A better headline for this piece might have been “Ten stocks to Buy at the Bottom”.

At long last, we have a once-a-decade entry point for the ten best stock in America at bargain basement prices.

Coming in here and betting the ranch is now a no-lose trade. If I’m right, the pandemic ends in three months, stocks will soar. If I’m wrong and the global epidemic explodes from here, you’ll be dead anyway and won’t care that the stock market crashed further.

Needless to say, I have a heavy tech orientation with this list, far and away the source of the bulk of earnings growth for the US economy for the foreseeable future. If anything, the coronavirus will accelerate the move away from shopping malls and towards online commerce as consumers seek to avoid direct contact with the virus.

What would I be avoiding here? Directly corona-related stocks like those in airlines, hotels, casinos, and cruise lines. Avoid human contact at all cost!

Microsoft (MSFT) – still has a near-monopoly on operating systems for personal computers and a huge cash balance. Their inroads with the Azure cloud services have been impressive. (MSFT) just reported an impressive $8.9 billion in Q4 earnings. It’s now yielding a respectable 1.26%.

Apple (AAPL) – Even with the Coronavirus, Apple still has a cash balance of $225 billion. Its 5G iPhone launches in the fall, unleashing enormous pent-up demand. Apple’s rapid move away from a dependence on hardware to services continues. It’s now yielding a respectable 1.13%.

Alphabet (GOOGL) – Has a massive 92% market share in search and remains the dominant advertising company on the planet. (GOOGL) just announced an incredible $8.9 billion in Q4 earnings.

QUALCOMM (QCOM) – Has a near-monopoly in chips needed for 5G phones. It also recently won a lawsuit against Apple over proprietary chip design.

Amazon (AMZN) – The world’s preeminent retailer is growing by leaps and bounds. Dragged down by its association with the world’s worst industry, (AMZN) is a bargain relative to other FANGs.

Visa (V) – The world’s largest credit company is a free call on the growth of the internet. We still need credit cards to buy things. And guess what? Coronavirus will accelerate the move of commerce out of malls, where you can get sick, to online.

American Express (AXP) – Ditto above, except it charges high fees, its stock has lagged Visa and Master Card in recent years and pays a 1.58% dividend.

NVIDIA (NVDA) – The leading graphics card maker that is essential for artificial intelligence, gaming, and bitcoin mining.

Advanced Micro Devices (AMD) – Stands to benefit enormously from the coming chip shortage created by the coming 5G.

Target (TGT) – The one retailer that has figured it out, both in their stores and online. It can’t be ALL tech.

Good Luck and Good Trading

John Thomas

Looks Like a “BUY” signal to Me

https://www.madhedgefundtrader.com/wp-content/uploads/2020/03/corona-spread.png316422Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-03-03 08:02:182020-03-03 16:11:55Ten Stocks to Buy Before You Die

Tech shares are hoping to stage a rebound after the coronavirus-fueled rout that saw the Nasdaq’s 2-day drop by 6.38%, which is its worst since June 2016.

Readers can now pencil in a fresh readjustment to growth expectations of zero to low single digits in tech shares for fiscal year of 2020.

That is why Thursday morning was greeted by another 3% drop at the open - proceed with caution to not get trapped in the proverbial dead cat bounce vortex in the short-term.

A major tech consolidation could take place because let’s get real, the unpredictability is having a major impact on technology companies and uncertainty is a substantial input in heightened risk.

What are the realistic scenarios that are still left on the table?

Tech firms could slash prices, a deflationary element that promotes deteriorating profit margins seen as a net negative to revenue causing companies to miss revenue targets.

Unsold inventory could lead to working capital issues crushing balance sheets for the smaller tech firms.

Loss-making enterprise confront solvency issues if debt repayment hardship ripples through finance departments and could be a serious threat to credit markets as a whole.

Firms trading on the Nasdaq will slash price targets and profit estimates that could uncoil another leg down in the Nasdaq index.

In fact, it has already happened as PayPal (PYPL), Microsoft (MSFT), and Apple (AAPL) issued revenue warnings saying they do not expect to meet their revenue goals because of the coronavirus.

On an operational level, softness is what I see when delving into the semantics of Amazon (AMZN) whose ranking algorithm demotes product sellers who go out of stock.

The coronavirus has crippled supply chains, and to avoid a lack of stock, sellers are raising prices to slow sales, while planning to move production to other countries.

This is on top of the backbreaking supply problems that companies face because of the ill-effects of the trade war.

