Mad Hedge Technology Letter

January 28, 2019

Fiat Lux

Featured Trade:

(BUY DIPS IN SEMIS, NOT TOPS),

(XLNX), (LRCX), (AMD), (TXN), (NVDA), (INTC), (SOXX), (SMH), (MU), (QQQ)

Mad Hedge Technology Letter

January 28, 2019

Fiat Lux

Featured Trade:

(BUY DIPS IN SEMIS, NOT TOPS),

(XLNX), (LRCX), (AMD), (TXN), (NVDA), (INTC), (SOXX), (SMH), (MU), (QQQ)

Don’t buy the dead cat bounce – that was the takeaway from a recent trading day that saw chips come alive with vigor.

Semiconductor stocks had their best day since March 2009.

The price action was nothing short of spectacular with names such as chip equipment manufacturer Lam Research (LRCX) gaining 15.7% and Texas Instruments (TXN) turning heads, up 6.91%.

The sector was washed out as the Mad Hedge Technology Letter has determined this part of tech as a no-fly zone since last summer.

When stocks get bombed out at these levels - sometimes even 60% like in Lam Research’s case, investors start to triage them into a value play and are susceptible to strong reversal days or weeks in this case.

The semi-conductor space has been that bad and tech growth has had a putrid last six months of trading.

In the short-term, broad-based tech market sentiment has turned positive with the lynchpins being an extremely oversold market because of the December meltdown and the Fed putting the kibosh on the rate-tightening plan.

Fueled by this relatively positive backdrop, tech stocks have rallied hard off their December lows, but that doesn’t mean investors should take out a bridge loan to bet the ranch on chip stocks.

Another premium example of the chip turnaround was the fortune of Xilinx (XLNX) who rocketed 18.44% in one day then followed that brilliant performance with another 4.06% jump.

A two-day performance of 22.50% stems from the underlying strength of the communication segment in the third quarter, driven by the wireless market producing growth from production of 5G and pre-5G deployments as well as some LTE upgrades.

Give credit to the company’s performance in Advanced Products which grew 51% YOY and universal growth across its end markets.

With respect to the transformation to a platform company, the 28-nanometer and 16-nanometer Zynq SoC products expanded robustly with Zynq sales growing 80% YOY led by the 16-nanometer multiprocessor systems-on-chip (MPSoC) products.

Core drivers were apparent in the application in communications, automotive, particularly Advanced Driver Assistance Systems (ADAS) as well as industrial end markets.

Zynq MPSoC revenues grew over 300% YOY.

These positive signals were just too positive to ignore.

Long term, the trade war complications threaten to corrode a substantial chunk of chip revenues at mainstay players like Intel (INTC) and Nvidia (NVDA).

Not only has the execution risk ratcheted up, but the regulatory risk of operating in China is rising higher than the nosebleed section because of the Huawei extradition case and paying costly tariffs to import back to America is a punch in the gut.

This fragility was highlighted by Intel (INTC) who brought the semiconductor story back down to earth with a mild earnings beat but laid an egg with a horrid annual 2019 forecast.

Intel telegraphed that they are slashing projections for cloud revenue and server sales.

Micron (MU) acquiesced in a similar forecast calling for a cloud hardware slowdown and bloated inventory would need to be further digested creating a lack of demand in new orders.

Then the ultimate stab through the heart - the 2019 guide was $1 billion less than initially forecasted amounting to the same level of revenue in 2018 - $73 billion in revenue and zero growth to the top line.

Making matters worse, the downdraft in guidance factored in that the backend of the year has the likelihood of outperforming to meet that flat projection of the same revenue from last year offering the bear camp fodder to dump Intel shares.

How can firms convincingly promise the back half is going to buttress its year-end performance under the drudgery of a fractious geopolitical set-up?

This screams uncertainty.

Love them or crucify them, the specific makeup of the semiconductor chip cycle entails a vulnerable boom-bust cycle that is the hallmark of the chip industry.

We are trending towards the latter stage of the bust portion of the cycle with management issuing code words such as “inventory adjustment.”

Firms will need to quickly work off this excess blubber to stoke the growth cycle again and that is what this strength in chip stocks is partly about.

Investors are front-running the shaving off of the blubber and getting in at rock bottom prices.

Amalgamate the revelation that demand is relatively healthy due to the next leg up in the technology race requiring companies to hem in adequate orders of next-gen chips for 5G, data servers, IoT products, video game consoles, autonomous vehicle technology, just to name a few.

But this demand is expected to come online in the late half of 2019 if management’s wishes come true.

To minimize unpredictable volatility in this part of tech and if you want to squeeze out the extra juice in this area, then traders can play it by going long the iShares PHLX Semiconductor ETF (SOXX) or VanEck Vectors Semiconductor ETF (SMH).

In many cases, hedge funds have made their entire annual performance in the first month of January because of this v-shaped move in chip shares.

Then there is the other long-term issue of elevated execution risks to chip companies because of an overly reliant manufacturing process in China.

If this trade war turns into a several decades affair which it is appearing more likely by the day, American chip companies will require relocating to a non-adversarial country preferably a democratic stronghold that can act as the fulcrum of a global supply chain channel moving forward.

