Financial markets have been incredibly volatile in the past months primarily due to the COVID-19 pandemic.

The situation was made even more unpredictable by the GameStop (GME) and bitcoin drama.

So it’s expected that investors are looking for guidance in this time of instability, and a good place to start is the Blackstone Group (BX).

Considering that the basic philosophy of this company is to “buy, fix, and sell,” it’s safe to say that Blackstone only puts its money, time, and effort in promising investments.

Around the time of the pandemic outbreak last year, Blackstone poured in roughly $2 billion investment in a biopharmaceutical company, Alnylam Pharmaceuticals (ALNY).

While Alnylam may be virtually unknown to the public, this is actually a promising company with an impressive backstory.

Founded in 2002, Alnylam is mainly known for its technology, RNAi or RNA interference.

This is a gene-silencing technique, which was discovered by Andrew Fire and Craig Mello back in 1998. The two won the Nobel Prize for it in 2006.

Even before the Nobel, Alnylam has already seen the potential of this technology and started developing it in the early 2000s.

For decades, this work had been underappreciated—up until the COVID-19 pandemic.

This is because the leading vaccine candidates right now, developed by Pfizer (PFE)-BioNTech (BNTX) and Moderna (MRNA), are both mRNA-based drugs.

Although the vaccine developers customized the technology, they still used the same delivery technique that Alnylam developed.

Clearly, there has been a lot of piggybacking on this discovery.

While Moderna, Pfizer, and BioNTech used the technology to create RNA-based drugs for the COVID-19 vaccines, Alnylam decided to utilize it to develop treatments for other diseases.

The first approval was hereditary transthyretin-mediated amyloidosis drug Onpattro, launched in 2018.

As of 2020, sales of this high-priced therapy reached roughly $300 million, ensuring that it was on pace with the company’s target.

Alnylam’s second approved treatment is ultra-rare genetic disease drug Givlaari, which hit the market early last year.

By the third quarter of 2020, sales of this acute hepatic porphyria drug climbed by $67 million despite the effects of the pandemic.

In the next decade, Givlaari is estimated to peak at $550 million annually.

By 2025, yearly sales for Givlaari and Onpattro are projected to hit roughly $1.5 billion in total.

Riding this momentum, Alnylam has been collaborating with Sanofi (SNY) to develop another rare disease drug, Vutrisiran. This could rival the company’s own Onpattro.

Aside from Vutsiriran, Alnylam and Sanofi are also working on a potential novel hemophilia treatment, Fitusiran.

The latest treatment to gain approval is rare kidney disorder drug Oxlumo, which is estimated to net Alnylam roughly $380,000 per patient annually.

While this may be a hefty price tag, it’s expected that insurance companies and governments will be the ones to ultimately shell out the money for these rare disease drugs.

Before 2021 ends, Alnylam is expected to gain FDA approval for another potential blockbuster drug, Inclisiran. This is a cholesterol-fighting treatment, which is a work in progress with Novartis (NVS).

Over the past decade, Blackstone has been quietly stashing multi-billion-dollar stakes in the life sciences.

In 2020 alone, the company poured roughly $16 billion into the industry. This is its largest investment theme for the entire year.

While this business has yet to make a dent on Blackstone’s $600 billion assets, the attention that the companies have been getting is worth noting—and a good place to start is Alnylam.

For a better context of its potential, Blackstone invested $3 billion in a dating app called Bumble (BMBL) back in 2018.

Fast forward to 2021, this company is now worth approximately $14 billion following its recent IPO.

With a market capitalization of roughly $15 billion and for a company that’s not anticipated to generate over $1 billion in annual revenue until 2022, Alnylam’s current price might be considered high by some investors.

Looking at its pipeline though, which is filled with potential blockbusters, and its track record that shows that the company definitely knows how to launch new drugs to the market, I believe Alnylam stock is worth considering right now.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-25 15:00:332021-03-02 16:54:57An Under the Radar Biopharma Play

I know you’re not going to want to hear this. I might as well be trying to pull your teeth, lead you down a garden path, or sell you a high-priced annuity.

But there is nothing to do in the market right now. Nada, diddly squat, bupkis, and for all you Limey’s out there, bugger all.

For during the first six weeks of 2021, we have pretty much squeezed all there is out of the market.

Not only did we nail the timing and the direction, we also got the lead sectors, financials, brokers, chips, and short bonds (MS), (GS), (BLK), (AMD). We also chased the Volatility Index (VIX) down from $38 to a lowly $20, baying and protesting all the way.

That enabled us to extract a 28.29% profit so far in 2021, the best return in the 13-year history of the Mad Hedge Fund Trader. The only other time you see numbers this high is when Ponzi schemes get busted. And not a dollar of this was earned from the really marginal plays like Bitcoin, SPAC’s, GameStop (GME), or pot stocks.

