management of the company in 2014, clearly had other ideas. The challenge for Nadella from day one was to move boldly into new technologies, while preserving its legacy Windows business lines.

So far, so good.

The key to the company?s new found success was it?s dumping of its old ?Wintel? strategy of yore that focused entirely on the growth of the PC market.

The problem was that the PC market stopped growing, as the world moved onto the Cloud and mobile.

The company is now rivaling Apple with $100 billion in cash, almost all held tax-free overseas.

EPS growth will reach 10% next year, beating other big competitors.

Windows and servers, the (MSFT)?s core products, still account for 80% of the firm?s business.

But its cloud presence is being ramped up at a frenetic pace, where the future for the company lies, nearly doubling YOY. Mobile technologies, where it has lagged until now, are also on fire.

Rave reviews from its latest operating system upgrade, Windows 10, also helped.

On top of all of this, Microsoft is paying a generous 3% dividend. It?s earnings multiple at 15X makes it a bargain compared to other big tech companies and the rest of the market.

As I explained in my recent research piece ?Switching From Growth to Value? (click here?), Microsoft makes a perfect investment for a mature bull market.

It is not only at a multiple discount to the rest of the market, now at 18X, it is cheap when compared to the rest of its own sector as well.

This is when investors and traders bail from their high priced stocks to safer, lower multiple companies.

Obviously, I don?t want to pile into Microsoft, or any other of the big tech stocks on top of a furious 10% spike. But it is now safely in the ?buy on the dip? camp, along with the rest of big tech.

The party has only just stated.

To read my interview with Bill Gates? father, click here for ?An Evening With Bill Gates, Sr.?.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/10/Microsoft-Logo-e1445631099676.jpg92400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-09-23 01:07:492016-09-23 01:07:49Old Tech is Back!

I first spoke to Steve Wozniak via HAM radio when I was 12 and he was the 14-year-old president of the Homestead High School Radio Club in Cupertino, California.

With seven children, my dad was pretty stingy with allowance money. But when it came to electronic parts, I had an unlimited budget, as that is where he saw the future.

So while other kids collected baseball cards, I stocked up on tubes, resistors, capacitors, and rheostats. This was back when you could buy WWII surplus parts from Radio Shack for pennies a pound.

Then the transistor came out, and building projects, like simple computers programmed with basic '1's' and '0's' suddenly became possible.

By junior high school, I had gained my radio license, learning Morse code at the required five words per minute, and a path opened that eventually led me to Woz.

Whenever I had a design problem, Woz always had a solution. He seemed to know everything about electronics.

I planned to attend De Anza College in the San Francisco Bay Area to collaborate with Woz, but then the State of California dropped a big fat scholarship to the University of Southern California in my lap, and we parted ways.

That?s government for you. The state thought I was smarter than Woz. Ha!

The last thing he taught me was this really cool way to make long distance phone calls for free with something called a 'blue box.'

I later heard that Woz went to work for some kind of fruit company designing computers, which sounded stupid to me at the time, but Woz was always a guy who marched to a different drummer.

A decade later, I was an ambitious young vice president at Morgan Stanley, and ran into Woz again while escorting Steve Jobs around to big institutional investors hawking an Apple (AAPL) secondary share offering.

By then he had gained a lot of weight. He fascinated me with stories about how he had gone from scrounging around for a bootleg $12 chip, to making $100 million on the Apple IPO in just three years.

The phrase ?only in America? has to come to mind.

We bought our planes at the same time, me a Cessna 340 twin, and he a Beechcraft Bonanza. When I heard he totaled his in a crash in Santa Cruz a few years later, I sent flowers to his hospital room, even though he was in a coma and wasn't expected to live.

In later years we moved into the same philanthropic circles at the San Francisco Ballet, the Computer Museum, and local art museums. To me, Woz always stood out at the social events as the only one who was not an inveterate social climber.

That was vintage Woz. He just didn't care.

When I finally stumbled across his autobiography, iWoz, I grabbed it and devoured the pages in a couple of days.

The tome filled in the holes about what I knew about the man: the wives, the rock concerts, his universal remote control idea, and the early days at Apple.

You also learn a lot about electronics and basic computer hardware and software design.

While there are a lot of 5th grade science teachers who wish they were billionaires, there is only one billionaire who aspired to teach 5th grade science. That is what Woz did for ten years.

Despite the billions, Steve is still an all right guy. To buy the book of his engaging and entertaining story from Amazon, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/02/Steve-Wozniak.jpg301382Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-08-02 01:06:322016-08-02 01:06:32Hanging Out With the Woz

Having been in this market for yonks, ages, and even a coon?s age, I have seen trading strategies come and go.

First, there was the nifty fifty during the 1960?s. Junk bonds had their day in the sun. Then portfolio insurance was all the rage.

Oops!

While the dollar was weak, international diversification was the flavor of the day. After foreign stocks turned bitter, the IPO mania and the Dotcom bubble of the nineties followed.

Macro trading dominated the new Millennium until the high frequency traders took over.

What is the cutting edge management strategy today?

