Featured Trade:

(WEDNESDAY, OCTOBER 17, 2018, HOUSTON GLOBAL STRATEGY LUNCHEON), (DON’T MISS THE SEPTEMBER 5 GLOBAL STRATEGY WEBINAR),

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or

THE WAR WITH CANADA STARTS ON TUESDAY),

(MSFT), (VXX), (TLT), (AAPL), (KO), (GM), (F)

I have spent all weekend sitting by the phone, waiting for the call from Washington D.C. to re-activate my status as a Marine combat pilot.

Failure of the administration to reach a new NAFTA trade agreement by the Friday deadline makes such a conflict with Canada inevitable.

And while you may laugh at the prospect of an invasion from the North, the last time this happened Washington burned. You can still see the black scorch marks inside the White House today.

This is all a replay for me, when in 1991, I enjoyed an all-expenses paid vacation courtesy of Uncle Sam. That’s when I spent a year shuttling American fighter pilots from RAF Lakenheath to forward bases at Ramstein, Aviano, Cyprus, and Dharan, Saudi Arabia.

It may seem unlikely that our nation’s military would require the services of a decrepit 66-year-old. However, in my last conflict I ran into another draftee who was then 66. It seems that the Air Force then had a lot of F-111 fighter bombers left over from Vietnam that no one knew how to fly.

That’s the great thing about the military. It never throws anything away. Not even me. The life of our remaining B-52 Stratofortress bombers at their final retirement in 2050 will be 100 years.

Perhaps Canada will decide that discretion is the better part of valor, and simply wait for the World Trade Organization to declare the Trump tariffs illegal, which they obviously all are.

That would then force the administration to withdraw from the organization the U.S. created at the end of WWII to regulate fair trade and go rogue. But then what else is new?

And while there was immense media time devoted to the NAFTA talks, which only oversees trade with partners with around $2 trillion each, China, the 800-pound gorilla, is still lurking out there. It has a $12.2 trillion GDP and Trump is imposing tariffs on another $200 billion of their imports there today.

The corner that Trump has painted himself into is that he has made himself SO unpopular abroad, insulting virtually everyone but Russia, that no leader is willing to risk doing a deal with him lest they get kicked out of office.

I certainly felt this in Europe this summer where the discussion was all about Trump all of the time. When you insult a nation’s leader you insult everyone in that country. I haven’t received that kind of treatment since the Vietnam War was running hot and heavy in 1968.

I’ll tell you, I’d much rather be flying combat missions over enemy territory without a parachute than trading a market like we had last week. For months now, it has been utterly devoid of low risk/high return entry points for all asset classes.

It’s been a slow-motion melt-up virtually every day against the most horrific news backdrop imaginable. Such is the wonder of massive global excess liquidity. It Trumps everything.

NASDAQ topped 8,000, proving that if you aren’t loaded to the gills with technology stocks, as I have been pleading all year, you are out of your freaking mind. If you don’t own Apple, you are doubly screwed.

I doubt that such data is available, but I bet the illiterate and the uneducated have been beating more literate types in performance by a huge margin.

The unresponsiveness to news isn’t the only thing afflicting this market. As the summer coughs and sputters its way to a close, we enter September, notorious as the most horrific trading month of the year. And we are launching into it with the Mad Hedge Market Timing Index stuck in the 70s, overbought territory, for weeks now.

Blockbuster earnings, the principal impetus for rising share prices in 2018, are now firmly in the rearview mirror, and won’t make a reappearance for another month. Then they die completely in 2019.

Perhaps this is why my long volatility position in the (VXX) is doing moderately well, even though the indexes have been hitting new all-time highs, with the S&P 500 briefing kissing $292. I rather practice my golf swing rather than try to outtrade this market, even though I don’t play golf.

Other than NAFTA, there was little to trade off of last week. Apple (AAPL) shares continue to break new records, hitting an incredible $228, in front of their big iPhone launch this month. Trump announced he was freezing wages on 1 million-plus federal employees next year. That will solve their tax problems for sure.

Coca-Cola (KO) bought British owned Costa for $5 billion, where I regularly breakfast while traveling abroad, in the hopes that perhaps its 501st new drink launch this year will be successful.

