Mad Hedge Technology Letter

December 17, 2021

Fiat Lux

Featured Trade:

(LOOKING FORWARD TO TECH IN 2022)

(FB), (NVDA), (AAPL), (MSFT), (AR), (VR)

Mad Hedge Technology Letter

December 17, 2021

Fiat Lux

Featured Trade:

(LOOKING FORWARD TO TECH IN 2022)

(FB), (NVDA), (AAPL), (MSFT), (AR), (VR)

Another pandemic year is on the verge of being in the books and we need to look yonder to 2022 and what it can offer.

Now that billions are being poured into the project, it’s not weird to say that advanced technology and the arteries and ventricles surrounding it, will all lead to developing this new world called the Metaverse.

The metaverse is a hypothesized iteration of the Internet, supporting persistent online 3-D virtual environments through conventional personal computing, as well as virtual and augmented reality headsets.

And I am not saying this is a new thing just to be cool, analyzing thousands of earnings reports, it’s clear that companies are deploying human capital around gaining a slice of this future Metaverse.

This idea is so prominent that Facebook (FB) changed its name to Meta to signal its commitment to this new technology.

Next year will be the year that we get closer to the real deal — a fully functioning Metaverse even if it might just be a beta version.

And it’s not just Facebook, Apple (AAPL), and Microsoft (MSFT) and the rest are in it too with Nvidia’s (NVDA) chips serving as a building block of the Metaverse.

Naturally, related technologies will be of great importance, and I can easily see a greater surge in augmented reality (AR) interest.

People should also keep a close eye on the introduction of Meta's internet-of-VR.

The idea of the metaverse and an advanced VR world must be seen through the prism of the pandemic which has forced us to become digital first even if many of us aren’t native digital users.

Many of us have had to learn on the go, for instance, download that Zoom video conferencing software or upgrade our home office.

This torrent of internet usage has its pitfalls like explosive growth in cyberattacks, making cybersecurity more important than ever.

Cybersecurity will no longer be seen as an “added extra” by organizations and will be built into the DNA of any and every IT system, from supply chains to infrastructure and devices.

Our reliance on internet leads nicely into 2022 becoming the year when 5G became mainstream.

We are edging towards that point where we need that extra speed to harness our work devices and to wield them in the most efficient and optimal way.

Many of you have had to upgrade data packages, build robust infrastructure into your home office and I don’t mean just buying a better office chair.

This could see the rise of “digital cities” along with new smart mobility services such as autonomous vehicles and 5G connected bicycles. We could also see a rise in private 5G networks for businesses in manufacturing and logistic sectors.

A new era of private connection for businesses will be launched, enabling greater data-driven insights and real-time business decisions.

2022 will see businesses continue to neglect the traditional office and many companies will be at best — hybrid.

We might start seeing companies go bankrupt because they can’t convince any workers to show up in physical form.

It’s already happening to the workers I talk to where limited remote working opportunities when interviewing for new jobs is a deal-breaker.

Next year is also when we finally see artificial intelligence on steroids.

The explosion of AI-powered gadgets, apps, websites, and tools is here for 2022.

It'll become harder to differentiate chatbots from human customer support agents. Other products such as future content recommendations on social media and streaming websites are likely to come from an AI rather than traditional data analysis.

The Internet of Things, AI, and automation will aid businesses to fill gaps created by the labor shortage while optimizing staff. In retail and hospitality, this will take the form of self-serve kiosks, autonomous order fulfillment, and AI-enabled drive-thrus, all freeing people up for higher-skilled roles.

Ultimately, an explosion of data requirements will offer complex challenges to firms that must manage large amounts of data.

This goes triple for many companies still struggling to fully digitize.

Although it’s hard to visualize, our reliance on technology will keep growing and the winners will be the ones who can harness these new technologies to supercharge their financial profiles.

It’s not that I am boring, but the companies leading the new stage of digital technologies are the biggest and richest of Silicon Valley, and I would rather ride the bandwagon with them than try the sexy contrarian play, especially with higher interest rates hurting start-up culture.

Mad Hedge Technology Letter

December 6, 2021

Fiat Lux

Featured Trade:

(THE HAWKS ARE HERE)

(ROKU), (ZM), (TWLO), (SNAP), (SQ), (MSFT), (CRM), (ADBE)

Higher inflation is something this tech bull cycle hasn’t dealt with, and it’s starting to rear its ugly head in the form of volatility and spades of it.

The Fed will have to increase interest rates or face runaway inflation that will crash the economy, but increasing interest rates will also make lives harder for tech companies.

