Mad Hedge Technology Letter

January 23, 2019

Fiat Lux

Featured Trade:

(WHY TECH IS FLEEING SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)

Mad Hedge Technology Letter

January 23, 2019

Fiat Lux

Featured Trade:

(WHY TECH IS FLEEING SILICON VALLEY),

(AAPL), (CRM), (MSFT), (FB), (AMZN), (GOOGL)

When did Marc Benioff become a real estate agent?

That is the main takeaway from the interview he gave to the world from the annual powerful people conference in Davos, Switzerland.

During the interview, he cut straight to the chase and described the cocktail of negative unintended consequences that the tsunami of tech profits has spawned.

His thesis, though not new, parlayed admirably with Bridgewater Associates Founder Ray Dalio interview in chronicling an economic landscape in which geopolitical turmoil finally catches up meaningfully with the movement of tech shares because of the underlying threat to influence concrete economic policy moving forward.

Why is he a real estate seller?

Well, he might as well be one in second-tier cities with copious amounts of tech talent such as Austin, Nashville, Sacramento, Atlanta, and Portland because these metro areas are about to experience a wild ride in the property market rollercoaster.

Benioff just added fuel to this fire.

The robust housing demand, lack of housing supply, mixed with the avalanche of inquisitive tech money will propel these housing markets to new heights and this phenomenon is happening as we speak.

Benioff lamented that San Francisco, where ironically he is from, is a diabolical “train wreck” and urged fellow tech CEOs to “walk down the street” and see it with their own eyes to observe the numerous homeless encampments dotted around the city limits.

The leader of Salesforce doesn’t mince his words when he talks and beelines to the heart of the issues.

After relinquishing some of his CEO duties to newly anointed Co-CEO Keith Block, Benioff will have the operational time and a wealth of resources to get on top of the pulse of not only tech issues but bigger picture stuff and he now has a mouthpiece for it with Time magazine which he and his wife recently bought.

In condemning large swaths of the beneficiaries of the Silicon Valley ethos, he has signaled that it won’t be smooth sailing for the rest of the year in tech wonderland, and he urged companies to transform their business model if they are irresponsible with user data.

The tech lash could get messier this year because companies that go rogue with personal data will face a cringeworthy reckoning as the tech lash fury seeps into government policy and the social stigma worsens.

I have walked around the streets of San Francisco myself. Places around Powell Bart station close to the Tenderloin district are eyesores. South of Market Street isn’t a place I would want to barbecue on a terrace either.

Summing it up, the unlimited tech talent reservoir that Silicon Valley gorged on isn’t flowing anymore because people don’t want to live there now.

This tech talent, equipped with heart-tugging stories from siblings and anecdotes from classmates getting shafted by the San Francisco dream, has recently put the Bay Area in the rear-view mirror for many who would have stayed if it were 20 years ago.

