(LAST CHANCE TO ATTEND THE THURSDAY, MAY 18, 2023 TAMPA FLORIDA STRATEGY LUNCHEON)

(LOOKING AT THE LARGE NUMBERS)

(TLT), (TBT) (BITCOIN), (MSTR), (BLOK), (HUT)

I think it’s time for me to go out on strike. I’m downing my tools, tearing up my punch card, and manning a picket line.

I get up at 5:00 AM every morning, well before the sun rises here on the west coast, looking for great low-risk high return trades. But for the last several weeks, there have been none, nada, bupkiss.

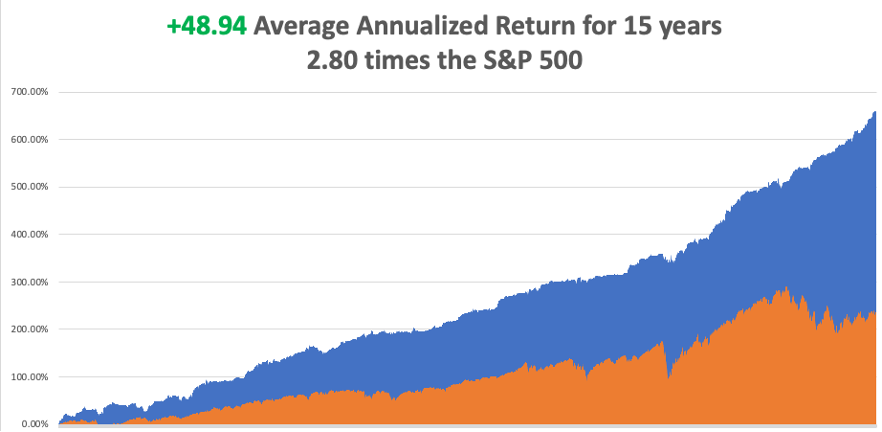

I have gotten spoiled over the last few years. The financial crisis, pandemic, recovery, and banking crisis provided me with an endless cornucopia of trading opportunities which doubled my average annualized return from 24% to a nosebleed 48.94%.

Part of the problem is that with a success rate of 90%, so much of the market is now copying my trades so that they are getting harder to execute. That wasn’t a problem when markets were booming. It is when trading volumes have shrunk dramatically, as they have done this year.

At The Economist magazine in London whenever plagiarism was discovered, they used to say that “Imitation is the sincerest former of flattery.”

There is no doubt that the economy is weakening, as the data has definitively shown over the last two weeks. It appears that after 500 basis points in interest rate rises in a year, the Fed’s harsh medicine is finally starting to work. The debt ceiling crisis, and regional banking crisis are scaring more investors further to the sidelines.

Notice how every stock market rally has become increasingly short-lived? Which all raises a heightened risk of recession.

Economies are like families. All are happy for the same reasons but are unhappy in myriad different ways.

In fact, they provide a generous helping of alphabet soup. If you look very closely, you can find some bay leaves, oregano, black pepper, and lots of V’s, W’s, U’s, and L’s.

Now, let’s play a game and see who can pick the letter that most accurately portrays the current economic outlook.

Here is a code key:

V – The very sharp collapse we saw in 2008 and again in 2020 is followed by an equally sharp recovery. I think it is safe to say we can now toss that one out the window. With technology hyper-accelerating, it is safe to write off the “V” recovery scenario.

W – The sharp recovery that began in October 2022 fails and we see a double dip back to those lows.

U – The economy stays at the bottom for a long time before it finally recovers.

L – The economy collapses and never recovers.

The question is, in which of these forecasts should we invest our hard-earned cash?

For a start, you can throw out the “L”. Every recession flushes out a lot of financial Cassandras who predict the economy will never recover. They are always wrong. Usually, they know more about marketing newsletters than economics.

I believe what we are seeing play out right now is the “W” scenario. This is the best possible scenario for traders, as it calls for a summer correction in the stock market when we can load the boat a second time. If you missed the October low you will get a second bite of the Apple (AAPL), both literally and figuratively.

If I’m wrong, we will get a “U”, a longer recovery. This cannot be dismissed lightly as the unemployment rate is clearly about to rise.

If I limited the outlook to only four possible scenarios, I’d be kidding you. The truth is far more complicated.

Each industry gets its own letter of the alphabet. Technology, some 27% of total stock market capitalization, gets no letter at all because it is thriving, thanks to the explosion of AI applications. That explains the single-minded pursuit of big tech by investors since January.

Someone asked me last week how long I would continue trading and I cited the example of Warren Buffett, who at 92 is 21 years older than me.

I have since found a better example.

Former Secretary of State under Nixon, Henry Kissinger, turns 100 this week, the only man in the world who President Biden, Vladimir Putin, and President Xi Jinping would immediately take a call from.

During the shuttle diplomacy between Israel and Egypt in 1974, I rode with the Secretary on Air Force One, then an antiquated Boeing 727, which is now in a museum in Seattle. For the rest of that story see below.

He gave me “Henry” privileges, while everyone else had to address him as “Mr. Secretary” because my knowledge of history exceeded that of anyone else then in the White House Press Corps, even those who had degrees in the subject.

It also helped that at that point I had already had six years of experience on the ground in the Middle East. It was all heady stuff for a journalist who at 22 was just starting out.

So, that sets the bar higher for me. The good news for you is that I’ll be sending out my wit, wisdom, and trade alerts for at least another 29 years.

So far in May, I have managed a modest +1.70% profit. My 2023 year-to-date performance is now at an eye-popping +63.45%. The S&P 500 (SPY) is up only a miniscule +8.15% so far in 2023. My trailing one-year return reached a 15-year high at +122.11% versus +6.70% for the S&P 500.

