Mad Hedge Technology Letter

July 30, 2021

Fiat Lux

Featured Trade:

(THE BEST WAY TO STREAMLINE YOUR TECH PORTFOLIO)

(MU), (PLTR), (AMD), (AMZN), (SQ), (PYPL)

Mad Hedge Technology Letter

July 30, 2021

Fiat Lux

Featured Trade:

(THE BEST WAY TO STREAMLINE YOUR TECH PORTFOLIO)

(MU), (PLTR), (AMD), (AMZN), (SQ), (PYPL)

Overperformance is mainly about the art of taking complicated data and finding perfect solutions for it. Trading in technology stocks is no different.

Investing in software-based cloud stocks has been one of the seminal themes I have promulgated since the launch of the Mad Hedge Technology Letter way back in February 2018.

I hit the nail on the head and many of you have prospered from my early calls on AMD, Micron to growth stocks like Square, PayPal, and Roku. I’ve hit on many of the cutting-edge themes.

Well, if you STILL thought every tech letter until now has been useless, this is the one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, I have a quick fix for you and your friends.

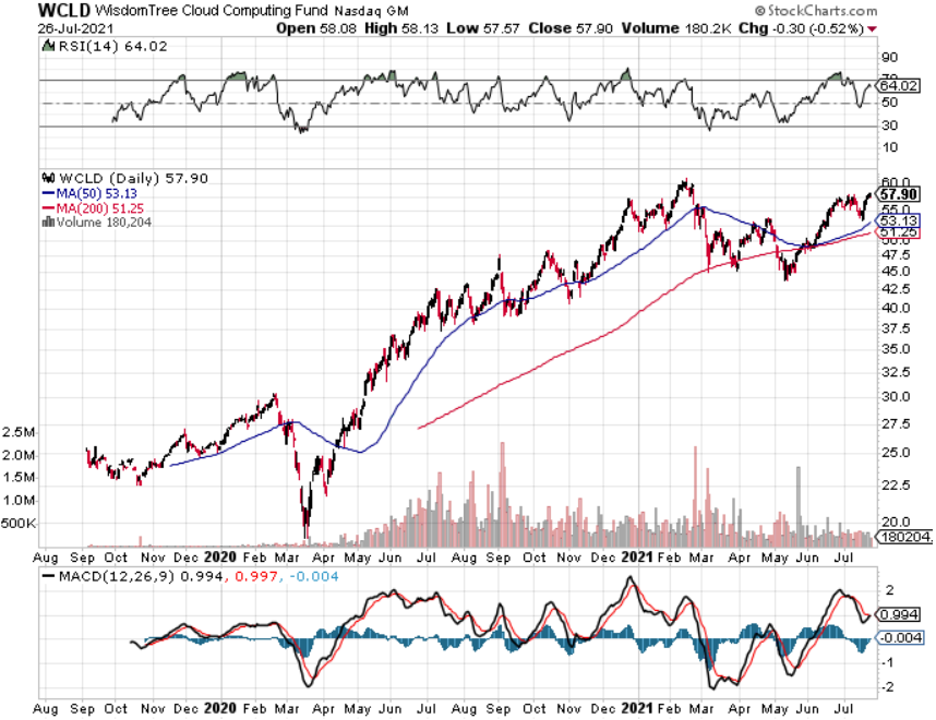

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

Yes, something like this does exist and we have been chronicling the development of the cloud since this tech letter’s launch.

The cloud is the concept powering the “shelter-at-home” trade which has been hotter than hot since March 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge of overwhelming the rest of the business world due to advancements in artificial intelligence and the Internet of Things (IoT) hyper-improving efficiencies.

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry.

Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise and often manually. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Speed, Ease, and Low Cost of Implementation – cloud software is installed via a network connection; it doesn’t require the higher cost of on-premise infrastructure setup maintenance, and installation.

Efficient Software Updates – upgrades and support are deployed via a network connection, which shifts the burden of software maintenance from the client to the software provider.

Easily Scalable – deployment via a network connection allows cloud SaaS businesses to grow as their units increase, with the ability to expand services to more users or add product enhancements with ease. Client acquisition can happen 24/7 and cloud SaaS companies can easily expand into international markets.

Business Model Advantages

High Recurring Revenue – cloud SaaS companies enjoy a subscription-based revenue model with smaller and more frequent transactions, while traditional software businesses rely on a single, large, upfront transaction. This model can result in a more predictable, annuity-like revenue stream making it easy for CFOs to solve long-term financial solutions.

