A company that did $182 billion of annual revenue last year expanding first quarter revenue at a 34% clip year-over-year is something that is hard to contemplate; but that is how big the big have gotten, and at the top of the heap is Alphabet (GOOGL).

Expect similar type of earnings reports from Amazon (AMZN).

The 4 tech firms of Alphabet (GOOGL), Apple (AAPL), Microsoft (MSFT) and Tesla (TSLA) were in perfect strategic position going into the public health crisis, and now we find ourselves almost at the climax of it, they are validating their current position in 2021 as companies that flourished through the pandemic and now find themselves with only green pastures in front of them.

Google has said it operates in a “competitive market place” but I do not know anyone who uses an internet search service that isn’t named Google.

It’s like trying to live in China without using Wechat, Alibaba, and Baidu.

We are talking about services that perform like utilities.

Just analyze consumers’ behavior during the onslaught of the public health crisis.

Their first reaction was to delegate these important moments to Google Search.

Billions of searches every day for “COVID” and related health information took place.

At the same time, people started to job search on Google as million lost their jobs and these unemployed first reaction was to do a google search on unemployment benefits and where they could find a job.

To help them, job seekers can now use Search quickly and easily find roles that do not require a college degree and Google is working together with the top employment websites to make the service even better.

And if you thought the reach of Google stopped there, then what about when not searching for jobs or health solutions on Google search.

Well, first, food delivery searches on Google, then, conveniently, since lockdowns pervaded the world, YouTube’s video streaming had its best year.

Users continue to find all types of informational content, from educational videos to podcasts on YouTube.

In fact, according to a recent study conducted by Ipsos, 77% of respondents say they used YouTube during 2020 to learn a new skill.

YouTube Shorts, Google’s TikTok imitation service, continues to gain popularity with over 6.5 billion daily views as of March, up from 3.5 billion at the end of 2020.

The financial metrics backed up the popularity in YouTube with YouTube advertising revenues of $6 billion, up 49%, driven by exceptional performance in direct response and ongoing strength in brand advertising.

Network advertising revenues of $6.8 billion, up 30%, driven by AdMob and Ad Manager.

What if you don’t have a device to watch YouTube or search on Google Search for jobs and food delivery?

Easy answer, buy a Google device.

Other revenues were $6.5 billion, up 46%, primarily driven by growth in Play and YouTube non-advertising revenues, followed by hardware, which benefited from the addition of Fitbit revenues. Google Services operating income was $19.5 billion, up 69%, and the operating margin was 38%.

Google has you covered.

Then what about the people who have jobs and need a cloud to store their files.

Google’s Cloud segment, including GCP and Google Workspace, revenues were $4 billion for the first quarter, up 46%.

GCP's revenue growth was again meaningfully above Cloud overall. Strong growth in Google Workspace revenues was driven by growth in both seats and average revenue per seat.

Google has that covered as well and fusing their cloud operability with Google’s suite of services like Gmail has been reliable for many work from home workers.

This company has covered all their bases and they were doing this before the public health crisis.

Alphabet currently has $1.55 trillion of market cap, but this is easily a $2 trillion company on its way to $3 trillion with no headwinds in sight.

I wouldn’t even call regulation that big of risk and obviously investors keep piling into this stock because they know that even if Google gets broken up, each individual part will be worth more unpacked as a single service because they are the best of breed already.

Microsoft and Alphabet are the two companies vying for the best and most powerful in the world.

At, $1.97 trillion in market cap, Microsoft is more expensive than Google because even though they both earn over $40 billion in profits per year, Microsoft makes that on 27% less revenue than Alphabet which is why they have a higher premium.

Microsoft is more efficient than Alphabet, but again, if Alphabet is broken up, watch for efficiency metrics to skyrocket as each individual business isn’t hindered by the bureaucracy that has turned into how Google operates.

If Alphabet can inch up the margin story, they will be a $2 trillion company and $3,000 stock by the end of 2021.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-28 16:02:402021-05-03 01:17:59Alphabet is a $3,000 Stock

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE CORRECTION IS OVER)

(PAVE), (NFLX), (AAPL), (AMD), (NVDA), (ROKU), (AAPL), (AMZN), (MSFT), (FB), (GOOGL), (TSLA), (KSU), (CP), (GS), (UNP) (LEN), (KBH), (PHM)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:04:402021-04-26 10:44:52April 26, 2021

This is a classic example of if it looks like a duck and quacks like a duck, it’s definitely not a duck….it’s a giraffe.

In stock market parlance, that means we have just suffered an eight-month correction which is now over. Look at the charts and a correction is nowhere to be found. The largest pullback we have seen in the past year has been a scant 12% dip right before the presidential election.

