Mad Hedge Technology Letter

May 29, 2019

Fiat Lux

Featured Trade:

(CHINA TO BAN FEDEX)

(HUAWEI), (AMZN), (FDX), (UPS), (DPSGY), (BABA), (ZTO)

Mad Hedge Technology Letter

May 29, 2019

Fiat Lux

Featured Trade:

(CHINA TO BAN FEDEX)

(HUAWEI), (AMZN), (FDX), (UPS), (DPSGY), (BABA), (ZTO)

Sell any and all rallies in FedEx (FDX) – that’s my quick takeaway from the Chinese communist party publishing a sharp retort to their de-facto mouthpiece of a publication called the Global Times signaling FedEx’s imminent demise in greater China.

The Global Times is often used as thinly veiled statements to a wider global audience and mimics the ideology of the ruling communist party and their main positions on critical issues.

As regards to FedEx’s business in China, it said:

“There are rising calls for China's postal service regulator to cut off FedEx from China market, as Huawei has accused the US express courier of diverting and rerouting its packages.”

FedEx is crushing the Chinese logistics market currently and is the go-to carrier holding firm at 54.6% market share.

They have been around in China for as long as the economic boom has percolated inside the mainland from 1984, far before any of its local competitors were even up and running by a decade or two.

FedEx’s latest acquisition of Dutch-based TNT Express in 2016 solidified its dominance.

Foreign competition is a mainstay of international shipping patterns in China with the top three rounded out by DHL (DPSGY) with a 25.07% market share and United Parcel Service (UPS) with a 16.94% market share.

If these assertive claims do result in FedEx meaningfully losing China revenue, UPS wouldn’t stand to pick up the leftovers and could be put out to pasture by the same issue of hailing from a country that has an active adversarial economic policy against China’s.

If anyone would benefit, it would by DHL, given that Germany has a far less hawkish stance towards China, and they are unwilling to bite off the hand that feeds them.

The current situation is a concerning sign for the future of Germany as an industrial power and ability to sustain itself against China Inc.

It could be somewhat true that Germany has overextended themselves and only time, Made in China 2025 project, and the mood of the Chinese communist party can delay the inevitability of full tech hegemony over their western European counterpart.

The communist party could choose to just bypass DHL altogether and kick out all foreign invaders gifting courier responsibilities to Alibaba-based (BABA) subsidiaries and the likes of ZTO Express (ZTO) who provide express delivery and other value-added logistics services in China.

DHL will hope that China delays any draconian measures and pray that its active partnership with a local logistic firm has real legs.

DHL's revenue sharing agreement with SF Express does not preclude them from the anger of Chinese regulators, but the risk of Chinese regulators favoring local couriers has risen another 25%.

Playing by the rules goes a long way in China, even if they change every day, and for customers across DHL’s target audience of industries including technology, health care, retail, automotive, and e-commerce.

DHL CEO Frank Appel said, "Combined with our global operations standards and network support, the agreement provides a solid foundation to continue exploring further opportunities in China in the coming years."

From an outside perspective, this sounds more like forced cooperation with forced technology transfers with the mainland companies slurping up Germany tech knowhow.

Doing a deal with the devil for access to a 1.3 billion customer market is being put through the ringer.

When I view the snippets through the lens of geopolitics, it’s hard to believe that at such a sensitive time, FedEx would actively “reroute” packages and knowingly approved this behavior, they simply can’t be that clumsy.

The situation smells like an overt show of nationalism by a group of individuals, and it questions the longevity of FedEx operating in China all the same.

FedEx promptly responded confessing:

“We regret that this isolated number of Huawei packages were inadvertently misrouted.”

An unintentional mistake offered a golden opportunity to tie the logistics company to the U.S. government’s aggressive nature and going forward FedEx will remain in a shroud of mystery until investors can get further grips on the rates of growth of their Chinese operations.

If FedEx were afraid about this, then they must be tearing their hair out about the domestic behemoth that is Amazon (AMZN) and their desires to install a full-service logistic service to blanket FedEx from e-commerce deliveries.

This has been the initial premise of my short call on FedEx, which has proved correct, and the regulatory nightmare in China will cast another cloud around its business.

