Mad Hedge Technology Letter

July 19, 2019

Fiat Lux

Featured Trade:

(CLOUD 101)

(AMZN), (MSFT), (GOOGL), (DOCU), (CRM), (ZS)

Mad Hedge Technology Letter

July 19, 2019

Fiat Lux

Featured Trade:

(CLOUD 101)

(AMZN), (MSFT), (GOOGL), (DOCU), (CRM), (ZS)

Mad Hedge Technology Letter

July 12, 2019

Fiat Lux

Featured Trade:

(CLOUD SECURITY ON THE MARCH)

(OKTA), (ZS), (CRM), (AMZN)

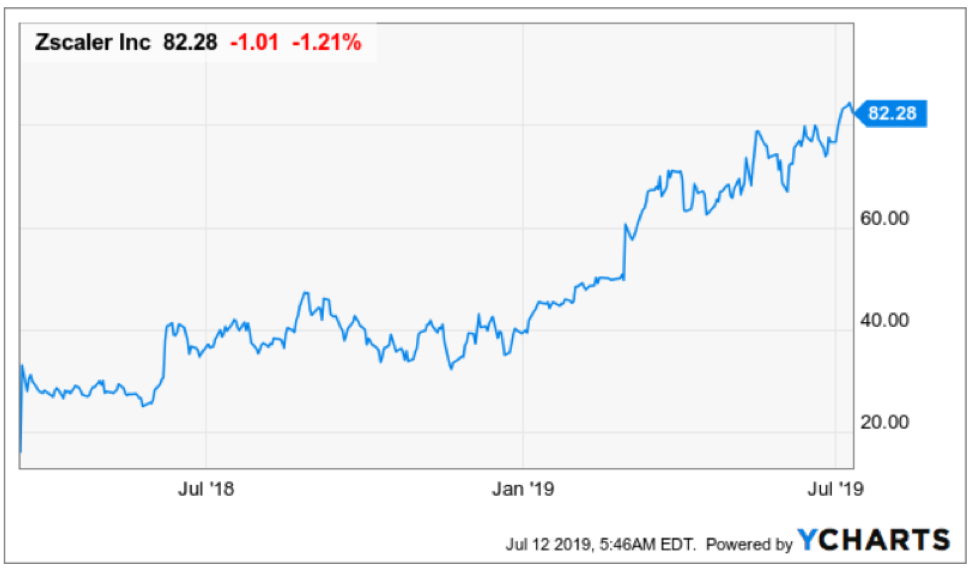

Take a look at these beauties that I recommended at the beginning of December 2018.

At that time, Okta (OKTA) was trading at $62 and Zscaler (ZS) was at $40 on the button – fast forward to today and Okta is now over $136 and Zscaler victoriously sitting at $82.

Oh, how do times change!

That was my reaction watching their performance for the past 7 months giving belief to my assessment that second-tier cloud companies will have a field day this year.

Cloud companies aren’t going away anytime soon, please tattoo that on your forehead.

There isn’t a hotter topic circulating the gossip winds these days than digital security pressured by geopolitics.

Okta is the best in show for identity management – a snazzy term for managing employees’ passwords.

Okta’s products are built on top of the Amazon Web Services cloud.

Coincidentally, Okta was erected in 2009 by a team of former Salesforce (CRM) executives. Salesforce is one of my favorite cloud-based software companies, offering a blueprint for success to other up-and-coming software companies.

Current Okta CEO and founder Todd McKinnon previously served as the Senior Vice President of Engineering at Salesforce.

Other founders include Okta COO Freddy Kerrest who also meandered through the corridors of Salesforce.

I can tell you that you could do much worse than starting a new software company with a collection of Salesforce upper echelon talent.

This all-star team is behind the insatiable growth of Okta whose revenue has grown over 600% since establishing itself.

Okta’s first-quarter results didn’t disappoint with revenues of $125 million—a rise of 50% year-over-year beating the consensus of $117 million.

Subscription revenues comprised 94% of sales and the company expects sales of $130 million amounting to a rise of 37% year-over-year.

Okta’s subscriber base has risen over 500% in the past 5 years and annual contract value of over $100,000 has expanded 60% annually.

The company still loses money but hopes to make some headway on this issue with projected EPS estimated to grow 25% annually in the next five years.

This year spawned a massive divergence between tech who has legs and tech who will be dragged down to the depths of the ocean floor by the heavy weight of regulation, overwhelming competition, or just flat out poor management or inferior product development.

Zscaler echoed similar positive sentiment of Okta by recording a quarter to remember growing revenue by 61% year-over-year while calculated billings grew 55% year-over-year.

In addition to the top line growth, operating margins improved 14% points year-over-year to 8%.

