Mad Hedge Technology Letter

July 30, 2021

Fiat Lux

Featured Trade:

(THE BEST WAY TO STREAMLINE YOUR TECH PORTFOLIO)

(MU), (PLTR), (AMD), (AMZN), (SQ), (PYPL)

Mad Hedge Technology Letter

July 30, 2021

Fiat Lux

Featured Trade:

(THE BEST WAY TO STREAMLINE YOUR TECH PORTFOLIO)

(MU), (PLTR), (AMD), (AMZN), (SQ), (PYPL)

Overperformance is mainly about the art of taking complicated data and finding perfect solutions for it. Trading in technology stocks is no different.

Investing in software-based cloud stocks has been one of the seminal themes I have promulgated since the launch of the Mad Hedge Technology Letter way back in February 2018.

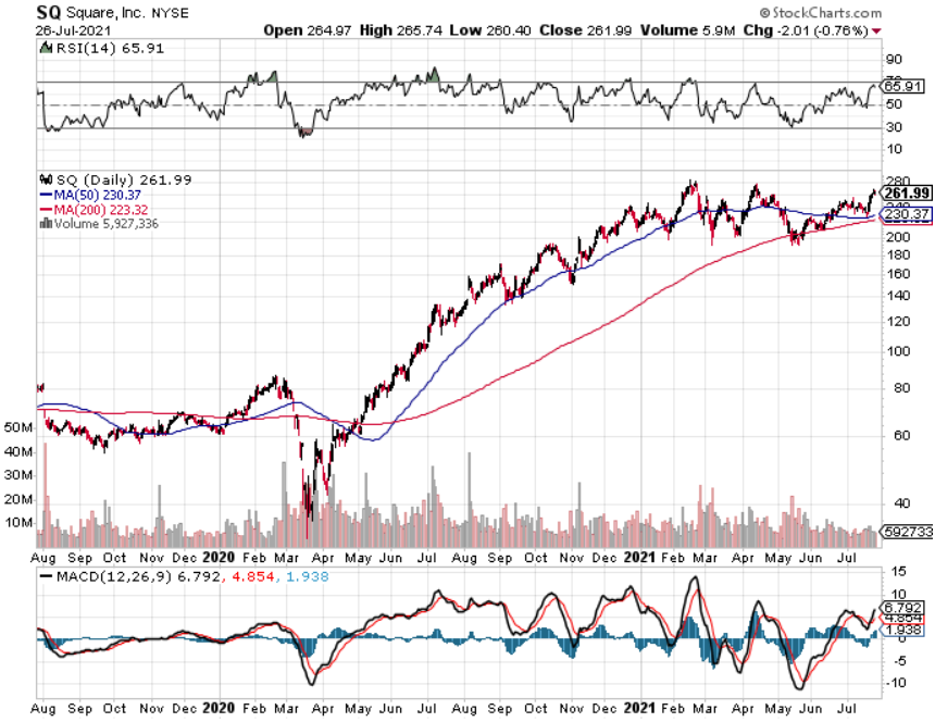

I hit the nail on the head and many of you have prospered from my early calls on AMD, Micron to growth stocks like Square, PayPal, and Roku. I’ve hit on many of the cutting-edge themes.

Well, if you STILL thought every tech letter until now has been useless, this is the one that should whet your appetite.

Instead of racking your brain to find the optimal cloud stock to invest in, I have a quick fix for you and your friends.

