Mad Hedge Technology Letter

August 17, 2020

Fiat Lux

Featured Trade:

(U.S. STYMIES THE ADVANCEMENT OF FOREIGN BAD ACTORS)

(BABA), (AAPL), (IQ), (NFLX), (FB), (GOOGL), (AMZN)

Mad Hedge Technology Letter

August 17, 2020

Fiat Lux

Featured Trade:

(U.S. STYMIES THE ADVANCEMENT OF FOREIGN BAD ACTORS)

(BABA), (AAPL), (IQ), (NFLX), (FB), (GOOGL), (AMZN)

Stay away from Chinese tech companies listed on the U.S. exchanges. I wouldn’t touch them with a 10-foot pole.

Not only are these firms unscrupulous, but the U.S. administration is specifically attacking them as a cornerstone campaign strategy as we close in on the November election.

The blitzkrieg has been increasing at a rapid clip with U.S. President Donald Trump banning social media asset TikTok and chat app WeChat.

Just in the last few hours, the U.S. administration has said they are also “looking at” going after Chinese eCommerce firm Alibaba (BABA) who is the Chinese Amazon.

If the trends continue, there could be no Chinese tech companies freely extracting American revenue by this November.

Things will only get worse.

No doubt the coronavirus fiasco has exacerbated tensions between the countries with both sides dealing with a plunging economy.

The only reason we do not hear about the depths of despair going on in the Chinese economy is because the media is suppressed there.

Chinese media is tightly controlled disabling any negative news that shines an unfavorable light on the Chinese communist party.

Then there is the immoral fraud aspect of Chinese tech companies as every mainland Chinese firm wishes to go public in New York because company financials are never audited, and they are immune from any criminal liability.

This is a recipe to enable reckless Chinese management who state opaque numbers in their financials in the hope that American investors will take the bait.

Another cheater has been unearthed by Wolfpack Research who along with Muddy Waters have made it their mission to root out the bad actors.

The supposed “Netflix (NFLX) of China” Chinese streaming service iQiyi (IQ) plunged in after-hours trade in the U.S. after it announced the Securities and Exchange Commission (SEC) has launched a probe into the company.

The case revolves around iQiyi falsifying their subscription numbers which everyone knows is the key to exhibiting growth in the company.

iQiyi said the SEC is “seeking the production of certain financial and operating records dating from January 1, 2018, as well as documents related to certain acquisitions and investments that were identified in a report issued by short-seller firm Wolfpack Research in April 2020.”

Wolfpack Research has accused iQiyi of inflating 2019 revenue by around 44%.

Wolfpack also said iQiyi artificially overexaggerated expenses among other data.

The SEC probe into iQiyi comes amid rising scrutiny on U.S.-listed Chinese companies following the Luckin Coffee debacle in which they committed the same act of falsifying numbers.

This copycat crime is clearly seen as a big winner in Mainland China encouraging a slew of companies to decide on the same strategy.

The Coffee company admitted to fabricating sales numbers for 2019. The company was subsequently delisted from the Nasdaq in June.

China and its tech firms are one of the few bipartisan issues with strong support from both sides of the aisle and I can only see the temperature in the kitchen getting hotter.

The side effect of purging the Chinese tech out of the U.S. is that it bolsters the investor case for American tech.

Not that they needed help in the first place.

If the government won’t allow foreign companies to compete with Silicon Valley, then the monopolies built by the likes of Apple (AAPL), Facebook (FB), Google (GOOGL), and Amazon (AMZN) will feel protected because of the government effectively widening their moats.

One might argue that the crimes these American companies have committed are just as bad as the Chinese firms, but they get a free pass for being American.

Remember this is the age of de-globalization with national governments protecting national companies and not the other way around.

Silicon Valley companies have tried to pervert the U.S. employment situation by maneuvering around U.S. nationals by applying for the foreign HB-1 visas in droves and underpaying mostly Chinese and Indian nationals to work for the likes of Google and Facebook.

We can’t say these Silicon Valley companies are saints. They certainly are not, but that doesn’t matter in today’s climate when government, billionaires, and tech moguls are assumed as scum from the get-go.

Then there is the personal data issue that can’t be said to be much better than what the Chinese companies are doing.