If I feel like I did a year’s worth of work during the first seven weeks of 2021, it’s because I have, issuing 60 trade alerts since January 1.

However, bonds (TLT) are reaching the end of their current leg down. The 1.34% yield we saw on Friday is suspiciously close to the 1.36% yields we saw during the 2012 and 2017 market double bottom.

So, there may be some wood to chop around these, levels, possibly for weeks or months.

This is important because a collapsing bond market has been the principal driver of the winning trades of 2021, such as in banks, brokers, money managers, and other domestic recovery plays.

And when one side of the barbell goes dead, what do you do? You buy the other side. FANGs are just completing a six-month “time” correction where they have gone absolutely nowhere. So, Facebook (FB), Amazon (AMZN), and Apple (AAPL) may be getting ready for a roll.

One other sector that might keep running is the SPDR Mining & Metals ETF (XME), and Freeport McMoRan (FCX). That’s because it's not just us buying metals to front-run a recovery, it’s the entire world. What do you think a $2 trillion infrastructure budget will do to this area?

New lows for bonds, as the ten-year US Treasury yield hits 1.26%, up 38 basis points since January 1 and a one-year high. 1.50% here we come! Ever hear the expression “Don’t fight the Fed”? All financials are off to the races, where we were 60% long. Biden’s $1.9 trillion rescue package will be 100% borrowed and take total US borrowing to a back-breaking 55% of GDP. I hate to sound like a broken record but keep selling rallies in the (TLT), buy (JPM), (BAC), (GS), (MS), and (BRK/B) on dips.

Volatility index hit a one-year Low, which is what you’d expect at the dawn of a decade-long bull market in stocks. The (VIX) may flat line here for a while before the next out-of-the-blue spike.

The Nikkei Stock Average topped 30,000, for the first time in 31 years, Yes, it’s been a long haul. I was heavily short in the initial 1990 meltdown from 39,000 to 20,000 and many fortunes were made. The top marked the end of the Japanese company’s ability to copy their way into leadership. After that, rapidly advancing technology made copying too slow to compete in a global economy.

A midwest storm upended energy markets, with oil popping $8 to $67 and gas deliveries spiking from $4 to $999. It would have gone higher, but the software only provided for three digits. Electricity prices are all over the map. Some 4 million Texas customers are without power. Fracking has ground to a halt. Windfarms are frozen solid. If you are a net producer (as I am), you are in heaven. The turmoil is expected to be gone by the weekend. It’s another high price paid for ignoring global warming.

Weekly Jobless Claims soared, to 861,000, casting a dark cloud over the economic recovery. The news took a 300-point bite out of the Dow. Illinois and California saw the biggest gains. We are not out of the woods yet.

SpaceX was valued at $74 Billion, according to an $850 billion venture capital fundraising round this week. However, Elon Musk’s rocket company won’t go public until men are landed on Mars. The company is also the launching pad for its Starlink global WIFI project, which will cost at least $10 billion to build out. Blowing up rockets is not a good backdrop for an IPO.

Cash is still pouring off the sidelines, with equity mutual funds attracting some $7.8 billion last week. As long as this is the case, which could be for years, any market corrections will be limited. Strangely, bond funds are still pulling in money too, some $5.7 billion. It’s called a liquidity-driven market, silly!

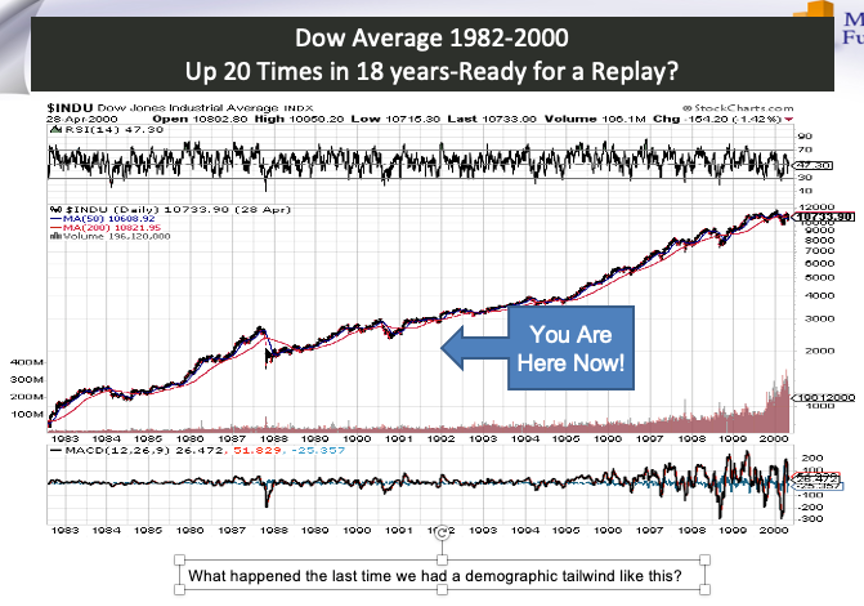

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch earned an amazing 17.27% so far in February after a blockbuster 10.21% in January. The Dow Average is up a trifling 2.92% so far in 2021.

