Mad Hedge Biotech and Healthcare Letter

January 13, 2022

Fiat Lux

Featured Trade:

(NO REST FOR THIS PANDEMIC SUPERSTAR)

(PFE), (MRK), (RHHBY), (DNAY), (JNJ), (LLY), (BNTX), (EDIT)

Mad Hedge Biotech and Healthcare Letter

January 13, 2022

Fiat Lux

Featured Trade:

(NO REST FOR THIS PANDEMIC SUPERSTAR)

(PFE), (MRK), (RHHBY), (DNAY), (JNJ), (LLY), (BNTX), (EDIT)

Amid the pandemic fatigue hounding everyone these days, one name continues to attack the situation with consistent vigor: Pfizer (PFE).

It’s not a stretch to say that its COVID franchise is the most popular line in Pfizer’s portfolio today.

Needless to say, this is highly lucrative from a shareholder’s point of view. The company’s vaccination business has recorded over 3 billion doses to generate roughly $36 billion in sales from Comirnaty alone in 2021.

Riding the momentum of its successful 2021, the company anticipates an even more successful 2022.

So far, Pfizer is targeting an increase in its Comirnaty production to hit at least 4 billion doses this year.

Aside from being one of the first companies to develop a vaccine, the company has also created a highly effective antiviral COVID treatment that can be taken orally: Paxlovid.

While Merck (MRK) has earlier announced its move to come up with a similar oral treatment, Pfizer’s pill proved to be more effective.

Actually, customers are starting to take note of the difference and are switching brands. France already canceled their agreement with Merck and decided to order Pfizer’s Paxlovid instead.

This once again underscored the dominance of Pfizer’s brilliant R&D segment and the company’s capacity to rapidly come up with highly effective solutions for issues involving COVID.

The way Pfizer has been handling the COVID situation can be compared to Roche’s (RHHBY) approach and eventual blockbuster success with Tamiflu over 20 years ago.

Although the flu is obviously not as deadly as the coronavirus, it still caused widespread economic breakdown and health problems.

When Tamiflu eventually entered the market, the world was finally granted a simple medical answer for what was initially thought to be an unsolvable health problem.

Pfizer’s Paxlovid could very well be the Tamiflu for COVID.

Looking at Paxlovid’s effect in terms of revenue, it’s safe to say that this oral treatment can drive medium-term growth for Pfizer.

To date, Pfizer disclosed that Paxlovid would be sold for roughly $700 for each treatment course.

Let’s use the US numbers as an example to help put things in perspective. So far, the country has recorded approximately 170,000 cases per day.

If we assume that this will be the average for 2022, then there will be about 62 million COVID patients this year.

Let’s say that only 40% of these patients qualify for Pfizer’s treatment; then this would reach 24 million people at $700 each to rake in roughly $17 billion in total revenue in the US alone.

The number would definitely be significantly higher considering that Paxlovid will be offered as a global COVID treatment.

It’s evident that Pfizer’s efforts are paying off, as the sheer earnings power of the company’s COVID-19 pandemic franchise could provide a medium-term boon for its investors.

In 2021, Pfizer recorded a 130% growth in its revenue, with the numbers still climbing.

While its pandemic response has become its primary growth driver, Pfizer’s other key segments also posted promising revenues.

To sustain its climb, the company has continued to invest in R&D heavily.

A notable investment it made recently is an $8 million upfront payment to Codex DNA (DNAY) for the smaller biotechnology company to “produce certain materials of interest to Pfizer.”

According to the deal involving the exclusive product, Codex expects $10 million in technical milestone payments, up to $60 million in clinical development milestones, and $180 million in sales milestones.

Codex DNA is a small biotechnology company with a market capitalization of $267 million. It’s a spinoff from a California company called Synthetic Genomics.

While Pfizer and Codex have yet to share their plans publicly, we can hypothesize that it has something to do with the large biopharma using the small biotech’s technology to accelerate its mRNA vaccine development process.

After all, Codex’s distinct value proposition lies in its rare ability to automate various elements of the entire process. Its push-button, end-to-end solutions promise to build functional grade synthetic mRNA and DNA.

In effect, this will save cost and time for its clients.

Aside from Pfizer, this small biotech has been collaborating with other organizations like Duke University and MIT.

