?The December, 1999 Green Book, the internal forecasting paper of the Federal Reserve, has a disclaimer which said ?not to be used externally, and harmful if swallowed?, said president of the Dallas Fed, Richard Fisher.

?The December, 1999 Green Book, the internal forecasting paper of the Federal Reserve, has a disclaimer which said ?not to be used externally, and harmful if swallowed?, said president of the Dallas Fed, Richard Fisher.

We received another raft of data this morning confirming my suspicion that the economic data is slowly turning over from modestly positive to mixed.

The Challenger, Grey, & Christmas report showed that there were 51,758 job cuts in February, down 3% from January. But the first two months of 2012 revealed that layoffs announced by private companies are up 18% YOY. Consumer products, transportations, and retail showed the greatest losses.? They are seeing temps are being turned into full timers, creating no net gain in employment. Government job cuts are starting to wane as well. This is definitely a mixed bag, at best.

The Department of Labor weekly jobless claims showed a modest increase, moving from 354,000, up to 8,000 to 362,000. There was a slight uptick in four week moving average which most economists prefer to track. Continuing claims rose from 3.406 million to 3.416 million. There are still a hefty 7.5 million unemployed receiving benefits. Some analysts are blaming the uptick on the end of the early spring and the return to normal winter weather.

The reason that I am regurgitating all of these numbers in excruciating detail is that this is the type of metamorphosing data flow you see before a rounding top in the stock market. Such tops spawn from data that flip from clear to muddled, putting the risk of an economic slowdown squarely on the table, and can take a few months to unfold.

The recent numbers from China, Europe, and Brazil are already screaming at us that this is the case. But hedge fund traders can be a dull lot, and sometimes must be hit in the head with a hammer several times before they get the message.

Of course, we get the big kahuna tomorrow, the February nonfarm payroll, the most closely watched economic indicator by the market. It is safe to say that the market is priced for perfection here. If it comes in line at 200,000, you could get a snore. But even the slightest disappointment could bring a repeat of Tuesday?s 200 point swoon. Check in at 8:30 EST to see if I?m right.

You Said What?

I received a flurry of inquires the other day when Ben Bernanke mention the word ?sterilization? in his recent congressional testimony. And he wasn?t giving advice to the country?s wayward teenaged girls, either.

Sterilization refers to a specific style of monetary policy. Sterilized policies seek to manipulate the money markets without changing the overall money supply. The Fed implemented just such a strategy last summer when they initiated their ?twist? policy. This involved buying 10, 20, and 30 Treasury bonds and selling short an equal amount of short term Treasury bills.

The goal here was to force investors out of the safety of Treasury bonds and into riskier assets like stocks, commodities, and real estate. Given the market action since then, I?d say that he at least partially succeeded.

Dollar for dollar there is no change in the Fed?s balance sheet when sterilized actions are undertaken, although there is a huge increase in the risk profile of their portfolio. A private institution would be insane to do this at this stage of the economic cycle, as the risk of capital loss is great. But governments are exempt from mark to market rules and can carry this paper at cost or par, whatever they want. That?s why we have a central bank.

The Fed is now running up against a unique problem. The twist program is so large that it is literally running out of short term securities to sell. When this happens, they may well resort to 28 day repurchase agreements instead, which are essentially sales of short term paper out the back door. This is what Uncle Ben was attempting to explain to our congressional leaders, which I?m sure went straight over their heads.

The really interesting thing here is why Bernanke is suddenly interested in sterilization? These are the types of polices you pursue to head off inflation. With wages continuing to fall it is difficult to see why this should be an issue.

Maybe he?s looking at the price of gasoline or the stock market instead, which have recently been going through the roof. Perhaps he?s looking several years down the road. The great challenge for the Federal Reserve from here will be unwinding their massive $2.8 trillion balance sheet it build up during the Great Recession without triggering runaway price increases.

If Bernanke does have an inkling of coming inflation it could have huge implications for a security dear to my heart, the (TBT), a leveraged ETF that benefits from falling Treasury bond prices. Although it has been flat lining for the last four months, you better keep this one on your short list. It?s just a matter of time before we get an upside breakout.

For an excellent explanation of the history of monetary sterilization, please click here.

