I will be evacuating the City of San Francisco upon the completion of this newsletter.

The smoke from the wildfires has rendered the air here so thick that it has become unbreathable. It reminds me of the smog in Los Angeles I endured during the 1960s before all the environmental regulation kicked in. All Bay Area schools are now closed and anyone who gets out of town will do so.

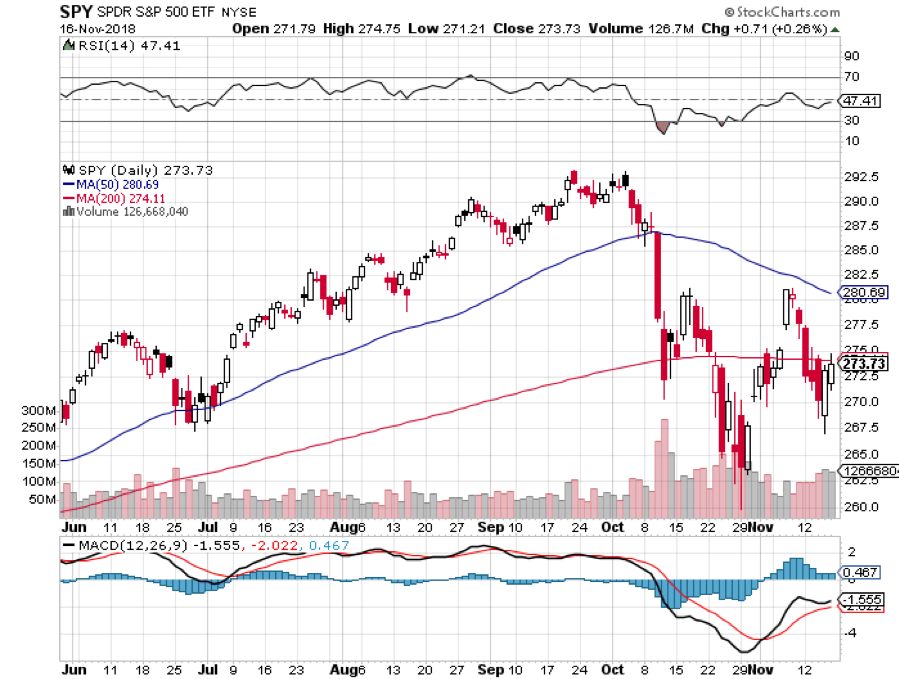

There has been a mass evacuation going on of a different sort and that has been investors fleeing the stock market. Twice last week we saw major swoons, one for 900 points and another for 600. Look at your daily bar chart for the year and the bars are tiny until October when they suddenly become huge. It’s really quite impressive.

Concerns for stocks are mounting everywhere. Big chunks of the economy are already in recession, including autos, real estate, semiconductors, agricultural, and banking. The FANGs provided the sole support in the market….until they didn’t. Most are down 30% from their tops, or more.

In fact, the charts show that we may have forged an inverse head and shoulders for the (SPY) last week, presaging greater gains in the weeks ahead.

The timeframe for the post-midterm election yearend rally is getting shorter by the day. What’s the worst case scenario? That we get a sideways range trade instead which, by the way, we are perfectly positioned to capture with our model trading portfolio.

There are a lot of hopes hanging on the November 29 G-20 Summit which could hatch a surprise China trade deal when the leaders of the two great countries meet. Daily leaks are hitting the markets that something might be in the works. In the old days, I used to attend every one of these until they got boring.

You’ll know when a deal is about to get done with China when hardline trade advisor Peter Navarro suddenly and out of the blue gets fired. That would be worth 1,000 Dow points alone.

It was a week when the good were punished and the bad were taken out and shot. Wal-Mart (WMT) saw a 4% hickey after a fabulous earnings report. NVIDIA (NVDA) was drawn and quartered with a 20% plunge after they disappointed only slightly because their crypto mining business fell off, thanks to the Bitcoin crash.

Apple (AAPL) fell $39 from its October highs, on a report that demand for facial recognition chips is fading, evaporating $170 billion in market capitalization. Some technology stocks have fallen so much they already have the next recession baked in the price. That makes them a steal at present levels for long term players.

The US dollar surged to an 18-month high. Look for more gains with interest rates hikes continuing unabated. Avoid emerging markets (EEM) and commodities (FCX) like the plague.

After a two-year search, Amazon (AMZN) picked New York and Virginia for HQ 2 and 3 in a prelude to the breakup of the once trillion-dollar company. The stock held up well in the wake of another administration antitrust attack.

Oil crashed too, hitting a lowly $55 a barrel, on oversupply concerns. What else would you expect with China slowing down, the world’s largest marginal new buyer of Texas tea? Are all these crashes telling us we are already in a recession or is it just the Fed’s shrinkage of the money supply?

The British government seemed on the verge of collapse over a Brexit battle taking the stuffing out of the pound. A new election could be imminent. I never thought Brexit would happen. It would mean Britain committing economic suicide.

US Retails Sales soared in October, up a red hot 0.8% versus 0.5% expected, proving that the main economy remains strong. Don’t tell the stock market or oil which think we are already in recession.

My year-to-date performance rocketed to a new all-time high of +33.71%, and my trailing one-year return stands at 35.89%. November so far stands at +4.08%. And this is against a Dow Average that is up a miniscule 2.41% so far in 2018.

My nine-year return ballooned to 310.18%. The average annualized return stands at 34.46%. 2018 is turning into a perfect trading year for me, as I’m sure it is for you.

I used every stock market meltdown to add aggressively to my December long positions, betting that share prices go up, sideways, or down small by then.

The new names I picked up this week include Amazon (AMZN), Apple (AAPL), Salesforce (CRM), NVIDIA (NVDA), Square (SQ), and a short position in Tesla (TSLA). I also doubled up my short position in the United States US Treasury Bond Fund (TLT).

