He is at it again.

No, not Elon Musk, but Andy Rubin – the Godfather of the Android operating system could create another ground-breaking shift in the world of technology.

Apple’s (AAPL) iOS system was the leader of the pack until Rubin’s timely intervention.

When Apple debuted the iPhone and, shortly after, the Apple app store, there was nothing remotely comparable at the time.

The roaring success of the iPhone and its app store could have been so much more to the global smartphone audience if it consumed everybody.

You could smell broad-based world domination, but it never materialized.

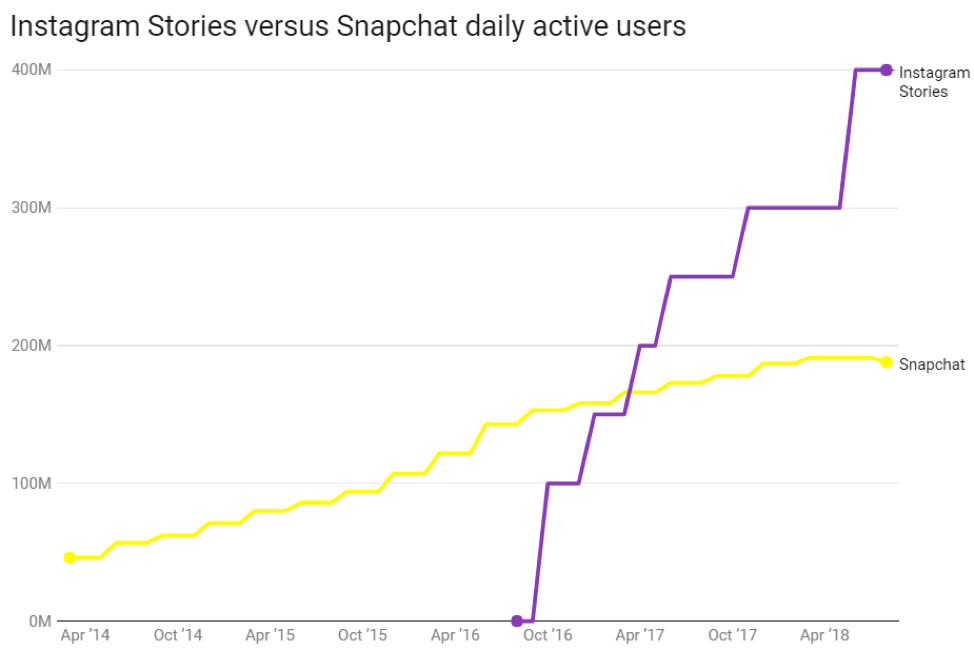

Android now has 85% of the global smartphone market share, and Apple has carved out the last 15% albeit in the high-income markets.

You can thank Microsoft (MSFT) for all of this – let me explain.

Android was hands down the best purchase ever made by Google for a paltry sum of just $50 million.

It was in 2005 when Android was bought by Google and Rubin’s work commenced overseeing the construction of a platform that could avoid licensing restrictions dragging down the industry.

Android was initially commissioned by Google to build a platform to stymie another potential Microsoft monopoly, but this time, in the mobile space.

Google didn’t want to be blown away by Microsoft as the pivot to mobile was picking up steam.

Google assumed that Microsoft had the best chance to execute the shift to mobile because of the universal acceptance of the Windows operating system.

And little did they know that Steve Jobs had a game changer up his sleeve when he rolled out the iPhone.

The premise was very simple for Android - offer supreme customer value, massively scale a global platform, and catalyze explosive growth.

Easier said than done.

In the end, Rubin was able to generate a blanketed adoption of the Android operating system in smartphones.

Apple has been, by and large, the victor of hardware because even though the Android system is more popular, the manufacturer of Android-based phones cuts across a broad swath of different international companies from Google itself to Samsung, LG, and the various Chinese makers.

Around half of Americans are proud to be an iPhone owner and Apple was able to ensure they were the only manufacturer of their proprietary iOS system harvesting all the profits.

Onlookers aren’t giving Android the credit it duly deserves in the global scheme of things.

Fortunately for Google and Rubin, Microsoft CEO Steve Ballmer fudged his opportunity while Palm, Symbian, and BlackBerry never stuck around either for recorded posterity. It could of easily have gone the other way.

Android has become so entrenched in non-iPhone smartphones that Google was fined $5 billion for being too dominant in Europe or for what regulators tout as illegally cementing their position. The battle is still going on in court with a final verdict coming shortly.

