Global Market Comments

December 10, 2019

Fiat Lux

Featured Trade:

(MAD HEDGE FUND TRADER ANNOUNCES STRATEGIC PARTNERSHIP WITH TASTYTRADE),

(A NOTE ON OPTIONS CALLED AWAY),

(MSFT), (TLT), (BA), (GOOGL), (SPY)

Global Market Comments

December 10, 2019

Fiat Lux

Featured Trade:

(MAD HEDGE FUND TRADER ANNOUNCES STRATEGIC PARTNERSHIP WITH TASTYTRADE),

(A NOTE ON OPTIONS CALLED AWAY),

(MSFT), (TLT), (BA), (GOOGL), (SPY)

Global Market Comments

December 2, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or 2020 IS ALREADY HAPPENING),

(TSLA), (X), (GE), (FCX), (SLB), (GOOGL), (MSFT), (GLD)

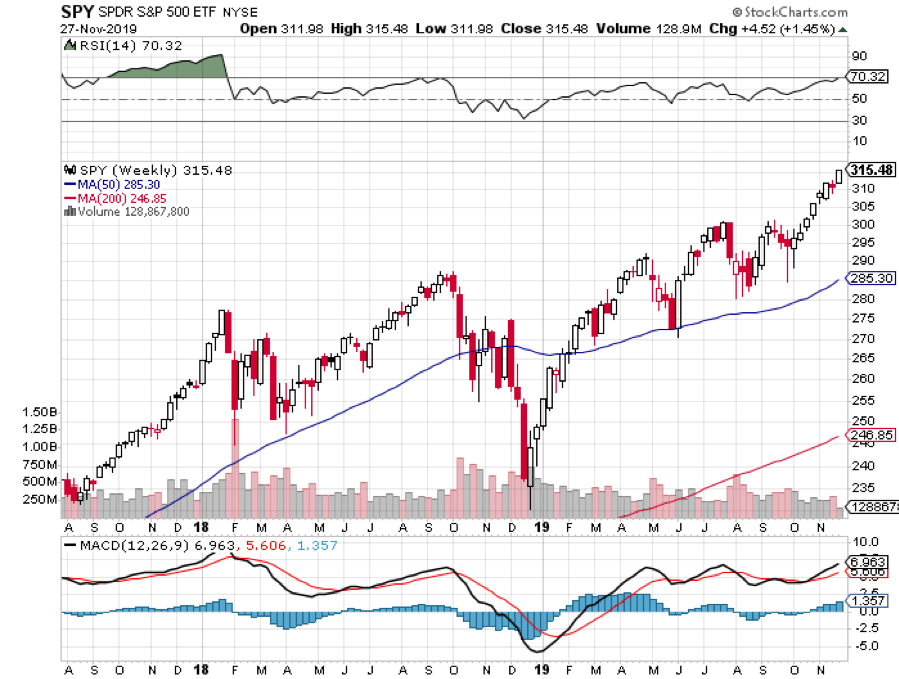

You know the melt-up that is going on in the stock market right now? That is your 2020 performance being pulled forward.

One thing I have noticed over the past half-century of trading is that when market participants agree on a direction, it gets accelerated. Once the traditional October selloff failed to show, it was pedal to the metal to achieve new all-time highs.

Traders have become so overconfident that they have already completed this year’s performance and are now working on next year's. They are in effect pulling performance forward from 2020.

This historic run is taking place in the face of year-on-year earnings growth that is zero. ALL of the 29% price appreciation in the S&P 500 (SPY) in 2019 has been due to multiple expansion, from 14 times earnings to 19 times, a 20-year high. Market multiples rising by 50% anytime is almost unprecedented in history. I can only recall that happening twice: in 1929 and 1999.

So, that leaves only two possibilities for 2020. Either the multiple rises to a new 20-year multiple high, say to 20, 21, or 22, or the stock market goes down.

With a trade war-induced global economic slowdown still unfolding, don’t expect any respite from a sudden earnings recovery. Enjoy 2019 because the more we go up now means the more we will go down in 2020.

Were you waiting for the euphoria to make a market top? This is it. Sharply rising markets in the face of sharply falling earnings can only end in tears.

Needless to say, risk in the stock market is very high right now.

Jay Powell gave the market another boost, promising to hit the Fed’s 2% inflation target, giving plenty of room for wage hikes. The last inflation reading was 1.7% YOY. He might as well have said Dow 29,000 by yearend. I wish it were always this easy.