The double standard is not surprising, and a heavy dose of politics has been injected into the global tech ecosphere to the detriment of cross border trade.

In the fog of war, this is why I have largely focused on U.S. software companies with subscription revenue because it offers more visibility than an unstable revenue model like Uber or Lyft.

In any case, nobody can blame the U.S. government for going this route since, after all, Facebook, Google, Amazon, and Netflix are all banned in China as well.

You don’t see U.S. tech companies trading on the Shenzhen tech index for a reason and after this monster run-up from the March nadir, it’s obvious why Chinese tech firms want to keep that funnel to U.S. investor capital clear.

This series of events that effectively coddles American big tech will insulate them from any real share weakness. The trend is your friend and I am bullish on American big tech.

Mad Hedge Technology Letter

April 13, 2020

Fiat Lux

Featured Trade:

(THE BEST SHORT PLAYS IN TECH)

(EHTH), (IQ)

Fed’s Neel Kashkari described the path of the U.S. economy as a “long, hard road” boding ill for the tech sector. During economically unpredictable times, avoiding tech stocks that could be sinkholes is crucial to protecting a portfolio, which is why it's useful to consider the best short plays in tech.

One person I drop everything to listen to is Muddy Waters Research Founder and CEO Carson Block.

Block is best described as a short-seller, and his calls on allegedly fraudulent accounting practices in publicly traded Chinese companies are typically spot on.

Block has found another potential gem and he is willing to bet on it by acquiring a short position in eHealth, Inc. (EHTH) which owns a digital health insurance exchange.

His gripes revolve around shoddy management who hoped to “pump the stock,” and shares reacted by dropping more than 17% at last Wednesday’s open after Block’s premarket disclosure.

The second part of Block’s argument centered around artificial growth caused by higher TV marketing spend resulting in high churn rates.

His evidence derives from management manipulating its presentation of churn to be misleadingly low and booking multi-year 'tail' revenue at the end of each cohort's estimated life, which is extremely aggressive in light of the significantly elevated churn.

Block didn’t stop there, turning his attention to another Chinese tech company that is billed as the Netflix of China called iQIYI, Inc. (IQ).

Activist firm Wolfpack Research alleges that iQiyi “was committing fraud well before its IPO in 2018” on the Nasdaq, and it’s “continued to do so ever since.”

The Netflix of China has been fudging its numbers for quite a while and is the most egregious example of accounting fraud.

How do they do it?

The inflation of its barter transaction revenue. Barter sublicensing revenues are determined by IQ’s internal estimates of the value of the content it traded.

In other words, IQ’s management can effectively assign any value they want to these transactions, providing an easy opportunity to inflate revenues.

Based on the highest-end estimated value per non-exclusive episode provided by a former IQ employee involved in content acquisition, IQ would have needed to barter the licenses for ~3.9x and ~3.2x the total number of TV series episodes produced by all Chinese production companies to legitimately reach its reported barter revenues in 2018 and 2019, respectively.

IQ is a mature company and will turn 10 years old this month - yet has burned money for 10 consecutive years.

Even worse, losses are rapidly accelerating, unlike its growth and the company is doing more to mask their rotten core.

IQ lost around $1.5B in 2019, $170 million more than 2018.

Meanwhile, paying subscriber growth in 4Q19 hit a nadir at only 0.7%. IQ’s advertising revenue was also crashed -15% in 2019 and it still has a negative gross margin.

The Chinese consumer mindset is to never pay for digital content because they can just find it on the web for free, meaning digital streamers like IQ must go to extreme lengths to create “growth.”

The reverberation from the coronavirus is that tech investors are more risk adverse than ever and any whiff of illegality will scare them off.

Even though the Fed has basically swallowed every asset class we have with its latest move, that will not save the marginal tech companies with dishonest business models.

iQIYI, Inc. (IQ) and eHealth, Inc. (EHTH) are high-risk tech companies that readers should avoid like the plague.

Mad Hedge Technology Letter

July 5, 2019

Fiat Lux

Featured Trade:

(THE BALL IS IN NETFLIX’S COURT)

(NFLX), (DIS), (AAPL), (IQ), (KHC)

Being as volatile as it is, investors are afforded ample opportunity to get into one of the premium tech stocks in the land Netflix (NFLX).