If the Amazon algorithm punishes the seller, once stock is replenished, they must overspend on advertising to climb back to the top of product searches.

The surveys I have taken out with Amazon sellers in the last few days show a precarious situation where sellers are stretched to the limit relying on numerous uncertain variables that are completely out of their control,

Even if the local government allows Chinese factories to restart, it will be understaffed while workers from other provinces self-quarantine.

The third-party marketplace accounts for more than half of Amazon’s retail sales with a robust base of manufacturers and sellers in China.

Google (GOOGL) and Microsoft are accelerating efforts to shift hardware production to Southeast Asia amid the worsening coronavirus outbreak, opening factories in Vietnam and Thailand as well.

Google is set to begin production of the Pixel 4A smartphone and also plans to manufacture its next-generation flagship smartphone called the Pixel 5 in Vietnam.

Google is also on the verge of building factories in Thailand for "smart home" related products, including voice-activated smart speakers like the Nest Mini.

Google and Microsoft’s plans are a giant shift away from their prior generation-long China manufacturing strategy and the coronavirus has only supported a strategy to remove China as a core manufacturing hub.

It is getting so bad in China that they are evaluating the feasibility and cost implications to uninstall some production equipment and ship it from China to Vietnam, literally packing up and taking their show on the road.

The have already initiated the process by asking a key sourcing contact to convert an old Nokia factory in the northern Vietnamese province of Bac Ninh to handle the production of Pixel phones.

Data center server production was also rerouted to Taiwan last year.

The coronavirus threat is only speeding up the move into South East Asia and Google and Microsoft hope to avoid the geopolitical risk in the region.

Remember that all of this rejigging of production will add costs and only the biggest can absorb mega hits to the balance sheets.

As for the coronavirus, business is becoming more complicated as the ban on Chinese nationals and flights from China could build barriers to business, and now South Korea has joined the list.

Korea’s Samsung Electronics, the world's largest smartphone maker, has operated a smartphone supply chain in northern Vietnam for years but still relies on some components made in China.

While there are many moving parts, the average investor needs to wait on optimal entry points.

Japan announced school shutdowns for a month and tech shares have only priced in the coronavirus eventually entering the U.S., but if there are mass shutdowns of American cities and schools, then tech shares will see another stinging sell-off.

The contagion could eventually lead to the Olympics in Tokyo being canceled, high-profile corporate management getting infected, and the Chinese economy being sidelined for most of 2020.

All of these events are highly negative to the global economy which is why potential risks have exploded through the roof in such a short time.

Slinging mud at the wall will not work in times like this, but this does have the makings of a once-in-a-year entry point into tech shares.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-02-28 08:02:572020-05-11 13:13:54The True Cost of the Coronavirus

Google (GOOGL) and Facebook (FB) are dominant to the extent that the U.S. administration is hoping to dismantle them.

The two companies enjoy a flourishing duopoly and guzzle up digital ad dollars.

Governments around the world are scratching their heads attempting to figure out how to put a dent in these fortresses and so far, have been unsuccessful.

Big tech has made governments look bad, to say the least, and their response has been even more shambolic.

Alphabet installed Google CEO Sundar Pichai as the top decision-maker for all Alphabet assets preparing for the onslaught of digital privacy headwinds and regulation that the E.U., U.S., and everyone else will throw at them.

Luckily, they do not need to deal with the Chinese communist party as big tech minus Apple was effectively banned years ago.

What’s on Google and Facebook’s plate right now?

Attorney General William Barr has pointed the finger at these two platforms for hiding behind a clause that gives them immunity from lawsuits while their platforms carry material promoting illicit and immoral conduct and suppressing opinions.

Barr is currently looking into potential changes to Section 230 of the Communications Decency Act, which was passed in 1996 and has been also referred to as the supercharger to tech riches.

What could eventually come of this?

Barr could decide for the Justice Department to explore ways to limit the provision, which protects internet companies from liability for user-generated content.

This could open up Google and Facebook to higher costs of managing content on their platforms and lawsuits related to malcontent in which they fail to remove.

Even though platforms love to market that they actively thwart bad actors, at the end of the day, they aren’t on the hook for what happens.

Massive alterations could fundamentally weaken their business models and force them to review each word and photo that is thrown upon their platform.

They have already hired an army of hourly paid contractors, but at their massive scale, content is simply impossible to smother.