This is my fourth double-digit month in a row. My 2021 year-to-date performance soared to 27.28%. After the February 19 option expiration, I am now 80% in cash, with a single long in Tesla (TSLA) left.

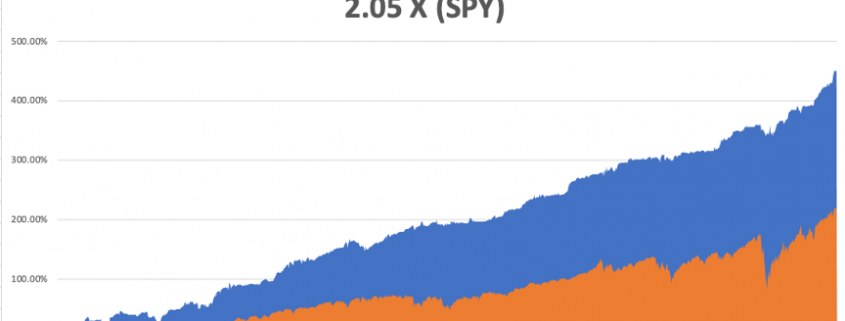

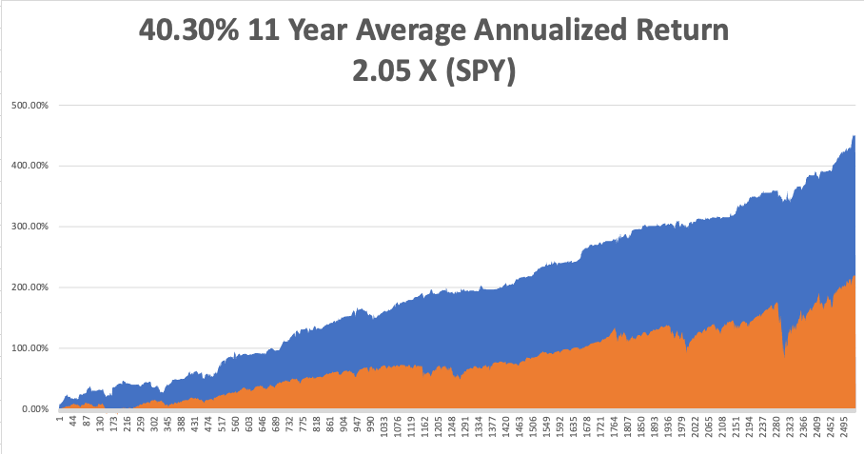

That brings my 11-year total return to 450.03%, some 2.05 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an Everest-like new high of 40.30%.

My trailing one-year return exploded to 94.09%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 109.00% since the March 20, 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 28 million and deaths approaching 500,000, which you can find here. We are now running at a heart breaking 3,000 deaths a day. But that is down 35% from the recent high.

The coming week will be a boring one on the data front.

On Monday, February 22, at 8:30 AM EST, the Chicago Fed National Activity Index is out. Zoon (ZM) reports.

On Tuesday, February 23 at 9:00 AM, the S&P Case-Shiller National Home Price Index for December is announced. Square (SQ) and Intuit (INTU) report.

On Wednesday, February 24 at 8:30 AM, New Home Sales for January are printed. NVIDIA (NVDA) reports.

On Thursday, February 25 at 9:30 AM, Weekly Jobless Claims are printed. US Durable Goods for January and Q4 GDP are out. Salesforce (CRM), (Moderna (MRNA), and Airbnb (ABNB) report.

On Friday, February 26 at 8:30 AM, US Personal Income and Spending are published. DraftKings (DKNG) reports. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, if you want to see what it is like to work at Amazon, watch the movie Nomadland. It’s an artsy Francis McDormand film made with a $4 million budget about the end of life, which I caught over the weekend on Hulu.

It covers a contemporary trend in US society where retirees with no savings move into RVs and live off the grid, working occasionally to earn gas money. They raved about it in Europe.

If I don’t keep those trade alerts coming, that could be me in a couple of years.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/11yr-feb22.png454864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-22 09:02:012021-02-22 10:23:06The Market Outlook for the Week Ahead, or Time for a Break

The fuss over GameStop (GME) has aimed the spotlight on several small- and even mid-cap stocks that hold a high level of short interest.

For quite some time now, retail investors have been identifying others with similar qualities as GME: a short interest standing at more than 20% of the total float, a market capitalization above $1 billion, and a stock price of roughly $20 per share or even less.

Now, these traders have turned their attention to the biotech industry and one stock that caught their attention is Sorrento Therapeutics (SRNE).