It has also been working with large biopharmas, including Johnson & Johnson (JNJ), Eli Lilly (LLY), BioNTech (BNTX), Merck, and even gene therapy expert Editas (EDIT).

For 2022, Pfizer is anticipated to generate at least $96 billion in sales, showing off a jaw-dropping 17.2% jump from its 2021 revenue and a 229% increase from 2020.

As we slowly accept that COVID will become a staple in our lives in the coming years, I think investors would be wise to add proven “experts” in their portfolio to take advantage of the ever-present and increasing demand.

Mad Hedge Biotech and Healthcare Letter

January 11, 2022

Fiat Lux

Featured Trade:

(A GOOD STOCK TAINTED WITH CYNICISM)

(BIIB), (LLY), (RHHBY), (SAVA), (PRTA), (SAGE)

Last year, talks that Samsung was in the process of making a $42 billion buyout bid for Biogen (BIIB) brought about a mixture of cynicism, hope, intrigue, and excitement over a potential agreement.

It was especially intriguing since the reported offer was roughly 20% more than Biogen's expected $35 billion projected value.

Eventually, this report was proven to be false.

But the mere fact that it garnered such traction and interest only highlighted Biogen’s seemingly debilitated state following their failure to deliver on a promised unprecedented motherlode following the controversial Alzheimer’s drug approval and lukewarm reception.

If you recall, experts expected Biogen’s Alzheimer’s drug, Aduhelm, to generate double-digit billions in sales considering its list price of approximately $50,000 annually and the roughly 5.8 million individuals diagnosed with the condition in the US alone.

Theoretically, Aduhelm’s addressable market was projected at $325 billion.

At that time, Aduhelm was anticipated to rake in at least $50 billion per annum—a projection that was reflected in the 55% increase in the company’s share price.

However, things didn’t go according to plan. Aduhelm’s accelerated FDA approval caused so much uproar that it eventually affected the drug’s marketability as well.

In an attempt to temper the protests, Biogen cut the cost of Aduhelm to almost half, with the drug priced at $28,000 annually instead of its original $50,000.

Despite this, the projected mega-blockbuster’s sales continued to disappoint, with its third-quarter earnings in 2021 only reaching a measly $300,000.

This January, though, Aduhelm might have a shot at saving redemption courtesy of a potential Medicare reimbursement scheme.

Ultimately, however, the decision to offer any form of reimbursement scheme will not only affect Biogen but all the Alzheimer’s disease treatments in the future.

This is actually one of the critical points that many people missed when Aduhelm gained approval.

In focusing too much on the share price of Biogen, they appeared to have misinterpreted the true purpose of the FDA’s decision.

Granting an accelerated approval for Aduhelm did not mean that the FDA was handing the company a chance to generate double-digit billions in sales.

What the agency intended was to demonstrate support for Biogen's thesis regarding a potential Alzheimer’s therapy.

That is, you can slow down the patients’ cognitive decline by aiming to reduce the amyloid-beta levels in their brains.

The FDA’s decision has, in effect, opened the floodgates not only for Biogen’s Aduhelm, but for all the other biotechnology companies working on the same idea.

To date, the companies developing their own Alzheimer’s disease treatment include Eli Lilly (LLY) with Donanemab and Roche (RHHBY) with Gantenerumab.

Both are expected to release results within the year or early 2023.

Other names are Anavex Life Sciences (SAVA) and Prothena (PRTA).

Outside its Aduhelm efforts, Biogen has also been developing new treatments, as demonstrated by the $4 billion investment it made on its R&D last year.

One promising candidate that can deliver blockbuster sales is its major depressive disorder treatment Zuranolone, which is a collaboration with Sage Therapeutics (SAGE).

Meanwhile, Biogen is also working with Ionis (IONS) to develop a successor for its spinal muscular atrophy treatment Spinraza.

Since this top-selling drug is expected to lose patent protection in 2023, the company has spent $60 million to come up with a new and more potent version: BIIB115.

For context, Spinraza recorded more than $2 billion in sales in 2021.

At this point, investor sentiment on the company has stooped at an incredibly low level. Unfortunately, the weak rollout of its Alzheimer’s treatment has planted suspicions regarding Biogen’s entire pipeline.

However, I think this kind of pessimism is quite misguided.