Amazon (AMZN) is within sofa change of becoming the next $1 trillion market cap company, making the parents of founder Jeff Bezos the most successful angel investors in history, worth $30 billion.

U.S. auto sales are in free fall. Car company shares (GM), (F) continued their slide as they are pummeled on every side by administration economic policies. One has to ask the question of how long the American economy can survive after losing a major leg like this one. Home sales, another vital component, are also suddenly awful.

Trump attacked big tech. The market yawned.

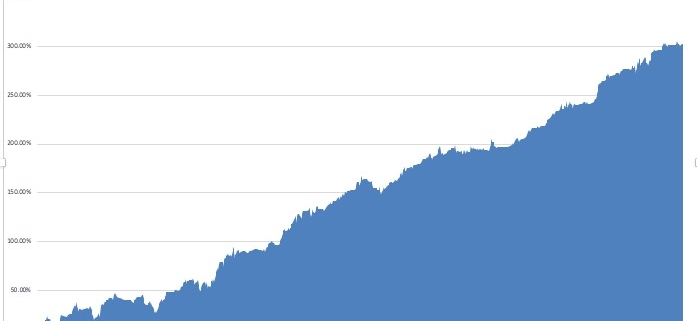

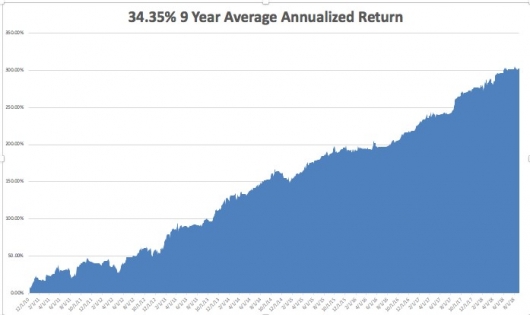

With the Mad Hedge Market Timing Index at 71 and bounces around in the 70s all week, I am not inclined to reach for trades here. All three of my current positions are making money, my longs in Microsoft (MSFT) and volatility (VXX) and my short in the U.S. Treasury bond market (TLT). August finally brought in a performance burst in the final days, leaving us with a respectable return of 2.13%. My 2018 year-to-date performance has clawed its way back up to 25.30% and my nine-year return appreciated to 303.48%. The Averaged Annualized Return stands at 34.35%. The more narrowly focused Mad Hedge Technology Fund Trade Alert performance is annualizing now at an impressive 28.59%.

This coming week housing statistics will give the most important insights on the state of the economy. On Monday, September 3, there was a national holiday, Labor Day.

On Tuesday, September 4, at 9:45 AM the PMI Manufacturers Index is out. August Construction Spending is out at 10:00 AM.

On Wednesday, September 5 at 7:00 AM, we learn MBA Mortgage Applications for the previous week.

Thursday, September 6 leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a rise of 3,000 last week to 213,000. Also announced at 9:45 AM are the August PMI Services Index.

On Friday, September 7 the Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me, the high point of my weekend was the funeral services for Senator John McCain. Boy, the Squids really know how to put on a ceremony. I suspect it may market a turning point for our broken American politics.

In the meantime, King Canute sits in his throne at the seashore ordering the tide not to rise.

Good luck and good trading.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/average-annualized-image-2-e1536069988463.jpg315530MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-09-04 14:29:162018-09-04 14:29:16The Market Outlook for the Week Ahead, or The War with Canada Starts on Tuesday

The technology-laced film Ready Player One gives viewers a snapshot into the future where technology, income inequality, and society have run their course, and the year 2045 looks vastly different from the world of 2018.

Set in a semi-dystopian backdrop, the movie offers us a deeper insight into how certain technology trends will permeate into everyday life.

The first and most obvious future trend is the copious use of avatars.

Avatars will become the new normal. The first place that humans will find them is through the use of social media and entertainment, as children eventually becoming a part of us like our social media profiles today.

The Mad Hedge Technology Letter has incessantly hammered home about the phenomenon of gaming, and this will incorporate virtual reality allowing gamers access to a new digital world.

This was the on show in the film where the likes of protagonist Wade Watts, played by Tye Sheridan spent most of his life playing in the virtual world of Oasis using his character Parzival.

This could be your child in the future.