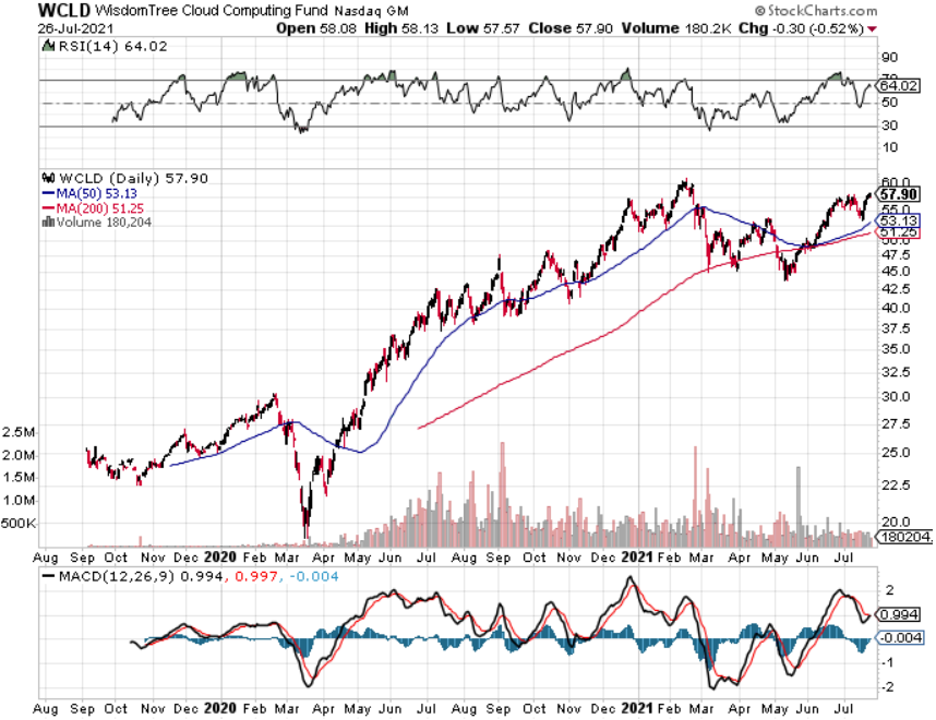

Invest in The WisdomTree Cloud Computing Fund (WCLD) which aims to track the price and yield performance, before fees and expenses, of the BVP Nasdaq Emerging Cloud Index (EMCLOUD).

What Is Cloud Computing?

The “cloud” refers to the aggregation of information online that can be accessed from anywhere, on any device remotely.

Yes, something like this does exist and we have been chronicling the development of the cloud since this tech letter’s launch.

The cloud is the concept powering the “shelter-at-home” trade which has been hotter than hot since March 2020.

Cloud companies provide on-demand services to a centralized pool of information technology (IT) resources via a network connection.

Even though cloud computing already touches a significant portion of our everyday lives, the adoption is on the verge of overwhelming the rest of the business world due to advancements in artificial intelligence and the Internet of Things (IoT) hyper-improving efficiencies.

The Cloud Software Advantage

Cloud computing has particularly transformed the software industry.

Over the last decade, cloud Software-as-a-Service (SaaS) businesses have dominated traditional software companies as the new industry standard for deploying and updating software. Cloud-based SaaS companies provide software applications and services via a network connection from a remote location, whereas traditional software is delivered and supported on-premise and often manually. I will give you a list of differences to several distinct fundamental advantages for cloud versus traditional software.

Product Advantages

Speed, Ease, and Low Cost of Implementation – cloud software is installed via a network connection; it doesn’t require the higher cost of on-premise infrastructure setup maintenance, and installation.

Efficient Software Updates – upgrades and support are deployed via a network connection, which shifts the burden of software maintenance from the client to the software provider.

Easily Scalable – deployment via a network connection allows cloud SaaS businesses to grow as their units increase, with the ability to expand services to more users or add product enhancements with ease. Client acquisition can happen 24/7 and cloud SaaS companies can easily expand into international markets.

Business Model Advantages

High Recurring Revenue – cloud SaaS companies enjoy a subscription-based revenue model with smaller and more frequent transactions, while traditional software businesses rely on a single, large, upfront transaction. This model can result in a more predictable, annuity-like revenue stream making it easy for CFOs to solve long-term financial solutions.