The quarterly results demonstrate the leverage in cloud security business models and the ability to drive growth and profitability.

String together a third consecutive quarter of profitability is just part of the battle, Zscaler will continue to aggressively invest for significant market opportunity that lie ahead.

Cloud security potential means going after a $20.3 billion Total Addressable Market in calendar 2019.

Let me divulge a tad bit about the competitive landscape and why Zscaler is brilliantly positioned for success.

As organizations increasingly make the shift to the cloud, traditional firewall and VPN vendors are finally acknowledging that the legacy security appliances can secure the new digital enterprise and are attempting to build a security cloud using single tenant software designed for on-premise appliances just like you can't create a Netflix service by stacking thousands of DVD players in the cloud.

You can't offer an inline high-performance security cloud by spinning up a bunch of virtual machines in a public cloud. This is a defensive strategy of cloud imitators which, in our view, serves the self-preservation of the vendor, not the needs of the customers.

Zscaler has a significant competitive advantage as a result of the technology, architecture and maturity of cloud security platform including one, Zscaler was born in the cloud, for the cloud just like Salesforce and Workday.

Two, Zscaler has a purpose built globally distributed multi-tenant cloud for fast user experience, unlike imitation cloud, Zscaler requires no back hauling from front doors to a central computing data center of a public cloud.

Three, Zscaler performs SSL inspection at scale as a purpose-built proxy for better security.

Lastly, Zscaler continues to deliver zero trust network access that provides application access without network access reducing business risk unlike firewalls and VPNs.

The duo of Okta and Zscaler are the bright lights of the cloud generation and leading the digital economy in digital security.

Global Market Comments

July 12, 2019

Fiat Lux

Featured Trade:

(THE QUANTUM COMPUTER IN YOUR FUTURE),

(AMZN), (GOOG),

(THE WORST TRADE IN HISTORY), (AAPL)

Global Market Comments

July 11, 2019

Fiat Lux

Featured Trade:

(THE INSIDER’S VIEW ON THE FUTURE OF TECHNOLOGY),

(AMZN), (GOOG), (DELL), (MSFT), (EBAY),

(MY DATE WITH HITLER’S GIRLFRIEND)

How would you like to learn the latest, most important technology trends hitting the global economy today, prepared by one of the most knowledgeable and experienced people in the industry?

It's very simple. Just click on the link below for a wrist-breaking .pdf file packed with 360 slides. It was prepared by my old friend and former Morgan Stanley colleague, Mary Meeker.

Meeker gained fame as the legendary investment banker for technology issues during the Dotcom Boom. She brought to market such blockbusters as Netscape. She also piled investors very early into Amazon (AMZN), Google (GOOG), Dell Computer (DELL), Microsoft (MSFT), and eBay (EBAY) when many of these stocks were trading at single-digit prices. You can understand why she is so popular.

Since 2010, Mary has been with the leading Silicon Valley venture capital firm Kleiner, Perkins, Caufield & Byers. She initially prepared Internet Trends 2018 as a broad ranging 50,000-foot view of technology for her firm. It has since been presented at a number of conferences.