No, Not This One

If you can pick up any emerging market with a multiple of less than 20, it is a great long term investment,? said professor Jeremy Siegel at the University of Pennsylvania Wharton School of Business.

As a potentially profitable opportunity presents itself, John will send you an alert with specific trade information as to what should be bought, when to buy it, and at what price. Read more

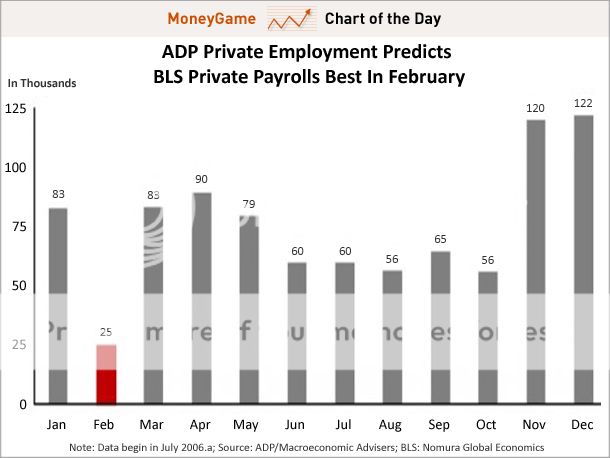

Don?t expect much market volatility until we get the February nonfarm payroll report on Friday at 8:30 EST. Consensus has them coming in at around 200,000. However, we may have just gotten a valuable preview to those figures.

According to the Japanese broker, Nomura Securities, the ADP National Employment Report, a monthly analysis of the hiring trends of 344,000 private businesses, is most aligned with the official jobs report in February. Since 2006, the average February gap is only 25,000, which is less than half of the gap of other months.

The ADP came in this morning at 216,000, and the market yawned. That presages that the Friday consensus expectation could be right. While a good number, especially coming on a series of positive monthly reports, it won?t exactly set the markets on fire. That could pave the way for a further downside test in the equity markets, as well as other risk assets, especially gold, silver, and the other metals.

You don?t want to bet the ranch on historic correlations. Still, I thought you?d like to know.

Once, an Extinct Species

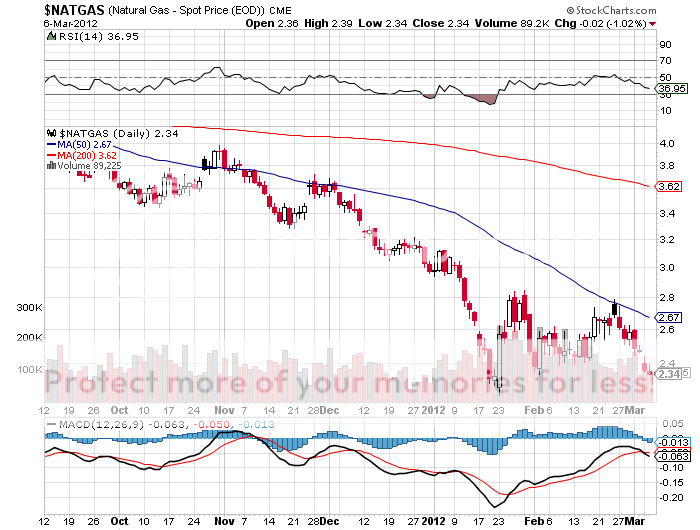

I am constantly asked if there are any ways investors can take advantage of the collapse of the natural gas market, where at $2.34/MBTU prices are plumbing decade lows. I have recently made good money buying puts on the ETF (UNG), but these are not for the faint of heart. They call this contract the ?widow maker? for a good reason.

You don?t want to touch the gas producing companies, like Chesapeake (CHK) and Devon (DVN), because prices are probably going to stay down for years. Good firms that benefit from the increased volume of gas pumped are few and far between. Unless you are a large consumer of this despised molecule, such as an electric power company or a petrochemical plant, it is tough to find a profitable niche.