Any strength in FedEx shares will be met with a cascade of selling activity, and as the economy slows down because of tariff-induced headwinds, this is a stock to outright short.

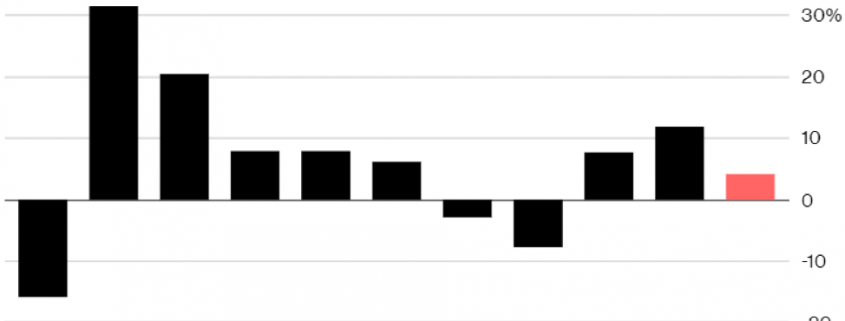

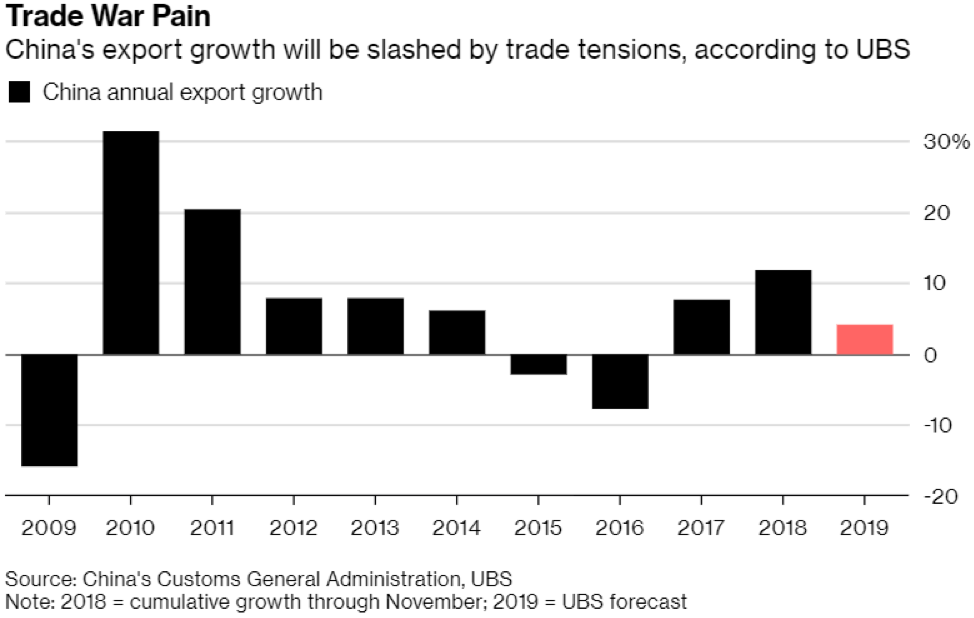

Back to China, FedEx slashed its full-year profit forecast for the second time in three months after reporting weaker-than-expected third quarter earnings.

The Chinese economy is absolutely slowing down, and its effects are impacting surrounding Asian nations.

Manufacturing cuts will cause the number of courier packages to slide in China and there is no telling how bad this trade stand-off could get.

It doesn’t look good for FedEx, and I reiterate my short stance on the company.

Mad Hedge Technology Letter

May 21, 2019

Fiat Lux

Featured Trade:

(HUAWEI HITS THE FAN)

(HUAWEI), (MU), (NVDA), (GOOGL), (FB), (TWTR), (APPL)

If you ever needed a signal to stay away from chip stocks short-term, then the Huawei ban by the American administration was right on cue.

Huawei, the largest telecommunications company in China, is heavily dependent on U.S. semiconductor parts and would be seriously damaged without an ample supply of key U.S. components

The surgical U.S. ban may cause China and Huawei to push back its 5G network build until the ban is lifted while having an impact on many global component suppliers.

The Chinese communist party has exhibited a habit for retaliation and could target Apple (AAPL) who is squarely in their crosshairs after this provocative move.

