Global Market Comments

February 14, 2019

Fiat Lux

Featured Trade:

(WHY I’M AVOIDING PFIZER LIKE THE PLAGUE)

(PFE), (MRK), (MVS),

(THE LIQUIDITY CRISIS COMING TO A MARKET NEAR YOU),

(TLT), (TBT), (MUB), (LQD),

(TESTIMONIAL)

Global Market Comments

February 14, 2019

Fiat Lux

Featured Trade:

(WHY I’M AVOIDING PFIZER LIKE THE PLAGUE)

(PFE), (MRK), (MVS),

(THE LIQUIDITY CRISIS COMING TO A MARKET NEAR YOU),

(TLT), (TBT), (MUB), (LQD),

(TESTIMONIAL)

Global Market Comments

February 13, 2019

Fiat Lux

Featured Trade:

(BIDDING MORE FOR THE STARS),

(SPY), (INDU), (NVDA)

(NOW THE FAT LADY IS REALLY SINGING FOR THE BOND MARKET),

(TLT), (TBT)

Global Market Comments

February 8, 2019

Fiat Lux

Featured Trade:

(FEBRUARY 6 BIWEEKLY STRATEGY WEBINAR Q&A),

(TLT), (FXA), (NVDA), (SPY), (IEUR),

(VIX), (UUP), (FXE), (AMD), (MU), (SOYB)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader February 6 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Why are you so convinced bonds (TLT) are going to drop in 2019?

A: I think the Fed will regain the confidence to start raising rates again in the second half. Wage inflation is starting to appear, especially at the minimum wage level in several states. That will crater the bond market as well as the stock market, just as we saw in the second half of 2018. We’re in unknown territory in the bond market; we’re issuing astronomical WWII levels of debt and it’s only a matter of time before the Federal government crowds out private sector borrowers. Even if the bond market sidelines during this time, we will still make the maximum profit in the kind of option bear put spreads I have been putting on.

Q: Why did the Aussie (FXA) go down when they suddenly flipped from rising to cutting interest rates?

A: Interest rate differentials are the principal driver of all foreign exchange rates. They always have been and always will be. Rising rates almost always lead to a stronger currency. And with the US Fed on pause for the foreseeable future, we think the Aussie will be stronger going into 2019.

Q: Do you see the 10-year US Treasury yield going back up to 3.25% this year?

A: Yes, it’ll probably happen in the second half of the year—once the Fed gets its mojo back and decides that high employment and inflation are the bigger threats to the economy.

Q: Has NVIDIA (NVDA) bottomed here?

A: Probably, but you don’t want to touch the semiconductor chip companies until the summer. That’s when all the industry insiders expect the industry to turn and start discounting rocketing earnings after the next recession.

Q: Are stocks expensive here (SPY)?

A: On a trailing basis no, on a forward basis definitely yes. The current price/earnings multiple for the market is 17 now against a 14-20 range in 2018. So, we are dead in the middle of that range now. That’s OK when earnings are rapidly rising as they did last year. But they are falling now and at an increasingly increasing pace.

Q: Do you think the administration used the shutdown to bring forth a recession? To kickstart the pro-economic platform for reelection in 2020?

A: The administration’s view is that the economy is the strongest it’s ever been with no chance of future recession and that they will win the election as a slam dunk. If you believe that, buy stocks; if you don’t, sell them.

Q: How bad do you think Europe (IEUR) will get and does that mean the dollar (UUP) could see parity with the Euro (FXE) soon?

A: Europe is bad but they’re not going to raise interest rates anymore. However, they’re not going to cut them either because they’re already at zero. You need rising rates to see a stronger currency and the fact that the U.S. stopped raising rates is an argument for the Euro to go higher.

Q: Are we about to settle into a fading Volatility Index (VIX) environment for the rest of the year?