Chasing this one higher is a dangerous thought, as habitual 30% dips is part and parcel of being attached to this supreme online streaming stock.

December of 2018 gave you that sinking feeling when Netflix dropped off a cliff dipping to $260 but spiking after the turn of the year as the Fed swiveled on a dime to save the equity market from implosion.

Let’s make no bones about it, the long-term narrative for Netflix is intact as it’s ever been.

The company simply makes a great product, period, and systematically taps endless demand.

What many cable companies don’t understand is that you cannot make a high-quality film product that wedges in annoying commercials and equally as obnoxious, dictate the window of time in which they should watch the content.

Optionality is value and Netflix has this spot on.

I know many Millennial consumers that would rather jump off a building than subject themselves to commercials.

These factors erode the quality of the product just as if an employer would dictate to one of his or her employees that wanted to take a vacation to Africa.

But the vacation to Africa would have some strings attached.

He or she would only be able to visit at the height of summer in 120-degree Fahrenheit weather while every activity he or she chose to do, would be pre-empted by numerous advertisements that he or she must be shown.

Consumers don’t need these sideshows anymore; the world has developed away from these models and corporates have lost this control.

The loss of corporate control of the consumers is because the internet gives consumers millions of different options at the tip of their fingers.

Tapping into the optionality and the habits that revolve around it is paramount to corporate America.

This is the same reason why big box food companies like Kraft Heinz (KHC) is getting smacked around, consumers have better options and are more aware of them because of technology.

Another example of corporate miscalculation comes in the form of supply chains being redirected from China to South East Asia.

It was clear as day that during my time in China that companies were making a terrible mistake going into China in the first place.

This shows how many corporates are dragged down by a lack of vision and do an awful job of anticipating paradigm shifts that are becoming more common because of the accelerating rate of change of the corporate climate, weather, technology, rule of law, and human migration.

Netflix is effectively blocked from China and China has its own Netflix called iQIYI (IQ), they had no chance from the beginning like Google, Amazon, Facebook, and the many other American tech firms.

Netflix’s business model now has scale working for them and growth numbers will be the main recipients going forward if they focus on high quality content.

That means expect high pay packages to the best media talent in the world.

They can afford to pay a tier 1 actor $50 million per movie because the data buttresses this strategy.

At the same time, Netflix is crushing competition by hoarding the talent with extraordinary pay packages while allowing these highly paid specialists 100% creative control over what they do.

Who would want to work for a company that paid more than double and whose management gave them free reign on creative decisions?

Sounds like an artist’s dream and it’s exactly that for actors like Will Smith who have signed onto Netflix’s project.

I would even suggest that Netflix needs to overpay actors just for the reason of taking them off the market for competitors.

This truly is the lucrative golden age for actors, producers, and directors who are the top 1% of their craft, but for everyone else, it’s a hard slog.

This usually means becoming a tier 1 actor before the migration to online streaming happened.

The picture I am painting is that Netflix’s success and future prospects aren’t about Disney or other competitors, but entirely about them.

He who has the most chips at the table with the best cards is in best position to win and the same goes for Netflix.

The rest of the bunch like Apple (AAPL) and Disney who are late to the party will be feeding off the rest of what Netflix cannot exploit and that’s the best-case scenario.

Disney should be able to have moderate success with its array of great movie, television, and sports content.

I’d be surprised if Disney failed because they possess the ingredients to concoct a delicious cocktail.

Apple has a harder proposition because of the lack of entertainment value in their content. They are still tied to the hardware sales and much of the service sales come from their app store and servicing the hardware.

But Apple does have money, and a lot of it to throw at the problem, but I don’t believe CEO of Apple Tim Cook is the right man to navigate through the travails of the online content world. He’s an operations guy and has never proved anything more than that.

Netflix still has substantial opportunity to grow its brand and the runway is long.

The demand for watching great original movies and television programs without commercials whenever consumers want is still in the first innings.

Even though Disney will remove some non-original content from Netflix’s platform, the content spend on a massive pipeline of new projects will more than fill the void left by Disney’s content.

