Who’s been buttering your bread more than any other?

Which publicly listed company has created the most wealth in history?

I’ll give you some hints.

The founder never took a bath, was a devout vegetarian, and dropped out of college after the first semester. The only class he finished was for calligraphy. And he was a first-class asshole.

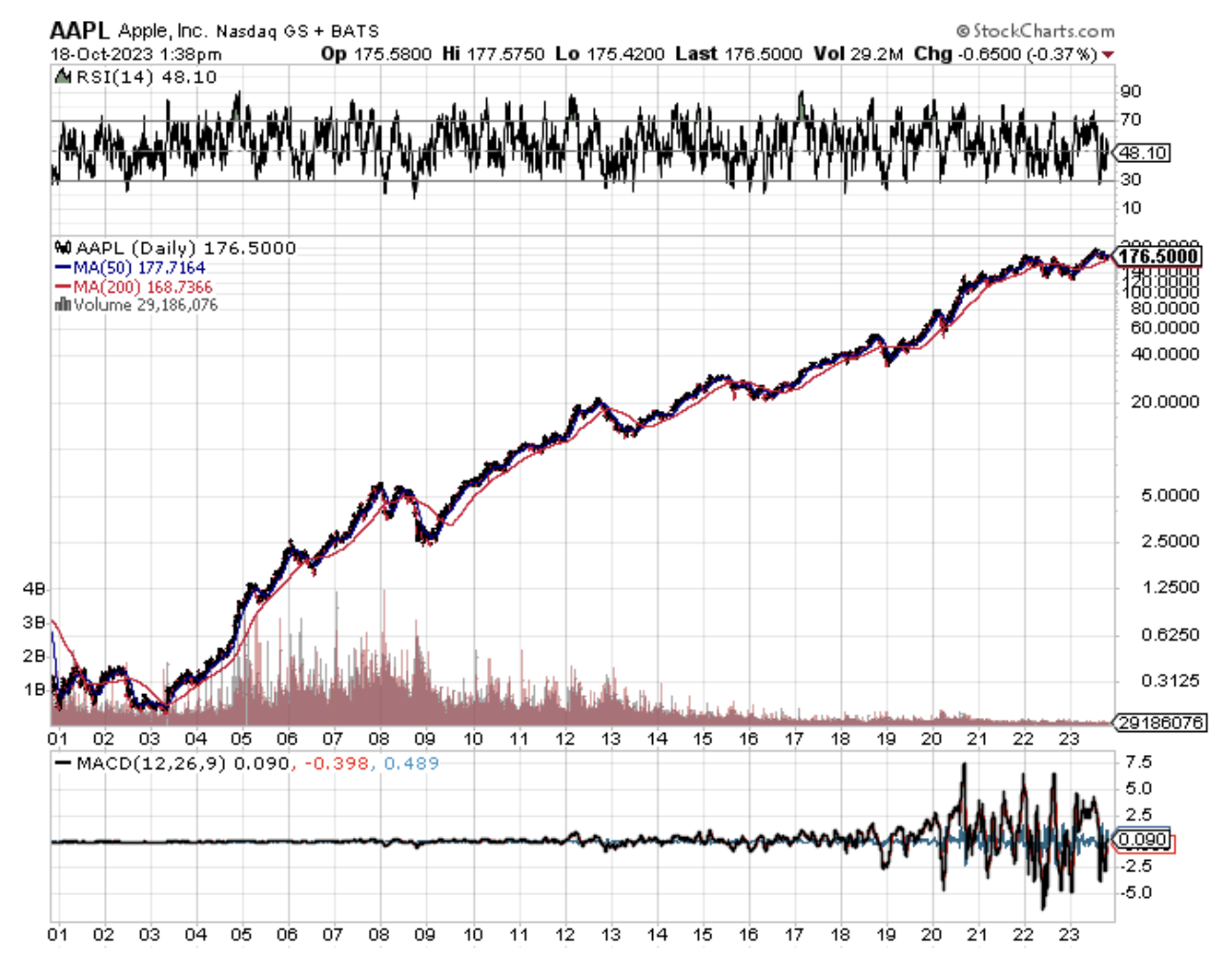

Silicon Valley residents will immediately recognize this character as Steve Jobs, the co-founder of Apple (AAPL).

In 43 years, his firm created over $3 trillion of wealth for his shareholders, making it the largest in the world.