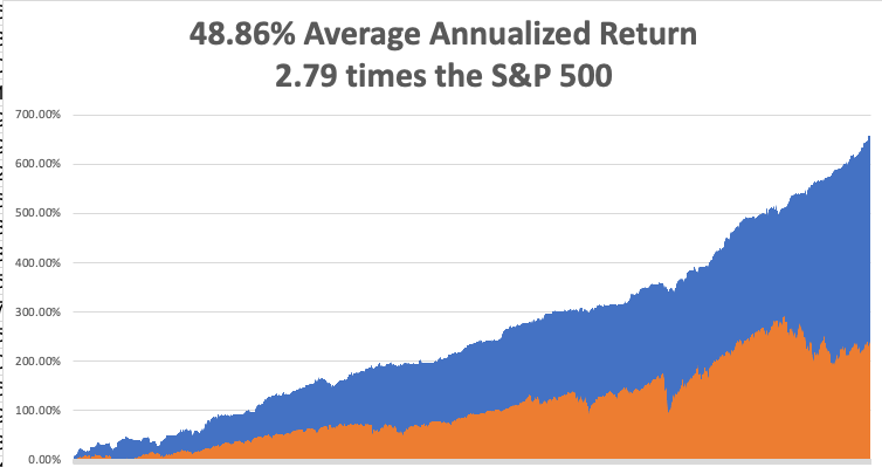

That brings my 15-year total return to +660.64%. My average annualized return has blasted up to +48.94%, another new high, some 2.80 times the S&P 500 over the same period.

Some 41 of my 44 trades this year have been profitable. My last 21 consecutive trade alerts have been profitable.

I initiated only one new trade last week, a long in Tesla (TSLA). That leaves me with my two remaining positions. Those include longs in Tesla and the bond market (TLT), which expires this coming Friday. I now have a very rare 80% cash position due to the lack of high-return, low-risk trades.

Treasury Secretary Yellen Warns of Economic Catastrophe, if the debt ceiling is not raised. Congress has voted 98 times to raise the debt ceiling to $31 trillion over 106 years to pay for money already spent. One-third of this was under the previous president who back then warned that he would default. It’s a grasp for power the House just doesn’t have. There really isn’t such a thing as a debt ceiling which has gained an importance far beyond its original housekeeping intention.

Boeing Lands Blockbuster 300 Plane Order, from Ireland’s Ryan Air worth $40 billion. Europe’s Top budget air carrier is loading up on the once troubled 737 MAX. Keeping buying (BA) on dips, now the world’s largest aircraft manufacturer.

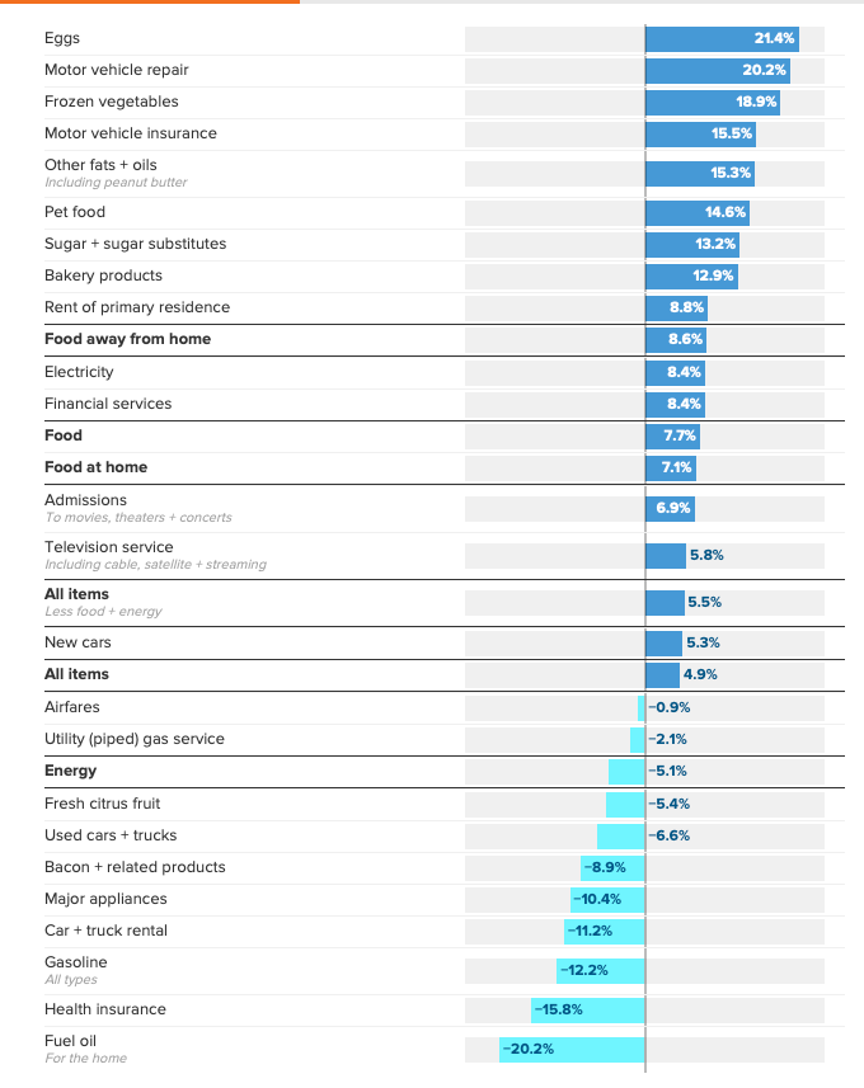

CPI Hits 4.9% YOY, after the 0.40% report for April. It’s still headed in the right direction as far as the Fed is concerned and puts a September cut on the table. Eggs were the leader, up 21.4%, while fuel oil is the laggard, down 20.2%. My own 4% inflation rate forecast by yearend is starting to look conservative. Perish the thought!