The relocation will not occur overnight but will have to take place in tranches, and the same chip companies will be on the hook for the relocation fees and resulting capex that is tied with this commitment.

That is all benign in the short term and chip stocks have a little more to run, but on a risk reward proposition, it doesn’t make sense right now to pick up pennies in front of the steamroller.

If the Nasdaq (QQQ) retests December lows because of global growth falls off a cliff, then this mini run in chips will freeze and thawing out won’t happen in a blink of an eye either.

But if you are a long-term investor, I would recommend my favorite chip stock AMD who is actively draining CPU market share from Intel and whose innovation pipeline rivals only Nvidia.

Global Market Comments

December 28, 2017

Fiat Lux

SPECIAL ISSUE ABOUT THE FAR FUTURE

Featured Trade:

(PEAKING INTO THE FUTURE WITH RAY KURZWEIL),

(GOOG), (INTC), (AAPL), (TXN)

This is the most important research piece you will ever read, bar none. But you have to finish it to understand why. So, I will get on with the show.

I have been hammering away at my followers at investment conferences, webinars, and strategy luncheons this year about one recurring theme. Things are good, and about to get better, a whole lot better.

The driver will be the exploding rate of technological innovation in electronics, biotechnology, and energy. The 2020s are shaping up to be another roaring twenties, and asset prices are going to go through the roof.

To flesh out some hard numbers about growth rates that are realistically possible and which industries will be the leaders, I hooked up with my old friend, Ray Kurzweil, one of the most brilliant minds in computer science.

Ray is currently a director of Engineering at Google (GOOG) heading up a team that is developing stronger artificial intelligence. He is an MIT grad with a double major in computer science and creative writing. He was the principal inventor of the CCD flatbed scanner, first text-to-speech synthesizer, and the commercially marketed large-vocabulary speech recognition.

When he was still a teenager, Ray was personally awarded a science prize by President Lyndon Johnson. He has received 20 honorary doctorates and has authored 7 books. It was upon Ray’s shoulders that many of today’s technological miracles were built.

His most recent book, The Singularity is Near: When Humans Transcend Biology, was a New York Times bestseller. In it, he makes hundreds of predictions about the next 100 years that will make you fall out of your chair.

I met Ray at one of my favorite San Francisco restaurants, Morton’s on Sutter Street. I ordered a dozen oysters, a filet mignon wrapped in bacon, and drowned it all down with a fine bottle of Duckhorn merlot. Ray had a wedge salad with no dressing, a giant handful of nutritional supplements, and a bottle of water. That’s Ray, one cheap date.

The Future of Man

A singularity is defined as a single event that has monumental consequences. Astrophysicists refer to the big bang and black holes in this way. Ray’s singularity has humans and machines merging to become single entities, partially by 2040 and completely by 2100.

All of our thought processes will include built-in links to the cloud making humans super smart. Skin that absorbs energy from the sun will eliminate the need to eat. Nanobots will replace blood cells, which are far more efficient at moving oxygen. A revolution in biotechnology will enable us to eliminate all medical causes of death.

Most organs can now be partially or completely replaced. Eventually, they all will become renewable by taking one of your existing cells and cloning it into a completely new organ. We will become much more like machines, and machines will become more like us.

The first industrial revolution extended the reach of our bodies, and the second is extending the reach of our minds.

And, oh yes, prostitution will be legalized and move completely online. Sounds like a turn-off? How about virtually doing it with your favorite movie star? Your favorite investment advisor? Yikes!

Ironically, one of the great accelerants towards this singularity has been the war in Iraq. More than 50,000 young men and women came home missing arms and legs (in Vietnam these were all fatalities, thanks to the absence of modern carbon fiber body armor).

Generous government research budgets have delivered huge advances in titanium artificial limbs and the ability to control them only with thoughts. Quadriplegics can now hit computer keystrokes merely by thinking about them.

Kurzweil argues that exponentially growing information technology is encompassing more and more things that we care about, like healthcare and medicine. Reprogramming of biology will be the next big thing and is a crucial part of his “singularity.”

Our bodies are governed by obsolete genetic programs that evolved in a bygone era. For example, over millions of years, our bodies developed genes to store fat cells to protect against a poor hunting season in the following year. That gave us a great evolutionary advantage 10,000 years ago. But it is not so great now with obesity becoming the country’s number one health problem.

We would love to turn off these genes through reprogramming, confident that the hunting at the supermarket next year will be good. We can do this in mice now which, in experiments, can eat like crazy but never gain weight.

The happy rodents enjoy the full benefits of caloric restriction with no hint of diabetes or heart disease. A product like this would be revolutionary, not just for us, health care providers, and the government, but, ironically, for fast food restaurants as well.

Within the last five years, we have learned how to reprogram stem cells to rebuild the hearts of heart attack victims. The stem cells are harvested from skin cells, not human embryos, ducking the political and religious issue of the past.

And if we can turn off genes, why not the ones in cancer cells that enable them to pursue unlimited reproduction until they kill its host? That development would cure all cancers, and is probably only a decade off.

The Future of Computing

If this all sounds like science fiction, you’d be right. But Ray points out that humans have chronically underestimated the rate of technological innovation.