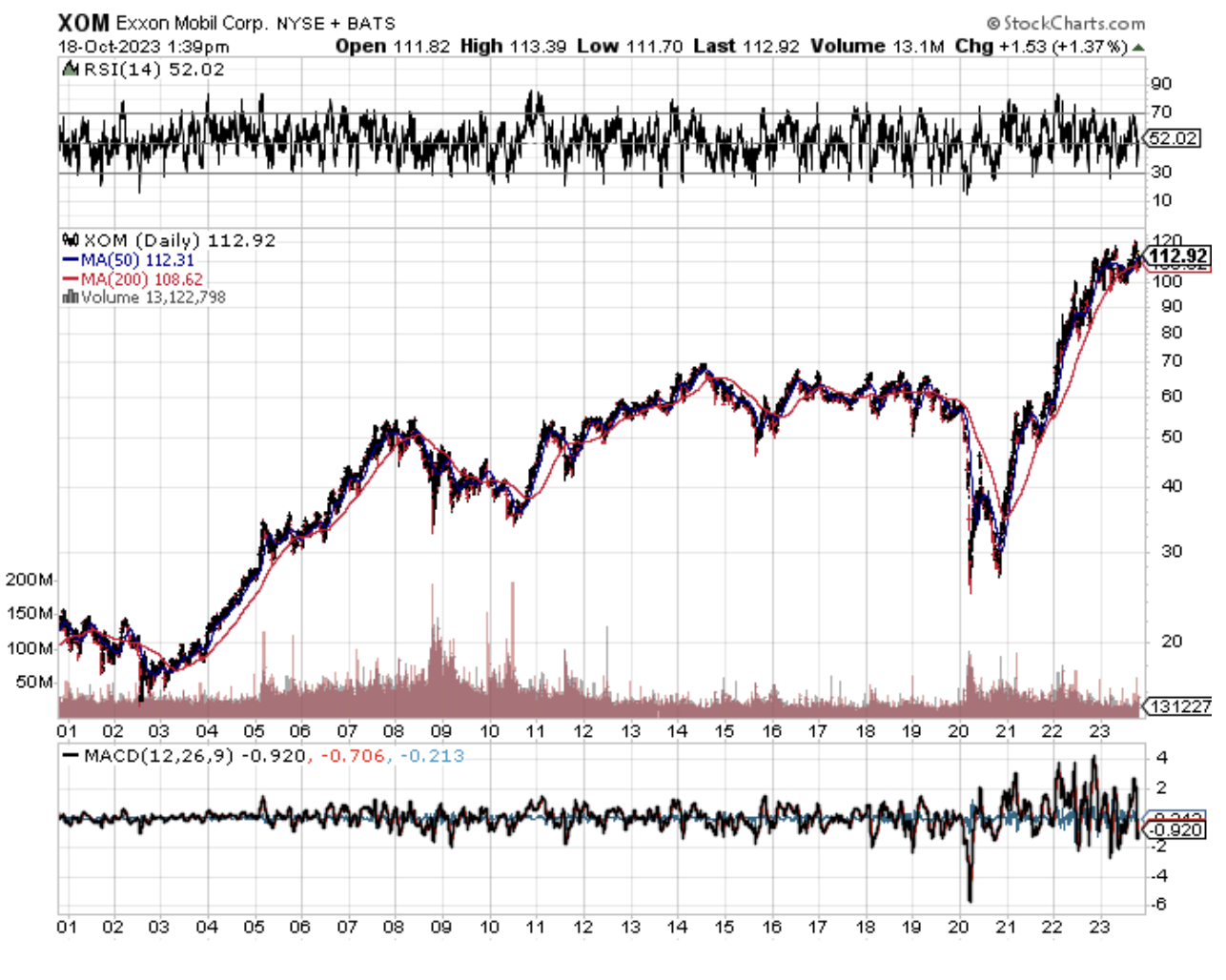

Until a decade ago, Exxon (XOM) held the top spot, creating $900 million in new wealth, although to be fair, it took 100 years to do it.

To be completely and historically accurate, most of the original seven sister oil companies are decedents of John D. Rockefeller’s Standard Oil Company.

Add the present value of these together, and Rockefeller is far and away the biggest money maker of all time. And he made most of this before income taxes were invented in 1913!

Reviewing the performance of other top-performing companies, it is truly amazing how much wealth was created from a technology boom that started in the 1980s.

Investors’ laser-like focus on the Magnificent Seven is well justified.

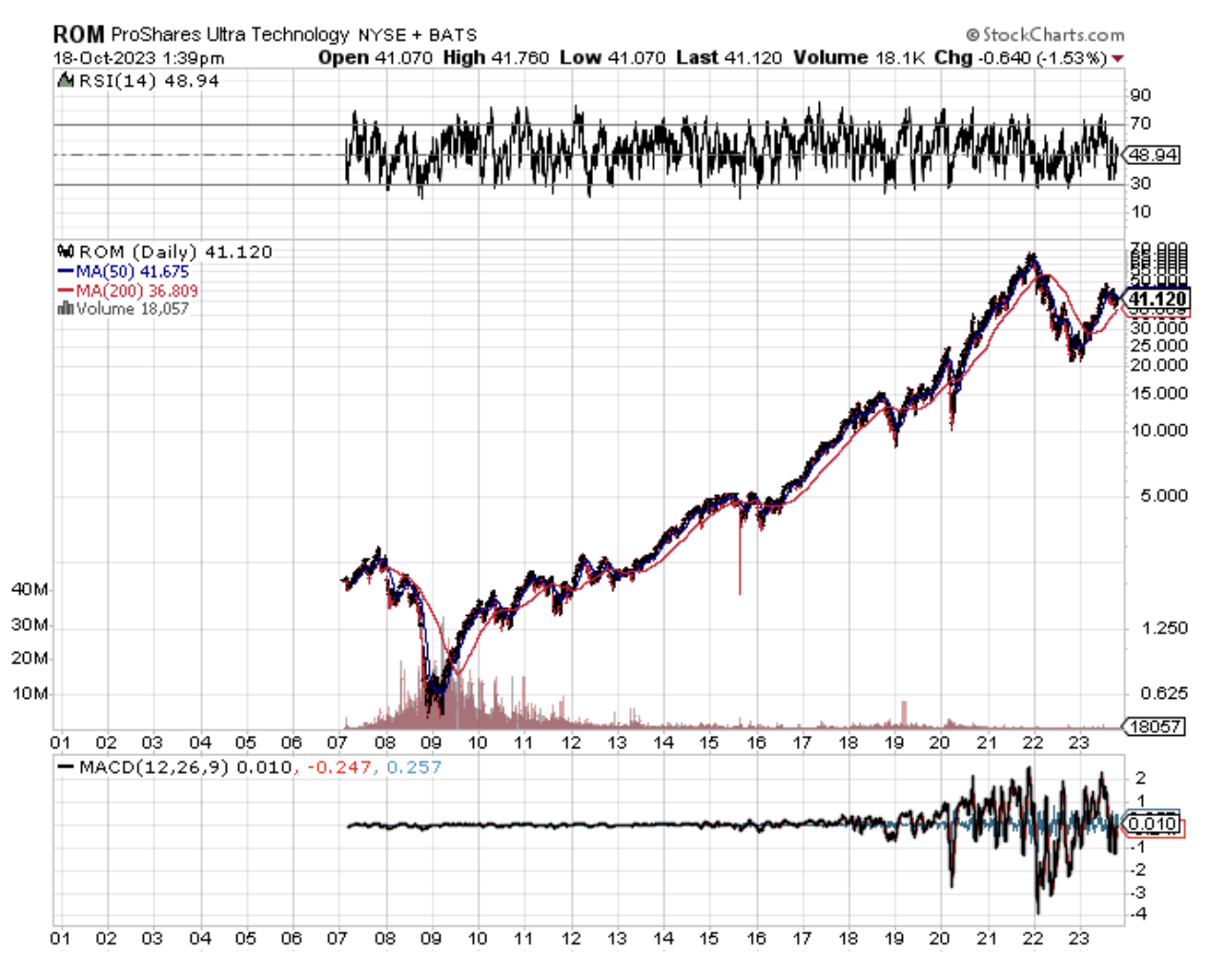

That’s why I often tell guests during my lectures around the world that if they really want to be lazy, just buy the ProShares Ultra Technology ETF (ROM) and forget everything else.

Another college dropout’s efforts, those of Bill Gates Microsoft (MSFT), produced an annualized return of 25% since 1986. That made him the third greatest wealth creator in history.

It also made him the world's richest man, until Jeff Bezos and Elon Musk came along. Gates is thought to have single-handedly created an additional 1,000 millionaires as so many employees were aided in stock options.

Facebook (FB) is the youngest on the list of top money makers, creating an annualized 34.5% return since it went public in 2012.

Alphabet (GOOG) is the second newest on the list, racking up a 24.9% annualized return since 2004.

Amazon (AMZN) is 14th on the list of all-time wealth creators and has just entered its 20th year as a public company.

Being an armchair business and financial historian, many runners-up were major companies in my day, but generate snores among Millennials now.