The Oil Collapse is Signaling a Recession, as is weakness in all other commodities, even lithium. Texas tea has plunged 22% I three weeks to a new two year low at $62. It’s one of the worst performing asset classes of 2023. Widespread EV adoption is finally making a big dent, as are the price wars there. OPEC Plus production cuts were unable to stem the decline. Buy (USO) on dips as an economic recovery play.

Is a Bank Short Selling Ban Coming? The Feds could bar hedge funds from launching raids on small regional bank shares with the aim of taking them to zero. Such a ban was enforced for all banks in 2008.

Elon Musk Appoints New Twitter CEO, removing a major management distraction. Linda Yaccarino is the new CEO of Twitter, poached from her from online advertising at NBC. This is a positive for Tesla, as it frees up the heavy burden of turning around Twitter from Musk, allowing him to devote more time to Tesla. It also reduced the risk that Musk will sell more Tesla shares to finance said turnaround. Guess who just got the worst job in the world? Buy (TSLA) on dips.

Weekly Jobless Claims jump to 264,000, a new 18 month high, providing another recession indicator.

US Budget Deficit Shrinks to $1.5 Trillion, down from a $3 trillion peak during the previous administration. Government Bond selling will drop by a similar amount. That’s still up $130 billion from 2022. Increased tax revenues from a recovering economy is the reason. Buy (TLT) on every dip.

Google Ramps Up AI Effort, launching a new suite of AI tools at its annual developer conference. With a 93% market share in online search (GOOGL) has a lot to defend. The stock popped 4% on the news.

FANGS to Rise 50% by Yearend, says Fundstrat’s ultra-bull Tom Lee. I think he’s right, once the debt ceiling debacle gets out of the way. The contribution of AI is being vastly underestimated.

Berkshire Hathaway (BRK/B) Earnings Soar, with operating earnings up 12.6% in Q1, but Warren Buffet expects business to slow. Many companies now have to unwind big pandemic inventories with aggressive sales, crimping inflation. That’s why Berkshire owns $130 billion in cash and Treasury bills.

My Ten Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, May 15 at 7:30 AM EST the NY Emore State Manufacturing Index is out.

On Tuesday, May 16 at 6:00 AM, Retail Sales are announced. On Wednesday, May 17 at 11:00 AM the US Building Permits are printed. On Thursday, May 18 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer.

On Friday, May 19 at 2:00 PM the University of Baker Hughes Rig Count is released.

As for me, Egypt and I have a long history together. However, when I first visited there in 1974, they tried to kill me.

I was accompanying US Secretary of State Henry Kissinger on Air Force One as part of his “shuttle diplomacy” between Tel Aviv and Cairo. Every Arab terrorist organization had vowed to shoot our plane down.

When we hit the runway in Cairo, I looked out the window and saw a dozen armored personnel carriers chasing us just down the runway. All on board suddenly got that queasy, gut-churning feeling, except for Henry.

When the plane stopped, they surrounded us, then turned around, pointing their guns outward. They were there to protect us.

The sighs of relief were audible. In a lifetime of heart-rending landings, this was certainly one of the most interesting ones. Those State Department people are such wimps! Henry was nonplussed, as usual.

As a result of the talks Israel eventually handed back Sinai in return for an American guarantee of peace which has held to this day. Egyptian president Anwar Sadat was assassinated by his own bodyguard for his efforts shortly afterwards.

Israel was so opposed to the talks that when I traveled to Tel Aviv, El Al Airline security made sure my luggage got lost. So the Israeli airline gave me $25 to buy replacement clothes until my suitcase was delivered. On that budget, all I could afford were the surplus Israeli army fatigues at the Jerusalem flea market.

A week later, my clothes still had not caught up with me when I boarded the plane with Henry. That meant walking the streets of Cairo in my Israeli army uniform. It would be an understatement to say that I attracted a lot of attention.

I was besieged with offers to buy my clothes. Egypt had lost four wars against Israel in the previous 30 years, and war souvenirs were definitely in short supply.

By the time I left the country, I was stripped bare of all Israeli artifacts, down to my towels from the Tel Aviv Hilton, and boarded the British Airways flight to London wearing a cheap pair of Russian blue jeans I had taken in trade.

Levi Strauss never had a thing to worry about.

The bewitching North African country today is still a prisoner of a medieval religion that has left its people stranded in the Middle Ages. While its GDP has doubled in the last 70 years, so has its population, to 110 million, meaning there has been no improvement per capital income at all in a half century. That is a staggering number for a country that is mostly desert.

In 2019, I took my two teenaged daughters to Egypt to visit the pyramids and ride camels as part of an impromptu trip around the world. My logic then was that at the current rate of climate change, this trip might not be possible in five years.

As it turns out, it was not possible in six months when the pandemic started.

We were immediately picked up by Egyptian Intelligence right at the gate who remembered exactly who I was. It seems they never throw anything out in Egypt.

After a brief interrogation where I disclosed my innocent intentions, they released us. No, I wasn’t working for The Economist anymore. Yes, I was just a retired old man with his children. They even gave us a free ride to the Nile Hilton where I spent my first honeymoon in 1977.

Some people will believe anything! And I never did get that suitcase back.Good luck and good trading!