This is because humans evolved to become linear thinking animals. If a million years ago we saw a gazelle running from left to right, our brains calculated that one second later it would progress ten feet further to the right. That’s where we threw the spear. This gave us a huge advantage over other animals and is why we became the dominant species.

However, much of science, technology, and innovation grows at an exponential rate and is where we make our most egregious forecasting errors. Count to seven, and you get to seven. However, double something seven times and you get to a billion.

The history of the progress of communications is a good example of an exponential effect. The spoken language took hundreds of thousands of year to develop. Written language emerged thousands of years, books in 100 years, the telegraph in a century, and telephones 50 years later.

Some ten years after Steve Jobs brought out his Apple II personal computer, the growth of the Internet went hyperbolic. Within three years of the iPhone launch, social media exploded out of nowhere.

At the beginning of the 20th century, $1,000 bought 10 X -5th power worth of calculations per second in our primitive adding machines. A hundred years later a grand got you 10 X 8th power calculations, a 10 trillion-fold improvement. The present century will see gains many times this.

The iPhone itself is several thousand times smaller, a million times cheaper, and billions of times more powerful than computers of 40 years ago. That increases the price per performance by the trillions. More dramatic improvements will accelerate from here.

Moore’s law is another example of how fast this process works. Intel (INTC) founder Gordon Moore published a paper in 1965 predicting a doubling of the number of transistors on a printed circuit board every two years. Since electrons had shorter distances to travel, speeds would double as well.

Moore thought that theoretical limits imposed by the laws of physics would bring this doubling trend to end by 2018 when the gates become too small for the electrons to pass through. For decades, I have read research reports predicting that this immutable deadline would bring an end to innovation and technological growth, and bring an economic Armageddon.

Ray argues that nothing could be further from the truth. A paradigm shift will simply allow us to leapfrog conventional silicon-based semiconductor technologies and move on to bigger and better things. We did this when we jumped from vacuum tubes to transistors in 1949, and again in 1959 when Texas Instruments (TXN) invented the first integrated circuit.

Paradigm shifts occurred every ten years in the past century, every five years in the last decade, and will occur every couple of years in the 2020s. So fasten your seatbelts!

Nanotechnology has already allowed manufacturers to extend the 2018 Moore’s Law limit to 2022. On the drawing board are much more advanced computing technologies including calcium-based systems using the alternating direction of spinning electrons, and nanotubes.

Perhaps the most promising is DNA-based computing, a high research priority at IBM and several other major firms. I earned my own 15 minutes of fame in the scientific world 40 years ago as a member of the first team ever to sequence a piece of DNA which is why Ray knows who I am.

DeoxyriboNucleic Acid makes up the genes that contain the programming that makes us who we are. It is a fantastically efficient means of storing and transmitting information. And it is found in every single cell in our bodies, all 10 trillion of them.

The great thing about DNA is that it replicates itself. Just throw it some sugar. That eliminates the cost of building the giant $2 billion silicon-based chip fabrication plants of today.

The entire human genome is a sequential binary code containing only 800 MB information which after you eliminate redundancies, has a mere 30-100 MB of useful information, about the size of an off-the-shelf software program like Word for Windows. Unwind a single DNA molecule and it is only six feet long.

What this means is that, just when many believe that our computer power is peaking, it is in fact just launching on an era of exponential growth. Supercomputers surpassed human brain computational ability in 2012, about 10 to the 16th power (ten quadrillion) calculations per second.

That power will be available on a low-end laptop by 2020. By 2050, this prospective single laptop will have the same computing power of the entire human race, about 9 billion individuals. It will also be small enough to implant in our brains.

The Future of the Economy

Ray is not really that interested in financial markets or, for that matter, making money. Where technology will be in a half-century and how to get us there are what get his juices flowing. However, I did manage to tease a few mind-boggling thoughts from him.

At the current rate of change, the 21st century will see 200 times the technological progress that we saw in the 20th century. Shouldn’t corporate profits, and therefore share prices, rise by as much?

Technology is rapidly increasing its share of the economy and increasing its influence on other sectors. That’s why tech has been everyone’s favorite sector for the past 30 years and will remain so for the foreseeable future. For two centuries, technology has been eliminating jobs at the bottom of the economy and creating new ones at the top.

Stock analysts and investors make a fatal flaw in estimating future earnings based on the linear trends of the past, instead of the exceptional growth that will occur in the future.

In the last century, the Dow appreciated from 100 to 10,000, an increase of 100 times. If we grow at that rate in this century, the Dow should increase by 10,000% to 1 million by 2100. But so far, we are up only 6%, even though we are already 18 years into the new century.

The index is seriously lagging but will play catch up in a major way during the 2020s when economic growth jumps from 2% to 4% or more, thanks to the effects of massively accelerating technological change.

Some 100 years ago, one-third of jobs were in farming, one third were in manufacturing, and one third in services. If you predicted then that in a century farming and manufacturing would each be 3% of total employment and that something else unknown would come along for the rest of us, people would have been horrified. But that’s exactly what happened.

Solar energy use is also on an exponential path. It is now 1% of the world’s supply but is only seven doublings away from becoming 100%. Then we will consume only one 10,000th of the sunlight hitting the earth. Geothermal energy offers the same opportunities.