Believe it or not, General Motors (GM) still ranks as the 8th greatest wealth creator of all time, even though it went bankrupt in 2008.

Ma Bell or AT&T (T) ranks number 17th but was merged out of existence in 2005. A regrouping of Bell System spinoffs possesses the (T) ticker symbol today.

Among its distant relatives are Comcast (CCV) and Verizon Communications (VZ).

Warren Buffet’s Berkshire Hathaway (BRKY) ranks 12th as an income generator, with an annualized return of only 11.94%.

Its performance is diluted by the low returns afforded by the textile business before Buffet took it over in 1962. Buffet’s returns since then have been double that.

Analyzing the vast expanse of data over the last 100 years proves that single stock picking is a mug's game.

Since 1926, only 4% of publically traded stocks made ALL of the wealth generated by the stock market.

The other 96% either made no money to speak of, or went out of business.

This is why the Mad Hedge Fund Trader focuses on only 10%-20% of the market at any given time, the money-making part.

In other words, you have a one in 25 chance of picking a winner.

A modest 30 companies accounted for 30% of this wealth, while 50 stocks accounted for 40%.

You can only conclude that stocks make terrible investments, not even coming close to beating the minimal returns of one-month Treasury bills, a cash equivalent.

It also is a strong argument in favor of indexed investment in that through investing in all major companies, you are guaranteed to grab the outsized winners.

That is unless you follow the Diary of a Mad Hedge Fund Trader, which picked Amazon, Apple, Facebook, Google, NVIDIA, and Tesla right out of the gate.

If you want to learn more about the number crunching behind this piece, please visit the research of Hendrik Bessembinder at the W.P. Carey School of Business at Arizona State University.

Such a Money Maker!

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/Steve-Jobs-Oct17.png316637MHFTFhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTF2023-10-19 09:04:372023-10-19 18:13:31Who Was the Greatest Wealth Creator in History?

I am constantly on the lookout for ten baggers, stocks that have the potential to rise tenfold over the long term.

Look at the great long-term track records compiled by the most outstanding money managers, and they always have a handful of these that account for the bulk of their outperformance, or alpha, as it is known in the industry.

I’ve found another live one for you.

News came out last week that Elon Musk’s SpaceX has just landed a $70 million contract with the Department of Defense for the creation of its military Star Shield satellite network.

Elon Musk’s SpaceX is so forcefully pushing forward rocket technology that he is setting up one of the great investment opportunities of the century.

In the past decade, his start-up has accomplished more breakthroughs in advanced rocket technology than seen in the last 60 years, since the golden age of the Apollo space program.

As a result, we are now on the threshold of another great leap forward into space. Musk’s ultimate goal is to make mankind an “interplanetary species.”

There is only one catch.

SpaceX is not yet a public company, being owned by a handful of fortunate insiders and venture capital firms. But you should get a shot at the brass ring someday.

The rocket launch and satellite industry is the biggest business you have never heard of, accounting for $200 billion a year in sales globally. This is probably because there are no pure stock market plays.

Only two major companies are public, Boeing (BA) and Lockheed Martin (LMT), and their rocket businesses are overwhelmed by other aerospace lines.

The high value-added product here is satellite design and construction, with rocket launches completing the job.

Once dominated by the US, the market for launches has long since been ceded to foreign competitors. The business is now captured by Europe (the Arianne 5), and China (the Long March 5). Space business for Russia and itsAngara A5 rocket abruptly ended with its invasion of Ukraine.

Until recently, American rocket makers were unable to compete because decades of generous government contracts enabled costs to spiral wildly out of control.

Whenever I move from the private to the governmental sphere, I am always horrified by the gross indifference to costs. This is the world of the $10,000 coffee maker and the $20,000 toilet seat.

Until 2010, there was only a single US company building rockets, the United Launch Alliance (ULA), a joint venture of Boeing and Lockheed Martin. ULA builds the aging Delta IV and Atlas V rockets.

The vehicles are launched from Cape Canaveral, Florida and Vandenberg Air Force Base in California, both of which I had the privilege to witness. They look like huge Roman candles that just keep on going until they disappear into the blackness of space.

Enter SpaceX.

Extreme entrepreneur Elon Musk has shown a keen interest in space travel throughout his life. The sale of his interest in PayPal, his invention, to eBay (EBAY) in 2002 for $165 million, gave him the means to do something about it.

He then discovered Tom Mueller, a childhood rocket genius from remote Idaho who built the largest ever amateur liquid-fueled vehicle, with 13,000 pounds of thrust. Musk teamed up with Mueller to found SpaceX in 2002.

Two decades of grinding hard work, bold experimentation, and heart-rending testing ensued, made vastly more difficult by the 2008 Great Recession.

SpaceX’s Falcon 9 first flew in June 2010 and successfully orbited Earth. In December 2010, it launched the Dragon space capsule and recovered it at sea. It was the first private company ever to accomplish this feat.

Dragon successfully docked with the International Space Station (ISS) in May 2012. NASA has since provided $440 million to SpaceX for further Dragon development.

The result was the launch of the Dragon V2 (no doubt another historical reference) in May 2014, large enough to carry seven astronauts.

The largest SpaceX rocket now in testing has Mars capability, the 27-engine, 394-foot-high Starship, the largest rocket ever built.

Commit all these names to memory. You are going to hear a lot about them.

Musk’s spectacular success with SpaceX can be traced to several different innovations.

He has taken the Silicon Valley hyper-competitive ethos and financial model and applied it to the aerospace industry, the home of the bloated bureaucracy, the no-bid contract, and the agonizingly long time frame.

For example, his initial avionics budget for the early Falcon 1 rocket was $10,000 and was spent on off-the-shelf consumer electronics. It turns out that their quality had improved so much in recent years they met military standards.

But no one ever bothered to test them. $10,000 wouldn’t have covered the food at the design meetings at Boeing or Lockheed Martin, which would have stretched over the years.

Similarly, Musk sent out the specs for a third-party valve actuator no more complicated than a garage door opener, and a $120,000, one-year bid came back. He ended up building it in-house for $3,000. Musk now tries to build as many parts in-house as possible, giving it additional design and competitive advantages.

This tightwad, full speed ahead and damn the torpedoes philosophy overrides every part that goes into SpaceX rockets.

Amazingly, the company is using 3D printers to make rocket parts, instead of having each one custom-made.

Machines guided by computers carve rocket engines out of a single block of Inconel nickel-chromium super alloy, foregoing the need for conventional welding, a frequent cause of engine failures.

SpaceX is using every launch to simultaneously test dozens of new parts on every flight, a huge cost saver that involves extra risks that NASA would never take. It also uses parts that are interchangeable for all its rocket types, another substantial cost saver.