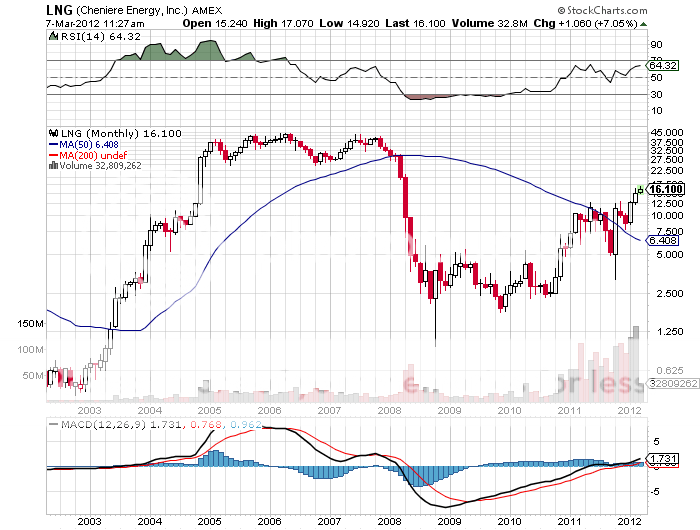

However, there is one company that delivers a narrow rifle shot that could do extremely well in coming years, and that is Cheniere Energy (LNG). I first started following (LNG) a decade ago when I was still wildcatting for CH4 in the Texas Barnet Shale.

Back when natural gas was trading at a loft $5/MBTU, Qatar invested $50 billion in in developing its own substantial gas resources. The plan was to liquefy the gas at -256 degrees Fahrenheit in the Middle East, ship it to the US in a fleet of specialized LNG carriers, and have Cheniere convert it back into gas at its Sabine River plant for distribution to an energy hungry US market through the Creole Trail pipeline. It all looked like a great plan, and (LNG) shares traded up to $45.

Then ?fracking? technology came along and blew up the entire model. The discovery of a new 100 year supply of gas under our feet caused gas prices to crash from a post Amaranth peak of $17/MBTU down to $2/MBTU. Any plans to import LNG from the other side of the world were rendered utterly worthless. Chenier?s billion dollar investment in a gasification plant was now worth only so much scrap metal. (LNG) shares plumbed low single digits as the firm flirted with bankruptcy.

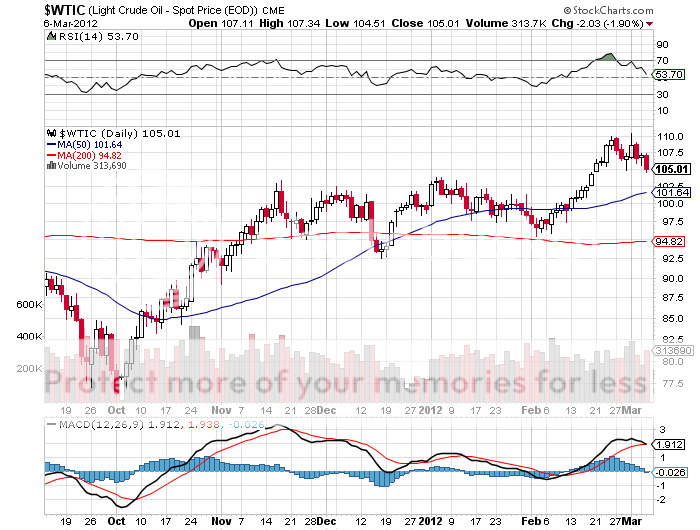

Enter China. The Middle Kingdom?s voracious demand for energy in this recovery has caused the price of oil to soar from a 2008 low of $30 to $110. Despite accounting for an overwhelming share of the world?s new energy purchases, Chinese cities are suffering from brown outs due to power shortages. This is why China is resisting immense American pressure to quit buying Texas tea from Iran.

Enter the arbitrage. While oil has been spiking, gas has been crashing. Gas is now selling at 15% of the cost of oil on an adjusted BTU basis. Another way of saying this is that you can buy oil for $16 a barrel instead of $110. It only takes a second with an abacus to understand the appeal of such a disparity.

Gas also has the additional benefits in that it is much cleaner burning than crude, lacks the sulfur and nitrogen dioxides, and produces half the carbon dioxide. That?s a big deal in Beijing where the air is so thick you can cut it with a knife on a bad day.