Content generators understand how to sidestep machine learning algorithms which are based on backdated data, meaning they would not be able to catch a new iteration of past content.

Absolving themselves of any responsibility for policing their platforms has been an important catalyst in the outperformance in shares for both Facebook and Google.

The social side of this has cringeworthy unintended consequences.

The Computer & Communications Industry Association, a tech trade group that counts Google and Facebook as members want the government to stay out of it as they believe they are overreaching.

Government has been slowly making inroads in combatting the strength of these digital platforms, and the first successful foray was when Congress eliminated the liability protection for companies that knowingly facilitate online sex trafficking.

Big tech won’t go with a whimper and they will propose a range of changes to avoid direct damage to their business model such as raising the bar a smidgeon on which companies can have the shield, to carving out other laws negating attempt to weaken their platforms, to delaying the repealing of Section 230.

There is too much shareholder value on the line and as the coronavirus rears its ugly head, it’s ironic that investors perceive safety in not only the U.S. dollar but in the vaunted FANG tech group.

Ultimately, the math wins out and these companies with gargantuan earnings can weather any storm with a moat as wide as ever.

It’s to the point that a $10 billion fine is a massive victory, and what other group of companies can boast about that?

We can only trade the market we have in front of us and not the one we want.

I pulled the trigger on a Google call spread and I believe this narrow group of power tech players and their partners in crime cloud stocks of the likes of Twitter (TWTR), eBay (EBAY), Fortinet (FTNT), Adobe (ADBE), and a few others will hoist the market on its back like I predicted it would at the beginning of the trading year.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-02-21 04:02:152020-05-11 13:13:05Why the Government is Gunning for Google and Facebook

Not only have Facebook (FB), Apple (AAPL), Netflix (NFLX), and Alphabet (GOOGL) been at the core of our investment performance for the past decade years, we also gobble up their products and services like kids eating their candy stash the day after Halloween.

Three of the FANGs have already won the race to become the first $1 trillion in history, Apple, Amazon, and Microsoft.

In fact, the FANGs are so popular that we need more of them, a lot more. So how do we find a new FANG?

Here is where it gets complicated. None of the four have perfect business models. All excel in many things but are deficient at others.

So, there are at least four different answers as to what makes a FANG. A more accurate answer would probably be 4 squared, or four to the tenth power.

I will list the eight crucial elements that make a FANG.

1) Product Differentiation

In medieval times, location was the most important determinant of business success. If you owned Ye Olde Shoppe at the foot of London Bridge, you prospered.

Then, great distribution was crucial. This occurred during the 19th century when the railroads ran the economy.

Products followed with the automobile boom of the 20th century, when those who dreamed up 18-inch tailfins dominated. This strategy was applied to all consumer products.

The Financial age came next, when cheap money was used to assemble massive conglomerates that was the primary determinant of success.

The eighties and nineties spawned the era of global brands, be it Coca Cola, MacDonald’s, Lexus, or Gucci.

Today, the global economy is ruled by those who can provide the best services. Facebook offers you personal access to a network of 1.5 billion. Apple will sell you a phone that can perform a magical array of tricks.

Netflix will stream any video content imaginable with lightning speed. Alphabet will deliver you any piece of information you want as fast as you can type, but charges advertisers hundreds of billions of dollars to get in your way.

This has created what I call an “Apple” effect. It stampedes buyers to pay the highest premiums for the best products, assuring global dominance.

While Apple accounts for less than 10% of the smart phone market, it captures a stunning 92% of the net profits. Everyone else is just an “also ran.”

Instead of driving my car into a dingy dealership every few months to get ripped off for a tune up, Tesla (TSLA) does it remotely, online, while I sleep, for free.

Unlike battling for a smelly New York taxi cab in a snow storm, a smiling Uber driver will show up instantly, know where to go, automatically bill me at a discount price, and even give me restaurant recommendations in Kabul.

And you all know what Amazon can do. It beats the hell out of looking for a parking space at a mall these days, only to be told they don’t have your size (48 XLT).

2. Visionary Capital

If you have a great vision, you can get unlimited financing free from investors anywhere. That puts those who must pay for expensive external financing for growth at a huge disadvantage.

Have a great vision, and the world is your oyster.

Elon Musk figured this out early with Tesla. By promising a “carbon-free economy,” he has been able to raise tens of billions of equity capital even though his firm has never made a real profit.

Alphabet is “organizing the world’s information”, while Facebook is “connecting the world.”

