Mad Hedge Technology Letter

April 24, 2018

Fiat Lux

Featured Trade:

(WHAT THE MEDIA REALLY WANTS FROM YOU),

(TRNC), (AMZN), (FB), (GOOGL), (USPS), (SFTBY)

Mad Hedge Technology Letter

April 24, 2018

Fiat Lux

Featured Trade:

(WHAT THE MEDIA REALLY WANTS FROM YOU),

(TRNC), (AMZN), (FB), (GOOGL), (USPS), (SFTBY)

Publishing magnate and self-described populist William Randolph Hearst was a deep admirer of Adolph Hitler and did not shy away from using his newspapers as a de-facto mouthpiece spouting off Der Fuhrer's propaganda.

Hearst created content sympathizing with the Nazi ethos and even mobilized an embedded secret agent from the German government to act as a correspondent that followed hot, daily scoops inside Germany.

Hearst also used his publishing clout to pull the strings in the 1932 presidential election backing candidate John Nance Garner or "Cactus Jack" who later agreed to be Franklin D. Roosevelt's running mate.

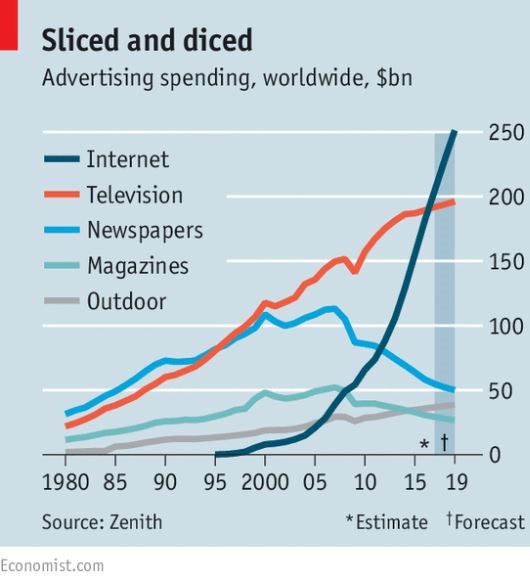

The fusion of politics and media has been chiseled into human DNA since antiquity. However, the purpose of newspapers has evolved significantly since it became impossible to break even about 10 years ago.

Print newspapers are a lot like the US Postal Service - they specialize in losing money.

However, the (USPS) was never politicized as was the publishing industry until President Trump managed to commingle the loss-making mail outfit and Amazon as a joint problem roiling society.

The politicization comes at a cost to society.

All the well-intentioned journalists involved in earnest and quality journalism lose out because the new normal for newspapers has evolved into a William Hearst-like blatant tool promoting targeted interests.

Do you ever wonder why the Washington Post hardly ever publishes content harmful to the image of Amazon?

Because it is owned by the same man, Jeff Bezos, who founded Amazon (AMZN) in 1994, as he cruised in his car cross-country from New York to Seattle where he would start his tech empire.

Effectively, Jeff Bezos has the ear of each corner of the political power grid in Washington.

And while the president has been attacking Bezos as a job destroyer on a daily basis, Amazon has in fact been the largest private job CREATOR in the US. It added a staggering 130,000 new jobs in 2017, and an eye-popping 560,000 jobs over the past 10 years.

Last year saw Laurene Powell Jobs, widow to Steve Jobs, acquire the Boston-based American magazine The Atlantic.

The Atlantic earns more than $10 million per year in revenue and lures in over 33 million readers per month.

Billionaire biotech investor Patrick Soon-Shiong reached a deal with Tronc Inc. (TRNC), which possesses a vast array of various legacy media assets, to take over the LA Times and San Diego Union-Tribune for $500 million.

Tronc Inc. is on the verge of catching another bid with SoftBanks' (SFTBY) Masayoshi Son, looking to scoop up parts of the extensive portfolio.

Private equity group Apollo and media firm Gannett Company are also in the mix to acquire Tronc Inc.

Some of Tronc Inc.'s crown assets are the Chicago Tribune, the New York Daily News, and the Baltimore Sun among other regional newspapers with a large audience base.

Tronc's shares spiked almost 10% on whispers of the rumored news.

The courting of these news media assets comes at a time when Google (GOOGL) is funding a project to automate more than 30,000 stories per month for the local media as a cost-effective way to advance the business model.

Quality journalism written by a human is the last thing in which these mega-tech companies are interested.

The first thought that came into my head when I heard about SoftBank's vision fund swooping in for another company was data grab.

We have seen this story time and time again.

Newspapers and how an online subscriber behaves on a digital newspaper platform offer valuable data points that cannot be extracted elsewhere.