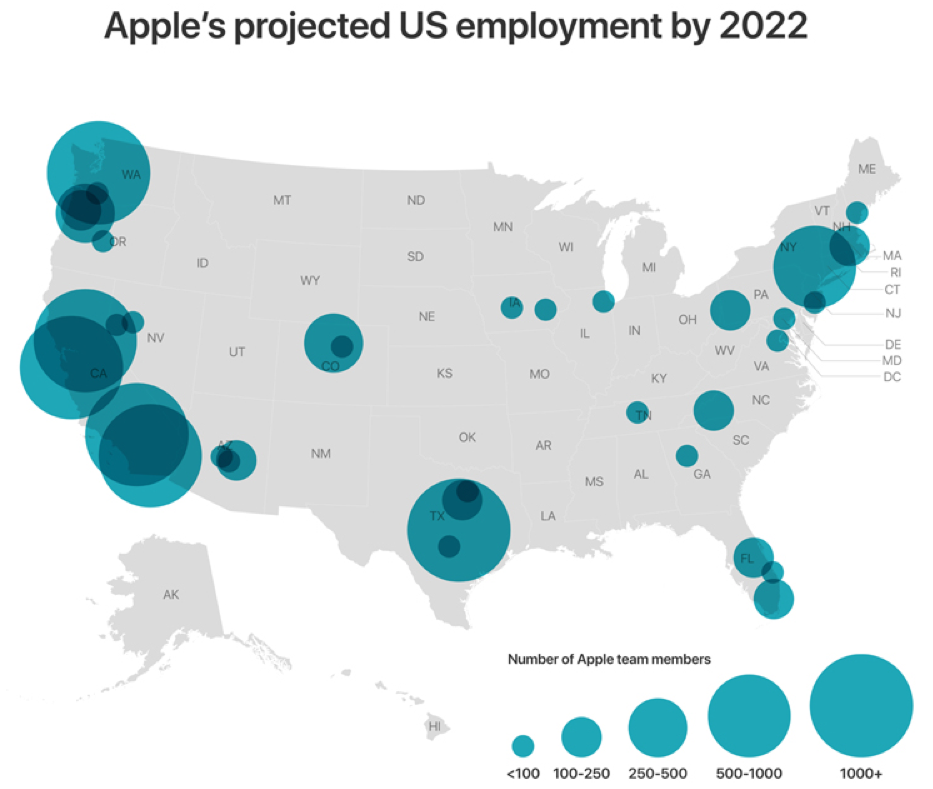

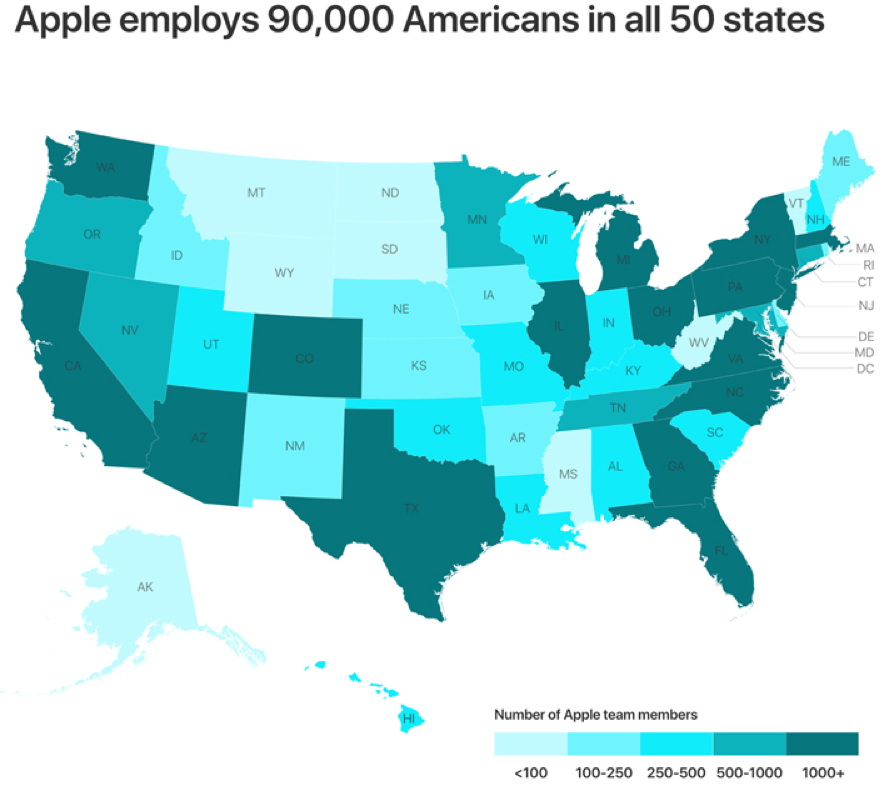

This is exactly what Apple’s $1 billion investment into a new tech campus in Austin, Texas and Amazon adding 500 employees in Nashville, Tennessee are all about. Apple also added numbers in San Diego, Atlanta, Culver City, and Boulder just to name a few.

Apple currently employs 90,000 people in 50 states and is in the works to create 20,000 more jobs in the US by 2023.

Most of these new jobs won’t be in Silicon Valley.

Since the tech talent isn’t giddy-upping into Silicon Valley anymore, tech firms must get off their saddle and go find them.

The tables have turned but that is what happens when the heart of western tech becomes unlivable to the average tech worker earning $150,000 per year.

I also mind you that these external forces have nothing to do with pure technology, pure technology improves with each iteration and gaps up with each revolutionary idea.

That will not change.