We are only running out of energy if you limit yourself to 19th-century methods. Energy costs will plummet. Eventually, energy will be essentially free when compared to today’s costs, further boosting corporate profits.

Hyper-growth in technology means that we will be battling with deflation for the rest of the century, as the cost of production and price of everything fall off a cliff. That makes our 10-year Treasury bonds a steal at a generous 2.60% yield, a full 460 basis points over the real long-term inflation rate of negative 2% a year.

US Treasuries could eventually trade down to the 0.40% yields seen in Japan only a couple of years ago. This means that the bull market in bonds is still in its early stages, and could continue for decades.

The upshot for all of this these technologies will rapidly eliminate poverty, not just in the US but around the world. Each industry will need to continuously reinvent its business model, or disappear.

The takeaway for investors that stocks, as well as other asset prices, are now wildly undervalued given their spectacular future earnings potential. It also makes the Dow target of 1 million by 2100 absurdly low, and off by a factor of 10 or even 100. Will we be donning our “Dow 100 Million” then?

Other Random Thoughts

As we ordered dessert, Ray launched into another stream of random thoughts. I asked for Morton’s exquisite double chocolate mousse. Ray had another handful of supplements. Yep, Mr. Cheap Date.

The number of college students has grown from 50,000 to 12 million since the 1870s. A kid in Africa with a cell phone has more access to accurate information than the president of the United States did 15 years ago.

The great superpower, the Soviet Union, was wiped out by a few fax machines distributing information in 1991.

Company offices will become entirely virtual by 2025.

Cows are very inefficient at producing meat. In the near future, cloned muscle tissue will be produced in factories, disease free, and at a fraction of the present cost without the participation of the animal. PETA will be thrilled.

Use of nanomaterials to build ultra light but ultra strong cars cuts fuel consumption dramatically. Battery efficiencies will improve by 10 to 100 times. Imagine powering Tesla Model S1 with a 10-pound battery! Advances in nanotube construction mean the weight of the vehicle will drop from the present 3 tons to just 100 pounds but will be far safer.

Ray is also on a scientific advisory panel for the US Army. Uncertain about my own security clearance, he was reluctant to go into detail. Suffice it to say that the weight of an M1 Abrams main battle tank will shrink from 70 tons to 1 ton, but will be 100 times stronger.

A zero tolerance policy towards biotechnology by the environmental movement exposes their intellectual and moral bankruptcy. Opposing a technology with so many positive benefits for humankind and the environment will inevitably alienate them from the media and the public who will see the insanity of their position.

Artificial intelligence is already far more prevalent than you understand. The advent of strong artificial intelligence will be the most significant development of this century. You can’t buy a book from Amazon, withdraw money from your bank, or book a flight without relying on AI.

Ray finished up by saying that by 2100 humans will have the choice of living in a biological, or in a totally virtual, online form. In the end, we will all just be files.

Personally, I prefer the former, as the best things in life are biological, and free!

I walked over to the valet parking, stunned and disoriented by the mother load of insight I had just obtained, and it wasn’t just the merlot talking, either! Imagine what they talk about at Google all day.

To buy The Singularity is Near at discount Amazon pricing, please click here. It is worth purchasing the book just to read Ray’s single chapter on the future of the economy.

Mad Hedge Technology Letter

December 4, 2018

Fiat Lux

Featured Trade:

(THE CHIP STOCKS HAVE BOTTOMED)

(NVDA), (AMD), (INTC)

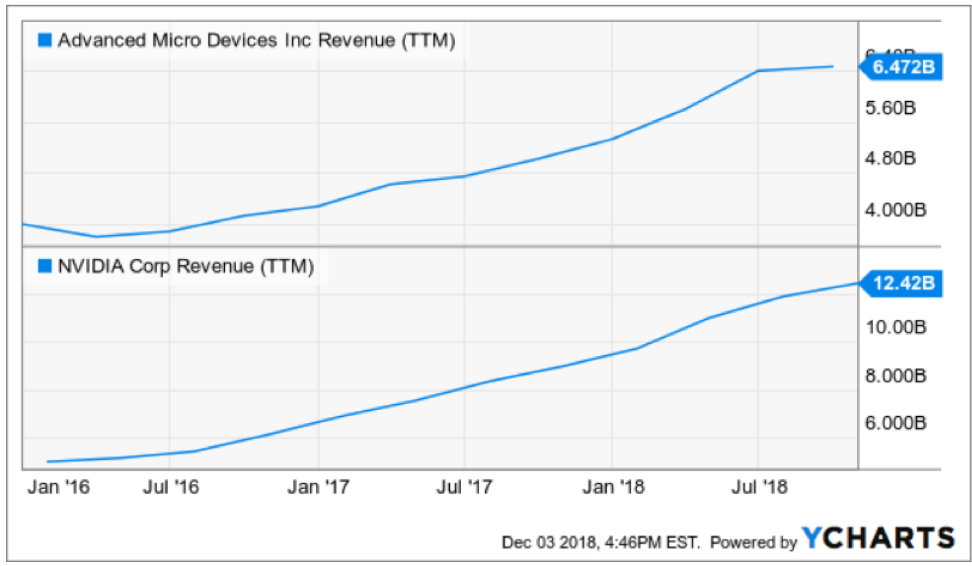

Now that the trade war has officially been put on ice, two short-term trades to scoop up out there for the taking would be chip leaders Advanced Micro Devices (AMD) and Nvidia (NVDA).