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

2019 Over Sinai

https://www.madhedgefundtrader.com/wp-content/uploads/2023/05/plane-window.jpg331441Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-15 09:02:502023-05-15 16:49:18The Market Outlook for the Week Ahead, or I’m Going on Strike!

Below please find subscribers’ Q&A for the May 10 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: Why is the market down on such great inflation data?

A: Yes, a 4.9% annualized inflation rate is a big improvement from 9.1% nine months ago. The market only cares about the debt ceiling debacle right now. I’ve been teaching people about the stock market for about 55 years, and I can tell you that all investors have one great fear, and it's not the fear of losing money—that they can handle. It’s the fear of looking stupid. And if they load the boat with stock now, and the US government defaults and the market drops 25%, they will look really stupid. This is not a black swan. It has probably been the most advertised market negative in history. We’ve known about the debt default since December when the Democrats chose not to raise the debt ceiling because they thought they could gain a political advantage by letting the Republicans fumble the issue, and they are reaping such advantages by the bucketload. So, even though everyone knows that this will be settled, it has settled 98 consecutive times in the last 106 years, and they don’t want to do anything before a deal. And by the way, this was only put into place during WWI to meter the rate of government borrowing during the war, so I would say it’s lost its purpose. However, it's hard to make any changes at all in the government these days. What that does do, is create big gaps up in the market when they are resolved, and big gaps down when they are not resolved. That’s why we’re doing nothing.

Q: Do you like regional banks here—are they a buy? And do you like the Schwab LEAPS?

A: Yes on the Charles Schwab LEAPS (SCHW), because you have two years for that to work out. With regional banks as a stock buy here, you’re really buying a lottery ticket because if they do get attacked by short sellers, you get wiped out practically overnight (as has happened 4 times.) On the other hand, if the US Treasury or the FCC makes selling bank shares or lending bank shares illegal, then you’ll have the regional banks just roar, because the sellers will be gone. There are too many better things to do than to make a high-risk trade on bank shares, especially after the debt ceiling is resolved.

Q: Is Apple (APPL) trade a long?

A: Yes, on any pullback. I think big tech leads for the next 10 years once we get out of our current quagmire. So it’s a question of how much pain you’re willing to take in the meantime. My target for Apple this year is $200.

Q: iShares 20 Plus Year Treasury Bond ETF (TLT) is up today; would it be worth selling out of the money call spreads with the same expiration date as our long position?

A: No, it is not. At $104, it’s not a great short, or otherwise, I’d do it myself. When we get up to $109, then you want to go short like with the $114 puts or $115 puts. But down here if you’re shorting say, the $109s, and we go to $109 the next day or week, then you get stopped out. Remember any shorts of bonds here is now a long-term counter-trend trade—you’re betting that your position expires in the money before a long-term trend to the upside reasserts itself. So no, that’s why I’m not doing any shorts right here. Also, we’re not low enough to buy it yet. You get down to $101 or $102, I’ll look at buying call spreads, but here in the middle is never a good place to trade.

Q: Are you still expecting a correction in May?

A: May isn’t over yet. When they say “Sell in May and go away,” they don’t tell you if it’s May 1st or May 30th, so I’m happy where I am. There’s no law that says you have to get every trade of the year. I think doing nothing is the best solution right now, especially with a 62% profit already in the bank this year.

Q: Is it too late for bank LEAPS?

A: I would say, on a two-year view, no. I’m looking for these shares to double in two years, so a bet that it’s unchanged or higher right now is a pretty good bet, I would say—especially if it gives you a 100% return in one or two years. So yes, all the big bank LEAPS are still good, and with small banks, too much is unknown right now for a highly leveraged bet in that sector.

Q: What do you mean when you say one-year LEAPS is a call spread?

A: When I say one year LEAP, I mean at the money, and then short the next strike higher, and that gives you the maximum leverage. Something like 20:1 leverage when you go that aggressive. But now is the time to be aggressive; that's when these LEAPS are all on sale.

Q: Near-term iShares 20 Plus Year Treasury Bond ETF (TLT) move?

A: Sorry to say, sideways. That's why I'm doing nothing. I’m waiting for the market to tell me what to do. If it goes down, I want to buy it, if it goes up, I want to sell it, if it goes sideways, I want to go on vacation—very simple trading strategy.

Q: What about commercial real estate?

A: I don’t want to touch it, and the Real Estate Investment Trusts (REITs) on those have been horrible. Maybe later in the year when the REITs are at bankruptcy levels, it might be worth a buy. But you have to be careful on your REITs; there are good REITs and there are bad REITs, and you don’t want to be anywhere near the commercial ones. With things like cell phone towers, assisted care living facilities—you know, dedicated LEAPS in safe areas would be a good place. And the yields, by the way, are very high, if they pay.

Q: If the US defaults, what would you buy?

A: Everything, because everything will be at a low for the year; so that’s an easy one. By the way, when we got the banking crisis in March, I adopted an everything strategy then: buy all big banks and brokers—and it turned out to be the best trade of the year. The same is going to happen with the debt default.

Q: How long will it take for the regional bank construction to play out?

A: I think the regional banks have completely separated themselves out from the big banks. You only want to own the big banks because you get big returns on those, and the risk/reward ratio is overwhelmingly in favor of big banks, unlike with small banks. Therefore, you only buy the big banks in that situation. If you feel like buying a lottery ticket on your local bank because it’s down 80%, go ahead and do so, but remember that's what it is—a lottery ticket, with a big payoff if you win.

Q: Bitcoin has recently been weak off its top. Do you expect another leg up in Bitcoin prices?

