Rivian Automotive Inc. (RIVN), the California-based EV company, touched $153 billion in market valuation making Rivian the largest U.S. company with zero revenue.

Exuberance can take you this far, but the company will need to show investors sales after the pixie dust wears off.

I understand that part of the narrative is that this could be the next Tesla (TSLA), and back of the napkin math shows us if it is a certain percentage of Tesla going forward then it would be certain billions of dollars.

The $150 billion valuation is too fast too soon, but when traders grab a hold of this rocket, all they need to do is add a little fuel.

It does speak loudly to investors that there is excess liquidity ebbing and flowing in the financial system where a stock can go this high just based on potential.

Let’s see the damn car first!

Granted, the car looks fantastic based on internet reviews, and if they do become the Tesla of pickup trucks, then anything that means reversion in the stock will be muted.

Word on the street is that only employees are driving the truck around now and the greater public should start receiving their Rivian orders at the end of 2021 or 2022.

EV peer Lucid Group Inc. also rallied intensely closing up 24% and eclipsing the valuation of Ford in the process. Lucid is now a $91 billion company, compared to Ford’s $79 billion.

Rivian will also need to compete with the upcoming European EV behemoths with Volkswagen that is Europe’s largest automaker with about 10 million vehicle deliveries per year, making it the global number two behind Toyota Motor Corp.

Rivian’s trucks are called the R1T and an electric SUV — R1S.

They forecast annual production will hit 150,000 vehicles at its main facility by late 2023.

At one point, Rivian was worth more than almost 90% of S&P 500 companies, including stocks like Goldman Sachs Group Inc., Boeing Co., Citigroup Inc., Starbucks Corp.

Rivian also benefited from Tesla’s Founder Elon Musk selling big tranches of stock which gave EV investors the green light to pile into Rivian even if it’s not for the long term.

Pricing for Rivian’s models starts around $70,000, and each features a base driving range of more than 300 miles on a full charge.

The hope is that mass affluent truck shoppers won’t be able to get enough of Rivian. Remember, the Ford F-150 is the best-selling vehicle in the country. In fact, the top six automobiles in the U.S. by sales are either pickup trucks or SUVs.

Amazon’s 20% stake in the company is the stamp of approval for many investors on the fence and they have already ordered 100,000 units for delivery by the end of 2030.

I could easily see Amazon ramping up orders quickly if they like the quality of the first two models.

Whether the stock should be $150 billion with 0 sales or not, is not really the full story of Rivian.

With only a narrow snapshot of what’s really going on, the high valuation is more a story of the momentum of the market in November that has seen big tech rejuvenate.

Rivian merely just got caught up in the updraft.

I am not diminishing the company, but they will need to demonstrate consistent earnings to build those long-term holders of the stock and I do believe they can do it.

The specs of the car look and feel like a Tesla and if they can replicate 80% of the quality with their first iterations, socially, they could catch on fire and become the new hip car to the masses.

This does set the stage for a critical first earnings report where the first sales will be thoroughly dissected with a fine-tooth comb and possible offer an entry point to investors after people realize this isn’t a $150 billion company yet.

Remember that it took Tesla years to stabilize their volatile stock, and Rivian might have to go through the same right of passage to be legit.

Rivian has the potential to become the #2 behind Tesla and that’s worth $90 billion right there, it’ll be interesting to see what pans out after that.

As for buying the stock, wait for a big sell-off then slowly scale in.

https://www.madhedgefundtrader.com/wp-content/uploads/2021/11/rivian-truck-2.png520936Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-11-17 14:02:292021-11-23 23:46:44The Tesla of Pick-Up Trucks

Peak streaming — that’s what the indicators are telling us.

It’s been a good run — lots of money made so far.

The streaming industry is resting after the pandemic pulled revenue forward a few years.

It won’t be as easy now, as the maturity of the industry means that it becomes a war inside the war, instead of the tide-lifts-all-boats type of growth.

The latter is what everyone hopes, but doesn’t always get.

The world’s largest entertainment company, Disney, posted a significant slowdown in subscriber sign-ups at its flagship streaming service in the most recent quarter.

Disney+ added only two million subscribers last quarter bringing its total to 118.1 million.

Analysts had expected this quarter’s total to come to 125.3 million. During the previous quarter, Disney+ had added more than 12 million new subscribers.

First, the follow-through from consumers just wanting to experience outside and the services attached to them ring true.