As we try to understand the pace of interest hikes, certain tech companies will fare much better in this inflationary environment than others. To deduce the winners from the losers, investors should understand exactly how inflation affects each particular tech company.

Talk has gone from the Fed moving early to raise short-term rates, to the Fed moving even in early spring which in turn is spooking risk markets from cryptocurrencies, the S&P, and the Nasdaq.

Fed Chair Jerome Fed has done a poor job communicating his sudden hawkish tone and the market has had to quickly reprice risk assets because of the surprising nature of the hawkishness.

In the short-term, tech stocks will need some time to digest this new expectation, which I see as quite healthy, but short-term tough to swallow.

Fed Cleveland President Loretta Mester told the media she is “very open” to scaling back the Fed’s asset purchases at a faster pace so it can raise interest rates a couple of times next year if needed so this isn’t just one guy in Powell trying to move the needle.

Clearly, the Fed is moving in unison, and they threaten to become a major force in moving markets which is all we care about.

All that pressure is causing component and labor costs to rise. Companies that don't have enough pricing power to pass those costs on to their customers will likely see their gross and operating margins shrink.

This matters because tech companies offer some of the most generous salaries in the U.S. and substantial increases in pay hurts them the most.

Higher interest rates attract more consumers and businesses to put more money in higher-yield bonds and savings accounts.

There are 3 ways that higher rates are actually a gut punch to tech growth companies.

First, they increase the costs of borrowing incremental capital to expand a business. In more cases than not, tech growth companies rely on borrowed money because their operation is not yet sustainably profitable. That's bad news for high-growth tech companies, which are burning cash with widening losses.

Second, it reduces the long-term estimates for a company's earnings and free cash flow (FCF) growth meaning their underlying stock price is rerated downwards in the anticipation of this new reality.

Loss accruing tech companies commonly suffer an exodus as their underlying shares are repriced to reflect higher costs.

Just this morning we saw Roku (ROKU), Zoom Video Communications (ZM), Snap (SNAP), Twilio (TWLO), Square (SQ) breach 52-week lows.

The breadth of the market has been hollowed and the goalposts have indeed narrowed because of the hawkish tone at the Fed.

Lastly, higher interest rates drive institutional money into fixed income.

They do this largely by taking profits from crypto, tech stocks, or moving their stash on the sidelines then resurfacing the money into “safer” assets that anticipate weakening bond yields at the longer end of the curve.

So I won’t sit here and say sell all and every tech stock, it’s more nuanced than that.

I executed one position in December and that was Microsoft (MSFT) and it got pulled down with the broader market.

More importantly, I didn’t bet the ranch.

Ultimately, we still bask in the ideology that the tech bull market isn’t over yet because it isn’t, but this aggressiveness out of the blue has forced the overall tech market to temporarily rest with growth tech suffering major drawdowns.

In doing that, the ceiling for a Santa Claus rally is somewhat capped to the upside.

The Fed could have waited until January.

Sure, there will still be winners in tech and the odds of these winners are driven firmly behind the biggest and best like Microsoft, Amazon, Google, and Apple.

These are the type of companies that have the pricing power to raise prices and get away with it because consumers will be willing to pay it.

Other potential winners include cloud service giants like Salesforce (CRM) and Adobe (ADBE). These again are top-quality software stocks that can pass up higher enterprise software costs to the firms that can pay for it.

It’s entirely possible that the Fed could end up walking back some of these aggressive stances in the interest-raising process next year.

Don’t fight the Fed and don’t expect tech growth stocks to reverse until we receive more clarity with interest rate policy, if a reverse is triggered, it will play out with Apple, Amazon, Google, and Facebook, and Microsoft leading the way higher.

Global Market Comments

December 3, 2021

Fiat Lux

Featured Trade:

(DECEMBER 1 BIWEEKLY STRATEGY WEBINAR Q&A),

(PYPL), (MA), (AXP), (SQ), (TLT), (TBT), (TSLA), (AAPL), (FB), (MSFT), (AA), (FCX), (BITO), (COPA.L)

Mad Hedge Technology Letter

November 22, 2021

Fiat Lux

Featured Trade:

(RENOMINATION BOOSTS BIG TECH)

(FB), (GOOGL), (AMZN), (MSFT), (AAPL)

U.S. President Joe Biden is doing all he can do to make sure that the US Central Bank stays accommodative to big tech investors.

He let the doves back in the driving seat which is highly positive for corporate America and terrible for penny-pinching savers.