The data will reveal the political ideas, topics of interest, and other sensitive information deduced into a comprehensive data profile.

Effectively, a company such as SoftBank will be able to create a functional shadow profile for almost anyone.

The concept of shadow profiling emerged from the acrimony of Mark Zuckerberg's testimony in Washington and could be the next point of heated contention.

What are shadow profiles?

Shadow profiles are digital profiles crafted by data that were not directly handed over to Facebook (FB) by the user.

This data is extracted through fringe third parties, other friends on Facebook if they post content unique to you, and specifically through the "find your friends" function that recommends the uploading of an entire digital address book giving Facebook access to everyone you know.

Scarily, there is no opt-out for shadow profiling, and there probably won't be another congressional testimony about this topic anytime soon.

If Facebook wanted to turn into the FBI, it would be easy.

The treasure trove of data would give insight on the subtle nuances of authentic human behavior.

This artificial profile would seem real.

If you are an Android user like most of the world, Google could fill out the most comprehensive profile with a high degree of accuracy on most people.

The scandalous bit about shadow profiling is that these profiles are whipped up even if a user has never signed up for Facebook.

Shadow profiling, along with other data, becomes more precise as the volume of data piles up. To understand the behavior, trends, and tastes of most of the world's population is incredibly valuable.

Facebook could use this shadow profiling data to understand the wide range of non-Facebook user behavior.

This way of monetizing data would be highly illegal if leaked to an actionable third party and would be significantly worse than the Cambridge Analytica scandal.

This data should be deleted immediately, but Facebook has a backdoor way to keep the data in the system.

If Facebook got slammed for data leakage then others are in danger, too. That's because Facebook is not the only player mining data for money.

It wouldn't be surprising if other large cap tech companies started to create these shadow profiles to get dirt on their competitors as well as other use cases.

Tech is evolving at such a fast pace. It subconsciously encourages the never-give-up mentality that coerces firms to stay one step ahead, which Amazon has been able to do since its inception.

Newspaper companies are next in line to be absorbed by large cap techs continuously expanding web assets that hyper-focus on exponential data generation.

These newspapers will defend tech's interests in the economy similar to how newspapers were used as William Hearst's rallying cry for politics.

Jeff Bezos has chosen silence to react to President Trump's tweet offensive, but he could easily mobilize his newspaper to protect Amazon's interests.

Bezos just shrugs his shoulders and goes about his day because he knows Washington cannot do anything to change Amazon's dominance at the top of the tech food chain.

Better take the high road.

Not only do these big tech companies know who you talk to, what you buy, and where you are, but now they are given deeper access into the identity of users.

Be on the lookout for these assets to get cherry-picked and look forward to reading your future newspaper owned by Google, Facebook and the usual cast of characters.

The recently elevated existential risk that big cap tech is coping with will see meaningful reforms that will implement better defensive tactics, pre-emptive posturing to promote a positive big-picture narrative, and a bulletproof attempt to protect the moats around lucrative business models.

Stay away from these legacy newspaper stocks and only weigh up the media stocks that have already pivoted to the online streaming business model of scaling original premium content.

__________________________________________________________________________________________________

Quote of the Day

"The real danger is not that computers will begin to think like men, but that men will begin to think like computers." - said journalist Sydney Harris.

Global Market Comments

April 23, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or HERE COMES THE FOUR HORSEMEN OF THE APOCALYPSE),

(SPY), (GOOGL), (TLT), (GLD), (AAPL), (VIX), (VXX), (C), (JPM),

(HOW TO AVOID PONZI SCHEMES),

(TESTIMONIAL)

Have you liked 2018 so far?

Good.

Because if you are an index player, you get to do it all over again. For the major stock indexes are now unchanged on the year. In effect, it is January 1 once more.

Unless of course you are a follower of the Mad Hedge Fund Trader. In that case, you are up an eye-popping 19.75% so far in 2018. But more on that later.

Last week we caught the first glimpse in this cycle of the investment Four Housemen of the Apocalypse. Interest rates are rising, the yield on the 10-year Treasury bond (TLT) reaching a four-year high at 2.96%. When we hit 3.00%, expect all hell to break loose.

The economic data is rolling over bit by bit, although it is more like a death by a thousand cuts than a major swoon. The heavy hand of major tariff increases for steel and aluminum is making itself felt. Chinese investment in the US is falling like a rock.

The duty on newsprint imports from Canada is about to put what's left of the newspaper business out of business. Gee, how did this industry get targeted above all others?

The dollar is weak (UUP), thanks to endless talk about trade wars.

