Global Market Comments

March 27, 2020

Fiat Lux

Featured Trade:

(MARCH 25 BIWEEKLY STRATEGY WEBINAR Q&A),

(ROM), (BA), (VIX), (UPRO), (SSO), (UBER), (LYFT), (MDT),

(GLD), (GOLD), (NEM), (GDX), (UGL)

Global Market Comments

March 27, 2020

Fiat Lux

Featured Trade:

(MARCH 25 BIWEEKLY STRATEGY WEBINAR Q&A),

(ROM), (BA), (VIX), (UPRO), (SSO), (UBER), (LYFT), (MDT),

(GLD), (GOLD), (NEM), (GDX), (UGL)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader March 25 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Since we flipped the off button on the economy, I don’t see how we can simply flip the on button and have a V-shaped recovery. It seems much more unlikely that it will get back to pre-recession levels.

A: Actually, all we really need is confidence. Confident people can go outside and not get sick. Once we start seeing a dramatic decline in the number of new cases, the shelter-in-place orders may be cancelled, and we can go outside and go back to work. It’s really that simple. So, we will get an initial V-shaped recovery probably in the third quarter, and after that, it will be a slower return spread over several quarters to get back to normal. Everybody wants to get back to normal and let's face it, there's an enormous amount of deferred consumption going on. I have hardly spent any money myself other than what I’ve spent online. All of those purchases get deferred, so in the recovery, there's going to be a massive binge of entertainment, shopping, and travel that is all being pent up now—that will get unleashed once the airlines start flying again and the shelter-in-place orders are cancelled. We’re not losing so much of this growth, we’re just deferring it. Obviously, some of the growth is gone permanently; you can forget about any kind of vacation in the next couple of months. I would say, the great majority of consumption in the US—and thus growth and thus stock appreciation—is just being deferred, not cancelled outright.

Q: Other than the ProShares Ultra Technology ETF (ROM), do you have any other leveraged sectors coming into the recovery?

A: There is a 50/50 chance the Roaring 20s started 2 days ago, on Monday, March 23 at the afternoon lows. We may go back and test those lows one more time, which at this point is 3,700 points below here, but we are clocking 1,000 points a day. It doesn’t take much, like a bad non-farm payroll number, to go back and test those lows. The good news is out; they're not going to spend any more money other than the $10 trillion they're putting in now.

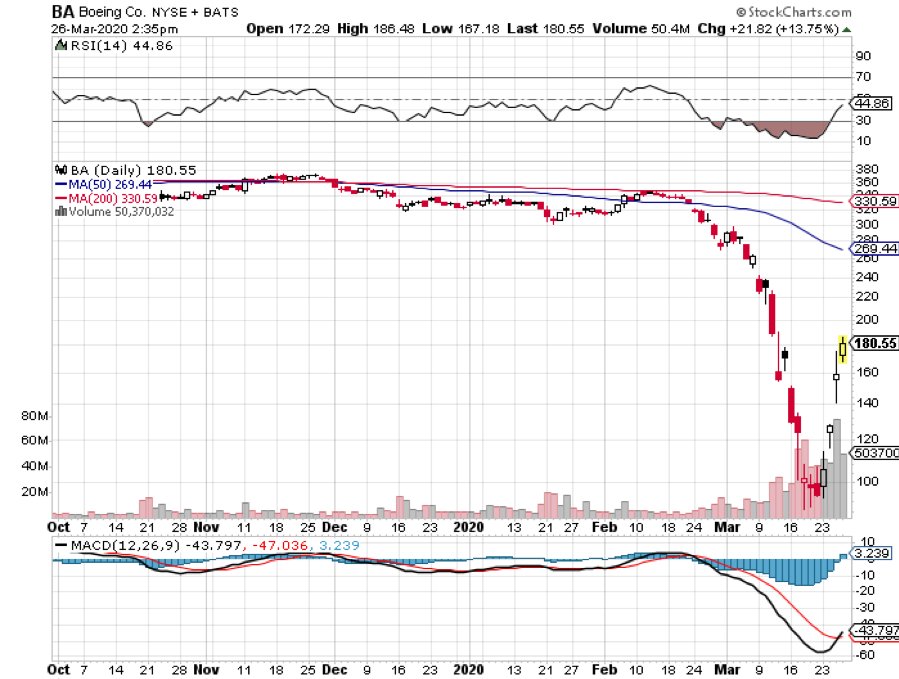

Q: Would you buy Boeing (BA) here? Is this the bottom?

