Mad Hedge Technology Letter

January 31, 2020

Fiat Lux

Featured Trade:

(APPLE OUTSHINES THE REST)

(AAPL)

Mad Hedge Technology Letter

January 31, 2020

Fiat Lux

Featured Trade:

(APPLE OUTSHINES THE REST)

(AAPL)

I'll give credit when credit is due.

Apple CEO Tim Cook pulled off a quarter to remember.

And yes, I've been hypercritical of his lack of innovation, but I can't question the way he’s insulated the company from being exposed to softness in mainland China.

Analysts expected $88 billion in revenue and Apple easily surpassed this number by posting $91 billion.

When you look under the surface, there are usually some chinks in the armor.

But this time around Apple's quarter was practically flawless albeit with some frosty guidance.

It's no secret that the quality of a Chinese smartphone has picked up and now rivals some of Apple's best products.

However, Apple turned a weakness into a strength and sales of iPhones was one of the highlights of an outstanding quarter.

In fact, it was the iPhone 11 that carried the load this time.

In total, iPhone Revenue rose 8% to almost $56 billion and they shipped 72.9 million units.

The outperformance doesn't just end there.

Wearables have become a meaningful revenue driver in itself.

Specifically, ear buds and the Apple watch have captivated Apple customers who are scooping up these products in droves.

In the prior quarter, 75% of people who bought the Apple watch were first time buyers.

This added up to wearables clocking in $7.3 billion in revenue this past quarter.

Apple’s outperformance dovetails nicely with my overarching theme of the FANG group plus Microsoft separating themselves from the other tech companies in 2020.

The network effect that these companies possess is unrivaled and the longer they stay in business, the stronger these effects seep in.

If there was a negative part of the quarter, Tim Cook failed to delve into the new Apple streaming product and avoided giving too much detail.

Fortunately, Apple has not bet the ranch on streaming and have stuck to what they know best.

Ultimately, Cook struck a lukewarm tone, especially with the spread of China’s coronavirus threatening to shut down production operations for several manufacturers.

The company has restricted employee travel and shut one store due to the outbreak.

Looking forward, management said “there will definitely be an impact on China in terms of consumption.”

Apple is slated to release its first 5G phone later this year which has been the catalyst for the price appreciation in shares.

Apple continues to be a multiprong revenue machine and any dip should be bought.

This is the type of company that should be part of any multi-asset portfolio.

Global Market Comments

January 9, 2020

Fiat Lux

Featured Trade:

(WEDNESDAY, FEBRUARY 5 MELBOURNE, AUSTRALIA STRATEGY LUNCHEON)

(CAPTURING SOME YIELD WITH CELL PHONE REITS),

(CCI), (AMT), (SBAC),

(JNK), (SPG), (AMLP), (AAPL), (VZ), (T), (TMUS), (S)

I am constantly bombarded with requests for high-yield, low-risk investments in this ultra-low interest rates world.

While high-yield energy Master Limited Partnerships LIKE (AMLP) can offer double-digit returns, they carry immense risks. After all, if the prices of oil drop to $5-$10 a barrel, replaced by alternatives as I eventually expect, all of these instruments will get wiped out.

You can earn 5%-8% from equity-linked junk bonds. However, their fates are tied to the future of the stock market at a 20-year valuation high against flat earnings.

You might then migrate to Real Estate Investment Trusts (REITs) like Simon Property Group (SPG), which acts as a pass-through vehicle for investments in a variety of property investments. However, many of these are tied to shopping malls and the retail industry, the black hole of investment today.

So where is the yield-hungry investor to go?