Anecdotal evidence of inflation is everywhere. By this I mean that the price is rising for everything you have to buy, like your home, health care, college education, and website upgrades, while everything you want to sell, such as your own labor, is seeing the price fall.

We're not in a recession yet. Call this a pre-recession, which is a long-leading indicator of a stock market top. The real thing shouldn't show until late 2019 or 2020.

There was a kerfuffle over the outlook for Apple (AAPL) last week, which temporarily demolished the entire technology sector. iPhone sales estimates have been cut, and the parts pipeline has been drying up.

If you're a short-term trader, you should have sold your position in April 13 when I did. If you are a long-term investor, ignore it. You always get this kind of price action in between product cycles. I still see $200 a share in 2018. This too will pass.

This month, I have been busier than a one-armed paper hanger, sending out Trade Alerts across all asset classes almost every day.

Last week, I bought the Volatility Index (VXX) at the low, took profits in longs in gold (GLD), JP Morgan (JPM), Alphabet (GOOGL), and shorts in the US Treasury bond market (TLT), the S&P 500 (SPY), and the Volatility Index (VXX).

It is amazing how well that "buy low, sell high" thing works when you actually execute it. As a result, profits have been raining on the heads of Mad Hedge Trade Alert followers.

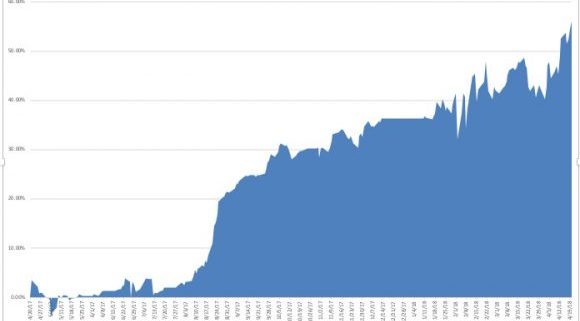

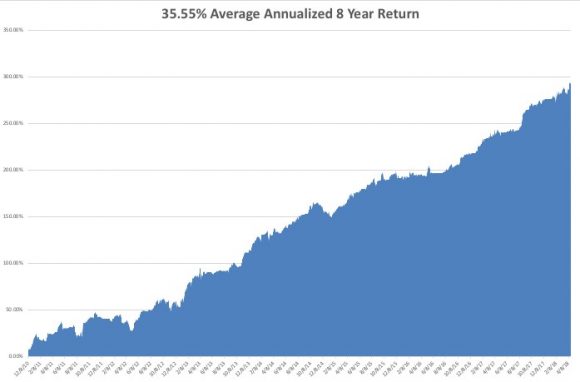

That brings April up to an amazing +12.99% profit, my 2018 year-to-date to +19.75%, my trailing one-year return to +56.09%, and my eight-year performance to a new all-time high of 296.22%. This brings my annualized return up to 35.55% since inception.

The last 14 consecutive Trade Alerts have been profitable. As for next week, I am going in with a net short position, with my stock longs in Alphabet (GOOGL) and Citigroup (C) fully hedged up.

And the best is yet to come!

I couldn't help but laugh when I heard that Republican House Speaker Paul Ryan announced his retirement in order to spend more time with his family. He must have the world's most unusual teenagers.

When I take my own teens out to lunch to visit with their friends, I have to sit on the opposite side of the restaurant, hide behind a newspaper, wear an oversized hat, and pretend I don't know them, even though the bill always mysteriously shows up on my table.

This will be FANG week on the earnings front, the most important of the quarter.

On Monday, April 23, at 10:00 AM, we get March Existing-Home Sales. Expect the Sohn Investment Conference in New York to suck up a lot of airtime. Alphabet (GOOGL) reports.

On Tuesday, April 24, at 8:30 AM EST, we receive the February S&P CoreLogic Case-Shiller Home Price Index, which may see prices accelerate from the last 6.3% annual rate. Caterpillar (CAT) and Coca Cola (KO) report.

On Wednesday, April 25, at 2:00 PM, the weekly EIA Petroleum Statistics are out. Facebook (FB), Advanced Micro Devices (AMD), and Boeing (BA) report.

Thursday, April 26, leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a fall of 9,000 last week. At the same time, we get March Durable Goods Orders. American Airlines (AAL), Raytheon (RTN), and KB Homes (KBH) report.

On Friday, April 27, at 8:30 AM EST, we get an early read on US Q1 GDP.

We get the Baker Hughes Rig Count at 1:00 PM EST. Last week brought an increase of 8. Chevron (CVX) reports.