I caught the absolute bottom after the October meltdown. Will lightning strike twice in the same place? One can only hope. One hedge fund friend said I was up so much this year it would be stupid NOT to bet big now.

The Mad Hedge Technology Letter is really shooting the lights out the month, up 8.63%. It picked up Salesforce (CRM), NVIDIA (NVDA), Square (SQ), and Apple (AAPL) last week, all right at market bottoms.

The coming week will be all about October housing data which everyone is expecting to be weak.

Monday, November 19 at 10:00 EST, the Home Builders Index will be out. Will the rot continue? I’ll be condo shopping in Reno this weekend to see how much of the next recession is already priced in.

On Tuesday, November 20 at 8:30 AM, October Housing Starts and Building Permits are released.

On Wednesday, November 21 at 10:00 AM, October Existing Home Sales are published.

At 10:30 AM, the Energy Information Administration announces oil inventory figures with its Petroleum Status Report.

Thursday, November 22, all market will be closed for Thanksgiving Day.

On Friday, November 23, the stock market will be open only for a half day, closing at 1:00 PM EST. Second string trading will be desultory, and low volume.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I'd be roaming the High Sierras along the Eastern shore of Lake Tahoe looking for a couple of good Christmas trees to chop down. I have two US Forest Service permits in hand at $10 each, so everything will be legit.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/11/John-Thomas-Ax.png375522MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-19 03:06:042018-11-19 02:57:54The Market Outlook for the Week Ahead, or Mass Evacuation

If you thought software week at the Mad Hedge Technology Letter was over, you were absolutely wrong.

I have done my best to offer a barrage of cloud-based software stocks with monstrous upside potential that would put any other industry companies six feet under.

Silicon Valley software companies have access to quinine in a mosquito-infested market – digitally savvy talent.

This talent is the best and brightest the world has to offer, and they want to work for a dominant company that gets it.

Much of this involves companies with bright futures, career opportunities galore, solving deep-rooted problems, all applying a treasure trove of data and a mountain of capital your rich uncle would giggle at.

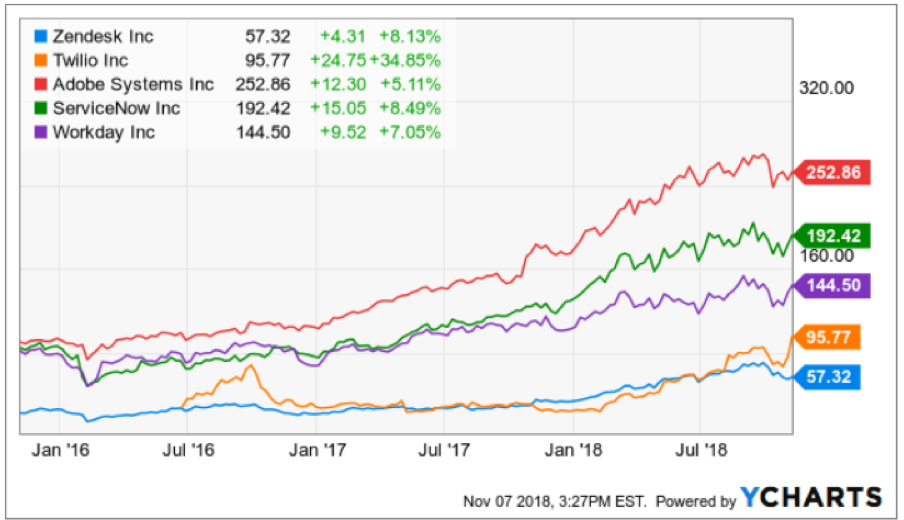

In the short term, I have been succinctly rewarded by my software picks with communication software Twilio (TWLO) rocketing upward 35% intraday at the time of this writing from when I recommended it just a few days ago.

Another Mad Hedge Technology Letter recommendation Zendesk (ZEN), a software company solving customer support tickets across various channels, is up a tame 10% after the election.

All in all, I would desire readers to access due caution as the volatility can bite you badly with crappy entry points, but the upside cannot be denied.

The turbocharged price action means the pivot to software with its new best friend, the software as a service (SaaS) pricing model, encapsulates the outsized profits this industry will rake in going forward.

Without further ado, I’d like to slip in two more companies rounding out a robust quintet of software companies – I bring to you Workday (WDAY) and Service Now (NOW).

Workday is a software company based on a critical component of every successful company – human resources.

Unsurprisingly, human resources are tardy to this wave of software modernization.

Sensibly, companies have chosen short-term software fixes that drive profits with instant success rather than to update its human resource department’s processes.

Big mistake.

I would argue that getting the right people in the doors is paramount and can save substantial time because of the wasted time rooting out toxic employees who weren’t suitable fits.

Ultimately, I have concluded the worst-case scenario entails the enterprise resource planning market stagnating driving minimal growth to the cloud, however, this minimal growth would be substantial enough for Workday to outperform.

The landscape as of now only involves several vendors with a competitive (SaaS) solution auguring well for Workday allowing them to capture a further chunk of market share.

