Mad Hedge Technology Letter

September 19, 2018

Fiat Lux

Featured Trade:

(IBM’S SELF DESTRUCT),

(IBM), (BIDU), (BABA), (AAPL), (INTC), (AMD), (AMZN), (MSFT), (ORCL)

Mad Hedge Technology Letter

September 19, 2018

Fiat Lux

Featured Trade:

(IBM’S SELF DESTRUCT),

(IBM), (BIDU), (BABA), (AAPL), (INTC), (AMD), (AMZN), (MSFT), (ORCL)

International Business Machines Corporation (IBM) shares do not need the squeeze of a contentious trade war to dent its share price.

It is doing it all by itself.

Stories have been rife over the past few years of shrinking revenue in China.

And that was during the golden years of China when American tech ran riot on the mainland before the dynamic rise of Baidu (BIDU), Alibaba (BABA), and Tencent, otherwise known as the BATs.

Then the Oracle of Omaha Warren Buffett drove a stake through the heart of IBM shares earlier this year by announcing he was fed up with the company’s direction and dumped a 35-year position.

Buffett unloaded all of his shares in favor of putting down an additional 75 million shares in Apple (AAPL) in the first quarter of 2018.

Topping off his Apple position now sees Buffett owning a mammoth 165.3 million total shares in the resurgent tech company.

Buffett’s shrewd decision has been rewarded, and Apple’s stock has rocketed more than 20% since he jovially declared his purchase in May.

IBM has been a rare misstep for Buffett, who took a moderate loss on his IBM position disclosing an average cost basis of $170 on 64 million shares that Berkshire bought in 2011.

IBM has flatlined since that Buffett interview, and slid around 25% since its peak in mid-2014.

IBM is grappling with the same conundrum most legacy companies deal with – top line contraction.

In 2014, IBM registered a tad under $93 billion in annual revenue, and followed up the next three years with even lower revenue.

A horrible recipe for success to say the least.

In an era of turbo-charged tech companies whose value now comprise over a quarter of the S&P, IBM has really fluffed its lines.

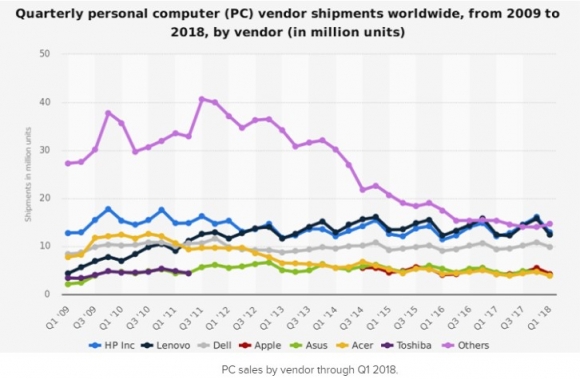

IBM’s prospects have been stapled to the PC market for years.

A recent JP Morgan note revealed the PC market could contract by 5% to 7% in the fourth quarter because of CPU shortages from Intel (INTC).

The report’s timing couldn’t have been worse for IBM.

The PC industry has been tanking for the past six consecutive years unable to shirk shrinking volume.

Intel is another company I have been lukewarm on lately because it is being outmaneuvered by chip competitor Advanced Micro Devices (AMD).

Even worse, this year has been a bad one for Intel’s management, which saw former CEO Brian Krzanich resign for sleeping with a coworker.

The poor management has had a spillover effect with Intel needing to delay new product launches as well.

To read more about my timely recommendation to pile into AMD in mid-August at $19, please click here.

Meanwhile, AMD shares have gone parabolic and surpassed an intraday price of $34 recently.

Investors should ask themselves, why invest in IBM when there are so many other tech companies that are growing, and growing revenue by 20% or more per year?

If IBM does manage to eke out top line growth in 2018, it will be by 1% to 2%, similar to Oracle’s recent performance.