Driving out young people who envision a long-term future elsewhere than the San Francisco Bay Area forces Silicon Valley to adapt to the new patterns revealing themselves.

Sacramento has experienced a dizzying rise of newcomers from the Bay Area itself.

Some are even commuting, making that 60-mile jaunt past Davis, but that will give way to entire tech operations moving to the state capitol.

Millennials are reaching that age of family formation and they are fleeing to places that are affordable and possible to become a new home buyer.

These are some of the practical issues that tech has failed to embrace and to maintain the furious pace of growth that investors' capricious expectations harbor.

Silicon Valley will have to become more practical adding a dash of empathy as well instead of just going by the raw and heartless data.

We aren’t robots yet, and much of the world still augurs to emotional decisions and disregards the empirical data.

My favorite tech companies are not only saying the right things but are doing the right things as well.

Microsoft (MSFT) just laid down a marker promising $500 million to build more affordable housing in Seattle.

Sustainability does not only mean building a sustainable business model on the balance sheet, but this definition is growing to be inclusive of upholding the stability and long-term prospects of a local area.

Microsoft has put the trust in its products at the fore of their business model.

Each time CEO of Microsoft Satya Nadella interviews, he preaches about the universal trust that consumers possess in Microsoft.

He is not off on his claims and Microsoft is riding this mantra all the way to the bank while sidestepping regulatory scrutiny.

Nadella is always smartly one step ahead.

All this screams going long Microsoft by buying the dips.

Sell the rallies in the names that have a crisis of trust such as Facebook (FB) and Google (GOOGL).

I was recently gouged $250 on my monthly phone bill by Google because of a technicality from cell phone service Google Fi.

All a specialist said was that according to the data, I should be charged almost as if I should be shamed for even questioning their business model.

Not only that, the best and brightest from Stanford, University of California at Berkeley, and Ivy league schools do not want to work for Facebook and Google anymore.

These brands have been tainted.

The result will be needing to overpay to secure the able forces needed to pursue growth and success.

Not only that, upper management has left in droves “pursuing new opportunities.”

Google is also grappling with an Apple problem - no new innovative products and it’s yet to be seen if Waymo, the autonomous driving business, can be that solid growth driver going forward.

As the economy creeps closer and closer to the end of the cycle, investors won’t be willing to drain money down some loss-making outfit in the name of growth.

Therefore, software companies based on innovation fused with stable profits will be the go-to formula in tech investing in 2019 and Amazon (AMZN), Salesforce (CRM), and Microsoft (MSFT) are ahead of the curve.

Don’t get me wrong - Silicon Valley is still alive and kicking.

But, instead of physical offices being planted in the Bay Area, the tech industry will give way to the “spirit” of Silicon Valley with offices in far-flung places.

And remember that all of these new tech talent strongholds will need housing, and housing that an IT worker making $150,000 per year desires.

Global Market Comments

January 23, 2018

Fiat Lux

Featured Trade:

(PLAYING THE SHORT SIDE WITH VERTICAL BEAR PUT SPREADS), (TLT)

(WHY TECHNICAL ANALYSIS DOESN’T WORK)

(FB), (AAPL), (AMZN), (GOOG), (MSFT), (VIX)

Global Market Comments

January 22, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or WHY I LOVE THE STOCK MARKET),

(SPY), (TLT), (MSFT), (CRM), (AMZN), (FXE)

(HOW TO EXECUTE A VERTICAL BULL CALL SPREAD),

(AAPL)

I love working in the stock market.

Not only can it be entertaining, it can be downright hilarious. All of the talking heads on TV who were ultra bearish on the December 24 Christmas Eve Massacre are now hyper bullish, stumbling over each other trying to buy back the shares they sold 20%-30% lower.

January is turning into a mirror image of December. Last month you never got the rally to sell into. This month you can’t get a decent dip to buy into. The worst December in history was followed by the best January in 30 years with the mere turning of a page of the calendar.

I suspected as much was coming. That’s why I lurched from 10% to 60% invested during the first few days of 2019. All that’s left now is to take profits.

We got a particularly nice 336-point gap up in the Dow Average ($INDU) on Friday with rumors of progress on the China trade talks. However, those who bought on such speculations over the past nine months have all been badly burned.