Even though I am still bearish on the chip sector as a whole, the mini rapprochement signals a much-needed reprieve to China-sensitive stocks that have been beaten down for most of the year.

The timing is favorable now to jump into some of the avant-garde chip stocks and succinctly two companies that have captured the imagination of the global gaming revolution by constructing the critical GPUs needed to display the mouth-watering graphics that appear life-like.

They are two dominators that have cornered the GPU market and don’t apologize for it.

Even if next year fails to pinpoint a comprehensive détente, China-based supply chains will have more time to make epochal decisions to whether risk the full brunt of a future multilateral spat or mosey on over to greener pastures to insulate themselves from tariff and political fallout.

Most of American tech supply chains are in China now, but that doesn’t mean that can’t change.

Either way, ratcheting down the tone of the jawboning will help chip stocks and the GPU mainstay firms should finish out the year resolutely.

After building an abnormally high amount of inventory due to last year's bitcoin euphoria, Nvidia got ahead of itself drowning in excess GPU units with evaporating crypto mining demand from the bitcoin crash.

It was never imagined that the crypto phenomenon could incite a build-up of inventory channels to the levels that started to erode pricing, but when you consider that two companies and not one were pumping out the GPU units, they simply overdid it.

Conveniently enough, management on both sides blamed each other.

In any case, I believe the spike in inventory says more to the crash and burn of bitcoin pricing than having something to do with these two solidly run companies.

Bitcoin revenue stream only accounted for 10% of revenue at last year’s peak of crypto ecstasy.

The Mad Hedge Technology Letter has steered wide and clear of the crypto phenomenon because even though the blockchain technology is indeed intriguing, there are probably a few more crash and burn scenarios to unfold before it becomes legitimately accepted in mainstream finance.

In any effect, GPU pricing has started to turn the corner up 15% from the September lows, and for the first time since earlier in the year, inventory levels are starting to flush itself out.

The “crypto hangover” headlines roughed up shares of the duopolists but now the light is at the end of the tunnel, and combined with the ceasefire in Washington, has created a positive platform for these two favorites to trade into yearend.

The record-breaking sales volume from Black Friday and Cyber Monday is a minor boost giving credence to the inventory channels clear-up.

Jubilant shoppers were gobbling up GPUs to dish out to gamer friends and family.

At the annual Siggraph conference in Vancouver, Canada, CEO of Nvidia Jensen Huang said, “Turing is Nvidia’s most important innovation in computer graphics in more than a decade.”

The development of real-time ray tracing is the “holy grail” of the GPU industry.

The Turing products render graphics six times faster than their predecessor Pascal-based chip.

Nvidia has rolled out three new graphics cards based on this technology.

In fact, the Turing T4 Cloud GPU has been a massive success in the data center space.

Not only is gaming benefitting from these high-end chips, they can be slotted around offering a diverse set of functionalities.

Ian Buck, Vice President and General Manager of Accelerated Computing at Nvidia said, “We have never before seen such rapid adoption of a data center processor.”

Nvidia’s T4 offers the modern cloud of today the performance and efficiency needed for compute-intensive workloads at scale.

The two companies continue to manufacture top-level GPUs that the competition cannot touch.

The headwinds facing these two titans are of a temporary basis and will eventually dry up.

Both missed on earnings and the stocks sold off badly.

The one-off short-term headwinds will quickly shore up.

The lucky opportunity for investors to get into a best of breed at a cheaper price does not come around too often.

If the near-term fluctuations provide too intense, both companies are great long-term buy and hold stocks.

The bad news has been mostly baked into the pie at this point.

The reset in expectations should factor in the evolving inventory situation and the crypto headwinds.

I fully expect both companies to convincingly beat earnings on the top and bottom line next quarter.

Core gaming demand is robust and by next earnings, the companies will be back to their normal selves – systematically crushing earnings expectations.

This one-off in performance was a curveball, and AMD is a company that I am bullish on with AMD snatching away market share from Intel (INTC).

German’s large tech e-tailer Mindfactory published a survey showing AMD doubling the number of CPUs sold leaving Intel in the dust in November.

Intel’s CPU sales are nosediving quickly because of AMD’s innovative designs and reliable production performance.

Intel has essentially gifted a huge swath of the CPU market to AMD, and AMD has embraced the change and is running with it.

I expect AMD to turn the screws next year on Intel and hoover up more of the CPU market.

Add in that 50% of AMD’s revenue comes from newly launched products and then you can start to cook up why these companies are ahead of the game.

They concoct best in show products leverage with groundbreaking technology and scale up these state-of-the-art offerings to the strongest segments of the chip industry and presto!

You have a magical recipe of success.

At the Mad Hedge Lake Tahoe Conference at the end of October, AMD plummeted to around $17 and I convincingly proclaimed this stock a buy without hesitation.

The stock is up over 25% since then to almost $24, and I believe this stock is in it for the long haul.