The price hikes are also another net negative, as it makes consumers less enthused about signing up.

This had to be expected and many of these streaming companies would honestly admit that they couldn’t continue the pandemic era performance.

A reversion to the mean is not the end of streaming and Disney’s streaming services.

It is still on track to reach previous guidance of between 230 million and 260 million paid Disney+ subscribers globally by the end of fiscal 2024.

Dig deeper into the streaming data and it shows that customers in India didn’t sign up because of a delay of Indian Premier League cricket games that were to air on the service.

Another indicator of the pivot to outside business is the Disney theme park revenue climbing 99%.

The trend towards outdoor activities means a slew of cancellations of the monthly subscriptions.

Netflix was the rare streaming company that bucked the trend.

Netflix streaming service added 4.4 million subscribers—or about a million more than it had forecast—on the strength of new popular shows like “Squid Game.”

Moving forward, the bar rises quite a bit for the quality of content.

Viewers are demanding more or they are riding Space Mountain in Anaheim.

Streaming companies won’t be able to pedal out mediocre shows and movies, and secondly, there is no patience for customers as the number of streaming options has multiplied.

The deeper underbelly shows us that the general trend of linear TV cancellations and streaming signups appears to be continuing even if the rate of signups is slowing.

Disney, WarnerMedia, and AMC Networks all reaffirmed previous full-year and future year forecasts. And while pandemic gains may have slowed, production slowdowns and shutdowns have also ended, which will lead to a surge of new content for all of the streaming services.

Disney investors will be zeroed in to see if the company can pump out some blockbusters, but a glut of content might mean not enough eyeballs to digest these blockbusters.

Coronavirus-related production delays continue to disrupt its pipeline of content delivery.

Disney subscriber growth could ramp back up in the latter half of 2022 when they have better titles coming to market.

Another issue for Disney is if they are willing to produce more adult content and veer away from the younger cohort they are used to entertaining.

I don’t mean X rated, but the 25-44 aged bunch, everyone is sick of the superhero movies.

When it comes to attracting subscribers to Disney+, the company in November and December will be relying on a Beatles documentary, “The Beatles: Get Back,” additional Marvel Studios and Lucasfilm Ltd. shows and films that include a new “Home Alone” feature.

In April, Jeff Bezos said more than 175 million Amazon Prime members had streamed shows and movies in the past year.

Beyond the big three — Netflix, Disney+, and Amazon Prime — things get cloudier.

In July, NBCUniversal’s Peacock reported 54 million net new subscribers and more than 20 million monthly active accounts.

Other players with potentially strong platforms include WarnerMedia’s HBO Max, with a reported 69.4 million global subscribers, and Apple TV+, which is rumored to have about 20 million U.S. subscribers.

The major streaming competitors are also actively expanding their footprint abroad to acquire more growth, but the issue I have there is that the average revenue per user (ARPU) is nothing close to what it is in North America.

Although oversees revenue could provide a little bump to earnings, it won’t recreate their earnings composition.

Which leads me to a broader take on tech, it’s slowing down because we have been in the same cycle which was essentially initiated by the smartphone, the cloud, 3G super apps, and high-speed internet.

Those super levers are showing exhaustion.

It’s not a coincidence that Facebook’s Mark Zuckerberg was desperately trotting out his vision for the Metaverse and Apple removing personal data tracking from its ecosystem.

These are late cycle signs that shouldn’t be missed.

Big tech has become a great deal more mercantilist during the latter half of this bull market, yet we aren’t at the point of cannibalization, but I do envision that moment 5-7 years out from now.

Until then, high quality tech will grind higher while slowly raising their monthly prices, and the low-quality tech products will fall by the wayside because they lack the killer content.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-11-12 14:02:262021-11-19 21:14:03Peak Streaming Growth Isn't the End of Streaming

Welcome to the first day of November, when the seasonals swing from negative to positive. The hard six months are over. The next six should be like shooting fish in a barrel.

At least that’s what happened in the past. The period from November 1 to May 31 has delivered the highest stock returns for the past 75 years.

So how do we play a hand that we have already been dealt full of aces and kings?

Load the boat with financials, like (MS), (GS), (BLK), (JPM), and (BAC). Notice that when we had the sharpest rise in interest rates in a year, financials barely moved when they should have crashed? That means they will soon start going up again.

You might have also observed that technology stock has been flat-lining when rising rates should have floored them. That means their torrid 20% earnings growth will keep floating their boats.

