YouTube has to be the online streaming asset of the year even relegating Netflix (NFLX) to the minor leagues – I’ll tell you why.

India is the new China.

Netflix’s growth strategy is intertwined with India and the management has been extraordinarily vocal about their interests there.

The Indian online streaming renaissance isn’t just fueling Netflix’s rise. In fact, YouTube and its free platform are performing miracles along the Ganges River.

How big is YouTube in India?

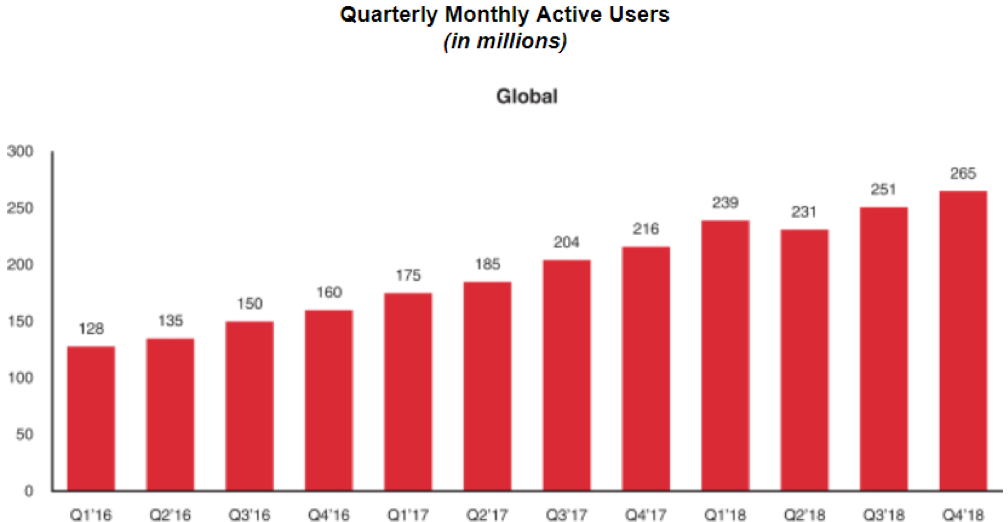

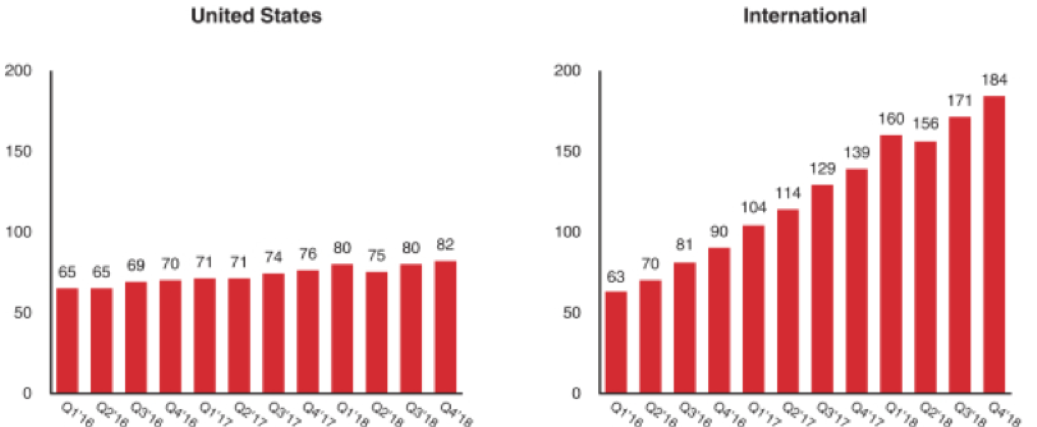

YouTube already has 245 million monthly active users in India penetrating 85% of the country’s internet population making India one of its best-performing markets.

The company says more than 60% of its streaming hours in India come from outside the six metros, meaning YouTube has captured the hearts and minds of the rural population who cannot afford to pay for online content.

KPMG forecasts India’s online streaming audience to surpass 550 million by 2023 and YouTube will capture 70% of the 550 million audience.

How did YouTube manage to do this?

First, the content is free with ads allowing rural Indians to join in.

Second, local Indians became hooked on Alphabet’s YouTube with Alphabet (GOOGL) taking an already brilliant platform and supercharged it by tailoring it to popular local influencers that are joining in droves inciting a massive network effect.

Effectively, YouTube attracted these influencers with eye-popping audiences to create organic and original content without the $8 billion Netflix planned content budget in 2019.

YouTube was able to do this by borrowing the Instagram format but transferring it to a more effective video platform model.