As for me, I am going to take advantage of good weather in San Francisco and bike my way across the San Francisco-Oakland Bay Bridge to Treasure Island.

Good Luck and Good Trading.

Mad Hedge Technology Letter

April 19, 2018

Fiat Lux

Featured Trade:

(HOW ROKU IS WINNING THE STREAMING WARS),

(ROKU), (FB), (AMZN), (NFLX), (GOOGL), (BBY), (DIS)

The whole digital ad industry dodged a bullet.

Facebook (FB) CEO Mark Zuckerberg's wizardry on Capitol Hill will stave off the data regulation hyenas for the time being.

One company in particular is perfectly placed to reap the benefits.

The Facebook of online streaming - Roku (ROKU).

Roku is a cluster of in-house, manufactured, online streaming devices offering OTT (over-the-top) content in the form of channels on its proprietary platform.

The company has two foundational drivers propelling business - selling hardware devices and selling digital ads.

It pays dividends to be entrenched at the intersection of two monumental generational trends of cord cutters' mass migration to online streaming, and the disruption of the digital ad revolution that is shaking up traditional media giants.

The percentage of American homes paying for an online streaming service ripped higher to 55% of households, which is up from 49% the previous year.

This $2.1 billion per month spend on streaming service is specifically as a result of access to premium content at an affordable price relative to traditional cable bundles.

Roku is a microcosm of the healthy climate for quality technology stocks in 2018.

It is among countless other firms that leverage large-scale data or cloud tools to capture profits.

Roku is best of breed of smart TV platforms and is in the early stages of robust growth.

This year will be the first year Roku's ad revenue surpasses hardware sales, indicating strong platform growth.

Roku pinpointed building account user growth, top-line gross revenue, and enhancing the platform capabilities as ways to move the business forward.

This year will also be the first year Roku posts an overall profit.

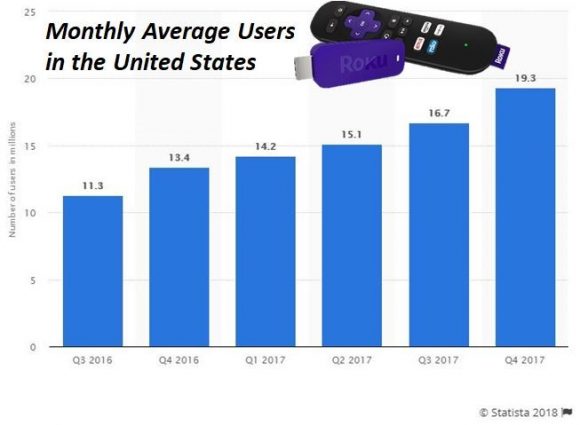

Active accounts grew 44% YOY to 19.3 million.

Roku offers consumers a cheap point of entry selling its Roku express box for only $29.99.

Its device is even free with a two-month purchase of Sling TV, which is the best online substitute to a legacy cable package. It has two sets of unique bundles available, charging $20 per month and $40 per month.

Once the Roku home screen populates, users can choose content through a la carte streaming options.

There is no monthly fee to operate Roku, and the device is used primarily by millennials.

More than 60% of 18- to 29-year-olds watch TV from online streaming, according to a Pew survey.

The quality and easy-to-use interface aids user navigation across the ecosystem.

It's the most convenient avenue to subscribe to multiple online streaming services all on one platform. It entices finicky users with extra mobility - those who love to jump around to different services based on particular upcoming content loaded up in the pipeline.

Many of these services offer no contract, cancel-anytime models that millennials love rather than the "old-school" rigid rules of cable providers that mostly charge a cancellation penalty of $300.

It is shocking how far traditional media fell behind the curve, but they are in rapid catch-up mode now.

Remember that content is king, and the overall boost in content quality has really shaken Hollywood executives to their core.

The golden age of streaming continues unabated with a Netflix 2018 annual content budget of $8 billion.

Roku does not create original content and it desires no skin in the game.

Content is expensive, and Roku would rather become the best place to host it.

Netflix's 2017 total revenue was a staggering $11.69 billion in 2017, and content costs will easily surpass 50% of total revenue in 2018. Overnight, it has become one of the biggest players in Hollywood, as its presence at the Emmy Awards amply demonstrates.

Exorbitant content costs are the new normal in 2018, and Spotify has reason to moan about the cost of content being 79% of total revenue.

Heightened content costs are the main reason why firms relying on content creation lose money each year.

However, as the overall pie grows, there is room for the tide to lift all boats. Being the premier platform to host premium content is why Roku's business model is eerily similar to Facebook's hyper-targeting ad model.

They make money the same way.

