Mad Hedge Biotech & Healthcare Letter

August 31, 2021

Fiat Lux

FEATURED TRADE:

(A CANCER PIONEER FOR THE BOOKS)

(SEGN), (MRK), (BMY), (PFE), (GILD), (RHHBY), (TAK), (GMAB)

Mad Hedge Biotech & Healthcare Letter

August 31, 2021

Fiat Lux

FEATURED TRADE:

(A CANCER PIONEER FOR THE BOOKS)

(SEGN), (MRK), (BMY), (PFE), (GILD), (RHHBY), (TAK), (GMAB)

When choosing a biotechnology company to invest in, a good sign to look out for is when management continuously looks for ways to expand its technology.

This means you’re looking at a stock that’s likely to appreciate multiple folds.

Seagen (SEGN) does this in spades.

Since it was founded in 1997, Seagen (SEGN) has reached almost $30.67 billion in market capitalization.

Reviewing its growth story, I think its powerful growth strategy is one of the key elements that help the company with its advancements.

That is, Seagen is aggressively developing and expanding its different labels for the approved drugs in its portfolio while also actively discovering innovative and new treatments and molecules.

Simply put, Seagen’s growth and expansion can be likened to a tree that keeps forming new additional branches.

Over the years, the company has experienced a remarkable transformation from a single-product firm to a diversified and ever-expanding player, particularly in the oncology medication market—a strategy that paid off.

After all, the market for cancer drugs isn’t the type to stand still.

This sector is renowned for its fast-paced demands and rapid growth. If you look at how much has been done, remember that several types of cancer that seemed incurable a mere 10 years ago are now no longer considered death sentences thanks to the innovative therapies discovered.

If roughly 15 years ago, the standard cancer treatment only involved chemotherapy and surgery, the recent years have granted us access to newer technologies like targeted therapy and immunotherapy.

Lately, CAR-T therapy has been hailed as the most effective means of treating blood cancer. Meanwhile, the likes of Merck’s (MRK) Keytruda and Bristol-Myers Squibb (BMY) Opdivo have made chemotherapy and surgery more effective as well.

So, it wouldn’t be a surprise anymore if the technology in the oncology sector advances further in the years to come.

Another relatively fresh innovation is the antibody-drug conjugate (ADC) technology.

This takes and combines all the positive effects of chemotherapy and targeted therapy while simultaneously eliminating the adverse effects of chemotherapy on the patient’s body.

Unlike chemotherapy, ADCs specifically target and eliminate tumor cells and works to spare the healthy ones. Once the tumor cells are detected, a toxic drug is released to kill them.

Basically, it works like a “smart bomb” in that it annihilates only the enemies and protects the allies.

The first drug to be approved based on ADCs is Mylotarg from Pfizer (PFE), which was 20 years ago.

However, it was only in recent years that this technology finally gained traction and attracted commercial success.

So far, roughly 56 pharmaceutical companies are working on developing ADCs.

Aside from Pfizer, another pioneer in ADCs is Seagen. Unlike Pfizer, this company has chosen to continue focusing on the development of the treatment.

Other companies working on ADC technology include Immunomedics, which Gilead Sciences (GILD) acquired, and Roche (RHHBY).

However, Seagen’s work looks to be the most promising in this segment.

Its first ADC drug is Adcetris, which was approved in 2011 for Hodgkin’s lymphoma and made in cooperation with Takeda Pharmaceutical (TAK).

Its indication was later expanded to cover another white blood cell disease, Peripheral T-cell lymphoma (PTCL).

Seagen already holds roughly 45% of the market share in the Hodgkin’s lymphoma segment alone, and this is expected to rise to 50% by 2026.

In terms of projected sales in the US, Adceris is estimated to generate about $1.7 billion by 2026.

On top of that, Seagen also rakes in royalties from Adceris sales outside the US thanks to its Takeda partnership.

Riding the momentum of Adceris, Seagen expanded its ADC pipeline and later gained approval for Padcev in 2019.

This drug received the go signal to treat a fairly common disease in the oncology space: metastatic bladder cancer.