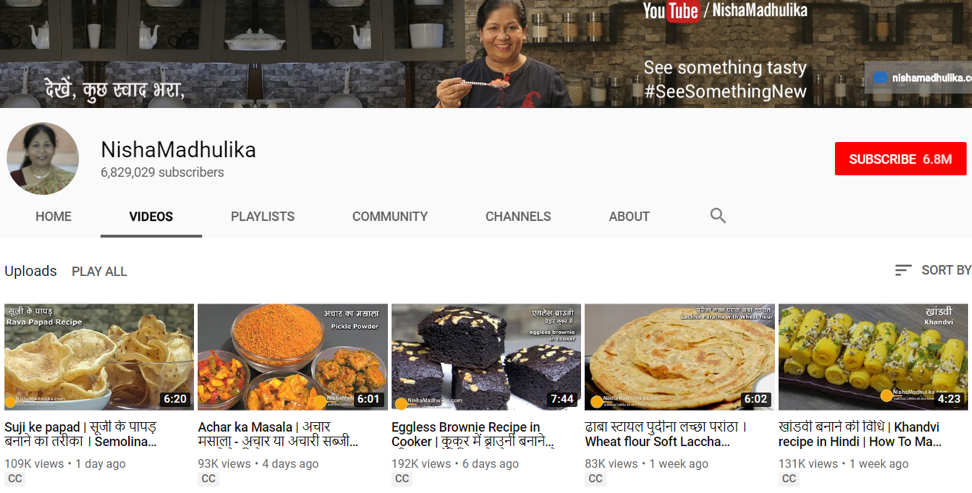

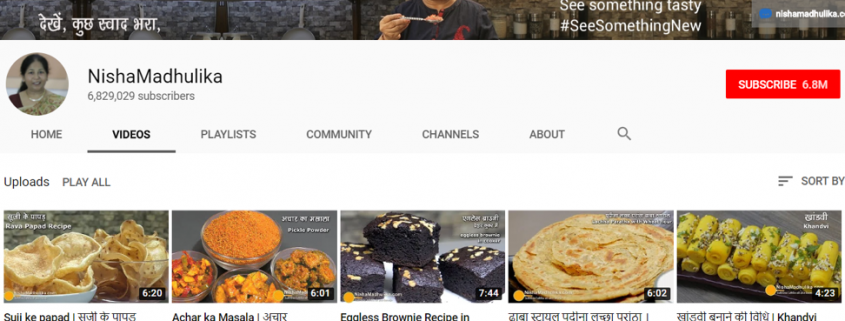

Take for instance Nisha Madhulika whose channel has blossomed into one of the most popular Hindi language-based online cooking channels on the internet.

To see one of her videos, please click here.

Her channel has over 6.8 subscribers, yet, accumulating subscribers is one thing, and making money is another.

Past videos that were posted around 2-3 weeks ago have views between 200,000 to 400,000.

These influencers build up revenue by displaying 3rd party ads generated by Alphabet.

A general rule of thumb is that for every 1 million view, ad revenue collected is around $2,000.

Therefore, Nisha and fellow YouTubers with massive audiences are incentivized to pump out high-quality content in high volume.

Scrolling through her numbers, Nisha appears to average around $700 of revenue per video.

She sprinkles in the occasional viral video that garners 1.5 million views which would earn her a tidy $3,000 for a single video.

Not bad and that is before any of the possible marketing opportunities are quantified.

As long as she focuses on the quality of the videos, she can consistently earn $700 per video, then she can do more by partnering with affiliates to sell 3rd party products and receive a commission that is trackable through the links she leaves at the bottom of her videos.

Nisha’s video business works like this, her channel entails producing 3-5 short videos per week producing around 9-11 million views per month adding up to between $18,000-$22,000 in revenue per month.

Remember that while she is accumulating views for newly posted videos, there are still viewers rummaging through her older content demonstrating the beauty of the network effect.

Older videos in Nisha’s case usually add an extra $3,000-$5,000 per month to the bottom line in pure profit.

Many influencers curate, edit, design, and film the content themselves, or subcontract these jobs for a cheap fee.

An influencer could run their YouTube channel for less than $100 per month minus the fees for the equipment.

YouTube has created a powerful platform for content creators to monetize their original content and give them incentives to stick around and build a business.

Netflix has more of a mercenary model where they contract highly paid actors to contribute a finite amount of content for a fee.

YouTube’s model penetrates to the heart of the average person with regular people instead of propping up overpaid Hollywood actors like Netflix.

In many cases, YouTube’s influencers offer live, raw, and personal access, and the data suggests that live, unscripted content are one of the most monetizable types of content on the market due to its original nature and unpredictability.

That is why live sports like the NFL and NBA are easy to sell, monetize, and in great demand.

I do believe that Netflix has a great product but overpaying for Hollywood’s best talent is not sustainable because the cost-benefit ratio isn’t worth it, which is why Netflix is raising customer prices to monetize the quality of streaming content better.

With other big tech players coming into the market, it will push up the costs for Hollywood talent putting more short-term pressure on their financial model.

Even if Netflix does get the right actors to provide content, they do have their fair share of bad movies.

YouTube’s performance in India will be hard to compete with, even harder when they avoid expensive mistakes, a bad video is simply glossed over and ignored.

Netflix is in the midst of testing a mobile-only Indian subscription package for around $3.64 per month, or 250 Indian rupees, to respond to YouTube’s godlike presence there.

Remember that most rural Indians do not have access to hardware such as computers, laptops, or tablets, and run their lives with cheap Chinese smartphones from Oppo and Vivo.

If you thought $3.64 was a cheap streaming package, then Amazon (AMZN) takes it one step further by offering Amazon prime video for $1.88 per month or 129 Indian rupees.

I like Netflix’s product and the narrative is still intact, but I adore and love YouTube’s transformation that has caught many of us by surprise.

This massive shift wouldn’t be possible without Google’s army of best of breed ad tech.

Even more poignant, YouTube takes direct to consumers to a rawer entry point enhancing the special experience.

The problem with Hollywood talent is that reformulating them onto Netflix’s platform brings them closer to the audience to a certain degree, but not like Nisha’s cooking channel where she can speak directly to the viewer and even interact with her audience in the comment section.

YouTube has mastered this relationship between content creator and audience, and no matter how many times I watch Will Smith’s Bright, I can’t expect him to reply to my comments.

Well, there’s not even a comment section on Netflix’s platform.

In short, Netflix’s Indian strategy is incomplete and I predict that YouTube will extend its lead there because the scalability is well-suited for the Indian rural audience who have little or no discretionary income.

The freemium model wins out again.

Affixing a Netflix grade streaming asset to Alphabet’s booming digital ad business is a match made in heaven.

Buy Alphabet on the dip – YouTube’s outperformance in 2019 will surpass expectations and carry Alphabet shares to new all-time highs this calendar year.