A: I do not. Bitcoin was the perfect asset to have when we had a huge oversupply of cash and a shortage of assets. Now, is the opposite: we have an oversupply of assets and a shortage of cash, and that may remain true for another 10 years or so. So, if you have Bitcoin, I’d be unloading any positions you have now and falling down on your knees, thanking goodness you were able to recover this much of your loss. The other problem is you now have a lot of the intermediaries going bankrupt or shut down by the SEC or the US Treasury. So, that is an additional risk, which you don’t have buying JP Morgan (JPM), for example, or the Australian dollar (FXA), or oil (USO), or copper (FCX). It’s just so far out there on the risk/reward basis. Only large institutions and miners are in the market now—most individuals have been scared away for life.

Q: Would you buy PayPal (PYPL) on the dip? The earnings were terrible.

A: Yes, I would. It is now discounting a recession. If you don't get a recession, you get a big recovery in PayPal.

Q: Do you think that a Ukraine-Russia war will end soon?

A: I would doubt that the Russia-Ukraine war lasts more than a year, and when it ends, it will create the biggest global economic stimulus since the Marshall Plan. Also, American companies will be at the front of the line on the reconstruction deals because we supplied a lot of the weapons and intelligence. Looking at the Marshall Plan in modern terms: $17 billion in 1947 money would be on the order of a $1 trillion today—you basically have to rebuild an entire country. And guess who’s good at building countries? We are. We have all the big engineering companies to do it. Buy Caterpillar (CAT) for sure. By the way, I’ll be spending my summer vacation working on the Ukraine War for the US Marine Corps and NATO. At least the Belgians have better food.

Q: What do you think about pharmaceuticals like Eli Lilly (LLY)?

A: We’ve been recommending them in the Mad Hedge Biotech & Health Care letter for literally years. They’re absolutely kicking butt with their weight loss drug Mounjaro—to the extent that there are shortages of supplies, a black market, and big price increases coming, so it’s all about the weight loss boom. I hate to think of what the combined overweightness of America is, but it’s got to be somewhere in the millions of tons (and I am one of the guilty parties myself.)

Q: There's talk that EVs put out a lot of sulfur that increases climate change issues. What do you think?

A: Absolutely not true, as there is no sulfur in an EV. I don't know where they would come out of an electric engine running on a lithium battery. It’s just another bit of fake news coming out of the oil industry, which is pretty much around us all day, every day. You just have to get used to that. Conventional international combustion engines do emit a lot of sulfur in the form of sulfur dioxide and the big three have been sued over this for at least 50 years.

Q: When will the debt ceiling negotiations end?

A: There are two indicators you look for in predicting the end of a debt ceiling crisis (the last one of which was 12 years ago): #1. When the government announces it can’t send out social security checks anymore because they have no more money, and #2. A big drop in the stock market that scares all the billionaires, cuts their wealth, and makes them threaten to withdraw funding from the politicians who are blocking this thing. Another big indicator is when the Department of Defense announces they have no more money to pay military salaries. Almost all military presence in the United States is in red states and is a major support for economies. And the reason is that's where land was cheapest during WWI, which was when we did a very rapid buildup in the number of military bases. So, watch for those indicators and look for a massive rally when this happens. The US government is basically a giant recycling machine. It takes money off the coast, where all the wealth and taxes are paid, and spends it inland, where all the infrastructure and military have to be paid for. The only military spending on the coasts is in Hawaii, cyber warfare in California, and shipbuilding on the east coast. Anything that interferes with the process of moving money off the coasts and inland is doomed to fail for sure. That’s my one-minute analysis on the cash flows inside the US economy.

Q: I read that the clarity of Lake Tahoe is the best ever. Is this true?

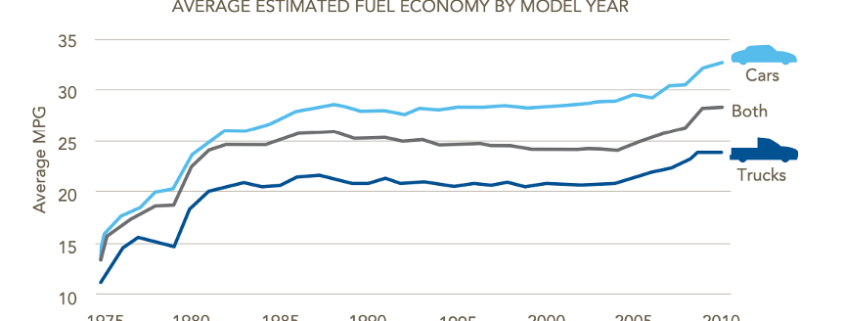

A: Yes, it is. It is an example of a major effort to save the environment that succeeded, but you had to live 70 years to see it. The biggest factor was improving gas mileage for cars. The average fuel economy for new model cars has increased from 12 miles per gallon in 1950 to 35 today. Notice that cars have gotten a lot smaller too. That cuts by two-thirds the carbon dioxide going into the atmosphere which can combine with nitrogen to make nitric acid which fell into the lake. Several big development projects were stopped in their tracks. So was a planned freeway around the lake. Some 17 golf courses are now banned from using fertilizer. Sewage is now piped out of the valley instead of into the lake. A record 70 inches of rainfall this year helped dilute the water. Finally, an ill-conceived freshwater shrimp farming industry ended when the shrimp all starved to death when the lake became too clear, eliminating their poop from the picture. There is now a campaign to clean garbage off the bottom which I help fund. We even found “Fredo’s” body from The Godfather! As a result, the lake clarity has improved from 50 feet in 1970 to 115 feet, the same as when Mark Twain first visited Lake Tahoe in 1861.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Want to Know What Happens Next?

https://www.madhedgefundtrader.com/wp-content/uploads/2023/05/estimate.png434864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-12 09:02:442023-05-12 12:10:04May 10 Biweekly Strategy Webinar Q&A

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOLDEN AGE OF BIG BANKING HAS JUST BEGUN) (JPM), (FRC), (BAC), (C), (WFC), (AAPL), (GOOGL), (META), (AMZN), (TSLA), (NVDA), (CRM), ($VIX), (USO), (TLT), (QQQ)

The United States is about to change beyond all recognition.