High Client Retention with Longer Revenue Periods – cloud software becomes embedded in client workflow, resulting in higher switching costs and client retention. Importantly, many clients prefer the pay-as-you-go transaction model, which can lead to longer periods of recurring revenue as upselling product enhancements does not require an additional sales cycle.

Lower Expenses – cloud SaaS companies can have lower R&D costs because they don’t need to support various types of networking infrastructure at each client location.

I believe the product and business model advantages of cloud SaaS companies have historically led to higher margins, growth, higher free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must satisfy critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device, or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based, or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD component are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 100% from the nadir we saw in March 2020 and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many tech portfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a pure play on cloud computing software, because they do have other hybrid-sort of businesses, but the elements of its cloud business are nothing short of brilliant.

ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So, you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more chutzpah because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger precisely because they take advantage of the law of small numbers.

One stock that has the chance for a legitimate 10-bagger is my call on Palantir (PLTR).

Palantir is a tech firm that builds and deploys software platforms for the intelligence community in the United States to assist in counterterrorism investigations and operations.

This is one of the no-brainers that procure revenue from Democrat and Republican administrations.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a tech portfolio to target those extraordinary, extra-salacious tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner, and don’t forget about PLTR while you’re at it.

Global Market Comments

July 30, 2021

Fiat Lux

Featured Trade:

(JULY 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (CRSP), (TLT), (TBT), (BABA), (BIDU), (FXI), (RAD), (TSLA), (NASD), (NKLA), (NIO), (INTC), (MU), (NVDA), (AMD), (TSM), (VXX), (XVZ), (SVXY), (FCX), (ROM), (SPG)

July 28 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the July 28 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Lake Tahoe, NV.

Q: What is your plan with the (SPY) $443-$448 and the $445/450 vertical bear put spreads?

A: I’m going to keep those until we hit the lower strike price on either one and then I’ll just stop out. If the market doesn’t go down in August, then we are going straight up for the rest of the year as the earnings power of big tech is now so overwhelming. Sorry, that’s my discipline and I’m sticking to it. Usually, what happens 90% of the time when we go through the strike, and then go back down again by expiration for a max profit. But the only way to guarantee that you'll keep your losses small is by stopping out of these things quickly. That’s easy to do when you know that 95% of the time the next trade alert you’ll get is a winner.

Q: Are you still expecting a 5% correction?

A: I am. I think once we get all these great earnings reports out of the way this week, we’re going to be in for a beating. I just don't see stocks going straight up all the way through August, so that’s another reason why I'm hanging on to my short positions in the S&P 500 (SPY).

Q: What’s the best way to play CRISPR Therapeutics (CRSP) right now?

A: That is with the $125-$130 vertical bull call spread LEAPS with any maturity in 2022. We had a run in (CRSP) from $100 up to $170 and I didn’t take the damn profit! And now we’ve gone all the way back down to $118 again. Welcome to the biotech space. You always take the ballistic moves. Someday I should read my own research and find out why I should be doing this. For those who missed (CRSP) the last time, we are one proprietary drug announcement, one joint venture announcement, or one more miracle cure away from another run to $170. So that will probably happen in the next year, you get the $125-$130 call spread, and you will double your money easily on that.

Q: I’m down 40% on the United States Treasury Bond Fund (TLT) January $130-$135 vertical bear put spread LEAPS. What would you do?

A: Number one, if you have any more cash I would double up. Number two, I would wait, because I would think that starting from the Fall, the Fed will start to taper; even if they do it just a little bit, that means we have a new trend, the end of the free lunch is upon us, and the (TLT) will drop from $150 down to $132 where it was in March so fast it will make your head spin. I'm hanging onto my own short position in (TLT). If you are new to the (TLT) space and you want some free money, put on the January 2020 $150-$155 vertical bear put spread now will generate about a 75% return by the January 21, 2022 options expiration. I just didn't figure on a 6.5% GDP growth rate generating a 1.1% bond yield, but that’s what we have. I'm sorry, it’s just not in the playbook. Historically, bonds yield exactly what the nominal GDP growth rate is; that means bonds should be yielding 6.50% now, instead of 1.1%. They will yield 6.5% in the future, but not right now. And that's the great thing about LEAPS—you have a whole year or 6 months for your thesis to play out and become right, so hang on to those bond shorts.

Q: Do you have any ideas about the target for Facebook (FB) by the end of the year?