Chinese Internet giant Alibaba (BABA) invented a holiday from scratch, “Singles Day,” November 11, which has quickly become the most feverish shopping day in history. In 2019, they booked an unbelievable $30.8 billion in sales in a single 24 hours period, up 27% from the previous year.

And you know the great thing about visions? Not only do venture capitalists and consumers love them, so do stock investors.

3) Global Reach

You have to go global or be gone. A company with 7 billion customers will beat one with only 330 million all day long.

Go global, and economies of scale kick in enormously. This is only possible if you digitize everything from the point of sale to the senior management. Some two-thirds of Facebook users are outside the US, although half its profits are homegrown.

By the way, the Mad Hedge Fund Trader is global, with readers in 135 countries. Our marginal cost of production is zero, and the entire firm is run off my American Express card. It’s a great business model. And boy, do I get a ton of frequent flier points! Whenever I board Virgin Atlantic’s nonstop from San Francisco to London, the entire crew stands up to salute.

4) Likeability

Who doesn’t like Mark Zuckerberg, with his ever-present hoodies, skinny jeans, and self-effacing demeanor. And who did Facebook send to Washington to testify about internet regulation but the attractive, razor-sharp, and witty Sheryl Sandberg? The senators ate out of her hand.

Bill Gates and Steve Ballmer? Not so likable. Their arrogance invited a ten-year antitrust suit against Microsoft (MSFT) from the Justice Department which half the legal profession made a living off of.

And here’s the thing. If people like you, so will consumers, regulators, and yes, even equity investors. It makes a big difference to the bottom line and your investment performance.

5) Vertical Integration

Crucial to the success of the FANGs is their complete control of the customer experience through vertical integration.

When FANGs don’t manufacture their own products, as Apple does, they source them, rebrand them, and sell them as their own, like Amazon.

The return on investment for advertising is plummeting. Just ask the National Football League. So, it has become essential for companies to keep a death grip on the customer the second they enter your site.

Some, like Amazon again, will keep chasing you long after you have left their sites with special offers and alternative products. Even if you change computers they will hunt you down.

One of my teenaged daughters used my computer to buy a swimsuit last summer, and let me tell you, booting up in the morning has been a real joy ever since.

This was the genius of the Apple store network. Buy one Apple product and they own you for life, like an indentured servant. They all integrate and talk to each other, a huge advantage for a small business owner. And they are cool.

No pimple-faced geeks wearing horn-rimmed glasses here. Get your iPhone fixed and you don’t talk to a technician, but a “genius.” It’s all about control.

Expect other strong brands to open their own store chains soon.

6) Artificial Intelligence

There is probably no more commonly known but least understood term in technology today. It’s like counting the number of people who have finished Dr. Stephen Hawking’s “A Brief History of Time” (I have).

A trillion-dollar company absolutely must be able to learn from human data input and then use algorithms to analyze it. Data has become the oxygen of the modern economy.

The company then use other algos to predict what you’re most likely buying next and then thrust it in front of your face screaming at the top of its lungs.

This has been evolving for decades.

First, there was demographic targeting. White suburban middle-class guys have all got to like Budweiser, right?

This turned into social targeting. If two friends “liked” the same brand, regardless of their demographics, they should be targeted by same advertisers.

Now we live in the age of behavioral targeting. There is no better predictor of future purchases than current activities. So, if I buy a plane ticket to Paris, offerings of Paris guidebooks, tours, French cookbooks, French dating services, and even seller of discount black berets suddenly start coming out of the woodwork.

It would be a vast understatement to say that behavioral targeting is the most successful marketing strategy ever invented. So, guess what? We’re going to get a lot more of it.

As depressing as this may sound, the number one goal of almost all new technological advancements these days is to get you to buy more stuff.

Better to use the public computer at the library to buy your copy of “50 Shades of Gray.”

7) Accelerant

If you want to throw gasoline on the growth of a company, you absolutely have to have the best people to do it. The companies with the smartest staff can suck in free capital, invent faster, develop speedier services, and always be ahead of the curve when compared to the competition.

This has led to enormous disparities in income. Companies will pay anything for winners, but virtually nothing for losers.

I’ll never forget the first day I walked on to the trading floor at Morgan Stanley (MS). I am 6’4” and am used to towering over those around me. But at Morgan, almost all the salesmen were my height or a few inches shorter.

The company specifically selected these people because they delivered better sales records. Height is intimidating, especially to short customers.