High Client Retention with Longer Revenue Periods – cloud software becomes embedded in client workflow, resulting in higher switching costs and client retention. Importantly, many clients prefer the pay-as-you-go transaction model, which can lead to longer periods of recurring revenue as upselling product enhancements does not require an additional sales cycle.

Lower Expenses – cloud SaaS companies can have lower R&D costs because they don’t need to support various types of networking infrastructure at each client location.

I believe the product and business model advantages of cloud SaaS companies have historically led to higher margins, growth, higher free cash flow, and efficiency characteristics as compared to non-cloud software companies.

How does the WCLD ETF select its indexed cloud companies?

Each company must satisfy critical criteria such as they must derive the majority of revenue from business-oriented software products, as determined by the following checklist.

+ Provided to customers through a cloud delivery model – e.g., hosted on remote and multi-tenant server architecture, accessed through a web browser or mobile device, or consumed as an application programming interface (API).

+ Provided to customers through a cloud economic model – e.g., as a subscription-based, volume-based, or transaction-based offering Annual revenue growth, of at least:

+ 15% in each of the last two years for new additions

+ 7% for current securities in at least one of the last two years

Some of the stocks that would epitomize the characteristics of a WCLD component are Salesforce, Microsoft, Amazon-- I mean, they are all up, you know, well over 100% from the nadir we saw in March 2020 and contain the emerging growth traits that make this ETF so robust.

If you peel back the label and you look at the contents of many tech portfolios, they tend to favor some of the large-cap names like Amazon, not because they are “big” but because the numbers behave like emerging growth companies even when the law of large numbers indicate that to push the needle that far in the short-term is a gravity-defying endeavor.

We all know quite well that Amazon isn't necessarily a pure play on cloud computing software, because they do have other hybrid-sort of businesses, but the elements of its cloud business are nothing short of brilliant.

ETF funds like WCLD, what they look to do is to cue off of pure plays and include pure plays that are growing faster than the broader tech market at large. So, you're not going to necessarily see the vanilla tech of the world in that portfolio. You're going to see a portfolio that's going to have a little bit more sort of explosive nature to it, names with a little more mojo, a little bit more chutzpah because you're focusing on smaller names that have the possibility to go parabolic and gift you a 10-bagger precisely because they take advantage of the law of small numbers.

One stock that has the chance for a legitimate 10-bagger is my call on Palantir (PLTR).

Palantir is a tech firm that builds and deploys software platforms for the intelligence community in the United States to assist in counterterrorism investigations and operations.

This is one of the no-brainers that procure revenue from Democrat and Republican administrations.

In a global market where the search for yield couldn’t be tougher right now, right-sizing a tech portfolio to target those extraordinary, extra-salacious tech growth companies is one of the few ways to produce alpha without overleveraging.

No doubt there will be periods of volatility, but if a long-term horizon is something suited for you, this super-growth strategy is a winner, and don’t forget about PLTR while you’re at it.

“When we launch a product, we're already working on the next one. And possibly even the next, next one.” – Said Current CEO of Apple Tim Cook

Global Market Comments

July 30, 2021

Fiat Lux

Featured Trade:

(JULY 28 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (CRSP), (TLT), (TBT), (BABA), (BIDU), (FXI), (RAD), (TSLA), (NASD), (NKLA), (NIO), (INTC), (MU), (NVDA), (AMD), (TSM), (VXX), (XVZ), (SVXY), (FCX), (ROM), (SPG)

July 28 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the July 28 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Lake Tahoe, NV.

Q: What is your plan with the (SPY) $443-$448 and the $445/450 vertical bear put spreads?

A: I’m going to keep those until we hit the lower strike price on either one and then I’ll just stop out. If the market doesn’t go down in August, then we are going straight up for the rest of the year as the earnings power of big tech is now so overwhelming. Sorry, that’s my discipline and I’m sticking to it. Usually, what happens 90% of the time when we go through the strike, and then go back down again by expiration for a max profit. But the only way to guarantee that you'll keep your losses small is by stopping out of these things quickly. That’s easy to do when you know that 95% of the time the next trade alert you’ll get is a winner.