A: I would say up about 20% from current levels. Not only from Facebook but all the other big tech FANGS too. Analysts are wildly underestimating the growth of these companies in the new post-pandemic world.

Q: Do you think the worst of the pandemic will be over by September?

A: Yes, we will be back on a downtrend by September at the latest and that will trigger the next leg up in the bull market. Delta with its great infectious and fatality rates is panicking people into getting shots. The US government is about to require vaccinations for all federal employees and that will get another 5 million vaccinated. Americans have the freedom to do whatever they want but they don’t have the freedom to kill their neighbors with fatal infections.

Q: What should I do with my China (BABA), (BIDU), (FXI) position? Should I be doubling down?

A: Not yet, and there’s no point in selling your positions now because you’ve already taken a big hit, and all the big names are down 50% from the February high. I wouldn't double down yet because you don’t know what's happening in China, nobody does, not even the Chinese. This is their way of addressing the concentration of the wealth in the top 1% as has happened here in the US as well. They’re targeting all the billionaire stocks and crushing them by restricting overseas flotations and so on, so it ends when it ends, and when that happens all the China stocks will double; but I have absolutely no idea when that's going to happen. That being said, I have been getting phone calls from hedge funds who aren’t in China asking if it's time to get in, so that's always an interesting precursor.

Q: What happened to the flu?

A: It got wiped out by all the Covid measures we took; all the mask-wearing, social distancing, all that stuff also eliminates transmission of flu viruses. Viruses are viruses, they’re all transmitted the same way, and we saw this in the Rite Aid (RAD) earnings and the 55% drop in its stock, which were down enormously because their sales of flu medicines went to zero, and that was a big part of their business. I didn’t get the flu last year either because I didn’t get Covid; I was extremely vigilant on defensive measures in the pandemic, all of which worked.

Q: Why would the Fed taper or do much of anything when Powell wants to be reappointed in February 2022?

A: I don’t think he is going to get reappointed when his four-year term is up in early 2022. His policies have been excellent, but never underestimate the desire of a president to have his own man in the office. I think Powell will go his way after doing an outstanding job, and they will appoint another hyper dove to the position when his job is up.

Q: What are your thoughts on the Chinese electric auto company Nio competing here in the U.S.?

A: They will never compete here in the U.S. China has actually been making electric cars longer than Tesla (TSLA) has but has never been able to get the quality up to U.S. standards. Look what happened to Nikola (NKLA) who’s founder was just indicted. Avoid (NIO) and all the other alternative startup electric car companies—they will never catch up with Tesla, and you will lose all your money. Can I be any clearer than that?

Q: You recently raised the ten-year price target up for the Dow Average from 120,000 to 240,000. What is Nasdaq's target 10 years out?

A: I would say they’re even higher. I think Nasdaq (NASD) could go up 10X in 10 years, from 14,000 to 140,000 because they are accounting for 50% of all earnings in the U.S. now, and that will increase going forward, so the stocks have to go ballistic.

Q: What do you think of Intel (INTC)?

A: I don’t like it. They had a huge rally when they fired their old CEO and brought in a new one. There was a lot of talk on reforming and restructuring the company and the stock rallied. Since then, the market has started insisting on performance which hasn’t happened yet so the stock gave up its gains. When it does happen, you’ll get a rally in the stock, not until then, and that could be years off. So I'd much rather own the companies that have wiped out Intel: (MU), (NVDA), (AMD), and (TSM).

Q: When you do recommend buying the Volatility Index (VIX), do you recommend buying the (VIX) or the (VXX)?

A: You can only buy the VIX in the futures market or through ETFs and ETNs, like the (VXX), the (XVZ), and the (SVXY), or options on these. I would be very careful in buying that because time decay is an absolute killer in that security, and that's why all the professionals only play it from the short side. That's also why these spikes in prices literally last only hours because you have professionals hammering (VIX). Somebody told me once that 50% of all the professional traders in the CME make their living shorting the (VIX) and the (VXX). So, if you think you’re better than the professionals, go for it. My guess is that you’re not and there are much better ways to make money like buying 6-to-12-month LEAPS on big tech stocks.

Q: Can the Delta variant get a bigger pullback?

A: Yes. I expect one in August, about 5%. But if Delta gets worse, the selloff gets worse. You saw what it did last year, down 40% in the (SPY) in only two months, so yes, it all depends on the Delta virus. I'm not really worrying about Delta, it's the next one, Epsilon or Lambda, which could be the real killer. That's when the fatality rate goes from 2% to 50%, and if you think I'm crazy, that's exactly what happened in 1919. Go read The Great Influenza book by John Barry that came out 20 years ago, which instantly became a best seller last year for some reason.