Hong Kong stalled the rally with the passage of a pro-democracy support by congress, with sanctions. China is warning of “firm countermeasures.” That throws cold water on any trade deal for 2019. New all-time highs for stocks may have to take a vacation.

US Q3 GDP was revised up to 2.1%, an improvement of 0.2% from the last read. The trade war seems to be costing us 1% of growth a year or about one-third of the total. That’s why we’re getting such a strong stock market move on the possibility of a trade deal. No-deal means lookout below.

Durable Goods came in at 0.6% in October, a nine-month high and better than expected. What does this week’s spate of positive data means, the first in many months? Is the recession risk over? If so, how much is already in the price?

Stocks love a steepening yield curve, with long term interest rates rising faster than short term ones. It puts the recession talk on hold, if not in abeyance.

It’s time to go dumpster diving, as the upside breakout in the Russell 2000 demonstrated last week. So, it’s time to start looking at the forlorn and the ignored of this bull market, like US Steel (X), General Electric (GE), Freeport McMoRan (FCX), and Schlumberger (SLB). There are no fundamentals in any of these names, they’ve just been down for so long anything looks like up from here. The liquidity-driven bull market has to find some fresh meat to rotate into, even temporarily, or it will die.

S&P Case Shiller rose 3.2% in September, the third consecutive month of price increases. Only San Francisco is showing falling prices. Phoenix (6.0%), Charlotte (4.6%), and Tampa (4.5%) are showing the greatest prices rises. Only a shortage of inventory is preventing prices from rising faster, now at a record low of 3.9 months. The builders who went under ten years ago aren’t building anymore.

New Home Sales drop 0.7%, in October, but are still up a massive 31.6% YOY. Sales in the northeast and south plunged, while those in the Midwest and west rise. The seasonally adjusted annual rate is 733,000 units. The Median Home Price fell 3.6% to $316,700. A 30-year fixed-rate mortgage at 3.66% is a major factor.

Merger mania in drug land continues, with the Novartis takeover of The Medicines Co. for $9.7 billion. It wants to take on Amgen (AMGN), Regeneron (REGN), and Sanofi in the heart drug space. No wonder this is the top-performing sector since I launched the Mad Hedge Biotech and Healthcare Letter.

Tesla shattered, both windows and sales records with an incredible 250,000 cyber trucks sold in a week. It’s one of the largest consumer orders in history, second only to the Tesla Model 3 launch four years ago. I may get one myself to make the Lake Tahoe run on a single 500-mile charge. Keep buying (TSLA) on dips. It is the clearest ten bagger out there.

Who is the mystery gold (GLD) buyer? Someone made a massive bet in the options market that gold will rise above $4,000 an ounce in 18 months. It would take a 32% move just to get gold back to its old $1,927 high. If the trade war continues, we may get it.

This was a week for the Mad Hedge Trader Alert Service to burst upon new all-time highs. I know this sounds boring, but I made all the money long technology stocks. This is net a -2.16% loss on my short position in Tesla (TSLA). If I’d only held on two more days this would have been a big winner over the disappointment over the shocking Cyber truck design. My long positions have shrunk to my core (MSFT) and (GOOGL).

By the way, running out of positions at a market top is a good thing.