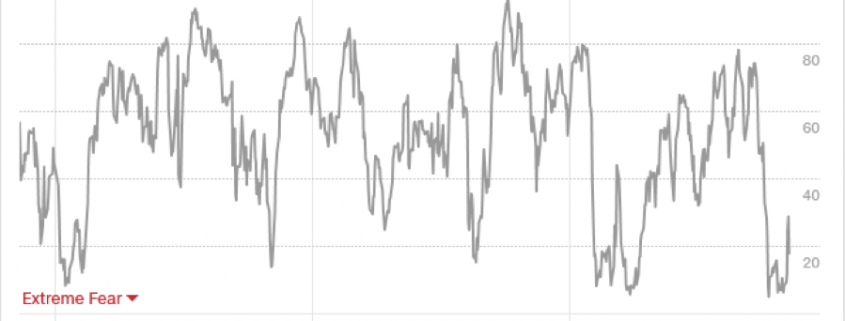

A: No, we are not; the (VIX) has been fading for 6 weeks. We’re approaching a bottom with the (VIX) here at $15, and the next big move in will probably be to the upside. The market has gotten WAY too complacent.

Q: Which are the most worrisome signals you see in the U.S. economy right now?

A: Weak earnings and sales guidance from all U.S. companies going forward and the immense jump in jobless claims last week as well as the ever-exploding amounts of government debt. Did I mention the trade war with China and the next government shutdown? Traders have a lot on their plate right now.

Q: How far will Lam Research (LRCX) go?

A: We’ve just had a massive 46% move up, so I wouldn’t chase it up here. However, long term there is still an easy double in this stock. They’re tied in with the semiconductor companies; NVIDIA, Advanced Micron Devices (AMD) and Micron Technology (MU) all trade in a group and may take one more run at the lows. Short term it’s overbought, long term it’s a screaming buy.

Q: Will the ag crisis feed into the main economy?

A: It could. All ag storage in the country is full, so farmers are putting the new harvest under tarps where it is rotting away and then claiming on their insurance. If you add another harvest on top of that it will be a disaster of epic proportions. China is America’s largest ag customer. It took decades of investment to develop them a client, and they are never coming back in their previous size. The trust is gone. Bankruptcies are at a ten-year high and that could eventually take down some regional banks which in turn hurt the big banks. However, ag is only 2% of the US economy, so it won’t cause the next recession. It’s really more of a story of local suffering.

Q: If you give out stop and not filled at stop price, when and how do you adjust to exit?

A: I would quickly enter it and if you’re not done quickly move it down five cents. If you don’t get done, do it again. There is no way to know where the real market is in until you put in a real order. There are 11 different option exchanges online and they are changing prices every millisecond. Furthermore, spread trades can get one leg done on one exchange and the second leg done on another, so prices can be all over the place.

Q: What data goes into the Mad Hedge Market Timing Index and how do you use it to time the markets?

A: It uses a basket of 30 different indicators which constantly changes according to what generates the highest return in a 30 year backtest. It includes a lot of conventional data points, like moving averages and RSIs, along with some of our own internal proprietary ones. When we are getting a reading below 20, we are looking to buy. Any reading over 65 and we are looking to sell, and over 80 we will only go short. It works like a charm. It paid for my new Tesla! I hope this helps.

Global Market Comments

February 4, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or FROM PANIC TO EUPHORIA),

(SPY), (TLT), (AAPL), (GLD),

What a difference a month makes!

In a mere 31 days, we lurched from the worst December in history to the best January in 30 years. Traders have gone from lining up to jump off the Golden Gate Bridge to ordering Dom Perignon Champaign on Market Street.

However, not everything is as it appears. The suicide prevention hotline on the bridge has been broken for years, and you can now pick up Dom Perignon at Costco for only $120 a bottle.

Clearly, investors are enjoying the show but are keeping one eye on the exit. Perhaps that’s why gold (GLD) hit an 8-month high as nervous investors Hoover up a downside hedge against their long positions.