In 2020, Sorrento was hailed as one of the hottest COVID-19 stocks as it jumped an impressive 135% since the year started.

However, the hype dissipated quickly, with the stock falling almost 50% by August that same year.

The company’s volatility was expected considering Sorrento’s early entry, but delayed progress in the COVID-19 race.

As 2020 rolled out, investors started ditching the stock in favor of other developers like Moderna (MRNA), Pfizer (PFE), BioNTech (BNTX), Novavax (NVAX), and AstraZeneca (AZN).

Come 2021, however, the stock seems to bounce back.

Sorrento’s shares have been climbing since the year started following the company’s encouraging data on COVI-MSC, which is its entry in the race to find a potent COVID-19 treatment.

COVI-MSC works as a stem cell treatment developed for COVID-19 patients suffering from acute respiratory distress.

Based on its report in January, Sorrento disclosed that the first three individuals who went through their COVI-MSC treatment were discharged from the hospital within only a week.

Meanwhile, the fourth patient, the one who needed mechanical ventilation due to deteriorating respiratory condition, experienced rapid improvement of his condition and was discharged from the hospital the night of his third COVI-MSC infusion.

On a more promising note, none of the patients experienced any adverse effect following their COVI-MSC treatment.

Outside its COVID-19 treatment program, this San Diego-based biotechnology company has been working on therapies for cancer, neurodegenerative, autoimmune, and inflammatory conditions.

It has multiple “shots on goal” particularly in the oncology department, with its non-small cell lung cancer treatment Abivertinib as the leading candidate to date.

Sorrento’s pain management pipeline, which is headlined by Ztildo, is ripe for expansion thanks to its strategic collaboration with SCILEX.

The company also has its hands in other high-growth sectors in the biotech world, paying particular attention to non-opioid pain relief and immunotherapy.

These projects indicate that Sorrento is no one-trick pony.

In fact, even if its COVID-19 program falls flat – a very real possibility considering that COVI-MSC still needs to go through multiple trials – Sorrento has several initiatives to fall back on.

With three shots on goal, namely, its COVID-19 program, its oncology platform, and non-opioid pain treatment, Sorrento has ensured that it’s well-positioned for success.

If approved, Sorrento’s current pipeline comprising diagnostic kits and therapies could generate over $2 billion in short-term sales.

At the moment though, Sorrento’s $4.02 billion market capitalization makes it a tiny biotechnology company compared to its competitors.

Given its robust pipeline, it’s evident that Sorrento still needs to boost its capitalization to push through with all the plans.

For context, its most dominant rival in the COVID-19 treatment market is Gilead Sciences (GILD), which has $84.38 billion in market capitalization, rakes in $800 million each quarter from sales of Remdesivir.

Let’s say Sorrento expands to the vaccine market, it still cannot catch up with the leader in that arena, Moderna (MRNA), which has $70.97 billion in market capitalization.

Looking at Sorrento’s performance, this company remains an underappreciated stock loaded with potential.

From a business perspective, Sorrento offers a solid pipeline of candidates that could present promising results to push the stock price up.

At this point, the positive updates on its COVID-19 program can cause the stock price to rise exponentially, putting short sellers looking in an unfortunate position.

Overall, Sorrento has the potential to double in value. However, bear in mind that it still has a long way to go. Hence, this company is best as a long-term investment.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-16 15:00:562021-02-18 22:07:52Short-Squeeze Drama: Biotech Edition

We just completed the best week in the 13-year history of the Mad Hedge Fund Trader.

Kudos have been coming in from all over the world, with stories of retirements financed, mortgages paid off, and college educations paid for. Some Mad Hedge Concierge clients are reporting windfall profits of $1 million a day.

The key was calling the GameStop (GME) fiasco the one hit wonder that it was, and using it as an opportunity to go 100% long, pedal to the metal, and bet the ranch. When the market gives you a gift, you grab it with both hands as if your life depended on it and don’t let go.

It worked.

That’s what 50 years of practice gets you, the ability to spot the gold coins lying on the street ignored by everyone else and pocket them immediately. A record $4.2 billion poured into technology stock funds last week as investors call the end of the six-month big tech correction. The barbell approach is working like a charm, with buying bouncing back and forth like a ping pong ball between domestics, technology, or both sectors go up at the same time. It’s better than owning a printing press for $100 bills.

The Mad Hedge Technology Letter also spotted which way the gale force winds were blowing and piled on the longs as well. (AMZN), (QCOM), and (CRWD), it’s all music to my ears. My old friend Jeff retired, paving the way for another doubling in his stock (AMZN).

We now are getting a clearer picture of how 2021 will play out in the stock market. Periods of sideways action will be followed by big gaps up, eventually taking us to a Dow Average of 40,000.

The sweet spot continues. As low as interest rates and inflation remain low and a tidal wave of new money is pouring into the economy, you have a rich uncle writing you a check every month from the stock market.