The incessant demand for online streaming functionality and smart TV operating systems show no signs of waning with Amazon (AMZN) announcing a new partnership with frenemy Best Buy (BBY) to produce smart TVs with Best Buy's in-house TV brand Insignia.

This is the first time Best Buy has been afforded a direct route to Amazon customers.

Disney (DIS) is turning around its legacy company into an online streaming behemoth announcing its first foray into online streaming with ESPN+.

Disney has tripled down on online streaming, acquiring New York-based BAMTech in late 2017, a company focused on developing streaming technology and made famous by its production of pro baseball's MLB TV.

BAMTech exudes pure quality. Anyone who has used MLB TV streaming service understands the great end-product it offers consumers.

The outstanding success with MLB TV attracted new online streaming converts to BAMTech to execute the transition to online streaming, including the WWE, Fox Sports, PlayStation Vue, and Hulu.

HBO went to BAMTech in 2014, after botching its attempt at creating a reliable stand-alone streaming service.

Disney's BAMTech-produced online streaming service will come to market in 2019, and will certainly be available on Roku TV.

Expect new blockbuster hits to debut on this new streaming service, such as new versions of Star Wars.

It is the perfect stock to mutate into an online streaming service because it possesses amazing content especially through ESPN.

The announcement of ESPN+ levitated Roku shares by 10% because investors understand this is the first baby step to shifting more of its content online.

This was on top of the announcement that Stephen A. Cohen's Point72 Asset Management had acquired a 5.1% stake in Roku for about $14 billion.

Furthermore, every major streaming service that enters Roku's system is worth an extra 5% to 10% bump in share price because of the wave of eyeballs and digital ads that grow Roku's coffers.

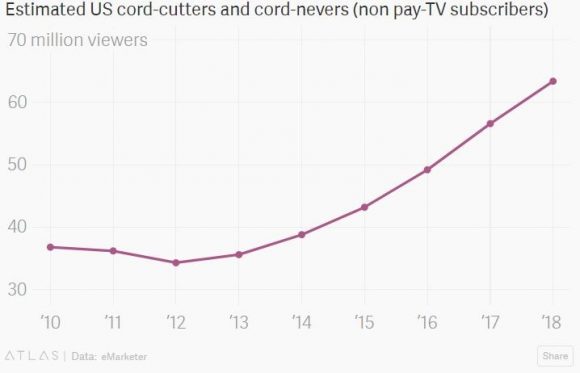

It is certain that 2018 and 2019 will sway more cord cutters to adopt Roku TV as this cohort approaches 70 million in 2018 on its way to 80 million in 2019.

The critical growth lever is its digital ad business as it hopes to take home a slice of this $70 billion per year business that is 75% controlled by Alphabet (GOOGL) and Facebook.

Roku has made great strides with half of Ad Age's top 200 advertisers already on the Roku interface.

Roku is taking the playbook right out from under Facebook's nose, piling funds into further enhancing its ad-tech division.

The blood, sweat, and tears shed is showing up in the financials with ARPU (Average Revenue per User) rocketing by 48% YOY, and more than 65% of this gap up is attributed to digital ad revenue.

Total revenue was up 29% YOY to $513 million, and platform revenue grew 129% in Q4 2017 to $85.4 million.

It is estimated that ad revenue will surpass $300 million in 2018, up from around $200 million in 2017.

Roku expects total revenue to grow 32% in 2018, approaching $700 million.

Profit margins are thriving under the platform segment, pumping out a stellar 74.6% in gross margin.

Roku does not make money on the hardware. Its push into ad distribution will ramp up as its digital ad revenue beelines toward an expected $700 million windfall by 2020.

Roku has a fantastic growth trajectory relative to other tech companies. Heightened volatility will make sell-offs hard to swallow but give fabulous entry points into a budding business.

The fertile path of international user adoption has barely scratched the surface. However, Netflix's successful foray abroad will inject confidence that Roku will have no problem expanding to greener pastures overseas as domestic account growth is always first to mature.

__________________________________________________________________________________________________

Quote of the Day

"AI is one of the most important things humanity is working on. It is more profound than electricity or fire." - said Google CEO Sundar Pichai

Mad Hedge Technology Letter

April 18, 2018

Fiat Lux

Featured Trade:

(WHY YOU SHOULD STILL BE BUYING FACEBOOK ON THIS DIP),

(FB), (GOOGL), (AMZN), (NFLX)

He did just enough.

He did 5% enough, but it should have been 10%.

That was the performance of the highly controversial data company Facebook (FB) in the wake of Mark Zuckerberg's (the aforementioned "he") testimony in front of politicians who failed to correctly pronounce his name let alone understand his business model.