According to my friend, Anthony Scaramucci, of Skybridge Capital, activist shareholder trading now has the unfair advantage.

Anthony, known as the ?Mooch? to his friends, is so convinced of the merit of this bold, in-your-face approach that he has devoted nearly 40% of his assets to this aggressive posture.

That is no accident.

Have you ever heard the term ?unintended consequences?? Scaramucci argues that The Financial Stability Act of 2010, otherwise known as Dodd-Frank produced that effect with a turbocharger.

The Act brought in a raft of new shareholder rights intended to help Mom & Pop. But activist investors have, so far, been the prime beneficiaries of the reform, using the new regulations to shake down companies for quick profits.

Historic low interest rates are allowing them to leverage up at minimal cost, increasing their firepower.

These include known sharks (once spurned as ?green mailers?) like my former neighbor, Carl Icahn, and his younger, more agile competitor, Bill Ackman.

They can simply buy a small number of shares in a target company and demand a management change, share buy backs, the spinning off of assets, several seats on the board, and even making allegations of criminal activity, which are often unfounded.

A message from Icahn on the voicemail is not something management is eager to hear.

He even shook down Apple (AAPL) last year, with great success, harvesting a near double on the trade.

This is why names like Herbalife (HLF), Netflix (NFLX), and JC Penny?s (JCP) are constantly bombarding the airwaves.

The net result of this is that savvy activist shareholders have effectively replaced the traditional ?buy and hold? strategy as a way to add alpha, or outperformance.

This has enabled activist oriented hedge funds to beat the pants off of traditional macro hedge funds because many historical cross asset relationships they follow have broken down.

Tell me about it!

Suddenly, the world no longer makes sense to them and has apparently gone mad, at the investors? expense. Long/short equity managers, which comprise 43% of the funds out there, are also underperforming for the sixth consecutive year.

The activist managers themselves justify their often harsh actions by arguing that individual shareholders can ride to riches on their coattails. Shaking up management can result in better-run companies, even if it is at the point of a gun.

Activism accelerates evolution, breaks up clubby boards of insiders, and enhances the bottom line. Corporations can be forced to retool and restructure.

How does the individual investor get involved in the new wave of activist investors? The short answer is that they don?t. There are few, if any, such exchange traded funds (ETFs) in existence.

Doing the quantitative screens to generate short lists of potential activist targets, and then listening to the jungle telegraph regarding who is coming into play, are well beyond the resources of your average Joe.

You can try to give your money to the best activist managers. But they are either closed to new investors, or have very high minimum initial investments, often in the $1-$10 million range.

If you are lucky enough to get your dosh in, you will find the talent very expensive. Activist funds are one of the last redoubts of the old 2%/20% management fee and performance bonus structure. And ?hockey stick? bonus schedules are not unheard of.

When I ran my old hedge fund, we made 40% a year like clockwork. I took the first 10%, the limited partners the remaining 30% and they were thrilled to get it.

And you wonder why the small guys feel the market is rigged.

The activist trend won?t last forever. Interest rates will inevitably rise, making the strategy expensive to finance. If the stock market keeps rising, as I expect, then cheap targets will become as scarce as hen?s teeth.

Eventually, gobs of money will pour into the strategy, compressing returns as the Johnny-come-latelys pile in. In the end, trading around activist shareholders will get tossed into the dustbin of history, along with all the other investment fads.

Checking in With the ?Mooch?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/09/John-Thomas-with-Anthony-Scaramucci.jpg294382Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-07-19 01:07:552016-07-19 01:07:55Why Activist Investors Have the Upper Hand

With the stock market falling for the next few weeks, or even months, it?s time to rehash how to profit from falling markets one more time.

There is nothing worse than closing the barn door after the horses have bolted.

No doubt, you will receive a wealth of short selling and hedging ideas from your other research sources and the media at the next market bottom. That is always how it seems to play out.

So I am going to get you out ahead of the curve, putting you through a refresher course on how to best trade falling markets now, while stock markets are still only 3% short of an all time high, and unchanged on the year.

Market?s could be down 10% by the time this is all over.

THAT IS MY LINE IN THE SAND!

There is nothing worse than fumbling around in the dark looking for the matches after a storm has knocked the power out.

I?m not saying that you should sell short the market right here. But there will come a time when you will need to do so. Watch my Trade Alerts for the best market timing. So here are the best ways to profit from declining stock prices, broken down by security type:

Bear ETFs

Of course the granddaddy of them all is the ProShares Short S&P 500 Fund (SH), a non leveraged bear ETF that is supposed to match the fall in the S&P 500 point for point on the downside. Hence, a 10% decline in the (SPY) is supposed to generate a 10% gain the in the (SH).

In actual practice, it doesn?t work out like that. The ETF has to pay management operating fees and expenses, which can be substantial. After all, nobody works for free.

There is also the ?cost of carry,? whereby owners have to pay the price for borrowing and selling short shares. They are also liable for paying the quarterly dividends for the shares they have borrowed, around 2% a year. And then you have to pay the commissions and spread for buying the ETF.