While the reality is that Aduhelm may never achieve the mega-blockbuster status it was once believed to reach, the situation shouldn’t necessarily diminish the truth that Biogen is actually performing quite well—and it will continue to do just fine.

Mad Hedge Biotech and Healthcare Letter

November 11, 2021

Fiat Lux

Featured Trade:

(A HIGH-QUALITY DIVIDEND STOCK WITH MORE ROOM TO GROW)

(LLY), (INCY), (GILD), (ABBV), (PFE), (NVO), (BIIB)

Investors can enjoy long-term recurring income and stability with dividend stocks. However, paying out dividends is largely discretionary.

Each business frequently determines whether it’s in a good position to hand out part of its profits to shareholders.

One method to assess a dividend’s safety is reviewing a company’s history and whether it makes regular payouts. The longer its track record shows a consistent payment, the more preferable the business.

There’s a stock particularly known for paying dividends every year for over a century in the biotechnology and healthcare sector: Eli Lilly (LLY).

While Eli Lilly’s dividend yield is only 1.5% at its current share price, which is a bit over the S&P 500’s average reported at less than 1.3%, the company has been paying out dividends since 1885.

Apart from its consistent payouts throughout the years, Eli Lilly also holds promising potential for future hikes.

At the moment, the quarterly payout of Eli Lilly is $0.85, which is 75% higher than its 2015 payout of $0.49.

This number can still climb thanks to its robust revenue growth of 19.2% year over year, with its current approved drug portfolio generating $13.55 billion in the first six months of 2021.

In the first two quarters of the year alone, several products recorded year-over-year sales growth of over 20%.

Eli Lilly isn’t content in growing its dividend, though. It’s also working on expanding its drug portfolio.

Among its existing drugs, the company has been maximizing Olumiant to include more indications.

One of the recent advancements involving Olumiant is Eli Lilly’s work with Incyte (INCY), which utilizes the drug as a treatment for COVID-19 patients.

In fact, the FDA has recently approved the use of Olumiant with or without the need to combine it with Gilead Sciences (GILD) Remdesivir.

However, Olumiant’s application as a COVID-19 treatment isn’t the most promising expansion for this drug.

Just recently, Eli Lilly and Incyte disclosed that Olumiant could be used as a treatment for an autoimmune disorder more commonly known as alopecia areata—an indication that could very well transform the drug into the company’s next blockbuster.

In a nutshell, Olumiant can help alopecia patients regrow their hair at a more rapid speed and consistent rate than other competitors.

So far, the drug has recorded an 80% hair growth among those who tested it.

In the previous months, the FDA included Olumiant and AbbVie’s (ABBV) Rinvoq in the list of JAK inhibitors that needed to carry a warning label sharing their severe potential side effects like blood clots and even cancer.

Despite this, Eli Lilly’s product proved to be safe for alopecia patients.

If approved for alopecia, Olumiant could become a groundbreaking treatment sought after by roughly 147 million people across the globe who suffer from the condition.

For context, the global market for alopecia is projected to grow in revenue from $ 7.6 billion in 2020 to reach over $ 14.2 billion by 2028 annually.

Alopecia areata, which is the target market of Eli Lilly, is expected to hold about 35% of the total. This puts the addressable market for Olumiant at $5 billion by 2028.

Considering that another name has been working to dominate the market, Pfizer’s (PFE) Cibingo, we can realistically assume that Eli Lilly will get at least 15% of the market share worldwide.

This would mean roughly $750 million in yearly revenue for Olumiant’s alopecia market alone.

Other than its work on alopecia areata, Eli Lilly has another potential blockbuster. This time, the treatment is targeting the diabetes sector.

The company has an up-and-coming treatment called Tirzepatide, which could not only expand Eli Lilly’s diabetes market share but also provide a strong competitor against Novo Nordisk’s (NVO) top-selling Ozempic.

Tirzepatide is the successor of Eli Lilly’s bestseller Trulicity, which logged $2.99 billion in the first half of 2021 and is set to lose patent protection by 2027.

Looking at Tirzepatide’s trajectory, the drug is projected to reach peak annual sales worth $10 billion—an amount that could easily offset the gradual decline in sales by Trulicity.