It gets better. We just learned that the GDP growth rate plunged in Q3 from a rip-roaring 6% rate to only 2%. What happens next? That 4% wasn’t lost, just deferred into 2022. The rip-roaring 6% growth rate returns. That’s why stocks are pushing up to new all-time highs right now.

So, buy the dips. We may have seen our last 5% correction of 2021. The only unknown is how markets will react to a Fed taper, which could come as early as Wednesday. But on the heels of that, we will get a $1.75 billion rescue package, the biggest in 50 years. One will cancel out the other, and then some.

Take a look at the ProShares Ultra Technology Fund (ROM), the 2X long ETF. I just analyzed its 30 largest holdings. Half are tech stocks that have been trash and are down 30% or more. The other half are at all-times highs, like Microsoft (MSFT) and Alphabet (GOOGL).

What happens next when the seasonals are a tailwind? The tech stocks that are down will rally because they are cheap, while the high stocks keep going because they are best of breed. I think (ROM) has $150 written all over it by March.

You’ve got to love Elon Musk, whose net worth is approaching $300 billion. When the pandemic broke, every automaker cancelled their chip orders for the rest of the year while Tesla took them all. Today, Detroit has millions of cars built but in storage because they are all missing chips. In the meantime, Tesla is snagging orders for 100,000 cars at a time.

Like I say, you gotta love Musk. Hey, Elon, call me! Why don’t you just buy the entire US coal industry and shut it down. It would only cost $5 billion, as market caps are so low. That would have more impact on the environment than another million Teslas. Worst affected would be China, where 70% of US coal now goes.

A continued major driver of the bull case for stocks is profit margins of historic proportions.

Q1 saw a 13% margin, Q2 13.5% and Q3 12.3%, and Q3 had to carry the dead weight of a delta impaired GDP growth rate of only 2.0%. Imagine what companies can do in Q4 when the growth rate is returning to a torrid 6% rate.

This has been one of my basic assumptions for the entire year and it seems it was I was alone in having it. This is where the 90% year-to-date performance comes from.

Inflation is Here to Stay, says top investing heavyweights, at least 4% through 2022. That means high inflation, higher financial shares, and higher Bitcoin prices. It’s going to take two years to unwind the mess at the ports that is driving prices.

Covid is Getting Knocked Out by a One-Two Punch, via a new round of booster shots and imminent childhood vaccinations. It could take new cases to zero in a year and give us a booming economy.

S&P Case Shiller is Still Rocketing, the National Home Price Index up 19.8% YOY in August. Phoenix (33.3%), San Diego (26.2%), and Tampa (25.9%) were the hot cities. This will continue for a decade but as a slower rate.

New Home Sales Pop, to 800,000. Annual median prices jump at an annual 18.7% to $408,000. The share of homes selling over $1 million increased from 5% to 9% in a year. It cost $500,000 to get a starter home in an Oakland slum these days. Homebuilders Sentiment Soars to 80. Buy (KBH), (PUL), and (LEN) on dips.

Bonds Melt Up, creating one of the best trade entry points of the year. A successful 30-year auction this week that took yields from 1.71% down to 1.52% in a heartbeat. It makes no sense. Buying bonds here is like buying oil in the full knowledge that someday it will go to zero. I am doubling my short position here. Look at the (TLT) December 2022 $150-$155 vertical bear put spread LEAPS which is offering a 14-month return of 54%. This is the month when the Fed has promised to begin the first of six interest rate hikes. Just buy it and forget about it.

Proof that the Roaring Twenties is Here. It’s demand that is spiking, the greatest ever seen, not supplies that are drying up in the supply chain issue. It should continue for a decade and the bull market in stocks that follows it. You heard it here first. Dow 240,000 here we come.

Apple Blows it in Q3, with millions of its phones lost at sea and no idea when unloads are possible, costing it $6 billion in sales. Revenues were up a ballistic 29% YOY. Buy (AAPL) on dips. I see $200 a year next year.

Amazon Craters, with both shrinking revenues and profits. Supply chain problems about with several billion of inventory trapped at sea off the coast of Long Beach. It plans to hire 275,000 to handle the Christmas rush. The stock hit a one year low. There is a time to buy (AMZN) on the dip, but not quite yet.