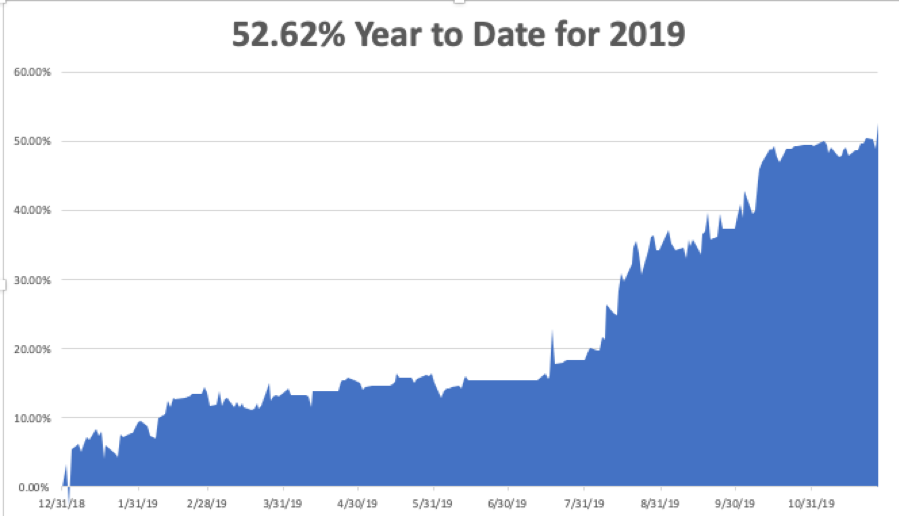

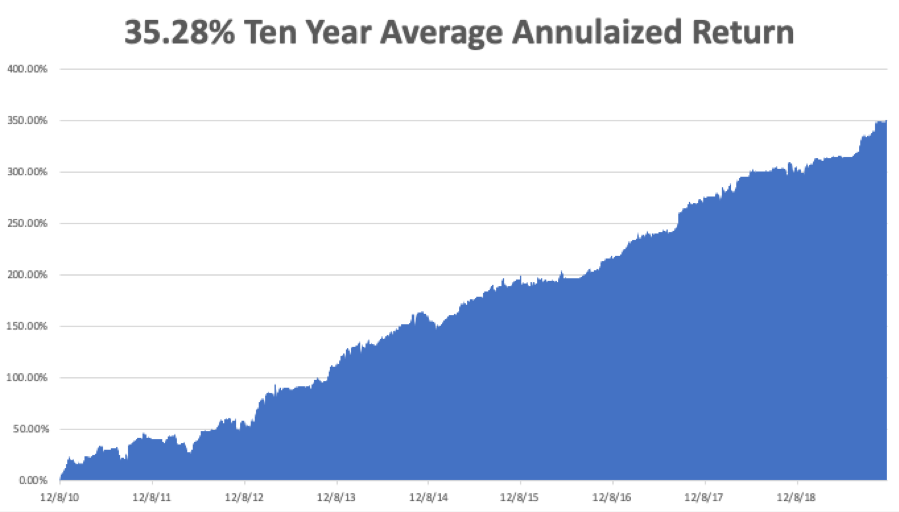

My Global Trading Dispatch performance held steady at +352.76% for the past ten years, pennies short of an all-time high. My 2019 year-to-date catapulted back up to +52.62%. We closed out November with a respectable +3.07% profit. My ten-year average annualized profit ground back up to +35.28%.

The coming week will be hot with the jobs data trifecta.

On Monday, December 2 at 8:00 AM, the ISM Manufacturing PMI for November is out.

On Tuesday, December 3 at 2:30 PM, the API Crude Oil Stocks are announced.

On Wednesday, December 4, at 6:15 AM, the private sector ADP Employment Report is published.

On Thursday, December 5 at 8:30 AM, the Weekly Jobless Claims are printed.

On Friday, December 6 at 8:30 AM, the November Nonfarm Payroll Report is released.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I am going to battle my way through the blizzards at Donner Pass this weekend to get back to the San Francisco Bay Area. There, I’ll be helping the local Boy Scout troop to set up their Christmas tree lot. The enterprise helps finance all the camping trips for the coming year.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

December 2, 2019

Fiat Lux

Featured Trade:

(THE DRONE WARS HAVE STARTED),

(DJI), (AMZN), (WMT), (UBER), (GOOGL), (FDX), (UPS)

Drones whip by like mini whirling dervishes but are actually hardworking aerial robots that carry out surveillance and inspections for utilities, construction sites, airplanes, and trains from onboard cameras.

Drone delivery appears to be the next transportation bottleneck in the e-commerce wars as Amazon (AMZN) and Uber (UBER) pile capital investment into the technology.

In 2013, Founder and CEO of Amazon Jeff Bezos audaciously said that Amazon would have drone delivery operational by 2018.

But the Federal Aviation Administration (FAA) did not acquiesce to Bezos’s ambitious timeline.

Progress has been slow.

When it comes to consumer appetite, the demand for drones will be voracious but only if delivered in a way to add value to the customer experience.

The last thing the world needs is billions of unmanned drones polluting the sky and parked in the sky.

More than 60% of consumers would accept the delivery of dry goods through a drone delivery service, it contrasts to only 26% of fresh produce or meat.

Clearly, fresh foods are more complicated to deliver because of temperature requirements to accommodate the products, and more R&D will need to take place to find a solution.

“When we (Amazon) have a full drone fleet, you'll be able to order anything and get it in 30 minutes if you live near a hub that's serviced by drones," said Amazon’s CEO of Worldwide Consumer Jeff Wilke

Amazon has spent more than six years developing drones which may one day drop packages in backyards assuming regulators green light it.