Most investors have missed the true meaning of the JP Morgan takeover of First Republic Bank for sofa change, some $10.6 billion. It in fact heralds the golden age of big banking. The US is about to move from 4,000 banks to four, with all of the profits accruing at the top.

Look at the details of the (JPM)/(FRC) deal and you will become utterly convinced.

(JPM) bought a $90 billion loan portfolio for 87 cents on the dollar, despite the fact that the actual default rate was under 1%. The FDIC agreed to split losses for five years on residential losses and seven years on commercial ones. The deal is accretive to (JPM) book value and earnings. (JPM) gets an entire wealth management business, lock, stock, and barrel. Indeed, CEO Jamie Diamond was almost embarrassed by what a great deal he got.

It was the deal of the century, a true gift for the ages. If this is the model going forward, you want to load the boat with every big bank share out there.

And the amazing thing was that (JPM) made the highest bid among a half dozen contenders.

Along with Health Care, banking is the last unconsolidated US industry. We have five railroads, four airlines, three trucking companies, three telephone companies, two cell phone providers….and 4,000 banks?

Other countries get by with much less. England has five major banks, Australia four, and Germany two, one of which goes bankrupt every decade (I’m not naming names). America’s financial system is an anachronism of its federal system where each of the 50 states is treated like a mini country.

The net net of this will be a massive capital drain from the entire country to New York where the big banks are concentrated. Local economies in the Midwest and the South will collapse for lack of funding. The West Coast will be OK with behemoth technology companies spinning off gigantic cash flows.

The other big story here is the dramatic change in the administration’s antitrust policy. Until now, it has opposed every large merger as an undue concentration of economic power. Then suddenly, the second largest bank merger in history took place on a weekend, and there will be more to come.

All it takes is a Twitter run by depositors. Every weekend has become a waiting game for the foreseeable future.

Needless to say, this makes all the big banks a screaming buy. Hoover up every one of the coming dip, including (JPM), (BAC), (C), and (WFC).

Big is beautiful.

To prove I am not perfect, my position in First Republic Bank (FRC) still sits on my broker statement a week after it filed for bankruptcy, dead, moribund, and worthless as if it is some form of punishment. It’s a very small position but it stings nonetheless.

It’s like they want to punish me for leading them astray. They have been copying my trades for ages without paying for them and I hope they took a big one in (FRC).

So far in May, I have managed a modest +0.55% profit. My 2023 year-to-date performance is now at an eye-popping +62.30%. The S&P 500 (SPY) is up only a miniscule +8.40% so far in 2023. My trailing one-year return reached a 15-year high at +120.45% versus -3.67% for the S&P 500.

That brings my 15-year total return to +659.49%. My average annualized return has blasted up to +48.86%, another new high, some 2.79 times the S&P 500 over the same period.

Some 40 of my 43 trades this year have been profitable. My last 20 consecutive trade alerts have been profitable.

I initiated no new trades last week, content to run off existing profitable ones. With the Volatility Index at a two-year low at 15.78%, opportunities are few and far between. Those include both longs and shorts in Tesla (TSLA), a long in the bond market (TLT), and a short in the (QQQ).

That leaves me with only one remaining position, a short-dated long in the bond market. I now have a very rare 90% cash position due to the lack of high-return, low-risk trades.