Wade Watts character is the new cool for Generation Z, as they are largely unconcerned about underage drinking and partying like the generations before them.

Gaming and hanging out on their preferred social media platforms are the new cool.

The companies dictating the current video game industry will have the first crack at it to realize profits and develop new businesses such as Microsoft (MSFT), Nvidia (NVDA), Advanced Micro Devices (AMD), Electronic Arts Inc. (EA), Take-Two Interactive Software, Inc. (TTWO), and Activision Blizzard, Inc. (ATVI).

Children just aren’t going outside like they used to and per most studies, they are addicted to the smartphone you bought them at age 10.

Most studies have found that once a child becomes hooked on technology, it is hard to reverse the habit, as once they enter into adult life and start their career, they become even more reliant on the technologies that got them to that point in the first place.

If your kid is already staring at tech devices three to four hours per day now for activities other than school work, expect that to grow to a minimum of six to seven hours per day once he hits puberty and smartphone time limits begin to fade away.

This all means that VR and gaming could be the handsome winner in all this, and the use of social media platforms will reap the benefits as well.

Generation Z just surpassed Millennials in terms of population comprising 25% of the American populace.

Neither of these generations have grown up with VR in their daily lives because the technology wasn’t advanced enough to really make a dent in their lives.

More than 75% of Generation Z has access to a smartphone, and they can truly be called the first generation of digital natives.

Avatars will push deeper into everyday life because the facial tracking technology has advanced by leaps and bounds.

Instead of cartoon-like avatars, lifelike avatars have replaced the less refined versions. It will be a tough time going forward distinguishing what is real and what is fake.

If you think fake news is a problem now, imagine how fake it will become in the future.

This could devastate the news industry as news organizations run the risk of melting down at any point, or just being completely taken over by tech companies and their algorithms, which is already happening now with Alphabet (GOOGL).

The future looks bleak for all newspaper assets, and the ones with the most advanced digital strategies will survive.

Newspapers only have so much time they can hang on with digital ad revenue, the reason they are still in business.

Viewers don’t want to see ads – period. And at some point, they will be disrupted as well.

Swashbuckling youth already have downloaded ad-blockers to completely remove ads from their lives, and refuse to open any website that forces them to white list a website.

There are children in Generation Z who might never have seen an ad before because their digital native capability allows them to navigate around ads with adept skill.

Or the easy solution for many Millennials is just watch Netflix because the platform is ad-less. The aversion to ads is so strong that traditional media giants such as Fox are experimenting with six-second ads because that is all a viewer can tolerate these days.

The traditional media giants were forced to adopt this new format after Alphabet’s YouTube rolled out micro-ads.

Popular browser Mozilla announced it will block all tracking scripts by default beginning in 2019, thwarting unregulated data collection and relentless ad pop-ups.

The reason why digital ads will have an existential crisis is because companies will be able to monetize the pure data, forcing companies with huge digital ad businesses such as Facebook (FB) to battle with the new competition that only wants your data and not hawk ads.

This is already happening in the e-brokerage space with disruptors such as Robinhood, which charges no commission and is more interested in collecting data and getting by with interest payment revenue.

Let’s face it, digital ads are not a high-quality business even though they are a high-margin business. As tech moves forward, the quality of tech will rise eliminating all low-grade tech that is still profiting in 2018.

On the business side of things, automation is replacing humans faster than humans realize, and the replacement will be an avatar representing the face of a company.

For lower-end services, an avatar chosen by the customer will populate to often give better service than a human can provide.

If this type of service is scaled, it would offer a massive cut in costs for American corporations saving on employee costs.

It will have the same effect that self-checkout kiosks have at supermarkets, wiping out another position at the low-end.

The front-end avatar that will service you is all possible because of the rapid advancement of artificial intelligence.

Every possible situation will be programmed in the software and executed briskly.

If customers desire the human touch, they will have to pay up.

Human interaction will command a premium price because human interaction cannot be automated.

The financial industry has a huge target on its back, and swaths of financial advisors could be sacked in favor of avatars with the functional software behind it to produce profits.

In fact, many financial advisors are instructed to refrain from recommendations now and urged to collect input to enter into a proprietary algorithm that will decide the customers’ portfolio.