SpaceX has effectively combined three nine-engine Falcon 9 rockets to create the 27-engine Falcon Heavy, the world’s largest operational rocket. It has a load capacity of a staggering 53 metric tons, the same as a fully loaded Boeing 737 can carry. It has half the thrust of the gargantuan Saturn V moon rocket that last flew in 1973.

Musk is able to capture synergies among his three companies not available to any competitor. SpaceX gets the manufacturing efficiencies of a mass-production carmaker.

Tesla Motors has access to the futuristic space-age technology of a rocket maker. Solar City (SCTY) provides cheap solar energy to all of the above.

And herein lies the play.

As a result of all these efforts, SpaceX today can deliver what ULA does for 73% less money with vastly superior technology and capability. Specifically, its Falcon Heavy can deliver a 116,600-pound payload into low earth orbit for only $90 million, compared to the $380 million price tag for a ULA Delta IV 57, 156-pound launch.

In other words, SpaceX can deliver cargo to space for $772 a pound, compared to the $7,515 a pound UAL charges the US government. That’s a hell of a price advantage.

You would wonder when the free enterprise system is going to kick in and why SpaceX doesn’t already own this market.

But selling rockets is not the same as shifting iPhones, laptops, watches, or cars. There is a large overlap with the national defense of every country involved.

Many of the satellite launches are military in nature and top secret. As the cargoes are so valuable, costing tens of millions of dollars each, reliability and long track records are big issues.

Enter the wonderful world of Washington DC politics. UAL constructs its Delta IV rocket in Decatur, Alabama, the home state of Senator Richard Shelby, the powerful head of the Banking, Finance, and Urban Affairs Committee.

The first Delta rocket was launched in 1960, and much of its original ancient designs persist in the modern variants. It is a major job creator in the state.

ULA has no rocket engine of its own. So it bought engines from Russia, complete with blueprints, hardly a reliable supplier. Magically, the engines have so far been exempted from the economic and trade sanctions enforced by the US against Russia for its invasion of Ukraine.

ULA has since signed a contract with Amazon’s Jeff Bezos-owned Blue Origin, which is also attempting to develop a private rocket business but is miles behind SpaceX.

Musk testified in front of Congress in 2014 about the viability of SpaceX rockets as a financially attractive, cost-saving option. His goal is to break the ULA monopoly and get the US government to buy American. You wouldn’t think this is such a tough job, but it is.

Elon became a US citizen in 2002 primarily to qualify for bidding on government rocket contracts, addressing national security concerns.

NASA did hold open bidding to build a space capsule to ferry astronauts to the International Space Station. Boeing won a $4.2 billion contract, while SpaceX received only $2.6 billion, despite superior technology and a lower price.

It is all part of a 50-year plan that Musk confidently outlined to me 25 years ago. So far, everything has played out as predicted.

The Holy Grail for the space industry has long been the building of reusable rockets, thought by many industry veterans to be impossible.

Imagine what the economics of the airline business would be if you threw away the airplane after every flight. It would cost $1 million for one person to fly from San Francisco to Los Angeles.

This is how the launch business has been conducted since the inception of the industry in the 1950s.

SpaceX is on the verge of accomplishing exactly that. It will do so by using its Super Draco engines and thrusters to land rockets at a platform at sea. Then you just reload the propellant and relaunch.

What's coming down the line? A SpaceX cargo business where you can ship high value products like semiconductors from Silicon Value to Australia in 30 minutes, or to Europe in 20 minutes.

Talk about disruptive innovation with a turbocharger!

The company has built its own spaceport in Brownsville, Texas that will be able to launch multiple rockets a day.

The Hawthorne, CA factory (where I charge my own Tesla S-1 when in LA) now has the capacity to build 160 rockets a year. This will eventually be ramped up to hundreds.

SpaceX is the only organization that offers a launch price list on its website (click here for that link), as much as Amazon sells its books. The Falcon 9 will carry 28,930 pounds of cargo into low earth orbit for only $60.2 million. Sounds like a bargain to me.

This no doubt includes an assortment of tax breaks, which Musk has proven adept at harvesting. Elon has been a quick learner of the ways of Washington.

Customers have included the Thai telecommunications firm, Rupert Murdock’s Sky News Japan, an Israeli telecommunications group, and the US Air Force.

So when do we mere mortals get to buy the stock? Analysts now estimate that SpaceX is worth up to $200 billion.

The current exponential growth in broadband and SpaceX’s Starlink will lead to a similar growth in satellite orders, and therefore rocket launches. So the commercial future of the company looks especially bright.

However, Musk is in no rush to go public. A permanent, viable, and sustainable colony on Mars has always been a fundamental goal of SpaceX. It would be a huge distraction for a publicly managed company. That makes it a tough sell to investors in the public markets.

You can well imagine that the next recession would bring cries from shareholders for cost-cutting that would put the Mars program at the top of any list of projects to go on the chopping block. So Musk prefers to wait until the Mars project is well established before entertaining an IPO.

Musk expects to launch a trip to Mars by 2027 and establish a colony that will eventually grow to 80,000. Tickets will be sold for $500,000. Click here for the details.

There are other considerations. Many employees and early venture capital investors wish to realize their gains and move on. Public ownership would also give the company extra ammunition for cutting through Washington red tape. These factors point to an IPO that is earlier than later.

On the other hand, Musk may not care. The last net worth estimate I saw for his net worth was $300 billion. If his many companies increase in value by ten times over the next decade, as I expect, that would increase his wealth to $3 trillion, making him the richest person in the world by miles.

If an IPO does come, investors should jump in with both boots. While the value of the firm may have already increased tenfold by then, there may be another tenfold gain to come. Get on the Elon Musk train before it leaves the station.

To describe Elon as a larger-than-life figure would be something of an understatement. Musk is the person on which the fictional playboy/industrialist/technology genius, Tony Stark in the Iron Man movies, has been based.

Musk has said he wishes to die on Mars, but not on impact. Perhaps it would be the ideal retirement for him, say around 2045 when he will be 75.

To visit the SpaceX website, please click here. It offers very cool videos of rocket launches and a discussion with Elon Musk on the need for a Mars mission.

Catching a Dragon by the Tail

This Could Be the Stock Performance

Is Mars the Next Hot Retirement Spot?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/05/Capsule-Re-entry-Parashutes-e1432763072757.jpg400264DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2023-10-10 09:02:522023-10-10 19:45:23Will SpaceX Be Your Next Ten Bagger?

Thanks to China's “one child only” policy adopted 40 years ago, and a cultural preference for children who grow up to become family safety nets, there are now 32 million more boys under the age of 20 than girls.

Large-scale interference with the natural male-to-female ratio has been tracked with some fascination by demographers for years and is constantly generating unintended consequences.