In the US, the average number of new cases of metastatic bladder cancer is 83,000. Given its market size and potential to become part of a combination therapy with the ever-popular Keytruda, Padcev is expected to generate at least $2.6 billion in sales by 2026.

Gaining more confidence in its expertise in the oncology sector, Seagen continued its expansion and gained regulatory approval for breast cancer treatment Tukysa.

Tukysa is expected to bring roughly $1 billion in annual sales in the US and European markets. This figure is projected to rise when it eventually also gains approval for colorectal cancer.

Another notable drug in Seagen’s pipeline is Tisotumab Vedotin (TV), which is a collaboration with Genmab (GMAB). TV is a cervical cancer treatment and is expected to gain approval by the end of 2021.

Shifting gears, let’s take a look at the upcoming growth of Seagen. Initially, its 2021 guidance put its annual sales at $1.28 billion for all the products.

However, Seagen has already exceeded expectations, with Adceris reporting $700 million in sales for a single quarter this year. Actually, both Adceris and Padcev are well on their way into becoming blockbusters in a year or two, thanks to their continuously expanding applications.

Overall, Seagen is an excellent long-term investment.

Aside from its work with giant biopharmaceutical companies like Merck and BMY, its current portfolio of treatments and pipeline programs present a myriad of opportunities for Seagen.

Moreover, its ability to develop powerful treatments and leverage the science of ADCs make Seagen one of the most promising oncology stocks in the market today.

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

August 31, 2021

Fiat Lux

Featured Trade:

(WHY YOU MUST AVOID ALL EV PLAYS EXCEPT TESLA),

(TSLA), (GM)

Mad Hedge Technology Letter

August 30, 2021

Fiat Lux

Featured Trade:

(A GREAT ALTERNATIVE IN THE AD TECH SPACE)

(SNAP), (AMZN), (FB), (GOOGL), (SDC)

I know many readers gripe about certain tech stocks being too expensive like Google (GOOGL), Facebook (FB), or even Amazon (AMZN), but that’s not the case for all high-quality tech names out there.

There are still deals to be had.

An undervalued tech name in the same industry, albeit more diminutive than the three I just mentioned, is ad revenue platform Snap Inc. (SNAP).

Their story is a good one and their revenue model appears to be maturing at an optimal time while still exhibiting many elements of explosive growth.

To see what I mean — Snap grew both revenue and daily active users at the highest rates they have achieved in the last four years.

Daily active users grew 23% year-over-year to 293 million — expanding revenue by 116% year-over-year to $982 million.

This outperformance reflects the momentum in SNAP's core advertising business and the positive results of their team serving ad partners helping them to generate a return on investment.

SNAP benefited from a favorable operating environment and continued success with both direct response and large brand advertisers — continue to leverage performant ad products to grow an advertiser base globally.

Adjusted EBITDA improved by $213 million compared to last year, marking the third adjusted EBITDA profitable quarter in the last 12 months as SNAP continues to demonstrate the leverage in their business as they scale.

They are also fully absorbed in making progress against revenue and Average Revenue Per User (ARPU) opportunities, which I believe will be driven by three key priorities.

First, driving ROI through measurement, ranking, and optimization.

Second, investing in aggressive sales and marketing functions by continuing to train, hire, and build for scale.

And third, building innovative ad experiences around video and augmented reality, with a focus on shopping and commerce.

The commitment to these three priorities, along with a unique reach and large, engaged community, allows SNAP to drive performance at scale for businesses around the world.

They have proven through results in North America that with a robust team, surrounding resources, and a local focus, they can accelerate revenue.

They are now taking that model and replicating it in several markets that they have identified as having a large digital advertising market and significant levels of existing Snapchat adoption.

It’s true to say they still have a lot of room to grow in some of the world's most established ad markets outside of North America, especially in Europe.

For example, in the UK, France, and the Netherlands, SNAP reaches over 90% of 13- to 24-year-olds — 75% of 13- to 34-year-olds.

SNAP continues to invest heavily in video advertising, with the goal of driving results for advertising partners and connecting them to the Snapchat Generation.

For example, SNAP worked with Nielsen to help U.S. advertisers understand how to more efficiently reach their target audiences via Snap Ads.