Even the company’s breast cancer drug, Verzenio, is set to show off impressive growth soon. In the first half of 2021, the treatment raked in $610 million in sales, demonstrating a 53.8% increase year-over-year.

Considering Eli Lilly’s efforts to distinguish its breast cancer treatment from Pfizer’s Ibrance, Verzenio is anticipated to generate $4.6 billion in annual sales by 2024.

Another exciting development is Eli Lilly’s Alzheimer’s disease treatment Donanemab.

Although Phase 3 data are expected to be released in 2023, this candidate is already reported to be a superior treatment than Biogen’s (BIIB) controversial Aduhelm.

These are some of the results of Eli Lilly’s efforts to continue expanding in the diabetes area, as seen in its ramped-up R&D spending.

So far, the company boosted its research investment by 21% year-over-year to reach $3.36 billion.

While doing this isn’t exactly a guarantee of commercial success, it’s undoubtedly a solid strategy to protect and enhance its pipeline.

Overall, Eli Lilly is a high-quality stock with a verifiable and impressive history of innovation.

Given the promising lineup of approved drugs and pipeline candidates of Eli Lilly, it’s reasonable to expect roughly a 15% yearly earnings growth from the company over the next 5 years.

Mad Hedge Bitcoin Letter

October 14, 2021

Fiat Lux

Featured Trade:

(WHAT’S NEW IN BIOTECH)

(CGTX), (BIIB), (LLY), (ABBV), (NVS), (TAK), (PYXS), (PFE),

(AZN), (GILD), (GSK), (IMGN), (ISO), (TMO), (BIO)

As the biotechnology world is ever-evolving, with several companies going public every few months, let me share some of the most promising names that recently emerged.

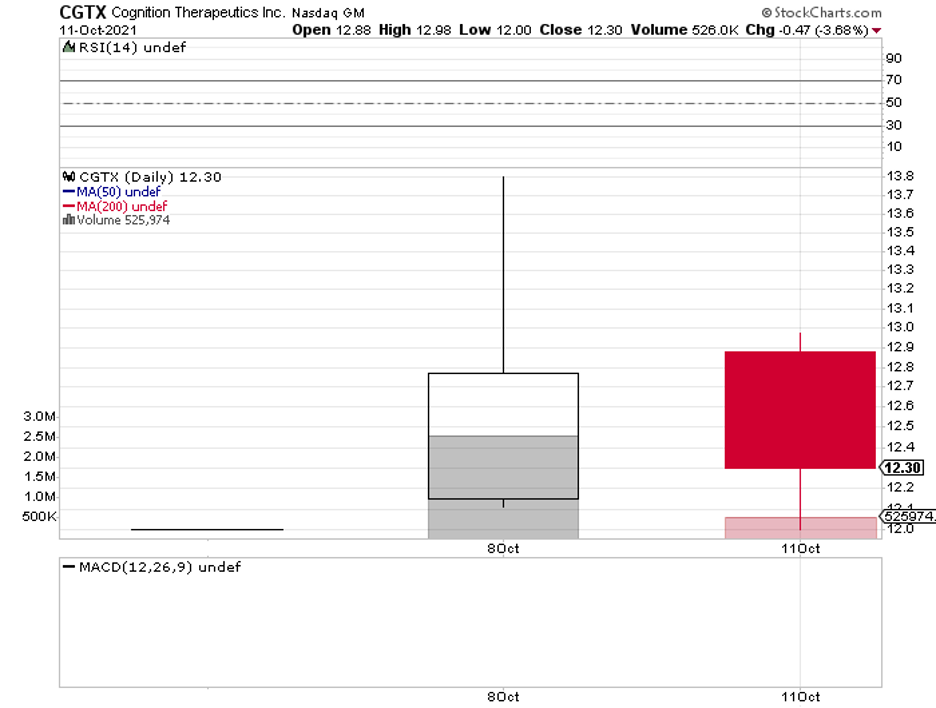

The first is Cognition Therapeutics (CGTX), a company working on treatments for Alzheimer’s disease and macular degeneration.

Its most promising candidate is an Alzheimer’s treatment called CT1812, which is currently under Phase 2 trials. Looking at the timeline, CGTX expects to release topline data by 2023.

With the expected growth of the aging population, focusing on treating various forms of Alzheimer’s is a promising direction for Cognition Therapeutics.