A: The bottom was at $94 on Monday; we went up 100% in three days and now we’re at $180. Incredible moves, and a total lack of liquidity. One reason I haven't added any positions lately is that they have closed the New Yok Stock Exchange floor and its not clear that of I send out a trade alert, it could get done. We have gone totally online, so I just want to see what happens as a result of that. I don’t want to be putting out trade alerts that no one can get in or out of, heaven forbid.

Q: What do you mean by “The spike to $80 in the Volatility Index (VIX) was totally artificial?”

A: When you have a series of cascading shorts triggered by margin calls, that is artificial. I have seen this happen many times before, both on the upside and the downside. This happened twice in the (VIX) in the last two years. When you go from a (VIX) of $25 to $80 and back down to $39 in days, which is what we did, you know it was a one-time-only spike and we are not going to visit the $80 level again— at least not until the next financial crisis because those positions are gone and are never coming back. A (VIX) of $80 means we are going to have 1,000 point move in the Dow Average for the next 30 days.

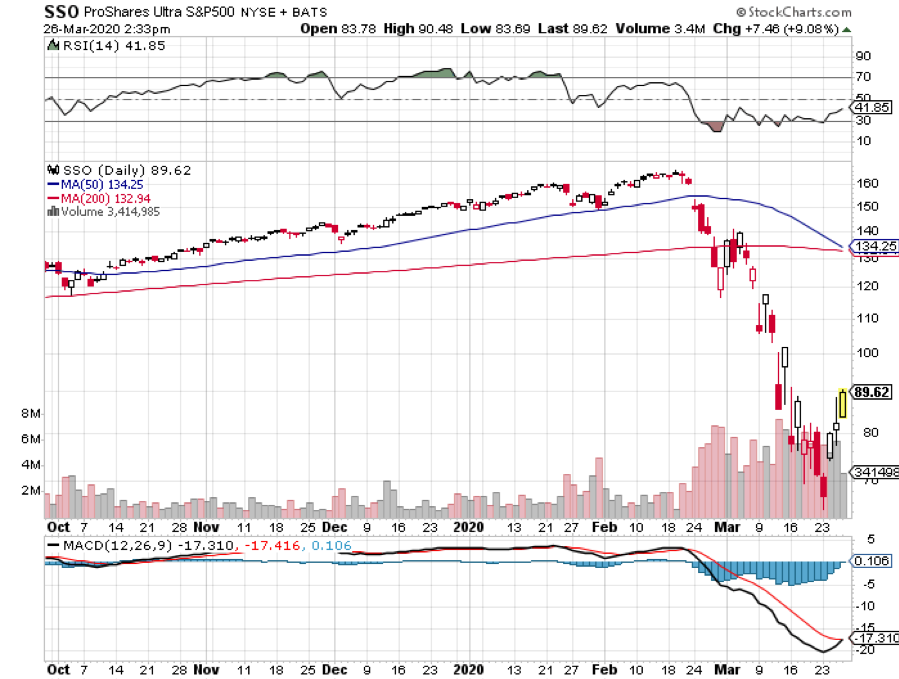

Q: I bought some ProShares Ultra Pro ETF (UPRO) which is the 3x long the S&P 500 at $1,829. Do I take profits by selling calls or just hold longer?

A: I would just sell the whole position outright. The (UPRO) is so incredibly volatile that you are rewarded heavily for just coming out completely and then reopening fresh positions on these big meltdown days. We will probably be doing trade alerts on (UPRO) or its cousin, the 2x long ProShares Ultra S&P 500 (SSO) sometime in the near future.

Q: With 2-year LEAPs, would you go at the money or out of the money?