Biden’s decision to re-elect incumbent Fed Chair Jerome Powell was cheered by the market locking in his ultra-low interest rate policies for yet another term.

Even more brazen was the appointment of Vice Chair, an even more pronounced dove Dr. Lael Brainard.

The second in command often helps signal Fed policy and gives it a dovish twist and clears the way for all systems go in 2022.

Any inclination that interest rates would rise faster than expected is now a non-starter, and the Fed will push its "lower for longer" mantra in the face of surging inflation for as long as they can make excuses for it.

Ostensibly, the path of easiest conjecture leads me to say that the five biggest stocks in the S&P 500 – Facebook, Apple, Amazon, Microsoft, and Google, which are around 30% of the market and growing, will do well in 2022.

Long-term, they have comprised an average of about 14% of the entire stock market, and 2022 should be the year they knock on the 35% threshold.

This essentially means that the stock market is techs to win or lose and everyone else is just a footnote.

And yeah I know…it’s been like that for quite a while now; but it’s more prevalent than ever.

We are rolling into a year where big tech will weaponize their cash horde to issue low-interest corporate bonds of their own company debt and then spin those cash harvests into higher rate corporate bonds that cheapen their cost of doing business because they pocket the higher interest payments as profits.

Industry leaders are able to borrow more cheaply and in greater quantities, and the size of their balance sheets also offers incredible optionality.

This also means they can buy back more shares and also leverage up their balance sheets.

Preferential access to cheap money also cheapens the process of expansion, or in buying rivals, more easily. In effect, lower rates give leading companies an unfair set of tools to accelerate their dominance and which no regulator dares to prevent.

What does this mean in practice for investors? If falling rates have spiced up valuations of the biggest tech stocks on the way up, it implies they may struggle if rates rise, particularly as this would mean investors place less of a premium on future earnings.

But since the expectations are lower for longer, the market will be comfortable with the nominal rate even in the face of surging inflation, meaning it’s a net positive for tech stocks in 2022.

Powell and Baird will move as slow as needed and anything faster than that will shock the tech market and we will get a 5% drop which will be a golden buying opportunity.

I have read many experts’ take on tech preaching that regulation is here and coming fast to take down big tech.

However, I am in the camp that Congress will do hardly anything, and any investigation will end with a slap on the wrist which is fine.

I don’t subscribe to this ridiculous idea that superstars eventually tend to fall to earth.

I believe the current climate has set up big tech to gain an even bigger market share, crush the little guy faster, and trigger EPS to grow uncontrollably.

That’s what I am seeing on the ground with my own eyes, as opposed to baseless claims that big tech will revert back to the mean.

This sets the stage for big tech to benefit from such elevated rates of profitability next year, they will be happy to overpay for smaller companies to whom they will give an ultimatum to either sell up or get killed by them.

Numerous signs point to a devastatingly profitable and comically successful 2022 for the most recognizable and biggest tech firms who will refine their tech and harness their balance sheets in a systematically lethal way.

Unprofitable startups have a mountain climb as it relates to competing in their industries and they can thank President Joe Biden for that; they will be unduly penalized as a group that will result in lower share prices that force them to crawl on their knees to venture capitalists for capital injections.

Global Market Comments

November 8, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or A PERFECT UPSIDE STORM),

(GOOGL), (MSFT), (GS), (MS), (BRKB), (ROM), (TLT), (TBT)

(BITO), (ETHE)

Welcome to the perfect storm.

If there was ever any doubt that the market was going straight up for the rest of the year, it was dashed when the infrastructure budget passed on late Friday night with bipartisan support. Another $1.2 trillion will be dumped into the economy next year, adding 6% to GDP growth.

Of course, the stock market started sniffing out this possibility and resumed racing yet again to new all-time highs on September 30.

The latest round of earnings reports proved that corporate profit margins are exploding, along with profits. Demand is through the roof. It turned out that demand WASN’T lost, just deferred, as I vociferously begged followers to buy stocks at the April 2020 bottom.

Interest rates went down instead of up sharply on news of the Fed taper.

And the 10% correction that many expected never showed, forcing managers to chase the market so they can be seen as fully invested in the right names at yearend. That means buying more Alphabet (GOOGL), Microsoft (MSFT), Goldman Sachs (GS), and Morgan Stanley (MS) at whatever price so managers can look like the brilliant people that they really AREN’T.

There is no doubt that the economic data is turning from mixed to red hot.