In fact, Netflix should thank Disney for all those years that Disney allowed them to build their brand through 3rd party premium content like the television program Friends.

I believe Netflix does not need 3rd party content anymore, that is how much Netflix has bolted ahead in the past few years.

The company has introduced price hikes with its 4K premium package going from $14 to $16 per month.

But Netflix is still underpricing itself to the consumer to grab market share, and there is still pricing headway in the future if the company wants it.

In the coming months, Netflix plans to offer more detailed reporting on its metrics and the transparency will give investors even more insight into why this company is brilliant.

I believe the numbers will show that Netflix is absolutely killing it.

As for the trading, Netflix has settled in a range of $320 to $380 and any dips to the $340 range should be quite appetizing.

Add incrementally and use any large dip to drop your cost basis.

Stand aside if you cannot handle heightened volatility.

Mad Hedge Technology Letter

December 17, 2018

Fiat Lux

Featured Trade:

(WHY TENCENT WILL REMAIN TRAPPED IN CHINA)

(TME), (SPOT), (IQ), (GOOGL), (FB)

So you thought that Tencent Music Entertainment (TME), the Spotify (SPOT) of China, going public at $13 a share on the New York Stock exchange would mean the music streaming giant would potentially tyrannize the Western music streaming market.

Relax, it will never happen, China’s personal data laws are analogous to Facebook’s (FB) lax data guidelines multiplied by a factor of 10.

There is no possible scenario in which a Chinese content service constructed at the magnitude of Tencent Music Entertainment Group would ever get the thumbs up from American regulators.

The ongoing trade war has effectively barred any Chinese capital’s ability to snap up key American technological firms, as well as stymieing any Chinese tech unicorns dishing out streaming content in participating in a monetary relationship with the American consumer.

In August, the Department of the Treasury which chairs the Committee on Foreign Investment in the United States (CFIUS) rolled out an expansionary pilot program widening CFIUS’ jurisdiction to review foreign non-controlling, non-passive investments in companies that produce, design, test, manufacture, fabricate, or develop “critical technologies” within certain industries deemed paramount to national security.

Even though the amendment does not specify China, it means China.

If you had a hunch that Tencent would take over the music streaming world, then the better question is to ask yourself if Tencent Entertainment is equipped to take over the Chinese streaming world and monetize the product efficiently.

What really is (TME)?

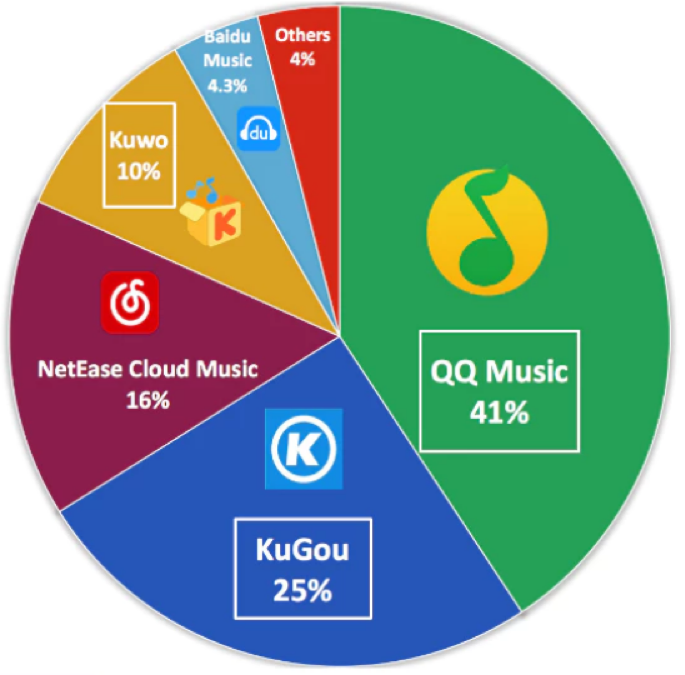

(TME) is the Tsar of Chinese music streaming with apps that allow users to stream music, sing karaoke, and watch musicians perform live. (TME) dominates this sphere of Chinese tech with a combined 800 million monthly active users.