A: This is the golden opportunity to go way out of the money because the return goes from 100% to 500%, or even 1000% if you go, say, 30%-50% out of the money. A lot of these stocks are ripe for very quick 30% bouncebacks, especially the (ROM). So yes, you want to do out of the money 20% to 30%. It will easily recover those losses in weeks if you are picking the right stocks. Over a two-year view, a lot of these big tech stocks could double by the time your LEAP expires, and then you will get the full profit. The rule of thumb is: the farther out of the money you go, the bigger the profit is. But I wouldn’t go for more than a 1000% profit in 2 years; you don't want to get greedy, after all.

Q: You called the Dow to hit 15,000. Is that still possible? We got down to the 18 handle.

A: Yes, if the coronavirus data gets worse, which is certain, we could get another panic selloff. How will the market handle 100,000 US deaths, given the exponential rise in cases we are seeing? With cases doubling every three days that is entirely within range. So, I would say, there is a 50% chance we hit the bottom on Monday at 18,000, and 50% chance we go lower.

Q: Do you know anything about the coronavirus stocks like Regeneron (REGN)?

A: Actually, I do, it's covered by the Mad Hedge Biotech & Health Care Letter, click here for the link. If you get the Biotech Letter, you already know all about stocks like Regeneron. Regeneron literally has hundreds of drugs in testing right now to work as vaccines or antivirals, and some of them, like their arthritis drug, have already been proven to work. So, we just have to get through the accelerated trials and testing to unleash it on the market. But for anybody who has a drug, it's going to take a year to mass-produce enough to inoculate the entire country, let alone the world. So, don't make any big bets on getting a vaccine any time soon—it's a very long process. Even in normal times, some of these drugs take months to manufacture.

Q: Are there any ventilator stocks out there?

A: There are; a company called Medtronic (MDT), which the Mad Hedge Biotech & Healthcare Letter also covers. They are the largest ventilator company in the US. Their normal production is 100 machines a week. Now, they are increasing that to 500 a week as fast as they can, but it isn’t enough. We need about 100,000 ventilators. China is now selling ventilators to the US. Elon Musk from Tesla (TSLA) just bought 1,000 ventilators in China and had them shipped over to San Francisco at his own expense, and Virgin Atlantic just flew over a 747 full of ventilators and masks and other medical supplies from China. So yes, there are stocks out there to play these things, they have already had large moves. We liked them anyway, even before the pandemic, so those calls were quite good. And China thinks their epidemic is over, so they are happy to sell us all the medical supplies they can make.

Q: Why did 30-year mortgage rates just go up instead of down? I thought the Fed rate cuts were supposed to take them down; am I missing something?

A: In order to get 30-year mortgage rates down, you have to have buyers of 30-year loans, and right now there are buyers of nothing. The lending that is happening is from banks lending their own money, which is only a tiny percentage of the total loan market. When the Fed moves into the mortgage market, you will see those yields move to the 2% range. The other problem is how to get a loan if all the banks are closed. They are running skeletal staff now, and you can’t close on real estate deals because all the notaries and title offices are closed; so essentially the real estate industry is going to shut down right now and hopefully, we’ll finish that in a month.

Q: Do you think Uber (UBER) and Lyft (LYFT) will go bankrupt?

A: It is a possibility because one to one human contact inside a car is about the last situation you want to be in during a pandemic. Their traffic was down 25% according to a number I saw. It’s very heavily leveraged, very heavily indebted, and those are the companies that don’t survive long in this kind of crisis. So, I would say there is a chance they will go under. I never liked these companies anyway; they are under regulatory assault by everybody, depend on non-union drivers working for $5 an hour, and there are just too many other better things to do.

Q: Is this the end of corporate buybacks?

A: To some extent, yes. A future Congress may make it either illegal or highly tax corporate buybacks, in some fashion or another because twice in 12 years now, we have had companies load up on buying back their own stock, boosting CEO compensation to the hundreds of millions—if not billions—and then going broke and asking for government bailouts. Something will be done to address that. If you take buybacks out of the market (the last 10,000-point gain in the Dow were essentially all corporate buybacks), we may not see a 20X earnings multiple again for another generation. Individuals were net sellers of stock for those two years. We only reached those extreme highs because of buybacks, so you take those out of the equation and it's going to get a lot harder to get back to the super inflated share prices like we had in January.