We will see a Capital spending renaissance in 2022 as the economy shifts from manufacturing to service-driven, and services account for 80% of US GDP. It’s a perfect formula for an economy that is catching on fire.

As for the missing 5 million workers, I think what we are seeing is a 9/11 effect. That’s when people become aware of the transitory nature of life and ask themselves why they are working at a job they hate, some 80% of the labor force, especially at the minimum wage level. They retrain for better-paying, more meaningful professions, retire early, or otherwise go missing in action.

There is another category of missing workers: those who have made so much in the stock market and Bitcoin in the last 18 months they never have to work another day in their life. Are there 5 million of them? Maybe.

And how come everybody in the world knows that interest rates are rising except the bond market? The United States Treasury Bond Fund (TLT) has seen two, count them, two massive three-point RALLIES in the last ten days. The (TLT) may give all this back this week when we get hot inflation data.

It is a positioning issue and a classic “buy the rumor, sell the news” on interest rates. When the entire world is short bonds, they can only go UP. This means we are likely to see a $141-$151 (TLT) range in bonds for the next six months until we start to see actual interest rate RISES.

The Fed Tapers! The Fed taper starts immediately and will accelerate in 2022 until it goes to zero by June. Stocks took off, while bonds dove a $1.50 as soon as they noticed that “transitory” was missing from the release. Will the first interest rate hike in four years be moved up to June? Or do we get a double rate hike in December 2022? That’s where we may see the real volatility, after the market close. Semiconductor growth stocks hit new all-time highs. Financials moving back to highs, as are big tech stocks.

Q3 GDP comes in at a weak 2.0%, down from a 6% rate in Q2, thanks to the ravages of the delta virus, now in the rearview mirror. What happens next? That 4% wasn’t lost, just deferred into 2022. The rip-roaring 6% growth rate returns. That’s why stocks are pushing up to new all-time highs right now. I’m looking for a 5% growth rate next year as government stimulus spending eventually fades.

Nonfarm Payroll Report explodes to the upside in October at 531,000. The Headline Unemployment Rate drops to 4.6%. Pandemic benefits have ended, and a wider vaccination rate encouraged workers it is safe to go back on the job. The back months were revised up 250,000. Manufacturing was up 60,000 and Leisure & Hospitality was up 164,000, The U-6 “discouraged worker” unemployment rate fell to 8.3%. And there is massive pent-up hiring is yet to come. The US could see full employment by the end of Q3 anticipating a 6% GDP growth rate. The markets loved it and the (SPY) is zeroing in my $475 yearend target.

Inflation is rampaging, according to the Department of Commerce, which saw a sizzling 4.4% rate in September. That’s the fastest rate in 30 years. Rising energy and wage costs are big issues. This is why Goldman Sachs has moved up its forecast for the first interest rate rise to July 2022.

US Consumer Spending bounces back, up 0.6% in September after a hot 1% move in August. Demand for services took the lead as shortages head off spending on goods, like cars.

Ethereum hits a new all-time high, ticking at $4,670 in response to the Fed’s immediate taper. Bitcoin is still consolidating its recent three-month doubling. Buy (BITO), (ETHE), and (BLOK) on dips.

US Stock Buy Backs hit record in Q3, topping a staggering $224 billion, and the best is yet to come as companies try to burn through 2021 repurchase budgets. And you wonder why the stock market is going up?

US Dollar hits one-year high on red hot jobs data, presaging higher interest rates. Everyone seems to know that rates are rising except the bond market.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a massive +8.95% gain in October, followed by a decent 1.74% so far in November. My 2021 year-to-date performance maintained 90.30%. The Dow Average is up 16.7% so far in 2021.

After the recent ballistic move in the market, I am continuing to run my longs in Those include (MS), (GS), (BAC), (BRKB), and a short in the (TLT). All are approaching their maximum profit point and we have nothing left but time decay to capture. So, I am going to run these into the November 19 expiration in 9 trading days. It’s like having a rich uncle write you a check one a day.

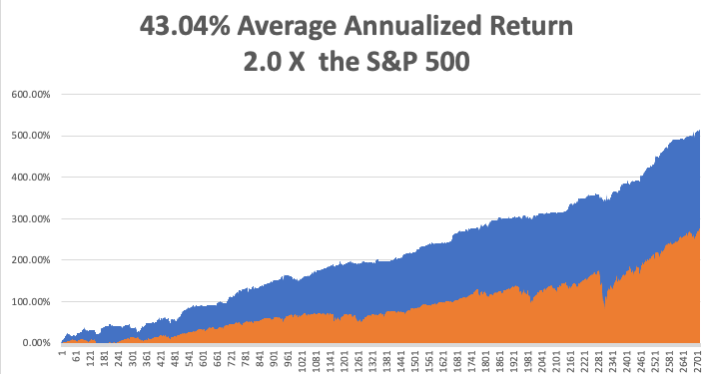

That brings my 12-year total return to 512.85%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 43.04 easily the highest in the industry.