Big banks have enjoyed their time in the sun, but technology will disrupt them in the near future. This is why you have seen huge run-ups in innovative fintech companies such as Square (SQ) and PayPal (PYPL).

Many forms of outside entertainment are on the chopping block, as well as indoor entertainment such as Hollywood.

Hollywood A-list actors command hefty premiums to contract their services, and that could all crumble if younger audiences prefer avatar-based films with the human roles performed by unknowns.

Johnny Depp earns more than $50 million for one movie, and these insane amounts could deflate rapidly if human participation in films becomes marginalized.

Ready Player One was a test case for how much technology could be infused into a movie, and the audience easily absorbed it.

I could argue that audiences could argue even more in this VR format.

The movie had a budget of $175 million, and returned $582 million at the box office.

The resounding success will encourage more directors to inject technology into their movies, and they will have to, if they hope to tempt younger audiences to the movie theater.

Going to the movie theater is another activity that has struggled to cope against the rise of Netflix and technology.

Theaters have been forced to improve the overall experience of watching a film with prime seating, comfortable seats, and other extras that never existed.

Every industry is going through the same headache of competing with technological disruption.

Stagnation is akin to surrendering in 2018.

And it wasn’t just a fringe director creating Ready Player One, it was visionary director Steven Spielberg, one of the most famous movie directors to ever exist.

This will pave the way for other lesser-known movie directors relying on technology to pump out the profits.

They wouldn’t be the first people or the first industry to go down this road either.

“The worst thing a kid can say about homework is that it is too hard. The worst thing a kid can say about a game is it's too easy,” – said American media scholar Henry Jenkins III.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/Ready-Player-One-movie-image-1.jpg540422MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-09-04 01:05:402018-08-31 20:49:13Ready Player One’s Insight into the Future of Technology

Mad Hedge Technology Letter August 27, 2018 Fiat Lux

Featured Trade:

(WHY ALIBABA IS THE FIRST STOCK TO BUY WITH THE OUTBREAK OF TRADE PEACE),

(BABA), (GOOGL), (AMZN), (YELP), (MSFT), (MU), (ZTE), (HUAWEI)

According to the government agency, China Internet Network Information Center, the Chinese Internet community has surpassed 802 million, which only represents a 57.7% penetration rate, miles behind the 89% penetration rate in America.

The gargantuan scale of the Chinese Internet world means China has three times as many Internet users than America, and this is a big deal.

The additional 30 million added to the Chinese Internet ecosphere in the first half of 2018 shows the scale in which local Chinese tech companies are playing with and use to their clear-cut advantage.

Ostensibly, most business strategies in China revolve around scaled tactics as the backbone to operations.

There is even more room to expand in the Middle Kingdom and one clear victor sits atop the parapet looking at the riffraff below and that is Chinese Internet conglomerate Alibaba (BABA).

Alibaba, led by Chinese Internet pioneer Jack Ma, posted its highest-performing growth quarter in the past four years.

Total quarterly revenue ballooned an incredible 61% YOY to $11.8 billion, highlighting the dominant position Alibaba possesses in the Chinese e-commerce landscape.

If you want to know what Amazon (AMZN) is going to do next watch Alibaba.

Profit margins were somewhat sacrificed in the process because of M&A activity that saw Alibaba move into the physical supermarket business snapping up 35 Hema supermarket locations then reinvesting into the business. Echoes of Whole Foods?

Alibaba did not stop there, funneling another $3 billion into food delivery app ele.me, which plans to merge its operations with Yelp (YELP) lookalike app Koubei.

If you thought Silicon Valley moves at a rapid pace, the Chinese Internet space moves faster than lighting.

Alibaba last year dipped into the retail segment as well pocketing a department store chain with 29 stores along with 17 shopping malls.

Alibaba is the closest replica the world has to Amazon and thus is an ideal barometer of the health of the overall Chinese consumer and a peek under the complicated hood that is the Chinese economy.

Alibaba also provides onlookers at how China and its Internet behemoths are coping with the global trading war that has invaded the news headlines from its outset.

The short answer to all this is that China is coping quite well and by no means is ready to back down.

Indeed, there will be peripheral pressures exerted from the fringes, but the core engines remain intact and Chairman Xi can fall asleep in his Beijing abode more than peacefully.