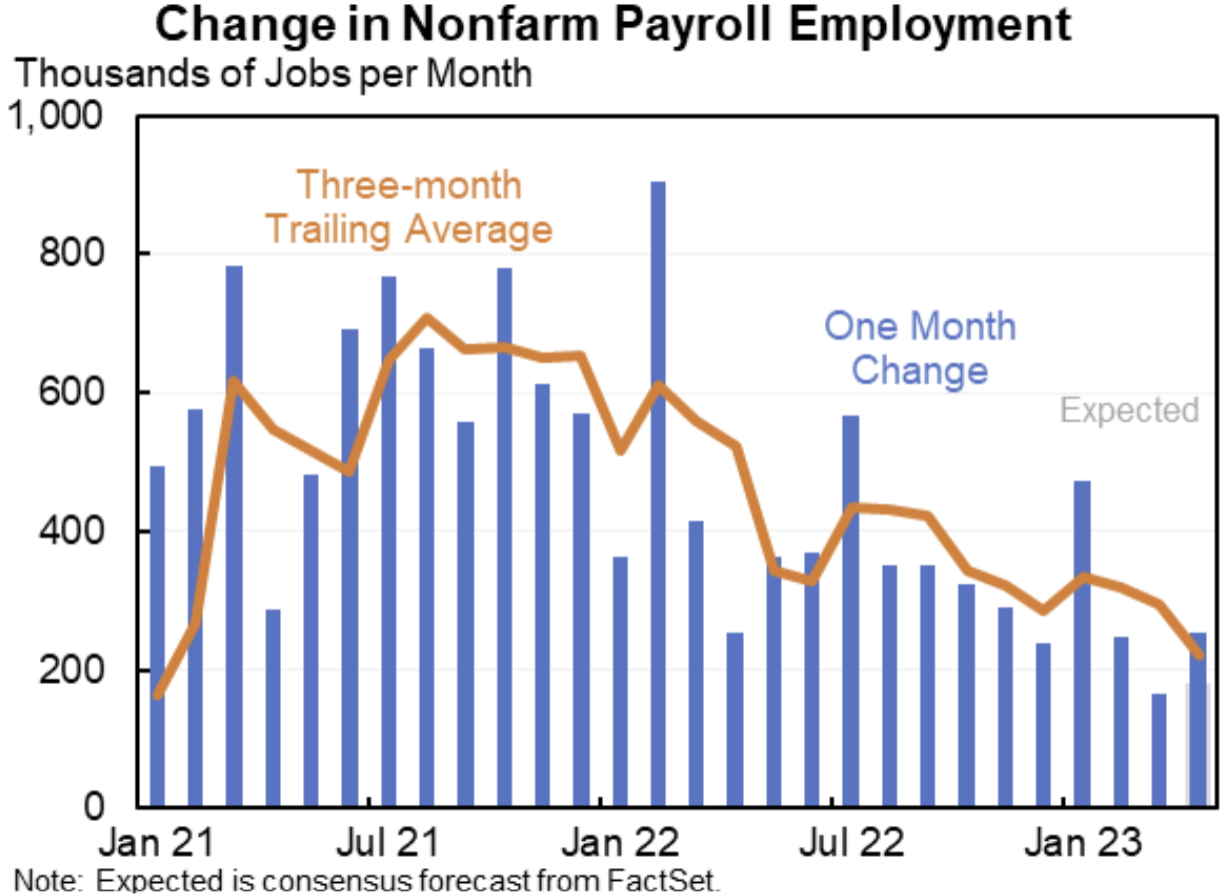

The Fed Raises Rates 0.25%, likely the last such move in this cycle. Futures markets are now discounting a 25-basis point CUT by September, the beginning of a new decade-long falling rate cycle. The problem is that AI is creating more jobs than it is destroying, keeping the Fed fixated on the wrong data.

Nonfarm Payroll Jumps by 253,000, another hot number. The headline Unemployment Rate dropped to a half-century low of 3.4%. These figures suggest for rate hikes to come.

The JP Morgan Buys First Republic Bank from the FDIC, for $10.6 billion, thus wiping out the shareholders. It’s a huge win for (JPM), which picked up 87 branches and $90 billion in loans in the wealthiest part of the country, taking the share up $5. What you lost on (FRC) you made pack on (JPM) LEAPS. Live and learn. On to the next trade! The FDIC got out for nearly free, a big win for the government.

Government DefaultDate Moved Up to June 1, by US Treasury Secretary Janet Yellen, smacking the bond market for three points. The House remains an albatross around the bond market’s debt.

Europe Ekes Out 0.1% Growth in Q1, versus a 1.1% rate for the US. This is despite the drag of the Ukraine War, energy shortages, high inflation, and Brexit. What’s the difference between the US and Europe? We allow immigrants who become customers, while the continent doesn’t.

You Only Need to Buy Seven Stocks This Year, as the rest are going nowhere. That include (AAPL), (GOOGL), (META), (AMZN), (TSLA), (NVDA), (CRM). Watch out when the next rotation broadens out to the rest of the market.

Is Volatility Bottoming Now? The Fed announcement of a 25 basis point hike on Wednesday could end the move up in stocks. After that, shares will only have an imminent debt default and US government downgrade to focus on. ($VIX) seven-week fade will end that revisit the old highs in the high $20’s. Great shorting opportunities are setting up.

Oil (USO) Crashes 5% on US debt default fears in the biggest drop since January. This is the worst asset class to own going into a recession. EV competition is also starting to take a bite. No gas needed here. $66 a barrel here we come.

More Tesla Price Cuts to Come, with swelling inventories forcing Musk’s hand. The only consolation is that Detroit will suffer more. Musk is cutting profits while the big three are accelerating losses. Tesla has excess inventory for the first time in its 20-year history.

Apple (AAPL) Earnings Beat, led by stronger than expected Q1 iPhone sales at $53.1 billion. EPS came in at $1.53 versus $1.42 expected, revenues at $94.84 billion versus $92.96. Mac and iPad sales are down YOY. Services rose 5.3%. Apple bought back a stunning $90 billion of its own shares and paid dividends. The shares popped $3. The long-term growth play here is low prices phone in India where second hand phone sales have been burgeoning. That's why Apple is now offering to buy your old phone. Next stop: New Delhi.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper-accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, May 8 at 7:30 AM EST, the Consumer Inflation Expectations are out.

On Tuesday, May 9 at 6:00 AM, the NFIB Business Optimism Index is announced. On Wednesday, May 10 at 11:00 AM, the US Inflation rate is printed. On Thursday, May 11 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index.

On Friday, May 12 at 8:30, the University of Michigan Consumer Sentiment Index for April is released.

As for me, I have been going down memory lane looking at my old travel photos looking for new story ideas and I hit the jackpot.

Most people collect postcards from their foreign travels. I collect lifetime bans from whole countries.

During the 1970s, The Economist magazine of London sent me to investigate the remote country of Nauru, one half degree south of the equator in the middle of the Pacific Ocean.

At the time, they had the world’s highest per capita income due to the fact that the island was entirely composed of valuable bird guano essential for agriculture. Before the Haber-Bosch Process to convert nitrogen into ammonia was discovered, guano was the world’s sole source of high grade fertilizer.