If that’s all the pain we have to suffer to be rewarded with an 80% gain, I’ll take that all day long.

Instead, what we have seen has been a series of sector-specific rolling corrections that were masked by the indexes that were steadily grinding up.

During this time, the best quality stocks endured pretty dramatic hits, like Netflix (NFLX) (-21%), Apple (AAPL) (-26%), Advanced Micro Devices (AMD) (-25%), NVIDIA (NVDA) (-28%), and Roku (ROKU) (-40%).

Stocks sold off hard after Q1 earnings. They are doing the same now with Q2 earnings. That ends on Tuesday after the close when the 800-pound gorilla of them all announces on Wednesday, April 28.

After that, we could be in for another leg in the bull market that could take us up by 10% by the summer.

Some 85% of all companies are now beating forecasts handily. But half are seeing shares fall after the announcement. That shows how professional the market is getting. So, if you eliminate the earnings announcement, you eliminate the share falls?

This is all in the face of economic growth predictions of lifetime proportions. Analysts are now looking for 43% earnings growth in Q2, 55% in Q3, and 75% in Q4. These are WWII-type numbers.

And the Fed put is still good at the bank. Jerome Powell is promising no rate rises until 2023 on an almost daily basis.

It all sets up a continuing pattern of sideways “time” corrections like we’ve just seen followed by frenetic legs up to new highs. This could go on for years.

It worked last time.

The coming week should be quite a blockbuster. It is only the fifth time in history that the five largest stocks in the S&P 500 accounting for 25% of the market cap all report in the same week. These are Apple (AAPL), Amazon (AMZN), Microsoft (MSFT), Facebook (FB), and Alphabet (GOOGL).

That’s going to leave a mark! Biden’s rumored proposal that high-end earners will see doubled capital gains taxes knocked 500 points of the Dow in seconds. The new tax would apply to Americans earning a net income of $1 million or more. Never mind that congress would have to approve the move first, as Trump found out to his chagrin. It’s a trial balloon that was shot down immediately. Trump had planned to cut capital gains to a 15% rate and run a bigger deficit.

It would only apply to Americans who own stocks and never sell. Guess why? To avoid taxes, dummy!

US Stock Funds take in a record $157 billion in March. That beats the record $144 billion that came in during February. Warning: these massive cash flows are consistent with short-term market tops. Vanguard and iShares index funds took in far and away the most money. The Global X US Infrastructure Fund (PAVE) was one of the most popular directed funds.

The labor shortage is on, with companies engaging in mass hiring and paying signing bonuses for low-end jobs. I was awoken by workers putting up a fence next door on a Saturday morning. They’re working weekends to pay back the debts they ran up last year to keep eating. If you are planning any jobs this year, buy the materials now. The country will be out of everything in three months, with current quarter GDP topping a historic 10%.

SPACS have crashed, with the average SPAC down 23% since the February top, and some like Virgin Galactic Holdings off by 50%. Don’t touch these things with a ten-foot pole, as 80% will go under or shut down with no investments. It reminds me of five online pet food companies at the Dotcom Bubble top. It's all a symptom of too much cash flooding the financial system.

Takeover battle for Kansas City Southern (KSU) ensues, with Canadian Nation making a sweeter $33.7 billion offer than Canadian Pacific’s (CP) $30 billion bid. It just shows how valuable railroads really are in a booming economy that urgently needs to move a lot of stuff. Good thing I’m long (UNP). Is the Reading Railroad still available? How about the B&O or the Short Line?

Yellen sets Zero Emissions Target for 2035. That sets up one of the biggest investment opportunities of the century. The trick is to find companies that have viable technologies that can make a stand-alone profit that haven’t already gone up ten times, like Tesla (TSLA). Most of the new EV IPOs aren’t going to make it. This will be a major focus of Mad Hedge research going forward. I hope I live that long!

Existing Home Sales down 12.3% YOY, down 3.7% in March, to 6.03 million units. Prices are up 17.02% YOY, the highest on record. Sales of homes over $1 million are up 108%. Inventory is still the issue, down to only 1.07 million units, off 28% in a year. Truly stunning numbers.

New Home Sales up a ballistic 20.7% YOY in March on a signed contracts basis. This is in the face of rising home mortgage interest rates. The flight to the suburbs continues. Homebuilder stocks took off like a scalded chimp. Buy (LEN), (KBH), and (PHM) on dips.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 9.48% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

I used the dip early in the week to add two more positions in Goldman Sachs (GS) and Union Pacific (UNP). I suffered a day of buyer’s remorse on Thursday when Biden floated his capital gains plan and tanked the Dow by 500 points. Then everything took off like a rocket to new highs on Friday.