The Total Ad Ratings study analyzed how over 30 cross-platform advertising campaigns reached people on both Snapchat and television.

The analysis showed that Snapchat campaigns contributed an average of 16% incremental reach to advertisers' target audiences, and over 70% of the Gen Z audience that was reached by Snapchat was not reached by TV-only campaigns.

This is especially important as people are increasingly cutting the cord, and mobile content consumption continues to grow, presenting SNAP with a large opportunity to help advertisers reach the Snapchat Generation at scale.

Augmented reality advertising is delivering a return on investment that is measurable and repeatable, which is encouraging the incremental businesses to invest in AR.

For example, Smile Direct Club (SDC) leveraged a Goal-Based Bidding Click optimization for Augmented Reality (AR), which drove 49% of Snap customer leads in Q2 and was the most effective ad unit at driving traffic for their business compared to other social channels.

The success of the Lens ultimately encouraged Smile Direct Club to include AR Lenses as part of their long-term business strategy.

SNAP is betting the ranch on efforts to help advertisers improve conversions and ROI, and recently launched optimization for AR, which allows advertisers to optimize their AR campaigns for down-funnel purchases and fits well into the broader shopping strategy.

SNAPs bread and butter region of North America is hitting on all cylinders with revenue growing 129% year-over-year in Q2, while ARPU grew 116% year-over-year as they continue to benefit from significant investments made in sales teams and sales support in the prior year.

At a 30-thousand-foot level, the global internet services market was valued at over $450 billion in 2020, the year in which the pandemic fundamentally altered how society functions, accelerating a push towards digital offerings.

The internet market is expected to grow at a compound annual growth rate of 5% through 2027 and reach a value of $652 billion. US-based equities presently control close to 30% of the total global market share in the industry.

My takeaway from this is that even though there is GOOGL and FB in this space, the pie is growing so fast that there is easily room for others like SNAP.

One must believe that if SNAP keeps operating anywhere close to its pandemic performance relative to other companies, they are surely guaranteed to be a buy-the-dip company.

In terms of price action, that’s exactly what we have witnessed as the price has zig-zagged up by 300% — the stock price goes two levels up and retraces back one — rinse and repeat.

Just view the big down days as optimal entry points into a burgeoning social media platform and deploy capital.

In the short term, on the monetization side, I have to note that the fiscal comparisons will be more challenging in the second half as SNAP begins to lap the acceleration in top-line growth that they experienced in the prior year.

Once that sell-off gets baked into the equation via a 3-5% sell-off, readers should jump back into SNAP.

“It's not about working harder; it's about working the system.” – Said Co-founder and CEO of the American social media company Snap Evan Spiegel

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline. Read more

Global Market Comments

August 30, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or THE HIGHER WE GO THE CHEAPER WE GET),

(JPM), (BAC), (C), (GS), (MS), (BLK), (FCX), (X),

(WYNN), (MGM), (ALK), (LUV), (HAL), (SLB), (TLT)

I am sitting here holed up in my office in San Francisco.

Lake Tahoe is being evacuated as the Caldor fire is only ten miles away and the winds are blowing towards it. The visibility there is no more than 500 yards. The ski resorts are pointing their snow cannons towards their buildings to ward off flames.

Conditions are not much better here in Fog City. We are under a “stay at home” order due to intense smoke and heat. Even here, the fire engines are patrolling by once an hour.

The Boy Scout trip got cancelled this weekend, so the girls are having a cooking competition, chocolate chip waffles versus a German chocolate cake.

To make matters worse, I have been typing with only one finger all week, thanks to the elbow surgery I had on Tuesday. Next time, I’ll think twice before taking down a 300-pound steer. When I told the doctor how I incurred this injury, he laughed. “At your age?”

Which leaves me to contemplate this squirrelly stock market of ours. I have always been a numbers guy. But the higher the indexes rise, the cheaper stocks get. That’s not supposed to happen, but that is the fact.

We started out 2021 with an S&P 500 price earnings multiple of 25X. Now, we are down to a lowly 21X and the (SPY) is 20% higher, rising from $360 to $450.25.