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

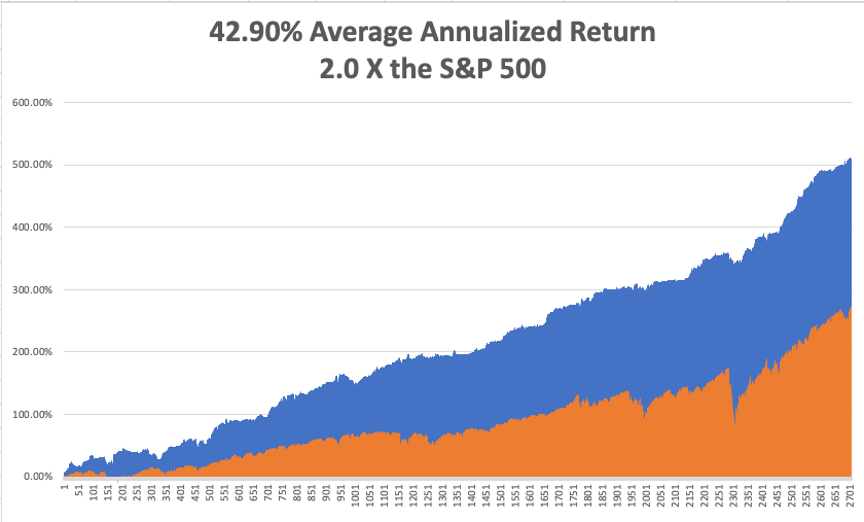

My Mad Hedge Global Trading Dispatch saw a massive +8.95% gain in =October. My 2021 year-to-date performance maintained 88.55%. The Dow Average is up 17.06% so far in 2021.

After the recent ballistic move in the market, I am continuing to run my longs in Those include (MS), (GS), (BAC), and a short in the (TLT). All are approaching their maximum profit point and we have nothing left but time decay to capture. So, I am going to run these into the November 19 expiration in 14 trading days. It’s like have a rich uncle write you a check one a day.

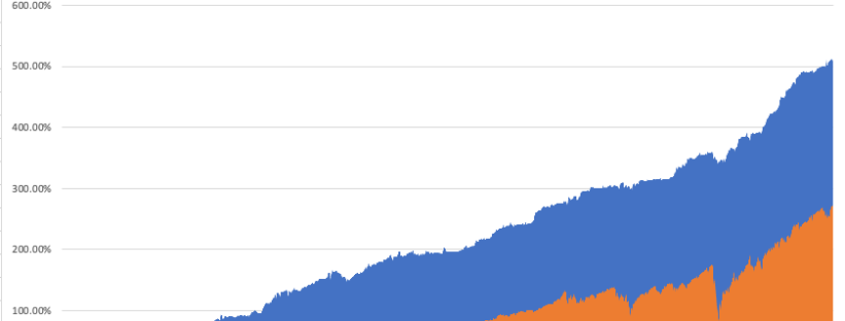

That brings my 12-year total return to 511.10%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.90%, easily the highest in the industry.

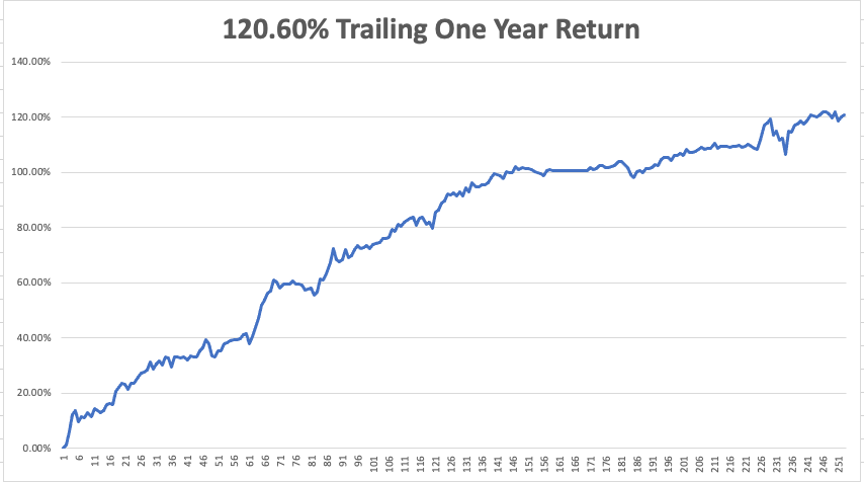

My trailing one-year return popped back to positively eye-popping 120.60%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 46 million and rising quickly and deaths topping 746,000, which you can find here.