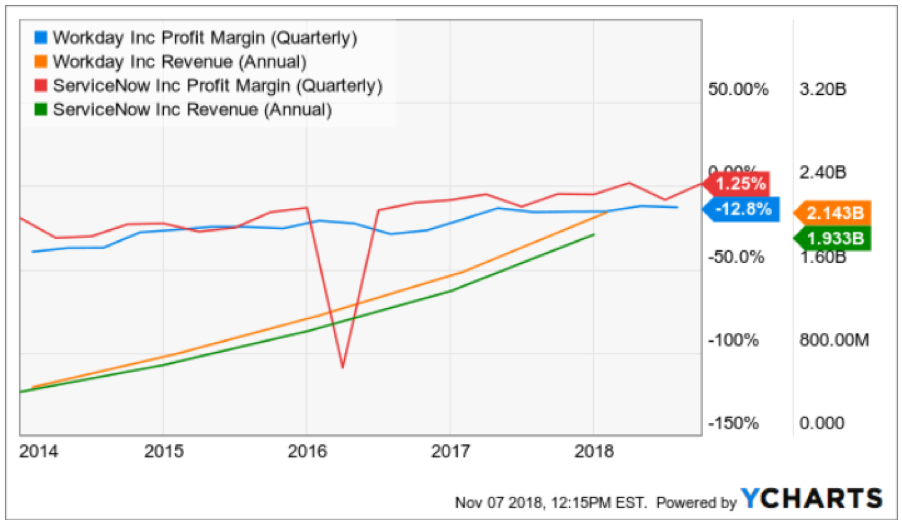

Workday’s growth metrics back up my thesis with its businesses posting a 3-year EPS growth rate of 291% and a 3-year sales growth rate of 36%, painting a picture of a company that will turn profitable in the next few years.

They can even showboat their glittering array of heavy-hitting customers who purchase their software that include Walmart (WMT), Target (TGT), and Bank of America (BAC).

The one headwind tarnishing these types of software companies is the stock-based compensation awarded to employees.

SBC rose 21% YOY and is slightly worrying in an otherwise stellar company. This method of compensation only works when the stock is rising and is a major issue for new Facebook (FB) hires who will prefer cash over its burnt-out share price.

If Workday doesn’t whet your appetite, then how about sampling a main dish of ServiceNow.

This company completes technology service management tasks offering a centralized service catalog for workers to request technology services or information about applications and processes that are being used in the system.

Admirably, this software helps IT workers fix IT system problems which in this day and age is useful considering the bottleneck of chaos many tech and non-tech companies face.

And more often than not, the chaos inundates the in-house IT departments causing the whole business to go offline.

Putting out digital fires is a perpetual business that will never flame out.

As websites and enterprise systems become more complicated, a bombardment of errors are prone to crop up and instant remedies are crucial to carrying out businesses in a time sensitive manner.

Even ask the best tech company in the universe Amazon (AMZN), whose move off Oracle’s (ORCL) database software was the ultimate reason for a serious outage in one of its biggest warehouses on this past Amazon Prime Day, according to Amazon’s internal documents.

The faux paux underscores the hurdles Amazon and other companies could face as they seek to move completely off the Oracle legacy database software whose development has stayed relatively stagnant for a generation.

The slipup was minutes and snowballed into excruciating hours on Amazon Prime Day resulting in over 15,000 delayed packages and roughly $90,000 in wasted labor costs.

Crikey!

These numbers didn’t even consider the wasted man-hours spent by developers troubleshooting and solving the errors or any potential lost sales.

When these mammoth tech giants are running at an incredible scale, a small blip can result in job losses, lost revenue, lost time, a slew of IT engineer sackings, and for some smaller companies, an existential crisis.

The large-scale acts as a powerful multiplier to the lost resources and cost, and as you can see with the Amazon debacle, a few hours can make or break a developer’s career.

Fortunately, IT budgets are higher up the food chain than human resource budgets while more than inching up every year. This is the main reason why I believe ServiceNow will outperform Workday.

The proof is in the pudding and when I scrutinize various metrics, the truth is filtered out.

ServiceNow’s quarterly growth rate is 35% which is higher than Workday’s who slipped back to 28% last quarter even though the 3-year growth rate is in the mid-30%.

Put mildly, accelerating sales growth is better than decelerating sales growth.

Both companies have a market cap in the low $30 billion and almost identical annual sales in the $2 billion range.

However, ServiceNow presides over significantly higher quarterly profit margins than Workday and will achieve profitability sooner than Workday.

In short, Workday loses more money than ServiceNow.

I believe in the underlying thesis of HR modernization underpinning Workday’s rapidly growing revenue and this secular trend is here to stay.

But I much rather put my hard-earned money on a company tied to IT modernization which is imminent and harder to put on the backburner because of its strategic position at the forefront of the tech curve.

HR CAN be put on the backburner and kept analog longer, and as the economy inches closer to a recession, this expense will be shifted further away from greener pastures supported by the fact that companies decelerate hiring new talent in poor economic environments.

To wrap it up, I do believe ServiceNow is the Burmese python consuming a cow, but that doesn’t mean I am bearish on Workday.

Workday will flourish, just not as much on a relative basis as ServiceNow.

Effectively, these stocks are well placed to move higher even after the violent moves upward this year. As the economic cycle moves further into the late innings, the importance of cloud-based software companies will become magnified further.

As for the software week at the Mad Hedge Technology letter, these solid five picks will offer deep insight into one of the most compelling parts of the internet sector.

As many observers have found out, not all tech firms are created equal and that is made even trickier with the existence of the vaunted FANGs who are the real Burmese python in the current tech landscape.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-11-08 01:06:462018-11-07 17:58:08It’s All About Software, Software, Software

One of the few people who can magnify pressure on the venture capitalists of Silicon Valley is none other than Masayoshi Son.

What a ride it has been so far. At least for him.

His $100 billion SoftBank Vision Fund has put the Sand Hill Road faithful in a tizzy – utterly revolutionizing an industry and showing who the true power broker is in Silicon Valley.

He has even gone so far as doubling down his prospects by claiming that he will raise a $100 billion fund every few years and spend $50 billion per year.

This capital logically would flow into what he knows best – technology and the best technology money can buy.