That leaves me 80% invested and 20% in cash. The markets went up too fast to get the last match of money in the market.

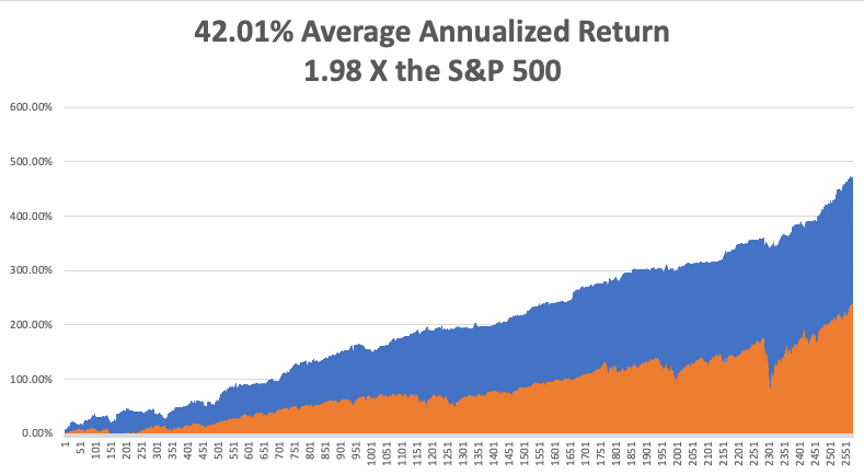

My 2021 year-to-date performance soared to 53.57%. The Dow Average is up 12.3% so far in 2021.

That brings my 11-year total return to 476.12%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.01%, the highest in the industry.

My trailing one-year return exploded to positively eye-popping 132.09%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 31.9million and deaths topping 570,000, which you can find here.

The coming week will be big on the data front, with a couple of historic numbers expected.

On Monday, April 26, at 8:30 AM, US Durable Goods for March are out. Earnings for Tesla (TSLA) and NXP Semiconductors (NXP) are out.

On Tuesday, April 27, at 9:00 AM, we learn the S&P Case Shiller National Home Price Index for February. We also get earnings for Alphabet (GOOGL), Microsoft (MSFT), and Visa (V).

On Wednesday, April 28 at 2:00 PM, The Fed Open Market Committee releases its Interest Rates Decision. The following press conference is more important. Apple (AAPL), Boeing (BA), and QUALCOMM (QCOM) earnings are out.

On Thursday, April 29 at 8:30 AM, the Weekly Jobless Claims are printed. We also obtain the blockbuster US GDP for Q1. Amazon (AMZN), Caterpillar (CAT, and Merck (MRK) release earnings.

On Friday, April 30 at 8:30 AM, we get US Personal Income and Spending for March. Exxon Mobile (XOM) and Chevron (CVX) release earnings. Berkshire Hathaway (BRK/B) announces the next day. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, after telling you last week why I walked so funny, let me tell you the other reason.

In 1987, to celebrate obtaining my British commercial pilot’s license, I decided to fly a tiny single-engine Grumman Tiger from London to Malta and back.

It turned out to be a one-way trip.

Flying over the many French medieval castles was divine. Flying the length of the Italian coast at 500 feet was fabulous, except for the engine failure over the American airbase at Naples.

But I was a US citizen, wore a New York Yankees baseball cap, and seemed an alright guy, so the Air Force fixed me up for free and sent me on my way. Fortunately, I spotted the heavy cable connecting Sicily with the mainland well in advance.

I had trouble finding Malta and was running low on fuel. So I tuned into a local radio station and homed in on that.

It was on the way home that the trouble started.

I stopped by Palermo in Sicily to see where my grandfather came from and to search for the caves where my great-grandmother lived during the waning days of WWII. Little did I know that Palermo was the worst wind shear airport in Europe.

My next leg home took me over 200 miles of the Mediterranean to Sardinia.

I got about 50 feet into the air when a 70-knot gust of wind flipped me on my side perpendicular to the runway and aimed me right at an Alitalia passenger jet with 100 passengers awaiting takeoff. I managed to level the plane right before I hit the ground.

I heard the British pilot say on the air “Well, that was interesting.”

Giant fire engines descended upon me, but I was fine, sitting on my cockpit, admiring the tree that had suddenly sprouted through my port wing.

Then the Carabinieri arrested me for endangering the lives of 100 Italian tourists. Two days later, the Ente Nazionale per l’Avizione Civile held a hearing and found me innocent, as the wind shear could not be foreseen. I think they really liked my hat, as most probably had distant relatives in New York.