In fact, the global market for this neurodegenerative disease is projected to grow from $2.9 billion in 2018 to a whopping $10.5 billion by 2025.

So far, the major competitors of Cognition Therapeutics in this area include Biogen (BIIB), Eli Lilly (LLY), AbbVie (ABBV), Novartis (NVS), and Takeda (TAK).

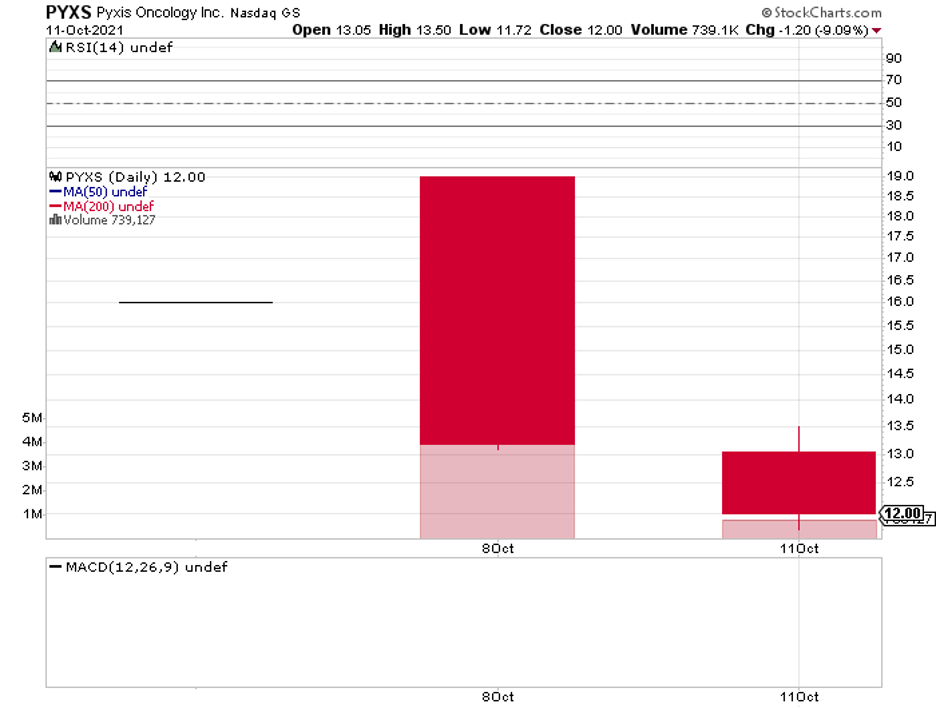

The second promising biotech company is Pyxis Oncology (PYXS), which is a spinoff from Pfizer (PFE).

Pyxis is focused on developing next-generation treatments targeting difficult-to-treat types of cancer.

Basically, the company’s goal is to create therapies that can directly kill tumor cells. It also wants to get rid of the underlying problems that lead to the uncontrollable spread of tumors and the weakening of the immune system.

To do this, Pyxis has come up with novel antibody drug conjugate (ACT) candidates and other monoclonal antibody (mAb) pipelines.

Its lead candidate is called ADC PYX-201, a potential treatment for non-small cell lung cancer and breast cancer.

The goal of ADC PYX-201 is to target actively multiplying tumors while boosting the immune response of the patient’s body. Pyxis plans to submit it as a non-small cell lung cancer treatment candidate by mid-2022.

If approved, then ADC PYX-201 will be under patent protection until 2037.

This holds great potential for Pyxis’ cashflow, as the market for non-small cell lung cancer worldwide is anticipated to rise from $6.2 billion in 2016 to over $12 billion by 2025.

With this potential of ADC treatments, Pyxis can expect competition from the likes of AstraZeneca (AZN), Gilead Sciences (GILD), GlaxoSmithKline (GSK), and ImmunoGen (IMGN).