Timely delivery is important but the diversity of products that can be delivered is just as important.

This is not a one-size-fits-all solution.

Amazon has already ravaged through more than $35 billion on shipping costs this year, more than double what it spent two years ago.

It is yet to be determined whether the four-wheeled delivery robots they are testing that roll on sidewalks will ultimately be slipped into the delivery process, but at least they are making headway and allocating new resources to it by announcing plans for a new facility outside Boston to design and build robots.

Major companies such as Alphabet (GOOGL), FedEx (FDX) and UPS (UPS) are all investing in drone delivery all hoping to be the ones to lead this industry in the future.

The drone battles are taking place under the backdrop of military and political gamesmanship because drones have a large and legitimate role in military affairs.

Even though America’s e-commerce companies hope to take drones and nicely fit it into their delivery service, America is not even close to dominating.

One word – China.

The US-China Economic and Security Review Commission recommended that the US government promote advanced manufacturing and robotics technologies, monitor China’s advances, review bilateral investments and cooperation, and consider closely vetting proprietary academic research.

The Shenzhen, China-based drone company DJI Technology is the dominant worldwide market leader in the civilian drone industry, accounting for over 75% of the global drone market.

In 2017, the U.S. Army banned the military application of DJI drones because the Pentagon was worried that DJI would leak data to the Chinese government.

In 2018, the Defense Department banned the purchase of all commercial off-the-shelf unmanned aircraft system (UAS).

An amendment from Sen. Chris Murphy in the 2020 defense policy bill would ban all Chinese-made drones and Chinese-manufactured parts from military purpose.

DJI’s dramatic rise in the drone race has been nothing but breathtaking dwarfing Western competitors such as France’s Parrot.

They are cost-effective, making them the go-to product for individual consumers.

China has not only succeeded in pulling ahead in the drone wars, but are also pushing the envelope in areas like hypersonic weapons, artificial intelligence, and 5G.

The U.S. military has limited options now because of a generation of underinvestment and inactivity causing a dwindling of U.S. supply of the smallest class of unmanned aerial systems (UASs) that are needed for reconnaissance missions.

DJI has a near-monopoly for one of the most important pieces of technology moving forward.

“We don’t have much of a small UAS industrial base because DJI dumped so many low-price quadcopters on the market, and we then became dependent on them,” said Ellen Lord, the Pentagon’s chief weapons buyer. “We want to rebuild that capability,” she added.

China’s DJI was hit by the recent tariff tsunami levied by the U.S. administration and the drone maker has decided to pass on the cost to the consumer.

DJI has also been banned from bidding for any U.S. military contracts because the Trump administration has concerns that DJI is a national security threat.

DJI reacted to the move by commenting that they are “obviously false” and is “unsubstantiated speculation.”

The second tranche of tariffs, which is scheduled to go live on December 15th, will put an additional 15% tariff on virtually everything that comes to the United States from China, including laptops, smartphones, and drones.

The DJI Mavic Air, now costs $919 on Best Buy instead of $799. Similarly, the DJI Mavic 2 Pro which I have crowned as the best drone to buy in 2019 will cost $1,729, up from $1,499.

Apart from DJI, China has state money pouring into the sector with the most cutting-edge drone technology in the works called Tianyi quadcopter built by a subsidiary of a state aerospace corporation.

It is designed to carry out ground-level reconnaissance and hyper-targeted strikes in cities.

The unmanned aerial vehicles (UAV) are still in the works, but once ready, could be available on the international market as a cheap and versatile option widening the gulf between America’s military in drone technology.

The drone is designed to be controlled by soldiers on the ground, has an operational distance of 5km (3 miles) and has a vertical range of 6km.

It will be loaded with infrared and laser detectors to enable night surveillance operations and is armed with two 50mm rockets designed to strike from up to 1km.

Sadly, there are no quality drone plays on the American public markets that I can confidently recommend.

The seriousness of the lack of investment really appears in the weakness of U.S. military drone capabilities and on the consumer side of things, drones will be a supercharger input to revenue growth for the likes of Walmart (WMT), Amazon, and the e-commerce companies.

It might be time to wake up and support the creation of a national champion in this critical technology then spin off the commercial synergies in similar fashion to how the personal computer and the internet developed.

The longer we wait, the further we fall behind.