Unsurprisingly, the price action of Oracle (ORCL) for the past year has been flatter than a bicycle ride around Beijing.

Live by the sword and die by the sword.

Thus, the Mad Hedge Technology Letter has been ushering readers into high-performance stocks that will bring technological and societal changes.

If you put a gun to my head and forced me to give sage investment advice, then the answer would be straightforward.

Buy Amazon (AMZN) and Microsoft (MSFT) on the dip and every dip.

This is a way to print money as if you had a rich uncle writing you checks every month.

Legacy tech is another story.

The IBMs and the Oracles of the world are bringing up the tech sector’s rear.

To add insult to injury, the lion’s share of IBM’s revenue is carved out from abroad, and the recent surge in the dollar is not doing IBM any favors.

IBM’s Watson initiative was billed as the savior for Big Blue.

The artificial intelligence initiative would integrate health care data into an actionable app.

The expectations were high hoping this division would drag up IBM from its long period of malaise.

IBM bet big on this division ploughing more than $15 billion into it from 2010-2015, predicting this would be the beginning of a new renaissance for the historic American company.

This game changing move fell on deaf ears and has been a massive bust.

IBM swallowed up three companies to ramp up this shift into the AI world - Phytel, Explorys, and Truven.

The treasure trove of health care data and proprietary analytics systems these companies came with were what this division needed to turn the corner.

These three companies were strong before the buy out and engineers were upbeat hoping Watson would elevate these companies to another level.

Wistfully, IBM Management led by CEO Ginni Rometty grossly mishandled Watson’s execution.

Phytel boasted 160 engineers at the time of IBM’s purchase and confusingly slashed half the workforce earlier this year.

Engineers at the firm even lamented that now, even smaller firms were “eating them alive.”

Unimpressed with the direction of the artificial intelligence division at IBM, many of these three companies’ best and brightest engineers jumped ship.

The inability for IBM to integrate Watson reared its ugly head in plain daylight when MD Anderson Cancer Center in Texas halted its Watson project after draining $62 million.

This was one of many errors that Watson AI accrued.

The failure to quicken clinical decision-making to match patients to clinical trials was an example of how futile IBM had become.

In short, a spectacular breakdown in execution mixed with an abrupt brain drain of AI engineers quickly imploded the prospect of Watson ever succeeding.

In 2013, IBM confidently boasted that Watson would be its “first killer app” in health care.

Internal leaks shined a brighter light on IBM’s subpar management skills.

One engineer described IBM’s management as having “no idea” what they were doing.

Another engineer said they were uncertain of a “road map” and “pivoted many times.”

Phytel, an industry leader at the time focusing on population health management, was bleeding money.

The engineers explained further, chiming in that IBM’s management had zero technical experience that led management wanting to create products that were “simply impossible.”

Not only were these products impossible, but they in no way took advantage of the resources these three companies had at their disposal.

Do you still want to invest in IBM?

Fast forward to today.

IBM is being sued in federal court with the plaintiff’s, former employees at the firm, claiming the company unfairly discriminated against elderly employees, firing them because of their age.

The documents submitted by the plaintiff’s state that “IBM has laid off 20,000 employees who were over the age of 40” since 2012.

This prototypical legacy company has more problems than the eye can see in every nook and cranny of the company.

If you have IBM shares now, dump them as soon as you can and run for cover.

It’s a miracle that IBM shares have eked out a paltry gain this year. And this thesis is constant with one of my overarching themes – stay away from all legacy tech firms with no cutting-edge proprietary technologies and stagnating growth.

________________________________________________________________________________________________

Quote of the Day

“Some say Google is God. Others say Google is Satan. But if they think Google is too powerful, remember that with search engines unlike other companies, all it takes is a single click to go to another search engine,” said Alphabet cofounder Sergey Brin.