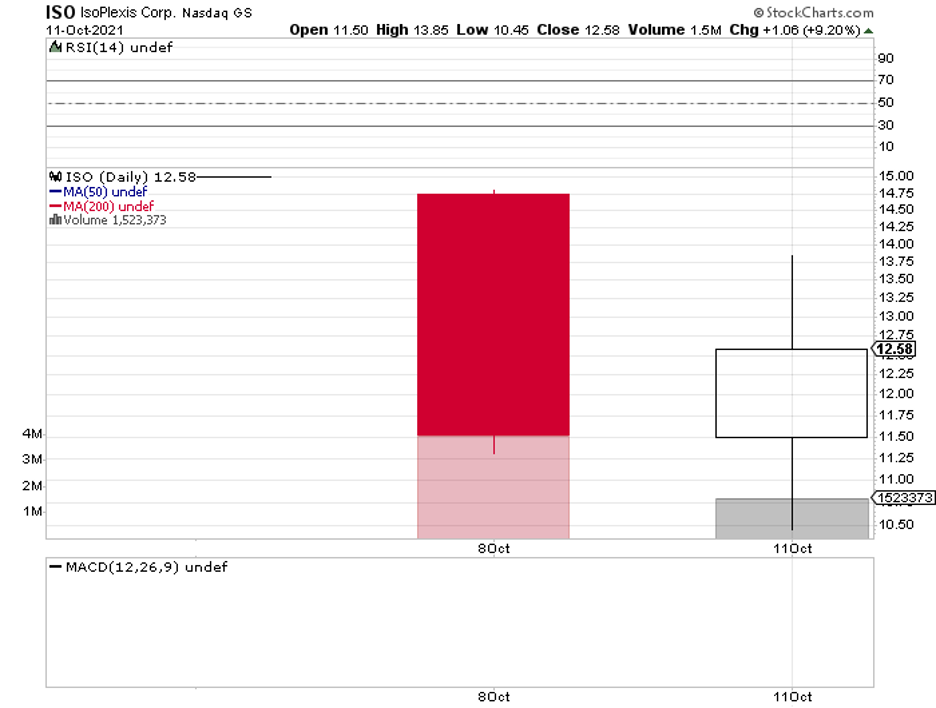

The last name on today’s list is IsoPlexis Corporation (ISO).

This company is the first to focus on dynamic proteomics and single-cell biology in an effort to develop “walk-away automation” products that aid in shortening the therapeutic development timelines by acquiring “multiplexed proteomics with very low sample volumes that reflect in vivo biology to clarify lead candidates.”

In layman’s terms, IsoPlexis is working on a technology that aims to identify every protein in the body to speed up the development of new therapies for rare diseases.

This is a lucrative business, with IsoPlexis targeting at least $34 billion in the total addressable market.

Considering that IsoPlexis is a pioneer in this field, it is possible for it to gain the lion’s share of the segment and position itself as an undisputed leader for years.

More importantly, IsoPlexis can use its patented technology, “Proteomic Barcoded,” to expand the use cases to cover other lucrative markets.

For example, IsoPlexis can apply its technology to cancer immunology and targeted oncology by predicting the progression of cancer cells in the body.

Adding cell therapies to the company’s pipeline is also a very realistic possibility since its technology can be utilized to create CAR-T cell therapies as well.

In fact, IsoPlexis’ approach is already being used in developing treatments for leukemia and melanoma.

Another profitable avenue for IsoPlexis’ technology is the vaccines sector.

Since the development of vaccines requires profiling the responses of the respiratory and immune systems, the company’s data would accelerate the entire process.

So far, the major rivals of IsoPlexis in this space include Thermo Fisher Scientific (TMO) and Bio Rad Laboratories (BIO).

While all these biotech companies offer promising products and technologies, they’re all still in the early stages of development.

This makes them high-risk investments and are likely suitable for those who are willing to invest in the long term.

For those who want to see movement faster and sooner, it might be best to watch these stocks from the sidelines.

Mad Hedge Biotech & Healthcare Letter

September 2, 2021

Fiat Lux

FEATURED TRADE:

(BIOTECHS ARE OUT FOR BLOOD)

(BIIB), (LLY), (BAYRY), (NVS), (SNY)

Tracing its origins in Greek mythology to the infamous Dracula tales, stories centered on the restorative powers of blood have captivated our imagination for millennia.

In the past two decades, however, the concept of hailing blood as the elixir of youth has come a long way from ancient folklore.

These days, this idea has reached the medical world with highly renowned researchers throwing their names behind the study of the regenerative ability of young blood.

From mere storybook fantasies, this concept has become one of the serious contenders alongside the likes of Biogen (BIIB), Eli Lilly (LLY), and Bayer (BAYRY) in the fight against Alzheimer’s, Parkinson’s, and even stroke.