Mad Hedge Technology Letter

November 27, 2019

Fiat Lux

Featured Trade:

(THE SAD TRUTH ABOUT DIGITAL MARKETING),

(FB), (YELP), (GOOGL)

Granted that technology companies have been the mule carrying the load for the broader market, beneath it is an ugly underbelly of venomous spirits.

Digital tech companies are frauds.

This could crater the broader market if the worst-case scenarios play out.

What do I mean by labeling them frauds?

Well, first, not all tech companies are charlatans. The ones producing components like semiconductor companies and others creating hardware are not the target of my wrath.

Since content has migrated into an all-out assault on traditional media, there is a dirty little secret that is festering because the new online media isn’t regulated.

The numbers are all a lie.

Much of the analytics and calculus involved with crafting cost to the other side is being entirely gamed by tech companies quoting prices based on fake analytics.

Instagram switched over its algorithm to displaying photos chronologically, to now display posts that engage the most, more specifically, what gets clicked the most.

Consumers have complained about it being significantly harder to gain likes and followers because, for the ones that don’t have many clicks, it’s harder to get those added clicks if your post is relegated down the feed.

The platform has also been a breeding ground for fabricating likes, friends, views, clicks and so on. Companies can be hired per like, resulting in a beefed-up profile built on fantasy.

Ad companies gauge each Instagram profile by the amount of engagement generated and if most of them are fraudulent likes, there will be weak follow-through in sales after ad purchases since a good chunk of the potential audience is a mirage.

Instagram is the preferred social platform of most influencers and Facebook is attempting to merge both assets into one in order to claim to regulators that they can’t be separated.

Much of digital marketing has migrated down the path of growing a large following for the reason to qualify as an effective brand ambassador and siphon off influencer marketing budgets from corporates who desperately want to penetrate a target audience.

In an age of automated robocalls and strict email rules, companies hesitantly confess that the only way to reach their end buyer is through social media channels.

Corporates are wasting billions of dollars because they aren’t getting what they really pay for and are basically being fleeced by tech companies.

And if you think this is mutually exclusive to Facebook (FB) and Instagram, it happens in every tech company that involves data.

Tech companies are monetarily incentivized to flat out lie about their data, partially because the penalties are minimal or absent in many cases.

Marginal tactics to fast-track the process by buying likes should be rooted out of the eco-system.

They are not only hurting the trust users have with the platform, but misrepresenting the brand that associates with a product.

Tech firms ward off anyone and everything from taking a peek at internal data by claiming it is their proprietary IP causing them to effectively police themselves.

That is not even the worst part of it all.

Parent company Facebook is turning a blind eye to something that could crash the company.

Mark Zuckerberg's old classmate Aaron Greenspan published a report complaining that over 50% of Facebook accounts are fake.

Facebook is on record admitting that between 2-3% of accounts are fake, but that number is a dream and artificially low by a country mile.

If it is true that half of Facebook accounts are fake, this would mean that Facebook sits on over 1 billion fake accounts.

Never mind the fake likes or clicks issue, Facebook shareholders could lose most of their worth in this stock if the truth is ever discovered.

Remember, the network effect works on the way down just like it works on the way up as a de-facto force multiplier.

Facebook and many other tech firms are a black box just like the Google (GOOGL) search algorithm.

Yelp (YELP), the online review company, could potentially sub-contract out fake reviews and never disclose how many of them are truly fake, they have no incentive to.

I recently stayed in an Airbnb rental whose active management was sub-contracted to a local property manager.

When I met him, he told me “This apartment was just bought and you are the first guest to stay in this apartment, so if there are any issues, please contact us as soon as possible.”

Wait, hold on, in my head, I am thinking, how did I see 45 great reviews from the apartment’s profile if I am the first guest?

I logged on to reread some reviews and some of the responses were completely inaccurate about the apartment.

It was clear these were made up and paid for and I was, in fact, the first to stay in this apartment like the property manager said.

Expectedly, there was more wrong with the apartment than just the fake reviews.

The television, stove, and hot water didn’t work, the key to the apartment was half broken and I had to perform miracles just to get the front door open.

There is a reckoning coming to technology companies because of the rampant misuse of the technology by nefarious actors monetizing the platform while perverting it.

Companies look the other way because they don’t want a revaluation of their business model which would add costs and, in some cases, bankrupt a company if the problem isn’t fixable.

As we move forward, the problems enlarge.