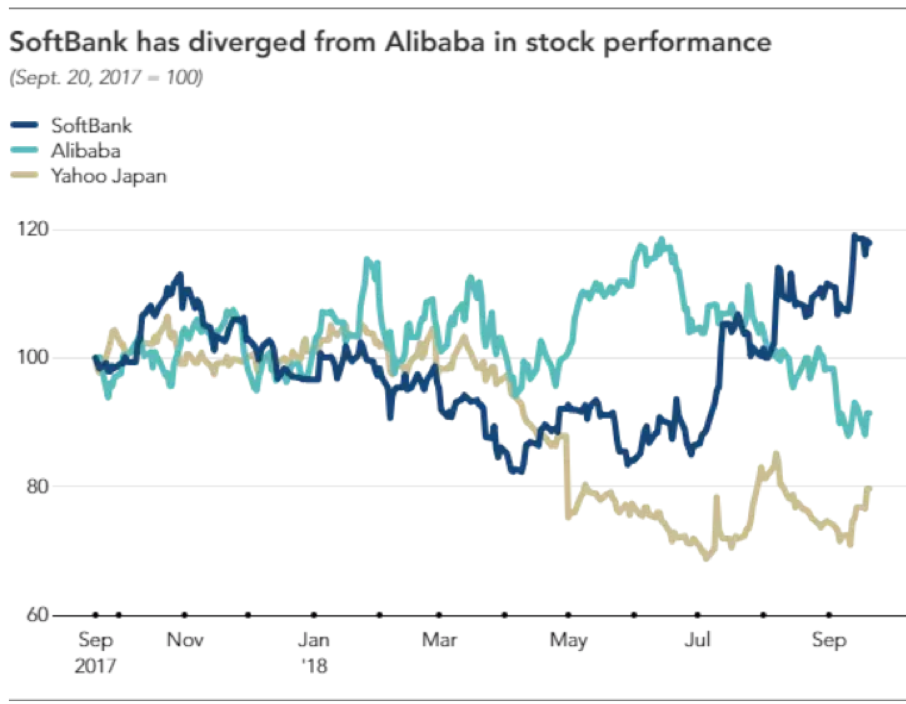

As Yahoo Japan and Alibaba (BABA) shares have floundered, SoftBank’s stock has decoupled from the duo displaying explosive brawn.

SoftBank’s stock is up 30% in the past few months and I can tell you it’s not because of his Japanese telecommunications business which has served him well until now as his cash cow.

Yahoo Japan, in which SoftBank owns a 48.17% stake, has existing synergies with SoftBank’s Japanese business, but has experienced a tumble in share price as Son turns his laser-like focus to his epic Vision Fund.

His tech investments are bearing fruit and not only that, Son revealed his Alibaba investment is about to clean up shop to the tune of $11.7 billion next year shooting SoftBank shares into orbit.

A good portion of the lucrative windfall will arrive from derivatives connected to the sale of Alibaba, and the other 60% comes from the paper profits finally realized in this shrewd piece of business.

Equally paramount, SoftBank’s Vision Fund hauled in $2.13 billion in operating profits from the April-June quarter underscoring the effectiveness of Masayoshi Son’s tech ardor.

Son said it best of the performance of the Vision Fund saying, “Results have actually been too good.”

So good that after this June, Son changed his schedule to spend 3% of his time on his telecom business down from 97% before June.

His telecommunications business in Japan has turned into a footnote.

It was the first quarter that Son’s tech investments eclipsed his legacy communications company.

Son vies to rinse and repeat this strategy to the horror of other venture capitalists.

The bottomless pit of capital he brings to the table predictably raises the prices for everyone in the tech investment world.

Son’s capital warfare strategy revolves around one main trope – Artificial Intelligence.

He also strictly selects industry leaders which have a high chance of dominating their field of expertise.

Geographically speaking, the fund has pinpointed America and China as the best sources of companies. India takes in the bronze medal.

Unsurprisingly, these two heavyweights are the unequivocal leaders in artificial intelligence spearheading this movement with the utmost zeal.

His eyes have been squarely set on Silicon Valley for quite some time and his record speaks for himself scooping up stakes in power players such as Uber, WeWork, Slack, and GM (GM) Cruise.

Other stakes in Chinese firms he’s picked up are China’s Uber Didi Chuxing, China’s GrubHub (GRUB) Ele.me and the first digital insurer in China named Zhongan International costing him $500 million.

Other notable deals done are its sale of Flipkart to Walmart (WMT) for $4 billion giving SoftBank a $1.5 billion or 60% profit on the $2.5 billion position.

In 2016, the entire venture capitalist industry registered $75.3 billion in capital allocation according to the National Venture Capital Association.

This one company is rivalling that same spending power by itself.

Its smallest deal isn’t even small at $100 million, baffling the local players forcing them to scurry back to the drawing board.

The reverberation has been intense and far-reaching in Silicon Valley with former stalwarts such as Kleiner Perkins Caufield & Byers breaking up, outmaneuvered by this fresh newcomer with unlimited capital.

Let me remind you that it was considered standard to cautiously wade into investment with several millions.

Venture capitalists would take stock of the progress and reassess if they wanted to delve in some more.

There was no bazooka strategy then.

SoftBank has thrown this tactic out the window by offering aspiring firms showing promise boatloads of capital up front even overpaying in some cases.

Conveniently, Son stations himself nearby at a nine-acre estate in Woodside, California complete with an Italianate mansion he bought for $117.5 million in 2012.

It was one of the most expensive properties ever purchased in the state of California even topping Hostess Brands owner Daren Metropoulos, who bought the Playboy Mansion from Hugh Hefner in 2016 for $100 million.

If you think Son is posh – he is not. He only fits himself out in the Japanese budget clothing brand Uniqlo. He just needed a comfortable place to stay and he hates hotels.

In August, SoftBank decided to top off the $4.4 billion investment in WeWork, an American office space-share company, with another $1 billion leading Son to proclaim that WeWork would be his “next Alibaba.”