And that’s what the FANGs have, the programming equivalents of a crack all-6’4” sales team.

A few years ago, my son got a job as the head of International SEO at Google. He was rare in that he spoke fluent Japanese and carried three passports, US, British, and Japanese (born in London with a Japanese mom and American dad).

However, when he met his team, they all spoke multiple languages, were binational, and were valedictorians, National Merit Scholars, and Eagle Scouts to boot!

This is why immigration is such a hot button issue in Silicon Valley these days. If you can’t get a work visa for a graduating PhD in Computer Science from Stanford, he’ll just go back to China or India to start a local competitor that may someday eat your lunch.

By the way, if you get a FANG on your resume, even for a short period, you are set for life. Oh, and by the way, Apple gets 100,000 resumes a month!

8) Geography

It all about location, location, location. It’s no accident that Silicon Valley took root near two world class universities, the University of California at Berkeley (my alma mater), and the godless heathens at Stanford across the bay.

When the pioneers moved west in covered wagons in 1849, they came to a fork in the road. The god fearing families went right to the verdant farmland of Oregon, while young men cashing in on the latest get-rich-quick scheme chose left for the gold fields of California. Nothing has changed since.

Cal in particular was the recipient of massive government funding for the Manhattan Project that built the first atomic bomb during WWII. The tailwind lingers to this day. The world’s first cyclotron still occupies a local roundabout.

Universities provide the raw materials essential to create hot house local economies like the San Francisco Bay Area. And as much as every region in the US or country in the world would like to do this, none have been able to.

There is only one place in the world were a company can hire 1,000 engineers from scratch on short notice, and that is the Bay Area.

Also, innovation is city centered. Some two-thirds of future GDP growth will emanate from cities.

So, if you want to move your career forward, you better count on spending some serious time in Silicon Valley, New York, London, and Tokyo.

I’ve done all four and it paid handsomely.

So there you have it. Now we know what makes a FANG. I’ll be addressing who the most likely FANG candidates are in a future letter.

I want to thank my friend, Scott Galloway of New York University’s Stern School of Business for some of the concepts in this piece. His book, “The Four” is a must read for the serious tech investor.

So Where is the Next FANG?

https://www.madhedgefundtrader.com/wp-content/uploads/2018/02/john-laptop.jpg388335Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2020-02-20 04:02:462020-05-11 14:24:07Finding a New FANG

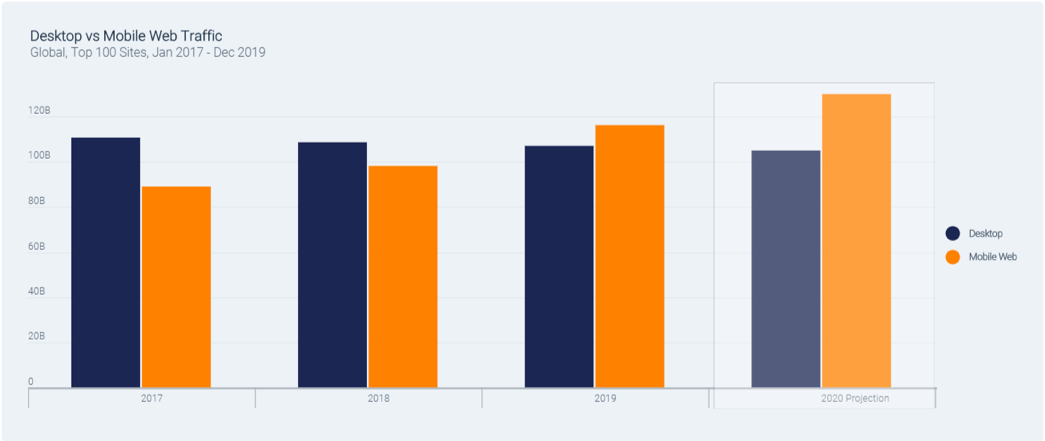

Behavioral trends have a sizable say in which tech companies will outperform the next and a recent report from SimilarWeb offers insight into how much users navigate around the monstrosity known as the internet.

The optimal way to comprehend the trends are from a top-down method by absorbing the divergence between desktop traffic and mobile traffic.

It’s no secret that the last decade delivered consumers a massive leap in mobile phone performance in which tech companies were able to neatly package applications that acted as monetization platforms by offering software and services to the end-user.