A reason for the stalemate between the two governments is that both are quietly confident they have the levers in place to absorb whatever Molotov cocktails the other has to throw at them.

Investors would be mad to dismiss China’s capabilities after experiencing a mesmerizing economic rise enriching hundreds of millions of Chinese nationals that can be found comfortably living in western megacities in luxury real estate often with a real estate portfolio dotted around the world.

Alibaba’s management made it known on the earnings report that it is not worried much about the trade war because it is largely focused on the domestic Chinese consumer, which has been one of the best economic stories of the past decade.

The overseas expansion unfolding under Alibaba’s tutelage is away from the western world and predominantly focused on Southeast Asia and Eastern Europe where cheap, value-for-money hardware and software allows citizens at these income levels to participate in the e-commerce game.

These individuals can’t afford iPhones on a salary of peanuts. And Alibaba has targeted the undeveloped world as a potential lever of substantial growth.

The regulatory harshness of the west has shut out Huawei and ZTE from its shores. Australia followed suit as well, banning the two telecom companies even though it enjoys a better relationship with Beijing than Europe or North America.

China has already planned a workaround because the engines driving the Chinese tech miracle are semiconductor companies such as Micron (MU), which sells boatloads of DRAM memory chips to Chinese tech companies that flood the world with smartphones and other gadgets.

Beijing has already formulated a plan to circumvent American chips by tapping Korean, European, and Japanese chips to replace the current American supply that could vanish at any time.

Shenzhen-based chip company HiSilicon fully owned by Huawei is responsible for supplying Huawei with chips and is the biggest local designer of integrated circuits in China.

This is what the future of China looks like when China can finally build up the adequate supply necessary to achieve its plans to dominate global technology, America, and the world.

But the plan is still in the process of playing out. The awkwardness was highly visible when the administration’s ban of selling U.S. manufactured components to telecommunications company ZTE resulted in the company almost shutting down until a last-second change of heart by the administration.

The near-death experience will invigorate ZTE to muster its own local supply of chips to avoid the unreliable foreign supply and a deja vu feeling.

American chip companies won’t be able to enjoy the Chinese market for long as all these negative experiences for Chinese companies has forced Chinese tech companies to search and secure a guaranteed chip supply.

At the same time, Chinese local smartphone players have gone from 0 to 60 in no time with companies that barely existed a few years ago, such as Oppo, Vivo coming into the fore along with Huawei picking up 43% of the global smartphone market.

This is bad news for Apple as local competitors are learning fast and furious how to build premium smartphones via re-engineering the current technology or through forced technology transfers.

These companies subsequently offer these phones at the lowest possible price point. And at some point in the near future Apple could be expendable if Chinese smartphones start to display the type of quality the best phones show.

Chinese domestic consumption and investment comprise 90% of the GDP growth in China and are propped up by three robust trends including real wage growth boosting the middle-class population, high savings rate that of which Americans would be jealous, and easy access to credit vehicles.

When I was recently in the Middle Kingdom, it was highly evident that as the generations became younger, their quality of life was higher than their parents.

The opposite is happening in America with millennials earning demonstrably less than their parents’ generation while the American middle class is shrinking at an accelerated pace.

Beijing knows this and hopes to wait things out as it feels time is a positive variable for China and not America.

It is true that if this trade war took place in 20 years in the future, China would be in a stronger strategic position to extract whatever concessions it desires because even though Chinese growth is slowing, it is still growing at 6.5%.

And if you don’t believe what I just said then just look at Alibaba’s cloud division, which grew 93% YOY opening artificial intelligence-based data centers around Europe to battle Amazon (AMZN) and Microsoft (MSFT).

Europe was once Elysian Fields for American tech companies, but with European regulators going after American tech and China encroaching on European turf, the future looks a lot less certain for the FANGs there than ever before.

Alibaba’s operating margins dipped 10% YOY but the slide will be returned to shareholders in the future in the form of high-quality revenue and is worth the investment into the most innovative ideas of tomorrow.

I did not even mention the large stake Alibaba has in Ant Financial, which operates the ubiquitous digital payment app Alipay.

It would be analogous to Amazon if it owned Visa.