Global Market Comments

August 23, 2018

Fiat Lux

Featured Trade:

(WHY THE DOW IS GOING TO 120,000),

(X), (IBM), (GM), (MSFT), (INTC), (DELL),

($INDU), (NFLX), (AMZN), (AAPL), (GOOGL),

(THE MAD HEDGE CONCIERGE SERVICE HAS AN OPENING),

(TESTIMONIAL)

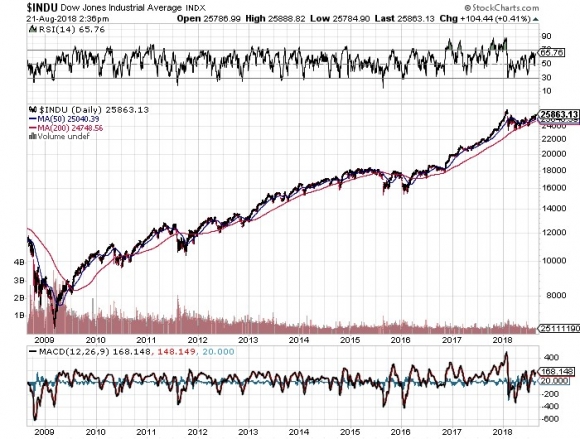

For years, I have been predicting that a new Golden Age was setting up for America, a repeat of the Roaring Twenties. The response I received was that I was a permabull, a nut job, or a conman simply trying to sell more newsletters.

Now some strategists are finally starting to agree with me. They too are recognizing that a ganging up of three generations of investment preferences will combine to drive markets higher during the 2020s, much higher.

How high are we talking? How about a Dow Average of 120,000 by 2030, up another 465% from here? That is a 20-fold gain from the March 2009 bottom.

It’s all about demographics, which are creating an epic structural shortage of stocks. I’m talking about the 80 million Baby Boomers, 65 million from Generation X, and now 85 million Millennials. Add the three generations together and you end up with a staggering 230 million investors chasing stocks, the most in history, perhaps by a factor of two.

Oh, and by the way, the number of shares out there to buy is actually shrinking, thanks to a record $1 trillion in corporate stock buybacks.

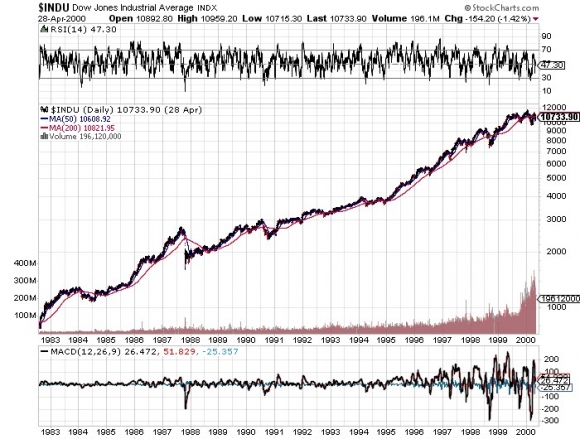

I’m not talking pie in the sky stuff here. Such ballistic moves have happened many times in history. And I am not talking about the 17th century tulip bubble. They have happened in my lifetime. From August 1982 until April 2000 the Dow Average rose, you guessed it, exactly 20 times, from 600 to 12,000, when the Dotcom bubble popped.

What have the Millennials been buying? I know many, like my kids, their friends, and the many new Millennials who have recently been subscribing to the Diary of a Mad Hedge Fund Trader. Yes, it seems you can learn new tricks from an old dog. But they are a different kind of investor.

Like all of us, they buy companies they know, work for, and are comfortable with. During my Dad’s generation that meant loading your portfolio with U.S. Steel (X), IBM (IBM), and General Motors (GM).

For my generation that meant buying Microsoft (MSFT), Intel (INTC), and Dell Computer (DELL).

For Millennials that means focusing on Netflix (NFLX), Amazon (AMZN), Apple (AAPL), and Alphabet (GOOGL).