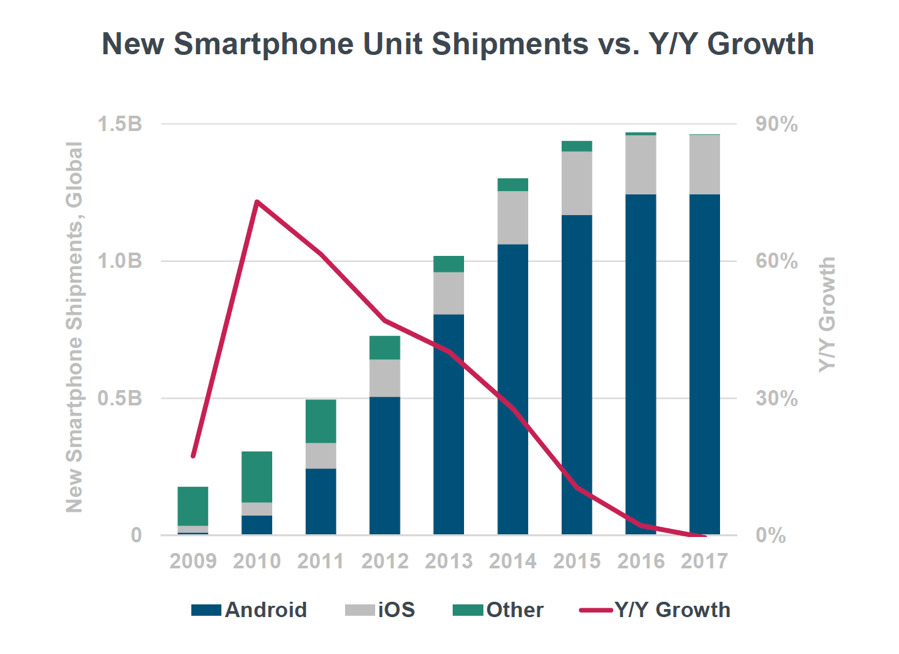

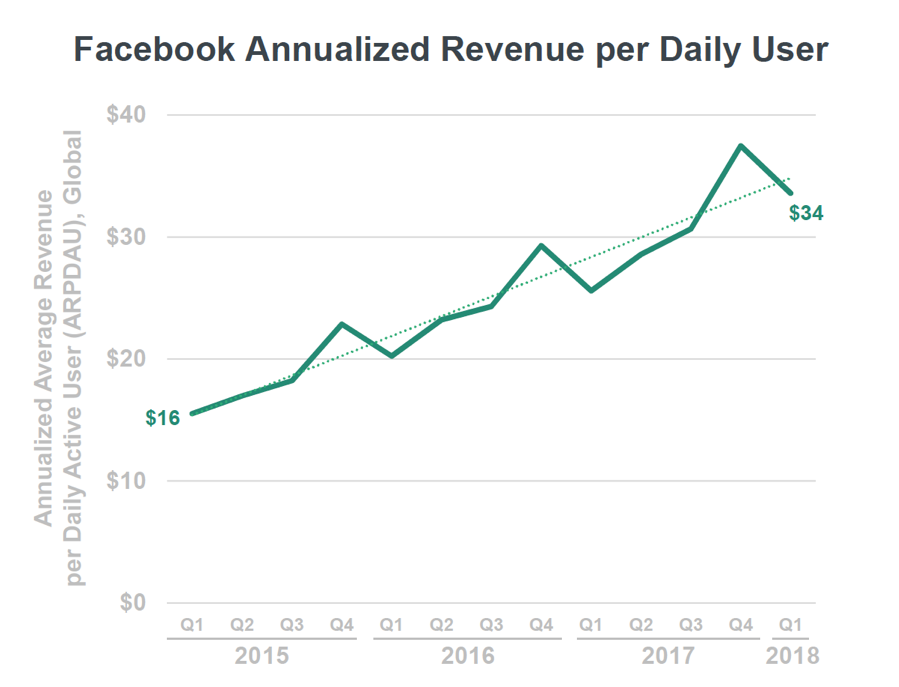

Depending on your interest in technology, you may want to just quickly scroll through the report or analyze each and every single slide. Each slide is a gold mine of information for geeks such as myself. I list a few sample ones below.

The report also gives you some indication of the deep research in which the Diary of a Mad Hedge Fund Trader and the Mad Hedge Technology Letter engage to get you winning Trade Alerts.

To download the report in full please click here.

Enjoy.

Global Market Comments

June 21, 2019

Fiat Lux

Featured Trade:

(MONDAY, JULY 8 VENICE, ITALY STRATEGY LUNCHEON)

(PLAYING THE SHORT SIDE WITH VERTICAL BEAR PUT SPREADS), (TLT)

(WHY TECHNICAL ANALYSIS DOESN’T WORK)

(FB), (AAPL), (AMZN), (GOOG), (MSFT), (VIX)

Global Market Comments

June 14, 2019

Fiat Lux

Featured Trade:

(WEDNESDAY JUNE 26 BRISBANE, AUSTRALIA STRATEGY LUNCHEON)

(MAY 29 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (BYND), (AMZN), (GOOG), (AAPL), (CRM), (UT), (RTN), (DIS), (TLT), (HAL), (BABA), (BIDU), (SLV), (EEM)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader June 12 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Do you think Tesla (TSLA) will survive?

A: Not only do I think it will survive, but it’ll go up 10 times from the current level. That’s why we urged people to buy the stock at $180. Tesla is so far ahead of the competition, it is incredible. They will sell 400,000 cars this year. The number two electric car competitor will sell only 25,000. They have a ten-year head start in the technology and they are increasing that lead every day. Battery costs will drop another 90% over the next decade eventually making these cars incredibly cheap. Increase sales by ten times and double profit margins and eventually, you get to a $1 trillion company.

Q: Beyond Meat (BYND)—the veggie burger stock—just crashed 25% after JP Morgan downgraded the stock. Are you a buyer here?

A: Absolutely not; veggie burgers are not my area of expertise. Although there will be a large long-term market here potentially worth $140 billion, short term, the profits in no way justify the current stock price which exists only for lack of anything else going on in the market. You don’t get rich buying stocks at 37 times company sales.

Q: Are you worried about antitrust fears destroying the Tech stocks?