Still individuals can protect themselves from downside exposure in their core portfolios through buying the (SH) against it (click here for the prospectus: http://www.proshares.com/funds/sh.html). Short selling is not cheap. But it?s better than watching your gains of the last seven years go up in smoke.

My favorite is the (RWM) a short play on the Russell 2000, which falls 1.5X faster than the big cap indexes in bear markets (click here for the prospectus: http://www.proshares.com/funds/rwm.html).

Leveraged Bear ETFs

My favorite is the ProShares Ultra Short S&P 500 (SDS), a 2X leveraged ETF (click here for the? prospectus: http://www.proshares.com/funds/sds.html). A 10% decline in the (SPY) generates a 20% profit, maybe.

Keep in mind that by shorting double the market, you are liable for double the cost of shorting, which can total 5% a year or more. This shows up over time in the tracking error against the underlying index. Therefore, you should date, not marry, this ETF or you might be disappointed.

3X Leveraged Bear ETFs

The 3X bear ETFs, like the UltraPro Short S&P 500 (SPXU), are to be avoided like the plague (click here for the prospectus: http://www.proshares.com/funds/spxu.html).

First, you have to be pretty good to cover the 8% cost of carry embedded in this fund. They also reset the amount of index they are short at the end of each day, creating an enormous tracking error.

Eventually, they all go to zero, and have to be periodically redenominated to keep from doing so. Dealing spreads can be very wide, further added to costs.

Yes, I know the charts can be tempting. Leave these for the professional hedge fund intra day traders they are meant for.

Buying Put Options

For a small amount of capital, you can buy a ton of downside protection. For example, the April (SPY) $182 puts I bought for $4,872 allowed me to sell short $145,600 worth of large cap stocks at $182 (8 X 100 X $6.09).

Go for distant maturities out several months to minimize time decay and damp down daily price volatility. Your market timing better be good with these, because when the market goes against you, put options can go poof, and disappear pretty quickly.

That?s why you read this newsletter.

Selling Call Options

One of the lowest risk ways to coin it in a market heading south is to engage in ?buy writes?. This involves selling short call options against stock you already own, but may not want to sell for tax or other reasons.

If the market goes sideways, or falls, and the options expire worthless, then the average cost of your shares is effectively lowered. If the shares rise substantially they get called away, but at a higher price, so you make more money. Then you just buy them back on the next dip. It is a win-win-win.

I?ll give you a concrete example. Let?s say you own 100 shares of Apple (AAPL), which closed on Friday at $95.13, worth $9,513. If you sell short 1 July, 2016 $100 call at $1.30 against them, you take in $130 in premium income ($1.30 X 100 because one call option contract is exercisable into 100 shares).

If Apple close2 below $100 on the July 15, 2016 expiration date, the options expire worthless and you keep your stock and the premium. You are then free to repeat the strategy for the following month. If (AAPL) closes anywhere above $100 and your shares get called away, you still make money on the trade.

Selling Futures

This is what the pros do, as futures contracts trade on countless exchanges around the world for every conceivable stock index or commodity. It is easy to hedge out all of the risk for an entire portfolio of shares by simply selling short futures contracts for a stock index.

For example, let?s say you have a portfolio of predominantly large cap stocks worth $100,000. If you sell short 1 June, 2016 contract for the S&P 500 against it, you will eliminate most of the potential losses for your portfolio in a falling market.

The margin requirement for one contract is only $5,000. However if you are short the futures and the market rises, then you have a big problem, and the losses can prove ruinous.

But most individuals are not set up to trade futures. The educational, financial, and disclosure requirements are beyond mom and pop investing for their retirement fund.

Most 401ks and IRAs don?t permit the inclusion of futures contracts. Only 25% of the readers of this letter trade the futures market. Regulators do whatever they can to keep the uninitiated and untrained away from this instrument.

That said, get the futures markets right, and it is the quickest way to make a fortune, if your market direc

tion is correct.

Buying Volatility

Volatility (VIX) is a mathematical construct derived from how much the S&P 500 moves over the next 30 days. You can gain exposure to it through buying the iPath S&P 500 VIX Short Term Futures ETN (VXX), or buying call and put options on the (VIX) itself.

If markets fall, volatility rises, and if markets rise, then volatility falls. You can therefore protect a stock portfolio from losses through buying the (VIX).

I have written endlessly about the (VIX) and its implications over the years. For my latest in-depth piece with all the bells and whistles, please read ?Buy Flood Insurance With the (VXX)? by clicking here.

Selling Short IPO?s

Another way to make money in a down market is to sell short recent initial public offerings. These tend to go down much faster than the main market. That?s because many are held by hot hands, known as ?flippers,? and don?t have a broad institutional shareholder base.

Many of the recent ones don?t make money and are based on an, as yet, unproven business model. These are the ones that take the biggest hits.

This is another mathematical creation based on the number of rising days over falling days. Rising markets bring increasing momentum, while falling markets produce falling momentum.

So selling short momentum produces additional protection during the early stages of a bear market. Blackrock has issued a tailor made ETF to capture just this kind of move through its iShares MSCI Momentum Factor ETF (MTUM). To learn more, please read the prospectus by clicking here: https://www.ishares.com/us/products/251614/MTUM.