Q: Are you still expecting a 5% correction?

A: I am. I think once we get all these great earnings reports out of the way this week, we’re going to be in for a beating. I just don't see stocks going straight up all the way through August, so that’s another reason why I'm hanging on to my short positions in the S&P 500 (SPY).

Q: What’s the best way to play CRISPR Therapeutics (CRSP) right now?

A: That is with the $125-$130 vertical bull call spread LEAPS with any maturity in 2022. We had a run in (CRSP) from $100 up to $170 and I didn’t take the damn profit! And now we’ve gone all the way back down to $118 again. Welcome to the biotech space. You always take the ballistic moves. Someday I should read my own research and find out why I should be doing this. For those who missed (CRSP) the last time, we are one proprietary drug announcement, one joint venture announcement, or one more miracle cure away from another run to $170. So that will probably happen in the next year, you get the $125-$130 call spread, and you will double your money easily on that.

Q: I’m down 40% on the United States Treasury Bond Fund (TLT) January $130-$135 vertical bear put spread LEAPS. What would you do?

A: Number one, if you have any more cash I would double up. Number two, I would wait, because I would think that starting from the Fall, the Fed will start to taper; even if they do it just a little bit, that means we have a new trend, the end of the free lunch is upon us, and the (TLT) will drop from $150 down to $132 where it was in March so fast it will make your head spin. I'm hanging onto my own short position in (TLT). If you are new to the (TLT) space and you want some free money, put on the January 2020 $150-$155 vertical bear put spread now will generate about a 75% return by the January 21, 2022 options expiration. I just didn't figure on a 6.5% GDP growth rate generating a 1.1% bond yield, but that’s what we have. I'm sorry, it’s just not in the playbook. Historically, bonds yield exactly what the nominal GDP growth rate is; that means bonds should be yielding 6.50% now, instead of 1.1%. They will yield 6.5% in the future, but not right now. And that's the great thing about LEAPS—you have a whole year or 6 months for your thesis to play out and become right, so hang on to those bond shorts.

Q: Do you have any ideas about the target for Facebook (FB) by the end of the year?

A: I would say up about 20% from current levels. Not only from Facebook but all the other big tech FANGS too. Analysts are wildly underestimating the growth of these companies in the new post-pandemic world.

Q: Do you think the worst of the pandemic will be over by September?

A: Yes, we will be back on a downtrend by September at the latest and that will trigger the next leg up in the bull market. Delta with its great infectious and fatality rates is panicking people into getting shots. The US government is about to require vaccinations for all federal employees and that will get another 5 million vaccinated. Americans have the freedom to do whatever they want but they don’t have the freedom to kill their neighbors with fatal infections.

Q: What should I do with my China (BABA), (BIDU), (FXI) position? Should I be doubling down?

A: Not yet, and there’s no point in selling your positions now because you’ve already taken a big hit, and all the big names are down 50% from the February high. I wouldn't double down yet because you don’t know what's happening in China, nobody does, not even the Chinese. This is their way of addressing the concentration of the wealth in the top 1% as has happened here in the US as well. They’re targeting all the billionaire stocks and crushing them by restricting overseas flotations and so on, so it ends when it ends, and when that happens all the China stocks will double; but I have absolutely no idea when that's going to happen. That being said, I have been getting phone calls from hedge funds who aren’t in China asking if it's time to get in, so that's always an interesting precursor.

Q: What happened to the flu?

A: It got wiped out by all the Covid measures we took; all the mask-wearing, social distancing, all that stuff also eliminates transmission of flu viruses. Viruses are viruses, they’re all transmitted the same way, and we saw this in the Rite Aid (RAD) earnings and the 55% drop in its stock, which were down enormously because their sales of flu medicines went to zero, and that was a big part of their business. I didn’t get the flu last year either because I didn’t get Covid; I was extremely vigilant on defensive measures in the pandemic, all of which worked.