Until early in the last century, starving rural mothers abandoned unwanted female newborns in the hills to be taken away by “spirits.” Today, pregnant women resort to the modern-day equivalent by getting ultrasounds and undergoing abortions when they learn they are carrying girls.

Millions of children are “little emperors,” spoiled male-only children who have been raised to expect the world to revolve around them. The resulting shortage of women has led to an epidemic of “bride kidnapping” in surrounding countries. Stealing of male children is widespread in Vietnam, Cambodia, Laos, and Mongolia.

The end result has been a barbell-shaped demographic curve unlike that seen in any other country. The Beijing government says the program has succeeded in bringing the fertility rate from 3.0 down to 1.8, well below the 2.1 replacement rate. As a result, the Middle Kingdom's population today is only 1.2 billion instead of the 1.8 billion it would have been.

Political scientists have long speculated that an excess of young men would lead to more bellicose foreign policies by the Middle Kingdom. But so far the choice has been for commerce, to the detriment of America's trade balance and Internet security.

In practice, the one-child policy has only been applied to those who live in cities or have government jobs. That is about two-thirds of the population. On my last trip to China, I spent a weekend walking around Shenzhen city parks. The locals doted over their single children, while visitors from the countryside played games with their three, four, or five children. The contrast couldn’t have been more striking.

Economists now wonder if the practice will also shave points offChina's long-term economic growth rate. The early evidence is that it did. Parents with boys tend to be bigger savers, so they can help sons with the initial big-ticket items in life, like education, homes, and even cars.

The end game for this policy has to be the Japanese disease; a huge population of senior citizens with insufficient numbers of young workers to support them. The markets won't ignore this.

In the latest round of reforms announced by the Chinese government was the demise of the one-child policy. But no matter how hard you try; you can’t change the number of people born 40 years ago. The boomerang effects of this policy could last for centuries.

While recently winging my way across the South Pacific a few years ago and browsing the local papers, I spotted an unusual job offer:

WANTED: Social worker, tax-free salary of $60,000 with free accommodation and transportation, no experience necessary, must be flexible and self-sufficient.

With the unemployment rate rising for recent college grads, I was amazed that they were even advertising for such a job. Usually, such plum positions get farmed out to a close relative of the hiring officials involved.

Intrigued, I read on.

To apply, you first had to fly to Auckland, New Zealand, then catch a flight to Tahiti. After that you must endure another long flight to the remote Gambler Island, then charter a boat for a 36-hour voyage.

Once there, you had to row ashore to a hidden cove on the island, as there was no dock or even a beach.

It turns out that the job of a lifetime is on remote Pitcairn Island, some 2,700 miles ENE of New Zealand, home to the modern descendants of the mutineers of the HMS Bounty.

History buffs will recall that in 1790, Fletcher Christian led a rebellion against the tyrannical Captain William Bligh, casting him adrift in a lifeboat.

He then kidnapped several Tahitian women and disappeared off the face of the earth. When he stumbled across Pitcairn, which was absent from contemporary naval charts, he burned the ship to avoid detection.

An off-course British ship didn’t find the island until some 40 years later, only to find that Christian had been killed for his involvement in a love triangle decades earlier.

The job is not without its challenges. There is only one doctor, and electric power is switched on only 10 hours a day. Supply ships visit every three months. The local language is a blend of 18th century English and Tahitian called Pitkern, for which there is no dictionary.

Previous workers have a history of going native. Oh, and 10% of the island’s 54 residents are registered sex offenders, due to its long history of incest.

The next time someone you know complains about being unable to find a job, just tell them they are not looking hard enough, and to brush up on their Pitkern.

For more on the job situation, please visit my website by clicking here.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Bounty-ship-story-2-image-1-e1526508746559.jpg242350MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2023-10-03 09:02:382023-10-03 12:51:08Who Says There Aren't Any Good Jobs?

I have long told my listeners at conferences, webinars, and strategy luncheons my definition of the “new inflation”: the price for whatever you have to buy is rising, as with your home, health care, and a college education.

The price of the things you need to sell, such as your labor and services, is falling.

So while official government numbers show that the overall rate of inflation is muted at multigenerational highs, the reality is that the standard of living of most Americans is being squeezed at an alarming rate by both startling price increases and real wage cuts.

I finally found someone who agrees with me.

David Stockman was president Ronald Reagan’s director of the Office of Management and Budget from 1981-1985. I regularly jousted with David at White House press conferences, pointing out that the budgets he was proposing would not produce a balanced budget, as he claimed.

Instead, I argued that they would lead to an enormous expansion of the federal deficit. In the end, I was right, with the national debt growing 400% during the Reagan years.

To his credit, David later admitted to running two sets of books for the national accounts, one for external consumption for people like me, and a second internal one for the president with much more dire consequences.

When David finally made the second set of books public, there was hell to pay. It was a fiery departure. I knew Ronald Reagan really well, and when the cameras weren’t rolling, he could get really angry.

After a falling out with Reagan over exactly the issues I brought up, Stockman disappeared for three decades.

He is now back with a vengeance.

He is running a blog named David Stockman’s Contra Corner (click here for the link at http://davidstockmanscontracorner.com ), a site he says “where mainstream delusions and cant about the Welfare State, the Bailout State, Bubble Finance, and Beltway Banditry are ripped, refuted and rebuked.” (Good writing was never his thing).

Despite this rant, there is no place I won’t go to discover some valid arguments and useful statistics, and Stockman is no exception.

For a start, home utility prices have been skyrocketing for the past decade, nearly doubling. Over the last 12 months alone, it has jumped by 5.3%, while natural gas is up more than 10%, compared to an annual Consumer Price Index rise of only 3.3%.

But utilities have such a low 5% weighting in the Fed’s inflation calculation it barely moves the needle.

Wait, it gets better.

Gasoline costs have also been on a relentless uptrend since the nineties. Crude oil is up from a $10 low to today’s print of $95. Retail gasoline has popped from $1 a gallon to $5.50 in California, and that’s off from the year’s high at $3.50.

That works out to an annualized increase of 57%, or more than triple the official inflation rate.

The nation’s 40 million renting households have been similarly punished with price increases. They have averaged a 5.0% annual rate, nearly double the inflation rate.

The country’s 75 million homeowners are getting hit in the pocketbook as well. They have seen the cost of water, sewer, and trash collection balloon at a 4.8% annualized rate. And this has been an almost entirely straight-line move, with no pullbacks. And home insurance? It is absolutely through the roof.

David recites a dirty laundry list of Fed omissions and understatements on the inflation front, including gold, silver, and commodities prices.

All of these nickels and dimes add up to quite a lot for a family of four who is trying to scrape by on a median household income of $69,000 a year. And Heaven help you if you try to live on that in California.

