Mad Hedge Technology Letter

May 30, 2019

Fiat Lux

Featured Trade:

(IS TARGET THE NEXT FANG?)

(TGT), (AMZN), (WMT)

Mad Hedge Technology Letter

May 30, 2019

Fiat Lux

Featured Trade:

(IS TARGET THE NEXT FANG?)

(TGT), (AMZN), (WMT)

This is the Mad Hedge Technology Letter finding you the best technology recommendations and sometimes, they come from unpredictable sources.

Retail and the digitization of this industry has made this area one of the biggest recipients of technology through the e-commerce portals such as Amazon (AMZN) and its competitors.

I have gone on record saying that Walmart is the next FANG and I do stand by that assertion.

Another company nipping at the heels of Walmart (WMT) and vying to become the next tech gamechanger is Target.

Target (TGT) has made all the right moves in all the right places by hyper digitizing their own operations, so much so, that it has morphed straight into the firing line of Silicon Valley and its commercial interests.

The first quarter marked Target’s eighth consecutive quarter of comparable sales increases.

Comparable sales growth of 4.8% exceeded even the most outlandish expectations.

There has been a positive response to Target’s same-day digital fulfillment services which was a response in large part to their competitor Amazon.

The fulfillment operations drove well over half of digital sales growth in the quarter.

The crucial ability to offer these same-day services, which delivers customers a high level of satisfaction, is a result of a carefully orchestrated strategy to put stores in the center of fulfillment.

In fact, Target stores handled more than 80% of the first quarter digital volume, including all of the same-day options combined with digital orders shipped directly from stores to guests’ homes.

The first quarter performance was also stronger than expected, up against an expectation for a rate decline, operating margins increased about 20 basis points in the quarter.

This performance reflected the precision of disciplined expense control tied with a favorable mix of digital fulfillment meaning that first quarter earnings per share grew more than 15% at the top end of the guidance range.

The clear outperformance occurred from multiple drivers, including strong holiday performance in the Valentine's Day and Easter periods, along with the powerful everyday traffic in the Food, Beverage, and Essential categories.

Target’s customers are responding passionately, driving rapid growth of the same-day options, including Drive-Up, and in-store pickup.

Perusing recent results, last year’s tariffs passed with minimal carnage and Target has put in motion contingency plans this time around to mitigate the impact of additional tariffs already scheduled for next month.

The China trade war does pose a serious potential drag on margins, and if e-commerce gets hit with higher cost of goods, then not only will Target feel the torture, but so will the likes of Amazon and Walmart.

Geopolitical risk is the main burden holding back the broad market, and the price action has reflected the increasing risk that the trade war will destroy earnings growth and become a strong catalyst for an equity reset.

This is the main reason why I cannot say with utter conviction to buy the company today.

In a top down world, the issues at the top take precedent and investors must absorb this.

Ultimately, Target’s growth strategy entails building and rolling out a comprehensive set of digital fulfillment capabilities, allowing them to provide customers with a convenient fulfillment option for every shopping journey.

As a result of those efforts, Target now offers more digital fulfillment options across more of the country than anyone else in retail.

When customers are planning on being out and about, they can shop on their digital device and Target is able to deliver their order in an hour or two.

Target offers in-store pickup in every one of the 1,851 locations, and Target even walks the order out to the parking lot in more than 1,250 stores.

There are no fees for either of the same-day options.

Shipt, the same-day grocery delivery service acquired by Target last year, offers unlimited free same-day delivery from Target and more than 50 other retailers across the country for $99 annual fee.

A portion of Target’s digital orders are and will continue to be shipped from upstream fulfillment centers. And other items will continue to be shipped directly by other vendors.

Target has effectively transitioned into the Amazon style fulfillment center strategy based on speed and scale.

Target is on track to grow digital sales by more than $1 billion in 2019 and fulfilling even higher percentages of this volume from in-house stores.

Using stores as digital hubs enhances Target’s speed and reduces cost, and importantly, moving to store fulfillment does not increase the frequency of split shipments.

In fact, even though store fulfillment continues to grow rapidly, the rate of split shipments this year is running lower both in Target stores and in total compared with last year.

This allowed management to enhance customers experience which can be seen by repeat business.

There are essentially only three e-commerce companies that have taken full advantage arming themselves with a wicked fulfillment center operation – Amazon, Walmart, and Target.