Enter the long term contracts. During the 1960?s and 1970?s Japan entered into huge long term contracts to buy LNG from Australia and Indonesia to feed their own economic miracle of the day. Because very expensive, hard to get or offshore supplies were tapped, the price was set at $16/MBTU. Those contacts are now expiring. Do you think they?ll renew at the old price, or go to Cheniere for the $2 stuff. Gee, let me think about that one for a bit.

Enter Fukushima. The nuclear meltdown last March prompted Japan to shut down 49 of 54 nuclear power plants that accounted for 25% of the country?s electric power generation. The brownouts that followed forced a sweltering summer on millions as the government urged consumers to shut off air conditioners to save juice. Power companies there have been scrambling to obtain conventional energy supplies, and have been a major factor in driving oil up from $75 to $100 since the fall. Cheap gas supplies from the US would meet this demand nicely.

The trigger. Last May, Cheniere got US government permission to export 2.2 billion cubic feet a day for 20 years. That would require it to convert the existing gasification plant to a liquifaction plant, something that can be done with some expensive re-engineering. It has already found several large international buyers to take delivery of the new end product. All that was missing was the money to finish the plant. My hedge fund buddies have been accumulating this stock since October, when it bottomed at $3, expecting an angel investor to appear. But it was one of those ?someday, it might happen? kind of stories better lead to long term players.

Then last week, Blackstone jumped in with a beefy $2 billion investment in Cheniere. That will enable them to obtain an additional $3 billion in debt financing needed to finish the first of two export facilities. They are now expected to come online in 2016.

How does Cheniere stack up as an investment? Frankly, it is kind of scary. The market cap is only $2 billion, and it pays no dividend. When the current spate of deals are done, it will have $5 billion in debt. The Stock has just run up from $3 to $17. And these facilities are dangerous to operate. One blew up in Texas in 1937 and killed 300 schoolchildren. As a result, local permits for these are very hard to come by.

But as you can see, a whole host of geopolitical, technology and economic strands tie together in this one company, all of which are positive for the share price. If the story comes true, as Blackstone hopes, then there could be a double or triple in the shares for the patient. To learn more about Cheniere Energy, please click here for their website at http://www.cheniere.com/default.shtml.

Did Somebody Light a Match?

?We?ve had several false starts in this recovery. People jump on the train just before it runs off the tracks. You have to be wary about that,? said a well-known economist.

My friend was having a hard time finding someone to attend a reception who was knowledgeable about financial markets, White House intrigue, international politics, and nuclear weapons.

I asked who was coming. She said Reagan?s Treasury Secretary George Shultz, Clinton?s Defense Secretary William Perry, and Senate Armed Services Chairman Sam Nunn. I said I?d be there wearing my darkest suit, cleanest shirt, and would be on my best behavior, to boot.

When I arrived at San Francisco?s Mark Hopkins Hotel, I was expecting the usual mob scene. I was shocked when I saw the three senior statesmen making small talk with their wives and a handful of others.

It was a rare opportunity to grill high level officials on a range of top secret issues that I would have killed for during my days as a journalist for The Economist magazine. I guess arms control is not exactly a hot button issue these days. I moved in for the kill.

I have known George Shultz for decades, back when he was the CEO of the San Francisco based heavy engineering company, Bechtel Corp. I saluted him as ?Captain Schultz?, his WWII Marine Corp rank, which has been our inside joke for years. Since the Marine Corps didn?t know what to do with a PhD in economics from MIT, they put him in charge of an anti-aircraft unit in the South Pacific, as he already was familiar with ballistics, trajectories, and apogees.

I asked him why Reagan was so obsessed with Nicaragua, and if he really believed that if we didn?t fight them there, we would be fighting them in the streets of Los Angeles. He replied that the socialist regime had granted the Soviets bases for listening posts that would be used to monitor US West Coast military movements in exchange for free arms supplies. Closing those bases was the true motivation for the entire Nicaragua policy. To his credit, George was the only senior official to threaten resignation when he learned of the Iran-contra scandal.

I asked his reaction when he met Soviet premier Mikhail Gorbachev in Reykjavik in 1986 when he proposed total nuclear disarmament. Shultz said he knew the breakthrough was coming because the KGB analyzed a Reagan speech in which he had made just such a proposal.