As for the plane, the wreckage was sent back to England by insurance syndicate Lloyds of London, where it was disassembled. Inside the starboard wing tank, they found a rag which the American mechanics in Naples had left by accident.

If I had continued my flight, the rag would have settled over my fuel intake vavle, cut off my gas supply, and I would have crashed into the sea and disappeared forever. Ironically, it would have been close to where French author Antoine de St.-Exupery (The Little Prince) crashed in 1945.

In the end, the crash only cost me a disk in my back, which I had removed in London and led to my funny walk.

Sometimes, it is better to be lucky than smart.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Antoine de St.-Exupery on the Old 50 Franc Note

https://www.madhedgefundtrader.com/wp-content/uploads/2021/04/g-bebe-e1647874970894.png295450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-26 10:02:432021-04-26 10:45:23The Market Outlook for the Week Ahead, or The Correction is Over

If you have to ask what this classic phrase from Britain’s colonial past means, you are too young to know.

The stock market equivalent is that there is nothing to do. Just sit back and relax, watching the value of your stocks go up every day. Let the greatest monetary and fiscal stimulus work its inevitable magic.

When I said last week that stocks might go up every day in April, I wasn’t kidding. NASDAQ (QQQ) has gone up every day this month except one. The S&P 500 has seen only two down days when it was virtually unchanged.

And the best may be yet to come.

The mere prospect of a $2.3 infrastructure trillion budget is enough to keep stocks powering upward for the foreseeable future. Biden may have to negotiate the total down to get it through congress and that may be the cause of the next correction…in about three months.

What really had the phones buzzing on Thursday was the bizarre move in the bond market. After seeing spectacularly positive data, the Weekly Jobless Claims plunging by 200,000 and Retail Sales coming in at a prolific 9.8%, bonds should have crashed.

Instead, the (TLT) jumped by $2.60. That took interest rate and inflation fears packing and sent the indexes soaring to all-time highs once again.

It’s proof yet again that inflation is the boogie man that will never show. Despite the incredible strength of the economy, any time anyone tries to raise prices, another company comes along with a better product or service at half the price. Such is the relentless tide of technology.

In the meantime, Goldilocks has moved in, unpacked her bags, gotten comfortable, and has settled in for the duration. I have been so aggressive in trading the market for the last six months it is wearing me out.

So, I took a rare Saturday off, weeding the garden, setting up a new computer, and generally fixing things that I haven’t had time to attend to since last year. I lived almost normally….for a day.

One of the best Earnings Seasons in history started last week, with 25% growth expected at 81% beating forecasts. JP Morgan (JPM) and Bank of America (BAC) kicks off on Wednesday, with the big kahuna, Apple (AAPL) reporting on April 28. Expect stocks to rally until then. It may give us the first hint of the massive stimulus on the economy to come. Q2 and Q3 will be the monster quarters.

Equity Funds pick up a half trillion dollars in five months, more than they attracted over the last 12 years. It’s all rocket fuel for the ongoing market melt-up. With the Volatility Index (VIX) at a one-year low at $17, the best may be yet to come. Equity investors are the most bullish in years.

Tesla is upgraded to $1,071 per share by research firm Canaccord Genuity. The company is transitioning from low-volume high-priced cars to high-volume low-priced cars, as seen in the 47% leaps in sales during Q1. The stationary battery business is booming, thanks to a new generation of technology. Tesla is developing an Apple-type brand value in the energy market, which is worth a big premium, which competitors can’t match. Tesla has brought a machine gun to a knife fight. Global chip shortages are a risk. The stock jumped $25 on the news.

Consumer Price Index comes in muted at 0.6% in April and 2.6% YOY. The market had been fearing worse, sparking another leg up in technology stocks. Much of the gain was from a jump in gasoline prices, which are now falling. Food prices are also rising.

JP Morgan pops on upside earnings surprise, with Q1 profits soaring from $2.9 billion a year ago to an eye-popping $14.5 billion. Revenues were up 14% to $33.1 billion. Loan demand is weakening because so many people are getting government money for free. Credit card debts are being paid down.

Retail Sales explode in March, up a staggering 9.8%. New spending at bars and restaurants was a major factor, and we haven’t even started yet! Stocks soar to new highs, and the bond market takes off like a scalded chimp, taking ten-year US Treasury yields below 1.57%. It confirms my thesis that when we see actual real numbers of an unprecedented recovery, we get another new leg in the bull market.

Weekly Jobless Claims collapse to 576,000, the lowest of 2021. That's down a massive 193,000 jobs from the previous week. Herd immunity is here! Keep getting those shots!