Other retailers that either do not have the capital to scale, and the resources to digitize will continue to lose business because they simply can’t provide the same quality of customer experience these trio offer.

The financials reflect the great success Target is experiencing today.

Over the last 2 years, earnings results have beaten EPS estimates 63% of the time and have beaten revenue estimates 88% of the time.

Target has taken some apparel market share away from the mall group with comp sales up 4.8% when consensus was 4.2%.

Digital sales were up 42% year-over-year in Q1 signaling that the success or failure of digitizing a business is the x-factor in 2019.

That trend could perpetuate this summer, with Target executives convinced today that the company's brand-new partnership with Vineyard Vines is already one of the most successful in its history.

Digital purchases that originate online now represent 7.1% of Target’s total transactions, up from 5.2% a year ago showing how the digital business is making even deeper inroads each year.

Total revenue was up 5% to $17.63 billion from $16.78 billion last year, smashing estimates of $17.52 billion.

These three e-commerce companies will be the ones standing when the dust settles, and unluckily, there will be some periods when geopolitics and other macroeconomic issues overwhelm the individual stock story.

All else being equal, Target is a smart long-term hold and this firm is in the first innings of a massive digital transformation.

I am confident they will overdeliver on the rest of their annual financial targets.

“If you go back to 1800, everybody was poor. I mean everybody. The Industrial Revolution kicked in, and a lot of countries benefited, but by no means everyone.” – Said Founder of Microsoft Bill Gates

Mad Hedge Technology Letter

May 29, 2019

Fiat Lux

Featured Trade:

(CHINA TO BAN FEDEX)

(HUAWEI), (AMZN), (FDX), (UPS), (DPSGY), (BABA), (ZTO)

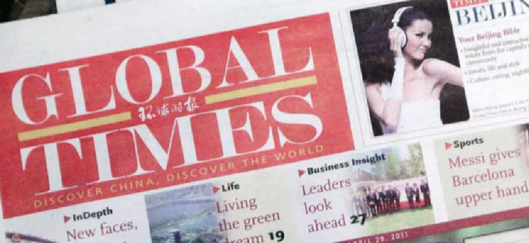

Sell any and all rallies in FedEx (FDX) – that’s my quick takeaway from the Chinese communist party publishing a sharp retort to their de-facto mouthpiece of a publication called the Global Times signaling FedEx’s imminent demise in greater China.

The Global Times is often used as thinly veiled statements to a wider global audience and mimics the ideology of the ruling communist party and their main positions on critical issues.

As regards to FedEx’s business in China, it said:

“There are rising calls for China's postal service regulator to cut off FedEx from China market, as Huawei has accused the US express courier of diverting and rerouting its packages.”

FedEx is crushing the Chinese logistics market currently and is the go-to carrier holding firm at 54.6% market share.

They have been around in China for as long as the economic boom has percolated inside the mainland from 1984, far before any of its local competitors were even up and running by a decade or two.

FedEx’s latest acquisition of Dutch-based TNT Express in 2016 solidified its dominance.

Foreign competition is a mainstay of international shipping patterns in China with the top three rounded out by DHL (DPSGY) with a 25.07% market share and United Parcel Service (UPS) with a 16.94% market share.

If these assertive claims do result in FedEx meaningfully losing China revenue, UPS wouldn’t stand to pick up the leftovers and could be put out to pasture by the same issue of hailing from a country that has an active adversarial economic policy against China’s.

If anyone would benefit, it would by DHL, given that Germany has a far less hawkish stance towards China, and they are unwilling to bite off the hand that feeds them.

The current situation is a concerning sign for the future of Germany as an industrial power and ability to sustain itself against China Inc.

It could be somewhat true that Germany has overextended themselves and only time, Made in China 2025 project, and the mood of the Chinese communist party can delay the inevitability of full tech hegemony over their western European counterpart.

The communist party could choose to just bypass DHL altogether and kick out all foreign invaders gifting courier responsibilities to Alibaba-based (BABA) subsidiaries and the likes of ZTO Express (ZTO) who provide express delivery and other value-added logistics services in China.

DHL will hope that China delays any draconian measures and pray that its active partnership with a local logistic firm has real legs.

DHL's revenue sharing agreement with SF Express does not preclude them from the anger of Chinese regulators, but the risk of Chinese regulators favoring local couriers has risen another 25%.