A: No, it really comes down to a choice: would you rather American or Chinese companies dominate technology? If we break up all our big tech companies, the only large ones left will be Chinese. It’s in the national interest to keep these companies going. If you did break up any of the FANGS, you’d be creating a ton of value. Amazon (AMZN) is probably worth double if it were broken up into four different pieces. Amazon Web Services alone, their cloud business, will probably be worth $1 trillion as a stand-alone company in five years. The same is true with Apple (AAPL) or Google (GOOG). So, that’s not a big threat overhanging the market.

Q: Is it time to buy Salesforce (CRM)?

A: Yes, you want to be picking up any cloud company you can on any kind of sizeable selloff, and although this isn’t a sizeable selloff, Salesforce is the dominant player in cloud plays; you just want to keep buying this all day long. We get back into it every chance we can.

Q: Do you think the proposed merger of United Technologies (UT) and Raytheon (RTN) will lower the business quality of United Tech’s aerospace business?

A: No, these are almost perfectly complementary companies. One is strong in aerospace while the other is weak, and vice versa with defense. You mesh the two together, you get big economies of scale. The resulting layoffs from the merger will show an increase in overall profitability.

Q: I had the Disney (DIS) shares put to me at $114 a share; would you buy these?

A: Disney stock is going to go up ahead of the summer blockbuster season, so the puts are going to expire being worthless. Sell the puts you have and then go short even more to make back your money. Go naked short a small non-leveraged amount Disney $114 puts, and that should bring in a nice return in an otherwise dead market. Make sure you wait for another selloff in the market to do that.

Q: What role does global warming play in your bullish hypothesis for the 2020s?

A: If people start to actually address global warming, it will be hugely positive for the global economy. It would demand the creation of a plethora of industries around the world, such as solar and other alternative energy industries. When I originally made my “Golden Age” forecast years ago, it was based on the demographics, not global warming; but now that you mention it, any kind of increase in government spending is positive for the global economy, even if it’s borrowed. Spending to avert global warming could be the turbocharger.

Q: Why not go long in the United States Treasury Bond Fund (TLT) into the Fed interest rate cuts?

A: I would, but only on a larger pullback. The problem is that at a 2.06% ten-year Treasury yield, three of the next five quarter-point cuts are already priced into the market. Ideally, if you can get down to $126 in the (TLT), that would be a sweet spot. I have a feeling we’re not going to pull back that far—if you can pull back five points from the recent high at $133, that would be a good point at which to be long in the (TLT).

Q: Extreme weather is driving energy demand to its highest peak since 2010...is there a play here in some energy companies that I’m missing?

A: No, if we’re going into recession and there’s a global supply glut of oil, you don’t want to be anywhere near the energy space whatsoever; and the charts we just went through—Halliburton (HAL) and so on—amply demonstrate that fact. The only play here in oil is on the short side. When US production is in the process of ramping up from 5 million (2005) to $12.3 million (now), to 17 million barrels a day (by 2024) you don’t want to have any exposure to the price of oil whatsoever.

Q: What about China’s FANGS—Alibaba (BABA) and Baidu (BIDU). What do you think of them?

A: I wanted to start buying these on extreme selloff days in anticipation of a trade deal that happens sometime next year. You actually did get rallies without a deal in these things showing that they have finally bottomed down. So yes, I want to be a player in the Chinese FANGS in expectation of a trade deal in the future sometime, but not soon.

Q: Silver (SLV) seems weaker than gold. What’s your view on this?

A: Silver is always the high beta play. It usually moves 1.5-2.5 times faster than gold, so not only do you get bigger rallies in silver, you get bigger selloffs also. The industrial case for silver basically disappeared when we went to digital cameras twenty years ago.

Q: Does this extended trade war mean the end for emerging markets (EEM)?

A: Yes, for the time being. Emerging markets are one of the biggest victims of trade wars. They are more dependent on trade than any of the major economies, so as long as we have a trade war that’s getting worse, we want to avoid emerging markets like the plague.

Q: We just got a huge rebound in the market out of dovish Fed comments. Is this delivering the way for a more dovish message for the rest of the year?

A: Yes, the market is discounting five interest rate cuts through next year; so far, the Fed has delivered none of them. If they delayed that cutting strategy at all, even for a month, it could lead to a 10% selloff in the stock market very quickly and that in and of itself will bring more Fed interest rate cuts. So, it is sort of a self-fulfilling prophecy. The bottom line is that we’re looking at an ultra-low interest rate world for the foreseeable future.

Good Luck and Good Trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

June 10, 2019

Fiat Lux

Featured Trade:

(JUNE 21 AUCKLAND NEW ZEALAND STRATEGY LUNCH)

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR THE GRAND PLAN)

(MSFT), (GOOGL), (AMZN), (TESLA), (TLT), ($TNX)