We have not had a correction of more than 4% since October. This could go on for years.

Where will the next surprise come from?

When Joe Biden gets his full $1.9 trillion in upfront rescue spending. With the grim tidings of three disastrous monthly jobs reports out, it couldn’t go any other way. The cost of waiting is just too high, especially for the 18 million U-6 unemployed and millions of small businesses hanging on by their fingernails. The Nonfarm Payroll Report came in very weak, at 49,000 in January. The headline Unemployment Rate was at 6.3%, a decline as more people are leaving the workforce. The U-6 broader “discouraged worker” unemployment rate is still at 11%. December was revised down to an even bigger 227,000 loss. Construction was down 10,000, Retail down 37,000, and Government Jobs were up 43,000. It’s the third disappointing month in a row so a double-dip recession is still on the table. We have a very long road to recovery.

Weekly Jobless Claims improved, dropping to 779,000, the lowest since November. The correlation with falling Covid-19 cases is almost perfect, which have declined by 35% in two weeks. Is the stock market getting ready to roar?

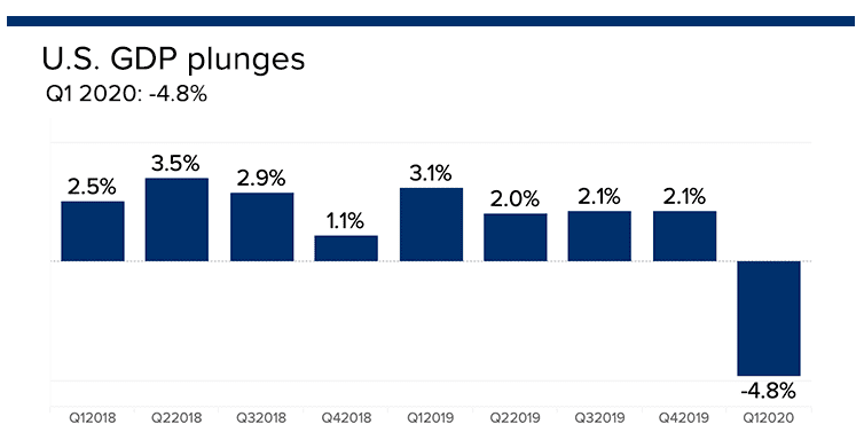

US GDP fell by 3.5% in 2020, wiping out all of 2019 and a good chunk of 2018 as well. The last quarter of 2020 came in at -4.8%, much worse than expected, and further downward revisions are coming, according to the Bureau of Economic Analysis. The economy won’t recover pre-pandemic levels until late 2022 or 2023. The biggest drags on the economy were dramatic falls in consumer spending, nonresidential fixed investment, and a trade war-induced plunge in exports.

Pending Home Sales fell, 0.3% in December, but are still up a staggering 21.4% YOY. It is the highest December reading on record, but the fourth straight month of declines. A historic shortage of supply is the main reason. The short squeeze play moved to silver, with prices hitting an eight-year high. Many local dealers are seeing business rise tenfold over the weekend and are running out of inventory. The white metal was up 35% in two days. It’s the largest one-day volume every. This time, the kids may have got it wrong, since all short positions in the options market are fully hedged with long positions in silver futures or silver bars. The GameStop players only saw the short side. Long term, I love (SLV) for industrial demand from electric cars and solar panels and see it going from today’s $28 to $50, but not today.

Apple (AAPL) is boosting share buybacks and is borrowing to do it. It’s issuing $14 billion in bonds out to 40 years in maturity at 95 basis points above Treasuries. If Apple is so aggressive in buying its own stock, maybe you should too.

The Apple car is moving forward, as incredible as it may seem. The company is in talks with South Korea’s Hyundai to produce autonomous self-driving electric vehicles that will be available by 2024. I’ll believe it when I see it. I’ve seen Apple self-driving cars in the Bay Area for years. It’s an interesting combination: Apple software, a South Korean design, and non-union Georgian metal bashing combined. Sounds like a winner to me. The GameStop (GME) game ends. Back to selling used video games in shopping malls. Millions were lost in the crash from $483 to $49. Back to buying real stocks with the systemic threat to the main market over.

Jeff Bezos retired, putting the operation of Amazon into the hands of Andy Jassy, the inventor and head of the cloud unit AWS. No move in the stock beyond the first few seconds. Jassy has been there since the beginning. If I were the second richest man in the world, after Elon Musk, I’d take some time off too. Now, maybe my former Morgan Stanley colleague will have drinks with me. Buy (AMZN) on dips. My two-year target is $5,000. Bombs away for the bond market, as the (TLT) hits a new 2021 low, taking ten-year yields up to 1.13%. I’m taking profits on the last of my bond shorts and piling money into financials, which love higher interest rates. Buy (JPM), (BAC), (C), and (BLK) on dips. A 1.50% yield on the ten-year US Treasury bond here we come! This is the quality trade of 2021. The ADP Private Employment recovered, up 174,000 in January after a 74,000 plunge in December. Leisure & Hospitality is the big variable.

