At this point, it is possible that the president may lose the November election.

He is 14 points behind Democratic candidate Joe Biden in the polls. The odds at the London betting polls have him losing by a similar amount. My old employer The Economist magazine in London gives him a 10% chance of winning using a mix of economic and polling data.

And this assumes the election is held today. The fact is that the president is digging himself into a deeper hole every day, taking the wrong side of every issue confronting the country today. He seems to be refighting the Civil War….and taking the Confederate side when even the State of Mississippi is taking its symbol off its flag.

So, what will the post-Trump world look like? Will taxes go through the roof? Will the market crash? Is it time to go 100% cash, change our names, and move to a country with no US extradition treaty?

I don’t think so. In fact, with stocks soaring to meteoric new highs every day, the market expects that a Biden administration will be great news for stocks, perhaps the best ever.

Taxes will certainly go up. Favorable tax treatment of the energy, real estate, and private equity funds will get axed. Carried interest will finally become history. Marginal tax rate on net income over $1 billion could get hiked to the Roosevelt levels of 80-90%.

Biden has already announced an increase in the corporate tax rate from 21% to 28%. That will cut earnings for the S&P 500 by $9 a share. But the stock market is not the economy, with S&P earnings only accounting for 10% of US GDP.

And the $9 companies lose in taxes they will make back and more from new government spending, which isn’t slowing down any time soon. Some 14,000 American bridges need to be rebuilt. The Interstate Highway System is a shambles. High-speed broadband needs to go rural. The electrification of the US needs to accelerate to accommodate the millions of electric cars headed our way.

I believe that eventually, 51 million Americans will lose their jobs as a result of the pandemic. Perhaps a third of those are never coming back because the future has been so accelerated. That will leave the broader U-6 Unemployment rate stuck in double digits for years, maybe for decades.

So, we’re going to need some kind of Roosevelt style programs like the Works Progress Administration (WPA) and the Civilian Conservation Corps (CCC) who built much of the monolithic infrastructure that we all enjoy today.

At least 300,000 educated workers could immediately be put to work in contact tracing. Millions more could be employed in national infrastructure programs. One thing is certain. A new administration won’t stop massive government spending, it will simply redirect it.

And let's face it. A Biden win would bring a big expansion of Obamacare. With the best healthcare technology in the world, private industry has done the world’s worst job controlling the pandemic.

Countries with well-run national healthcare systems like Australia, New Zealand, Japan, and Singapore have almost wiped out the disease. This is why I am avoiding the healthcare sector for the foreseeable future.

Who are the big winners of all this? Big tech (FB), (AAPL), (MSFT), (AMZN), medium tech (ADBE), fintech (SQ), (PYPL), the cloud (CRM), and biotech (SGEN), (REGN), and (ILMN).

Cybersecurity will always be in demand (FEYE), (PANW). The global chip shortage will continue to worsen (AMD), (MU), (NVDA).

And Tesla (TSLA)? What can I say? It is already up nearly 100-fold from my initial $16.50 recommendation in 2010, and I’ve bought three Tesla’s (two S’s and an X).

Followers of the Mad Hedge Trade Alert service know that I am already long these names up the wazoo, and is why I am up 26% in 2020. It’s simply a matter of all pre-pandemic trends hyper-accelerating, which we were already tapped into.

If you have to add a purely domestic sector, a gigantic Millennial tailwind will keep homebuilders bubbling for years like (LEN), (PHM), and (KBH).

And while you won’t find me as a player here, retail will recover. The sector has not prospered during the current administration, thanks to a trade war with China and the pandemic.