(TME) is a concoction of services including QQ Music, Kugou, Kuwo, and karaoke app WeSing making up over 70% of the music streaming industry in China.

Its daily active users (DAUs) spend over 70 minutes per day on the platform and have inked exclusive deals with elite Western artists.

Tencent Music's revenue nearly doubled YOY to $2 billion during the first nine months of 2018, and its net income more than tripled to $394 million.

The social entertainment services aspect has been a massive revenue driver for them including income from virtual gifts on WeSing, a platform where fans gift virtual items to favorite singers, and sign up for premium memberships giving users access to exclusive concerts.

This collection of clever services mixed with social media has been successful, and the reason why it comprises 70% of total revenue.

Paid membership has grown 24% YOY to 9.9 million while paid users only make up 4.4% in China. This is a huge change in the tech climate from the past when Chinese netizens would never pay for internet content. This has allowed the average revenue per user (ARPU) to creep up to $17.22 per paid user.

The other 30% of revenue can be attributed to its ad-less music service which is not ad-less for free users.

So, in fact, the 30% of the business that mirrors Spotify is its Achilles heels echoing the painstaking task of monetizing pure music content.

No company has ever shown that a pure music streaming internet model can be profitable, the music streaming graveyard is littered with the failed attempts of companies from the past.

The unit registered a mere $1.24 in average revenue per paid user during the third quarter, paltry compared to (TME)’s social media products.

(TME)’s combination of social media and music entertainment weighted towards virtual gifts’ income is a weak business model in the west and would not extrapolate in the western world.

It is a supremely China model only unique to China and other Asian countries.

Therefore, I would point out that even if this arm of Tencent could migrate to America, management knows better than to put square pegs in round holes.

That being said, its potential in China is its long runway and most Chinese content companies haven’t been able to crack the western market.

The only types of Chinese companies that have had any remnant of success in the west are hardware companies and look what happened to telecommunication equipment companies Huawei and ZTE recently – taken out by the western regulatory sledgehammer.

It’s crystal clear that the Chinese understanding of personal data and IP regulation simply don’t marry up with western standards, and that is why I suggested that these two massive tech worlds are in for a hard splintering dividing these two competing models.

There has been some intense jawboning going on behind the scenes as Huawei, who is in the lead to develop 5G technology, still needs Qualcomm’s radio access technology to make 5G a reality.

The scenario of a hard fork between western and Chinese 5G becomes more real each passing day.

Part of Tencent Music’s ability to perform revolves around its swanky position installed in the center of the most popular chat app in China called WeChat.

Using this position as a fulcrum, Tencent Music plans to invest 40% of the capital raised from its IPO on expanding its music library, 30% on product development, 15% on marketing, and the last 15% on M&A.

For right now, there is an elevated emphasis on growing the number of paid users and converting its free users to premium subscriptions.

Ironically enough, Spotify has a 9% stake in Tencent Music and Tencent has a 7.5% holding in Spotify. Just by having stakes in each other is enough reason to avoid migrating into the same competitive markets with each other.

If you read between the lines, the stakes seem more a pledge of trading expertise in developing each other’s business as you see traces of each other in both unicorns.

Would I invest in Tencent Music?

One word – No.

There are almost 1,000 pending lawsuits alleging copyright infringement, not a huge surprise here.

Tencent concedes around 20% of the music content is not licensed.

Pouring fuel on the fire, a Tencent Music executive is also being sued by a seed investor claiming he was bullied into selling his stake ahead of its IPO.

There are question marks surrounding this company and that might have been part of the justification of tapping up the American public markets to prepare for this next stage of uncertainty.

As it is, Spotify cannot make money because of the elevated royalty costs eroding its business model, (TME) probably can if it steals most of its music, but that is a suicide mission waiting to happen.

Fortunately, Tencent is a hybrid mix of not only pure music streaming but of social media fused with music apps through gift giving gimmicks and karaoke-themed services.

These higher margin drivers are the reason why Tencent is profitable and Spotify is not, plus the giant scale of servicing 800 million Chinese users that give credence to the freemium model.

However, it’s entirely feasible that Tencent Music could use a good portion of the $1.1 billion from the IPO to battle the slew of pending lawsuits waiting around the corner.