PayPal transactions were up 25% in 2020, showing the incredible extent of the online migration of the economy. Keep going with Fintech. There’s another double in (PYPL).

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch earned an amazing 14.15% during the first week of February after a blockbuster 10.21% in January. The Dow Average is up 3.47% so far in 2021. This is my fourth double-digit month in a row. My 2021 year-to-date performance soared to 24.36%.

I absolutely nailed the market bottom created by the GameStop fiasco, which I didn’t expect to last any more than days. I went 100% leveraged long, which enabled me to achieve the astounding numbers I am reporting today.

Not only did I get the market right, I picked the perfect sectors as well. I jumped 60% into financials, 20% in Tesla, 10% for commodities, and 10% in chips. I used the bond market meltdown to cover the last of my bond shorts. But all of my financial longs are essentially bond shorts.

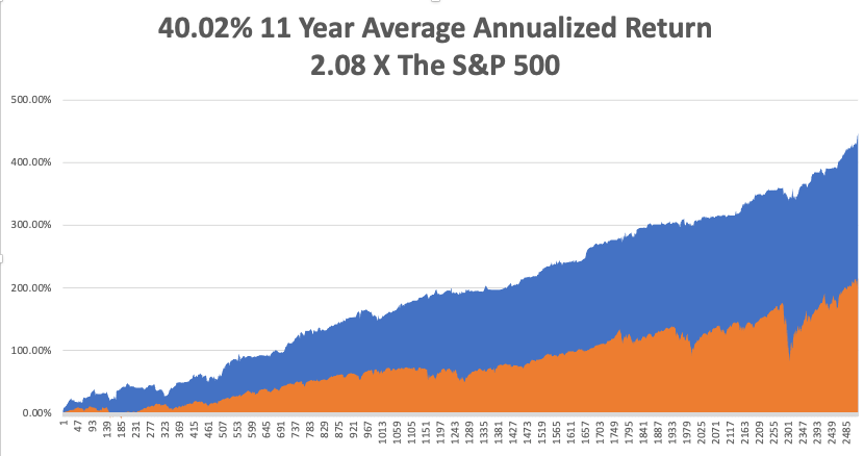

That brings my 11-year total return to 446.81%, some 2.08 times the S&P 500 over the same period. My 11-year average annualized return now stands at an Everest-like new high of 40.02%.

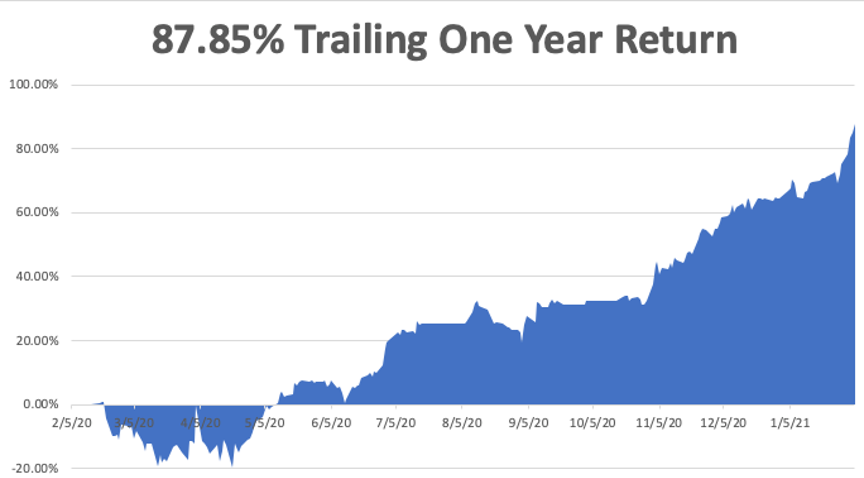

My trailing one-year return exploded to 87.85%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 105.58% since the March 20, 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 27 million and deaths 465,000, which you can find here. We are now running at a heartbreaking 3,000 deaths a day. But that is down 35% from the recent high.

The coming week will be a boring one on the data front.

On Monday, February 8 at 11:00 AM EST, Consumer Inflation Expectations for January are out. Softbank (SFTBY) and KKR & Co. (KKR) report.

On Tuesday, February 9 at 6:00 AM, the NFIB Business Optimism Index is released. Cisco Systems (CSCO) and Twitter (TWTR) report.

On Wednesday, February 10 at 8:30 AM, the US Core Inflation Rate is announced. Coca-Cola (KO) and Uber (UBER) report.

On Thursday, February 11 at 9:30 AM, Weekly Jobless Claims are printed. Walt Disney (DIS) and AstraZeneca (AZN) report.