Alibaba is one of the best tech companies in the world headed by a former Chinese English language teacher in Hangzhou.

If America becomes too difficult or expensive with which to do business, Alibaba and Chinese tech will just recalibrate their strategy to deeper infiltrate the confines of Southeast Asia and the rest of the undeveloped world.

Any price war on undeveloped soil favors the Chinese as they have mastered scale better than anyone on the planet.

The stellar Alibaba numbers also mean the trade war has no end in sight as each player thinks they have the upper hand. But it also means the tech giants from both countries will come out unscathed and will lead their country’s respective equity markets higher for the foreseeable future.

“Technology is nothing. What's important is that you have a faith in people, that they're basically good and smart, and if you give them tools, they'll do wonderful things with them,” – said Apple cofounder and former CEO Steve Jobs.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-27 01:05:482018-08-24 20:37:39Why Alibaba is the First Stock to Buy with the Outbreak of Trade Peace

Featured Trade:

(WHY THE DOW IS GOING TO 120,000),

(X), (IBM), (GM), (MSFT), (INTC), (DELL), ($INDU), (NFLX), (AMZN), (AAPL), (GOOGL),

(THE MAD HEDGE CONCIERGE SERVICE HAS AN OPENING),

(TESTIMONIAL)

For years, I have been predicting that a new Golden Age was setting up for America, a repeat of the Roaring Twenties. The response I received was that I was a permabull, a nut job, or a conman simply trying to sell more newsletters.

Now some strategists are finally starting to agree with me. They too are recognizing that a ganging up of three generations of investment preferences will combine to drive markets higher during the 2020s, much higher.

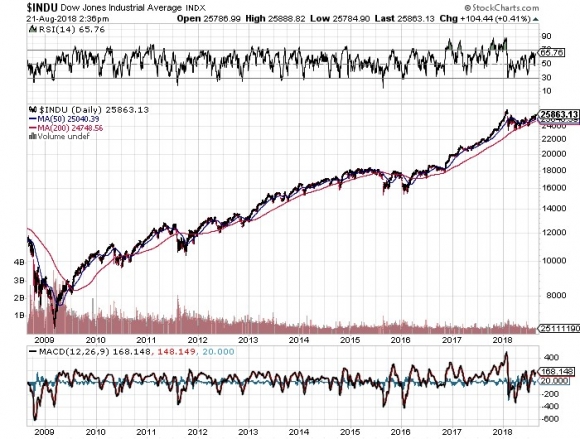

How high are we talking? How about a Dow Average of 120,000 by 2030, up another 465% from here? That is a 20-fold gain from the March 2009 bottom.

It’s all about demographics, which are creating an epic structural shortage of stocks. I’m talking about the 80 million Baby Boomers, 65 million from Generation X, and now 85 million Millennials. Add the three generations together and you end up with a staggering 230 million investors chasing stocks, the most in history, perhaps by a factor of two.

Oh, and by the way, the number of shares out there to buy is actually shrinking, thanks to a record $1 trillion in corporate stock buybacks.

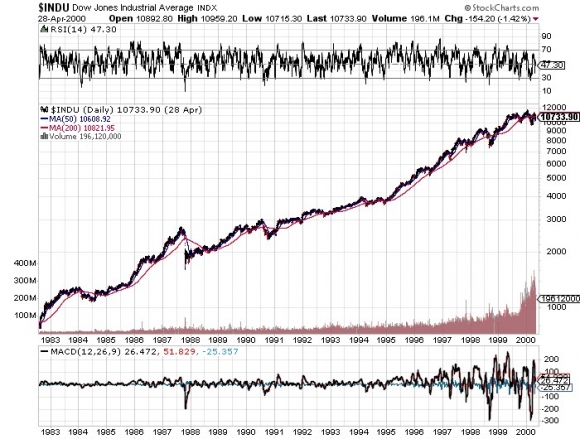

I’m not talking pie in the sky stuff here. Such ballistic moves have happened many times in history. And I am not talking about the 17th century tulip bubble. They have happened in my lifetime. From August 1982 until April 2000 the Dow Average rose, you guessed it, exactly 20 times, from 600 to 12,000, when the Dotcom bubble popped.