Would you want to invest in a company that went public just to fund their legal defense?

Definitely not.

Look at its streaming cousin iQIYI (IQ), shares peaked over $40 in June after its IPO and have swan-dived ever since going down in a straight line and is trading around $17 today.

In general, most Chinese tech stocks have been collateral damage of a wider trade war pitting the maestros of crude geopolitical strategies against each other.

This year has not been kind to Chinese tech shares, and considering most of Tencent’s music library has been stolen, investors would be crazy to invest in this company.

I am surprised this company held up as well as it did on IPO day because the timing of the IPO couldn’t have been worse in a segment of tech that is awfully difficult to become profitable in a country whose economy is softening by the day in an insanely volatile stock market.

And to be honest, I would have stopped listening about this company after knowing they face pending lawsuits of up to 1000.

As for Spotify, yes, they are the industry leader in music streaming but investors need concrete proof they can become profitable. I like the direction of increasing operating margins, but that all goes to naught if it’s in a perpetual loss-making enterprise. I would sit out on both these stocks with a much negative bias towards its ticking time bomb Chinese music version.

Regulation and the trade war have taken a huge swath of tech off the gravy trade such as semiconductors, Google, social media, hardware, American tech who possess supply chains in China and I would smush in Chinese tech ADR’s on that list too.

Stay away like the plague.

Global Market Comments

June 25, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, OR IS THIS A 1999 REPLAY?),

(AAPL), (FB), (NFLX), (AMZN), (GE), (WBT),

(JOIN ME ON THE QUEEN MARY 2 FOR MY JULY 11, 2018 SEMINAR AT SEA),

(JUNE 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(SQ), (PANW), (FEYE), (FB), (LRCX), (BABA), (MOMO), (IQ), (BIDU), (AMD), (MSFT), (EDIT), (NTLA), Bitcoin, (FXE), (SPY), (SPX)

Below please find subscribers' Q&A for the Mad Hedge Fund Trader June 20 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

As usual, every asset class long and short was covered. You are certainly an inquisitive lot, and keep those questions coming!

Q: What are your thoughts on Square (SQ) as a credit spread or buyout proposition?

A: I love Square long term, and I think there's another double in it. They were a takeover target, but now the stock's getting so expensive it may not be worth it. So, Square is a buy. However, look for a summer sell-off to get into a new position.

Q: The FANGs feel a little bubbly here; will they pull back on a market dip?

A: Yes, my entire portfolio of FANG options is designed to expire on the July 20th expiration. In fact, I may even come out before then as we reach the maximum profit point on these option call spreads. Then look for a summer meltdown to get back in. The FANGs could double from here. If I am wrong they will just continue to go straight up.

Q: Palo Alto Networks (PANW) has a new CEO; are you concerned?

A: Absolutely not, I love Palo Alto networks, as well as the (FEYE) FireEye. It's just a question of getting in at the right price. It's one of the many ballistic stocks in Tech this year that we've been recommending for a long time. Hacking an online theft is never going to go out of style.

Q: Is it time to sell Facebook (FB)?

A: Yes, if you're a trader. No, if you're a long-term investor. There's another double in it. You're going to have natural profit taking on all of these Techs for the short-term, and possibly for the summer, because they've just had enormous runs. If you aren't in the FANGs this year, you basically don't have any performance because almost all of the rest of the market has gone down.

Q: What are your thoughts on Lam Research (LRCX)?

A: The whole chip sector has had two big sell-offs this year because of their China exposure and the trade wars. Expect more to come. China gets 80% of their chips from the U.S. This is normal at the end of a 10-year bull market. It's also normal when a sector transitions from highly cyclical to secular, which is what's happening in the chip sector. Twice the volatility gets you twice the returns.

Q: Would you stay away from Chinese stocks like Alibaba (BABA), Momo Inc.(MOMO), IQ (IQ), and Baidu (BIDU)?

A: I have stayed away because of the trade war fears, and it was the completely wrong thing to do, because they've gone up as much as our Tech stocks, except for the last week. So yes, I would be buying dips on these big Chinese Tech stocks, because they are drinking the same Kool Aid as our Techs, and it's working.