The coming week will be slow on the data front.

On Monday, November 1 at 7:00 AM, the ISM Manufacturing PMI for October is out. Avis (CAR) Reports.

On Tuesday, November 2 at 1:30 PM, the API Crude Oil Stocks are released. Pfizer (PFE) reports.

On Wednesday, November 3 at 7:30 AM, the Private Sector Payroll Report is published. Etsy (ETSY) reports. At 11:00 AM, the Federal Reserve interest rate decision is announced, followed by a press conference.

On Thursday, November 4 at 8:30 AM, Weekly Jobless Claims are announced. Airbnb reports (ABNB).

On Friday, November 5 at 8:30 AM, The October Nonfarm Payroll Report is released. DraftKings (DKNG) reports. At 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

As for me, I have been known to occasionally overreach myself, and a trip to the bottom of the Grand Canyon a few years ago was a classic example.

I have done this trip many times before. Hike down the Kaibab Trail, follow the Colorado River for two miles, and then climb 5,000 feet back up the Bright Angle Trail for a total day trip of 27 miles.

I started early, carrying 36 pounds of water for myself and a companion. Near the bottom, there was a National Park sign stating that “Being Tired is Not a Reason to Call 911.” But I wasn’t worried.

The scenery was magnificent, the colors were brilliant, and each 1,000 foot descent revealed a new geologic age. I began the long slog back to the south rim.

As the sun set, it was clear that we weren’t going to make to the top. I was passed by a couple who RAN the entire route who told me “better hurry up.” I realized that I had erred in calculating the sunset, it'staking place an hour earlier in Arizona than in California.

By 8:00 PM it was pitch dark, the trail had completely iced up, and it was 500 feet straight down over the side. I only had 500 feet to go but the batteries on my flashlight died. I resigned myself to spending the night on the cliff face in freezing temperatures.

Then I saw three flashlights in the distance. Some 30 minutes later, I was approached by three Austrian Boy Scouts in full dress uniform. I mentioned I was a Scoutmaster and they offered to help us up.

I grabbed the belt of the last one, my companion grabbed my belt, and they hauled us up in the darkness. We made it to the top and I said, “thank you”, giving them the international scout secret handshake.

It turned out that I wasn’t in great shape as I thought I was. In fact, I hadn’t done the hike since I was a scout myself 30 years earlier. I couldn’t walk for three days.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Happy Halloween!

https://www.madhedgefundtrader.com/wp-content/uploads/2021/11/annualized-nov1.png522864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-11-01 11:02:372021-11-01 14:27:04The Market Outlook for the Week Ahead, or Let the Games Begin!

Following massive gains at the onset of the COVID-19 pandemic, several healthcare growth stocks have fallen a long way from their highs.

In fact, some high-quality names have become potential bargains due to the market's recent negative turn.

In this situation, we can apply Warren Buffett’s advice: "We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful."

That is, I think it might just be the time to be a bit greedy.

One of the companies affected by the massive pullback is Teladoc (TDOC).

Over the past 1.5 years, Teladoc has been on a rollercoaster ride when it comes to its price action.

Initially, the stock was regarded as merely a COVID-19 pandemic play with limited growth in the future.

Because of that perception, Teladoc's price started to drop the moment the people got their vaccine shots.

Some investors believe that when things go back to normal, the whole telehealth industry will become pointless.

I don't think that's the case.

I believe that digital medicine and the presence of virtual health services will become mainstays in our lives—and Teladoc is in an enviable position as one of the pioneers in this disruptive industry that's only starting to take on the healthcare system by storm.

When the pandemic started, it was nearly impossible for most people to gain access to healthcare.

Most patients were scared to travel to the doctor for consultations, causing them to cancel and postpone appointments.

What Teladoc offered is to turn the impossible possible for several patients who needed access to their healthcare providers—and its efforts were rewarded in spades.

In 2019, Teladoc reported $553 million in total revenue, increasing by 32% from its 2018 earnings.

By 2020, the business exploded to reach a whopping $1.09 billion, showing a massive 98% growth year-over-year. Moreover, visits and consultations skyrocketed by 206%.

To hold on to its lead, Teladoc has been working hard to bolster its competitive positioning. It seized a blockbuster acquisition and bought Livongo for $18.5 billion in cash and stock.

Adding Livongo to its portfolio means cornering the market on remote monitoring for patients suffering from chronic diseases.