But Zuckerberg did well.

Well enough that investors approved in droves.

Facebook shares tanked after the Cambridge Analytica scandal was disclosed, and the stock traded 16% below its February high.

The FANG stocks lost more than $200 billion in market value at one point when the headlines went viral.

Amazon (AMZN) and Netflix (NFLX) accounted for more than 30% of the S&P 500's 2018 gains in February, and their contribution has dipped to about 24% as of early April.

The leadership burden for large-cap tech is a resilient pillar propping up the equity market.

Let's get this straight - there has been no regulation as of yet but this moves forward any regulation that eventually was going to happen.

However, it could be a highly diluted version of any worst-case scenarios of which one could think.

The big question: Will earnings and guidance be sideswiped because of higher data costs?

And how many of the 2.2 billion MAU (Monthly Active Users) permanently deleted their Facebook accounts?

Facebook profile removals surged to 4,000 to 5,000 the first few days after the news hit and decreased to 2,000 per day in late March. The numbers further subsided to 1,000 at the start of April.

Deletions around the political testimony were clocking in between 1,000 to 2,000 per day.

To put this into perspective, the extirpation of accounts was only about 30% of the Snapchat rebellion where users quit in hoards because of a sub-optimal design refresh.

The media has done its best to sensationalize events and avoid the fact that hyper-targeting ad models has been around for years and has been used by various companies.

Facebook is not the only one.

Bottom line, there has been no material damage to user volume, and the testimony will empower tech because of Washington's botched question session.

Most of Facebook's profits come from less than 10% of user accounts.

Facebook is a one-trick pony with 98% of profits coming from ad revenue.

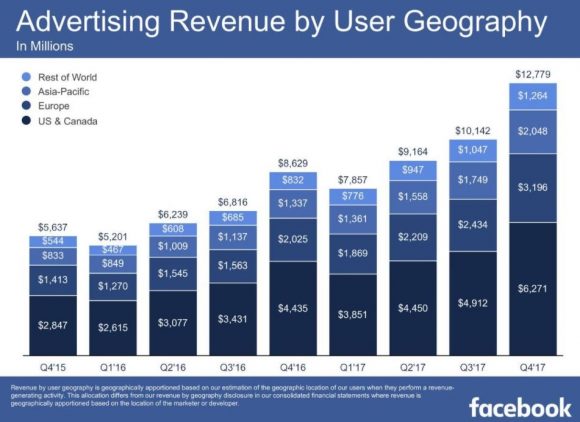

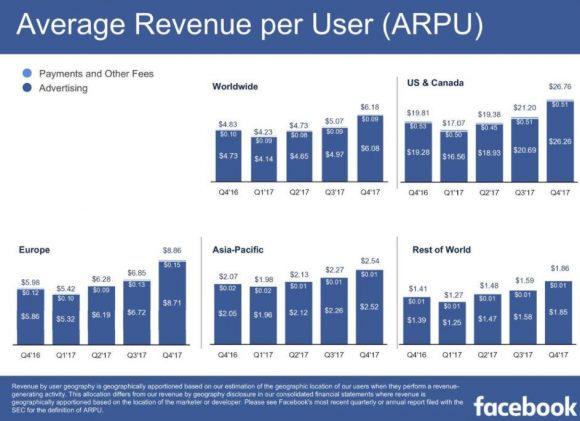

To add granularity, the bulk of revenue derives from developed nations mainly from North America, which make up more than 50%, and Europe at about 30% of total revenue.

Falling user engagement from the developed English speaking world would be a canary in the coal mine.

I am not talking about a few thousand profile deletions. However, a mass removal of 50,000 profiles or 100,000 profiles per day would throw Mark Zuckerberg into a tizzy.

If Facebook can convince users to stick around then Mark Zuckerberg is the ultimate winner.

With all the fearmongering, some facts get swept under the carpet. And it could be the case that many users are fine with Facebook possessing large swaths of their personal data.

In reality, users might prefer Facebook to Washington when it comes to possessing their personal information.

The performance of politicians lined up to interrogate Mark Zuckerberg was an unmitigated disaster for the political elite.

It is clear there is a competency issue with politicians. The generation bias has given us a fleet of politicians who have almost zero grasp of technology and its pervasive use in America's economy.

Many politicians showed a weak grasp of Facebook's profit engine.

Some politicians were more focused on Facebook's diversity policy than the real issue at hand.

Let's not forget Zuckerberg also controls 60% of voting rights through his accumulation of Facebook Class B shares and has an iron grip on any direction where the company traverses.