So I packed my camera, extra sunglasses, and a couple of pairs of shorts and headed for the most obscure part of the world. That involved catching Japan Airlines from Tokyo to Hawaii, Air Micronesia to Majuro in the Marshall Islands, and Air Nauru to the island nation in question.

There was a problem in Nauru. Calculating the market value of the bird crap leaving the island, I realized it in no way matched the national budget. It should have since the government owned the guano mines.

Whenever numbers don’t match up, I get interested.

I managed to wrangle an interview with the president of the country in the capital city of Demigomodu. It turns out that was no big deal as visitors were so rare in the least visited country in the world that he met with everyone!

When the president ducked out to take a call, I managed to steal a top-secret copy of the national budget. I took it back to my hotel and read it with great interest.

I discovered that the president’s wife had been commandeering Boeing 727s from Air Nauru to go on lavish shopping expeditions to Sydney, Australia where she was blowing $200,000 a day on jewelry, designer clothes, and purses, all at government expense. Just when I finished reading, there was a heavy knock on the door. The police had come to arrest me.

It didn’t take long for missing budget to be found. I was put on trial, sentenced to death for espionage, and locked up to await my fate. The trial took 20 minutes.

Then one morning I was awoken by the rattling of keys. My editor at The Economist, the late Peter Martin, had made a call and threatened the intervention of the British government. Visions of Her Majesty’s Navy loomed on the horizon.

I was put in handcuffs and placed on the next plane out of the country, a non-stop for Brisbane Australia. When I was seated next to an Australian passenger, he asked “Jees, what did you do mate, kill someone?” On arrival, I sent the story to the Australian papers.

I dined out on that story for years.

Alas, things have not gone well for Nauru in the intervening 50 years. The guano is all gone, mined to exhaustion. It is often cited as an environmental disaster. The population has rocketed from 4,000 to 10,000. Per capita incomes have plunged from $60,000 a year to $10,000. The country is now a ward of the Australian government to keep the Chinese from taking it over.

If you want to learn more about Nauru, which many believe to be a fictitious country, please click here.

As for me, I think I’ll pass. I don’t ever plan to visit Nauru again. Once lucky, twice forewarned.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2023/05/oceana-may2023.png6861024Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-08 09:02:522023-05-08 12:00:34The Market Outlook for the Week Ahead, or The Golden Age of Big Banking has Just Begun!

The job numbers have serious consequences for the tech sector - the biggest being there will be no recession in 2023 because everybody has a job.

Not only does everyone have jobs, they are also getting double the wage gains the Fed forecasted at 0.5% annualized to 6% year over year.

The tech sector has gotten rid of many good-paying jobs, many of those jobs were fake jobs that were absorbed to hoard talent when rates were at 0%.

It’s interesting that many of these tech stocks have exploded to the upside upon announcing job cuts, meaning investors don’t view the cuts through the prism of lost revenue but rather increasing productivity and delivering added efficiency.

Now, the entire bond investing complex is waiting on a Fed cut, which is why as of yesterday, 4 quarter percent rate cuts were priced in.

Fast forward 1 day and Fed future pricing is now pricing in 3-quarter percent rate cuts as investors believe we will stay higher for longer.

Higher for longer is bad for tech shares.

This extinguishes any hope of reducing inflation in the medium term.

It could be that we only get 1-2 quarter-point rate cuts in 2023 if the bond market is correct.

The Nasdaq has performed exquisitely in 2023 gaining 15% so far amid a souring backdrop of shrinking margins, increasing interest rates, federal government mismanagement on an epic level, domestic banking contagion from regional banks, and geopolitical strife.

The not so bad – not so good situation in tech stocks has manifested itself in the best tech stock Apple, which reported earnings yesterday.

Apple’s earnings report validated what I am seeing in the data.

The report was nothing special but good enough to believe that tech will narrowly avoid a recession in 2023.

The balance sheet is so ironclad that Apple even initiated a stock buyback of $90 billion.

Not too shabby.

Granted, there are few that can wield a strong balance sheet in the ways CEO Tim Cook can, but that’s not taking anything away from him.

Apple also told us about the 975 million paying subscribers to their services and that’s 150 million more than one year ago.

The takeaway is that Apple has a highly loyal customer base that continues to drive its dollars into the ecosystem.

Customer retention is incredibly high because they deliver products customers want.

Even their flagship product the iPhone and its revenue was up 2% year over year and beat forecast by $2.5 billion coming in at $51.33 billion when overall revenue decreased year over year.

iPhone revenue is just over half of Apple’s revenue.

A recession data point would be one in which to expect negative growth from iPhone revenue, so low single digits are fine.

The bottom line is that the US economy added 253,000 jobs to the overall job market and the unemployment rate is defying gravity.

US consumers keep spending, spending, and spending more.

Tech has turned into a 7 stock market and generous shareholder returns.

I admit that 2% iPhone revenue growth isn’t eye-popping, but that is where we are at this point in a late economic cycle.

Squeeze the juice out of the iPhone before the next big pivot to the next technology.

Similar can be said about the job market, everyone is trying to make their last buck before this whole thing gets a reset with 0% Fed fund interest rates.

Many even wish that 0% rates were already here.

Tech stocks will grind up as investors will bid up tech stocks, because they believe the Fed will cut sooner than initially thought. We’ll go back to that narrative for better or worse.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-05-05 15:02:352023-06-06 23:46:42Higher for Longer

Mad Hedge Technology Letter

April 28, 2023 Fiat Lux

Featured Trade:

(BUY AMAZON ON THE DIP)

(AMZN), (AAPL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-04-28 14:04:162023-04-28 16:30:42April 28, 2023

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.