Son continued to say that WeWork is “something completely new that uses technology to build and network communities.”

The rise of remote workers is taking the world by storm and this bet clearly follows this trend.

The unlimited coffee and beer found in the new Japanese Roppongi WeWork office that opened earlier this year was a nice touch.

WeWork plans to open 10-12 offices in Japan by the end of 2018.

Thus far, WeWork is operating in over 300 locations in over 20 countries.

Revenue is growing rapidly with the $900 million in 2017 a 12-fold improvement from 2014.

The newest addition to SoftBank’s dazzling array of unicorns is Bytedance, a start-up whose algorithms have fueled news-stream app Jinri Toutiao’s meteoric rise in China.

The deal values the company at $75 billion.

It also runs video sharing app Douyin, and overseas version TikTok.

Bytedance’s proprietary algorithm, serving to personalize streams for users, is the best in China.

They have been able to insulate themselves from local industry giants Tencent and Alibaba.

TikTok has piled up over 500 million users and brilliant investment like these is why Son revealed that the Vision Fund’s annual rate of return has been 44%.

SoftBank’s ceaseless ambition has them in the news again with whispers of investing in a Chinese online education space with a company called Zuoyebang.

China’s online education market is massive. In 2017, this industry pulled down over $33 billion in revenue, and 2018 is poised to break $55 billion.

Zuoyebang has lured in Goldman Sach’s (GS) as an investor.

This platform allows users to upload homework questions for third party assistance – the name of the app literally translates into “homework help.”

Cherry-picking off the top of the heap from the best artificial intelligence companies in the world is the secret recipe to outperforming your competitors.

At the same time, aggressively throwing money at these companies has effectively frozen out any resemblance of competition. Once the competition is frozen out, the value of these investments explodes, swiftly super-charged by rapidly expanding growth drivers.

How can you compete with a man who is willing to pay $300 million for a dog walking app?

Venture capitalist funds have been scrambling to reload and mimic a Vision Fund-like business of their own, but its not easy raising $100 billion quickly.

This genius strategy has made the founder of SoftBank the most powerful businessman in the world.

Son owns the future and will have the largest say on how the world and economies evolve going forward.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/Softbank-CEO-2.png539472MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2018-10-04 09:01:392018-10-04 08:51:07How Softbank is Taking Over the US Venture Capital Business

Warren Buffett is right, retail is a tough game in the face of the Amazon (AMZN) threat.

I wouldn't want to face off with them either.

Technology has been the biggest catalyst fueling a tectonic shift in the retail climate with large cap technology players usurping market share decimating competition.

The rise of e-commerce platforms has been nothing short of spectacular.

Management has also used technology to modernize the global supply chain, in-house operations, and ramp up the hyper-targeting of prime customers.

The treasure trove of big data collected has been the key to pinpointing the weaknesses and finding solutions.

Amazon knew all of this before everybody else. And, Jeff Bezos has already annihilated a large swath of the retail community that will never return.

Walmart was one of the first retailers to wipe out the small brick-and-mortar shops, and Amazon is attempting to do what Walmart did to others in the past.

Luckily, the sleeping giant of Walmart (WMT) has awoken and is laying the groundwork to launch a full-frontal assault on Amazon.

Better late than never.

More than 90% of Walmart's customers live within a 15-minute drive of one of their stores, but why drive 15 minutes with exorbitant gas prices when Amazon says you don't have to?

Once a laggard, Walmart is now instilling its newfound e-commerce operation with a new sense of zeal and purpose, offering Amazon a real threat and copying its best ideas such as two-day free shipping.

Someone must stand up to Amazon. And Walmart with its massive embedded base of loyal and fervent customers and revenue is the ideal challenger.

Currently, Amazon has extracted more than 49% of the U.S. e-commerce market in 2018.

Walmart trails Amazon by a wide margin, and the investment into developing its e-commerce business will boost the 3.7% e-commerce market share.

If Walmart maintains the drive to enhance tech operations, its e-commerce division could double its market share to more than 7.5% from its low base.

This is entirely manageable as it would only need to convert a small percentage of current non-digital customers into using its digital portals whose quality has remarkedly improved the past few years.

Redesigning the official website was timely as the new interface is sleeker, more functional than past versions, and just plain better.

There is even a tinge of Amazon in the design borrowing the best parts of its foe's design and integrating it into a modern look.

The statement of intent is there, and Amazon won't have a frictionless pathway to profits anymore.

Walmart CEO Doug McMillon has been the main man to ramp up the tech side of the business and has injected a fresh batch of youth into the management style.

Online purchases only comprise less than 20% of sales and that runway is still long and wide for a company that has only barely scratched the surface of its tech strategy.

Most tech companies are in the first innings of a long game, but Walmart is even further behind meaning there is ample room to grow.

Even McMillon believes that Walmart will morph into a certain "kind of technology company" going forward.

Not only is it beefing up its digital commerce strategy, but physical stores are getting makeovers to extract additional marginal revenue from each customer.

Walk into your nearest Walmart and you might notice it looks completely different than your father's Walmart.

It is also dabbling a bit with augmented reality to boost the in-store customer experience.

Walmart has installed an avalanche of self-checkout kiosks at the front of the store to ease and quicken customer payment.

The use of big data analytics is now aiding decisions on how to best create the optimal shopping environment for its customers.

In-store pickup automated machines called towers help customers in picking up their goods if they choose to drive to the physical store, thereby enhancing the customer service quality.

Walmart is no longer playing defense and sticking to what it knows.

It is on the front foot and should be.

Walmart announced e-commerce sales spiked 40% YOY in Q, and the man responsible for this execution is Marc Lore.

Who is Marc Lore?

Marc Lore is the chief executive officer of Walmart eCommerce U.S., and the showdown against Amazon is a personal gripe for him.