China’s (FXI) GDP grew by a staggering record of 18.3% in Q1 at an annualized rate YOY. Strong industrial production and exports were the leaders. It presages a similar explosive growth rate for the US in Q2. We won’t know until the end of July. Having your largest customers breaking growth records is great for your business too. Buy everything on dips.

Hedge funds nailed the Bond Crash, selling short some $100 billion in paper since January. It will be more than enough to cover their losses in equity shorts. When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 7.17% gain during the first half of April on the heels of a spectacular 20.60% profit in March.

It was a very busy week for trade alerts, with five positions expiring at their maximum profit points in (TSLA) and the (TLT). It’s been so long since I’ve had a loss, I forgot what they looked like.

I used a puzzling $2.60 spike in the (TLT) to add to my already substantial short position in bonds (TLT) with a distant May expiration. Ten-year US Treasury yields fell all the way to 1.51%.

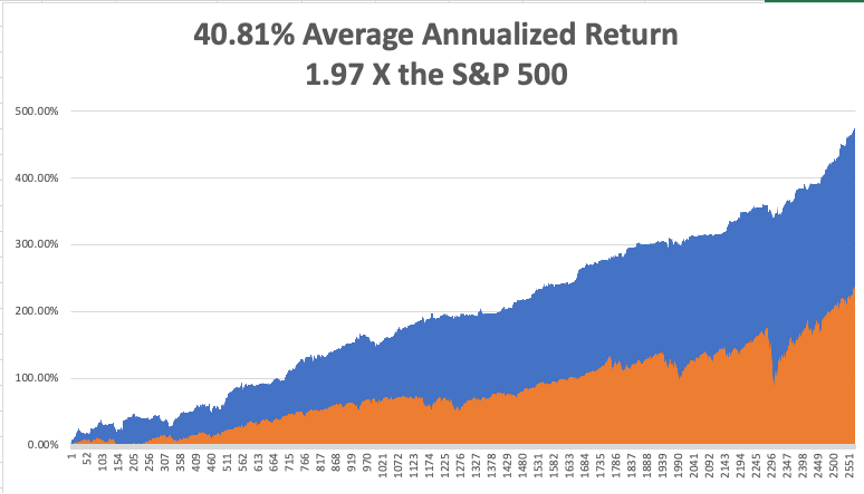

My 2021 year-to-date performance soared to 51.26%. The Dow Average is up 12.9% so far in 2021.

That brings my 11-year total return to 473.81%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 40.81%, the highest in the industry.

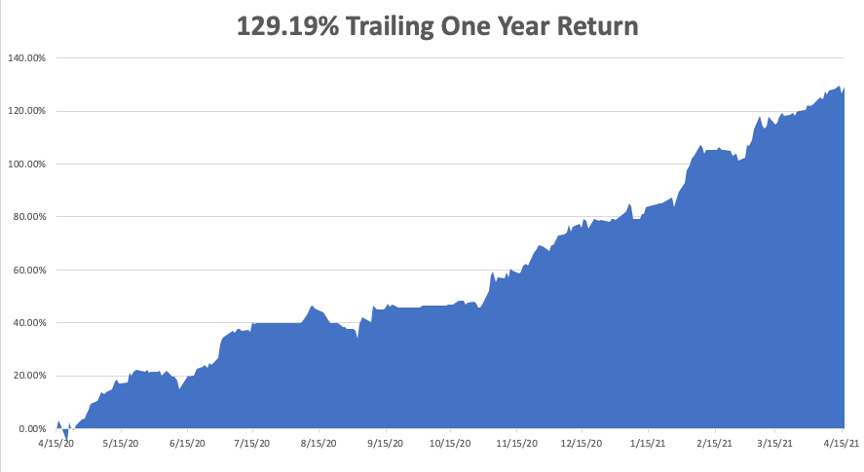

My trailing one-year return exploded to positively eye-popping 129.19%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives. Every time I think these numbers can’t be topped, they increase by another 10% during the following two weeks.

We need to keep an eye on the number of US Corona virus cases at 31.6million and deaths topping 567,000, which you can find here.

The coming week will be dull on the data front.

On Monday, April 19 at 11:00 AM, earnings for (IBM), Coka-Cola (KO), and United Airlines (UAL) are released.

On Tuesday, April 20, at 4:30 PM, API Crude Stocks are published. We also get earnings for Johnson & John (JNJ) and Netflix (NFLX).