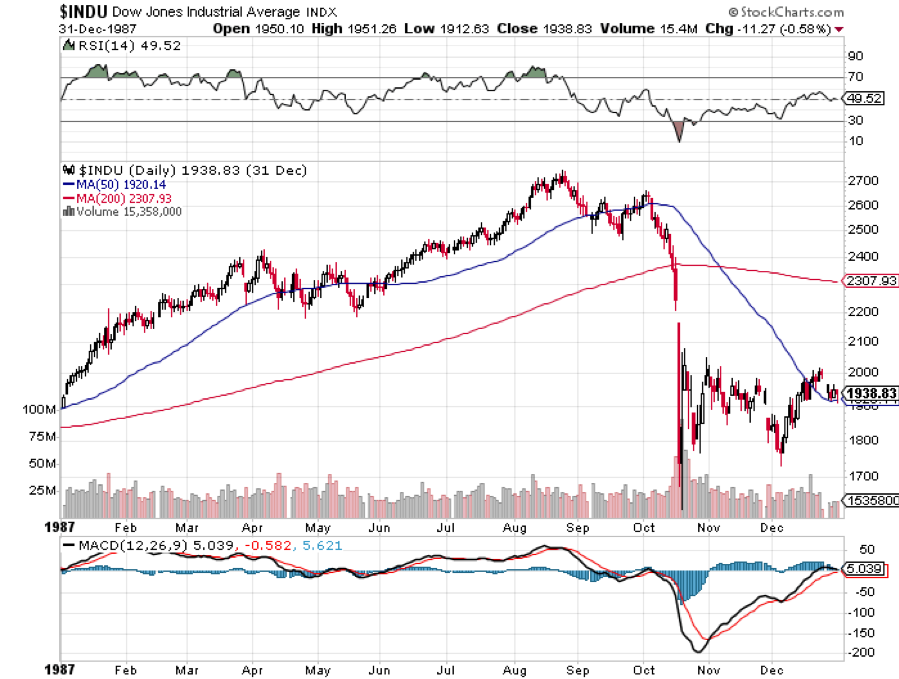

In fact, it has been the best January since 1987, with a ferocious start. The problem with that analogy is that I remember what followed that year (see chart below). After a robust first nine months of the year, the Dow Average (INDU) broke the 50-day moving average. It looked like just another minor correction and a buying opportunity.

The market ended up plunging 42% in weeks including a terrifying 20% capitulation swan dive on the last day. I tried actually to buy the stock at the close that day. The clerk just burst into tears and threw the handset on the floor. I didn’t get filled. Since the tape was running two hours late, NOBODY got filled on any orders entered after 12:00 PM.

It doesn’t help that markets have been rising in the face of a collapsing earnings picture. Look at the chart below and you’ll see that after peaking out at an annualized 26% a year ago in the wake the passage of the new tax bill, earnings have been rolling over like the Bismarck on their way to zero.

If you own stocks anywhere in the world, this chart should have made the hair on the back of your neck stand up. It’s almost as if the tax bill was delivering the OPPOSITE of its intended outcome.

How multiple expansion will we get in the face of fading earnings? How about none? How about negative!

A totally red-hot January Nonfarm payroll Report on Friday at 304,000 confirmed that the economy was still alive and well, at least on a trailing basis. Headline Unemployment Rate rose to 4.0%.

The Labor Department said that the government shutdown had no impact on the numbers because federal employees were furloughed and not unemployed. Tomato, tomahto.

However, 175,000 workers were laid off in the private sector and that is why the Unemployment Rate ticked up to a multi-month high. Noise from the shutdown is going to be affecting all data for months.

That’s also why part-time workers jumped 500,000 in January. A lot of federal employees started working as Uber drivers and pizza delivery guys to put food on the table without a paycheck.

Further confusing matters was the fact that December was revised down by 90,000.

Leisure & Hospitality led the way with 74,000 new jobs, followed by Construction with 52,000 and Health Care by 42,000 jobs.

The shutdown is over, but how much did it cost us? Standard & Poor’s says $6 billion but the restart costs will be greater. More recent estimates run as high as $11 billion.