Any meaningful regulation costs will be passed onto the advertisers as a cost of doing business.

This is the key lever investors don't fully understand.

Facebook currently uses an auction-based system for ad pricing but could easily slip in stand-alone regulatory fees to compensate the extra costs.

The industries move from CPC (cost per click) to CPM (cost per impression) including duopoly playmate Alphabet (GOOGL) is a great strategy to pad profits.

The only real incurred cost to Facebook is the in-house DevOps team responsible for platform enhancement.

Facebook tried to experiment in 2016 by charging Facebook-owned smartphone messaging service WhatsApp users a $1 per year fee to use the messaging service.

It has done the groundwork to roll out a mass paid service.

Facebook later decided against this move as many users of WhatsApp are from undeveloped countries with no access to credit card payment services.

Zuckerberg is awkward. However, he has come a long way since his hoody days, even using smoke and mirrors to wriggle out of probing questions.

Half the "grilling" he received in Washington was met with the same vanilla answer saying that his team will get back to them.

The peak of evasiveness was Zuckerberg's response to a question about the willingness to change the business model in the interest of protecting individual privacy.

Zuckerberg stated he was "not sure what that means."

The hammering in Facebook shares was overdone.

It is obvious Washington is no match for large cap tech.

Facebook's upside trajectory has been sacrificed in the short term, but one could argue regulation was on the way - regardless of this data breach.

Regulation is a natural progression for an industry with almost no meaningful regulation.

Therefore, a little regulation for tech does not mean the end of tech.

Facebook is not going out of business. Not anytime soon.

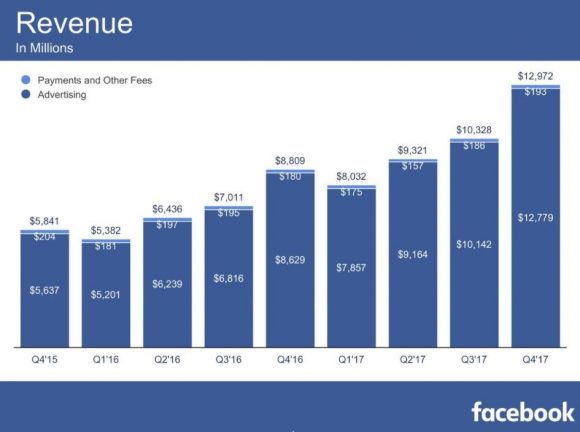

Facebook earned revenue of $27.64 billion in 2016, on the back of $40.65 billion in 2017.

Facebook does not need to be "fixed" - it just needs a few bandages in place before it goes back onto the field.

These bandages will damage operating margins that are currently at 57% in Q4 2017, but their long-term fundamentals are still intact.

The wall of worry is unfounded and ad engagement is still solid.

Facebook is in store for record bottom- and top-line numbers when earnings come out. Ad revenue numbers and the guidance will be the key metric to digest.

Investors might want Zuckerberg to kitchen sink the quarter because most of the bad news is already priced into the stock and might as well dig out all the skeletons in the closet.

Regulation is positive for Facebook because Facebook and the rest of the FANGs are in the best position to confront the regulations. The worst case scenario is finding a backdoor way to navigate through the new rules just as the backdoor way of profiting through ad distribution.

The headline hysteria makes it seem like Facebook is about to go under and file Chapter 11.

The bar has been set so low for upcoming earnings that any reasonable guidance will be seen as a victory.

Advertisers have no choice but to pay for Facebook ads if they want to grow business - that has not changed.

Facebook is growing so fast that the CEO could not name the competition when he was asked at the hearing.

There is a huge short squeeze setting up for the next earnings report due out on April 25, 2018.

Lastly, WhatsApp recently surpassed 1.5 billion MAU with users sending more than 60 billion messages every day.

Remember that Mark Zuckerberg purchased WhatsApp when it had around 500 million MAU back in February 2014.

This service hasn't even started to monetize yet and was a genius piece of business for $19.3 billion in 2014.

The valuation is at least double to triple the price of purchase now but seemed ludicrously expensive when Facebook snapped it up at the time.

Facebook has bottomed out, and the added bonus is it is quite insulated from all the tariff chaos whipsawing the equity markets.