At a national security level, depriving Huawei of U.S. semiconductor components now is still effective as China’s chip industry is still 5 years behind the Americans.

China has a national mandate to develop and surpass the U.S. chip industry and denying them the inner guts to build out their 5G network will have long-lasting ramifications around the world.

Starting with American chip companies, they will send chip companies such as Micron (MU) and Nvidia (NVDA) into the bargain basement where investors will be able to discount shop at generational lows because of a monumental drop in annual revenue.

Even worse for these firms, Huawei anticipated this move and stocked itself full of chips for an extra 3 months, meaning they were not going to increase shipments in a meaningful way in the short-term anyway.

This kills the chip trade for the rest of the first half of 2019, and once again backs up my thesis in avoiding hardware firms with Chinese exposure.

Alphabet (GOOGL) has cut ties with cooperating with Huawei and that means software and the apps that are built around the software too.

Gmail, YouTube, Google Maps and Chrome will be removed from future Huawei smartphones, and even though this doesn’t amount to much in mainland China, this is devastating for markets in Eastern Europe and Huawei smartphone owners in the European Union who absolutely rely on many of these Google-based apps and view Chinese smartphones as a viable alternative to high-end Apple phones.

Users who own an existing Huawei device with access to the Google Play Store will be able to download app updates from Google now, but these same users will not consider Huawei phones in the future when the Google Play Store is banned forcing them to go somewhere else for the new upgrade cycle.

The fallout further bifurcates the China and American tech ecosystems.

I would argue that China had already banned Google, Facebook (FB), Twitter (TWTR), and marginalized Amazon (AMZN) before the trade war even started.

The American government is merely putting in place the same measures the Chinese communist party has had in place for years against foreign competition.

The recent ban on Huawei was a proactive response to China backing away from negotiations that they already had verbally agreed upon after hawks inside the Chinese communist party gained the upper hand in the tireless fight against the reformist.

These hawks want to preserve the status quo because they benefit directly from the current system and economic structure in place.

The American administration appears to have taken on an even more aggressive tone with the Chinese, as the resulting tariffs are putting even more stress on the Chinese hawks.

However, there is only so much bending they can do until a full-scale fissure occurs and debt rated “A” which is its third-highest classification has recently been slashed to a negative outlook as the tariff headwinds pile up.

The U.S. administration could further delve into its party bag by rebanning Chinese tech firm ZTE who almost folded after the first ban of U.S. semiconductor components.

The U.S. administration is emboldened to play the hand they have now because as long as Chinese tech need U.S. chips, the ball is in the American’s court and going on the offensive now would be more effective than if they carried out the same strategy in the future.

China is clearly attempting to delay the process enough to get to the point where they can install their own in-house chips and can say adios to America and the chips they currently rely on.

It’s doubtful at the current pace of escalation if China can survive until that point in time.

How will China react?

Massive easing and dovishness by the Chinese central bank will be needed to maintain stability and remedy the economy.

The manufacturing sector will face another wave of mass layoffs and debt pressures will inch up.

Chinese exports will get slashed with international corporations looking to move elsewhere to stop the hemorrhaging and rid itself of uncertainty.

Many Chinese tech companies will have entire divisions disrupted and even shut down because of the lack of hardware needed to operate their businesses.

Imagine attempting to construct a smartphone without chips, almost like building a plane to fly without wings.

This is also an easy to decode message to corporate America letting them know that if they haven’t moved their supply chains out of China yet, then time is almost up.

Going forward, I do not envision any meaningful foreign tech supply chain that could survive operating in mainland China because nationalistic forces will aim for revenge sooner or later.

There are many positives to this story as the provocative decision has been carried out during a time when the American economy is fiercely strong and firing on all cylinders.

Unemployment is spectacularly low at 3.6%, the lowest rate since 1969, while wage growth has accelerated to 3.8% annually up from 3.4%.

The robust nature of the economy has led to stock market performance being incredibly resilient in the face of continuous global headline risk.

The positive reactions are in part based on the notion that investors expect the Fed Governor Jerome Powell to adopt an even more dovish stance towards rates.

It’s almost as if we are back to the bad news is good news narrative.