On Wednesday, April 21 at 1:00 PM, there is a big 20-year US Treasury bond auction. Chipotle (CMG) and Verizon (VZ) earnings are out. On Thursday, April 22 at 8:30 AM, the Weekly Jobless Claims are printed. At 10:00 AM Existing Home Sales for March are announced. Snap (SNAP) and Intel (INTC) announce earnings.

On Friday, April 23 at 10:00 AM, we get the New Home Sales for March. American Express (AXP) and Honeywell (HON) release earnings. At 2:00 PM, we learn the Baker-Hughes Rig Count.

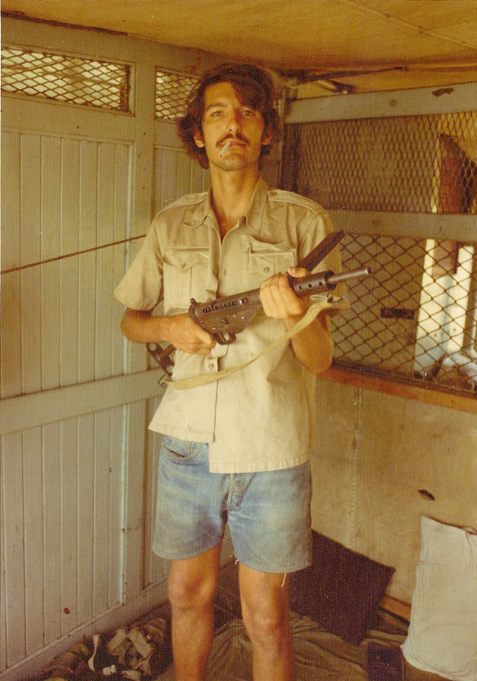

As for me, someone commented that I walk kind of funny the other day, and the memories flooded back.

In 1975, The Economist magazine in London heard rumors that a large part of the population was getting slaughtered in Cambodia. We expected this to happen after the fall of Vietnam, but not in the Land of the Khmers. So my editor, Peter Martin, sent me to check it out.

Hooking up with a right-wing guerrilla group financed by the CIA was the easy part. Humping 100 miles in 100-degree heat wasn’t.

We eventually came to a large village that was completely deserted. Then my guide said, “Over here.” He took me to a nearby cave containing the bodies of over 1,000 women, children, and old men that had been there for months.

I’ll never forget that smell.

With the evidence and plenty of pictures in hand, we started the trek back. Suddenly, there was a large explosion and the man 20 yards in front of me disappeared. He had stepped on a land mine. Then the machine-gun fire opened up. It was an ambush.

I picked up an M-16 to return fire, but it was bent, bloody, and unusable. I picked up a second rifle and fired until it was empty. Then everything suddenly went black.

I woke up days chained to a palm tree, covered in shrapnel wounds, a prisoner of the Khmer Rouge. Maggots infested my wounds, but I remembered from my Tropical Diseases class at UCLA that I should leave them alone because they only ate dead flesh and would prevent gang green. That class saved my life. Good thing I got an “A”.

I was given a bowl of rice a day to eat, which I had to gum because it was full of small pebbles and might break my teeth. Farmers loaded their crops with these so the greater weight could increase their income. I spent my time pulling shrapnel out of my legs with a crude pair of plyers.

Two weeks later, the American who set up the trip for me showed up with cases of claymore mines, rifles, ammunition, and antibiotics. My chains we cut and I began the long walk back to Thailand.

It’s nice to learn your true value.

Back in Bangkok, I saw a doctor who attended to the 50 caliber bullet that grazed my right hip. It was too old to sew up so he decided to clean it instead. “This won’t hurt a bit,” he said as he poured in hydrogen peroxide and scrubbed it with a stiff plastic brush.

It was the greatest pain of my life. Tears rolled down my face.

But you know what? The Economist got their story and the world found out about the Great Cambodian Genocide, where 3 million died. There is a museum in Phnom Penh devoted to it today.

So, if you want to know why I walk funny, be prepared for a long story. I still set off metal detectors.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Doing Research

https://www.madhedgefundtrader.com/wp-content/uploads/2018/10/John-Thomas-rifle.png681477Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-19 09:02:542021-04-19 11:13:14The Market Outlook for the Week Ahead, or Lie Back and Think of England

Below please find subscribers’ Q&A for the April 14 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA.

Q: How do you choose your buy areas?

A: It’s very simple; I read the Diary of a Mad Hedge Fund Trader. Beyond that, there are two main themes in the market right now: domestic recovery and tech; and I try to own both of those 50/50. It's impossible to know which one will be active and which one will be dead, and some of that rotation will happen on a day-by-day basis. As for single names, I tend to pick the ones I have been following the longest.