Playing by the rules goes a long way in China, even if they change every day, and for customers across DHL’s target audience of industries including technology, health care, retail, automotive, and e-commerce.

DHL CEO Frank Appel said, "Combined with our global operations standards and network support, the agreement provides a solid foundation to continue exploring further opportunities in China in the coming years."

From an outside perspective, this sounds more like forced cooperation with forced technology transfers with the mainland companies slurping up Germany tech knowhow.

Doing a deal with the devil for access to a 1.3 billion customer market is being put through the ringer.

When I view the snippets through the lens of geopolitics, it’s hard to believe that at such a sensitive time, FedEx would actively “reroute” packages and knowingly approved this behavior, they simply can’t be that clumsy.

The situation smells like an overt show of nationalism by a group of individuals, and it questions the longevity of FedEx operating in China all the same.

FedEx promptly responded confessing:

“We regret that this isolated number of Huawei packages were inadvertently misrouted.”

An unintentional mistake offered a golden opportunity to tie the logistics company to the U.S. government’s aggressive nature and going forward FedEx will remain in a shroud of mystery until investors can get further grips on the rates of growth of their Chinese operations.

If FedEx were afraid about this, then they must be tearing their hair out about the domestic behemoth that is Amazon (AMZN) and their desires to install a full-service logistic service to blanket FedEx from e-commerce deliveries.

This has been the initial premise of my short call on FedEx, which has proved correct, and the regulatory nightmare in China will cast another cloud around its business.

Any strength in FedEx shares will be met with a cascade of selling activity, and as the economy slows down because of tariff-induced headwinds, this is a stock to outright short.

Back to China, FedEx slashed its full-year profit forecast for the second time in three months after reporting weaker-than-expected third quarter earnings.

The Chinese economy is absolutely slowing down, and its effects are impacting surrounding Asian nations.

Manufacturing cuts will cause the number of courier packages to slide in China and there is no telling how bad this trade stand-off could get.

It doesn’t look good for FedEx, and I reiterate my short stance on the company.

“It must be pointed out that Huawei package incident either shows the incredibly poor quality of FedEx's service or that FedEx is playing a very disgraceful role.” – Said the Global Times of China

Mad Hedge Technology Letter

May 28, 2019

Fiat Lux

Featured Trade:

(CHINA’S RARE EARTH WEAPON)

(TSLA), (AAPL), (LMT), (BAESY), (RTN)

There are many ways to describe the trade war the U.S. administration finds itself in.

Many experts have chimed in too categorizing it as a fight for technological supremacy.

There are many different ways to skin a cat.

I’ll tell you what is really going on.

Above all else, this logjam has more to do with a battle for resources, and more specifically, rare earth elements that power the devices, cars, and gadgets that many westerners have become accustomed to.

Let’s make no bones about it, Beijing has cornered the rare earth’s market spanning from assets in the Congo and the cobalt that is produced there to supply on their own turf forcing the U.S. to be reliant on China for about 85% of its rare earth supply.

In other words, the rare earth industry in China is a large industry that is important to Chinese internal economics.

Rare earths are a group of elements on the periodic table with similar properties.

The elements are also critical to national governments because they are used in the defense industry for top-secret weaponry.

Permanent magnets can be used for several applications including serving as essential components of weapon systems and high-performance aircraft such as drones.

China has touted their own state-owned companies to reach deep into this market and make it their own.

The results are visible to the entire world and China gaining a stranglehold on these valuable inputs will have lasting consequences.

Rare earth metals are made up of 17 elements — lanthanum, cerium, praseodymium, neodymium, promethium, samarium, europium, gadolinium, terbium, dysprosium, holmium, erbium, thulium, ytterbium, lutetium, scandium, and yttrium.

U.S. companies will need to start developing new supply channels in other markets and Australia could allow U.S. companies' lifelines in securing the orders they need to function as a company.

Military companies important to national security devour these types of precious metals and Raytheon Co (RTN), Lockheed Martin Corp (LMT) and BAE Systems (BAESY) all produce sophisticated missiles with these elements powering their guidance systems, and sensors.

These traded companies’ shares could be in for short-term turbulence if China decides to pull the rug out from underneath banning Chinese companies doing business with American companies, or by slapping on tariffs to respond to the tariffs on Chinese imports.

California's Mountain Pass mine is the sole US rare earth facility with a caveat.