Each dip is met with a furious bout of buying and even though we are trudging along sideways, for the time being, this sets up a great second half of the year as China will be forced to fold or face mass employment or worse offering at least a short-term respite for investors to go risk on.

As for the chip sector, high inventories on semiconductor balance sheets and in the channel will continue, as well as weak end demand in nearly every semiconductor end market meaning a once-in-a-generation magnitude of memory oversupply.

The trade war will most likely turn for the worse giving investors even more beaten down prices that will turn into great entry points when the time is ripe.

If you can’t handle the heat, then get out of the kitchen.

Well, the kitchen is getting a little bit toasty right now.

Apple (AAPL) was handed down a demonstrably negative verdict when a regional Chinese court ruled that they infringed on two patents belonging to Qualcomm (QCOM).

The Qualcomm chips were connected to photo editing and another to swiping on a touch-screen device.

This means that Apple won’t be able to sell legacy iPhone models in China which is a damaging blow to revenue prospects because older iPhone models in China offer attractive price points to wallet-light Chinese.

And when you add this all up, the ban includes over half of the iPhones on sale in China.

In general, less affordable, sleeker, fresher iterations price out many Chinese who want a piece of the Apple dream.

Even though this was a nice victory for Qualcomm, it spells trouble for the broader tech sector.

Apple’s myriad of chip suppliers who have grappled with a torrent stream of woeful news this year relating to Apple’s supply of iPhones and supply forecast of iPhones are first on the chopping block.

It’s also an excruciating blow to American business in China and this could potentially rule out any American management taking future business trips to China.

Apple looks set to join its chip company compadres on the sidelines as a stock to avoid like the plague at the moment.

Apple is a great company and a perfect hold to eternity stock, but this is not the time to jump in and out of it.

Let me explain why.

The trade war centered on future technological hegemony is directly connected to the domination of current technology in artificial intelligence, chip development, and 5G.

China has been furiously catching up to American tech the last two decades through its vast program of foreign technological forced transfers and outright intellectual property theft.

I remember testing my first shoddy Chinese smartphone from the Chinese company Coolpad to gauge a sample of the burgeoning Chinese consumer device market on a blistering hot day in Beijing in the summer of 2010.

It was one of the first iterations of Chinese smartphones on the local market and the 3G smartphone was simply terrible.

The hardware was iffy, software was untenable, design was hodgepodge and it ceased working after 3 painstaking months of testing.

I breathed a sigh of relief because I knew it would be years before Chinese tech could ever produce something material.

Since then, China and the love given to its tech sector through the state protecting its homegrown companies have come a long way since those teething years filled with shabby products and inferior expertise of yesteryear.

Chinese cell phones are now comparable to iPhones for a fraction of the cost especially the new Huawei and Xiaomi models and the companies want recognition for their success.

I have interviewed scores of Huawei engineers who describe a life of grinding out a modest existence in mega-cities dotted around China.

They lament the 12-hour back-breaking work days, suffocating authoritarian management style, and the 3am on-call staff meetings, but they rejoice in the accomplishment of collecting that down payment for a standard Chinese apartment in a subpar constructed building.

They earn 30% of what Apple engineers make per year just to seize an average life in a second-tier Chinese city.

They don’t complain and accept it as a consequence of cut-throat competition in a country of 1.3 billion trying to hustle the best they can.

These unbearable timelines and the crunch to develop the national brand of Huawei and its other protected tech behemoths is how China rose up from the ashes of irrelevancy to become arguably competitive with the American tech machine that is Silicon Valley.

Even through all of the local hyper-growth, there was one unwritten rule that allowed one squeaky clean American company from Cupertino to evade all of the fractious competition and make an absolute killing in China.

Apple was protected in China before until now that is.

I find it dubious that the timing of the court verdict was the first business day after the arrest of CFO of Huawei Meng Wanzhou.

By connecting the dots, this appears as if it was an indirect ruling from the higher-ups signaling that Apple won’t be handed a free pass anymore and a warning shot fired to Washington.

Even worse, the Chinese regulatory environment is opaque at best-giving discretion to Chinese authorities to do as they see fit.

The opaque nature of Chinese regulation can draw out cases for years potentially drowning out the sales of iPhones and banishing Apple and its products in China to the history books.

