One has to be truly impressed with the bounce in biotech and pharmaceutical stocks over the past month.

This is something to pay attention to, as biotech and technology will be two of the top-performing stock market sectors for the next 20 years.

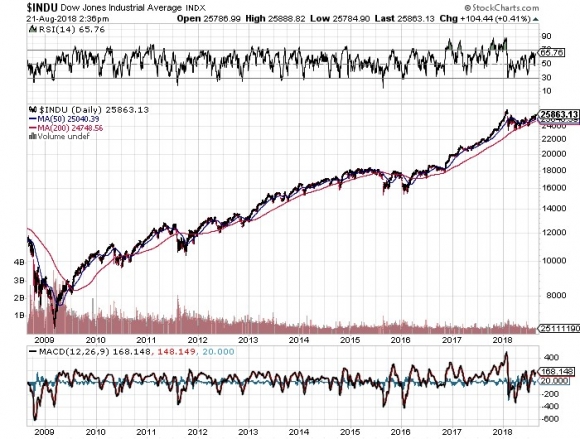

If you want to be lazy, just buy these two sectors on every dip and you should outperform the main indexes (SPY), (INDU) by three or four to one.

Since June, there were sign that life was returning to this beleaguered sector.

Suddenly, every company has become a takeover target.

(GILD) followers like me had long bemoaned the company’s failure to profitably deploy its cash mountain by growing through M&A.

Something had to replace their its drug eventually, once everyone in the world was cured of the dread disease.

Once the top-performing sector, they went from heroes to goats, so fast that it made your head spin.

What I called “The ATM Effect” kicked in big time.

That’s when frightened investors run to the sidelines and sell their best stocks to raise cash.

After all, no one wants to sell other stocks for a loss and admit defeat, at least in front of their clients.

It’s not that the companies themselves were without blood on their hands.

Valuations were getting, to use the polite term, getting “stretched” after a torrid five-year run.

Gilead Sciences (GILD) soaring from $18 to $125?

Celgene (CELG) rocketing from $20 to $142?

It was a performance for the ages.

If a financial advisor wasn’t in health care during the salad days, chances are that he is driving a taxi for Uber in a bad neighborhood by now.

Raise your hand if you think Americans aren’t paying enough for their prescription drugs.

Yes, I thought so.

Here’s the key issue for health care and biotech for investors.

It’s all about politics.

Much remains to be seen about the future of health care in America.

Obamacare weathered the last assault by the administration. Will it survive the next one?

Remember, Obamacare passed by one vote only after a year of cantankerous infighting, and then, only when a member changed parties (the late Pennsylvanian Arlen Specter).

Nobody knows.

However our health care is fixed, open bidding for government contracts would be anathema to the industry, something from which they have, until now, been exempted.

I believe the United States will eventually stagger toward a national single payer system. But it may take another 20 years of turmoil to get there.

California will certainly take the first step. It is now considering a statewide single payer system that would provide full coverage to the state’s $39 million residents.

The bad news is that it would cost $400 billion. The good news is that it would save the state $375 billion in expenses, so it may be worth doing.

The state legislature in Sacramento is currently mulling alternatives.

It’s easy to understand why these stocks were so popular and are found brimming to overflowing in client portfolios and personal 401k’s and IRA’s.

We are just entering a Golden Age for biotech and health care.

Profit growth for many firms is exceeding 20% a year.

Hyper-accelerating biotechnology is rapidly bringing to market dozens of billion-dollar-earning drugs that were, until recently, considered in the realm of science fiction.

And we have only just gotten started.

Cures for cancer, heart disease, arthritis, diabetes, AIDS, and dementia?

You can take your pick. And the new CRISPR technology is accelerating everything further.

If you missed biotech and health care the first time around, you’ve just been given a second chance at the brass ring.

Here’s a list of five top-quality names to get your feet wet:

Gilead Sciences (GILD) – Has the world’s top hepatitis cure, which it sells for $80,000 per treatment. For a full report, clear here for “Keep Gilead Sciences on Your Radar."

Celgene (CELG) – A biotech firm that specializes in cancer cures (thalidomide) and inflammatory diseases. It also produces Ritalin for the treatment of ADHD.

Allergan (AGN) – Has the world’s third largest low-cost generic drug business. In addition, it has built a major portfolio of drug therapies through more than two dozen acquisitions over the past decade.

Regeneron (REGN) – Already has a great anti-inflammatory drug, and is about to market a blockbuster anti-cholesterol drug that will substantially reduce heart disease.

If you want a lower risk, more diversified play in the area, you can buy the Health Care Select Sector SPDR (XLV). Please note that a basket of stocks is going to deliver a fraction of the volatility of single stocks.

Therefore, we have to be more aggressive with our positioning to make any money, picking call option strikes that are closer to the money.

Johnson and Johnson (JNJ) is the largest holding in the (XLV), with a 12.8% weighting, while Gilead Sciences (GILD) is the fourth, with a 5.1% share. For a list of the largest components of this ETF, please click here.

The other classic play in this area is the Biotech iShares ETF (IBB) issued by BlackRock (click here for the link).

Their largest holding is Biogen (BIIB), followed by Gilead Sciences (GILD), Celgene (CELG), Amgen (AMGN), and Regeneron Pharmaceuticals (REGN).

I’ll be shooting out Trade Alerts on biotech and health care names as soon as I see another sweet entry point.

Until then, enjoy the ride!