What does Rubin have on the menu this time?

After establishing his own private company to battle the tech Goliaths, he built an initial smartphone that was an unmitigated flop.

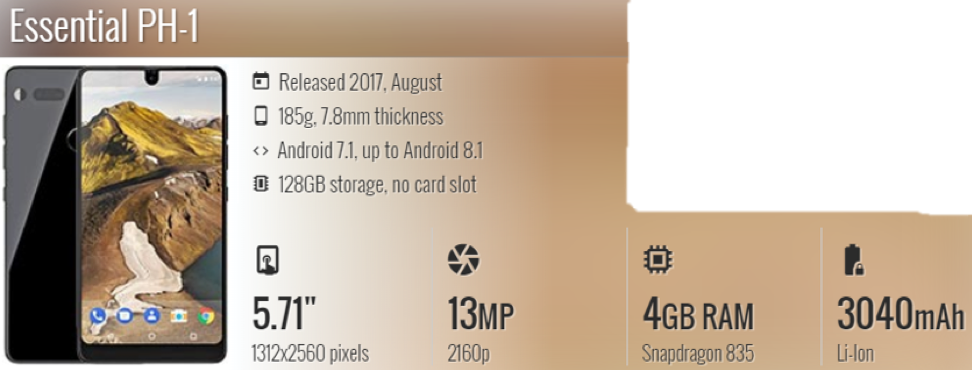

The Essential PH-1 smartphone offered a stock Android experience meant to appeal to the medium-tiered smartphone market.

The phone had solid hardware, enough juice in it to be competitive, a poor camera, and it did little to stand out from the crowd. There are many other cheaper substitutes with better brand recognition selling similar enough devices.

In general, it is a passable smartphone, but the initial price point was a reach in this ultra-competitive climate.

Sales were an outsized bust barely able to penetrate the American smartphone market.

Sprint offered the phone for $699 and registered 5,000 sales in the first month.

To put it into perspective, Apple routinely sells 40 or 50 million smartphones per quarter.

The Essential phone was discounted down to $499 in an attempt to salvage revenue. That didn’t work either.

You can now buy the phone on Amazon.com (AMZN) for $378.

All told, the phone did about 150,000 in sales and Rubin needed to rethink his vision.

Even as recently as this spring, takeover rumors swirled because of Essential’s stable of engineering firepower.

The vultures never swooped and Essential is back with a vengeance building their second phone - Essential Phone PH-2

To stem the tide and make their mark in the smartphone industry, Rubin decided Essential needed a fresh strategy requiring immense chutzpah.

Smartphones have essentially become commoditized in the mid-tier range and consumers look for the best specs at the lowest price point. Samsung has made a living picking off this type of buyer.

Rubin decided to align his future product with the technology that will change the world – artificial intelligence.

Artificial intelligence will be incorporated into the design for the phone to work for the user without him using it.

Yes, that’s right, the user will not have to even have his paws on the phone. The artificial intelligence will mimic the user’s behavior and carry out its functions and tasks alone.

Rubin said, “You can be off enjoying your life, having that dinner without touching your phone and you can trust your phone to do things on your behalf.”

This audacious strategy is a risky bet that consumers will be comfortable enough with artificial intelligence to allow them to venture out alone into this complicated world with no checks and balances from the user themselves.

Imagine some catastrophic scenario if the artificial intelligence taps into a user’s bank account and begins deploying hard-earned capital to exotic locations all over the world.

Smartphone competition has effectively made smartphones widely available for most of the world, but cultivating a smartphone company from scratch requires a dose of creative intuition.

Betting on the development of artificial intelligence is one of the few weapons in Rubin’s toolkit.

This could be Rubin’s last attempt at a smartphone and moving further out onto the risk curve means this could be a whale of a failure or a spectacular success. I can’t imagine his investors allowing him to produce another failed smartphone.

My bet is that consumers aren’t ready to absorb the type of levels of artificial intelligence that Rubin hopes to infuse into his new phone.

Even if he lays an egg, he will be back on another project in no time. That is the sort of slack you get by being the godfather of the Android operating system. Funding is as lush as a tropical forest.

Secretly, I want him to succeed because the world needs positive disruption to the Silicon Valley cohort of megacompanies from independent sources.

My bet is that a smartphone will not be the revolutionary new product the world is clamoring for. It’ll be something we have never seen before.

Please click here to visit Essential’s website.

A GOOD PHONE BUT TOO SIMILAR TO THE REST