Weekly Jobless Claims were up a stunning 53,000, to 253,000, an 18-month high. While government workers can’t claim, their private subcontractors can, hence the massive shutdown-driven jump.

Bitcoin hits a new one-year low at $3,400. Some $400 billion has gone to money Heaven since 2017. Only $113 billion in market capitalization remains. I told you it was a Ponzi scheme. US coal production hits a 39-year low as it is steadily replaced by natural gas and solar. Could there be a connection? Talk about data mining.

Earnings were mixed, with some companies coming out hero’s, others as goats.

Apple (AAPL) slightly beat expectations with revenues at $84.31 billion versus $83.97 billion expected, and earnings at $4.18 per share versus $4.17 expected. Guidance going forward is very cautious of a slowing China.

Good thing I saw the ambush coming and covered my short two days ago. A penny beat is the most managed earnings I have ever seen. To warn about earnings and then surprise to the upside is classic Tim Cook.

December Pending Home Sales cratered, down 2.2% in December and 9.8% YOY. Despite the dramatically lower mortgage interest rates, buyers fled the crashing stock market.

“PATIENCE” is still the order of the day at the Federal Reserve with its Open Market Committee Meeting ordering no interest rate rise. It was a trifecta for the doves. The free pass for stocks continues. That’s why I covered all my shorts starting from last week. Even a blind squirrel occasionally finds an acorn.

Tesla reported another profit for the second consecutive quarter, and the company is about to reach escape velocity. Model 3 production in 2019 is to reach 75% of the total output and we can expect a new pickup truck. A second factory in Shanghai will take the “3” to over a half million units a year. That $35,000 Tesla is just over the horizon.

Why are all major companies reporting good earnings but cautious guidance? Are they reading the newspapers, or do they know something we don’t? Not a great sign of a continuing bull market. Sell the next capitulation top.

This week was a classic example of how the harder I work, the luckier I get, and I have been working pretty hard lately.

I came out of a near money Apple (AAPL) put spread at cost, then rolled into a far money put spread just before the stock sold off. That little maneuver made me $1,030 in two days.

Then, I spotted a perfect “head and shoulders” top in the bond market set up by a three-point rally in the (TLT). When the red hot January Nonfarm Payroll report printed the next day at 5:30 AM PCT, bonds immediately gave back a full point.

It was all enough to boost my performance to a new all-time high after a hiatus of two months. Those who recently signed up for my service must think that I am some kind of freakin' genius! They’ll learn the truth soon enough.