Lore joined Walmart when his e-commerce company Jet.com was snapped up for $3.3 billion in 2016.

This was more of a talent and expertise grab that Walmart needed at the time to learn the ropes of the e-commerce business to better understand how to respond to Amazon.

Before Jet.com and Walmart, Lore was on the books at Bezos' Amazon.com where his feud began.

Lore joined Amazon by way of his e-commerce company Quidsi, which he cofounded and which was bought by Amazon for $545 million in 2011.

Following Amazon's purchase, Lore and Bezos did not always see eye to eye on how Quidsi would operate inside the confines of Amazon, creating long-lasting tension that has turning into bad blood.

Quidsi specialized in certain genres such as baby products and household goods. After Amazon sucked all the knowledge and life out of Quidsi, it fired the remaining 260 employees at its New Jersey headquarters and closed down the firm.

Bezos cited "unprofitability" for shuttering Quidsi, and the thinly veiled parting shot at Lore registered deeply inside the back of his mind.

Lore reinvented himself and launched a new e-commerce business called Jet.com.

After being absorbed by Walmart, Lore was repositioned to the top of Walmart's e-commerce division leading the helm.

Lore understands how to take on Amazon after working inside its Seattle headquarters for years after the Quidsi integration and knows how to beat the company at its own game.

He is the perfect person to help Walmart infuse success into its e-commerce division. Walmart is the optimal platform for Lore to get revenge against Jeff Bezos.

A win-win proposition.

Walmart e-commerce business is on track to rise 40% in 2018.

A few changes he set off right away were the expansion of Walmart's online selection adding more than 1,100 brands, setting up a creative discount program attracting more shoppers into physical stores, cooperating with Google to integrate voice-activated shopping mechanisms, and signing up a new in-house brand called Bonobos to design an exclusive portfolio of brands mirroring Amazon's 76 private labels on its platform.

Lore even took a page out of Amazon's playbook and made two-day free shipping possible for millions of products through its website.

Warren Buffett has said in the past that not investing in Amazon and not investing more in Walmart when he had the chance were two of his most regrettable mistakes.

It could be true that this time around Buffett jumped the gun in unloading his Walmart shares. I agree that retail can be scary, but not all retail is created equal.

For some particular retailers such as Walmart, the future doesn't look so bad.

I agree with Buffett that Walmart has more than tough competitors, but if Walmart emphasizes its digital first strategy via mobile and desktop, there is a lot of wiggle room to harvest gains from these positive changes.

Walmart has been used to growing 1% to 2% in U.S. same-store sales per year, and it was habitually assumed as a constant.

The growth of 4.5% proves that tech investments are paying dividends and even though margins are pressured, it's a must to stay competitive.

If Walmart can lure in growth investors who believe in the evolving tech narrative, it would expand the variety of investors interested in Walmart.

Walmart has a lot going for them and sometimes that gets lost around all the hoopla about the Amazon threat.

Walmart has the mind-boggling scale retailers dream of and migrating its own customers online is the key to unlocking new value.

Certainly, these customers will purchase more products after algorithms identify the products customers desire to buy.

Margins will suffer somewhat from this new strategy, but growing pains and reinvestment are sorely needed to turn around the ship.

Luckily, this legacy retailer is on the right path and has hit on the right strategy.

Once the technology is running efficiently, the average revenue per user will start to rise as with for all top-tier technology companies because of leveraged scale making it possible to boost profits.

In addition, there is potential digital ad business to nurture along if Walmart can shift a decent number of legacy customers to mobile or desktop platforms.

The future doesn't look so bleak for Walmart, neither does its share price.

"We will compete with technology, but win with people." - said CEO of Walmart Doug McMillon.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-20 01:05:212018-08-20 01:05:21Is Walmart the Next Amazon?

In its latest earnings report for Q2 2018 Netflix definitely disappointed. Revenues came in at $3.91 billion compared to an expected $3.94 billion. New subscribers came up short 1 million of those expected.

It also provided weaker guidance, expecting to ad only 5 million new subscribers versus an earlier expected 6 million, with most coming from international.

The stock market noticed, taking the shares from $420 down to $330, a loss of 21.42%. Is it time to bail on Reed Hasting's miracle firm? Or is it time to load the boat once again?

If you have any doubts just ask any former employee of Blockbuster. In 1997, Blockbuster was the 800-pound gorilla in the VHS video rental business, with 9,000 worldwide, a 31% market share, and a $5 million market capitalization.

Today, Blockbuster has only one store left somewhere in rural Alaska. There is but one company to blame for this turn of events, and that would be Netflix.

Not only did Blockbuster bite the dust, so did the entire $8 billion-a-year movie rental industry, including Movie Gallery, Hollywood Video, and the rental operations of Walmart (WMT) and Amazon (AMZN).

That year, Reed Hastings returned his rental of the video Apollo 11 a month late and was hit with a huge $40 late charge. He was struck with a bolt of lightning. "There must be a business opportunity here," he thought.

The next day, he and friend Marc Randolph bought an oversized greeting card, tossed the card, and mailed a CD in the remaining envelope to Hastings' house. It arrived the next day in perfect condition. It was a simple matter of geometry. While the CD sat in the middle of the envelope, the Post Office only stamped the corners. This simple experiment became the basis of a business that eventually grew to $186 billion.

Yes, and now you're all thinking, "Why didn't I think of that?"

Hastings was the scion of an East Coast patrician family, a member of the social register and a regular in the New York Times society pages. His great-grandfather, Alfred Lee Loomis, was an early quant who made a fortune.

He received his undergrad degree from Bowdoin College and then joined the Peace Corps. Following a two-year stint in Swaziland to teach math, Hastings then obtained a master's degree in Computer Science from Stanford University in 1988.