A few weeks ago, the biggest threat to the market was failure of the China trade talks and a new government shutdown. Now, with prices 3,250 points, or 15% higher, the biggest threat to the market is SUCCESS of the China trade talks and the END of the government shutdown. They could trigger a huge “buy the rumor, sell the news” market move.

And what if stocks rise virtually every day this month as they did during January a year ago? It could get followed by the February we saw last year which served up a horrific selloff.

Like a hot water heater with a corroded safety valve, pressure is building up in the stock market and it is just a matter of time before it explodes. The Volatility Index (VIX) has just halved from $36 to $17. The only question is whether the next big move will be to the upside or the downside.

Don’t get too bullish now. A ton of bad economic news will hit the market in February. China slowdown, European crash, Brexit, what’s not to hate?

Don’t forget that the deadline for the completion of the trade talks is March 1.

Special persecutor Robert Mueller could also drop his report on the market at any time. Just when you think that things can’t get any worse, they do so, in spades.

If nothing gets done, you can expect another Christmas Eve Massacre, except this time it will come nine months early. It could set up the double bottom for the entire correction.

On the other hand, if everything gets resolved all at once, you can count on share prices taking off to the upside and challenge the old highs. And it might all happen on the same day.

We started out the week discovering that Newmont Mining bought Goldcorp for $10 billion to create the world’s largest gold miner. That’s important because another classic sign of a long-term bottom for the barbarous relic is when the miners start taking over each other. I’ve seen it all before.

This was the week when economic data ceased to exist unless it comes from private sources. Entering the fifth week of the government shutdown, we are all now flying blind.

US Core Inflation rose only 2.2% YOY, after a miniscule 0.2% gain in December. Don’t count on that pay rise anytime soon. All your company’s money is going to share buybacks instead.

Apple’s Asian suppliers reported terrible numbers. iPhone prices in China were cut. Apple is also cutting back on hiring. Fewer iPhone sales mean fewer people are needed to make them. I think I’ll keep my Apple short position.

PG&E went Bankrupt in order to keep the lights on in the face of $30 billion in potential wildfire liabilities. It’s the second time in 20 years. Thank goodness for my solar panels. Power prices are about to spike up big time and I’m a net supplier to the grid.

Netflix raised prices and the stock soared. Their monthly take is jumping by 13%-18%. (NFLX) shares are now up by 50% since Christmas Eve. The Walking Dead and House of Cards just got more expensive.

Brexit went down in flames with a crushing 432 to 202 loss in the UK parliament, the worst in 100 years. The opposition tabled a vote of no confidence which failed by only ten votes, barely heading off a general election. Next to come is a new referendum on Brexit itself which will go down in flames. Buy the British pound (FXB).

What does the end of Brexit mean for the Global economy? It strengthens Europe, prevents Italy, Greece, Portugal, and France from leaving the European Community, preserves NATO, and stops the Russian hordes from overrunning Western Europe. Croissants will be cheaper in London too. That’s all.

The December Fed Beige Book came in moderate. “Trade war” was mentioned 20 times but “government shutdown" comes out only once. Inflation is low but companies can’t pass price increases on to consumers. Labor shortages are showing up everywhere, but with few wage increases. The auto industry is flatlining.

My January and 2019 year to date return exploded to +5.29%, boosting my trailing one-year return back up to +31.68%.

My nine-year return climbed up to +306.19%, just short of a new all-time high. The average annualized return revived to +34.00%.

I took profits on one of my big tech longs in Salesforce (CRM) which maxed out the gains in my options position. I love this stock and will be back in there again on the next dip.

I am keeping my option positions in Microsoft (MSFT) and Amazon (AMZN) to take advantage of the time decay over the four day weekend. I cashed in half of my short position in the bond market (TLT), taking advantage of the recent 4 ½ point decline there.

My long position in the Euro (FXE) survived the failure of Brexit and a no-confidence vote in Britain. It continues to bounce along the bottom.

I also kept my short positions in Apple (AAPL) and the S&P 500 (SPY). Happy days are definitely NOT here again, with a government shut down and a continuing trade war with China. I am now nearly neutral, with “RISK ON” positions “RISK OFF” ones.