Thus, it probably won’t shock you to find out that desktop traffic is down 3.3% since 2017 as users have migrated towards mobile and the trend has only been exaggerated by the younger generations as some have become entirely mobile-only users.

All told, the 30.6% expansion in mobile traffic has penalized tech firms who have neglected mobile-first strategies and one example would be Facebook (FB), who even though has a failing flagship product in Facebook.com, are compensated by Instagram, who is showing wild growth numbers.

The fact that mobile screens are smaller than desktop screens means that users are staying on web pages not as long as they used to – precisely 49 seconds to be exact.

This trend means that content generators are heavily incentivized to frontload content and scrunch it up at the top of the page. This also means that sellers who don’t populate on Google’s first page of search results are practically invisible.

The high stakes of internet commerce are not for the faint of heart and numerous companies have complained about algorithm changes toppling their algorithm-sensitive businesses.

Even using a brute force analysis and investing in companies that are in the top 15 of internet traffic, then the companies that scream undervalued are Twitter (TWTR) and eBay (EBAY).

Twitter is a company I have liked for quite a while and is definitely a buy on the dip candidate.

The asset is the 7th most visited property on the internet behind the likes of Instagram, Google, Baidu, Wikipedia, Amazon, and Facebook.

This position puts them just ahead of Pornhub.com, Netflix, and Yahoo.

And if you take one step back and analyze traffic from the top 100 sites, traffic is up 8% since 2018 and 11.8% since 2017 averaging 223 billion visits per month.

Rounding out the top 15 is eBay who I believe is undervalued along with Twitter - these two are legitimate buy and holds.

Ebay was the recipient of poor management for many years and they are now addressing these sore points.

Certain content is suitable for mobile such as adult sites, gambling sites, food & drink, pets & animals, health, community & society, sports, and lifestyle.

And just over the last year or two, other categories are gaining traction in mobile that once was dominated by desktop such as news and media, vehicle sites, travel, reference, finance, and others.

Many consumers are becoming more comfortable at doing more on mobile and spending more to the point where people are making large purchases on their iPhones.

The biggest loser by far was news - they are losing traffic in droves.

Traffic at the top 100 media publications was down 5.3% year-over-year from 2018 to 2019, a loss of 4 billion visits, and down by 7% since 2017.

Personally, I believe the state of the digital news industry is in shambles, and Twitter has moved into this space becoming the de facto news source while pushing the relevancy of news sites down the rankings.

Facebook and Twitter are essentially undercutting the news by forcing news companies to insert them between the reader and the news company because they have strategized a position so close to the user’s fingertips.

The negative sentiment in news is broad based on popular news, entertainment news and local news all showing decreases of more than 25%.

Finance and women’s interest news categories are the only ones showing positive traffic growth.

The state of internet traffic growth supports my underlying thesis of the big getting bigger and the subsequent network effect stimulating further synergies that drop straight down to the bottom line.

The top 10 biggest sites racked up a total of 167.5 billion monthly visits in 2019, up 10.7% over 2018 and the remaining 90 largest sites out of the top 100 only increased 2.3%.

This has set the stage for just five gargantuan tech firms to become worth more than $5 trillion or 15.7% of the S&P 500’s market value and 19.7% of the total U.S. stock market’s value.

Now we have real data backing up my iron-clad thesis and these cornerstone beliefs underpins my trading philosophy.

Many of the biggest wield a two-headed monster like Google who has Google.com and YouTube video streaming and Facebook, who have Facebook.com and Instagram.

It doesn’t matter that Facebook has lost 8.6% of traffic over the past year because Instagram compensates for Facebook being a poor product.

And if you are searching for another Facebook growth driver under their umbrella of assets then let’s pinpoint chat app WhatsApp who experienced 74% year-over-year traffic.

Beside the news sites, other outsized losers were Yahoo’s web traffic shrinking by 33.6% and Tumblr, which banned adult sites in 2018, leading to a 33% loss in traffic.

If I can sum up the data, buy the shares of companies who are in the top 15 of internet traffic and be on the lookout for any dip in eBay or Twitter because they are relatively undervalued.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/02/monthly-traffic.png4521056Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-02-14 10:02:532020-05-11 13:12:49Data Tells the Whole Story

Mad Hedge Technology Letter

February 12, 2020 Fiat Lux

Featured Trade:

(UBER’S DARK FUTURE)

(UBER), (LYFT), (FB), (AMZN), (NFLX), (GOOGL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-02-12 05:04:092020-02-11 17:55:42February 12, 2020

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.