Q: Does the Matterhorn have enough flat space on the top to stand on it?

A: Actually, there is a 6’x6’ sort of level rock to stand on top of the Matterhorn. If you slip, it’s a 5000’ fall straight down on any side, and on a good weather day in the summer, there are 200 people climbing the Matterhorn. There's sometimes a one-hour line just to take your turn to get to the top to take your pictures, and then get down again to make space for the next person. So that's what it's like climbing the Matterhorn, it's kind of like climbing Mount Everest, but I still like to do it every year just to make sure I can do it, and one year I hope to win the prize for the oldest climber of the year to climb the Matterhorn. Every year this German guy beats me; he’s two years older than me.

Q: When will Freeport McMoRan (FCX) start going up? I have the 2023 LEAPS

A: Good thing you have the two-year LEAPS because that gives you two years for inflation to show its ugly face once again. You just have to be patient with these. I think we’ll get a rally in the Fall along with all the other interest rate plays like banks, industrials, money management companies, and so on. (FCX) will certainly participate in that. In the meantime, if we get all the way down to $30 in Freeport McMoRan, I would double up your position.

Q: Why is oil (USO) not a buy? Oil is the ultimate inflation hedge.

A: Yes, unless all of the cars in the United States become electric in the next 15 years, which they will, wiping out half of all demand from the largest oil consumer. The United States consumes about 20 million barrels of oil a day, half of that is for cars, and if you take that out of the demand picture you dump 10 million barrels a day on the market and oil goes back to negative numbers like we saw last year. Never do counter-trend trades unless you’re a professional in from of a screen 24 hours a day.

Q: Should I take profits on my ProShares Ultra Technology ETF (ROM) November $90-$95 vertical bull spread and then enter a new spread when tech sells off?

A: Absolutely! When you have that much leverage and you get these price spikes, you sell! The leverage on this position is 2X on the ETF and 10X on the options for a total of 20X! Well done, nice trade and nice profit, go out and buy yourself a new Tesla and wait for the next dip in tech, which may have already started, and which could power on for the rest of August.

Q: What’s the next move for REITs?

A: REITs came off of historic lows last year; a lot of people thought they were going to go bankrupt, and for companies like (SPG) it was a close-run thing. I would be inclined to take profits on REITs here. The next thing to happen is for interest rates to go up and REITs don’t do that great in a rising rate environment.

Q: When is the off-season in Incline Village?

A: It’s the Spring and the Fall, in between ski season and the summer season. That means there are four months a year here, May/June and September/October, where I’m the only one here and the parking lots are empty. There is no one on the trails, the weather is perfect, the leaves are changing colors, and the roads aren’t crowded, so that is the time to be here. It’s a mob scene in the winter and a worse mob scene in the summer!

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

July 6, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or ALL EYES ON THE FANGS)

(FB), (AAPL), (AMZN), (MSFT), (NFLX), (NVDA), (AMD), (MU)

If you are a believer in the FANGS (FB), (AAPL), (AMZN), (MSFT), (NFLX), with NVIDIA (NVDA) as an add-on, last week was definitely your week.

They rose every day, ending the week with a melt-up of epic proportions. After eight months in the penalty box, tech came back with a vengeance and is now two months into their comeback tour.

The icing on the cake was Facebook’s big win in the antitrust suit from the FTC. That suitably deep-sixes the issue not just for (FB) but all of big tech, possibly for years. The five stocks above now account for a hefty 22% of the S&P 500 (SPY).

The question now on everyone’s mind is what’s next for tech? 25%? 30% 50%? The answer is all of the above, but you have to give it some time, like years.

We are now in an overbought market where big tech has become the cheapest sector. In addition, the global chip shortage promises to get worse before it gets better, with some products seeing a 10X increase in a single generation.

Companies that can’t get the chips they want are resigning products around the chips they can get on the fly.

This has created enormous spillover demand for marginal suppliers like Advanced Micro Devices (AMD) and Micron Technology (MU). It has also accelerated the evolution of technology.

Companies that already have decade-long supply chains already set up, like Tesla, now have a big advantage. That’s why (TSLA) has managed a healthy 27% gain in six weeks.