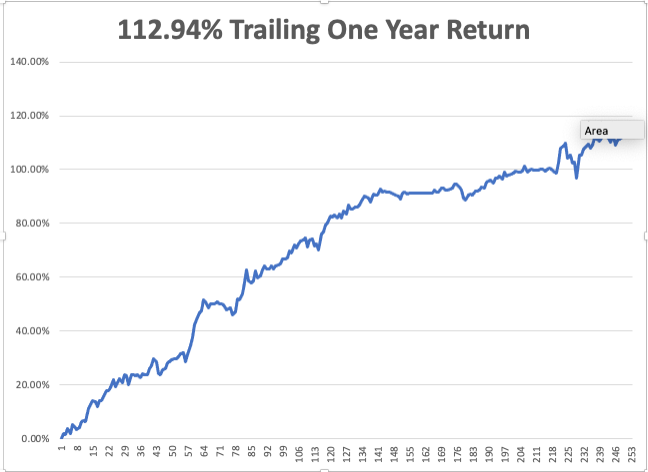

My trailing one-year return popped back to positively eye-popping 112.94%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 46.5 million and rising quickly and approaching 755,000 deaths, which you can find here.

The coming week will be all about the inflation numbers.

On Monday, November 8 at 9:00 AM, US Consumer Inflation Expectations for October are out. PayPal reports.

On Tuesday, November 9 at 8:30 AM, the all-important Producer Price Index is published. DR Horton (DHI) reports.

On Wednesday, November 10 at 8:30 AM, the Core Inflation Rate for October is printed. Walt Disney reports (DIS).

On Thursday, November 11 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, November 12 at 8:30 AM, the University of Michigan Consumer Sentiment is announced.

At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

As for me, dentists find my mouth fascinating as it is like a tour of the world. I have gold inlays from Japan, cheap ceramic fillings from Britain’s National Health, and loads of American silver amalgam.

But my front teeth are the most interesting as they were knocked out in a riot in Paris in 1968.

France was on fire that year. Riots on the city’s South Bank near Sorbonne University were a daily occurrence. A dozen blue police buses packed with riot police were permanently parked in front of the Notre Dame Cathedral ready for a rapid response across the river.

President Charles de Gaulle was in hiding at a French airbase in Germany. Many compared chaos to the modern-day equivalent of the French Revolution.

So, of course, I had to go.

This was back when there were five French francs to the US dollar and you could live on a loaf of bread, a chunk of cheese, and a bottle of wine for a dollar a day. I was 16.

The Paris Metro cost one franc. To save money, I camped out every night in the Parc des Buttes Chaumont, which had nice bridges to sleep under. When it rained, I visited the Louvre, taking advantage of my free student access. I got to know every corner. The French are great at castles….and museums.

To wash I would jump in the Seine River every once in a while. But in those days, not many people in France took baths anyway.

I joined a massive protest one night which originally began over the right of men to visit the women’s dorms at night. Then the police attacked. Demonstrators came equipped with crowbars and shovels to dig up heavy cobblestones dating to the 17th century to throw at the police, who then threw them back.

I got hit squarely in the mouth with an airborne projectile. My front teeth went flying and I never found them. I managed to get temporary crowns which lasted me until I got home. I carry a scar across my mouth to this day.

I visited the Left Bank just before the pandemic hit in 2019. The streets were all paved with asphalt to make the cobblestones underneath inaccessible. I showed my kids the bridges I used to sleep under, but they were unimpressed.

But when I showed them the Mona Lisa at the Louvre, she was as enigmatic as ever.

Everyone should have at least one Paris in 1968 in their lifetime. I’ve had many and am richer for it.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

1968

2019

Global Market Comments

November 5, 2021

Fiat Lux

Featured Trade:

(NOVEMBER 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(BRKB), (COIN), (IWM), (GOOGL), (MSFT), (MS), (GS), (JPM),

(BABA), (BIDU), (JD), (ROM), (PYPL), (FXE), (FXA), (FXB), (CRSP), (TSLA), (FXI), (BITO), (ETHE), (TLT), (TBT), (BITO), (CGW)