Mad Hedge Technology Letter

November 21, 2018

Fiat Lux

Featured Trade:

(FIVE TECH STOCKS TO SELL SHORT ON THE NEXT RALLY)

(WDC), (SNAP), (STX), (APRN), (AMZN), (KR), (WMT), (MSFT), (ATVI), (GME), (TTWO), (EA), (INTC), (AMD), (FB), (BBY), (COST), (MU)

Next year is poised to be a trading year that will bring tech investors an added dimension with the inclusion of Uber and Lyft to the public markets.

It seemed that everything that could have happened in 2018 happened.

Now, it’s time to bring you five companies that I believe could face a weak 2019.

Every rally should be met with a fresh wave of selling and one of these companies even has a good chance of not being around in 2020.

Western Digital (WDC)

I have been bearish on this company from the beginning of the Mad Hedge Technology Letter and this legacy firm is littered with numerous problems.

Western Digital’s structural story is broken at best.

They are in the business of selling hard disk drive products.

These products store data and have been around for a long time. Sure the technology has gotten better, but that does not mean the technology is more useful now.

The underlying issue with their business model is that companies are moving data and operations into cloud-based products like the Microsoft (MSFT) Azure and Amazon Web Services.

Why need a bulky hard drive to store stuff on when a cloud seamlessly connects with all devices and offers access to add-on tools that can boost efficiency and performance?

It’s a no-brainer for most companies and the efficiency effects are ratcheted up for large companies that can cohesively marry up all branches of the company onto one cloud system.

Even worse, (WDC) also manufactures the NAND chips that are placed in the hard drives.

NAND prices have faltered dropping 15% of late. NAND is like the ugly stepsister of DRAM whose large margins and higher demand insulate DRAM players who are dominated by Micron (MU), Samsung, and SK Hynix.

EPS is decelerating at a faster speed and quarterly sales revenue has plateaued.

Add this all up and you can understand why shares have halved this year and this was mainly a positive year for tech shares.

If there is a downtown next year in the broader market, watch out below as this company is first on the chopping block as well as its competitor Seagate Technology (STX).

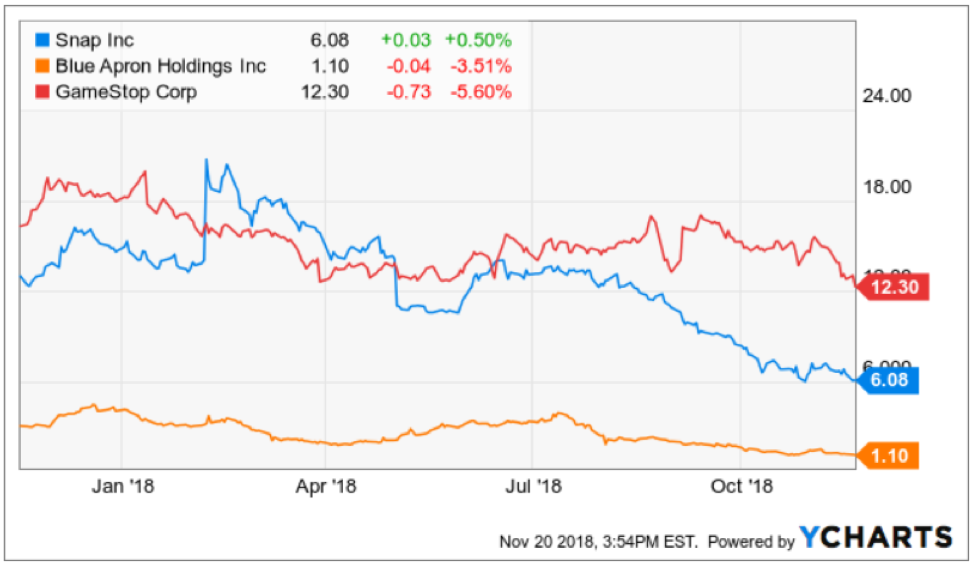

Snapchat (SNAP)

This company must be the tech king of terrible business models out there.

Snapchat is part of an industry the whole western world is attempting to burn down.

Social media has gone for cute and lovable to destroy at all cost. The murky data-collecting antics social media companies deploy have regulators eyeing these companies daily.

More successful and profitable firm Facebook (FB) completely misunderstood the seriousness of regulation by pigeonholing it as a public relation slip-up instead of a full-blown crisis threatening American democracy.

Snapchat is presiding over falling daily active user growth at such an early stage that usership doesn’t even pass 100 million DAUs.

Management also alienated the core user base of adolescent-aged users by botching the redesign that resulted in users bailing out of Snapchat.

Snapchat has been losing high-level executives in spades and fired a good chunk of their software development team tagging them as the scapegoat that messed up the redesign.

Even more imminent, Snapchat is burning cash and could face a cash crunch in the middle of next year.

They just announced a new spectacle product placing two frontal cameras on the glass frame. Smells like desperation and that is because this company needs a miracle to turn things around.

If they hit the lottery, Snap could have an uptick in its prospects.

GameStop (GME)

This part of technology is hot, benefiting from a generational shift to playing video games.

Video games are now seen as a full-blown cash cow industry attracting gaming leagues where professional players taking in annual salaries of over $1 million.

Gaming is not going away but the method of which gaming is consumed is changing.

Gamers no longer venture out to the typical suburban mall to visit the local video games store.