The severity of the chip shortage is wildly estimated if you look at future design plans of the biggest industries. A tech rally lasting months, if not years, was a totally natural progression.

I’ll tell you who else is dropping the ball. Analysts and strategists are consistently underestimating the strength of the economic recovery and the torrid growth of earnings. They are lagging by about six months. That is why 80% of announcements have delivered upside surprises.

There are more surprises to come.

When markets peaked in April, an eye-popping 92% of shares were above their 50-day moving average. Now, we are only at 52%. That suggests we have another month of excitement before we get another short-term correction.

June Nonfarm Payroll Report comes in hot, up 850,000, an eye-popping 150,000 better than expected. The headline Unemployment Rate moved up slightly to 5.9%. Accommodation gained 269,000, and Food Services & Drinking Places were up 194,000. It was a true Goldilocks number for the stock market, but not the million some had hoped for. My 30% forecast for the Dow Average is looking good.

The Infrastructure Bill extends the hot economy well into 2023 and longer. Analysts better start upgrading now, who have been badly lagging behind the recovery. Tech stocks saw this six weeks ago and began their torrid rally. Buy everything on dips and stick with the barbell strategy to catch all of the rotations.

Rents will continue to go through the roof. Good thing you don’t live in Boise, ID, which is seeing the fastest rent increases in the county at 39% YOY. Of course, having the Micron Technology (MU) HQ there is a major push. Don’t expect any respite. With home prices soaring, rents will get dragged up as prospective buyers are priced out of the market.

Weekly Jobless Claims moderate further, 364,000 Americans filed new claims for unemployment benefits last week - lowest since pandemic. Still elevated from a typical pre-pandemic week when we would see about 210,000 claims.

Softbank’s capital flooding into Crypto, with Japan's SoftBank Group Corp has invested $200 million in Mercado Bitcoin, one of the largest cryptocurrency exchanges in Latin America signaling the start of the first phase of big institutional money hoping to take advantage of the digital currency craze.

Goldman Sachs is the top financial pick according to JP Morgan Chase. All cylinders are firing and we’ve just come off a fabulous 15% dip. A move to more sustainable revenue streams, like wealth management, is the reason, which Morgan Stanley did decades ago under my watch. I’m looking for $450 on dips. Buy (GS) on dips.

Morgan Stanley doubles its dividend, now that it has passed the Fed stress test and the tethers are off. It also announced a share buyback of $12 billion over the next year which may be increased. Buy (MS) on dips.

S&P Case Shiller National Home Price Index for April hits new high, up 14.6%, the biggest increase in 30 years. Phoenix leads at +22.3%, followed by San Diego at +21.6% and Seattle at +20.2%. The numbers run from incredible to unbelievable.

CRISPR Therapeutics goes through the roof, up 12% at the highs, on successful drug trials by Intellia Therapeutics (NTLA) and Regeneron (REGN). The Mad Hedge Biotech Letter core holding provided the gene-editing technology behind the 45% gain in (NTLA) today. It enabled the 85% elimination of a rare inherited fatal liver disease, transthyretin amyloidosis. Say that fast three times. Buy (CRSP) on dips. With Editas, there are only three small companies that have a monopoly here.

Facebook wins antitrust action, a federal judge dismissing an FTC action against the company. The move set the entire tech sector on fire. It looks like all of NASDAQ is going to much higher highs. I bet you had a great day. The court found that (FB) did not enjoy a monopoly which might have forced them to sell off Instagram and WhatsApp.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

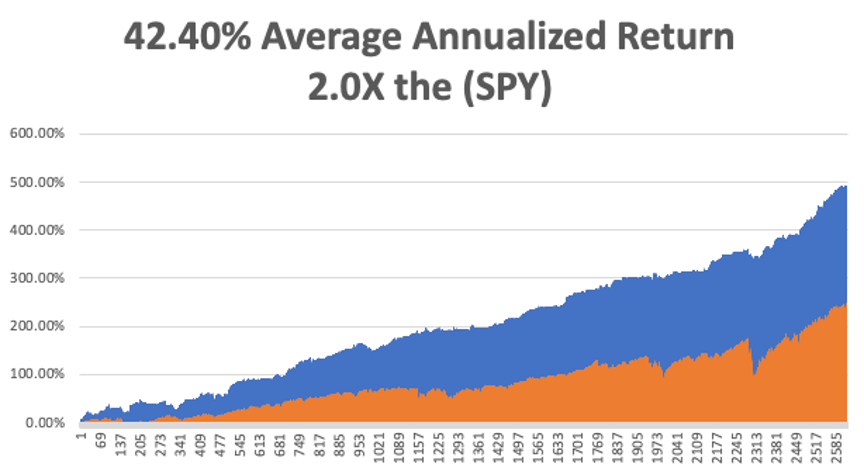

My Mad Hedge Global Trading Dispatch profit reached 0.71% gain so far in June on the heels of a spectacular 8.13% profit in May. That leaves me 100% in cash.