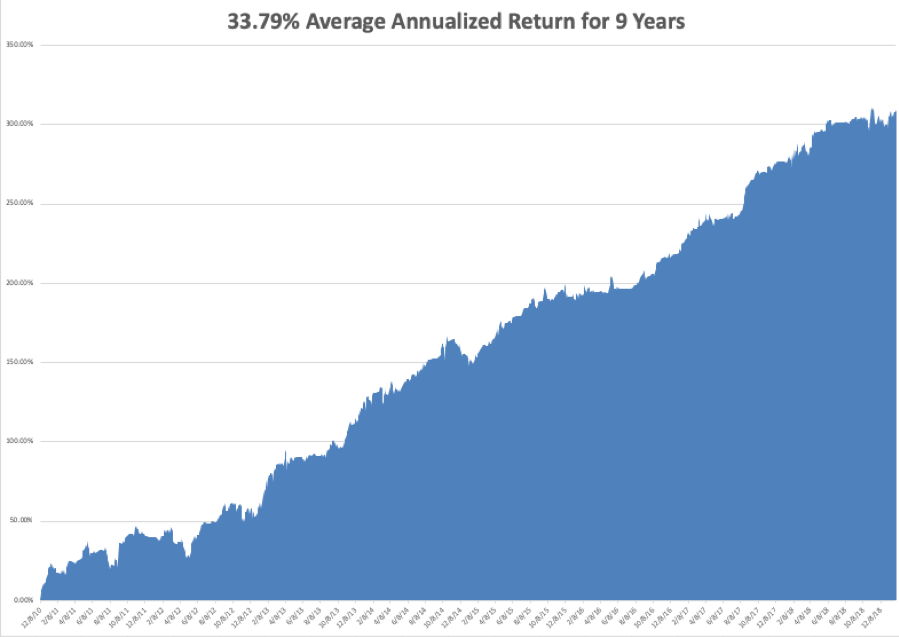

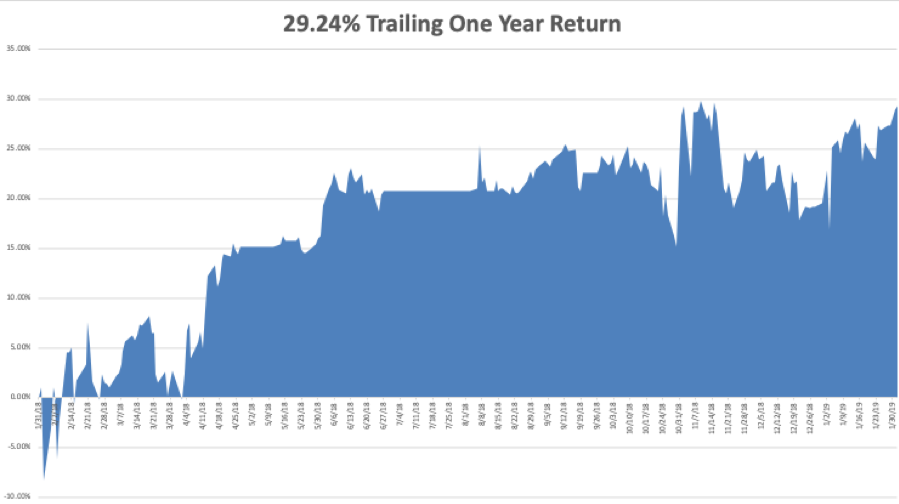

My January and 2019 year-to-date return soared to +9.66%, boosting my trailing one-year return back up to +29.24%. The is my hottest start to a New Year in a decade. Sometimes you have to make a sacrifice to the trading gods to get rewarded and that is what December was all about.

My nine-year return climbed up to +309.80%, a new pinnacle. The average annualized return revived to +33.79%.

I am now 80% in cash, short the bond market, and short Apple.

The upcoming week is still iffy on the data front because of the government shutdown. Some government data may be delayed and other completely missing. Private sources will continue reporting on schedule. All of the data will be completely skewed for at least the next three months. You can count on the shutdown to dominate all media until it is over.

Jobs data will be the big events over the coming five days along with some important housing numbers. We also have several heavies reporting earnings.

On Monday, February 4 at 10:00 AM, we get the much delayed December Factory Orders. Alphabet (GOOGL) reports.

On Tuesday, February 5, 10:00 AM EST, we learn the January ISM Non-Manufacturing Index.

On Wednesday, February 6 at 8:30 AM EST, the November Trade Balance is published.

Thursday, February 7 at 8:30 AM EST, we get Weekly Jobless Claims. December Consumer Credit follows at 9:30 AM and should be a humdinger. Intercontinental Exchange (ICE) reports.

On Friday, February 8, at 10:00 AM EST, Wholesale Inventories are out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’ll be sitting down with a case of Modelo Negro and a big bag of Cheetos to watch the commercials during the Super Bowl with my family. (My dad played for USC Varsity in 1948). I never forgave the Rams for defecting from Los Angeles, and Boston is too far away to care about.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 31, 2019

Fiat Lux

Featured Trade:

(MARKET GETS A FREE PASS FROM THE FED),

(SPY), ($INDU), (TLT), (GLD), (FXE), (UUP),

(APPLE SEIZES VICTORY FROM THE JAWS OF DEFEAT),

(AAPL)

When the Oxford English Dictionary considers the Word of the Year for 2019, I bet “PATIENCE” will be on the short list.

That was the noun that Federal Reserve governor Jerome Powell had in mind when describing the central bank's current stance on interest rates.