Q: Why would the Fed taper or do much of anything when Powell wants to be reappointed in February 2022?

A: I don’t think he is going to get reappointed when his four-year term is up in early 2022. His policies have been excellent, but never underestimate the desire of a president to have his own man in the office. I think Powell will go his way after doing an outstanding job, and they will appoint another hyper dove to the position when his job is up.

Q: What are your thoughts on the Chinese electric auto company Nio competing here in the U.S.?

A: They will never compete here in the U.S. China has actually been making electric cars longer than Tesla (TSLA) has but has never been able to get the quality up to U.S. standards. Look what happened to Nikola (NKLA) who’s founder was just indicted. Avoid (NIO) and all the other alternative startup electric car companies—they will never catch up with Tesla, and you will lose all your money. Can I be any clearer than that?

Q: You recently raised the ten-year price target up for the Dow Average from 120,000 to 240,000. What is Nasdaq's target 10 years out?

A: I would say they’re even higher. I think Nasdaq (NASD) could go up 10X in 10 years, from 14,000 to 140,000 because they are accounting for 50% of all earnings in the U.S. now, and that will increase going forward, so the stocks have to go ballistic.

Q: What do you think of Intel (INTC)?

A: I don’t like it. They had a huge rally when they fired their old CEO and brought in a new one. There was a lot of talk on reforming and restructuring the company and the stock rallied. Since then, the market has started insisting on performance which hasn’t happened yet so the stock gave up its gains. When it does happen, you’ll get a rally in the stock, not until then, and that could be years off. So I'd much rather own the companies that have wiped out Intel: (MU), (NVDA), (AMD), and (TSM).

Q: When you do recommend buying the Volatility Index (VIX), do you recommend buying the (VIX) or the (VXX)?

A: You can only buy the VIX in the futures market or through ETFs and ETNs, like the (VXX), the (XVZ), and the (SVXY), or options on these. I would be very careful in buying that because time decay is an absolute killer in that security, and that's why all the professionals only play it from the short side. That's also why these spikes in prices literally last only hours because you have professionals hammering (VIX). Somebody told me once that 50% of all the professional traders in the CME make their living shorting the (VIX) and the (VXX). So, if you think you’re better than the professionals, go for it. My guess is that you’re not and there are much better ways to make money like buying 6-to-12-month LEAPS on big tech stocks.

Q: Can the Delta variant get a bigger pullback?

A: Yes. I expect one in August, about 5%. But if Delta gets worse, the selloff gets worse. You saw what it did last year, down 40% in the (SPY) in only two months, so yes, it all depends on the Delta virus. I'm not really worrying about Delta, it's the next one, Epsilon or Lambda, which could be the real killer. That's when the fatality rate goes from 2% to 50%, and if you think I'm crazy, that's exactly what happened in 1919. Go read The Great Influenza book by John Barry that came out 20 years ago, which instantly became a best seller last year for some reason.

Q: Does the Matterhorn have enough flat space on the top to stand on it?

A: Actually, there is a 6’x6’ sort of level rock to stand on top of the Matterhorn. If you slip, it’s a 5000’ fall straight down on any side, and on a good weather day in the summer, there are 200 people climbing the Matterhorn. There's sometimes a one-hour line just to take your turn to get to the top to take your pictures, and then get down again to make space for the next person. So that's what it's like climbing the Matterhorn, it's kind of like climbing Mount Everest, but I still like to do it every year just to make sure I can do it, and one year I hope to win the prize for the oldest climber of the year to climb the Matterhorn. Every year this German guy beats me; he’s two years older than me.