__________________________________________________________________________________________________

Quote of the Day

"I'm on the Facebook board now. Little did they know that I thought Facebook was really stupid when I first heard about it back in 2005."- said founder and CEO of Netflix Reed Hastings

Global Market Comments

April 16, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THE WEEK THAT NOTHING HAPPENED),

(TLT), (GLD), (SPY), (QQQ), (USO), (UUP),

(VXX), (GOOGL), (JPM), (AAPL),

(HOW TO HANDLE THE FRIDAY, APRIL 20 OPTIONS EXPIRATION), (TLT), (VXX), (GOOGL), (JPM)

This was the week that American missiles were supposed to rain down upon war-torn Syria, embroiling Russia in the process. It didn't happen.

This was the week that the president was supposed to fire special prosecutor Robert Mueller, who with his personal lawyer is currently reading his private correspondence for the past decade with great interest. That didn't happen either.

It was also the week that China was supposed to raise the stakes in its trade war with the United States. Instead, President Xi offered a conciliatory speech, taking the high road.

What happens when you get a whole lot of nothing?

Stocks rally smartly, the S&P 500 (SPY) rising by 2.87% and the NASDAQ (QQQ) tacking on an impressive 3.45%. Several of the Mad Hedge long positions jumped by 10%.

And that pretty much sums up the state of the market today.

Get a quiet week and share prices will naturally rise, thanks to the power of that fastest earnings growth in history, stable interest rates, a falling dollar, and gargantuan share buybacks that are growing by the day.

With a price earnings multiple of only 16, shares are offering investors the best value in three years, and there is very little else to buy.

This is why I am running one of the most aggressive trading books in memory with a 70% long 30% short balance.

Something else unusual happened this week. I added my first short position of the year in the form of puts on the S&P 500 right at the Friday highs.

And, here is where I am sticking to my guns on my six-month range trade call. If you buy every dip and sell every rally in a market that is going nowhere, you will make a fortune over time.

Provided that the (SPY) stays between $250 and $277 that is exactly what followers of the Mad Hedge Fund Trader are going to do.

By the way, 3 1/2 months into 2018, the Dow Average is dead unchanged at 24,800.

Will next week be so quiet?

I doubt it, which is why I'm starting to hedge up my trading book for the first time in two years. Washington seems to be an endless font of chaos and volatility, and the pace of disruption is increasing.

The impending attack on Syria is shaping up to more than the one-hit wonder we saw last year. It's looking more like a prolonged air, sea, and ground campaign. When your policies are blowing up, nothing beats like bombing foreigners to distract attention.

Expect a 500-point dive in the Dow Average when this happens, followed by a rapid recovery. Gold (GLD) and oil prices (USO) will rocket. The firing of Robert Mueller is worth about 2,000 Dow points of downside.

Followers of the Mad Hedge Trade Alert Service continued to knock the cover off the ball.

I continued to use weakness to scale into long in the best technology companies Alphabet (GOOGL) and banks J.P. Morgan Chase (JPM), and Citigroup (C). A short position in the Volatility Index (VXX) is a nice thing to have during a dead week, which will expire shortly.

As hedges, I'm running a double short in the bond market (TLT) and a double long in gold (GLD). And then there is the aforementioned short position in the (SPY). I just marked to market my trading book and all 10 positions are in the money.

Finally, I took profits in my Apple (AAPL) long, which I bought at the absolute bottom during the February 9 meltdown. I expect the stock to hit a new all-time high in the next several weeks.

That brings April up to a +5.81% profit, my trailing one-year return to +50.23%, and my eight-year average performance to a new all-time high of 289.19%. This brings my annualized return up to 34.70%.

The coming week will be a slow one on the data front. However, there has been a noticeable slowing of the data across the board recently.

Is this a one-off weather-related event, or the beginning of something bigger? Is the trade war starting to decimate confidence and drag on the economy?

On Monday, April 16, at 8:30 AM, we get March Retail Sales. Bank of America (BAC) and Netflix (NFLX) report.

On Tuesday, April 17, at 8:30 AM EST, we receive March Housing Starts. Goldman Sachs (GS) and United Airlines (UAL) report.

On Wednesday, April 18, at 2:00 PM, the Fed Beige Book is released, giving an insider's view of our central bank's thinking on interest rates and the state of the economy. Morgan Stanley (MS) and American Express (AXP) report.

Thursday, April 19, leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a fall of 9,000 last week. Blackstone (BX) and Nucor (NUE) report.

On Friday, April 20, at 10:00 AM EST, we get the Baker Hughes Rig Count at 1:00 PM EST. Last week brought an increase of 8. General Electric (GE) and Schlumberger (SLB) report.

As for me, I'll be heading into San Francisco's Japantown this weekend for the annual Northern California Cherry Blossom Festival. I'll be viewing the magnificent flowers, listening to the Taiko drums, eating sushi, and practicing my rusty Japanese.

Good Luck and Good Trading.