The mushrooming of broad-band accessibility has migrated all games to direct downloads from the game manufacturers or gaming consoles’ official site.

The middleman has effectively been cut out.

That middleman is GameStop who will need to reinvent itself from a video game broker to something that can accrue real value in the video game world.

The long-term story is still intact for gaming manufactures of Activision (ATVI), EA Sports (EA), and Take-Two Interactive (TTWO).

The trio produces the highest quality American video games and has a broad portfolio of games that your kids know about.

GameStop’s annual revenue has been stagnant for the past four years.

It seems GameStop can’t find a way to boost its $9 billion of annual revenue and have been stuck on this number since 2015.

If you do wish to compare GameStop to a competitor, then they are up against Best Buy (BBY) which is a better and more efficiently run company.

Then if you have a yearning to buy video games from Best Buy, then you should ask yourself, why not just buy it from Amazon with 2-day free shipping as a prime member.

The silver lining of this business is that they have a nice niche collectibles division that hopes to deliver over $1 billion in annual sales next year growing at a 25% YOY clip.

But investors need to remember that this is mainly a trade-in used video game company.

Ultimately, the future looks bleak for GameStop in an era where the middleman has a direct path to the graveyard, and they have failed to digitize in an industry where digitization is at the forefront.

Blue Apron

This might be the company that is in most trouble on the list.

Active customers have fallen off a cliff declining by 25% so far in 2018.

Its third quarter earnings were nothing short of dreadful with revenue cratering 28% YOY to $150.6 million, missing estimates by $7 million.

The core business is disappearing like a Houdini act.

Revenue has been decelerating and the shrinking customer base is making the scope of the problem worse for management.

At first, Blue Apron basked in the glory of a first mover advantage and business was operating briskly.

But the lack of barriers to entry really hit the company between the eyes when Amazon (AMZN), Walmart (WMT), and Kroger (KR) rolled out their own version of the innovative meal kit.

Blue Apron recently announced it would lay off 4% of its workforce and its collaboration with big-box retailer Costco (COST) has been shelved indefinitely before the holiday season.

CFO of Blue Apron Tim Bensley forecasts that customers will continue to drop like flies in 2019.

The company has chosen to focus on higher-spending customers, meaning their total addressable market has been slashed and 2019 is shaping up to be a huge loss-making year for the company.

The change, in fact, has flustered investors and is a great explanation of why this stock is trading at $1.

The silver lining is that this stock can hardly trade any lower, but they have a mountain to climb along with strategic imperatives that must be immediately addressed as they descend into an existential crisis.

Intel (INTC)

This company is the best of the five so I am saving it for last.

Intel has fallen behind unable to keep up with upstart Advanced Micro Devices (AMD) led by stellar CEO Dr. Lisa Su.

Advanced Micro Devices is planning to launch a 7-nanometer CPU in the summer while Intel plans to roll out its next-generation 10-nanometer CPUs in early 2020.

The gulf is widening between the two with Advanced Micro Devices with the better technology.

As the new year inches closer, Intel will have a tough time beating last year's comps, and investors will need to reset expectations.

This year has really been a story of missteps for the chip titan.

Intel dealt with the specter security vulnerability that gave hackers access to private data but later fixed it.

Executive management problems haven’t helped at all.

Former CEO of Intel Brian Krzanich was fired soon after having an inappropriate relationship with an employee.

The company has been mired in R&D delays and engineering problems.

Dragging its feet could cause nightmares for its chip development for the long haul as they have lost significant market share to Advanced Micro Devices.

Then there is the general overhang of the trade war and Intel is one of the biggest earners on mainland China.

The tariff risk could hit the stock hard if the two sides get nasty with each other.

Then consider the chip sector is headed for a cyclical downturn which could dent the demand for Intel chip products.

The risks to this stock are endless and even though Intel registered a good earnings report last out, 2019 is set up with landmines galore.

If this stock treads water in 2019, I would call that a victory.

Mad Hedge Technology Letter

September 24, 2018

Fiat Lux

Featured Trade:

(BAD NEWS FROM MICRON TECHNOLOGY (MU),

(MU), (BABA), (KLAC), (LRCX), (INTC), (AMD), (NVDA), (HPQ)

If your stomach was on edge before, then you must feel quite queasy now.

That’s only if you didn’t get rid of your chip stocks when I told you to.

The chip sector has been rife with issues for quite some time now, and I’ve been firing off bearish chip stories the past few months.

Intel (INTC) was one of the last chip companies I told you to avoid like the plague, please click here to review that story.

The contagion has spread wider.

Micron (MU), the Boise, Idaho-based chip giant, delivered poor guidance from its latest earnings report, adding more carnage to this trouble sector.

It’s been rough sailing for many American-based chip companies lately that are not named Advanced Micro Devices (AMD) and Nvidia (NVDA).

The protracted ongoing trade war between America and China that sees no end in sight is the fundamental reason to stay away from these chip companies that are the meat and potatoes inside of all electronic devices.

Cofounder of Alibaba (BABA) Jack Ma, who recently stepped down from his position as chairman, told news outlets that this trade war could last “20 years” and is “going to be a mess.”