On Friday, February 12 at 2:00 PM, we learn the Baker-Hughes Rig Count. As we have a three day weekend following, option volatility should collapse. Moody’s (MCO) reports.

As for me, I went into Reno last week to replace the windshield on my Toyota Highlander, my Tahoe car, which below zero temperatures had cracked. One-third of the town was shut down and boarded up, while what remained was booming. A giant shopping mall near downtown has resumed construction, but with less retail and more residential. Reno is the third fastest-growing city in the US and has become a metaphor for the entire country.

Still waiting for my Covid-19 vaccination. I’m at the top of four lists. Even the military can’t get enough. With any luck, I’ll have it in weeks.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Markets Can Be Tricky

https://www.madhedgefundtrader.com/wp-content/uploads/2019/08/john-snake.png433391Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-08 10:02:242021-02-08 10:59:59The Market Outlook for the Week Ahead, or the Sweet Spot Continues

Below please find subscribers’ Q&A for the February 3 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Incline Village, NV.

Q: Is there a big difference between COVID-19 vaccines?

A: The best vaccine is the one you can get. It’s better than being dead. But there are important differences. The Pfizer (PFE) and Moderna (MRNA) vaccines are RNA vaccines, they’re very safe, and getting similar results. But the evidence shows that about 15% of Moderna recipients are coming down with flu-like symptoms on their second shot. Nobody knows why, as the two are almost biochemically identical. AstraZeneca is a killed virus type vaccine, which means if they have a manufacturing error, you end up giving the disease to people by accident, as with the original polio vaccine. So that's the less safe vaccine. So far, that one has only been used in Europe and Australia, as it is made in England. There isn’t enough data about the John & Johnson (JNJ) single-shot vaccine.

Q: Is Moderna (MRNA) a long term buy?

A: The trouble with all the vaccine plays is that we’re heading for a global vaccine glut in about 4 months when we’ll have something like 12 companies around the world making them. The rush for everyone to get a vaccination as soon as possible is leading to inevitable overproduction and falling stock prices. Moderna is already a 12 bagger for us. I’m not really looking to overstay my welcome, so to speak. Time to cash in and say, “Thank you very much, Mr. Market.” There will be another cycle down the road for (MRNA) as its technology is used to cure cancer, but not yet.

Q: Would you recommend a silver (SLV) LEAP?

A: Yes, silver was run up 35% for a day by the GameStop (GME) crowd and crashed the next day, which was to be expected because there are no short positions in silver. Everything was just hedged to look like there were short positions because the big banks had huge open short options positions that were public and hedges in the futures and silver bars that were private. The (GME) people only saw the public short positions. Long term, I would go for a $30-$32 vertical call spread expiring in 2023. Go out 2 years, and I think you could get silver at $50. So, a good LEAP might get you a 1000% return in two years. Those are the kinds of trades I like to do.

Q: What do you think of Amazon now that Jeff Bezos is retiring?

A: Buy the daylights out of it. That was the great unknown overhanging the stock for years, Jeff’s potential retirement. Now it's no longer unknown, you want to buy (AMZN). Even before the retirement, I was targeting $5,000 a share in two years. Now we have everybody under the sun raising their targets to $5,000 or more— we even had one upgrade today to $5,200. There are at least half a dozen businesses that Amazon can expand into, like healthcare, which will be multibillion-dollar earners. And then if you break it up because of antitrust, it doubles in value again, so that's a screaming buy here. We have flatlined for six months, so this could be a trigger for a long-term breakout.

Q: Is there anything else left after GameStop? Another short play?

A: Well, this was the worst short squeeze in 25 years, and everyone else covered their other shorts because they don't want to get wiped out like the one Melvin Capital. There were only around a dozen potential single-digit heavily shorted stocks out there, and those are mostly gone. So, the GameStop crowd will have to roll up their sleeves and do some hard work finding stocks the old fashion way—by doing research. I’m guessing that GameStop was a one-hit-wonder; we probably won’t be surprised again. At the same time, you should never underestimate the stupidity of other investors.

Q: What do you think of the cloud plays like Cloudera and Snowflake?

A: I love cloud plays and there will be more coming. The entire US economy is moving on to the cloud. But everyone else loves them too. Snowflake (SNOW) doubled on its first day, and Cloudera (CLDR) doubled over the last three months, so they're incredibly expensive and high risk. But you can't argue with their business models going forward—the cloud is here to stay.

Q: Would you buy LEAPS in financials?

A: Absolutely yes; go out two years for your maturity and 30% on your strike prices, you will get a ten bagger on the trade. If I’m wrong, it only goes to zero.

Q: Is US Steel (X) a buy?

A: Yes. They are being dragged up by the global commodity boom triggered by the global synchronized recovery. (X) took a hit today because they just priced a $700 million secondary share issue which the flippers dumped like a hot potato. If given the choice, I’d rather do a copper play with Freeport McMoRan (FCX) which is seeing much more buying from China. I bought it on Monday.