Buying Beta

Beta, or the magnitude of share price movements, also declines in down markets. So selling short beta provides yet another form of indirect insurance. The PowerShares S&P 500 High Beta Portfolio ETF (SPHB) is another niche product that captures this relationship.

The Index is compiled, maintained and calculated by Standard & Poor's and consists of the 100 stocks from the (SPX) with the highest sensitivity to market movements, or beta, over the past 12 months.

Another subsector that does well in plunging markets are publicly listed bearish hedge funds. There are a couple of these that are publicly listed and have already started to move.

One is the Advisor Shares Active Bear ETF (HDGE) (click here for the prospectus: http://www.advisorshares.com/fund/hdge). Keep in mind that this is an actively managed fund, not an index or mathematical relationship, so the volatility could be large.

Oops, Forgot to Hedge

https://www.madhedgefundtrader.com/wp-content/uploads/2014/04/Wile-E.-Coyote-TNT.jpg365496Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-05-23 01:06:362016-05-23 01:06:36Short Selling School 101

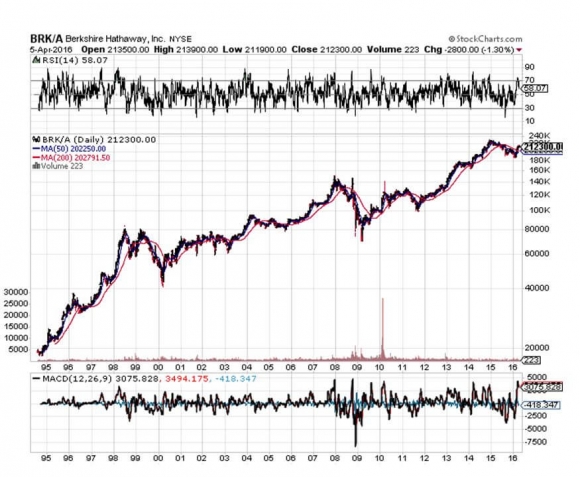

Sometime in the early 1970?s, a friend of mine said I should take a look at a stock named Berkshire Hathaway (BRKA) run by a young stud named Warren Buffett.

I thought, ?Why the hell should I invest in a company that makes sheets??

After all, the American textile industry was in the middle of a long trek toward extinction that began in the 1920?s, and was only briefly interrupted by the hyper prosperity of WWII. The industry?s travails were simply an outcome of ever rising US standards of living, which pushed wages, and therefore costs, up.

It turns out that Warren Buffett made a lot more than sheets. However, he is not a young stud anymore, just an old one, like me.

Since then, Warren?s annual letter to investors has been an absolute ?must read? for me when it is published every spring.

It has been edited for the past half century by my friend, Carol Loomis, who just retired after a 60-year career with Fortune magazine. (I never wrote for them because their freelance rates were lousy).

Witty, insightful, and downright funny, I view it as a cross between a Harvard Business School seminar and a Berkeley anti establishment demonstration. You will find me lifting from it my ?Quotes of the Day? for the daily newsletter over the next several issues. There are some real zingers.

And what a year it has been!

Berkshire?s gain in net worth was $18.3 billion, which increased the share value by 8.3%, and today, the market capitalization stands at an impressive $343.4 billion. (Sorry Warren, but I clocked 30% last year, eat your heart out).

The shares are not for small timers, as one now costs $214,801, and no, they don?t sell half shares. This compares to a 1965 per share market value of $23.80, and is why the media are always going gaga over Warren Buffett.

If you?re lazy and don?t want to do the math, that works out to a compound annualized return of an eye popping 21.6%. This is why guessing what Warren is going to do next has become a major cottage industry (Progressive Insurance anyone?).

Warren brought in these numbers despite the fact that its largest non-insurance subsidiary, the old Burlington Northern Santa Fe Railroad (BNSF) suffered an awful year.

Extensive upgrades under construction and terrible winter weather disrupted service, causing the railroad to lose market share to rival Union Pacific (UNP).

I was kind of pissed when Warren bought BNSF in 2009 for a blockbuster $44 billion, as it was long my favorite trading vehicles for the sector. Since then, its book value has doubled. Typical Warren.

Buffett plans to fix the railroad?s current problems with $6 billion in new capital investment this year, one of the largest single capital investments in American history. Warren isn?t doing anything small these days.

Buffett also got a hickey from his investment in UK supermarket chain Tesco, which ran up a $444 million loss for Berkshire in 2014. Warren admits he was too slow in getting out of the shares, a rare move for the Oracle of Omaha, who rarely sells anything (which avoids capital gains taxes).

Warren increased his investment in all of his ?Big Four? holdings, American Express (AXP), Coca-Cola (KO), IBM (IBM), and Wells Fargo (WFC).

In addition, Berkshire owns options on Bank of America (BAC) stock, which have a current exercise value of $12.5 billion (purchased the day after the Mad Hedge Fund Trader issued a Trade Alert on said stock for an instant 300% gain on the options).