That’s why these four stocks account for some 40% of this year’s 7% gain. Oh yes, and they bought a few Bitcoin along the way too, to their eternal grief.

There is one catch to this hyper-bullish scenario. Somewhere on the way to the next market apex at Dow 120,000 in 2030 we need to squeeze in a recession. That is increasingly becoming a topic of market discussion.

The consensus now is that an impending inverted yield curve will force a recession sometime between August 2019 to August 2020. Throwing fat on the fire will be a one-time only tax break and deficit spending that burns out sometime in 2019. These will be a major factor in U.S. corporate earnings growth dramatically slowing down from 26% today to 5% next year.

Bear markets in stocks historically precede recessions by an average of seven months so that puts the next peak in top prices taking place between February 2019 to February 2020.

When I get a better read on precise dates and market levels, you’ll be the first to know.

To read my full research piece on the topic please click here to read “Get Ready for the Coming Golden Age.”

Global Market Comments

August 16, 2018

Fiat Lux

SPECIAL ARTIFICIAL INTELLIGENCE ISSUE

Featured Trade:

(NEW PLAYS IN ARTIFICIAL INTELLIGENCE),

(NVDA), (AMD), (ADI), (AMAT), (AVGO), (CRUS),

(CY), (INTC), (LRCX), (MU), (TSM)

Mad Hedge Technology Letter

August 14, 2018

Fiat Lux

Featured Trade:

(BUY ADVANCED MICRO DEVICES ON THE INTEL STUMBLE),

(AMD), (NVDA), (INTC)

It's not an ideal time to own chip stocks because of the trade war jading the chip sector that has inextricable revenue links to mainland China.

But if you feel audacious and want a name to sink your teeth into that is hitting all the right notes, readers must look at Advanced Micro Devices, Inc. (AMD).

After all, what follows a trade war is trade peace, and the chips are the most oversold tech sector out there.

Intel Corporation's (INTC) loss is (AMD)'s gain.

It's a zero-sum game where companies are battling for the same contracts.

Chip companies are under relentless pressure to innovate and enhance bit growth and chip capacity.

They spend billions of dollars to retain and expand their talent pool and on R&D to produce the type of high-end chips for which end product companies clamor.

Sometimes, the development process stifles, delaying chip production and delivery of the chips.

Intel botching the 10nm (nanometer) process technology is a kick in the teeth opening up the pathway for (AMD) to harvest further market share gains.

Intel is experiencing a management crisis as of late with former CEO Brian Krzanich resigning in humiliation after details of an inappropriate relationship with an employee surfaced which breached company rules.

The delay is further proof that Intel fails to execute and develop chips relative to competition, and these announcements hurt investor sentiment and the bottom line.

AMD's comparable 7nm Rome is set to hit the market six to nine months before the Intel chips.

This time frame will allow AMD to make an all-out assault on the CPU market and adoptees will be plenty.

The recent success of AMD has coincided with the heaps of innovation generated by this reinvigorated company.

Namely the Radeon GPUs and Ryzen mobile processors have knocked the cover off the ball.

The Ryzen processors are hot because of their competitive power mixed together with a relatively lower cost.

With Intel on the back burner, these prominent chip models will boost earnings growth for AMD in the short term explaining AMD's meteoric rise from a year-to-date low of $9.50 on April 3, 2018, to an intraday high of more than $20 on July 30, 2018.

Any company that doubles in four months warrants my attention.

How did this all happen?

December 1, 2005 represented the high-water mark for (AMD) when shares surged past $40 only to crumble like a stale cookie down to $2 on September 1, 2008.

The price action was nothing short of horrific, and the three years of sequential decline was an investors nightmare.

The story starts in 1993 when AMD created a 50-50 partnership with Fujitsu called FASL to manufacture flash drives.

This monumental loss-making subsidiary later changed its name to Spansion and tore into AMD's profitability losing more than $250 million in its last nine months being an arm of AMD.