Here’s a quick explanation for this change.

At its core, one of the major causes of aging is when our systems go on overdrive in the performance of usual bodily functions.

That is, the body shifts away from the “regular” state or homeostasis and instead is forced to constantly be in alert mode.

This causes us to end up with a hyper pro-inflammatory immune system, which then malfunctions and results in damaged tissues and organs over time, exposing the body to diseases and conditions like neurodegeneration and heart attacks.

The solution is quite simple. Let’s just flush out those pro-inflammatory aging compounds—aka the overworked system. That way, we can delay (or probably even prevent) the aging process.

This can be done through a process called “parabiosis,” which has only been experimented on mice.

Basically, this works by connecting the circulatory system of an older mouse to a younger one. Then, the older mouse starts to get younger as well.

In 2005, researchers published a paper that studied two identical mice (one old and one young) to demonstrate the veracity of the concept.

To test the idea, they connected the circulatory systems of both mice. This means that the two lived off the same general blood pool, which comprises young and old blood.

In just 5 weeks, the older mouse’s stem cells started to divide again. Its muscles and liver cells also began to repair themselves.

Essentially, from a cellular viewpoint, the older mouse transformed into a younger version of itself.

Given the medical, moral, and ethical issues that come with the traditional “parabiosis,” biotechnology companies have searched for more efficient and effective ways to achieve these age-defying results other than the vampiric blood swap.

But, how can these results be replicated?

This is where “Total Plasma Exchange” (TPE) comes in.

TPE is done using an apheresis machine. The patient’s blood runs through this device, which then removes and discards filtered plasma via the reinfusion of red blood cells as well as other replacement fluids, including plasma or albumin.

Without going through the technical nitty-gritty, TPE involves the extraction of a large volume of blood from a patient, taking it apart into its individual components, then returning it to the same patient’s body sans the filtered-out components courtesy of the machine.

Recently, clinical trials on humans showed that TPE managed to slow disease progression among patients suffering from age-related disorders, like Alzheimer’s, by more than 66%.

While there’s no uniform cost for this treatment, the average estimate for every TPE session is roughly $101,140. Just how much this would cost in the long run heavily depends on the person’s condition and desired outcome.

At this point, the research is still in its early stages.

However, this hasn’t prevented rogue biohackers from testing out their own theories—and come up with surprisingly workable results.

In 2020, two 50-year-old self-confessed “biohackers” based in Russia hooked themselves up to blood collection machines. They then proceeded to replace practically half of the plasma coursing through their own veins with salty water.

After 3 days, their blood tests showed an improvement in their general well-being, as seen in their hormones, fats, and other indicators.

In particular, their immunity, cholesterol metabolism, and even liver function showed better performance.

So far, this concept has been explored by other researchers who are now replacing plasma with saline and adding other components like albumin.

These experiments are still being conducted on animals, but they have to date proven to be promising in terms of reducing inflammation in the brain and improving cognitive functions.

Primarily, the Russian biohackers and these experts are diluting the anti-aging factors to slow down or even eventually prevent aging.

Among the probable applications of plasma in the anti-aging movement, the dilution process seems to be the easiest and most convenient track to pursue—so much so that a company, called IMYu, was founded by top UC Berkley researchers to develop this strategy further.

Thus far, only a handful of biotechs have focused on this concept.

Some of the frontrunners are Massachusetts-based Elevian, which was founded in 2017, and Alkahest, which was acquired by Spanish pharmaceutical giant Grifols (GRF) for $146 million.

Meanwhile, a company called Nugenics Research has actually patented the name “Elixir” for its plasma-derived product under development.

There are also clinics like the Atlantis Anti-Aging Institute based in Florida and companies such as Ambrosia, which market plasma gathered from donors ages 16 to 25 and sell them for several thousand dollars for every transfusion.

Thus far, big pharma has yet to get its hands on this technology.

Only a handful of major companies, including Novartis (NVS) and Sanofi (SNY), have expressed interest in exploring these possibilities.

However, these innovations are only a glimpse of the incredible momentum driving the anti-aging industry these days.

It’s only a matter of time until we achieve a spectacularly extended lifespan with an impressively high quality of health and wellbeing.