The secret to understanding Buffett picks over the years is that cash flow is king.

This means that he has never participated in the many technology booms over the decades, or fads of any other description, for that matter.

He says this is because he will never buy a business he doesn?t intrinsically understand, and they didn?t offer computer programming as an elective in high school during the Great Depression.

No doubt this has lowered his potential returns, but with the benefit of much lower volatility.

That makes his position in (IBM) a bit of a mystery, the worst performing Dow stock of the past two years. I would much rather own Apple (AAPL) myself, which also boasts great cash flow, and even a dividend these days (with a 1.50% yield).

Warren will be the first to admit that even he makes mistakes, sometimes, disastrous ones. He cites his worst one ever as a perfect example, his purchase of Dexter Shoes for $433 million in 1993. This was right before China entered the shoe business as a major competitor.

Not only did the company quickly go under, he exponentially compounded the error through buying the firm with an exchange of Berkshire Hathaway stock, which is now worth a staggering $5.7 billion.

Ouch, and ouch again!

Warren has also been mostly missing in action on the international front, believing that the mother load of investment opportunities runs through the US, and that its best days lie ahead. I believe the same.

Still, he has dipped his toe in foreign waters from time to time, and I was sometimes quick to jump on his coattails. A favorite of mine was his purchase of 10% of Chinese electric car factory BYD (BYDDF) in 2009, where I have captured a few doubles over the years.

Buffett expounds at great length the attractions of the insurance industry, which today remains the core of his business. For payment of a premium up front, the buyers of insurance policies receive a mere promise to perform in the future, sometimes as much as a half century off.

In the meantime, Warren can invest the money any way he wants. The model has been a real printing press for Buffett since he took over his first insurer in 1951, GEICO.

Much of the letter promotes the upcoming shareholders annual meeting, known as the ?Woodstock of Capitalism?.

There, the conglomerate?s many products will be for sale, including, Justin Boots (I have a pair), the gecko from GEICO (which insures my Tesla S-1), and See?s Candies (a Christmas addiction, love the peanut brittle!).

There, visitors can try their hand at Ping-Pong against Ariel Hsing, a 2012 American Olympic Team member, after Bill Gates and Buffett wear her down first.

They can try their hand against a national bridge champion (don?t play for money). And then there is the newspaper-throwing contest (Buffett?s first gainful employment).

Some 40,000 descend on remote Omaha for the firm?s annual event. All flights to the city are booked well in advance, with fares up to triple normal rates.

Hotels sell out too, and many now charge three-day minimums (after Warren, what is there to do in Omaha for two more days other than to visit PayPal?s technical support?). Buffett recommends Airbnb as a low budget option (for the single shareholders?).

I was amazed to learn that Berkshire files a wrist breaking 24,100-page Federal tax return (and I thought mine was bad!). Add to this a mind numbing 3,400 separate state tax returns.

Overall, Berkshire holdings account for more than 3% of the total US gross domestic product, but a far lesser share of the government?s total tax revenues, thanks to careful planning.

Buffett ends his letter by advertising for new acquisitions and listing his criteria. They include:

(1) ?Large purchases (at least $75 million of pre-tax earnings unless the business will fit into one of our existing units),

(2) ?Demonstrated consistent earning power (future projections are of no interest to us, nor are ?turnaround? situations),

(3) ?Businesses earning good returns on equity while employing little or no debt,

(4) Managemen

t in place (we can?t supply it),

(5) Simple businesses (if there?s lots of technology, we won?t understand it),

(6) An offering price (we don?t want to waste our time or that of the seller by talking, even preliminarily, about a transaction when price is unknown).

https://www.madhedgefundtrader.com/wp-content/uploads/2015/04/Warren-Buffett-e1429740484967.jpg249400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-04-19 01:06:052016-04-19 01:06:05A Chat With Berkshire Hathaway?s Warren Buffett

Of the 200 million Americans who possess financial assets, probably all of them own Apple (AAPL), either directly through a trading account, or indirectly though an ETF (it is a massive 11.67% of the PowerShares QQQ), public or private pension fund.

So to say that traders are on pins and needles ahead of the upcoming quarterly earnings report would be an understatement.

A year ago, Apple issued one of the most perfect reports in the history of capitalism.

It blew away even the most optimistic forecasts, announcing earnings per share of $2.33, versus a consensus expectation of $2.16, and $1.75 last quarter.

The firm earned $13.6 billion in profits on $58 billion in gross profits, the largest quarterly profit in world history.

The company sold a staggering 61.2 million iPhones during the three-month period, 4 million more than expected. Insignificant iPad sales dropped from 13.9 to 12.6 million units. MacBooks were in line at 4.6 million units.

No mention was made whatsoever of problems with a strong dollar.? The company now sits on an unbelievable $194 billion in cash, the equivalent of the GDP of a medium sized country.

Most importantly, Apple expanded its share buy back program to $200 billion. The big question now is, will Apple buy another company, or a whole country?

Wow!

Since then the stock has been grinding sideways in the most tedious manner imaginable. It was a classic ?Buy the rumor, sell the news? set up.