That is the worst-case scenario that probably won’t happen.

For Apple to even appeal this ruling offers Steve Jobs' brainchild a rare dose of reality in China, and the bruised Apple brand will go back to the drawing board after receiving severe harm to its previous image of an ultra-luxury brand on the Chinese mainland.

For other American companies, there is no way to flush out additional clarity, and they will get stonewalled if they want more details regarding the path forward and that in itself will damage the price action of stocks tilted towards China because of the wave of uncertainty.

At the extreme minimum, this escalation of pressure will make it arduous to maneuver to some sort of trade agreement let alone in the abbreviated 90-day window agreed on in Buenos Aires.

The Chinese national psyche cares a great deal about saving face and this dig at its national prize will be hard to forget.

And China has a habit at looking at these types of events as inclusive actions tallied up broadly inside a comprehensive portfolio labeled and pigeonholed as America, Canada, and so on.

This conspicuous move has pushed forward Canada into the forefront of the firing line which could become the silver lining to this quagmire because Canada will have more incentive to join in on the China rebukes with America if they get blacklisted by Beijing.

Uniting together as one pan-North American and the European task force would be the best method to combat China’s stealthy business acumen whose capital and influence are far-flung and hard to quantify because of its various gateways to global western pressure points.

I can tell you right now that after doing a quick jaunt of Belarus, the Ukraine, and Hungary this winter, China’s deep pockets and nationals have completely taken over Central and Eastern Europe.

Chinese companies and products are plastered all over the place in each Russified city center and cityscapes built in the Soviet era.

Chinese students and workers have flooded these markets as they line up around the fringes of the Western world armed with gobs of capital and a land-grab mentality that borders Amazon’s ambition.

The Budapest property market has been cornered by Chinese citizens looking for the cheapest entry point to permanent residence in the Eurozone.

If you want to rent a flat in Budapest, odds are a Chinese owner will be glad to accept your monthly rent payments.

China believes that to truly have its tentacles deep inside the Western apparatus, they must initially corner the peripheries of the Western World that thirst for capital to build up local economies to match the power and stature of the Western big boys.

This has all added up to the Chinese government having an influential voice in European affairs because they have direct sway with conservative Prime Minister of Hungary Viktor Orban who has accepted Chinese capital.

US executives are praying to the celestial heavens that Meng is not extradited to America and made the scapegoat of the broader trade war.

This would be a bitter pill to swallow for Huawei’s founder Ren Zheng Fei whose family is considered royalty inside the upper-level Chinese establishment.

I assume that Ren will not back down quietly and is pushing and pulling the behind-the-scenes levers to do what he can for his daughter.

What does this all mean?

Headline risk has shot through the roof and investors could hear any day of the rumblings to the next chapter of the trade saga that is enveloping more and more corporate collateral damage.

Apple’s next quarter’s earnings are also on the line, and CEO of Apple Tim Cook could conveniently use it as a throwaway quarter hyping its progression as a new software and subscriptions company which is indeed in the works.

I figure this is the base case for Apple especially if there is no quick solution to this new iPhone ban.

The transition has been dramatically painful and happened a year or two too early for Apple’s liking.

Consequently, Apple reigning in its expectations has crushed the stock recently.

Certain global banks could set to be punished after the Wall Street Journal reported that HSBC and Standard Chartered facilitated the illegal payments for Huawei.

The British bank problems don’t stop there with Britain as a country barreling towards a complete ban of Huawei products after New Zealand just announced their own ban.

The three biggest Japanese telecommunication companies dumped fuel on Huawei’s bonfire citing security issues for excluding Huawei products from Japanese 5G development.

The roller-coaster action could also give impetus to Chairman Xi to execute a power grab on Chinese domestic technology sector gifting him additional control over tech behemoths in the name of national security fortifying his multiplying power in China.

He did the same with the People Liberation’s Army and I see no reason why he wouldn’t do the same with the Chinese tech sector especially if western countries avoid Huawei products.

The Chinese regulatory presence has already reared its ugly head banning new video game licenses to Tencent slashing revenue streams in 2018.

That is why Tencent shares have grossly underperformed this year.