My 2021 year-to-date performance appreciated to 68.60%. The Dow Average is up 13.7% so far in 2021.

I spent the week sitting in 100% cash, waiting for a better entry point on the long side. Up this much this year, there is no reason to reach for the marginal trade, then maybe instead of the certainty. I’ll leave that for the Millennials.

That brings my 11-year total return to 491.15%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.40%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 112.59%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 33.7 million and deaths topping 606,000, which you can find here.

The coming week will be a weak one on the data front.

On Monday, July 5, markets are closed for the US Independence Day celebration.

On Tuesday, July 6 at 10:00 AM, the ISM Non-Manufacturing Index for June is released.

On Wednesday, July 7 at 10:00 AM, the Federal Open Market Committee Meeting from the last meeting are published.

On Thursday, July 8 at 8:30 AM, the Weekly Jobless Claims are published.

On Friday, July 9 at 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, with all the hiking I have been doing during the pandemic, I have been listening to a lot of WWII audio books lately. That reminds me of an old friendship I had with Toshiro Mifune, then the most movie famous star in Japan.

Mifune was drafted into the Japanese army during WWII where he served as an aerial reconnaissance photographer. After the war, that led him to work as a cameraman at Toho Productions, then the largest movie company in Japan.

A friend submitted his photo with an application for a casting call without his knowledge, and Toshiro, a good-looking guy, was one of 48 picked out of 4,000. He then met the legendary director, Akia Kurosawa, and the two launched the golden age of Japanese cinema in the late 1940s.

In just a couple of years, they produced blockbuster classic films like the Seven Samurai, Rashomon, and Throne of Blood, all of which are now required viewing by every American film school, and where Mifune demonstrated his impressive skills with a sword he picked up in the army.

I met Toshiro late in his career when he was cast as Admiral Isoroku Yamamoto for the 1976 Universal movie Midway. The problem was that Mifune couldn’t speak a word of English. I was brought in to bring Toshiro up to par in a crash course held at his west Tokyo mansion every afternoon seven days a week. We became good friends.

After a heroic effort, Mifune’s English was still awful, so the producers brought in a voice actor to dub Mifune’s part in Midway. That was Paul Frees, who provided the voice for the Disneyland’s Haunted House and Pirates of the Caribbean rides, as well as the cartoon Boris Badenov. His voice is still attached to those rides today, and I recognize it every time I take the kids.

Midway was a huge success and Mifune’s next big role was to play Commander Mitamura in Stephen Spielberg’s 1941. He followed that up with a role as Toranaga in James Clavell’s 1980 miniseries, Shogun, another old friend. (Clavell is a story for another day). My tutoring skills came back into demand once again, with better results.

Mifune died in 1997 at 77 and I miss him still.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

July 2, 2021

Fiat Lux

Featured Trade:

(WHAT’S UP WITH MICRON?)

Semiconductor chips have been a contentious issue since a dearth of supply has crippled tech companies around the world.

Memory and storage have become increasingly critical across diverse end-market applications, spanning from the data center to the edge and from business to consumer.

Within this context, Micron (MU) is strengthening not only financially, but also competitively.

Micron is transforming into a product leadership company that will help with upcoming node transitions, strengthening product portfolio, and deeper customer engagements that will further enhance its competitive position.

Ironically, Micron's transformation is taking place against a global backdrop of unprecedented geopolitical and economical challenges.

In the near term, enterprise servers have been weak, and that’s impacting the demand outlook.

In the first half of 2020, strong cloud demand trends were building up through the year.

The inventories, by and large, accelerated in cloud for a while and accelerated in enterprise as well until covid hit, as financial and other sectors invested in enterprise server side, but the pandemic changed everything from March 2020.

This caused enterprise to be generally weak since then, but the Cloud demand, given the work-from-home and e-commerce and streaming, all these kinds of applications have driven strong growth on the cloud side, and the strength isn’t going away anytime soon.

The middle chunk of the calendar-year 2020 saw a surge in demand in cloud.