Not only did Powell say he was patient, he posited that the Fed was currently at a neutral interest rate. The last time he opened on this matter four months ago, the neutral rate was still 50 basis point higher, suggesting that more rate hikes were to come.

What a difference four months makes! The last time Powell spoke, the stock market crashed. Today, he might as well fire a flare gun signaling the beginning of a stampede by investors.

The Dow ($INDU) average at one point gained 500 points. Lower rates for longer term meant that bonds took it on the kisser. And gold (GLD) absolutely loved it as they now have less competition from interest-bearing instruments.

The US dollar (UUP) was taken out to the woodshed and beaten senseless paving the way for a nice pop in the euro (FXE). Even oil (USO) took the cue as cheaper interest rates mean a stronger global economy that will drink more Texas tea.

I believe that the Fed move today will definitely take a retest of the December 24 lows off the table for the time being. Now, if we can only get rid of that damn trade war with China, it will be off to the races for risk in general and stocks specifically.

Global Market Comments

January 29, 2019

Fiat Lux

Featured Trade:

(RISK CONTROL FOR DUMMIES),

(SPY), (AMZN), (TLT), (CRM), (VXX)

There is a method to my madness, although I understand that some new subscribers may need some convincing.

Whenever I change my positions, the market makes a major move or reaches a key crossroads, I look to stress test my portfolio by inflicting various extreme scenarios upon it and analyzing the outcome.

This is second nature for most hedge fund managers. In fact, the larger ones will use top of the line mainframes powered by $100 million worth of in-house custom programming to produce a real-time snapshot of their thousands of positions in all imaginable scenarios at all times.

If you want to invest with these guys feel free to do so. They require a $10-$25 million initial slug of capital, a one year lock up, charge a fixed management fee of 2% and a performance bonus of 20% or more.

You have to show minimum liquid assets of $2 million and sign 50 pages of disclosure documents. If you have ever sued a previous manager, forget it. The door slams shut. And, oh yes, the best performing funds are closed and have a ten-year waiting list to get in. Unless you are a major pension fund, they don’t want to hear from you.

Individual investors are not so sophisticated, and it clearly shows in their performance, which usually mirrors the indexes less a large haircut. So, I am going to let you in on my own, vastly simplified, dumbed down, seat of the pants, down and dirty style of risk management, scenario analysis, and stress testing that replicates 95% of the results of my vastly more expensive competitors.

There is no management fee, performance bonus, disclosure document, lock up, or upfront cash requirement. There’s just my token $3,000 a year subscription fee and that’s it. And I’m not choosy. I’ll take anyone whose credit card doesn’t get declined.

To make this even easier, you can perform your own analysis in the excel spreadsheet I post every day in the paid-up members section of Global Trading Dispatch. You can just download it and play around with it whenever you want, constructing your own best case and worst-case scenarios. To make this easy, I have posted this spreadsheet on my website for you to download by clicking here.

Since this is a “for dummies” explanation, I’ll keep this as simple as possible. No offense, we all started out as dummies, even me.

I’ll take Mad Hedge Model Trading Portfolio at the close of October 29, the date that the stock market bottomed and when I ramped up to a very aggressive 75% long with no hedges. This was the day when the Dow Average saw a 1,000 point intraday range, margin clerks were running rampant, and brokers were jumping out of windows.

I projected my portfolio returns in three possible scenarios: (1) The market collapses an additional 5% by the November 16 option expiration, some 15 trading days away, falling from $260 to $247, (2) the S&P 500 (SPY) rises 5% from $260 to $273 by November 16, and (3) the S&P 500 trades in a narrow range and remains around the then current level of $260.

Scenario 1 – The S&P 500 Falls 5%

A 5% loss and an average of a 5% decline in all stocks would take the (SPY) down to $247, well below the February $250 low, and off an astonishing 15.70% in one month. Such a cataclysmic move would have taken our year to date down to +11.03%. The (SPY) $150-$160 and (AMZN) $1,550-$1,600 call spreads would be total losses but are partly offset by maximum gains on all remaining positions, including the S&P 500 (SPY), Salesforce (CRM), and the United States US Treasury Bond Fund (TLT). My Puts on the iPath S&P 500 VIX Short Term Futures ETN (VXX) would become worthless.