We have recently seen a surge of new subscribers and for you I urge patience. In this kind of market the money is made on the “BUY”, so timing is everything. The goal is to make as much money you can, not to see how fast or how often you trade.

The upcoming week is very iffy on the data front because of the government shutdown. Some government data may be delayed and other completely missing. Private sources will continue reporting on schedule. All of the data will be completely skewed for at least the next three months. You can count on the shutdown to dominate all media until it is over.

Housing data will be the big events over the coming four days.

On Monday, January 21, markets are closed for Martin Luther King Day.

On Tuesday, January 22, 10:00 AM EST, the December Existing Home Sales are out. IBM (IBM) and Johnson & Johnson (JNJ) announce earnings.

On Wednesday, January 23 at 10:30 AM EST the Energy Information Administration announces oil inventory figures with its Petroleum Status Report. Lam Research (LRCX) and Procter & Gamble (PG) report.

Thursday, January 24 at 8:30 AM EST, we get Weekly Jobless Claims. At 10:00 AM, we learn December Leading Economic Indicators. Intel (INTC) and American Airlines (AA) report.

On Friday, January 25, at 10:00 AM EST, the latest read of December New Home Sales is released. The Baker-Hughes Rig Count follows at 1:00 PM. Schlumberger (SLB) announces earnings. Home Sales is released. AbbVie Inc (ABBV) and DR Horton (DHI) report.

As for me, I will be battling my way home from Lake Tahoe which received seven feet of snow last week. It was a real “snowmageddon.”

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

January 22, 2019

Fiat Lux

Featured Trade:

(HOW TO PLAY TECHNOLOGY STOCKS IN 2019),

(NFLX), (AAPL), (TSLA), (STT), (BLK)

In the past week, the tech sector has received information allowing investors to sketch a concise roadmap of what to expect in the tech sector for the rest of 2019.

One – the bull story in technology isn’t dead and the December sell-off in tech growth stocks was overdone.

Two – the path to tech profits is filled with more booby traps than in year’s past.

Three – the migration to digital is becoming more pronounced by the millisecond.

If you go back about a month ago when tech stocks were at their trough, traders were pricing in about a 60% chance of a recession in 2019 or early 2020 and the data didn’t support it.

What people were confusing themselves with was slowing growth instead of a lack of growth.

Then we got the disastrous news from Apple (AAPL) indicating business in China was petering out forcing them to change tactics cutting iPhone prices.

The tech market went into full-on panic mode and the revelation of weak China data did not help either.

Netflix (NFLX) reported and the online streaming app offered some respite with outperforming growth numbers.

Netflix has been a favorite of the Mad Hedge Technology Letter since its inception but the caveat with Founder and CEO of Netflix Reed Hastings brainchild is that the extreme volatility makes it difficult to trade around on a short-term basis.

The stock is up 50% from its nadir and its growth story is solid and will perpetuate.

The next bastion of juiced-up growth for Netflix is the international audience and these numbers are examined closely with a fine-tooth comb by investors attempting to understand the direction of the company.

The company audaciously added 8.8 million in new international subscribers last quarter which handily beat the 7.6 million estimates by 1.2 million.

Netflix also announced a few days earlier that it would raise the price of a monthly subscription between 13%-18%, and investors treated the news with celebratory shots of tequila.

It has been consensus for years that Netflix was severely underpricing their premium content, and analysts have been screaming and kicking trying to get Hastings to push up their monthly prices.

The price hike coincides with a year where I believe Netflix can grow revenue over 30%.

The mix of these two developments illuminate a few things about Netflix.

Netflix has the content that consumers want and even if competition rears its ugly head, they aren’t even in the same ballpark in terms of breadth and potency of content.

They are the king of contents and I don’t see anyone knocking them off their elevated perch in 2019.

In many ways, the Netflix long-term thesis mirrors the tech industry’s long-term thesis emphasizing supercharged growth by any means possible.

Even though this strategy is risky, it is working for Netflix and the capital isn’t drying up to go after the best content producers money can buy.

This earnings report should put to rest the growth warning sirens for now, tech will grow this year, but earnings results will be more of a mixed bag with the occasional miss.

This is in stark comparison to early 2018 where every tech company and their mother were scorching earnings forecasts by a magnitude of two or three.