Q: How long before an Italian bank collapses, and will they need a bailout?

A: I don’t think they will get a collapse; I think they will be bailed out inside Italy and won’t need all of Europe to do this. But the focus isn't on Europe right now, it's on the US.

Q: Do you think this virus is really subsiding in China based on their past history of dishonest reporting?

A: Yes, that is a risk, and that's why people aren’t betting the ranch right now—just because China is reporting a flattening of cases. And China could be hit with a second wave if they relax their quarantine too soon.

Q: What's your opinion on how the Fed is doing and Steve Mnuchin in this crisis?

A: I think the Fed is doing everything they possibly can. I agree with all of their moves—this is an all-hands-on-deck moment where you have to do everything you can to get the economy going. Notice it’s Steve Mnuchin doing all the negotiating, not the president, because nobody will talk to him. For a start, he may be a Corona carrier among other things, and you’re not seeing a lot of social distancing in these press conferences they are holding. About which 50% of the information they give out is incorrect, and that's the 50% coming from Donald Trump.

Q: What do you think about no debt and no pension liability?

A: That’s why Tech has been leading the upside for the last 10 years and will lead for the next 10. You can really narrow the market down to a dozen stocks and just focus on those and forget about everything else. They have no net debt or net pension fund liabilities.

Q: Why have we not heard from Warren Buffet?

A: I'm sure negotiations are going on all over the place regarding obtaining massive stakes in large trophy companies that he likes, such as airlines and banks. So that will be one of the market bottom indicators that I mentioned a couple of days ago in my letter on “Ten Signs of a Market is Bottoming.”

Q: What’s the outlook for gold?

A: Up. We just had to get the financial crisis element out of this before we could go back into gold, so I would be looking to buy SPDR Gold Shares ETF (GLD), the gold miners like Barrick Gold (GOLD) and Newmont Mining (NEM), the Van Eck Vectors Gold Miners ETF (GDX), and the 2X long ProShares Gold ETF (UGL).

Q: Does the Fed backstop give you any confidence in the bond market?

A: Yes, it does. I think we finally may be getting to the natural level of the market, which is around an 80-basis point yield. Let’s see how long we can go without any 50-point gyrations.

Q: Do you foresee a depression?

A: We are in a depression now. We could hit a 20% unemployment rate. The worst we saw during the Great Depression was 25%. But it will be a very short and sharp one, not a 12-year slog like we saw during the 1930s.

Good Luck and Good Trading and stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

March 26, 2020

Fiat Lux

Featured Trade:

(PFIZER PUSHES AHEAD WITH A CORONA CURE),

(PFE), (BNTX), (MYL)

Pfizer (PFE) has been widely recognized as one of the leading and largest vaccine makers in the industry.

Now, one of America’s biggest biotechnology companies will throw its weight behind German firm BioNTech (BNTX) in its quest to develop a COVID-19 vaccine.

Prior to this announcement, BioNTech has already been working inside China in collaboration with Chinese biopharmaceutical company Fosun Pharma (SHA: 600196).

Its partnership with Pfizer will entail efforts outside China and will be in collaboration with the University of Pennsylvania and the Bill and Melinda Gates Foundation. Specifically, the work will be done at sites in the US and Germany.

What we know so far about this experimental COVID vaccine is that it’s called BNT162.

Like the experimental vaccine from Moderna (MRNA), BioNTech’s version is also based on messenger RNA. Clinical trials will start by April.

BioNTech shares were up 55% following the announcement of this collaboration with Pfizer. Meanwhile, the giant biotechnology company’s shares jumped by 3.8%.

Before this coronavirus vaccine collaboration, BioNTech and Pfizer were already partners.

In 2018, the two companies agreed to work together in developing flu vaccines based on mRNA.

However, this recent expansion of their partnership gained more attention because of the intense focus on the efforts to combat the novel coronavirus.

The output of this partnership won’t be kept within the confines of the companies though.

According to Pfizer, any information or tool it comes up with will be shared with the entire scientific community.