AMD divested from this business with Spansion spinning itself out into its own public company.

Spansion was a disaster operating solo leading the company to file for Chapter 11 bankruptcy on March 1, 2009 and sacking 3,000 employees without severance pay.

AMD's turnaround started in 2014 when it hired Dr. Lisa Su who was once vice president of IBM's semiconductor research and development center.

She replaced Rory Read whose PC background made him highly expendable and unsuitable for the future of AMD as well as lacking the technical pedigree to make the decisions for the long-term vision of AMD.

His background as chief operating officer of Lenovo Group, Ltd. influenced him to heavily bet the ranch of the PC flash drive market, which has been in sequential decline for years.

This masterstroke is paying dividends for AMD.

Out of the gates, Lisa Su presented her vision in May 2015 when she detailed her long-term blueprint focusing on developing high-performance computing and graphics technologies for three growth areas: gaming, datacenter, and "immersive platforms" markets.

The change in direction worked out for AMD increasing top-line growth from $4 billion in 2015 to $5.33 billion in 2017.

The outperformance continues with AMD ringing in $3.41 billion for the first two quarters of 2018.

Because of Lisa Su, AMD chips found their way into Microsoft Xbox consoles among other businesses and the long-term vision is playing out positively to the benefit of shareholders.

AMD goes mano a mano with Nvidia (NVDA) in the highly lucrative GPU segment and data center.

Many analysts believed there was no way to come out of this unscathed. But as we have found out, this market is not a winner-takes-all market and there is space for other players to take a piece of the pie.

The Data Center market is poised to eclipse $70 billion by 2021.

AMD server chip projects to command 5.5% of market share in 2019, up from the 2.2% market share in 2018.

Two years later should be even healthier for AMD whose market share will rapidly grow to around 9.5%.

Crypto mining-based purchases of AMD GPU's were all the rage in 2017 with their products flying off shelves like hotcakes.

Last year saw crypto mining make up a material 10% of revenue because of Bitcoin's dazzling run up to $20,000.

High demand for Ryzen and Radeon products continues unabated and this segment will take in more than $4 billion in 2018.

This division's performance is the main reason why AMD annual revenues will increase 47% YOY in 2018 after a YOY rise of 50% in 2017.

Not only are GPU chips needed for crypto mining, the main buyers of GPU are companies developing artificial intelligence and machine learning.

The data center business is tied to the cloud industry, which is one of the hottest parts of technology in the world.

These robust secular trends and AMD's migration to these premium businesses solidifies the genius decision to allow Dr. Lisa Su to steer the ship.

Veering away from the legacy business that cratered its share price down to $2 and being part of a high-growth industry with great products will fuel the share price skyward.

The technology sector has been rife with M&A activity in 2018 with successful and failed mergers happening left and right.

AMD has been rumored for takeover numerous times. The share price received short boosts highlighting the attractiveness this name commands to outside investors.

Top-line growth is what is driving AMD in 2018, and it is in the middle of a growth sweet spot.

Nvidia has gone up 1,750% in the past five years while laying claim to 70% gross margins in its vaunted GPU division.

It will be demonstrably bullish if AMD can mildly replicate this growth trajectory, and I believe it will.

The Mad Hedge Technology Letter has advised readers to stay away from chip companies because of the complicated trade war.

If the trade war subsides or even ends, semiconductor chips will be the first group of stocks whose shares explode to the upside.

In any case, it's always great to understand the premium names in each industry, and I am bullish on AMD.

After the spike to more than $19, a pullback is warranted but it won't be long before these shares go back into overdrive.

Directly after the macro headwinds pass by will be the preferred time to enter into AMD unless you are a long-term investor and plan to buy and hold.

________________________________________________________________________________________________

Quote of the Day

"Especially in technology, we need revolutionary change, not incremental change," - said cofounder and CEO of Alphabet Larry Page.