What have the Millennials been buying? I know many, like my kids, their friends, and the many new Millennials who have recently been subscribing to the Diary of a Mad Hedge Fund Trader. Yes, it seems you can learn new tricks from an old dog. But they are a different kind of investor.

Like all of us, they buy companies they know, work for, and are comfortable with. During my Dad’s generation that meant loading your portfolio with U.S. Steel (X), IBM (IBM), and General Motors (GM).

For my generation that meant buying Microsoft (MSFT), Intel (INTC), and Dell Computer (DELL).

For Millennials that means focusing on Netflix (NFLX), Amazon (AMZN), Apple (AAPL), and Alphabet (GOOGL).

That’s why these four stocks account for some 40% of this year’s 7% gain. Oh yes, and they bought a few Bitcoin along the way too, to their eternal grief.

There is one catch to this hyper-bullish scenario. Somewhere on the way to the next market apex at Dow 120,000 in 2030 we need to squeeze in a recession. That is increasingly becoming a topic of market discussion.

The consensus now is that an impending inverted yield curve will force a recession sometime between August 2019 to August 2020. Throwing fat on the fire will be a one-time only tax break and deficit spending that burns out sometime in 2019. These will be a major factor in U.S. corporate earnings growth dramatically slowing down from 26% today to 5% next year.

Bear markets in stocks historically precede recessions by an average of seven months so that puts the next peak in top prices taking place between February 2019 to February 2020.

When I get a better read on precise dates and market levels, you’ll be the first to know.

To read my full research piece on the topic please click here to read “Get Ready for the Coming Golden Age.”

Dow 1982-2000 Up 20 Times in 18 Years

Dow 2009-Today Up 4.3 Times in 9 Years So Far

https://www.madhedgefundtrader.com/wp-content/uploads/2018/08/John-on-mechanical-bull-story-1-image-3-e1534972073238.jpg313250MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-23 01:08:052018-08-22 21:23:50Why the Dow is Going to 120,000

Mad Hedge Technology Letter August 22, 2018 Fiat Lux

Featured Trade: (WHAT’S IN STORE FOR TECH IN THE SECOND HALF OF 2018?), (GOOGL), (AMZN), (FB), (UTX), (UBER), (LYFT), (MSFT), (MU), (NVDA), (AAPL), (SMH)

Tech margins could be under pressure the second half of the year as headwinds from a multitude of sides could crimp profitability.

It has truly been a year to remember for the tech sector with companies enjoying all-time high probability and revenue.

The tech industries’ best of breed are surpassing and approaching the trillion-dollar valuation mark highlighting the potency of these unstoppable businesses.

Sadly, it can’t go on forever and periods of rest are needed to consolidate before shares relaunch to higher highs.

This could shift the narrative from the global trade war, which is perceived as the biggest risk to the current tech market to a domestic growth issue.

Healthy revenue beats and margin growth have been essential pillars in an era of easy money, non-existent tech regulation, and insatiable demand for everything tech.

Tech has enjoyed this nine-year bull market dominating other industries and taking over the S&P on a relative basis.

The lion’s share of growth in the overall market, by and large, has been derived from the tech sector, namely the most powerful names in Silicon Valley.

Late-stage bull markets are fraught with canaries in the coal mine offering clues for the short-term future.

Therefore, it is a good time to reassess the market risks going forward as we stampede into the tail end of the financial year.

The shortage of Silicon Valley workers is not a new phenomenon, but the dearth of talent is going from bad to worse.

Proof can be found in the controversial H-1B visa program used to hire foreign tech workers mainly to Silicon Valley.

A few examples are Alphabet (GOOGL), which was granted 1,213 H-1B approvals in 2017, a 31% YOY rise.

Alphabet’s competitor Facebook (FB) based in Menlo Park, Calif., was granted 720 H-1B approvals in 2017, a 53% YOY jump from 2016.

This lottery-based visa for highly skilled foreign workers underscores the difficulty in finding local American talent suitable for a role at one of these tech stalwarts.

Amazon (AMZN) made one of the biggest jumps in H-1B approvals with 2,515 in 2017, a 78% YOY surge.

The vote of non-confidence in hiring Americans shines an ugly light on American youth who are not applying themselves to the domestic higher education system as are foreigners.