Q: In my 401k, should I continue placing my money in growth or move to something like emerging markets or value?

A: It depends on your age. The younger you are, the more aggressive you should be and the more tech stocks you should own. Because if you’re young, you still have time to earn the money back if you lose it. If you’re old like me, you basically only want to be in value stocks because if you lose all the money or we have a recession, there's not enough time to go earn the money back; you’re in spending mode. That is classic financial advisor advice.

Q: When you say “Buy on dips”, what percentage do you mean? 5% or 10%

A: It depends on the volatility of the stock. For highly volatile stocks, 10% is a piece of cake. Some of the more boring ones with lower volatility you may have to buy after only a 2% correction; a classic example of that is the banks, like JP Morgan (JPM).

Q: Even though you’re not a fan of cryptocurrency, what do you think of Coinbase?

A: It’ll come out vastly overvalued because of the IPO push. Eventually, it may fall to a lower level. And Coinbase isn’t necessarily a business model dependent on bitcoin; it is a business model based on other people believing in bitcoin, and as long as there’s enough of those creating two-way transactions, they will make money. But all of these things these days are coming out super hyped; and you never want to touch an IPO—wait for it to drop 50%, as I once did with Tesla (TSLA).

Q: Please explain the barbell portfolio.

A: The barbell works when you have half tech, half domestic recovery. That way you always have something going up, because the market tends to rotate back and forth between the two sectors. But over the long term everything goes up, and that is exactly what has been happening.

Q: Is the ProShares Ultra Technology Fund (ROM) an ETF?

A: Yes, it is an ETF issuer with $53 billion worth of funds based in Bethesda, MD. (ROM) is a 2x long technology ETF, and their largest holdings include all the biggest tech stocks like Apple (AAPL), Microsoft (MSFT), Facebook (FB), and so on.

Q: Will all this government spending affect the market?

A: Yes, it will make it go up. All we’re waiting to see now is how fast the government can spend the money.

Q: What is the target for ROM?

A: $150 this year, and a lot more on the bull call spread. The only shortcoming of (ROM) is you can only go out six months on the expiration. Even then, you have a good shot at making a 500% return on the farthest out of the money LEAPS, the November $130-$135 vertical bull call spread. That's because market makers just don’t want to take the risk being short technology two years out. It’s just too difficult to hedge.

Q: There have been many comments about hyperinflation around the corner. Will we be seeing hyperinflation?

A: No, the people who have been predicting hyperinflation have been predicting it for at least 20 years, and instead we got deflation, so don’t pay attention to those people. My view is that technology is accelerating so fast, thanks to the pandemic, that we will see either zero inflation or we will see deflation. That has been the pattern for the last 40 years and I like betting on 40-year trends.

Q: When we get called away on our short options, is it easier to close the trade than to exercise your option?

A: No, any action you take in the market costs money, costs commissions, costs dealing spreads. And it's much easier just to exercise the option if you have to cover your short, which is either free or will cost you $15.

Q: Are you worried about overspending?

A: No, the proof in that is we have a 1.53% ten-year US Treasury yield, and $20 trillion in QE and government spending is already known, it’s already baked in the price. So don’t listen to me, listen to Mr. Market; and it says we haven't come close to reaching the limit yet on borrowing. Look at the markets, they're the ones who have the knowledge.

Q: My Walt Disney (DIS) LEAPs are getting killed. I don't understand why my LEAPS go down even on green days for the stock.

A: The answer is that the Volatility Index (VIX) has been going down as well. Remember, if you’re long volatility through LEAPS, and volatility goes down, you take a hit. That said, we’re getting close to the lows of the year for volatility here, so any further stock gains and your LEAPS should really take off. And remember when you buy LEAPS, you’re doing multiple bets; one is that volatility stays high and goes higher, and one is that your stock is high and goes higher. If both those things don’t happen, and you can lose money.

Q: How do you best short the (TLT)?

A: If you can do the futures market, Treasury bonds are always your best short there because you have 10 to 1 leverage.

Q: How would you do a spread on Crisper Technology (CRSP)?

A: We have a recommendation in the Mad Hedge Biotech & Healthcare service to be long the two-year LEAP on Crisper, the $160-$170 vertical bull call spread.

Q: When do you see the largest dip this year?

A: Probably over the summer, but it likely won’t be over 10%. Too much cash in the market, too much government spending, too much QE. People will be in “buy the dips” mode for years.

Q: Is the SPAC mania running out of steam?

A: Yes, you can only get so many SPACS promising to buy the same theme at a discount. I think eventually, 80% of these SPACS go out of business or return the money to investors uninvested because they are promising to buy things at great bargains in one of the most expensive markets in history, which can’t be done.