This addition to its business not only expands Teladoc's business, but also opens a massive addressable market worth $50 billion to the company.

Teladoc can leverage this vast network through cross-selling products and services, thereby creating the Amazon (AMZN) of the healthcare world—a platform with an unbeatable ecosystem and an irresistible value proposition.

Since the merger, the two companies have developed a full-person digital healthcare platform called Primary360.

Meanwhile, Teladoc's growth story carries on, with the total revenue for 2021 already approaching the $2 billion mark.

This signifies an impressive 84% increase on top of the company's COVID-19-induced spurt.

As for 2022, Teladoc is projected to grow at a conservative 29%.

Despite the impressive growth of Teladoc, the company has barely scraped the surface.

Overall, the virtual care market is estimated to be worth $250 billion annually. Although Teladoc holds the most significant share thus far, it's evident that it has less than 1% of the market share.

In fact, the telemedicine industry is projected to be valued at half a trillion dollars globally by 2030.

Considering that Teladoc's yearly revenue thus far is sitting at only $2 billion, the company definitely has a lucrative growth runway in the coming 9 years.

In 2020, its stock price roughly tripled from being under $100 to reaching $300. Recently, though, Teladoc's price has gone down to approximately $130.

Given its obvious room for growth, I say this stock is undervalued. So, investors are granted the chance to add this company to their portfolio at a relatively low price.

With the massive market potential of this industry, it comes as no surprise that Teladoc now faces intense competition in the field.

The strongest rivals of the company in the telehealth segment include Amwell (AMWL), Walmart (WMT), Hims and Hers Health (HIM), and even Amazon.

With the market's sheer size, though, the situation doesn't seem to be a winner-takes-all type.

The space is definitely massive enough to support more than one telehealth company.

However, Teladoc does have the advantage as the first mover. It also has its impeccable partnership with Livongo, making it an anytime-anywhere-healthcare service.

So far, I can say that Teladoc is off to an excellent start in a rapid growth segment. I especially appreciate the company's goal to disrupt the medicine and healthcare space—a field that is in dire need of a revolution to eliminate the debilitating costs and crippling inefficiencies.

More than that, I think Teladoc is becoming instrumental in boosting the reach of the most effective medical professionals and offering a remarkable platform to promote artificial intelligence innovation in healthcare.

When I ran the international equity trading desk at Morgan Stanley during the 1980s, there was always one guy I was trying to recruit and that was David Tepper at Goldman Sachs. Whenever we did a trade with David, we lost money.

If we sold David a stock it usually took off like a rocket. If we bought a stock from him it plummeted like a stone. Eventually, unable to lure David over with a monster salary, I had to ban trading with him as it was such a loser for us.

David never did get pried away from Goldman until he left to start his own firm, Appaloosa Management, after he was mistakenly passed over for partner two years in a row. After that, he racked up an annualized return of over 40%, near my own results.

But David was doing it with $20 billion in real money, while I was doing it with newsletters. In 2012, David received a $2.2 billion performance bonus from his fund, one of the largest in history. I bet the partners at Goldman are kicking themselves.

So, I thought it timely to check in with David, now the owner of the Carolina Panthers football team, to see what he thought about the market. The S&P 500, the Dow, Ten-year bond yields, and Bitcoin all simultaneously hit all-time highs last week, and we were long all of them.

David was phlegmatic at best. “There are times to make money and there are times to not lose money, and this is definitely time to make money.” However, nothing is cheap. There are no screaming buys here or screaming shorts. He did expect stocks to keep rising through the end of 2021.

Keep in mind that David is a trader just like me and rarely has a view beyond six months. His last 13F filing on June 30 showed that his five largest positions were T-Mobile (TMUS), Amazon (AMZN), Facebook (FB), Google (GOOG), and Uber (UBER). Uber was the only new buy.

David is not alone in his views.

Up 89.20% so far in 2021, I am sitting here dazed, shocked, and pinching myself. This has been far and away my best year in a 53-year career. I know a lot of you made a lot more. I stared down every correction this year, loaded the boat, and won.

It’s not always like this.

So I think we are in for a few weeks of profit-taking, sideways chop, and minimal action. I call this the “counting your money” time. Traders have visions of Ferraris dancing in their eyes. Then once we form a new base, it will become the springboard for a new yearend rally.

I don’t think stocks will fall enough to justify selling here. And you might miss the next bottom.

Until then, I’m thinking of taking up the banjo.