Which leads many shareholders to ask if, now that the stock is owned by every taxi driver, elevator operator , and shoe shine boy in the country (now I?m showing my age!), are we headed for another 45% selloff, much like the last time the stock peaked out in 2012?

Certainly, the grounds for concern are out there.

There are now no new blockbuster products coming out until we see the iPhone 7 in September 2016.

There are supply chain worries, as the global manufacturing network is now absolutely mammoth.

Some analysts are nervous about quality control, especially regarding new products like the Apple watch, which should sell an eye popping 30 million units this year.

However, I think this time it?s different.

While you weren?t looking, Apple has turned into a China play. No, they aren?t suddenly eating dim sum with chopsticks at corporate headquarters in Cupertino.

The Middle Kingdom, in short order, has become the firm?s largest grower of its earnings. This is a good thing. Last year saw an 80% growth of sales there. China is expected to become the largest market for Apple products this year.

What?s more, the ballistic growth there is expected to continue. Walk down the street in Shanghai these days, and you are amazed by how many people are speaking or texting into their iPhones, real and fake ones alike.

In fact, they have become the primary means through which people access the Internet there.

No doubt, this is due to Apple?s special relationship there with China Mobile (CHL), which now offers iPhone owners a great deal for their cell phone service. Did I mention that (CHL) has a staggering 750 million customers?

The iWatch is now viewed as the gateway for the sales of as many as 1.2 million future third party developed apps, the number iTunes offers now.

Apple Pay looks to replace Visa and Master Card at some point in the future. Apple TV is still lurking out there in the background.

We?ll learn more about all of this at the next developers conference in San Francisco in June.

All of this leads me to believe that there is far more fundamental support in terms of new products and business lines for the company than we saw during the last cycle.

There is also more distance in the rear view mirror since the passing of Steve Jobs. Successor Tim Cook has since proved himself as a world-class leader.

It turned out the timing for the company to transition from a founder-tyrant to a cutting edge administrator-manager was perfect. You don?t need to hold your breath anymore.

At least the stock market thinks so.

Therefore, I expect to see a $1 trillion market capitalization for Apple sometime in 2018, well up from today?s $602 billion. I think that means you need to use the current dip to load up on the stock.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/05/Apple-Logo.jpg305234Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-04-11 01:06:352016-04-11 01:06:35What To Do About Apple

Apple holders (AAPL) were ecstatic and even apoplectic when they heard that their beloved company would be joining the Dow Average last year.

The move required thousands of portfolio managers to add Apple to their portfolios, like the $32 billion worth of Dow index managers, whether they wanted to or not. From then on it would be illegal for them not to own Apple.

At the very least it put the fear of Jobs into moneymen everywhere, especially if the Dow is the benchmark they are measured against.

The world?s now second largest listed company replaced tired and flagging AT&T (T), one of my perennial favorite short positions.

The symbolism couldn?t be more evident. A former monopoly with a literally rusting infrastructure is getting booted for iPhones, iPads, iTunes, Apps and the Cloud. Oh, how the mighty have fallen.

AT&T was one of the oldest Dow stocks, joining the closely followed index in 1916. The new listing then had a symbolic move of its own, taking place the year after the first-ever transcontinental telephone call was placed.

Who made that call? Alexander Graham Bell in New York telephoned his former assistant, Thomas Watson, in San Francisco in a replay of the first phone call in history 50 years earlier in 1876, from room to room at their lab. ?Mr. Watson, come here, I want to see you,? the first words ever uttered on a phone line, were repeated once more.

AT&T, or ?Ma Bell? as it was known, lost its listing in 2004 after it merged with SBC Communications. It was reinstated a year later when the new firm?s name was changed back to AT&T.

However, Apple shareholders should be careful what they wish for.

There is not exactly a great track record for share price performance after a company joins the Dow, especially a technology stock.

In 1999, Microsoft (MSFT) fell 43% after becoming a Dow 30 stock, while Intel (INTC) shed 52%. Cisco Systems (CSCO) lost 16% after joining the club in 2009.

The problem is that Apple entered the index after a meteoric 18 month, 130% run up. So the Dow, having missed the rise in Apple on the upside, fully participated on the downside in the stock meltdown that followed.

Apple is the second largest component in the Dow, with a hefty $575 billion market capitalization. This means that future Dow corrections will be bigger and more ferocious than they would have been without Apple and with boring AT&T.

The volatility of the lead index has just gone up, a lot.

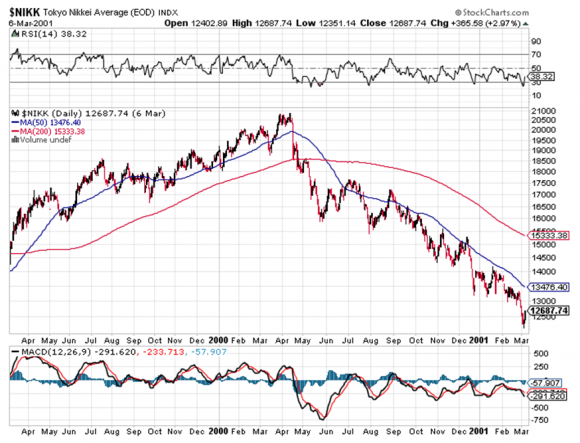

I remember too well that the Japanese made a similar blunder in 2000. The government wanted to have a national stock index that reflected the economy of the future, not of the past.