Mad Hedge Technology Letter

August 13, 2018

Fiat Lux

Featured Trade:

(GOOGLE'S NEW CHINESE PLAY),

(GOOGL), (BABA), (AAPL), (JD), (BIDU), (MU), (INTC)

As a bolt from the blue, Google search is headed back to China.

The project coined Dragonfly commenced in early 2017 as Google sought a way back into the lucrative Chinese market to sell its products.

The retracement to China then later sped up after Google CEO Sundar Pichai secretly met with a top Chinese official in December 2017.

The censored Google search application could be launched in the next six months to a year upon approval from the communist party.

Why China?

There are three times more smartphones in China than in the U.S. This market represents celestial scale unfounded in any other country.

The Chinese Internet population has roughly 772 million people with Internet penetration levels at about 55%.

The U.S. has maxed out its penetration level at 89% and there is little room to snatch up a new group of mass users. This is not the case in China, which has ample amounts of room to run.

In addition, Google hopes to roll out a news aggregation app mirrored on Chinese newsfeed app Jinri Toutiao that implements personalized artificial intelligence to cater toward each unique user's needs.

As of December 2017, users spent an average of 73 minutes per day on this app.

Jinri Toutiao has 120 million daily active users and has been given a valuation of around $35 billion.

The unbridled potential for American large cap tech companies in China is unrivaled.

But navigating around China's murky business environment under the comprehensive controls of the Great Firewall has proved cumbersome highlighting the executional prowess of Apple's (AAPL) iPhone business in China.

Why did Google leave in the first place?

The issue of censorship was the catalyst leading Google search to the exits.

Google was stunned by the exploits of the Chinese communist government, which maneuvered around Google's system targeting human rights activists among other things.

Operating abroad, companies do not always have complete control over the systems they build and the business processes that revolve around it.

Beijing continued to press Google to filter its search results in 2010, and anything but compliance spelled doom for Google's future in China.

Restricting speech is commonplace for many undeveloped countries with brutal regimes.

The U.S. has one of the most lenient free press laws in the world underlying the backbreaking hassle of operating in a country that actively and aggressively suppresses free speech deemed negative to the people in powerful positions.

After Google started rerouting mainland Chinese Google search to its filter-less Hong Kong servers, Google search was unceremoniously shut down within months.

A comeback is in the works at a time when China and America are at each other's throats in a tit-for-tat trade war, complicating the move to reinsert itself back in the Middle Kingdom.

Let's make no bones about it, this is a high-risk, high-reward strategy for Alphabet, which seeks to add yet another growth driver to its profit-making machine.

Out of the FANG group, only Apple has emerged to unlock the Chinese market with outstanding success.

All other American tech competition was rooted out. Only chip names such as Micron (MU) and Intel (INTC) latched onto the Chinese market largely because of the Chinese demand for chips.

This unfortunate development opened the path for the BATs to dominate in China, which is comprised of Baidu (BIDU), Alibaba (BABA), and Tencent.

Rewind back to 2010, Google search was directly competing against China's Baidu headed up by founder Robin Li.

Google had just 14% market share in search and was trailing far behind Baidu, which had 79% of market share.

In 2010, the difference in the quality of the search algorithms between the two couldn't have been larger.

When comparing these search engines, 85% of Google searches would populate vastly different results compared to Baidu's search platform.

Upon further inspection, Google search was deemed far more accurate than the market share leader Baidu, and that has not changed.

China's inferior technological abilities are well noted. The shortage of talent has forced them to institute forced technological transfers from western companies working in China, outright theft of technical know-how by state sponsored hackers, and the use of government loans to finance M&A activity in technological advanced countries.

In fact, Google leaving China robbed the Chinese tech sector of legitimate competition crushing the innovation trajectory or any remnants of one.

This led to the BATs running riot making money hand over fist but still trailing American tech by a country mile in terms of technical ability and innovation.

A lack of competition breeds complacency.