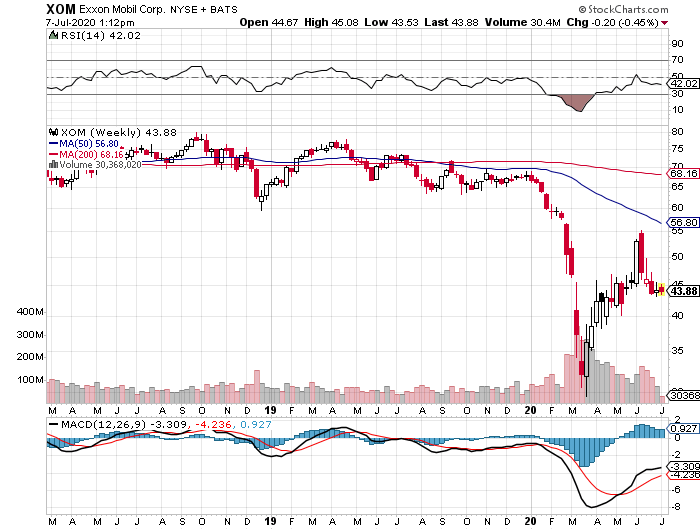

And the losers? There is a classification of “Trump” stocks you don’t want to be anywhere near. Energy will do terribly (XOM), (CVX), (XOM), with Texas tea possibly revisiting negative numbers. If you take away the tax breaks, energy hasn’t really made money in decades.

Defense stocks (RTN), (NOC), (LMT) will take a big hit from budget cutbacks and fewer wars. Coal (KOL) will finally get shut down for good, probably sold to China in bankruptcy proceedings. Industrials will continue to lag (X), (GE), with no more free handouts from the government and no technology advantage.

So if Biden wins, you don’t need to slit your wrists, hang yourself from the showerhead, or cease investing completely. Just take your stock market winnings and go out and get drunk instead.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-07-08 09:02:282020-07-08 08:56:44Trading the Blue Wave Stock Market

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader January 8Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: If the market is doing so well, why is the Fed flooding the market with liquidity?

A: It’s election year, so their primary focus is to get the president reelected and do everything they can to make sure that happens. If we continue at the current rate, the Fed will have zero ability to get us out of the next recession which will make it much deeper than it would be otherwise. Doing this level of borrowing and keeping interest rates near zero with the stock market going up 30% a year is insane, and we will be severely punished for it in the future.

Q: With the Volatility Index (VIX) near a 12-month low and the Mad Hedge Market Timing Index near an all-time high, is this a good time to put on LEAPs for the (VXX)?

A: Yes, in fact, a (VXX) LEAP (Long Term Equity Participation Security, or one-year-plus option spread), is the only LEAP I would put on right now. I get asked about LEAPs every day because returns on them are so huge, but I am holding back on a trade alert on a (VXX) leap because it seems like in January they really want to run this market high and run volatility down low. On the next move to a (VIX) in the $11 handle, you want to put out a one-year LEAP with a $16 strike. And that is essentially a guarantee that you will make money sometime in the coming year on a big down move in the stock market. (VXX) LEAPs are coming, just not yet.

Q: Do you think Iran is done with their attacks against the US or will there be more?

A: The belief there will be no more attacks is to call the end of a 40-year trend. There will be more attacks, and those are going to be your long side entry points. Every geopolitical crisis for the last 10 years has been a great entry point on the long side and the next one will be no different. Just hope you are not one of the victims.

Q: What would a war with Iran mean for the US economy and should I buy defense stocks?

A: You can take the Iraq war, which cost us about $4 trillion, and multiply that by three times to $12 trillion because Iran’s economy is three times the size of Iraq and has a much more sophisticated military. The Iranians are really in a good position because they know the US has no appetite for another Iraq, Afghanistan, or Vietnam. They just want us out of their neighborhood. As far as defense stocks, those really move on very long-term investments and production for government contracts. When you get an attack like this, you get a one-day pop of 5% and then they usually give it all back. So, I wouldn't be chasing defense stocks like Lockheed Martin (LMT), Northrop Grumman (NOC), and Raytheon (RTN) at these high levels—it’s a very high-risk trade.

Q: Will Boeing (BA) take heat from the Ukrainian crash in Tehran?

A: Yes. It’s down about $5, and you might even consider running the numbers on a February call spread. This may be the last chance to get into Boeing at those low levels. The 737 MAX will fly this year, their most important product.

Q: What’s your opinion on Thai Baht?

A: This really is the home here for opinion on all asset classes, large and small. The Thai Baht will rise. It’s a weak dollar play. Money is pouring into all the emerging currencies because of the massive overborrowing that’s going on in the U.S. Countries that overborrow and print money like crazy always debase their currencies over the long term. That makes emerging markets (EEM) a great buy, which are trading at half the valuation levels of US ones.