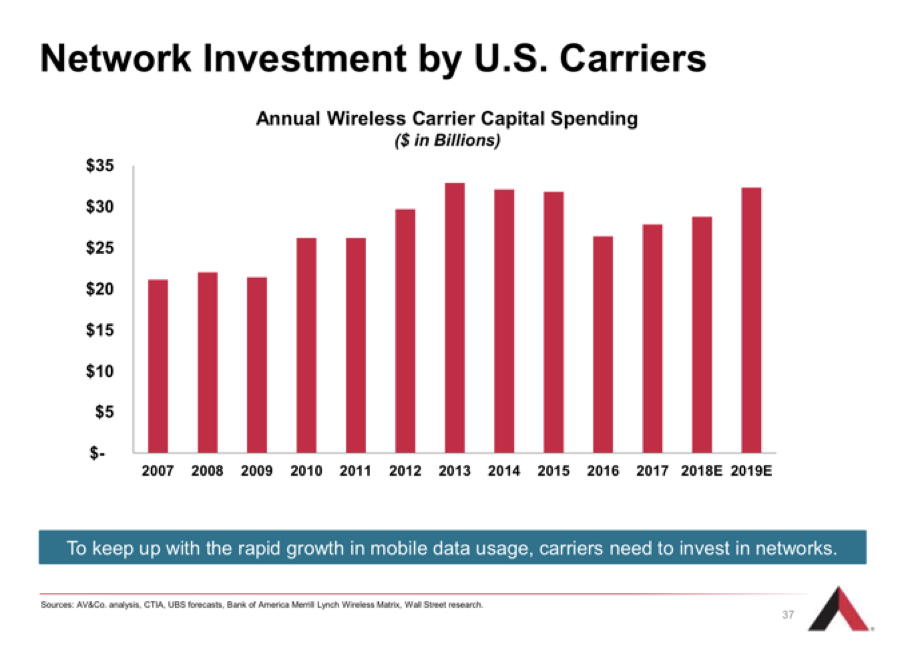

You may have heard about something called 5G. This refers to the rollout of fifth-generation wireless technology that will increase smartphone capabilities tenfold. Whole new technologies, like autonomous driving and artificial intelligence, will get a huge boost from the advent of 5G. Apple (AAPL) will launch its own 5G phone in September.

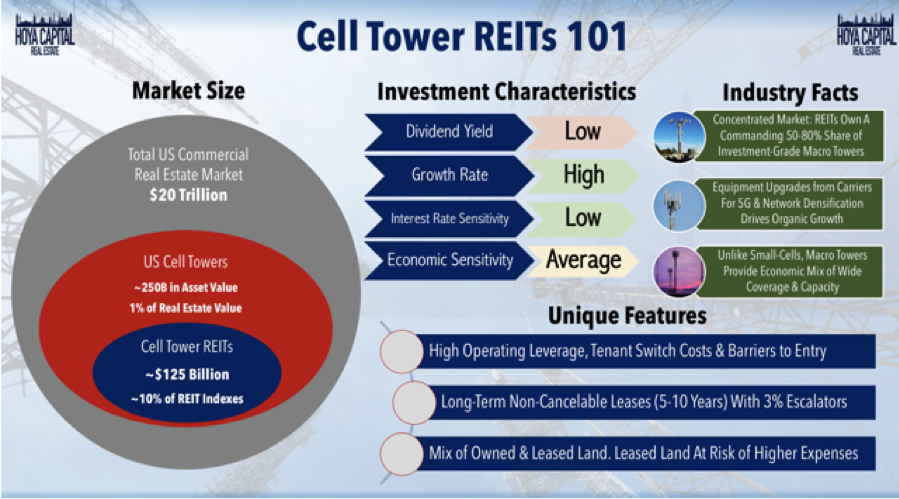

5G, like all cell phone transmissions, rely on 50-200-foot steel towers strategically placed throughout the country, frequently on mountain peaks or the tops of buildings. With demand from the big phone carriers soaring, there is a construction boom underway in cell phone towers. There just so happens to be a class of REITs that specializes in investment in this sector.