That brings me to the foremost question in your collective minds. Can I top an astonishing 100% profit this year? Only if we get another great entry point with a 5% correction.

I’m sure that when the financial history of our era is written something in the future, this will be known as the week that Bitcoin went mainstream. That was prompted by the SEC approval of the first futures ETF, the ProShares Bitcoin Futures ETF (BITO).

By giving this approval, which had been sought for years, unlocks $40 trillion worth of assets owned by 100 million shareholders managed under the Investment Company Act of 1940 to go into Bitcoin. The possibilities boggle the mind. The consensus year-end target for Bitcoin is now $100,000, or up 65%.

It’s not too late to subscribe at the founder's rate of $995 a year for the Mad Hedge Bitcoin Letter by clicking here. After that, the price goes up….a lot.

Morgan Stanley (MS) Announces Stellar Earnings, with profits at $3.71 billion, up 36.4%. Morgan Stanley Asset Management sucked in an amazing $300 billion so far in 2021, bringing their total assets to $4.5 trillion.

Goldman Sachs (GS) announces blockbuster earnings, and we are laughing all the way to the bank. Profits soared an eye popping 63% to $5.28 billion.

Existing Home Sales soar by 7% in September to a seasonally adjusted 6.29 million units. First time buyers accounted for only 28%, the lowest since 2015. A brief drop in interest rates is the reason. There are only 1.29 million homes for sale, only a 2.4 month supply.

Housing Starts fall by 1.6% in September. Higher materials and labor costs, rising land expenses, and soaring energy costs are the culprit. A pop in interest rates may mean that the slowdown could last through the winter.

Single Family Rents are surging especially for the top end of the market. Nationally, rents rose 9.3% in August year over year, up from a 2.2% year-over-year increase in August 2020, according to CoreLogic. Buy homebuilders on dips like (KBH), (LEN), and (PHM)

If the Rescue Package passes in whatever size, it will trigger a massive new surge in risk prices, including stocks and Bitcoin. Don’t act surprised when it happens. $3.5 trillion, $1.5 trillion who cares? That’s a ton of money to be dumped into the economy ahead of the 2022 elections.

Tesla profits smash records in Q3, reporting a shocking $1.62 billion profit on $13.76 billion in revenues. A 30.5% profit margin blew people away. Imagine how much they’ll earn when they make 25 million cars a year in ten years. Buy (TSLA) on big dips.

Weekly Jobless Claims dive to 290,000, a new post-pandemic low. Delta is in fast retreat. A pre-pandemic normal level of 225,000 is coming within range.

Rising Interest rates are tagging the Real Estate Market, with the 30-year fixed rate hitting 3.23%. Refis are off 7% on the week. The Fed taper is looming large, especially if the 30-year hits 4.0%, which it should, taking affordability down. My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

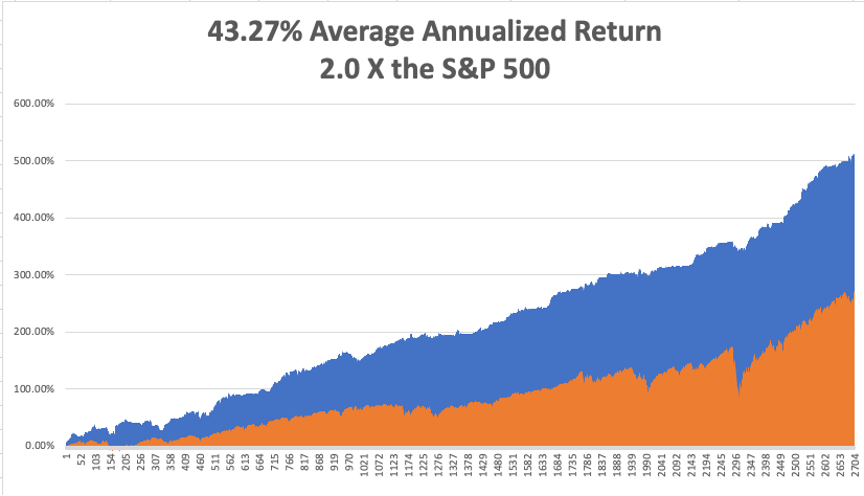

My Mad Hedge Global Trading Dispatch saw a heroic +9.60% gain so far in October. My 2021 year-to-date performance soared to 89.20%. The Dow Average is up 16.60% so far in 2021.