Q: U.S. hog farmers missed the opportunity of a lifetime last year because of African Swine Flu. Any thoughts on the price of pork and commodities for 2020?

A: They should do better now that we’re at least getting relief from an escalation of the trade war. However, I gave up covering agriculture because the American farmer is just too efficient; every year they just produce more and more crops with fewer and fewer inputs—it’s a loser’s game. They occasionally get bad weather and get a big price spike, but that Is totally unpredictable. I'm staying away from ag stocks. In terms of buying soybeans or Apple, or Google, or Amazon, I’ll take the tech stocks any day over ag’s. Plus, the insiders have a big advantage in ag’s.

Q: What is the ticker symbol for the Silver ETFs?

A: The Silver metal ETF is (SLV), Silver miners is (SIL), and the Silver Royalty Trust, Wheaton Precious Metals, is (WPM).

Q: Why has volatility been so minimal even with massive geopolitical risk going up?

A: Liquidity trumps all. This month, the fed is pumping a record $160 billion into the financial system, and all that money is going into stocks, making them go up and making volatility go down. Until that changes, this trend will continue.

Q: Apple just passed $300, is the next stop $400?

A: Yes, and we could get that this year in the run up to 5G in September. By the way, my average cost on my Apple shares split adjusted is 50 cents. I bought it in the late 1990s when the company was weeks away from bankruptcy.

Q: Any thoughts on Tesla (TSLA)?

A: Yes, go out and buy the car, not the stock. Wait for some kind of pullback. We have just had a fantastic run of good news kicking the stock from $180 up to $490. I think we will make it up to $550 on this run. But you don’t want to get involved unless you’re a day trader because now the risk is very high. The next big move for Tesla is going to be the announcement of a production factory in Berlin, where they will try to take on Mercedes, BMW, VW, and Audi on their home turf. Then, they will own Europe.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/John-Thomas-Hiking-e1537885559217.png465366Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-01-10 10:02:222020-05-11 14:15:58January 8 Biweekly Strategy Webinar Q&A

Yes, the same 3D printing that was once considered a raging but hopeless fad.

A lot has changed since then.

Early adopters were largely cut down at the knees as they tried to traverse the rocky terrain from a niche market to going full out mainstream.

Production complications and the lack of specialists in the industry meant that problems were rampant and nurturing an industry from scratch is harder than you think.

Believe me, I’ve been there and done that.

It is time to stand up and take notice of 3D printing, this time it is here to stay.

Certain tech companies love this technology like e-commerce company Etsy (ETSY) who focuses on personalized handcrafts.

The cost of production doesn’t change whether you’re producing one item or a million because of the economies of scale.

The previous 3D printing bonanza was a frenzy and this corner of tech became known for the use of buzzwords representing the potential to reinvent the world.

With lofty expectations, there was a natural disappointment when outsiders understood growing pains were part of the critical evolution instead of a direct route to profits.

The initial goal was to democratize production which sounds eerily similar to bitcoins mantra of democratizing money.

The way to do this was to make it simple to produce whatever one wishes.

That would assume that the general public could pick up professional production 3D printing skills on arrival.

That was wishful thinking.

The truth was that applying 3D printers was tedious.

Issues cropped up like faulty first-generation hardware or software -problems that overwhelmed newbies.

Then if everything was going smoothly on that front, there was the larger issue of realizing it’s just a lot harder to design specific things than initially thought without a deep working knowledge of computer-aided software (CAD) design.

Most people know how to throw a football, but that doesn’t mean that most people can be Super Bowl quarterback Tom Brady.

The high-quality 3D printing designs were reserved for authentic professionals that could put together complicated designs.

The move to compiling a comprehensive library will help spur on the 3D printing revolution while upping the foundational skill base.

Then there is the fact that 3D printing technology is heaps better now than it once was, and the printing technology has come down in price making it more affordable for the masses.

These trends will propel broad-based adoption and as the printing process standardizes, more products can rely on this technology from scratch.

The holy grail of 3D printing would be 3D printing on demand, but imagine this on-demand 3D printing would function to personalize a physical product on the spot.