Last September, the tech market looked above its head and saw a few boulders about to crush the herd, but investors shrugged it off.

As we move forward, the tech sector and the overall market is inching closer to a recession.

The low-hanging fruit has been pocketed and incremental gains aren’t no-brainers anymore – this can be gleaned from Tesla (TSLA) curtailing their workforce by 7%.

This news was delivered by a letter from CEO of Tesla Elon Musk noting that these decisions have been made with the goal of “increasing the Model 3 production rate and making many manufacturing engineering improvements in the coming months.”

Basically, Musk has telegraphed that staff needs to perform better, identify efficiencies that will save costs which in turn will boost profit margins.

This doesn’t mean that the era of tech growth is over, but this signals that tech companies are becoming more fidgety about loss-making operations and have ultimately targeted profits which shout at investors' late-cycle economics.

Musk needs to turn Tesla into a perennial profit machine to prove naysayers wrong, and now is the time to turn the page and max out his rocket fuel.

If the recession hits, investors could turn against Tesla and capital could dry up.

This newfound modesty towards the e-car business model is, in no doubt, exacerbated by the ratcheting up of fierce competition from the traditional automobile makers.

Tesla is in the e-car lead for battery technology, revolutionary production processes, and have a treasure trove of data that German companies would do anything to get their hands on.

Musk knows Tesla has fought this hard to get to this point, and he'd rather have the ball in his hands with 10 seconds left and a tie game just like Michael Jordan of the Chicago Bulls did.

Shaving off the excess has meant removing the customer referral program that was too costly that included benefits like half a year of free charging.

Part of this also has to do with Tesla losing their tax credit at the end of the year as well as giving more impetus to trimming costs.

Becoming a mass-market car manufacturer means it is important to price the car at affordable price points and that will be extremely difficult.

The goal is to deliver a $35,000 e-car that performs comparably to the rest of the fleet but produced with 7% less hands.

Can Musk do it?

I wouldn’t bet against him.

Musk means business and is hellbent for revenge against his arch enemies – the Tesla short community who he has habitually dragged under the bus through the media.

Piggybacking on this tougher profit-making climate is Boston-based finance company State Street Corporation’s (STT) announcement reducing headcount by 1,500 amounting to 6% of the global workforce.

The firm cited the urgent need to automate processes that will give the company a bigger foothold into the digital sphere.

The same theme was echoed at BlackRock Inc. (BLK), the world’s largest asset manager, who will eliminate 3% of its global workforce, or 500 people, amid an existential threat from the temporary ineffectiveness of passive investing.

In a rising market, it is guaranteed that assets at these types of funds almost always go up.

However, with an injection of recent volatility, passive investors have seen their balances dwindle with the market spawning abrupt outflows.

The need to zig and zag with the market is now painfully obvious and using technology to plug in the gaps will be cheaper and more appropriate for late cycle price action.

This is a suitable segue way into the third point – the fluid follow-through of the digital migration and the debacle of Sears prove my point.

Hedge fund manager Eddie Lampert and his firm ESL have navigated this famous American retailer into the ground.

This is what happens when the entire retail industry goes online when you don’t.

To make matters worse, Lampert has probably never set foot into his own investment.

Each time I roam the aisles of Sears, it’s about as crowded as a mortuary at midnight – an elementary story of a mismanaged enterprise.

Sears is an example of digital ignorance and it’s not the only one.

Gymboree Group, the baby clothing company, is another one to put on the list – the firm filed for Chapter 11 bankruptcy protection.

The company will close more than 800 Gymboree and Crazy 8 stores, this is the second time they have filed for bankruptcy protection in the past two years.

Unsurprisingly, the firm cited a sudden decrease in mall traffic and a surge in online alternatives as the reason for the economic softness.

The economy does not operate in a vacuum and any analog company who voluntarily misses the pivot to digital is voluntarily digging their own grave.

These three trends will only become more exaggerated moving forward threatening companies like Apple who fail to innovate after more than a decade of selling the same product, other companies don’t have the balance sheets to handle the same weakness.

Mad Hedge Technology Letter

January 15, 2019

Fiat Lux

Featured Trade:

(THE BALKANIZATION OF THE INTERNET),

(AAPL), (FB), (CTRP), (PDD), (BABA), (JD), (TME)

The Mad Hedge Technology Letter has a front-line seat to the carnage wrought by the balkanization of technology that is swiftly descending across all corners of the tech universe.