Theoretically, Xi could use this moment as a springboard to seize the reigns of Huawei citing illegal payments to Iran which would calm the trade tensions but beef up his clout in the tech community, a net negative for Silicon Valley.

In any case, there is substantial amount of uncertainty permeating the heart of the technology movement that could potentially splinter off violently into an American tech and Chinese tech world.

This hard landing would deprive China-based revenue and kill supply chains for American technology that have spent decades procuring these intricate systems.

For Chinese technology, they could be cut off from the important components required to develop the technology and chips they need to achieve its “Made in China 2025” state-subsidized targets aimed at rapidly expanding its high-tech sectors and developing its advanced manufacturing base.

The next few months will reshape the 2019 Silicon Valley landscape and certain companies are hoping their business models aren’t fully destroyed.

I can’t lie but I saw this coming when I became aware of the complicated relationship between foreign tech companies and its precious Chinese revenue, and I also never bought another Coolpad smartphone.

Mad Hedge Technology Letter

December 6, 2018

Fiat Lux

Featured Trade:

(A BIG ESCALATION OF THE TRADE WAR)

(INTU), (MSFT), (HUAWEI), (SQ), (ABDE)

CFO of Huawei Meng Wanzhou was arrested transiting in Vancouver and is facing extradition to the United States to face the accusation that she violated sanctions against Iran.

This doesn’t help calm the nerves of tech investors. Not at all.

Wanzhou is the daughter of Founder and President of Huawei Ren Zhengfei who springboarded to success after his close ties to the People’s Liberation Army helped propel his career in technology when Shenzhen opened up its economy in the 1980s.

He has never looked back since then developing Huawei into one of the key cogs of the global telecommunications infrastructure.

Huawei’s rapid ascent has been the defacto Achilles heel between the United States and Chinese tech relations gone sour.

China is hell-bent on dominating 5G and beyond, and the Chinese communist views Huawei as a critical component to executing this vision.

That being said, there are plenty of tech stories out there that are worth a look irrespective of the macro headaches.

In a time like this, avoiding China-themed tech stocks would offset some volatility as shares have been on a rollercoaster because of issues unrelated to the companies themselves.

Software companies with income streams closely linked to domestic revenue is a trope that I have recommended and will outperform the pure tech growth stocks in 2019.

A company that epitomizes these traits is Intuit (INTU). The problem with it is that it is too expensive right now as well as having growth-related road bumps.

Intuit is a company your family tax accountant loves and hates.

It is a financial software taking care of financial, accounting, and tax preparation for small businesses, accountants, and individuals.

The company is headquartered in Mountain View, California.

The bulk of its revenues derive from operations within the United States and that is music to my ears right now in this climate.

Intuit also owns TurboTax which is one of the most popular domestic income tax preparation software packages in the United States.

Quickbooks Online, another type of accounting software owned by Intuit, is the firm’s bread and butter product and expanded over 40% YOY.

Even with this premium growth, the small business unit was only able to grow 11% YOY.

Quickbooks Online now has 3.6 million subscribers demonstrating the large scope of its business.

Through feast or famine, people will always need accounting and financial software even with a fractious global trade war threatening to topple global trade.

This software stock will provide stable earnings and reliable profits because of its defensive nature.

However, its 3-year revenue growth of 12% is not what premium tech companies produce. Intuit needs to ramp up its revenue drive and I believe the changing of CEO from old hand Brad Smith to his hand-picked successor Sasan Goodarzi will do the trick.

Goodarzi has indicated that he intends to migrate up the value chain into the mid-tier business revenue stream hoping to land some notable deals.

His immediate job is to identify a solution to help accelerate the firm’s top-line growth again.

The addressable market is massive, and Intuit isn’t capitalizing on its position with smaller companies, leaving the opportunity to upsell more advanced software to customers on the table.

The alarm bells should be ringing.

Intuit requires an upgrade in its software strategy in an evolve-or-die tech climate.

Nurturing small business customers is part and parcel to adopting a legitimate growth strategy as the status quo moving forward.

Weeding out one’s core customer base is a kamikaze mission.

If Intuit nails this transition, then new income streams will open up while retaining old customers.

That being said, Intuit is still a good company and could become a great company if they want to.

They even have a dividend yield of 0.8%.