Hastings founded his first firm at the age of 30, Pure Software, which went public in 1995. It then merged with Atria Software in 1996 and as Pure Atria was acquired in 1997. That left him flush with cash and looking for new challenges.

Based on the successful mail experiment Hastings invested $2 million into the Netflix idea, which Marc Randolph ran for the first two years.

Netflix then become the lucky beneficiary of a number of sea changes in technology then underway, none of which it anticipated. Sales of DVD players were taking off. The Internet and online commerce were gaining respectability, and massive overinvestment in broadband led to exponential improvements in streaming speeds.

There was also a crucial Supreme Court decision regarding the Copyright Act of 1909 that protected the right to rent a video that you owned. Hollywood had been fighting rentals tooth and nail to protect their substantial profits from DVD sales.

Hastings assembled a team of former colleagues who managed to build a website and a primitive distribution system. The Netflix website went live on April 14, 1998. The site crashed within 90 minutes, overwhelmed by demand. A rushed trip to the nearest Fry's Electronics brought 10 more PCs, which were quickly wired in as servers. By the end of the first day, Netflix had rented 500 videos.

The DVD optical format first launched in March 1997, creating the DVD player industry. Sales reached 400,000 units by the first half of 1998 and prices collapsed, from $1,100 to $580 in the first year. Netflix was swept up in the tide and monthly revenues reached $100,000 within four months.

Since newly released titles were so expensive at $15, Netflix focused on older, niche films in anime, Chinese martial arts, Bollywood movies, and, yes, soft-core porn. Netflix later exited this market when Hastings accepted an appointment to the California State Board of Education.

The company thrived. The headcount rose from an initial three to more than 100. But it was losing money - some $11 million in 1998.

Then the company caught a major break. The French luxury goods tycoon, Bernard Arnault, CEO of LVMH, was desperate to get into the Dotcom Boom and invested $30 million in Netflix. This attracted another $100 million from other venture capitalists and angel investors.

This allowed the company to experiment with its business model. It launched next-day delivery in San Francisco, which proved wildly popular, new sign-ups, renewals, and customer loyalty soared. Then in a stroke of genius Netflix initiated its Marquee Program, which allowed customers to rent four DVDs a month for only $15.95 a month, with no late fees. DVD player sales in 1999 reached 6 million, but Netflix lost $29.8 million that year.

In 2000, the Marquee Program evolved into the Unlimited Movie Rental service and the price rose to $19.95. It included a free rental, which customers could obtain by entering their credit card data, which then renewed indefinitely. This is common now but was considered wildly aggressive in 2000. Netflix was also an early artificial intelligence user, using algorithms to find movies that both members of a couple would like based on past rental data.

Netflix is a company that did 100 things wrong, any one of which could have wiped out the firm. It was the few things it did right that led it to stardom.

Hastings worked out deals with manufacturers to include a free Netflix rental coupon with every DVD player sold. The move earned it valuable market share, but almost bled the company dry since most didn't return. But a labeling error caused hard-core Chinese porn discs to get sent out instead.

A programing glitch caused members' video queues to be sent out all at once, landing some happy subscribers with 300 videos all at once. Coupon counterfeiting was rife until the company began individually coding each one.

Netflix planned to go public in 2000. Existing shareholders rushed to top up their holdings in expectation of cashing in on a first-day pop in the share price. But the Dotcom Crash intervened, and all new tech IPOs were canceled for years. This episode of greed and attempt at insider trading left Netflix well-funded through the following recession. Netflix lost $57.4 million in 2000.

In the meantime, the installed base on DVD players reached 8.6 million by 2002. Then disaster struck. Hastings learned that Amazon was entering the DVD sales market, the only source of Netflix profits. Hastings flew up to Seattle to sell Netflix to Amazon. But Jeff Bezos only offered $12 million and Hastings walked. It was a rare miss for Bezos. DVD players dropped to $200, and demand for content soared.

An important part of the Netflix story was the self-destruction of industry leader Blockbuster. Hastings offered to sell Netflix to Blockbuster at the bargain price of $50 million. By then, Netflix had 300,000 paid subscribers compared to Blockbuster's 50 million. But Blockbuster charged late fees while Netflix didn't. That difference would change the world. However, CEO John Antioco passed believing that online commerce was nothing more than a passing fad. It was a disastrous decision.

To dress up the company's financials for an IPO in 2002, Hastings fired about 40% of the company's workforce to cut costs. On May 23, 2002, Reed Hastings stood on the floor of wealth manager Merrill Lynch as the stock started trading on NASDAQ under the ticker symbol of (NFLX) at $15 a share. The company raised another $82.5 million in the deal. A year later Netflix announced it had 1 million paid subscribers, and the stock soared to $75 and the stock later split 2 for 1.

Realizing his error, Blockbuster's Antioco launched an all-out effort to catch up with Netflix in online rentals. When that news hit the market, (NFLX) shares fell back to its IPO price of $15. Late in 2004, Blockbuster launched a clunky copy of the Netflix website, but without the magical algorithms in the backend that made it work so well. Blockbuster undercut Netflix on price by $2, offering memberships for $17.95. It immediately captured 50% of all new online sign-ups but continued with its notorious late fees.

Blockbuster Online was plagued with software glitches from the start and every day presented a new crisis. Netflix also fought back with its own price cut, to $17.99. Both companies bled money. Short sellers started accumulating big positions in Netflix stock. Hastings vowed to run Blockbuster out of the online market with a $90 a quarter ad spend.

This Netflix received some manna from heaven. Corporate raider Carl Icahn secretly accumulated a chunk of Blockbuster stock in the market and then demanded that the company pursue an asset stripping strategy. Icahn eventually obtained three board seats and became de facto CEO. So, to say that management time was distracted was a gross understatement.

Netflix received another gift when Walmart finally threw in the towel for online movie rentals. Hastings jumped in and did a deal whereby (WMT) would refer all future movie rental customers to Netflix.