They had watched with great envy America?s NASDAQ hog the global spotlight, soaring from 1,000 to 5,000 in just a couple of years.

So what did these geniuses do? They reconstituted the Nikkei Average from a 90% boring industrial, 10% technology index to a 50/50 weighting. And they did this mere weeks after NASDAQ peaked!

As a result, the Nikkei Average got the stuffing knocked out of it in the dotcom collapse. It fell a stunning 15% in the week just after the reconstitution announcement. It cratered from 21,000 to eventually bottom at 7,200. Without the reconstitution, it would have sold out at 10,000.

Having missed the dotcom boom on the upside, the Nikkei fully participated on the downside. Apple shareholders please take note.

Apple?s rise was amply chronicled by a steady series of Trade Alerts in this newsletter.

You can go back to my 2012 prediction that Apple would soar from $485 to $1,000 (click here). On a split adjusted basis we? already reached $931.

I followed that up with ?Apple is Ready to Explode? in October, 2013 (click here), when the post split share price was back at $70.

Indeed, I have issued more Trade Alerts to buy Apple over the seven-year life of this newsletter than any other single name.

It looks like I will be issuing a lot more Apple Trade Alerts in the near future as well.

Guess When the Index Reconstitution Took Place?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/03/Apple-Watch.jpg221398Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-03-07 01:06:152016-03-07 01:06:15What Happened When Apple Entered the Dow?

Anyone would be forgiven for thinking that the stock market has become bipolar.

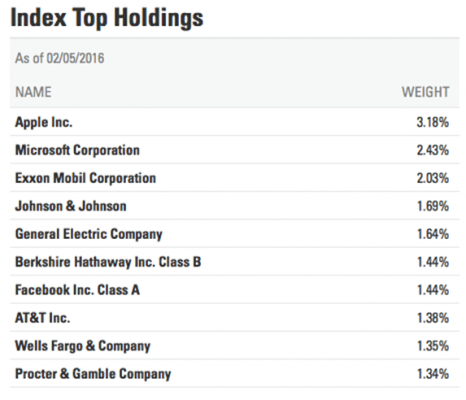

According to the Commerce Department?s Bureau of Economic Analysis, the answer is that corporate profits accounts for only a small part of the economy.

Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly, or are too small to have much of an impact.

Wages and salaries are in a three decade long decline. Interest and investment income is falling, because of the ultra low level of interest rates. Farm incomes are up, but are a tiny proportion of the total. Income from non-farm unincorporated business, mostly small business, is unimpressive.

It gets more complicated than that.

A disproportionate share of corporate profits is being earned overseas. So multinationals with a big foreign presence, like Apple (AAPL), Intel (INTC), Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes.

They really get to have their cake, and eat it too. Many of their business activities are contributing to foreign GDP?s, like China?s, more than they are here. Those with large domestic businesses, like retailers, earn less, but pay more in tax, as they lack the offshore entities in which to park them.

The message here is to not put all your faith in the headlines, but to look at the numbers behind the numbers. Those who bought in anticipation of good corporate profits last month, got those earnings, and then got slaughtered in the marketplace.

Caveat emptor. Buyer beware.

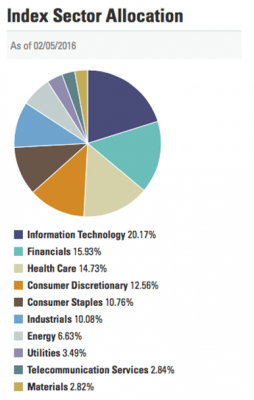

What?s In the S&P 500?

Has the Market Become Bipolar?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/09/bipolar-masks-e1455046648141.jpg287400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-02-10 01:07:452016-02-10 01:07:45The Bipolar Economy

Many ascribe Monday?s 312 point plunge in the Dow Average to an informational webinar posted by legendary corporate raider and hedge fund manager, Carl Icahn.

I have known Carl for 30 years, and I once owned and apartment in his building on the Upper East Side of Manhattan, near Sutton Place (which I later sold for a quick double).

Even then, he was opinionated, cantankerous, and never hesitated to make the bold move. Wall Street hated him.

At 79, he is nothing less than a force of nature. Whenever I see Carl, I say I want to be like him when I grow up.

I just watched the controversial video, entitled ?Danger Ahead ? A Message From Carl Icahn?, which has ruffled more than a few feathers in the establishment. But that has always been Carl?s strong suite.

Here are the high-points:

1) We should end the ?carried interest? treatment of hedge fund profits, which lets billionaire managers get off scot-free, while sticking a big tax bill with the little guy.

2) Foreign profits of US multinationals, some $2.2 trillion, should be brought home, taxed, and put to work.

3) Corporate inversions, whereby American companies reincorporate overseas to beat taxes, should be banned.