Q: I hear that short selling of volatility is coming back; is that a good thing?

A: Actually, it is a good thing, because it creates buyers on these dips when you had no short sellers left. The entire industry got wiped out in February creating $8 billion in losses. There was no one left to cover those shorts and support the market. Of course, the result was we got a lower low down here because of that. It's always better to have a two-way market to get a real price. Now professionals are sneaking back in on the short side, which is as it should be. This should never have been a retail product.

Q: Why are international markets so disconnected from the U.S.? Many Asian markets are down heavily while the U.S. are up.

A: The U.S. stock market benefits from a rising dollar and rising interest rates, whereas international markets suffer. When you have weak currencies in the emerging markets, people sell their stocks to avoid the currency hit, and that takes the emerging markets down massively. A lot of emerging market companies have their debts denominated in U.S. dollars, so they get killed by a strong greenback. Also, the emerging markets make a lot of money selling goods into China, so when the Chinese economy gets attacked by the U.S. and growth slows, it has the byproduct of attacking all our other allies in Southeast Asia.

Q: Is it a good idea to sell everything for the summer and just de-risk for my portfolio?

A: That's what I'm doing. Summer trading is usually horrible, and now we're going into the summer at close to a high for the year, with a terrible political backdrop and possible economic growth peaking right here. So, yes, it's a good time to sit back, count your money, and maybe even spend some of it on a European vacation.

Q: When do you think the yield curve will invert?

A: In a year, and that is typically when you get a peaking of economic growth and the stock market.

Q: Is the Fed's faster-than-expected desire to raise rates good for equities, or will investors likely sell this news as quantitative tightening continues?

A: Short-term they will buy the market on rising rates, they always do at the early part of an interest rate rising cycle. They sell stocks when you get to the middle or the end of a rate rising cycle.

Q: Do you think large Tech stocks are expensive here?

A: No, I think the Large-Cap Tech stocks can potentially double here. It can take another year to year and a half to do it, and if they don't do it in this cycle they will certainly do it in the next one, after the next recession in the 2020s. So, long term you want to think FANG, FANG, FANG, TECH, TECH, TECH. You really shouldn't have anything else in the long term, except for maybe Biotech, where you can now get in at a multiyear low.

Q: Can I buy a chip company like Advanced Micro Devices (AMD), or should I buy a cloud company, like Microsoft (MSFT)?

A: I would go with the Cloud company. The innovation there is incredible. Cloud is growing like the Internet itself was growing on its own in 1995, and with chip stocks like (AMD), you're going to get much higher volatility, but more gain. So, pick your poison. But I would go with the Cloud plays.

Q: Can we watch the recorded version of this webinar later?

A: Yes, we post the webinar on our website a couple hours later, if you're a paid subscriber.

Q: What about the CRISPR stocks?

A: They are a screaming buy right now, buy Editas Medicine (EDIT) and Intellia Therapeutics (NTLA) on the dip. The paper that triggered the sell-off saying that CRISPR causes cancer is complete BS.

Q: Only 30 million in Bitcoin was stolen in South Korea so will that still have an impact?

A: Yes, but there have been countless other hacks this year and the total loss is well over $500 million. In addition, Bitcoin is now down 70% from its December top so not all is well in cryptocurrency land.

Q: Should we expect any Trade Alerts before August 8?

A: Yes, some of my best trades have been done while only vacation. I once sold short the Euro (FXE) from the back of a camel in Morocco. Another time, I bought the S&P 500 (SPY) while hanging from a cliff face on the Matterhorn. Both of those made good money.

Q: Will the S&P 500 reach new highs before the end of the year?

A: Yes, once you get the election out of the way, that removes a huge amount of uncertainty from the market. If we could end our trade war before then, I think you're looking at another 10-15% in gains from this level by the end of the year. That takes you to an (SPX) of 3,100 by the end of 2018, which was my January 1 prediction.

Q: What does all the heavy mergers and acquisition activity mean for the market?

A: It means fewer stocks are left to trade. Stock shortages leads to higher prices, always, so it is a big market positive this year

Good Luck and Good Trading.

John Thomas

CEO and Publisher

The Diary of a Mad Hedge Fund Trader