Q: When will Freeport McMoRan (FCX) start going up? I have the 2023 LEAPS

A: Good thing you have the two-year LEAPS because that gives you two years for inflation to show its ugly face once again. You just have to be patient with these. I think we’ll get a rally in the Fall along with all the other interest rate plays like banks, industrials, money management companies, and so on. (FCX) will certainly participate in that. In the meantime, if we get all the way down to $30 in Freeport McMoRan, I would double up your position.

Q: Why is oil (USO) not a buy? Oil is the ultimate inflation hedge.

A: Yes, unless all of the cars in the United States become electric in the next 15 years, which they will, wiping out half of all demand from the largest oil consumer. The United States consumes about 20 million barrels of oil a day, half of that is for cars, and if you take that out of the demand picture you dump 10 million barrels a day on the market and oil goes back to negative numbers like we saw last year. Never do counter-trend trades unless you’re a professional in from of a screen 24 hours a day.

Q: Should I take profits on my ProShares Ultra Technology ETF (ROM) November $90-$95 vertical bull spread and then enter a new spread when tech sells off?

A: Absolutely! When you have that much leverage and you get these price spikes, you sell! The leverage on this position is 2X on the ETF and 10X on the options for a total of 20X! Well done, nice trade and nice profit, go out and buy yourself a new Tesla and wait for the next dip in tech, which may have already started, and which could power on for the rest of August.

Q: What’s the next move for REITs?

A: REITs came off of historic lows last year; a lot of people thought they were going to go bankrupt, and for companies like (SPG) it was a close-run thing. I would be inclined to take profits on REITs here. The next thing to happen is for interest rates to go up and REITs don’t do that great in a rising rate environment.

Q: When is the off-season in Incline Village?

A: It’s the Spring and the Fall, in between ski season and the summer season. That means there are four months a year here, May/June and September/October, where I’m the only one here and the parking lots are empty. There is no one on the trails, the weather is perfect, the leaves are changing colors, and the roads aren’t crowded, so that is the time to be here. It’s a mob scene in the winter and a worse mob scene in the summer!

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Mad Hedge Biotech & Healthcare Letter

July 29, 2021

Fiat Lux

FEATURED TRADE:

(A BIOTECH PREPARED FOR ANOTHER DOOMSDAY MARKET)

(BNTX), (PFE), (MRNA), (AZN), (JNJ), (GSK), (GILD)

If you’ve heard of Harry Dent Jr., then you know that he’s the economist who correctly and accurately forecasted the Japanese economic downturn back in 1989. He also hit the nail on the head when he predicted the collapse of the dot.com bubble in 2000.

Now, he’s saying that the stock market will crash in the next three months, describing it as “the biggest crash of our lifetime.”

There’s no precise method to determine if his pessimistic outlook is justified thus far.

Nonetheless, even if Dent turns out to be right, I don’t believe that all stocks will plummet. There are a handful of stocks that could soar if the stock market does crash this summer.

For instance, I think vaccine stocks would most likely take off if the new variants of COVID-19 triggered a market crash in the coming months.

After all, the best weapons we have in overcoming these issues are still vaccines.

I also think that one of the biggest—if not the biggest—winners in this segment is BioNTech (BNTX).

Let me share with you the reasons.

For one, BioNTech is actually the smallest of the biopharmaceutical companies in the vaccine market today.

Catalysts typically generate larger swings in stocks that hold smaller market capitalizations compared to those with bigger market caps.

It’s also telling that BioNTech and its co-vaccine developer, Pfizer (PFE), have started delving into tactics to handle the continuous rise of the Delta variant.

So far, what the partners have suggested includes adding a third dose to the COVID-19 vaccine to boost the immunity and protection of people against the new strain.

The two are also looking into beginning their clinical testing on a modified version of their vaccine, which would specifically target the Delta variant, by August.

BioNTech’s valuation also plays a key role. The company so far is the cheapest among the leading vaccine stocks, which include Moderna (MRNA) and AstraZeneca (AZN), based on its forward earnings multiples.