After the recent ballistic move in the market, I am continuing to run my longs and those include (MS), (GS), (BAC), and a short in the (TLT). All are approaching their maximum profit point and we have nothing left but time decay to capture. So, I am going to run these into the November 19 expiration in 14 trading days. It’s like having a rich uncle write you a check once a day.

That brings my 12-year total return to 512.75%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 43.75%, easily the highest in the industry.

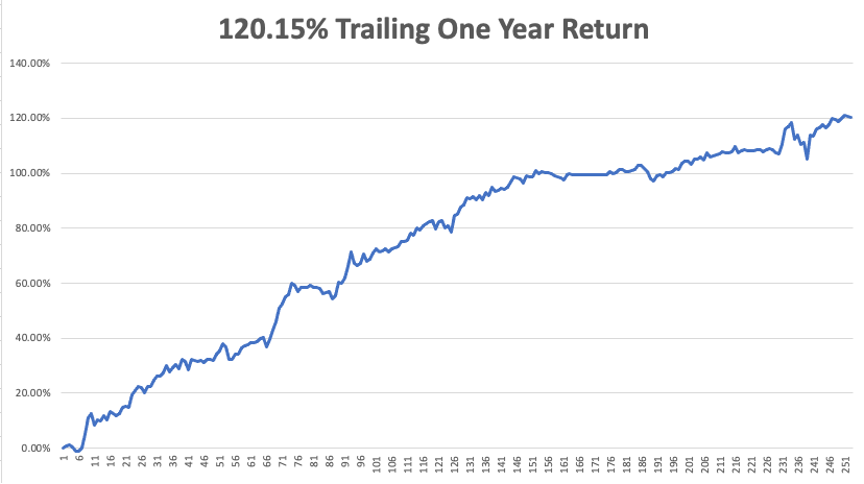

My trailing one-year return popped back to positively eye-popping 120.15%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases approaching 46 million and rising quickly and deaths topping 736,000, which you can find here.

The coming week will be slow on the data front.

On Monday, October 25 at 8:30 AM, the Chicago Fed National Activity Index is out. Facebook (FB) earnings are released.

On Tuesday, October 26 at 10:00 AM, the S&P Case-Shiller National Home Price for August Index is released. Alphabet (GOOGL) and Microsoft (MSFT) earnings are out at 5:00 PM.

On Wednesday, October 27 at 7:30 AM, Durable Goods Orders for September are printed. McDonald’s (MCD) earnings are out.

On Thursday, October 28 at 8:30 AM, Weekly Jobless Claims are announced. The first read on Q3 GDP is announced. Apple (AAPL) and Amazon (AMZN) earnings are out.

On Friday, October 29 at 8:45 AM, the US Personal Income & Spending for September is published. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

As for me, when I went to college in Los Angeles, the local rivalries between universities were intense.

UCLA and USC had a particularly intense rivalry, and I went to both. It was traditional to steal Tommy Trojan’s sword prior to each homecoming game and then paint the statue blue. USC had a mascot, a mixed breed dog called “Old Tire Biter.” Prior to one game, UCLA kidnapped the dog.

At halftime, the kidnappers appeared midfield, tied the dog to a helium-filled weather balloon, and let him waft away somewhere over the city. Enraged USC fans stormed the field only to find that the real dog was hidden in a nearby truck. The dog headed for the stratosphere was actually a stuffed one.

Of course, the greatest prank of all time was carried out by the California Institute of Technology in the 1961 Rose Bowl, which didn’t have a football team, on the Washington Huskies. Washington was famous for its elaborate card tricks, which spelled out team names and various corporate sponsors and images.

On the night before a game, imaginative mathematically-oriented Caltech students snuck into the stadium and changed the instructions on the back of each card packet sitting in the seats. When it came time to spell out an enormous “WASHINGTON”, “CALTECH: displayed instead. The incident was broadcast live on national TV ON NBC.

At Caltech, where I studied math, they are still talking about it today.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/10/caltech-e1635177813242.png301450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-10-25 11:02:252021-10-25 13:20:40The Market Outlook for the Week Ahead, or Taking a Break

Mad Hedge Technology Letter October 13, 2021 Fiat Lux

Featured Trade:

(AMERICA’S NEW SOCIAL CREDIT SYSTEM IS HERE) (ABNB), (PYPL), (FB), (GOOLG), (AMZN)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-10-13 14:04:262021-10-13 17:09:59October 13, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.