Think of a hungry customer walking into a restaurant and not even looking at a menu because one sentence would be enough to trigger specific models in the database that could conjure up the design for the meal.

This would involve integrating artificial intelligence into 3D printing and the production process would quicken to minutes, even seconds.

At some point, crafting the perfect meal or designing a personalized Tuscan villa could take minutes.

The 3D printing industry is reaching an inflection point where the advancement of the technology, expertise, and an updated production process are percolating together at the perfect time.

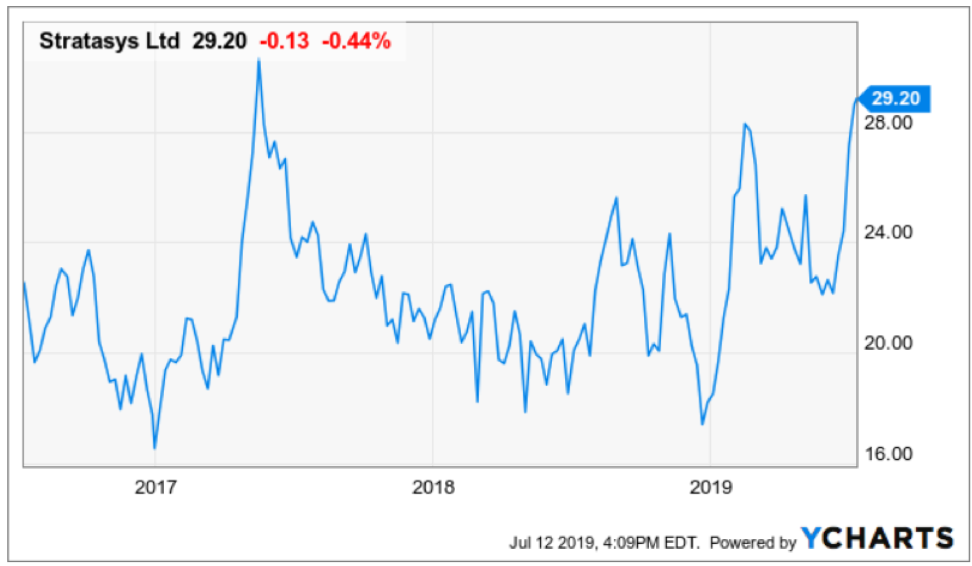

The company at the forefront of this phenomenon is Stratasys (SSYS).

Stratasys produces in-office prototypes and direct digital manufacturing systems for automotive, aerospace, industrial, recreational, electronic, medical and consumer products.

And when I talk about real pros who have the intellectual property to whip out a complex CAD-based 3D design, I am specifically talking about Stratasys who have been in this business since the industry was in its infancy.

And if you add in the integration of cloud software, 3D printing would dovetail nicely with it.

All the elements are in perfect in place to fuel this industry into the mainstream.

Take for example airplanes made by Boeing (BA) and Airbus - 3D printer-designed parts comprise only 0.1% of the actual plane now.

It is estimated that 3D printed design parts could potentially consist up to 25% of the overall plane.

These massive airline manufacturers like Boeing (BA) have profit margins of around 15% to 20%, and carving out more 3D printer-designed parts to integrate into the main design will boost profit margins close to 60%.

The development of the 3D printing process into aerospace technology is happening fast with Boeing inking a multi-year collaboration agreement with Swiss technology and engineering group Oerlikon to develop standard processes and materials for metal 3D printing.

Any combat pilot knows who Oerlikon is because they are famed for building ultra-highspeed machines to shoot down, you guessed it, airplanes and missiles.

They will collaborate to use the data resulting from their agreement to support the creation of a standard titanium 3D printing processes.

GE’s Aviation’s GEnx-2B aircraft engine for the Boeing 747-8 is applying a 3D printed bracket approved by the Federal Aviation Administration (FAA) for the engine, replacing a traditionally manufactured power door opening system (PDOS) bracket.

With the positive revelations that the (FAA) is supporting the adoption of 3D printing-based designs, GE has already started mass production of the 3D printed brackets at its Auburn, Alabama facility.