Micron is affected by this trade war more than any other American company, with half of its annual revenue derived from the Middle Kingdom.

Out of the $20.32 billion in annual revenue last year, more than $10 billion was from China alone.

Micron is a leader in selling DRAM chips, which are placed in most portable electronic devices such as smartphones, video game consoles, and laptop computers.

The commentary coming out from chip executives has been overly negative and spells doom and gloom - supporting my view to be cautious on chips through the end of the year.

At the Citi 2018 Global Technology Conference in New York, KLA-Tencor (KLAC) chief financial officer Bren Higgins characterized the winter season DRAM market as “little less than what we thought,” describing margins as “modestly weaker.”

Lam Research (LRCX), once one of my favorite chip plays, offered bearish rhetoric about the state of chip investments, saying on its earnings call that is expected “lower spending on new equipment by some of its memory customers.”

It doesn’t take a rocket scientist to know that “memory customer” is Intel, which is in the throes of a CPU chip shortage rocking the overall personal computer market.

Personal computers face a steep 7% drop in sales volume for the rest of the year, and the knock-on effect is rippling throughout the industry.

The lower volume of produced computers means less memory needed, adding up to less sales for Micron.

This rationale forced Micron to guide down its revenue growth from 22% to 16% for the last quarter of 2018.

Intel’s monumental lapse has offered a golden opportunity for competitor Advanced Micro Devices (AMD) to steal market share from Intel in broad daylight.

This was the exact thesis that provoked me to urge readers to pile into AMD shares like a Tokyo rush-hour subway car.

Shares have gone ballistic to say the least.

(AMD) is poised to seize and reposition itself in the global CPU market with a 70/30 market share, up from the paltry 90/10 market share before Intel’s debacle.

To make matters worse for Intel, widespread reports indicate its shortage problems are “worsening.”

Such is a dog-eat-dog world out there when a company can triple market share in a blink of an eye.

The rotation is real with HP (HPQ) planning to integrate AMD chips into 30% of its consumer PCs, and Dell already mentioning it will use AMD chips to make up for the shortages.

The resilience in chip demand remains the silver lining for this industry as price weakness and production shortages will be finite.

Server demand remains particularly robust.

Google, Amazon, Facebook, and Microsoft coughed up $34.7 billion on data centers to serve cloud-based operation in the first half of the year in 2018, a sharp increase of 59% YOY.

Investors have been paranoid of the boom-bust nature of the chip industry for decades.

Each cycle sees spending and chip pricing rocket, only for inventories to build up and demand to evaporate in an instant.

The beginning of the end always starts with lower guidance, followed up with missed earnings the next quarter.

This playbook has repeated itself over and over.

Micron guided first quarter revenue of 2019 in a range between $7.9 billion to $8.3 billion, lower than the consensus of $8.45 billion.

And, if all of this horrid chip news wasn’t reason to rip your hair out - here is the bombshell.

To wean itself off the reliance of American chips, Alibaba has created a subsidiary to produce its own chips called Pingtouge Semiconductor Company.

Pingtouge refers to honey badger in the Chinese language, symbolic for its tenacity in the face of adversity – perhaps a thinly-veiled dig at the American political system.

Former Chairman Ma pocketed this chip company Hangzhou C-SKY Microsystems last year. It will will be given ample leeway and resources to team up with Alibaba to roll out its first commercial chip next year.

Alibaba has rapidly grown into the third-largest cloud player in the world, and require an abundant source of chips moving forward.

Chips tricked out with artificial intelligence will be adopted by not only its data centers, but integrated with its autonomous driving technology and IoT products, which are markets that Alibaba is proud to be part.

You can find Alibaba’s cloud products present in more than 20 countries. And the company that Jack Ma built forecasts to generate more than 50% of its revenue from overseas markets soon.

It could be Jack Ma laughing all the way to the bank.

Ultimately, Micron produced fair results last quarter, but like Facebook found out, if investors believe the company is about to fall off a cliff, it offers little resistance to the share price on a short-term basis.

Could the cyclicality demons start to awake to drag this company down?

Partially, yes, but there are still many positives to take away from this leading chip company.

China will need years to remedy its addiction of American chips.

It will not be able to produce the scope of quality or quantity to just stop buying from American companies for the foreseeable future.

The authorized $10 billion share buyback gave Micron shares a nice lift earlier this year, but the industry dynamics are now deteriorating rapidly.

Chip sentiment is at its lowest ebb for some time, and I reaffirm my call to avoid this sector completely unless it’s the two cornerstone chip companies showing systematic resiliency - (AMD) or Nvidia (NVDA).

The administration initially slapped on a tariff rate of 10% on $200 billion worth of goods with intentions to scale it up.

If nothing is solved, the increase to 25% will cause another 5% to 10% drop in Micron and Intel.

Then if the administration plans to go after the rest of the $250 billion of Chinese imports, expect another dive in chip shares.

Either way, each jawboning tweet as we head deeper into this trade conflict will damage Micron’s shares.

This sector is getting squeezed from many sides now, and if you don’t go outright short chip companies, then stay away until the storm clouds pass over and you can reassess the situation.

Did You Say "BUY" or "SELL"

Did You Say "BUY" or "SELL" The Future is Closer than You Think

The Future is Closer than You Think