Q: Any chance you can include one-, three-, and five-year price targets?

A: No chance whatsoever. I’ve never heard of a fund manager that could do that and be right. Stocks are just too imprecise an instrument with all the emotion that’s involved. But for the better stocks, you can with confidence predict at least a double. And by the way, all my predictions for the last 13 years have been way, way on the low side, so I tend to be conservative. Like, remember when Amazon was at $10? I said it would go to $20. Boy was I right!

Q: How can you say the next four years will be good for the stock market?

A: Well, $10 trillion in fiscal stimulus, $10 trillion in QE; stocks tend to like that. Oh, and technology exponentially accelerating on all fronts and far more broadly than what we saw in the 1990s. Also, there is a certain person who is no longer president, so add about 10-20% on top of all stock valuations. Companies can finally do long term planning again, after being unable to do so for four years because policies were anti-trade, anti-business, and flip-flopping every other day. So yes, I think that's enough to make the next 4 four years good; and actually, I think the next 8 years could be good—I'm predicting Dow 120,000 by 2030, if you recall.

Q: When do you expect the next 5% correction if there is one? February is always very volatile.

A: With an unlimited liquidity market like we have, it is really tough to see negatives of any kind. What kind of negatives are out there? The pandemic doesn’t stop—that's the main one. There’s another one people aren't talking about: the reason we got all these vaccines so fast is they took all regulation and threw it out the window. What if one of these vaccines kill off a million people? That would be pretty negative for the market. Interest rates could rocket faster than expected. But I’m always short there so that would be a moneymaker. But these are pretty out there possibilities, and that is why the market is not backing off, and when it does, it only gives us 5%.

Q: Is the Fed stimulating the economy too much?

A: The bond market says no with a ten-year yield of 1.10%, and the bond market is always the ultimate arbiter of when the stimulus ends. That’s because the Fed can’t directly control bond market interest rates, only overnight rates. But when we get bonds up to, say, a 3% yield (which is probably 2 or 3 years off), that’s when we’re getting too much stimulus, and we’ll probably take our foot off the pedal way before then. I know Janet Yellen and she agrees with me on this point. She’ll be throttling back well before we see a 3% yield in the Treasury market.

Q: Do you manage other people’s money?

A: No, because it costs a million dollars in legal fees to set up even a small fund these days. When I set up my hedge fund 30 years ago, there were no regulatory costs because no one knew what a hedge fund was; they all thought they were doing something illegal, so they didn't have to register for anything. That’s why it’s changed now.

Q: What is your target on NVIDIA (NVDA), and will it split?

A: It’s an easy double, with a global chip shortage running rampant. They make the best graphics cards in the world, bar none. These big tech companies tend not to split until they get share prices into the thousands, which is what Apple (AAPL) and what Tesla (TSLA) did three or four times.

Q: If we get 3.25% in bonds, is that going to hurt gold?

A: Yes, and that’s one of the reasons I bailed on my gold positions a couple of weeks ago. It effectively turned into a bond long. A sharp rise in interest rates is bad for gold because we all know that gold yields to zero.

Q: What about Fireye (FEYE)?

A: Yes, we also love Fireye in addition to Palo Alto Networks (PANW) because there is a near-monopoly—there are only about six players in the entire cybersecurity industry and hacking is getting worse by the day. Look at the Solar Winds (SWI) fiasco and the national Russian hack there.

Q: What about copper as a recovery play?

A: Well, I voted with my feet on Monday when I bought a position in Freeport McMoRan, after it just sold off 15%. I think (FCX) could double at some point in the coming economic recovery. So, copper is an absolute winner, and when having to choose between copper and steel, I’ll pick copper all day long.

Q: What do you recommend for gold (GLD)?

A: Gold is a trading range for the time being. Buy the dips, sell the rallies; you won’t get more than about 10% or 15% range on that. And there are just better fish to fry right now, like financials, which benefit from rising interest rates as opposed to being punished. Bitcoin is stealing gold’s thunder and the markets keep creating more Bitcoins.

Q: Should high-frequency trading be banned?

A: I don’t think it should be. It does create liquidity; the effect on the market is wildly overexaggerated. They’re basically trading for pennies or tenths of pennies, so they do provide buying on selloffs and selling at huge price spikes. They do have a positive effect and they’re probably only taking about $10 or $20 billion in profit a year out of the market.

Q: Should I buy Wynn Resorts (WYNN) here?

A: Buy the dips for sure; this is a major recovery play. We here in Nevada are expecting an absolute tidal wave of people to hit the casinos once the pandemic ends, and (WYNN), (MGM), and (LVS) would be a great play in those areas.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/02/lake-tahoe-sunrise.png460612Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-05 09:34:282021-02-05 08:16:16February 3 Biweekly Strategy Webinar Q&A

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.