Defense companies are also dipping their toe into the water with aerospace company Lockheed Martin (LMT), the world’s largest defense contractor, winning a $5.8 million contract with the Office of Naval Research to help further develop 3D printing for the aerospace industry.

They will partner up to investigate the use of artificial intelligence in training robots to independently oversee the 3D printing of complex aerospace components.

3D printed designs have the potential to crash the cost of making big-ticket items from cars to nuclear plants while substantially shortening the manufacturing process.

As it stands, Stratasys is the industry leader in this field and if you believe in this long term then this stock would be for you.

It’s nonetheless still a speculative punt but a compelling pocket of the tech industry.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-10-16 07:02:582020-05-11 13:26:28Is 3D Printing a Waste of Space?

Yes, the same 3D printing that was once considered a raging but hopeless fad.

A lot has changed since then.

Early adopters were largely cut down at the knees as they tried to traverse the rocky terrain from a niche market to going full out mainstream.

The teething pains echo bitcoin which was the fad of 2017, on the contrary, this technology it is built on is rock solid, yet the path to sustainability is littered with corpses.

Production complications and the lack of specialists in the industry meant that problems were rampant and nurturing an industry from scratch is harder than you think.

It is time to stand up and take notice of 3D printing, this time it is here to stay.

Certain tech companies love this technology.

Etsy (ETSY) e-commerce participants gravitate towards 3D printing because it gets firms from paper to the real world in a fraction of the time.

The cost of production doesn’t change whether you’re producing one item or a million because of the economies of scale.

The previous 3D printing bonanza was a frenzy and this corner of tech became known for the use of buzzwords representing the potential to reinvent the world.

With lofty expectations, there was a natural disappointment when outsiders understood growing pains were part of the critical evolution instead of a direct route to profits.

The initial goal was to democratize production which sounds eerily similar to bitcoins mantra of democratizing money.

The way to do this was to make it simple to produce whatever one wishes.

That would assume that the general public could pick up professional production 3D printing skills on arrival.

That was wishful thinking.

The truth was that applying 3D printers was time-draining and aggravating.

Issues cropped up like faulty first-generation hardware or software -problems that overwhelmed newbies.

Then if everything was going smoothly on that front, there was the larger issue of realizing it’s just a lot harder to design specific things than initially thought without a deep working knowledge of computer-aided software (CAD) design.

Most people know how to throw a football, but that doesn’t mean that most people can wake up one day in their pajamas and convince themselves they will be the next starting quarterback to lead an NFL team to the Super Bowl.

The high-quality 3D printing designs were reserved for authentic professionals that could put together complicated designs.

The move to compiling a comprehensive library will help spur on the 3D printing revolution while upping the foundational skill base.

Then there is the fact that 3D printing technology is a lot better now than it once was, and the printing technology has come down in price making it more affordable for the masses.

These trends will propel broad-based adoption and as the printing process standardizes, more products can rely on this technology from scratch.

The holy grail of 3D printing would be 3D printing on demand like Netflix (NFLX), but imagine this on-demand 3D printing would function to personalize a physical product on the spot.

Think of a hungry customer walking into a restaurant and not even looking at a menu because one sentence would be enough to trigger specific models in the database that could conjure up the design for the meal.

This would involve integrating artificial intelligence into 3D printing and the production process would quicken to minutes, even seconds.

At some point, crafting the perfect meal or designing a personalized Tuscan villa could take minutes.

The 3D printing industry is reaching an inflection point where the advancement of the technology, expertise, and an updated production process are brewing together at the perfect time.

The company at the forefront of this phenomenon is Stratasys (SSYS).

Stratasys produces in-office prototypes and direct digital manufacturing systems for automotive, aerospace, industrial, recreational, electronic, medical and consumer products.

And when I talk about real pros who have the intellectual property to whip out a complex CAD-based 3D design, I am specifically talking about Stratasys who have been in this business since the industry was in infancy.

And if you add in the integration of cloud software, 3D printing would dovetail nicely with it.

All the elements are in place to fuel this industry into the mainstream.

Take for example airplanes made by Boeing (BA) and Airbus, 3D printer-designed parts comprise only 0.1% of the actual plane now.

It is estimated that 3D printed design parts could consist up to 20% of the overall plane.