Naturally, in the second half, Micron expects the cloud side to moderate as workers go back to the office signaling a pickup in the enterprise side of the business.

And don’t forget, in 2020, because of the pandemic, total smartphone unit sales were down by 10% year-over-year basis.

But in 2021, smartphone sales are expected to pick up as consumers feel the need to improve their phones and economies bounce back in North America.

In fact, smartphone sales are already picking up in the marketplace right now.

Not only is it a story of increasing smartphone sales as we go through calendar 2021 beyond the seasonally slower first quarter of the calendar, but it is also the story in 5G of higher content, both for memory and storage.

These are the demand drivers that are offering an optimistic outlook for DRAM demand in calendar-year 2021, continuing to improve, starting from the beginning of the year, particularly as we get past the seasonal calendar Q1 time frame.

I would expect a backdrop of demand expectation of 20% growth in DRAM.

Desktop PC sales have been weak due to pandemic-driven changes to customer buying patterns, but DRAM and NAND content growth continue to be a secular trend in the automotive market, supported by advanced infotainment systems and increased automation in cars. The pandemic has significantly impacted both auto production and demand in fiscal 2020, but there was a strong recovery toward the end of fiscal Q4, and expect sequential growth in sales of Micron products in the automotive market in Q1.

Huawei has been a large customer at approximately 10% of fiscal Q4 sales and Micron received notification to cut off sales given a month by the US government to do so. This is a highly negative event resulting in a loss of sales.

Micron estimates that 2020 industry DRAM bit demand growth is likely to be in the “mid-teens percent range”, while NAND bit demand growth is likely to be in the “mid-20s”.

Q4 revenue was approximately $6.1 billion, up 11% sequentially and 24% year over year which I would deem healthy.

DRAM revenue increased 22% sequentially and 29% year over year.

Micron is also holding higher levels of raw material during this period because of supply uncertainty and expects inventory levels to normalize over the course of 2021.

To sum it up, Micron’s management has started to see recovery in the mobile, auto, and consumer markets, but the pace of recovery has been moderated by the continued impact of the pandemic, and shortages of certain non-memory components in some end markets.

Enterprise demand is still weak, and customers may be carrying higher inventory.

Micron continues to execute well despite continued market uncertainty and geopolitical challenges.

The stock sold off on disappointing news that Huawei’s lost business was 10% of sales, weak enterprise activity, and negative PC sales momentum.

There has been a great deal of news regarding the shortage of chips, little do many know, non-chip components are also needed to build Micron’s chip products.

Even though their cloud business was up big during the pandemic, enterprise business was down big because office workers were sent home and management felt there was no reason to progress with the enterprise upgrade cycle.

The lack of smartphone sales affected sales for Micron’s chips as many people held off on their own smartphone upgrade cycle and maintained the phone they already had.

It was a mixed bag for sure, which is why Micron sold off on the earnings’ report and the stock will need time to digest shares after a pandemic-induced boost in expectations that led the stock higher from $42 to $92.

Expectations and performance got too far ahead of itself in the short-term and analyzing this earnings’ performance, it’s cut and dry that there are also many drawbacks to a NAND and DRAM chip business in the pandemic.

Some parts do well, and some do worse and that expectation wasn’t baked into the pricing.

Expect Micron to retrace further as the market has told us they will need to fix parts of their business such as the enterprise side, phone business, and PC desktop business for the stock to reaccelerate past $92.

Mad Hedge Technology Letter

April 21, 2021

Fiat Lux

Featured Trade:

(BUY OR SELL FIRST QUARTER TECH EARNINGS?)

(IBM), (MU), (SAMSUNG), (ZM), (GOOGL)

We are on the cusp of tech earnings which could either take us on the next leg up or leg down.

Going off of data points that we are getting from around the world, it’s clear that the secular bull market in big technology is as healthy as ever.

A few weeks ago, South Korea’s behemoth Samsung Electronics sounded off when it said first-quarter profit likely rose 44% because of the surge in sales of smartphones and TVs.

The work-from-home economy has made technology stocks the ultimate winner and now we need to assess what will happen to these very stocks in 2021.

Many analysts out there see an ongoing correction in names such as videoconferencing software company Zoom (ZM) which is going through a drawn-out consolidation phase after hyper-growth in their products last year.

That is not a bad thing, but frustrating in the short-term.

Tech stocks are renowned for getting ahead of itself.