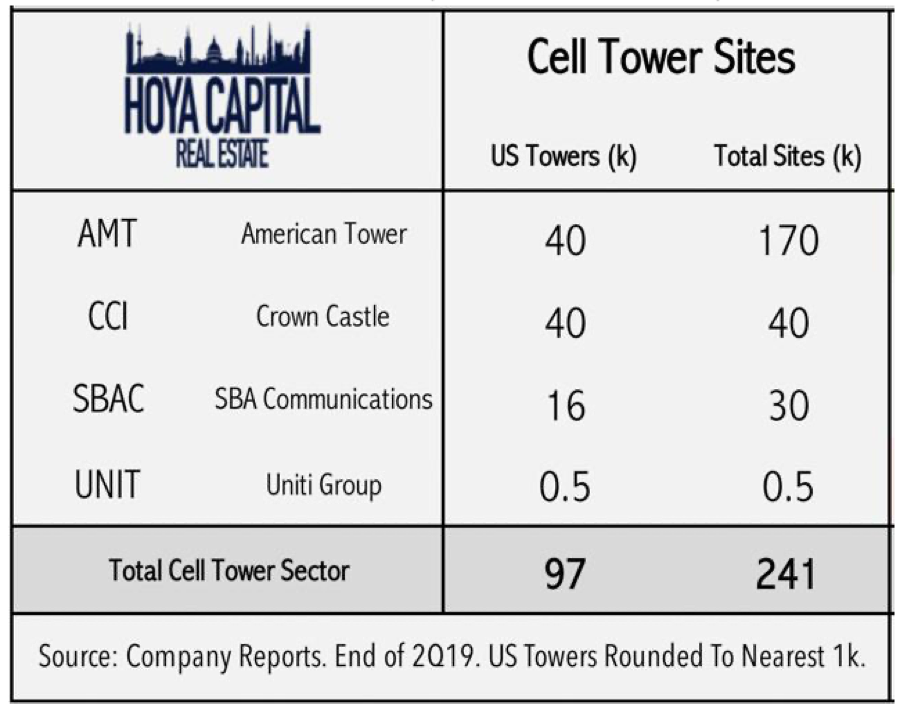

Cells Phone REITs constitute a $125 billion market and make up 10% of the REIT indexes. They own 50%-80% of all investment-grade towers. They are all benefiting from a massive upgrade cycle to accommodate the 5G rollout. These REITs own or lease the land under the cell towers and then lease them to the phone companies, like Verizon (VZ), AT&T (T), T-Mobile (TMUS), and Sprint (S) for ten years with 3% annual escalation contracts.

American Tower (AMT) is far and away the largest such REIT, with 170,000 towers, has provided an average annual return over the past ten years, and offers a fairly safe 1.65% yield. They are currently expanding in Africa. Even during the 2008 crash, (AMT) still delivered an 8% earnings growth.

SBA Communications (SBAC) is the runt of the sector with only 30,000 towers. However, it has a big presence in Central and South America and is seeing earnings grow at a prolific 80% annual rate. (SBAC) is offering a 1.48% yield at today’s prices.

Crown Castle International (CCI) is in the middle with 40,000 large towers and 65,000 small ones. 5G signals travel only a 1,000 meters, compared to several miles for 4G, requiring the construction of tens of thousands of small towers where (CCI) is best positioned. (CCI) offers a hefty 3.39% yield.

Small cell towers are roughly the size of an extra-large pizza box and will soon be found on every urban street corner in the US. AT&T (T) has estimated that there is a need for over 300,000 small cell phone towers in the US alone.

So, if you’re looking for a sea anchor for your portfolio, a low-risk, high-return investment that won’t see a lot of volatility, Cell phone REITs may be your thing. Buy (CCI) on dips.

Can you hear me now?