Q: What do you think about Joe Biden’s attempt to tame the semiconductor chip shortage?

A: Most people don't know that all chips for military weapons systems are already made in the US by chip factories owned by the military. And the pandemic showed that a just-in-time model is high risk because all of a sudden when the planes stop flying, you couldn't get chips from China anymore. Instead, they had to come by ship which takes six weeks, or never. So a lot of companies are moving production back to the US anyway because it is a good risk control measure. And of course, doing that in the midst of the worst semiconductor shortage in history shows the importance of this. Even Tesla has had to delay their semi truck because of chip shortages. Keep buying NVIDIA (NVDA), Micron Technology (MU), Advanced Micro Devices (AMD), and Applied Materials (AMAT) on dips.

Q: Do you see a sell the news type of event for upcoming earnings?

A: Yes, but not by much. We got that in the first quarter, and stocks sold off a little bit after they announced great earnings, and then raced back up to new highs. You could get a repeat of that, as people are just sitting on monster profits these days and you can’t blame them for wanting to pull out a little bit of money to spend on their summer vacation.

Q: Has the stock market gotten complacent about COVID risk?

A: No, I would say COVID is actually disappearing. Some 100 million Americans have been vaccinated, 5 million more a day getting vaccinated, this thing does actually go away by June. So after that, you only have to worry about the anti-vaxxers infecting the rest of the population before they die.

Q: Do you see any imminent foreign policy disasters in Asia, the Middle East, or Europe that could derail the stock market?

A: I don’t, but then you never see these things coming. They always come out of the blue, they're always black swans, and for the last 40 years, they have been buying opportunities. So pray for a geopolitical disaster of some sort, take the 5-10% selloff and buy because at the end of the day, American stockholders really don't care what’s going on in the rest of the world. They do care, however, about increasing their positions in long-term bull markets. I don't worry about politics at all; I don’t say that lightly because it’s taking 50 years of my own geopolitical experience and throwing it down the toilet because nobody cares.

Q: Would you buy Coinbase?

A: Absolutely not, not even with your money. These things always come out overpriced. If you do want to get in, wait for the 50% selloff first.

Q: Is Canada a play on the dollar?

A: Absolutely yes. If they get a weaker dollar, it increases Canadian pricing power and is good for their economy. Canada is also a great commodities play.

Q: The IRS is using Palantir (PLTR) software to find US citizens avoiding taxes with Bitcoin.

A: Yes, absolutely they are. Anybody who thinks this is tax-free money is delusional. And this is one reason to buy Palantir; they’re involved in all sorts of these government black ops type things and we have a very strong buy recommendation on Palantir and their 2-year LEAPS.

Q: Are NFTs, or Non-Fundable Tokens, another Ponzi scheme?

A: Absolutely, if you want to pay millions of dollars for Paris Hilton’s music collection, go ahead; I'd rather buy more Tesla.

Q: When do you think you can go to Guadalcanal again?

A: Well, I’m kind of thinking next winter. Guadalcanal is one of the only places you can go and get more diseases than you can here in the US. Last year, I went there and picked up a bunch of dog tags from marines who died in the 1942 battle there, sent them back to Washington DC, and had them traced and returned to the families. And I happen to know where there are literally hundreds of more dog tags I can do this with. It’s not an easy place to visit and it’s very far away though. Watch out for malaria. My dad got it there.

Q: Walt Disney is already above the pre-pandemic price. Do you suggest any other hotel company name at this time?

A: Go with the Las Vegas casinos, Wynn (WYNN) and MGM (MGM) would be really good ones. Las Vegas is absolutely exploding right now, and we haven't seen that yet in the earnings yet, so buy Las Vegas for sure.

Q: Is the upcoming Roaring Twenties priced into the stock market already?

A: Absolutely not. You didn't want to sell the last Roaring Twenties in 1921 as it still had another eight years to go. You could easily have eight years on this bull market as well. We have historic amounts of money set up to spend, but none of it has been actually spent yet. That didn’t exist in 1921. I think that when they do start hitting the economy with that money, that we get multiple legs up in stock prices.

To watch a replay of this webinar just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/John-Thomas-Beach-e1416856744606.png400276Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-16 09:02:052021-04-16 16:13:56April 14 Biweekly Strategy Webinar Q&A

(HOW TO EXECUTE A VERTICAL BULL CALL SPREAD)

(AAPL)

(TESTIMONIAL)

(DINING WITH THE BOTTOM 20%)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-25 10:08:222021-03-25 10:19:41March 25, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.