Waiting for tech stocks to grow into their valuation is no fun, however, ultimately, there is an avalanche of money piling into this sector because it is fundamentally underpinned by cash cow secular trends.

Part of that thesis also is applied internationally to giants like Samsung, the South Korean technology giant forecast January-March operating profit at $8.32 billion.

Samsung’s flagship Galaxy S21 smartphone series outsold the previous version by a two-to-one margin in the six weeks since its January launch.

Profit in Samsung’s television set and home appliance business also likely more than doubled due to continued stay-at-home demand.

Cross-town TV and home appliance rival LG Electronics announced its largest-ever preliminary quarterly operating profit for January-March.

The secular health is not only confined to Korea, as U.S. memory chip peer Micron Technology last month forecast third-quarter revenue above analyst estimates due to rising demand brought about by a global shift to remote work.

The price of DRAM chips widely used in laptops and other computing devices rose 5.3% in January-March from the previous three months.

Samsung will invest about 10 trillion won in its chip contract manufacturing business this year, compared to about 6 trillion won last year.

In addition to the performance, regulation is now set to offer another helping hand to U.S. tech with two top White House aides hosting a meeting on how to better equip the state of the U.S. supply chain.

Samsung is considering a new $17 billion chip plant in the United States.

On the night before an earnings flurry, we also got word from IBM that they finally reversed 4 years of declining revenue to post 1% revenue growth.

Like many big tech groups, IBM has jumped on the bandwagon of clients digitally transforming their businesses, using hybrid cloud and AI to capture new growth opportunities, increase productivity and create operating flexibility.

Their revenue performance this quarter reflects this. Global business service (GBS) cloud revenue growth accelerated to almost 30%, doubling its growth rate from the prior quarter with strong growth across the portfolio.

The numbers reflect expanding practices with ecosystem partners like Salesforce and Adobe and strong momentum in their acquisition of Red Hat.

IBM has doubled the number of Red Hat client engagements from the prior year to over 150, working with companies such as HBO, Marriott, Vodafone, and Honda.

They’ve now signed $2 billion of business in their Red Hat practice inception to date.

Across these, IBM's cloud revenue was up 18% in the quarter and over the last 12 months and now stands at over $26 billion for the last year.

Like many other tech firms, employment hiring is expanding with IBM hiring thousands of people in the past quarter.

Like other firms as well, M&A is an often-utilized growth strategy with IBM closing on six acquisitions since mid-December.

They are adding go-to-market and delivery capabilities in GBS, and technical skills in Red Hat. And they’re increasing R&D in areas like AI and quantum to drive innovation.

Across cloud and cognitive software, IBM continues to increase subscription and support renewal rates, driving the record deferred income levels.

Red Hat continued solid performance with normalized revenue growth of 15%, led by Red Hat Enterprise Linux and OpenShift, both of which continue to gain share.

Even IBM, the laggard of tech, is improving their balance sheet by whittling down $3 billion from year-end, their debt was down $5 billion. They have now reduced debt by about $17 billion from the peak.

IBM even still delivers shareholders a nice dividend.

The takeaways from IBM and Samsung will largely apply to many of the tech companies that are about to report earnings.

Hiring is up because the business is doing so well.

Even if these legacy operations are only growing minimally in IBM, their cloud operations are far and away the highest growth element in their portfolio, and the performance of Red Hat indicates that.

The secular tailwinds are indeed helped by the business environment undergirded by a work-from-home assumption which is why companies like Samsung are posting record sales in tablets, smartphones, and can’t keep up with the demand for chips.

We are getting indication that much of the transformation into the 2020 digital economy is here to stay, but the issue in April is that although companies are as healthy as could be, firms are now facing Himalayan-like comparisons with last year.

Last year, April was a time when technology took off like a scalded chimp, and fast forward to 2021, many tech firms won’t be able to beat those year-over-year numbers they posted during peak lockdown business.

What I expect is for many tech firms to announce that comparisons were tough to beat because of a once in a 100-year event that locked down most of the world, but many tech firms will reaccelerate growth after a period of earnings consolidation.

Expectations have gotten a little stretched and outperformers like Alphabet (GOOGL) are already up 25% year to date, but I can argue that the guys at Google are making miracles and are surpassing even astronomically high expectations.

That won’t be the case for other tech companies that will need miracle performance to outdo exorbitant forecasts, but just quite aren’t there like Google.

Consolidation through sideways price action could take hold in the second quarter as many tech firms need time to recalibrate so they can reaccelerate in the second half of the year which they indeed will.