The company also pledged its assistance to small biotechnology companies working on COVID-19 treatments and vaccines, going as far as offering its manufacturing power to help speed up the process.

Aside from its coronavirus efforts, the giant biotech has been working on plans to bolster its revenue streams.

Addressing the loss of exclusivity for seizure disorder drug Lyrica, an issue that weighed on the company’s top and bottom lines last year, Pfizer has been gearing up to merge the Upjohn unit with Mylan (MYL).

The merged companies will be called Viatris.

This is a good strategy. Since Upjohn is home to Lyrica and several older drugs nearing the end of their patent exclusivity, separating this unit will allow Pfizer to streamline its portfolio.

Instead of holding on to Lyrica as an anchor, the “new” Pfizer will focus on its new line of blockbuster drugs like breast cancer medication Ibrance and blood clot treatment Eliquis.

Apart from these, Pfizer is investing more on marketing its rising stars like Vyndaquel. The company’s pipeline is also filled with potential blockbusters particularly its 20-valent pneumococcal vaccine.

Although the Upjohn-Mylan merger will inevitably lower Pfizer’s dividend, shareholders of the giant biotech will still own part of Viatris. That means they would have a share in the dividend of the merged companies as well.

The combination of the dividends from both Pfizer and Viatris would total to roughly the same amount as the “old” Pfizer, which currently yields 5%.

What we’re experiencing right now is definitely unprecedented. COVID-19 has mutated from a respiratory disease affecting a single province in China into a global threat endangering everyone’s physical and financial well-being.

However, there’s always good news.

From an objective perspective, this coronavirus crisis has provided a rare opportunity for investors. After all, stock market corrections are actually quite common occurrences.

Looking at each correction in equities in the past, you can see that these were eventually triggered by a bull-market rally.

Remember, the ongoing vaccine research conducted by companies worldwide will yield results sooner or later. So even if COVID-19 is here to stay, it will no longer be a deadly threat in the long run.

In times like these, I think it’s more prudent to consider major biotechnology stocks when looking to invest.

This is because they have a higher capacity to keep trucking through this health crisis and to deal with its aftermath.

Despite the growing fear that this pandemic will lead us to a recession, Pfizer can still be easily categorized as a profitable company.

Considering that it’s trading at merely 13 times its expected earnings, this stock is quite a bargain.

Pfizer has a strong cash flow. Its long history shows that it has also weathered economic storms.

More importantly, it has a product pipeline that we find essential regardless of pandemics and strict quarantines. It doesn’t hurt that they’re priced attractively as well.

Global Market Comments

March 26, 2020

Fiat Lux

Featured Trade:

(REVISITING THE GREAT DEPRESSION)

(EXPLORING MY NEW YORK ROOTS)

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

AGNC, like a lot of stocks, has made a nice bounce since it bottomed out with the rest of the market.

There is a good possibility it may have peaked out here in the short term.

Therefore, I would like to take this opportunity to collect some call premium.

The last price for the April 3rd - $13.50 call for $0.80

My suggestion is to sell them at $0.80.

These are the calls that expire next Friday.

Assuming you collect the 80 cents, it will mean you would have collected $1.20 in call premium on this position.

If these calls are assigned next Friday, the total return would be 13%.

While the Diary of a Mad Hedge Fund Trader focuses on investment over a one week to a six-month time frame, Mad Day Trader, provided by Bill Davis, will exploit money-making opportunities over a brief ten minute to three-day window. It is ideally suited for day traders, but can also be used by long-term investors to improve market timing for entry and exit points. Read more

Mad Hedge Technology Letter

March 25, 2020

Fiat Lux

Featured Trade:

(ALGORITHMS RUN WILD)

($COMPQ), (TWTR)

Don’t underestimate trading algorithms.

The “Buy the Dip” psychology is broken and computerized trading has completely flooded the market with its personality.

That is exactly the dynamic of the current tech market, and it will mountain of generous offerings to reverse the trend in the form of monstrous stimulus and cash handouts.

As we entered 2020, the sentiment was sky-high, geopolitical tensions relatively calmed and three recent interest-rate cuts from the Federal Reserve drove tech stocks to record levels.