These massive airline manufacturers like Boeing (BA) have profit margins of around 15% to 20%, and carving out more 3D printer-designed parts to integrate into the main design will boost profit margins to up to 50%.

The development of the 3D printing process into aerospace technology is happening fast with Boeing inking a five-year collaboration agreement with Swiss technology and engineering group Oerlikon to develop standard processes and materials for metal 3D printing.

Any combat pilot knows who Oerlikon is because they are famed for building ultra-highspeed machines to shoot down, you guessed it, airplanes and missiles.

They will collaborate to use the data resulting from their agreement to support the creation of a standard titanium 3D printing processes.

Only last November, GE announced that GE’s Aviation’s GEnx-2B aircraft engine for the Boeing 747-8 will apply a 3D printed bracket approved by the Federal Aviation Administration (FAA) for the engine, replacing a traditionally manufactured power door opening system (PDOS) bracket.

With the positive revelations that the (FAA) is supporting the adoption of 3D printing-based designs, GE is preparing to begin imminent mass production of the 3D printed brackets at its Auburn, Alabama facility.

Eric Gatlin, general manager of GE Aviation’s additive integrated product team gushed that “It’s the first project we took from design to production in less than ten months.”

Defense companies are also dipping their toe into the water with aerospace company Lockheed Martin (LMT), the world’s largest defense contractor, winning a $5.8 million contract with the Office of Naval Research to help further develop 3D printing for the aerospace industry.

They will partner up to investigate the use of artificial intelligence in training robots to independently oversee the 3D printing of complex aerospace components.

3D printed designs have the potential to crash the cost of making big-ticket items from cars to nuclear plants while substantially shortening the manufacturing process.

Further emphasis on cornering the North America aerospace market could cement this stock as a no-brainer buy of 2019 as the (FAA) embraces more of the technology opening up the addressable market for the active participants.

As it stands, Stratasys is the industry leader in this field, and placing best of breed tech companies into your portfolio will put you in better position to weather the squalls of the capricious tech sector.

The company is still relatively unknown even though it has been around for ages.

Stratasys is a company to put on your radar and remember this space as the 3D printing market blossoms.

It’s nonetheless still a speculative punt but a compelling part of the tech industry.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/3d-printer.png612960Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-07-26 01:02:492019-08-27 14:48:51Why 3D Printing Will Boost the Airplane Industry

There are many ways to describe the trade war the U.S. administration finds itself in.

Many experts have chimed in too categorizing it as a fight for technological supremacy.

There are many different ways to skin a cat.

I’ll tell you what is really going on.

Above all else, this logjam has more to do with a battle for resources, and more specifically, rare earth elements that power the devices, cars, and gadgets that many westerners have become accustomed to.

Let’s make no bones about it, Beijing has cornered the rare earth’s market spanning from assets in the Congo and the cobalt that is produced there to supply on their own turf forcing the U.S. to be reliant on China for about 85% of its rare earth supply.

In other words, the rare earth industry in China is a large industry that is important to Chinese internal economics.

Rare earths are a group of elements on the periodic table with similar properties.

The elements are also critical to national governments because they are used in the defense industry for top-secret weaponry.

Permanent magnets can be used for several applications including serving as essential components of weapon systems and high-performance aircraft such as drones.

China has touted their own state-owned companies to reach deep into this market and make it their own.

The results are visible to the entire world and China gaining a stranglehold on these valuable inputs will have lasting consequences.

Rare earth metals are made up of 17 elements — lanthanum, cerium, praseodymium, neodymium, promethium, samarium, europium, gadolinium, terbium, dysprosium, holmium, erbium, thulium, ytterbium, lutetium, scandium, and yttrium.

U.S. companies will need to start developing new supply channels in other markets and Australia could allow U.S. companies' lifelines in securing the orders they need to function as a company.

Military companies important to national security devour these types of precious metals and Raytheon Co (RTN), Lockheed Martin Corp (LMT) and BAE Systems (BAESY) all produce sophisticated missiles with these elements powering their guidance systems, and sensors.

These traded companies’ shares could be in for short-term turbulence if China decides to pull the rug out from underneath banning Chinese companies doing business with American companies, or by slapping on tariffs to respond to the tariffs on Chinese imports.