In technology terms, this is frequently referred to as “splinternet.”

A quick explanation for the novices can be summed up by saying splinternet is the fragmenting of the Internet causing it to divide due to powerful forces such as technology, commerce, politics, nationalism, religion, and interests.

The rapid rise of global splinternet news stories will have an immediate ramification on your tech portfolio and it’s my job to untangle the knots.

What investors are seeing is the bifurcation of the global tech game into a binary world of Chinese and American tech.

Most recently, Central European country Poland, who was thought to be siding with the Chinese because of the growing presence by large-cap Chinese tech in Warsaw, announced government security had arrested a Huawei employee, Chinese national Wang Weijing, for allegedly spying on behalf of the Chinese state.

For all the naysayers that believe the administration’s hope of curtailing the theft of western technology was a bogus endeavor, this recent event buttresses the notion that Chinese state-funded tech companies are truly running nefariously throughout the world.

In fact, Poland has little to gain from this maneuver if you take the current status quo as your guidebook, and I would argue it is a net negative for Poland because Chinese tech is deeply embedded inside of the Poland tech structure bestowing profits and internet capabilities on multiple parties.

Making the case stronger against China, Poland has no flagship tech communications company that would serve as competition to the Chinese or could directly gain from this breach of trust.

The fringe of the Eurozone Central European nations and Eastern European countries bordering Russia running developing economies rely on Huawei and other low-cost Chinese tech suppliers like ZTE to offer value for money for a populace who cannot afford $1000 Apple (AAPL) iPhones and exorbitant western European telecommunications infrastructure equipment.

The Chinese beelining to this burgeoning area in Europe has given these less developed countries high-speed broadband internet for $10-$15 per month and 4G mobile service for $7 per month, a smidgeon of what westerners fork out for the same monthly service.

Poland rebuffing Huawei is an ominous sign for Chinese tech doing business in the Czech Republic and Hungary as European countries are moving towards denying Huawei in unison.

The last few years saw China create the same recipe of success for fueling economic expansion mimicking the American economy.

The tech sector led the way with outsized gains boosting productivity while analog companies transformed into digital companies to take advantage of the efficiencies high-tech provides.

At the same time, Beijing has initiated a muscular response to the accelerated growth of local tech companies.

The foul play of American tech in Europe has given impetus to Beijing to launch a power grab on local tech structures such as Baidu, Alibaba, and Tencent.

This couldn’t be more evident at Tencent who has failed to secure any new gaming licenses for their best gaming titles.

PlayerUnknown’s Battlegrounds (PUBG), a battle royale multiplayer, has been deprived of massive revenue because of Tencent’s inability to win a proper gaming license from the Chinese authorities to sell in-game add-ons.

In total, lost revenue has already cost Chinese video game companies over $2 billion in revenue since May 2017.

Beijing wants to temper the growing clout of private tech companies who were the recipient of the Chinese consumer’s gorge on technology in the last 20 years.

These companies have never been more infiltrated by the communist party and this can be mainly attributed to the acknowledgment by Beijing that Chinese tech companies are too powerful for their own good now and are a legitimate threat to the powers above.

That is what the sudden retirement of Founder of Alibaba Jack Ma told us who infuriated Chairman Xi because Ma was the first Chinese of note to meet American President Donald Trump at Trump Towers pledging to create a million jobs in America.

Ma later rescinded that statement and was put out to pasture by Beijing.

What does this all mean?

As the broad-based balkanization spreads like wildfire, Chinese and American tech companies’ addressable markets will shrink hamstringing the drive to accelerate revenue.

The potential loss of Europe for the Chinese could give way to Nokia, Siemens, and other western telecommunication companies to move in hijacking a bright spot for Huawei.

If Apple isn’t punching above their weight in China, well that almost certainly means that local tech companies aren’t having a cake walk in the park as well.

The winter sell-off turned the screws on tech first and then the rest of equities obediently, Chinese tech could have a similar domino effect to the Chinese economy boding badly for Chinese ADRs listed on the New York Stock Exchange (NYSE).