The owner of the mine ships over 50,000 tons of rare earth concentrate for processing in China, meaning that it will be harder than first thought to strip China out of the process.

China and America are in the first stages of a massive decoupling.

Not only smartphone operating systems will be affected with Huawei announcing it will roll out its own in-house operating system after Google announced that they will pull its apps and use of the Android system off of Huawei’s phone, but almost anything of significant value from an Ivy league computer engineering degree to electric cars will be retrenched on each side.

This is terrible news for Tesla (TSLA), and they could be hit next by the Chinese communist party if they deem electric cars integral to national security because of the data and sensors that deliver precious information back to Silicon Valley.

Tesla is in the midst of building a Gigafactory in Shanghai and their growth strategy is solely focused on China.

China standing up to the U.S. is a blunt force way of saying that nobody will dictate to the Chinese their future prospects except themselves.

They feel after 35 years of economic super growth, they should be granted with the options of choosing their destiny.

Huawei will feel the repercussions of these detrimental policies with their European business a big question going forward.

Germany was always a large bullseye for the Chinese government and scooping up robotic centerpiece Kuka, was a smash and grab in broad daylight.

The sleeping giant of Germany has woken up and is on the offensive after allowing the Chinese unfettered access for a generation.

Risks are high in Germany and they could be the first industrial power to be gutted and left behind the woodshed by China Inc and the CCP.

The U.S. faces a conundrum in that the method in which aided China’s rise of forced technology transfers and IP theft can only be stopped if actively removed, meaning we are headed for a game of chicken with the other side hoping the other side blinks first.

The market fallout will be deep and wide-ranging with the most movement in technology companies that are leveraged to China meaning chip companies.

But then there are the tech companies who have deeply embedded interests in China such as Apple (AAPL) whose supply chain is in the eye of the storm with Foxconn.

The worst possible case is China banning the sales of precious earth metals to the U.S. forcing the U.S. to buy from a 3rd party country which in turn would increase costs of American products.

This is what I would categorize as a hard landing and absolute decoupling.

The common denominator of this trade war is higher costs for the American consumer and mass layoffs in China – this is my base case.

However, I would argue that a rare earth's ban would not be as bad as initially thought because many consumers are tapped out with phones, tablets, and computers.

The elongated refresh cycle will not mean consumers will go without access to the internet and its services.

In terms of the stock market, this puts a wet towel on the positive momentum of early spring when the Nasdaq roared higher.

The Nasdaq could be stuck under 8,000 for the summer unless a rapprochement takes place which I would put at 30% for a structural détente and 65% for a kick the can down the road détente.

The ironic unintended consequence is the safe haven trade of buying treasuries has come back in vogue and could be a huge boon for the domestic real estate market.

This extends the bull market in properties at least another six months with lower rates allowing fresh buyers to take advantage of lower financing opportunities amid a bump in inventory.

The bull market absolutely needs the real estate market on-sides to perpetuate because of the fragile nature of this part of the late economic cycle.

I also believe that U.S. President Donald Trump will become even more brazen as stronger economic data stateside suggests he could pile on even more pressure on the Chinese communist party to coerce them into a big win that will aid him in his reelection efforts.

Let’s not forget that much of this has to do with the 2020 road back to the White House.

As it stands, corporate America has finally understood the message of moving their supply chain out of China which means mass layoffs for many Chinese particularly in the southern region around Guangzhou.

This is not a marketing charade, this trade war has teeth.

China’s Central Bank will be forced into dovish policy to help state-owned companies who many are akin to zombie companies and another relic of communism that has yet to be uprooted.

All this means debt, debt, and more debt piling up on the mainland and on American shores.

If you thought this was the time of austerity, then you are truly wrong.

The end game could be a Chinese yuan that drops like a heavy stone through the psychological threshold of $7 and on its way down to $7.50.

If this comes to pass, expect a 10% correction and a demonstrably strong U.S. dollar, Japanese yen, Swiss Franc, and a generational entry points into the equity market.

“Now there is a new long march, and we should make a new start.” – Said Chairman of China Xi Jinping

Mad Hedge Technology Letter

May 23, 2019

Fiat Lux

Featured Trade:

(ANOTHER 5G PLAY TO LOOK AT)

(EQIX), (CSCO), (GOOGL), (MSFT), (ORCL)