The analyst community, ever the lagging indicator that they are, had S&P forward earnings for 2022 all the way down to $175. They have been steadily climbing ever since and are now touching $200 a share.

This is what 20/20 hindsight gets you. That and $5 will get you a cup of coffee at Starbucks. It takes a madman like me to go out on a limb with high numbers and then be right.

So what follows an ever-cheaper market? A more expensive one. That means stocks will continue to my set-in-stone target of $475 for the (SPY) for yearend, and (SPY) earnings of over $200 per share.

It gets better.

(SPY) earnings should hit $300 a share by 2025 and $1,400 a share by 2030. That makes possible my (SPY) target of $1,800 and my Dow Average target of 240,000 in a decade.

What are markets getting right that analysts and bears are getting wrong?

The future has arrived.

The pandemic brought forward business models and profitability by a decade. Technology is hyper-accelerating on all fronts.

Cycles are temporary but adoption is permanent. We are never going back to the old pre-pandemic economy. As a result, stocks are now worth a lot more than they were only two years ago.

So what do we buy now? There is a second reopening trade at hand, the post-delta kind. That means buying banks (JPM), (BAC), (C), brokers (GS), (MS), money managers (BLK), commodities (FCX), (X), hotels (WYNN), (MGM), airlines (ALK), (LUV), and energy (HAL), (SLB).

And what do we avoid like the plague? Bonds (TLT), which offer only confiscatory yields in the face of rising inflation with gigantic negative interest rates.

As for technology stocks, they will go sideways to up small in the aftermath of their ballistic moves of the past three months.

You all know that I am a history buff and there are particular periods of history that are starting to disturb me.

In August, we saw ten new intraday highs for the S&P 500 (SPY). That has not happened since 1987. Remember what happened in 1987?

We have not seen 11 new highs in August since 1929. The only negative three months seen since 1929 are August, September, and October. Remember what happened in 1929?

If that doesn’t scare the living daylights out of you, then nothing will. So, it seems we are in for some kind of correction, even if it’s just the 5% kind.

As for me, I’m looking forward to 2030.

The “Everything” Rally is on, according to my friend, Strategas founder Tom Lee. You can see it in the recent strength of epicenter stocks like energy, hotels, airlines, and casinos. It could run into 2022.

The Taper is this year and interest rate rises are later, said Jay Powell at Jackson Hole last week. Markets will be jumpy, especially bonds. Fed governor Jay Powell’s every word was parsed for meaning. Dove all the way. The larger focus will be on the August Nonfarm Payroll report out this week.

Pfizer Covid vaccination gets full FDA approval, requiring millions more to get shots and bringing forward the end of the pandemic. All 5 million government employees will now get vaccinated, including the entire military. It’s the fastest drug approval in history. Some 37,000 new cases in one day. The stock market likes it. Take profits on (PFE)

Bitcoin tops $50,000 after breaking several key technical levels to the upside. Next stop is a double top at $66,000. It helps that Coinbase is buying $500 million worth of crypto for its own portfolio. Buy (COIN) on dips.

The US Dollar will crash in coming years, says Jeffry Gundlach and I think he is right. Emerging markets will become the next big play but not quite yet. Gold (GLD) will be a great hideout once it comes out of hibernation. China will soon return to outperforming the US. The dollars reserve currency status is at risk.

The lumber crash is saving $40,000 per home, says Toll Brothers (TOL) CEO, Doug Yearly. Last year, lumber prices surged from $300 per board foot to an insane $1,700, thanks to a Trump trade war with Canada and soaring demand. It all flows straight through the bottom line of the homebuilders which should rally from here. Buy (TOL) on dips.