In a nutshell, this is why everyone hates tech now and its already stomach-churning enough that these firms steal your personal data and sell it to whomever they want.

A harsh reckoning will eventually hit the involved companies, but until then, tech business models are manipulated to the extreme and they continue to print real and fake growth mixed together as one.

One day, that fake growth will vanish and these companies will have to explain why to their shareholders.

In the meantime, just assume all online reviews are fake and enjoy the bull market in tech.

Global Market Comments

November 25, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or CATCHING OUR BREATH),

(MSFT), (GOOGL), (TLT), (VIX), (TSLA)

Mad Hedge Technology Letter

November 20, 2019

Fiat Lux

Featured Trade:

(MY CURRENT TECHNOLOGY TRADING STRATEGY),

(GOOGL), (MSFT), (APPL), (ADBE), (AKAM), (VEEV), (FTNT), (WKDAY), (TTD)

Some might say that we were due for a revaluation of growth tech stocks.

They have contributed greatly in this nine-year bull market.

Profit-generating software stocks are the order of the day.

Tech has led the overall market higher after projected quarterly earnings growth of -9% came in better than expected at -5%.

We have ebbed and flowed from pricing in a full-out recession in mid-2020 to now believing a recession is further off than first thought.

The pendulum swing ruptured many growth stocks from Workday (WKDAY) to The Trade Desk, Inc. (TTD) plummeting 30%.

We have retraced some of those losses but momentum in share appreciation has shifted to the perceived safer variation of tech stocks.

Investors have cut volatility and headed into bulletproof companies of Apple (AAPL), Google (GOOGL), and Microsoft (MSFT).

These companies have significant competitive advantages, Teflon balance sheets, and print money.

The tech markets just about priced in the U.S - China trade war in the fall as broad-based volatility plummeted because of optimism around making a deal.

This, in turn, has boosted chips stocks along with investors front running the 5G revolution and the administration granting Huawei a reprieve was a cherry on top.

The Mad Hedge Technology Letter has taken every dip to initiate new longs in safe trades like software companies Adobe (ADBE) and Veeva Systems (VEEV).

Tech is at the point that all loss-making companies are out of the running for tech alerts because the moment there is a recession scare, these shares drop 10% and often don’t stop until they lose 30%.

Now there is a deeply embedded set of narrow tech leadership by a few dominant tech companies buttressed by a select set of second-tier software stocks.

I would put PayPal (PYPL) and Twitter (TWTR), which I currently have open trades on, in the ranks of the second tier and they should do well as long as economic growth does better than expected.

Their share prices dipped on weak guidance and the bad news appears to have been shaken out of these names.

Professional investors could also be hanging on to meet end-of-year performance targets.

I do expect unique entry points on software stocks that drop after bad future guidance.

Profitability has moved to the fore as the biggest factor in holding a name or not.

Newly minted IPOs have fared even worse showing the markets' waning appetite for loss makers like Uber (UBER) and Lyft (LYFT).

Loss-making companies often tout their ability to change the world and disrupt industry, but that has been discovered as nothing more than a ruse.

They aren’t disrupting the way we change the world. For example, Uber is a dressed-up taxi service and the new CEO has failed to create any new momentum in the unit economics that spectacularly fail by any type of metric.

Even worse for these growth stocks, as the economy starts to falter, there will be even less appetite for them, and even more appetite for safer tech stocks.

A worst-case scenario would see Uber drop to $10 and Lyft to $20.

New all-time highs have crystalized with Google (GOOGL) under the gauntlet of regulation hysteria displaying the domination of these big tech machines.

The ongoing, consistent rotation out of growth and into value hasn’t run its course yet and fortunately, by identifying this important trend, our readers will be well placed to advantageously position themselves going into 2020.

Growth stocks won’t make a comeback anytime soon and deteriorating conditions could trigger renewed synchronized global monetary policy easing and central bank stimulus.

And yes, more negative rates.

I believe Oracle (ORCL), Fortinet (FTNT), Akamai Technologies, Inc. (AKAM) could weather the storm next year.

Tech growth is slowing and trade uncertainty is high, and readers must have a sense of urgency to avoid the losers in this scenario.

U.S. economic growth could slow to 1.3% next year, avoiding a recession, and the lack of enterprise spend will reduce software sales and combine that with peak smartphone growth and it won’t be smooth sailing.

The Mad Hedge Technology Letter has the pulse of the tech market and will show you how to navigate this minefield.