For the lucky ones that do make it into the hallways of Silicon Valley, a great salary is waiting for them as they walk through the front door.

Reportedly, the average salary at Facebook is about $250,000 and Alphabet workers take home around $200,000 now.

Pay packages will continue to rise in Silicon Valley as tech companies vie for the same talent pool and have boatloads of capital to wield to hire them.

This is terrible for margins as wages are the costliest input to operate tech companies.

United Technologies Corp. (UTX) chief executive Gregory Hayes chimed in citing a horrid “labor shortage in the U.S. and in Europe.”

He followed that up by saying the company will have to grapple with this additional cost pressure.

Certain commodity prices are spiraling out of control and will dampen profits for some tech companies.

Uber and Lyft, ridesharing app companies, are sensitive to the price of oil, and a spike could hurt the attractiveness to recruit potential drivers.

The perpetually volatile oil market has been trending higher since January, from $47 per barrel and another spike could damage Uber’s path to its IPO next year.

Will Uber be able to lure drivers into its ecosystem if $100 per barrel becomes the new normal?

Probably not unless every potential driver rolls around in a Toyota Prius.

If oil slides because of a global recession instigated by the current administration aim to rein in trade partners, then Uber will be hard hit abroad because it boasts major operations in many foreign megacities.

A recession means less spending on Uber.

Either result will be negative for Uber and ridesharing companies won’t be the only companies to be hit.

Other victims will be tech companies incorporating transport as part of their business model, such as Amazon which will have to pass on more delivery costs to the customer or absorb the blows themselves.

Logistics is a massive expense for them transporting goods to and from fulfillment centers. And they have a freshly integrated Whole Foods business offering two-hour free delivery.

Higher transport costs will bite into the bottom line, which is always a contentious issue for Amazon shareholders.

Another red flag is the deceleration of the global smartphone market evident in the lackluster Samsung earnings reflecting a massive loss of market share to Chinese foes who will tear apart profit margins.

Even though Samsung has a stranglehold on the chip market, mobile shipments have fell off a cliff.

Damaging market share loss to Chinese smartphone makers Xiaomi and Huawei are undercutting Samsung products. Chinese companies offer better value for money and are scoring big in the emerging world where incomes are lower making Chinese phones more viable.

The same trend is happening to Samsung’s screen business and there could be no way back competing against cheaper, lower quality but good enough Chinese imitations.

Pouring gasoline on the fire is the Chinese investigation charging Micron (MU), SK Hynix, and Samsung for colluding together to prop up chip prices.

These three companies control more than 90% of the global DRAM chip market and China is its biggest customer.

The golden days are over for smartphone growth as customers are not flooding into stores to buy incremental improvements on new models.

Customers are staying away.

The smartphone market is turning into the American used car market with people holding on to their models longer and only upgrading if it makes practical sense.

Chinese smartphone makers will continue to grab global smartphone market share with their cheaper premium versions that western companies rather avoid.

Battling against Chinese companies almost always means slashing margins to the bone and highlights the importance of companies such as Apple (AAPL), which are great innovators and produce the best of the best justifying lofty pricing.

The stagnating smartphone market will hurt chip and component company revenues that have already been hit by the protectionist measures from the trade war.

They could turn into political bargaining chips and short-term pressures will slam these stocks.

This quarter’s earnings season has seen a slew of weak guidance from Facebook, Nvidia (NVDA) mixed in with great numbers from Alphabet and Amazon.

Beating these soaring estimates is not a guarantee anymore as we move into the latter part of the year.

Migrating into the highest quality names such as Amazon and Microsoft (MSFT) with bulletproof revenue drivers would be the sensible strategy if tech’s lofty valuations do not scare you off.

Tech has had its own cake and ate it too for years. But on the near horizon, overdelivering on earnings results will be an arduous chore if outside pressures do not relent.

It’s been fashionable in the past for market insiders to call the top of the tech market, but precisely calling the top is impossible.

The long-term tech story is still intact but be prepared for short-term turbulence.

“By giving people the power to share, we're making the world more transparent,” – said cofounder and CEO of Facebook Mark Zuckerberg.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-22 03:05:032018-08-22 06:23:58What’s in Store for Tech in the Second Half of 2018?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.