California's Mountain Pass mine is the sole US rare earth facility with a caveat.

The owner of the mine ships over 50,000 tons of rare earth concentrate for processing in China, meaning that it will be harder than first thought to strip China out of the process.

China and America are in the first stages of a massive decoupling.

Not only smartphone operating systems will be affected with Huawei announcing it will roll out its own in-house operating system after Google announced that they will pull its apps and use of the Android system off of Huawei’s phone, but almost anything of significant value from an Ivy league computer engineering degree to electric cars will be retrenched on each side.

This is terrible news for Tesla (TSLA), and they could be hit next by the Chinese communist party if they deem electric cars integral to national security because of the data and sensors that deliver precious information back to Silicon Valley.

Tesla is in the midst of building a Gigafactory in Shanghai and their growth strategy is solely focused on China.

China standing up to the U.S. is a blunt force way of saying that nobody will dictate to the Chinese their future prospects except themselves.

They feel after 35 years of economic super growth, they should be granted with the options of choosing their destiny.

Huawei will feel the repercussions of these detrimental policies with their European business a big question going forward.

Germany was always a large bullseye for the Chinese government and scooping up robotic centerpiece Kuka, was a smash and grab in broad daylight.

The sleeping giant of Germany has woken up and is on the offensive after allowing the Chinese unfettered access for a generation.

Risks are high in Germany and they could be the first industrial power to be gutted and left behind the woodshed by China Inc and the CCP.

The U.S. faces a conundrum in that the method in which aided China’s rise of forced technology transfers and IP theft can only be stopped if actively removed, meaning we are headed for a game of chicken with the other side hoping the other side blinks first.

The market fallout will be deep and wide-ranging with the most movement in technology companies that are leveraged to China meaning chip companies.

But then there are the tech companies who have deeply embedded interests in China such as Apple (AAPL) whose supply chain is in the eye of the storm with Foxconn.

The worst possible case is China banning the sales of precious earth metals to the U.S. forcing the U.S. to buy from a 3rd party country which in turn would increase costs of American products.

This is what I would categorize as a hard landing and absolute decoupling.

The common denominator of this trade war is higher costs for the American consumer and mass layoffs in China – this is my base case.

However, I would argue that a rare earth's ban would not be as bad as initially thought because many consumers are tapped out with phones, tablets, and computers.

The elongated refresh cycle will not mean consumers will go without access to the internet and its services.

In terms of the stock market, this puts a wet towel on the positive momentum of early spring when the Nasdaq roared higher.

The Nasdaq could be stuck under 8,000 for the summer unless a rapprochement takes place which I would put at 30% for a structural détente and 65% for a kick the can down the road détente.

The ironic unintended consequence is the safe haven trade of buying treasuries has come back in vogue and could be a huge boon for the domestic real estate market.

This extends the bull market in properties at least another six months with lower rates allowing fresh buyers to take advantage of lower financing opportunities amid a bump in inventory.

The bull market absolutely needs the real estate market on-sides to perpetuate because of the fragile nature of this part of the late economic cycle.

I also believe that U.S. President Donald Trump will become even more brazen as stronger economic data stateside suggests he could pile on even more pressure on the Chinese communist party to coerce them into a big win that will aid him in his reelection efforts.

Let’s not forget that much of this has to do with the 2020 road back to the White House.

As it stands, corporate America has finally understood the message of moving their supply chain out of China which means mass layoffs for many Chinese particularly in the southern region around Guangzhou.

This is not a marketing charade, this trade war has teeth.

China’s Central Bank will be forced into dovish policy to help state-owned companies who many are akin to zombie companies and another relic of communism that has yet to be uprooted.

All this means debt, debt, and more debt piling up on the mainland and on American shores.

If you thought this was the time of austerity, then you are truly wrong.

The end game could be a Chinese yuan that drops like a heavy stone through the psychological threshold of $7 and on its way down to $7.50.

If this comes to pass, expect a 10% correction and a demonstrably strong U.S. dollar, Japanese yen, Swiss Franc, and a generational entry points into the equity market.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-05-28 03:02:092019-07-11 13:02:17China's Rare Earth Weapon

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.