The cost of a few items has declined, but not by much. They are largely composed of cheap import substitutes from Asia, including apparel, shoes, household furniture, consumer electronics, toys, and appliances.

One area the Fed data doesn’t remotely come close to measuring is the plunging cost of technology. How do you measure the savings from products that didn’t exist 20 years ago, like smart phones, iPods, iPads, and solid-state hard drives? How do you measure the cost of services that are handed out for free as Google, Facebook, and X do?

I can personally tell the cost of my own business is probably 90% cheaper to run than it would have three decades ago. I remember shelling out $5,000 for a COMPAQ PC that costs $300 today but has 1,000 times the performance.

David finishes withhis usual tirade against the Fed, accusing them of obsessing over the noise of the daily data releases and missing the long-term trend.

Anyone like myself who watched in horror how long it took our central bank to recognize the seriousness of the 2008 financial crisis pr the pandemic would agree.

This all reminds me of what a college Economics professor once told me during the late 1960’s. “Statistics are like a bikini bathing suit. What they reveal is fascinating, but what they conceal is essential.”

What They Reveal is Fascinating....

https://www.madhedgefundtrader.com/wp-content/uploads/2015/08/Bikini-Clad-Girl.jpg410316Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-09-20 09:02:032023-09-20 16:22:14Tackling the Low Inflation Myth

I have been following quantum computing since they moved from the theoretical to the practical about five years ago.

The reason is very simple. They promise to bring a 1 trillion-fold increase in computing power at zero cost, promising to solve in seconds some of the world’s most vexing problems.

They also have the potential to ramp the stock market up at least ten times over the next decade and bring on a new golden age. No kidding!

Last week an academic paper leaked and was quickly withdrawn suggesting that Google has accomplished a major breakthrough in the field.

Google claims to have built the first quantum computer that can carry out calculations beyond the ability of today’s most powerful supercomputers, a landmark moment that has been hotly anticipated by researchers.

A paper by Google’s researchers was briefly posted earlier this week on a NASA website before being removed, claiming that their processor was able to perform a calculation in three minutes and 20 seconds that would take today’s most advanced classical computer, known as Summit, approximately 10,000 years. Yikes!

The researchers said this meant “quantum supremacy” when quantum computers carry out calculations that had previously been impossible, had been achieved. This dramatic speed-up relative to all known classical algorithms provides an experimental realization of quantum supremacy on a computational task and heralds the advent of a much-anticipated computing paradigm. This experiment marks the first computation that can only be performed on a quantum processor.

The system can only perform a single, highly technical calculation, according to the researchers, and the use of quantum machines to solve practical problems is still years away. But the Google researchers called it “a milestone towards full-scale quantum computing”.

They also predicted that the power of quantum machines would expand at a “double exponential rate”, compared to the exponential rate of Moore’s Law, which has driven advances in silicon chips in the first era of computing. That means a potential doubling of computing power every nine months with a halving of cost.

While prototypes of so-called quantum computers do exist, developed by companies ranging from IBM (IBM) to start-ups such as Rigetti Computing, they can only perform the same limited tasks classical computers can, albeit quicker. There is also a huge problem accessing stored data. Quantum computers, if they can be built at scale, will harness properties that extend beyond the limits of classical physics to offer exponential gains in computing power.

A November 2018 report by the Boston Consulting Group said they could “change the game in such fields as cryptography and chemistry (and thus material science, agriculture, and pharmaceuticals) not to mention artificial intelligence and machine learning . . . logistics, manufacturing, finance, and energy”.

Unlike the basic binary elements of classical computers, or bits, which represent either zeros or ones, quantum bits, or “qubits”, can represent both at the same time. By stringing together qubits, the number of states they could represent rises exponentially, making it possible to compute millions of possibilities instantly.

Some researchers have warned against overhyping the quantum supremacy, arguing that it does not suggest that quantum machines will quickly overtake traditional computers and bring a revolution in computing. Led by John Martinis, an experimental physicist from the University of California, Santa Barbara, Google first predicted it would reach quantum supremacy by the end of 2017. But the system it built, linking together 72 qubits proved too difficult to control. It eventually revamped the system to create a 53-qubit design it codenamed Sycamore.

The system was given the task of proving that a random-number generator was truly random. Though that job has little practical application, the Google researchers said that “other initial uses for this computational capability” included machine learning, materials science, and chemistry.

“It’s a significant milestone, and the first time that somebody has shown that quantum computers could outperform classical computers at all,” said Steve Brierley, founder of quantum software start-up Riverlane, who has worked in the field for 20 years and is an adviser on quantum technologies to the UK government. “It’s an amazing achievement.”

To illustrate where we are with Quantum computers today, think of it as 1945, when only five mainframe computers existed in the world, all in the US and England. That’s when IBM founder Thomas Watson famously predicted that “The total market for computers is five.”

Oops.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/10/mainframes.png486864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-30 09:02:252023-08-30 14:58:26Google’s Major Breakthrough in Quantum Computing

One of the most fascinating things I learned when I first joined the equity trading desk at Morgan Stanley during the early 1980s was how to parallel trade.

A customer order would come in to buy a million shares of General Motors (GM) and what did the in-house proprietary trading book do immediately?

It loaded the boat with the shares of Ford Motors (F).

When I asked about this tactic, I was taken away to a quiet corner of the office and read the riot act.

“This is how you legally front-run a customer,” I was told.

Buy (GM) in front of a customer order, and you will find yourself in Sing Sing shortly.

Ford (F), Toyota (TM), Nissan (NSANY), Daimler Benz (DDAIF), BMW (BMWYY), or Volkswagen (VWAPY), are no problem.

The logic here was very simple.

Perhaps the client completed an exhaustive piece of research concluding that (GM) earnings were about to rise.

Or maybe a client's old boy network picked up some valuable insider information.

(GM) doesn’t do business in isolation. It has tens of thousands of parts suppliers for a start. While whatever is good for (GM) is good for America, it is GREAT for the auto industry.

So through buying (F) on the back of a (GM) might not only match the (GM) share performance, it might even exceed it.

This is known as a Primary Parallel Trade.

This understanding led me on a lifelong quest to understand Cross Asset Class Correlations, which continue to this day.

Whenever you buy one thing, you buy another related thing as well, which might do considerably better.

I eventually made friends with a senior trader at Salomon Brothers while they were attempting to recruit me to run their Japanese desk.

I asked if this kind of legal front running happened on their desk.

“Absolutely,” he responded. But he then took Cross Asset Class Correlations to a whole new level for me.

Not only did Salomon’s buy (F) in that situation, they also bought palladium (PALL).

I was puzzled. Why palladium?

Because palladium is the principal metal used in catalytic converters, which remove toxic emissions from car exhaust, and has been required for every U.S. manufactured car since 1975.