Reagan had in fact pursued this as a lifetime goal, wanting to return the world to the pre nuclear age he knew in the 1930?s, although he never mentioned this in any election campaign. As a result of the Reykjavik Treaty, the number of nuclear warheads in the world has dropped from 70,000 to under 10,000. The Soviets then sold their excess plutonium to the US, which today generates 10% of the total US electric power generation.

Shultz argued that nuclear weapons were not all they were cracked up to be. Despite the US being armed to the teeth, they did nothing to stop the invasions of Korea, Hungary, Vietnam, Afghanistan, and Kuwait.

I had not met Bob Perry since the late nineties when I bumped into his delegation at Tokyo?s Okura Hotel during defense negotiations with the Japanese. He told me that the world was far closer to an accidental Armageddon than people realized.

Twice during his term as Defense Secretary he was awoken in the middle of the night by officers at the NORAD early warning system to be told that there were 200 nuclear missiles inbound from the Soviet Union. He was given five minutes to recommend to the president to launch a counterstrike. Four minutes later, they called back to tell him that there were no missiles, that it was just a computer glitch.

When the US bombed Belgrade in 1999, Russian president, Boris Yeltsin, in a drunken rage, ordered a full scale nuclear alert, which would have triggered an immediate American counter response. Fortunately, his generals ignored him.

Perry said the only reason that Israel hadn?t attacked Iran yet, was because the US was making aggressive efforts to collapse the economy there with its oil embargo. Enlisting the aid of Russia and China was key, but difficult since Iran is a major weapons buyer from these two countries. His argument was that the economic shock that a serious crisis would bring would damage their economies more than any benefits they could hope to gain from their existing Iranian trade.

I told Perry that I doubted Iran had the depth of engineering talent needed to run a full scale nuclear program of any substance. He said that aid from North Korea and past contributions from the AQ Khan network in Pakistan had helped them address this shortfall.

Ever in search of the profitable trade, I asked Perry if there was an? opportunity in nuclear the plays, like the Market Vectors Uranium and Nuclear Energy ETF (NLR) and Cameco Corp. (CCR), that have been severely beaten down by the Fukushima nuclear disaster. He said there definitely was. In fact, he personally was going to lead efforts to restart the moribund US nuclear industry. The key here is to promote 5th generation technology that uses small, modular designs, and alternative low risk fuels like thorium.

I had never met Senator Sam Nunn and had long been an antagonist, as he played a major role in ramping up the Vietnam War. Thanks to his efforts, the Air Force, at great expense, now has more C-130 Hercules transport planes that it could ever fly because they were assembled in his home state of Georgia. Still, I tried to be diplomatic.

Nunn believes that the most likely nuclear war will occur between India and Pakistan. Islamic terrorists are planning another attack on Mumbai. This time India will retaliate by invading Pakistan. The Pakistanis plan on wiping out this army by dropping an atomic bomb on their own territory, not expecting retaliation in kind. But India will escalate and go nuclear too. Over 100 million would die from the initial exchange. But when you add in unforeseen factors, like the broader environmental effects and crop failures (CORN), (WEAT), (SOYB), (DBA), that number could rise to 1-2 billion. This could happen as early as 2013.

Nunn applauded current administration efforts to cripple the Iranian economy which has caused their currency to fall 30% in the past six months. The strategy should be continued, even if innocents are hurt. He argued that further arms control talks with the Russians could be tough. They value these weapons more than we do, because that?s all they have left. Nunn delivered a stunner in telling me that Warren Buffet had contributed $50 million of his own money to enhance security at nuclear power plants in emerging markets. I hadn?t heard that.

As the event drew to a close, I returned to Secretary Shultz to grill him some more about the details of the Reykjavik conference held some 26 years ago. He responded with incredible detail about names, numbers, and negotiating postures. I then asked him how old he was. He said he was 91. I responded ?I want to be like you when I grow up?. He answered that I was ?a promising young man.? It was the best 60th birthday gift I could have received.

![]()

Oops, Wrong Number

?We are about to do something terrible to you. We are going to deprive you of an enemy,? Soviet commentator, Georgi Arbitov, told Secretary of State George Schultz at the end of the cold war.