Blockbuster finally decided to dump its despised late fees, costing it $400 million in annual revenues. Hundreds of stores were closed to cut costs. The downward spiral began. The value of Blockbuster fell to $684 million. With 4.2 million subscribers Netflix was now worth about $1.5 billion. Blockbuster lost an eye-popping $500 million in 2005.

DVD sales and rentals reached their all-time peak of $27 billion in 2006. Slightly more than 50% of Americans then had broadband access.

Blockbuster, growing weary of the competition from Netflix, finally decided to deliver a knockout blow. It launched its Total Access program in another attempt to bleed Netflix to death by undercutting Netflix's membership price by $2. It worked, and Netflix was facing another near-death experience. Blockbuster Online's share of new subscriptions soared to 70%, and total subscribers soared from 1.5 million to 3.5 million in months. The Netflix share fell to only 17%, and the company was now losing money for the first time in years.

In a last desperate act, Netflix offered to buy Blockbuster Online for $600 billion, and would have gone up to $1 billion just to eliminate the competition. An overconfident Blockbuster, smelling blood, refused. Movie Gallery and Hollywood Video were already on the bankruptcy trail, so why shouldn't Netflix go the same way?

And then the inexplicable happened. Icahn refused to pay Antioco a promised $7 million performance bonus based on the Blockbuster Online success. Instead, he offered only $2 million and Antioco resigned, collecting an $8 million severance bonus in the process. Icahn replaced him with Jim Keyes, the former CEO of 7-Eleven.

Keyes immediately pulled the plug on the Total Access discount, thus dooming Blockbuster Online. Instead, he ordered that the company's 6,000 remaining stores sell Slurpees and pizzas to return to profitability, in effect turning them into 7-Elevens that rented videos. It was one of the worst decisions in business history. Many of the senior staff resigned and sold their stock on hearing this news. Keyes in effect seized defeat from the jaws of victory.

Reinvigorated and with subscriptions soaring once again, Netflix launched headlong in online streaming. It introduced its set top box, Roku, in 2008. It then got Microsoft to offer Netflix streaming through its Xbox 360 game console that Christmas, instantly adding potentially10 million new subscribers.

And this is what makes Netflix Netflix. Although the company had the best recommendation engine in the industry, CineMatch, Hastings thought he could do better. So, in 2006, he offered a $1 million prize to anyone who could improve Cinematch's performance by 10%. To facilitate the competition, he made public the data on 100 million searches carried out by the firm's customers.

It was the largest data set put in the public domain. Some 40,000 teams in 186 countries entered the contest, including the best artificial intelligence and machine language and mathematical minds. It became the most famous scientific challenge of its day.

After a heated three-year struggle, a team named BellKor's Pragmatic Chaos won, a combination of three teams from Bell Labs, Hungary, and Canada. The copyright for the algorithm is owned by AT&T and licensed to Netflix for a fixed annual fee. AT&T also uses the winning algorithm for its own U-verse TV programming.

When the 2008 financial crisis hit, Netflix subscribers just kept on rising at the rate of 10,000 a day as consumers stayed at home and obtained cheaper forms of entertainment. Total subscriptions topped 10 million in 2009. Those at Blockbuster cratered. A new competitor appeared on the scene, Redbox, with 20,000 supermarket kiosks offering DVDs for 99 cents a day. But Netflix was hardly affected.

By 2012, Netflix subscriptions reached 20 million. Streaming was a blowout success, with half of its customers using streaming only to watch TV shows and movies. Hollywood beat a path to Hastings' door, with Paramount Pictures, Lionsgate, and MGM earning a collective $800 million in Netflix fees. Netflix now accounted for 60% of movies streamed and 20% of total broadband usage.

When Blockbuster finally declared Chapter 11 bankruptcy on September 23, 2010, so did its Canadian operations. That opened the way for Netflix to enter the international market, picking up 1 million new subscribers practically overnight. Next it launched into Latin America, introducing Spanish and Portuguese streaming in 43 countries.

As streaming replaced DVD rental by mail, Hastings attempted to spin off the rump of the business into a firm called Quickster. Customers would now have to open two accounts, one for streaming and one for mail and pay high prices. Customers and shareholders rebelled, taking the stock from $305 down to a heartbreaking $60. This was the last chance you could buy the stock at a decent price.

Hastings recanted on Quickster and let go the 200 staff applied to the unit. Icahn made a reappearance in this story, this time accumulating a 10% share in Netflix. After demanding management changes nothing happened, and Icahn eventually sold his shares for a large profit. Finally, Icahn made money in the video business.

Going forward, Netflix's strategy is finally straightforward. Create a virtuous circle whereby superior content attracts new subscribers, who then deliver the money for better content.

CineMatch knows more about what you want to watch than you do. The immense data it is generating gives Netflix not only the insight on how to sell you the next movie, it also proves unmatched insight into trends in the industry as a whole. It also makes Netflix unassailable in the movie industry.

That has given the firm the confidence to double its original content budget from $4 billion to $8 billion this year to produce Emmy-winning series such as House of Cards and Orange is the New Black.

So, the future for Netflix looks bright. As for me, I think I'll spend the rest of the evening watching the 1931 version of Frankenstein on Netflix.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2018-08-02 01:06:312018-08-29 13:33:44What's Next for Netflix?

Please be advised there will be no Technology Letter

Thursday, August 2, or Friday August 3,

as Editor Arthur Henry will be traveling.

Publication will resume Monday, August 6.

Thank you for your understanding.

Mad Hedge Technology Letter August 1, 2018 Fiat Lux

Featured Trade: (THE RACE DOWN TO ZERO), (SCHW), (FB), (WMT), (AMZN), (FFIDX), (BOX)

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.