Lots of car sales, which the (GM) buying implied, ALSO meant lots of palladium buying.

And here’s the sweetener.

Palladium trading is relatively illiquid.

So, if you catch a surge in the price of this white metal, you would earn a multiple of what you would make on your boring old parallel (F) trade.

This is known in the trade as a Secondary Parallel Trade.

A few months later, Morgan Stanley sent me to an investment conference to represent the firm.

I was having lunch with a trader at Goldman Sachs (GS) who would later become a famous hedge fund manager and asked him about the (GM)-(F)-(PALL) trade.

He said I would be an IDIOT not to take advantage of such correlations. Then he one-upped me.

You can do a Tertiary Parallel Trade here through buying mining equipment companies such as Caterpillar (CAT), Cummins (CMI), and Komatsu (KMTUY).

Since this guy was one of the smartest traders I ever ran into, I asked him if there was such a thing as a QuaternaryParallel Trade.

He answered “Abso******lutely,” as was his way.

But the first thing he always did when searching for Quaternary Parallel Trades would be to buy the country ETF for the world’s largest supplier of the commodity in question.

In the case of palladium, that would be South Africa (EZA), the world's largest non-sanctioned producer, which together accounts for 74% with Russia of the world’s total production.

Since then, I have discovered hundreds of what I can Parallel Trading Chains, and have been actively making money off of them. So have you, you just haven’t realized it yet.

I could go on and on.

If you ever become puzzled or confused about a trade alert I am sending out (Why on earth is he doing THAT?), there is often a parallel trade in play.

Do this for decades as I have and you learn that some parallel trades break down and die. The cross relationships no longer function.

The best example I can think of is the photography/silver connection. When the photography business was booming, silver prices rose smartly.

Digital photography wiped out this trade, and silver-based film development is still only used by a handful of professionals and hobbyists.

Oh, and Eastman Kodak (KODK) went bankrupt in 2012.

However, it seems that whenever one Parallel Trading Chain disappears, many more replace it.

You could build chains a mile long simply based on how well Apple (AAPL) is doing.

And guess what? There is a new parallel trade in silver developing. For whenever someone builds a solar panel anywhere in the world, they are using a small amount of silver for the wiring. Build several tens of millions of solar panels and that can add up to quite a lot of silver.

What goes around comes around.

Suffice it to say that parallel trading is an incredibly useful trading strategy.

Ignore it at your peril.

Sometimes Markets are Hard to Figure Out

https://www.madhedgefundtrader.com/wp-content/uploads/2023/06/john-thomas-mourning.jpg177171Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-08-10 09:02:402023-08-10 13:53:53How to Gain an Advantage with Parallel Trading

By the time you read this, I will be on a flight to New York City where I will meet with Concierge clients and host my Strategy Luncheon.

I will eventually end up at my chalet in Zermatt, Switzerland where I traditionally restart my year. Weather permitting, I will climb the 14,692-foot Matterhorn again. Is it seven times this year, or eight? I can’t remember.

Otherwise, I’ll rejoin Zermatt Search and Rescue again visiting old friends and pulling stranded Americans off of Alpine peaks. It seems I’m the only one up there who has a sense of humor and speaks English.

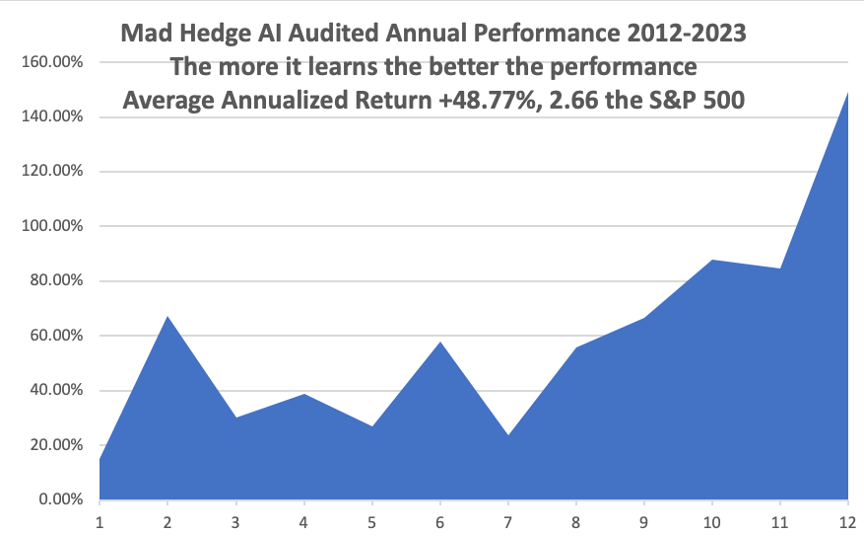

I leave you with a “mission accomplished.” We are closing out the first half up +64.39% so far in 2023. If all three remaining positions expire at max profit, we will be up +66.40%.

While most investors are only slowly becoming aware that we are in a bull market, you got the heads-up last October. Since the October 13 low, Mad Hedge has gained an awesome +76.15%! This is a year when a lot of people are wrong and YOU are right.

I have worked the hardest in my life the past year, and it is time for a break. I have also put myself through the most grueling training regimen ever, hiking 2,000 miles in torrential rains and snowshoeing another 600, all with a 50-pound pack.

Covid took a lot out of me in 2022.

Every year, it seems to get harder to keep the calendar at bay.

Getting out into the real world and soaking up new data and opinions is invaluable in shaping my own global view, and your performance benefits from it.

I will be traveling with my laptop and keeping in touch with the markets. While 18th century Internet service is passable, the bandwidth can be snail-like. So, unless I see something extraordinary, I will cut back on new Trade Alerts.

I never actually STOP working, I just change my office location from home offices in Incline Village and San Francisco, to a French castle, and Italian villa, or a Mediterranean mega yacht.

So, I deserve a break. I am risking over trading. I need to spend some time alone on a mountaintop, communing with the spirits, attempting to discover the new long-term market trends hiding themselves in the mist.

While on the road, I will continue writing my newsletter, giving you my daily dose of market insight. I will also be re-running some of my favorite research pieces from the past when my travel schedule does not allow Internet access.

This is to expose my thousands of new subscribers to the golden oldies and to remind the legacy readers who have since forgotten them.

I will be back in San Francisco in early August, glued to my screens once again for another year of toil in the salt mines. In the meantime, please feel free to email me. Concierge members can call me any time for free on WhatsApp.

In the meantime, I shall be raising a glass to all of you at dinner, the loyal readers of The Diary of a Mad Hedge Fund Trader. Salute! Prost! Kampai, and Cheers! Thanks for making this letter a huge success!