The reintegration of Google search into China will bring a whole new level of top-class ad technology into China.

This could be the beginning of a monumental ramp up in digital ad spend in China, which trails far behind North America and Europe in average revenue per person.

Discretionary spending is robust in China and advertisers want a piece of the action.

As much as this could be an opportunity for Alphabet to invigorate its cash-making enterprise, it is also a chance to enhance the overall Chinese tech sector.

Upon hearing Google will return, Baidu's Li laid down the gauntlet retorting that Baidu will "win one more time."

Having the communist party on your side as a tag team partner goes a long way in China and has been the main reason of foreign firms fleeing in droves in the past.

Alphabet won't have the same help.

Yet, it could learn a great deal from heading into this sensitive opportunity that could also lay the groundwork to operate in other countries with repressive governments bent on destroying freedom of speech.

Naturally, Alphabet employees weren't impressed with this new direction.

Silicon Valley is centered on left-wing social mores and adjusting its model to accommodate a totalitarian regime does not sit well with many workers.

Google saw a mini employee revolt because of Project Maven, a national defense program marrying artificial intelligence with combat operations in the United States.

Allowing Google's technology to possibly fall into the hands of Beijing would be unforgivable and a national embarrassment.

This idea is definitely not part of the low hanging fruit initiative.

This fruit is 20 feet high dangling from a distant branch.

If Alphabet pulls this off, it could add another surging driver to its portfolio, which prints money because of its digital ad segment.

It could potentially increase revenue by 30%.

Alphabet's successfully bringing in its Google search engine back from the cold, albeit censored search engine, could lay the groundwork for other American tech companies to enter the Chinese market, which would crush Alibaba, JD.com (JD), Tencent, and Baidu's share price.

Baidu dropped more than 6% upon this announcement.

The tech expertise level would naturally rise in China if American tech companies were permitted to set up shop, enhancing the total Chinese tech sector.

It would also apply pressure on China's communist government to open up its industries and do away with the protectionist stance that has been a bedrock policy fueling China's unbelievable rise from rags to riches.

China's top-level politicians must understand inward policies of this ilk do not mesh with the status of a country that is the world's second biggest economy. And it was only a matter of time before unyielding backlash ensued.

From the political side, it could possibly offer additional ammunition to the American administration if China wholeheartedly rejects Google's foray into the mainland, even if it complies with every miniscule, arcane rule Beijing throws at them.

It will prove that China is not willing to compromise or make a deal with the deal-obsessed American administration. And it will signal a dead-end road for any large cap American tech company with China aspirations.

The U.S. administration would use this as an "I told you so" moment, highlighting a history of perpetual unfair trade practices. Hopefully, it never gets to this point.

As it stands, many American large cap tech companies won't touch the Chinese market with a 10-foot pole, but the breathless scale is hard to pass up for others.

If Google is stonewalled, expect an even tougher response from the American administration hell-bent on preventing technological transfers to China.

Currently, the Committee on Foreign Investment in the United States (CFIUS) is attempting to recreate the rules to counteract the China threat.

The trade war is ultimately about global supremacy and being able to harness the biggest tool to achieve world hegemony, which is high caliber technology.

The treatment of Chinese and American tech companies by each other's government will give investors deep insight into how this all plays out.

This is Alphabet's last gasp chance at entering China. If it evolves into a spectacular failure, it always has its digital ad business to fall back on and the upcoming mass rollout of Waymo, its autonomous self-driving taxi business.

So why not take a stab at it?

________________________________________________________________________________________________

Quote of the Day

"If Google re-enters the market, it gives us the opportunity to player kill with real swords and spears and win one more time," - said founder and CEO of Baidu Robin Li.

Global Market Comments

August 6, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or FINDING A NEW GIG),

(FB), (TWTR), (INTC), (NFLX), (AAPL), (AMZN),

(RIGHTSIZING YOUR TRADING)