However, with real interest rates at zero (3.1% ten-year US Treasury yield minis 3.1% inflation rate), the geopolitical front quiet, and my Mad Hedge Market Timing Index at a 30 year low of only 4, I thought there was less than a 1% chance of this happening.

Scenario 2 – S&P 500 rises 5%

The impact of a 5% rise in the market is easy to calculate. All positions expire at their maximum profit point, taking our model trading portfolio up 37.03% for 2018. It would be a monster home run. I would make back a little bit on the (VXX) but not much because of time decay.

Scenario 3 – S&P 500 Remains Unchanged

Again, we do OK, given the circumstances. The year-to-date stands at a still respectable 22.03%. Only the (AMZN) $1,550-$1,600 call spread is a total loss. The (VXX) puts would become nearly a total loss.

As it turned out, Scenario 2 played out and was the way to go. I stopped out of the losing (AMZN) $1,550-$1,600 call spread two days later for only a 1.73% loss, instead of -12.23% in the worst-case scenario. It was a case of $12.23 worth of risk control that only cost me $1.73. I’ll do that all day long, even though it cost me money. When running hedge funds, you are judged on how you manage your losses, not your gains, which are easy.

I took profit on the rest of my positions when they reached 88%-95% of their maximum potential profits and thus cut my risk to zero during these uncertain times. October finished with a gain of +1.24. By the time I liquidated my last position and went 95% cash, I was up 32.95% so far in 2018, against a Dow average that is up 2% on the year. It was a performance for the ages.

Keep in mind that these are only estimates, not guarantees, nor are they set in stone. Future levels of securities, like index ETFs, are easy to estimate. For other positions, it is more of an educated guess. This analysis is only as good as its assumptions. As we used to say in the computer world, garbage in equals garbage out.

Professionals who may want to take this out a few iterations can make further assumptions about market volatility, options implied volatility or the future course of interest rates. And let’s face it, politics was a major influence this year.

Keep the number of positions small to keep your workload under control. Imagine being Goldman Sachs and doing this for several thousand positions a day across all asset classes.

Once you get the hang of this, you can start projecting the effect on your portfolio of all kinds of outlying events. What if a major world leader is assassinated? Piece of cake. How about another 9/11? No problem. Oil at $150 a barrel? That’s a gimme.

What if there is an Israeli attack on Iranian nuclear facilities? That might take you all of two minutes to figure out. The Federal Reserve launches a surprise QE5 out of the blue? I think you already know the answer.

Now that you know how to make money in the options market, thanks to my Trade Alert service, I am going to teach you how to hang on to it.

There is no point in being clever and executing profitable trades only to lose your profits through some simple, careless mistakes.

So I have posted a training video on Risk Management. Note: you have to be logged in to the www.madhedgefundtrader.com website to view it.

The first goal of risk control is to preserve whatever capital you have. I tell people that I am too old to lose all my money and start over again as a junior trader at Morgan Stanley. Therefore, I am pretty careful when it comes to risk control.

The other goal of risk control is the art of managing your portfolio to make sure it is profitable no matter what happens in the marketplace. Ideally, you want to be a winner whether the market moves up, down, or sideways. I do this on a regular basis.

Remember, we are not trying to beat an index here. Our goal is to make absolute returns, or real dollars, at all times, no matter what the market does. You can’t eat relative performance, nor can you use it to pay your bills.

So the second goal of every portfolio manager is to make it bomb proof. You never know when a flock of black swans is going to come out of nowhere, or another geopolitical shock occurs, causing the market crash.

I’ll also show you how to use my Trade Alert service to squeeze every dollar out of your trading.

So, let’s get on with it!

To watch the Introduction to Risk Management, please click here.