Intuit is an incredibly profitable company and has increased their 3-year EPS growth rate to 27%, presiding over high-profit margins of 33%.

Financial products which include financial software are incredibly sticky and I would lump accounting software into that group too.

Accountants do not fancy switching over accounting software every year and risk fudging the numbers.

The company has made around $1 billion in profits the past three years and annual revenue has steadily climbed from $4.19 billion in 2015 to $5.96 billion in 2018.

Management indicated that 2019 revenue will come in around $6.5 to $6.6 billion, a jump of around 8-10%.

In my books, 8-10% of a company of this ilk isn’t good enough.

I am hoping new management will roll out the Microsoft (MSFT) playbook which focused on its subscription as a service (SaaS) revenue stream and reaped the untold rewards.

Intuit needs to wean itself from selling packaged products.

And the 11% growth in last season's earnings report was a pitiful deceleration from 17% the year before.

It is clear that management has not pumped enough juice out of this baby and fresh blood should invigorate management at the top level.

Highlighting the attractive possibilities to grow the existing user base is the uptick in self-employed subscribers within QuickBooks online surging to around 745,000 from 425,000 YOY.

Cross-selling to this existing subscriber base would increase average revenue per user.

On a sour note, strength isn’t happening across the board with the desktop ecosystem revenues of $537 million sliding 4% YOY.

Intuit isn’t harnessing the tools they currently possess.

Converting the critical customer feedback into actionable results will boost the company’s products and would be a big first step in making this a premier software company along the lines of Adobe (ADBE).

They have the foundation set up to achieve an Adobe-like revenue trajectory.

A revamp to the sorely lacking functionality will drive more revenue and keep customers happy as well as pulling in more mid-tier income streams.

I wouldn’t label Intuit a strong buy at this point and short-term macro weakness is a great reason to hold off on this stock before making the plunge.

Longer term, I pray that fintech newcomer Square (SQ) won’t expand into the individual accounting software industry because the rate of innovation percolating inside of Square’s office walls is second to none.

Tax software would be on the chopping block if Square can get its act together and make a beeline towards this segment.

Technology rewards the brute force innovators and Square wants to disrupt anything that involves digital finance.

I believe Intuit has good and not great software, but the lack of innovation could decimate them down the line once a serious innovator starts to eye their addressable market.

In any case, if Intuit becomes cheaper sliding to the $150-$160 levels from the $207 today, that would serve as a smart entry point into this above average software stock.

However, there are higher quality software companies out there, especially many whose revenue isn’t decelerating and some whose annual revenue is doubling every two years like Square.

Mad Hedge Technology Letter

October 18, 2018

Fiat Lux

Featured Trade:

(UNDERSTANDING THE REAL COMPETITION),

(SPOT), (AAPL), (GOOGL), (MSFT), (HUAWEI)

Microsoft sells computers?

That was the bizarre look I got after telling my friend that Microsoft (MSFT) is in the business of selling laptops, desktop computers, and tablets that convert into laptops from a product line called Microsoft Surface.

This is not your father’s Microsoft.

Things are different now.

Everything changed once they got rid of Steve Ballmer whose inertia prevented Microsoft from taking advantage of the huge influence they culled in the tech sector from being the universal operating system for PCs.

Ballmer’s lack of technical expertise was his own downfall stemming from his terrible decision to buy Nokia’s handset business for $7.6 billion.

The board of directors forced him out and was a blessing in disguise.

Thousands were laid off in the Nokia handset division and a massive write-down was taken.

As big tech spread out their wings and branch off into various businesses they never imagined before, they have reinvented the former images of themselves.

This goes for Microsoft who’s taking their legacy business of Microsoft Office and Windows and leveraging it with the cloud to create a stellar product.

And with the cash hoard, not only are they creating new products by fusing together old products with new technologies, they are overlapping into other big tech companies’ turf.

The overlapping products can be seen in hardware products made by this software behemoth and their neighbors.

The Microsoft Surface division is up 25% YOY speaking volumes to the quality hardware Microsoft produce now even if you didn’t know about it.

Apple (AAPL) has attracted most of the conversation in the "smart" headphones space because of the AirPods.

The sleek white earbuds are becoming ubiquitous with the headphone space trending to a smaller and "true" wireless.