4) Corporate share buybacks, which amount to 4.5% of the outstanding float per year, are a short-term fix for company share prices only at the long-term price of a weaker balance sheets.

5) Some $4.5 trillion in borrowing by the Federal Reserve has crowded out the little guy. On this one, I disagree with Carl. With overnight rates at zero and ten year Treasury bonds yielding 2.06%, nobody is getting crowded out from anything.

6) Artificially low interest rates are fueling an unwarranted takeover boom and encouraging risky financial engineering.

7) Junk bonds (HYG), (JNK) are a bubble begging to pop. They are the result of a runaway Wall Street selling machine that saw big firms selling short their own issues to unwary customers.

Carl sums up by saying that while the Fed saved the US economy during 2008-09, they created the problem in the first place with Greenspan?s excessive easing in 2002-03.

He believes that the candidacy of outsider Donald Trump is a natural reaction to peoples? dissatisfaction with Washington and Wall Street.

I have to admit that Carl has brought up some serious points here. I agree with all, except the above-mentioned ?crowding out? issue. Combined, they are a detrimental tax on the long-term economic health of America.

Could this be an attempt by Carl to throw his hat into the political ring? Treasury Secretary in a future Trump administration was mentioned in later media interviews.

But at his age, even for Carl, that would be a reach.

While Icahn has been ringing the alarm bell on the stock market and junk bonds all year, he has been aggressively acquiring major stakes in in the energy and commodities sectors all year, while they are trading at generational lows.

He has zeroed in on two of my own favorite trades, Freeport McMoRan (FCX) and Cheniere Energy (LNG).

Carl is also holding a major position in Apple (AAPL), which he acquired two years ago just after I jumped in at $395. He believes the shares are absurdly cheap.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/09/Carl-Icahn-e1443558198697.jpg305400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-09-30 01:07:562015-09-30 01:07:56Carl Icahn Is At It Again

?The Solar Road Revisited?. Somehow this modernized version of Bob Dylan?s epic folk album doesn?t quite ring true when couched in terms of our hyper accelerating 21st century technology. Perhaps a Millennial bard will improve on this in the future on iTunes, Pandora, and Beats, of course?

Yet, such a futuristic invention has already been created, is raising money through crowdfunding, and even landed a small Federal Highway Administration grant.

We live in an age of exploding technologies. So, when I find some that are especially interesting, offer a potential long term impact on the global economy, or present immediate investment opportunities, I am going to update you in this newsletter.

One common complaint I hear during my road shows is that we are moving into the future so fast, that it is getting increasingly hard to keep up. That is, unless you live within sight of Apple (AAPL), Google (GOOG), Twitter (TWTR), and Facebook (FB) headquarters, which I do. These companies all have venture capital arms, which fund many of these things.

Sandpoint, Idaho based engineers Julie and Scott Brusaw are the founders of Solar Roadways, a tiny engineering company that seeks to convert the American highway system from old fashioned asphalt and concrete to tempered glass and LED?s.

They have raised $2 million through the crowdsourcing website Indiegogo, which saw its amazing videos on the project go viral and attract 15 million views (https://www.indiegogo.com/projects/solar-roadways ).

Caution: conservatives may want to avert their eyes during all of the global warming, anti gasoline, and tree hugging references. But this stuff raises big bucks in California.

What can solar roads do? Obviously, the green hexagonal panels they are made of convert sunlight into electricity, heating roads so they can remain free of ice and snow all year. I could really use that up at Lake Tahoe.

Surplus power can be sold to local utilities to pay for it. Electric cars, like my Tesla Model S-1 (TSLA), can recharge their batteries just by parking on it, as my toothbrush already does in my bathroom.

You can program the LED?s to embed changeable road signs, borders, parking lots, and crosswalks. They can highlight crossing animals (200 deaths a year now in the US), or impending road obstructions.

They can even display layouts for every kind of sport (basketball, tennis, etc). The glass can be cast to give it a better grip than contemporary roads. Highway deaths would plunge, as would insurance costs.

Driving trucks on glass? The material is so strong that it can support the heaviest, or some 62 tons. My question, can handle steel caterpillar tractor treads used in road repair equipment?

Of course, it always comes down to cost with these new technologies, many of which remain pie in the sky forever. Estimates are that these roads cost 50%-300% more than existing ones. Large-scale construction would bring that down through economies of scale via mass production. The design is really quite simple.

The vision is big. It would probably cost over $1 trillion just to pave over the existing 48,000 miles of the interstate highway system. Tens of thousands of blue-collar jobs would be created. It all sounds like a massive public works project would be required, of Rooseveltian, CCC magnitude.

This just gives you a flavor of the incredibly interesting things going on here in the San Francisco Bay area, which I learn about on a daily basis. Check out the site, if only to see the future of start up funding.

You can contribute $5, or just buy a tote bag.

Somehow, It?s Just Not the Same

?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/06/Moose.jpg240440Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-07-06 01:03:322015-07-06 01:03:32The Solar Road Revisited

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

3X Leveraged Bear ETFs

3X Leveraged Bear ETFs