If you want to take the opportunity to meet me in person, please find my strategy luncheon schedule below. To purchase tickets for the luncheons, please go to my online store and click on the country and city of your choice.

Thursday, July 6, 12:00 PM New York City

Thursday, July 13, 12:00 PM Seminar at Sea on the Queen Mary II

Thursday, July 19, 12:00 PM London England

Friday, July 27, 3:00 PM Cortina d’Ampezzo, Italy

Thursday, August 1, 12:00 PM Florence Italy

Thursday, August 4, 12:00 PM Vienna Austria

Saturday, August 5, 12:00 PM Rome Italy

I look forward to seeing you there, and thanks for supporting my research.

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

Mad Hedge Market Timing Index

Now Which One of These is for Austria?

https://www.madhedgefundtrader.com/wp-content/uploads/2023/06/john-thomas-red-wine.jpg292317Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-30 09:02:182023-06-30 12:14:08Taking Off for the 2023 Mad Hedge World Tour

Recently, I have been touting a 2022 track record of +84.63%.

I have a confession to make.

I lied.

In actual fact, my performance was far higher than that. In reality, I generated a multiple of that +84.63% figure.

That is because my published performance is only for my front-month short-term trade alerts. It does not include the LEAPS recommendations (Long Term Equity Anticipation Securities) issued in 2022, the details of which I include below.

LEAPS have the identical structure as a front month vertical bull call debit spread. The only difference is that while front-month call spreads have expiration dates of less than 30 days, LEAPS go out to 18-30 months.

LEAPS also have strike prices far out of-the-money instead of deep in-the-money, giving you infinitely more upside leverage. LEAPS are actually synthetic futures contracts on the underlying stock.

Of the 12 LEAPS executed in 2022, eight made money and four lost. But the successful trades win big, up to 1,260% in the case of NVDIA (NVDA). With the losers, you only write off the money you put up.

And you still have 18 months until expiration for my four losers, ample time for them to turn around and make money. In the case of my biggest loser for Rivian (RIVN), Tesla launched an unprecedented EV price way shortly after I added this position. Never take on Tesla in a price war. Black swans happen.

Of course, timing is everything in this business. I only add LEAPS during major market selloffs as the leverage is so great, over 20X in some cases, of which there were four in 2022.

If you would like to receive more extensive coverage of my LEAPS service, please sign up for the Mad Hedge Concierge Service where you can excess a separate website devoted entirely to LEAPS. Be aware that the Concierge Service is by application only, has a limited number of places, and there is usually a waiting list.

Given the numbers below, it is easy to understand why most professional full-time traders only invest their personal retirement funds in LEAPS.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Sweet Taste of LEAPS

https://www.madhedgefundtrader.com/wp-content/uploads/2023/06/john-thomas-red-wine.jpg292317Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-06-29 09:02:042023-06-29 12:30:12My 2022 LEAPS Track Record

One of the unfortunate aspects of the pandemic has been a tenfold increase in online fraud.

I get a dozen phishing attacks a day pretending to be Walmart, the Bank of America, and Amazon. And I never click on anything from Apple asking me to change my ID and password. The crooks are just getting too good.

However, where there are criminals there is investment gold.

The cybersecurity sector has been spurred upward with the rest of technology in recent months, creating a rare entry point on the cheap side of the longer-term charts.

The near-destruction of Sony (SNE) by North Korean hackers years ago has certainly put the fear of God into corporate America. Apparently, they have no sense of humor whatsoever north of the 38th parallel.

As a result, there is a generational upgrade in cybersecurity underway, with many potential targets boosting spending by multiples.

It’s not often that I get a stock recommendation from an army general. That is exactly what happened the other day when I was speaking to a three-star about the long-term implications of the escalating trade war.

He argued persuasively that the world will probably never again see large-scale armies fielded by major industrial nations. Wars of the future will be fought online, as they have been silently and invisibly over the past 20 years.

All of those trillions of dollars spent on big ticket, heavy metal weapons systems, like submarines and F-35 fighters ($122 million each) are pure pork designed by politicians to buy voters in marginal swing states.

The money would be far better spent where it is most needed, on the cyber warfare front. Needless to say, my friend shall remain anonymous.

The problem is that when wars become cheaper, you fight more of them, as is the case with online combat.

You probably don’t know this, but during the Bush administration, the Chinese military downloaded the entire contents of the Pentagon’s mainframe computers at least seven times.

This was a neat trick because these computers were in stand-alone, siloed, electromagnetically shielded facilities not connected to the Internet in any way. Here are essentially no secrets about anything anymore.

In the process, they obtained the designs of all of our most advanced weapons systems, including our best smart nukes. What have they done with this top-secret information?

Absolutely nothing.

Like many in senior levels of the US military, the Chinese have concluded that these weapons are a useless waste of valuable resources. Far better value for money are more hackers, coders, and servers, which the Chinese have pursued with a vengeance.

You have seen this in the substantial tightening up of the Chinese Internet through the deployment of the Great Firewall, which blocks local access to most foreign websites, including Wikipedia.

Try sending an email to someone in the middle Kingdom with a Gmail address. It is almost impossible. This is why Google (GOOG) closed their offices there years ago.

I know of these because several Chinese readers are complaining that they are unable to open my own Mad Hedge Trade Alerts, or access their foreign online brokerage accounts.

As a member of the Joint Chiefs of Staff recently told me, “The greatest threat to national defense is wasting money on national defense.”

Although my brass-hatted friend didn’t mention the company by name, the implication is that I need to go out and buy Palo Alto Networks (PANW) right now.

Palo Alto Networks, Inc. is an American network security company based in Santa Clara, California just across the water from my Bay area office.

The company’s core products are advanced firewalls designed to provide network security, visibility and granular control of network activity based on application, user, and content identification. To visit their website please click here.

Palo Alto Networks competes in the unified threat management and network security industry against Cisco (CSCO), FireEye (FEYE), Fortinet (FTNT), Check Point (CHKP), Juniper Networks (JNPR), and Cyberoam, among others.

The really interesting thing about this industry is that there really are no losers. That’s because companies are taking a layered approach to cybersecurity, parceling out contracts to many of the leading firms at once, looking to hedge their bets.

To say that top management has no idea what these products really do would be a huge understatement. Therefore, they buy all of them.

This makes a basket approach to the industry more feasible than usual. You can do this by buying the $435 million capitalized Pure Funds ISE Cyber Security ETF (HACK), which boasts CyberArk Software (CYBR and FireEye (FEYE) as its largest positions.

(HACK) has been a hedge fund favorite since the Sony attack.

For more information about (HACK), please click here.

And don’t forget to change your password.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/05/Hacker-image-story-3-image-5.jpg177285MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2023-06-28 09:02:232023-06-28 13:20:41Cybersecurity is Only Just Getting Started

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.