A schism has formed as the AirPods don’t satisfy the entire spectrum of smart headphone fans.

The retro ear-muff shaped headphone with more immersive sound is what I am talking about, and I do recognize that Beats has been in the market for a decade.

Microsoft chose to go this route with their smart headphones and this is their answer to the iconic AirPods and the Google (GOOGL) Pixel Buds.

This smart headphone comes with an embedded digital assistant and integrates noise cancellation.

I tried out the Microsoft's Surface Headphones before they came on the market, and I only had positive things to say about the quality and experience.

They sound impressive, the controls are easy to use, and the modern design is definitely a plus.

The color could use a little reimagination but all in all, I was pleased.

Microsoft Cortana, Microsoft’s digital assistant, for all who don’t know, is also slipped into the experience and a tap on the right earcup will summon Cortana.

It seems that Microsoft still needs a few kinks to work out with Cortana, but voice activation and smart assistants like Siri and Google Assistant can be found in almost every hardware and software product now.

Headphones are city workers’ second most important smart device because of its functionality.

Have you ever been on the New York metro and seen how many people are wearing smart headphones?

Quality headphones shut off the outside world and warm up the insides with the user’s favorites on Spotify (SPOT) or Apple Music.

Stressing out on the commute into work in an Uber is common and calming the frayed nerves before workers enter into the office of dungeons and dragons has a type of value that can never be replicated.

Urban dwellers need high-quality smart headphones and these big tech companies are acutely aware of this.

Google has made an audacious attempt to integrate real-time foreign translation into the Pixel Buds. It only works with Google’s Pixel phones, is hard to operate, and needs the Google Translate app on the phone.

It’s a good first step but the applications using smart headphones are endless.

Smart assistants are the key.

As they become more adept at processing the real world, they streamline and better a human’s life.

Microsoft’s smart headphones have embedded Skype, one of Ballmer’s positive acquisitions during his tenure. And with Cortana integration, it could morph into a natural extension of the Windows 10 experience.

Microsoft’s smart headphones morph into a point of conversion for more of Microsoft’s hardware products as they start to construct an expanding moat.

Headphones used to be more or less the same.

Plug it into the jack and you’re on your merry way.

The headphones of today are looking more different from each other with every iteration.

This was glaringly evident when Apple chose to no longer sell any phones with a 3.5mm headphone jack.

Ironically enough, Google dumped the headphone jack with its Pixel 2 phones a year later even though they bashed Apple for it a few months earlier.

The reason was mainly functional as Google said, “We want the display to go closer and closer to the edge.”

Gradually, smartphones will get rid of everything except a razor-thin screen. All the other clunky business in and around it needs to go. This is the first step and home buttons have been chopped off smartphones as well.

It is fine to get consumed in the battle of smart products between Silicon Valley companies, but there is a larger threat.

Chinese smart products are rapidly catching up to what American companies can produce.

The Middle Kingdom hasn’t surpassed American tech expertise yet but they are debuting devices relative to the competition that could only be dreamed about a few years ago.

Huawei's flagship smartphone Mate 20 and Mate 20 Pro pack a lot of punch and this must be frightening to the FANGs.

The timing of the phone debut is a big victory for American smartphone companies because this phone is good enough to grab market share from existing American companies but aren’t allowed to sell inside America.

Congress putting the kibosh on any sliver of a chance to partner with an American carrier means that there will be no chance of Chinese phones gutting the American smartphone market.

What it does mean is that they will invade and dominate other markets such as South East Asia, Eastern Europe, and Russia.

The same will go for any Chinese smart device.

Huawei has given up trying to circumvent the government blockade.

The Huawei Mate 20 is priced around $800 and the Mate 20 Pro at $1140. They are probably two of the best smartphones ever made and are a direct threat to any American company’s revenue that manufactures smartphones and smart devices.

Mad Hedge Technology Letter

August 27, 2018

Fiat Lux

Featured Trade:

(WHY ALIBABA IS THE FIRST STOCK TO BUY WITH THE OUTBREAK OF TRADE PEACE),

(BABA), (GOOGL), (AMZN), (YELP), (MSFT), (MU), (ZTE), (HUAWEI)