To date, BioNTech trades at roughly 6.3 times its expected earnings—a low valuation that wouldn’t last long, especially if fears about the new variants spark another massive downturn in the market.

Thus far, BioNTech and Pfizer have delivered roughly 392 million vaccine doses to the US alone.

However, the country is anticipating increasing demand for it, pushing it to sign up for an additional 200 million doses.

The duo plans to deliver 110 million doses to the US by the end of 2021 and the rest of the orders by April 2022.

In a separate agreement, the US also ordered 500 million doses as donations to developing countries across the globe.

In comparison, Moderna delivered 137.3 million, while Johnson and Johnson (JNJ) supplied 13.1 million.

On top of these, Pfizer and BioNTech are working to expand the reach of their vaccine.

The companies recently sealed an agreement with Biovac, a company in South Africa, to produce vaccine shots from a plant in Cape Town. Similar initiatives are under exploration in Latin America.

Riding the momentum of its COVID-19 vaccine, BioNTech is also working to develop a highly effective and widely tolerated malaria vaccine.

The malaria vaccine candidate is expected to build on two decades’ worth of mRNA research, which BioNTech used to co-develop the COVID-19 vaccine with Pfizer.

The clinical trial for this new project is planned to start by the end of 2022.

At this point, only one malaria vaccine is available on the market: GlaxoSmithKline’s (GSK) Mosquirix, which offers about 30% effectiveness in safeguarding kids from the mosquito-borne virus.

If successful, BioNTech will be easing a massive burden globally, as over 400,000 children die from malaria every year.

In addition to its malaria vaccine candidate, BioNTech is also looking into using its mRNA expertise to diversify its pipeline to include cancer treatments, including colorectal cancer, advanced melanoma, and other malignant solid tumors.

BioNTech’s move to attempt to conquer the oncology sector gained even more traction following its recent acquisition of Kite, a manufacturing plant under Gilead Sciences (GILD).

Kite primarily focuses on an experimental kind of cancer treatment relating to neoantigen T-cell receptor cell therapy.

In the first quarter of 2021, BioNTech was able to boost its sales by over 7,295%.

Its total revenues within that period reached $2.49 billion, which indicates a healthier revenue stream compared to its main competitor, Moderna, which raked in $1.9 billion.

In terms of sales outlook for the entire year, BioNTech also forges ahead with $26 billion, while Moderna anticipates $19.2 billion.

Needless to say, these numbers show how undervalued BioNTech has been lately.

Given the new developments concerning the new variants and the company’s expanded coverage of the market, it’s clear to see that the future looks bright for BioNTech regardless of Dent’s doomsday market predictions.

Global Market Comments

July 29, 2021

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(HOW TO GAIN AN ADVANTAGE WITH PARALLEL TRADING),

(GM), (F), (TM), (NSANY), (DDAIF), BMW (BMWYY), (VWAPY),

(PALL), (GS), (RSX), (EZA), (CAT), (CMI), (KMTUY),

(KODK), (SLV), (AAPL)

Hi John,

You are a wonderful example for men to follow. Energetic, roping a steer? Climbing a mountain with a 40lb backpack for 10 miles? Incredible.

But the big one is your humble willingness to help us little guys who need your help. You take the jitters out of trading for us. And I for one am looking forward to great trading results. You have opened my eyes to the marvelous benefits of Vertical Bull Call Spread trades. Thank you for all you do!

Because of all the great pictures of you from all over the globe and at all ages, it makes me feel that I know you. Thank you for going the extra mile in keeping us informed of what you are doing and where you are going. That is truly great in an age when people do not get too much of an opportunity to personally meet in person to get to know each other.

Best regards,

Bill

Seminole, Florida

Mad Hedge Technology Letter

July 28, 2021

Fiat Lux

Featured Trade:

(THE REAL RULES OF TECH)

(MSFT), (FB), (GOOGL), (AAPL), (AMZN), (NFLX), (TSLA)