Last year, the Shanghai index was one of the worst performing stock markets in the world.

And if the trade wars are really ravaging a few key limbs from local Chinese tech firms, then companies exposed to the Chinese consumer such as Alibaba (BABA), JD.com (JD), Pinduoduo (PDD), Ctrip.com International (CTRP) and Tencent Music Entertainment (TME) could fall off a cliff.

This has already been in the works.

These companies are a good barometer of the health of the Chinese consumer and have had an abysmal last six months of price action.

The vicious cycle will repeat itself with worsening Chinese data drying up the demand for Chinese tech services and the Chinese consumer tightening their purse strings as they try to save money from a cratering economy.

It could become a self-fulfilling prophecy and that is what other indicators such as negative automobile sales and a rapidly failing real estate market are telling us.

The 65 million ghost apartments dotted around China don't help.

This could be the perfect opportunity to instigate wide-ranging reforms to open up the financial, insurance, a tech market to the west, something many analysts thought China would do after joining the World Trade Organization (WTO).

However, Beijing’s retrenchment preferring to pedal mercantilism and cold-blooded power grabs could offer Chairman Xi the prospect of further consolidating his authority by sticking his fingers deeper into the local tech structures giving the state even more control.

I would guess this is a false dawn.

American tech will confront balkanization headwinds of its own evidence in Vietnam as the government blamed Zuckerberg’s Facebook (FB) for failing to root out anti-government rhetoric which is illegal in the communist-based country.

If you haven’t figured it out yet – there is an underlying suitability issue with western tech services that tie up with authoritarian governments.

It many times leads the western tech companies to be a pawn in a political game that later turns into a bloody mess.

The weak rule of law has spawned a convenient practice of blaming western tech to distract from internal disputes strengthening the nationalist case of a purported western tech firm gone rogue.

This could lead Facebook to be removed in Vietnam, and the $238 million in ad revenue that will vanish.

Headaches are sprouting up across Europe with Facebook clashing with more stringent data privacy rules through General Data Protection Regulation (GDPR).

German’s largest national Sunday newspaper Bild am Sonntag claimed from sources that the Federal Cartel Office will summon Facebook to halt collecting some user data.

This could take a machete to ad revenue in a critical lucrative market for Facebook, and this experience is being echoed by other American tech companies who are running full speed into complicated regulatory quagmires outside of America.

Adding benzine to the flames, Deputy Attorney General Rod Rosenstein speaking at a cybercrime symposium at Georgetown University’s Law Center in Washington added to the tech misery explaining that to “secure devices requires additional testing and validation—which slows production times — and costs more money.”

This is not bullish to the overall tech picture at all.

Hamstringing tech is not ideal to promoting economic growth, but the decades of unchecked growth is finally reverting back to the mean with regulation rearing its unpretty head and the balkanization of tech forcing countries to pick between China or America.

The silver lining is that the American economy remains resilient taking the body blows of a government shutdown, interest rate drama, and trade war uncertainty in full stride.

The net-net is that American and Chinese tech firms could experience decelerating revenue growth far dire than any worst-case scenario forecasted by industry analysts.

Therefore, I forecast that American tech shares have limited upside for the next 6-10 weeks and Chinese tech is dead money in that same time span.

Any rally is ripe for another sell-off if there are no meaningful breakthroughs in the trade war and if China’s economic data continues to falter.

The global growth scare could actually come home to roost.

The supposed narrowing of trade differences has been nothing more than tactical, and procuring any fundamental victories is a hard ask in the short term.

In an ideal world, China would open the floodgates and allow the world to join them in an economic détente, however, based on Chairman Xi’s record of purging his mainland enemies and the military, slamming the gates shut and padlocking them seems more likely at this point.

Seizing the rights to an untimed Chairmanship term has its perks – this is one of them and he is using the entire assortment of options available to him.

Traders should look at deep in-the-money vertical bear put spreads on any sharp rally to specific out-of-fashion tech names saddled with regulatory and data balkanization headwinds, or tech firms with a large footprint in mainland China.

Global Market Comments

January 14, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or IS THE BULL MARKET BACK?),

(SPY), (TLT), (MSFT), (AMZN), (CRM), (AAPL), (FXE),

(TESTIMONIAL)