China’s crackdown creates investment opportunities, says emerging investing legend Mark Mobius. He sees corporate governance improving over the long term. The gems are to be found among smaller companies not affected by Beijing’s hard-line. Mobius loves India too.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

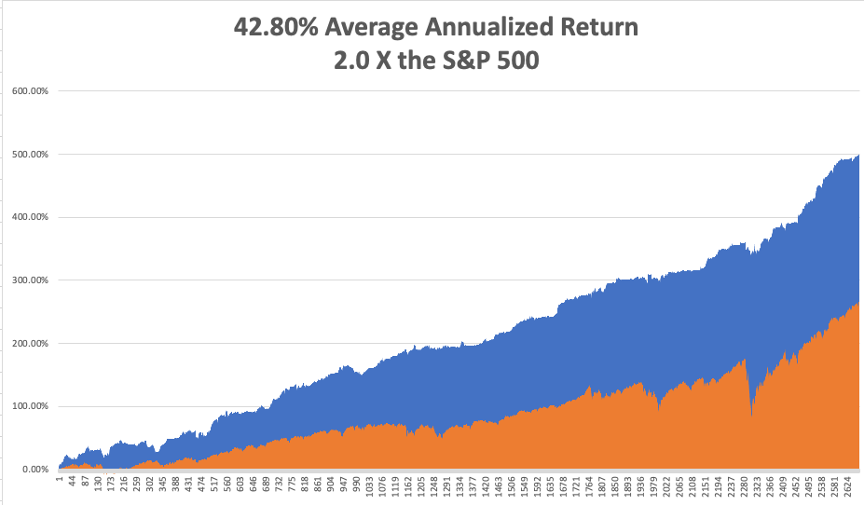

My Mad Hedge Global Trading Dispatch saw a healthy +7.62% gain in August. My 2021 year-to-date performance appreciated to 76.83%. The Dow Average was up 15.87% so far in 2021.

That leaves me 80% in cash at 20% in short (TLT) and long (SPY). I’m keeping positions small as long as we are at extreme overbought conditions.

That brings my 12-year total return to 499.38%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.80%, easily the highest in the industry.

My trailing one-year return popped back to positively eye-popping 116.67%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 39 million and rising quickly and deaths topping 638,000, which you can find here.

The coming week will bring our monthly blockbuster jobs reports on the data front.

On Monday, August 30 at 11:00 AM, Pending Home Sales are published. Zoom (ZM) reports.

On Tuesday, August 31, at 10:00 AM, S&P Case Shiller National Home Price Index for June is released. CrowdStrike (CRWD) reports.

On Wednesday, September 1 at 10:45 AM, the ADP Private Employment report is disclosed.

On Thursday, September 2 at 8:30 AM, Weekly Jobless Claims are announced. DocuSign (DOCU) reports.

On Friday, September 3 at 8:30 AM, the all-important August Nonfarm Payroll report is printed. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

Oh and the German chocolate cake won, but please don’t tell anyone.

As for me, given the losses in Afghanistan this week, I am reminded of my several attempts to get into this troubled country.

During the 1970s, Afghanistan was the place to go for hippies, adventurers, and world travelers, so of course, I made a beeline for straight for it.

It was the poorest country in the world, their only exports being heroin and the blue semiprecious stone lapis lazuli, and illegal export of lapis carried a death penalty.

Towns like Herat and Kandahar had colonies of westerners who spent their days high on hash and living life in the 14th century. The one cultural goal was to visit the giant 6th century stone Buddhas of Bamiyan 80 miles northwest of Kabul.

I made it as far as New Delhi in 1976 and was booked on the bus for Islamabad and Kabul ($25 one-way). Before I could leave, I was hit with amoebic dysentery.

Instead of Afghanistan, I flew to Sydney, Australia where I had friends and knew Medicare would take care of me for free. I spent two months in the Royal North Shore Hospital where I dropped 50 pounds, ending up at 125 pounds.

I tried to go to Afghanistan again in 2010 when I had a large number of followers of the Mad Hedge Fund Trader stationed there, thanks to the generous military high-speed broadband. The CIA waved me off, saying I wouldn’t last a day as I was such an obvious target.

So, alas, given the recent regime change, it looks like I’ll never make it to Afghanistan. I won’t live long enough to make it to the next regime change. It’s just one more concession I’ll have to make to my age. I’ll just have to content myself reading A One Thousand and One Nights at home instead. The Taliban blew up the stone Buddhas of Bamiyan in 2001.

In the meantime, I am on call for grief counseling for the Marine Corps for widows and survivors. Business has been thankfully slow for the last several years. But I’ll be staying close to the phone this weekend just in case.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

India in 1976