For 10 years, traders and the algorithms they harnessed were handsomely rewarded by aggressively betting against elevated volatility.

Cogent chart trends are the algorithms’ lustful partner in bed and now that every single short-term model is flashing sell, sell, sell - there isn't much bulls can do to fight back.

Many tech hedge funds have settled on similar conclusions - the best defense right now is unwinding portfolios to return to cash.

Incessant margin calls roiling any logical strategy has struck fear into many traders who levered up 10X.

What you could possibly see is the Minsky moment: That stability ultimately breeds instability because the only input in which becomes the difference make is volatility producing massive violence on upside and downside moves.

The ones who can absorb elevated risk are nibbling and unleveraged hoping to time the turn when stocks finally react positively to good data.

The current battle in the fog of war is that of two different economic scenarios that have direct influence in which ways the algorithms flip – either shutdown the country ala Wuhan, China for an extended period of time or send the troops back to work.

Hedge fund billionaire Bill Ackman gave his 2-cents restating his passionate plea for a 30-day-shutdown to fight the coronavirus pandemic.

Former Goldman Sachs CEO Lloyd Blankfein is in favor of sending back the asymptomatic younger generation workers sooner than later.

Initially, Blankfein gave his backing for “extreme measures” in order to flatten the curve, but promoted healthy workers returning “within a very few weeks.”

Blankfein's argument rests on that if people don’t go back to work, the economy might become too damaged to recover from inciting another crash.

This contrasts starkly with Ackman’s idea of “testing, testing, testing”, which would theoretically dismantle the potency of the virus but take longer for the economy to restart.

U.S. President Donald Trump has relayed his desire to open up business by Easter Sunday.

So as mostly professional politicians hash out a towering aid package of over $2 trillion, firms will get more of an indicator of how and when the business world opens up again.

Trading algorithms are on a knives edge because of the uncertainty – until they are illegal – it is something we are stuck with.

These trading formulas are preset based on biases that start with a series of inputs and the most critical input is volatility or better known as the fear index.

If the lockdowns are extended, the flood of negative news will force algorithms to sell on the extra volatility.

When things go bonkers, many of these preset formulas sell which exacerbates the down move further simply because more than enough people have the same preset algorithm.

Cutting position size when market volatility explodes is not a farfetched theory and is quite a common trading nostrum.

Even if many of these trades would be good long-term bets, many trading algorithms are focused on short-term trades and by this, I mean milliseconds and not days.

Another input into trading algorithms are Twitter feeds.

The platform is scraped for keywords from mass media news sources and synthesized into a specific output that is fed into a computer algorithm.

These headlines offer insight into what the sentiment is for the trading day – negative, positive, or neutral.

This scraping of data is especially relevant in today’s chaotic trading world where 10% moves up or down in one day is the new normal.

Because of Dodd-Frank Wall Street reform, many of the big banks have shuttered trading operations hurting the market’s liquidity situation causing spreads to widen and down moves to accelerate.

But now that the Fed has landed the Sikorsky UH-60 Black Hawk on the helipad and the money is waiting to helicopter down as they have announced “unlimited” asset buying and guaranteeing of corporate bonds to aid financial markets.

How does computerized trading roil markets?

Here is an example. A recent trading day included more than $100 billion of selling, the worst week since the financial crisis and was triggered by a hedging strategy called “vol targeting”—using volatility as a central input in trading decisions—and other systematic tactics.

Funds making decisions based on volatility, including some with names such as volatility-targeting funds and risk-parity funds, have risen in popularity.

Risk-parity funds manage an estimated $300 billion.

Risk parity is an approach focused on allocation of risk, usually defined as volatility, rather than allocation of capital.

That is what we have now – a cesspool of risk parity hedge funds layered by high frequency funds layered by short/long vol funds layered by arbitrage funds all levered 15X.

The take into consideration that they are supercharged by massive volume-based computer algorithms and trying to head for the exit door at the same time.

Ironically, this could be one of catalysts for shares to recalibrate and head back up north as traders start to front-run the peak of the health crisis.

Let’s hope that it happens sooner than later and that the government doesn’t manage to screw up delivering the helicopter money.