Mad Hedge Technology Letter

January 8, 2020

Fiat Lux

Featured Trade:

(THE TOP IS NOT IN FOR TECH STOCKS))

(AAPL), (FB), (GOOGL)

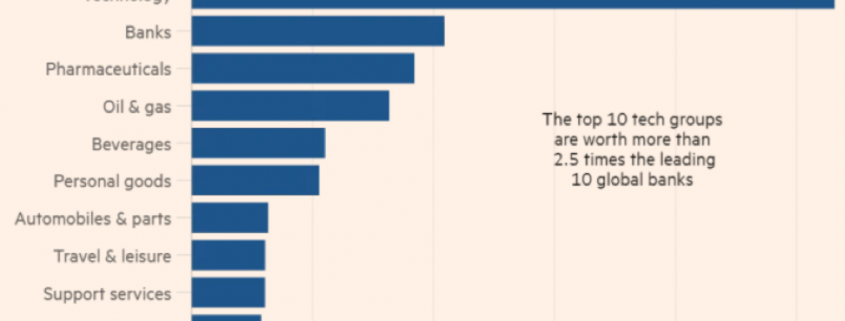

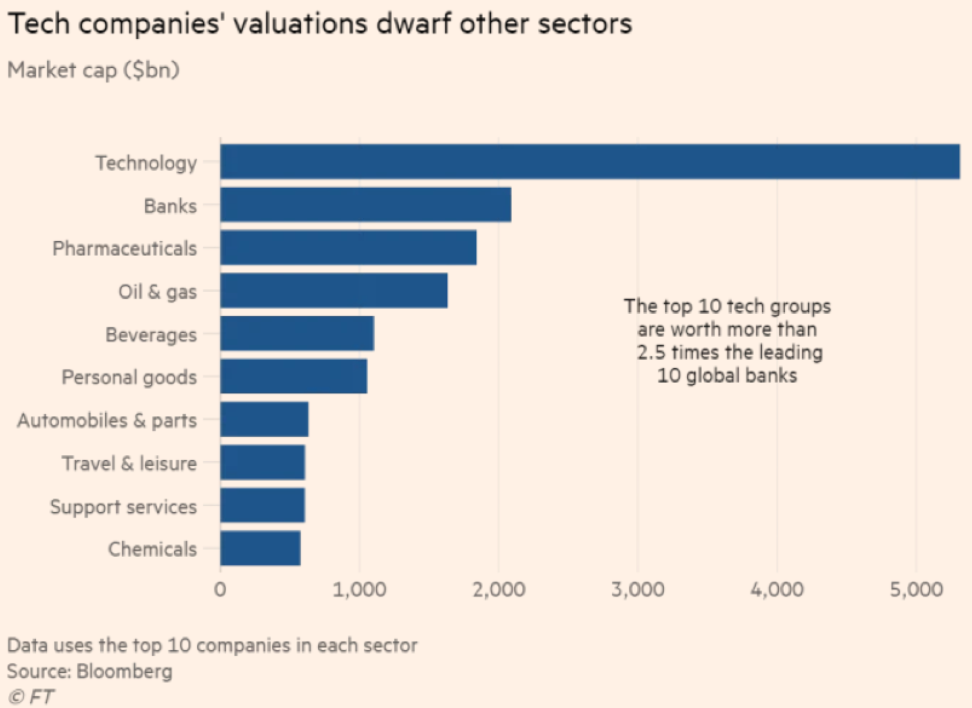

Tech shares are pricey, but that doesn’t mean they can’t get more expensive.

Strength often begets strength.

Let’s take for instance Apple (AAPL) – it delivered investors 86% in 2019 and that was their best performance in the past 10 years.

This was on the heels of a tumultuous 2018 where Apple sank 6%.

Many of the best of brightest of the tech industry beat the S&P last year, which itself gained 29%.

And as Apple leapfrogged into the software as a service business, they find themselves shunning China hardware revenue that got themselves into the 2018 mess.

Apple is betting that the confines of stateside consumer culture will offer greener pastures.

Overall, the market is pricing in a lukewarm 2020 for tech earnings boding well for the elite tech stocks that celebrated touchdown after touchdown in 2019.

Surpassing low expectations could be another rewind back to Q4 2019 which was a time that offered tech shares a platform to surge to all-time highs.

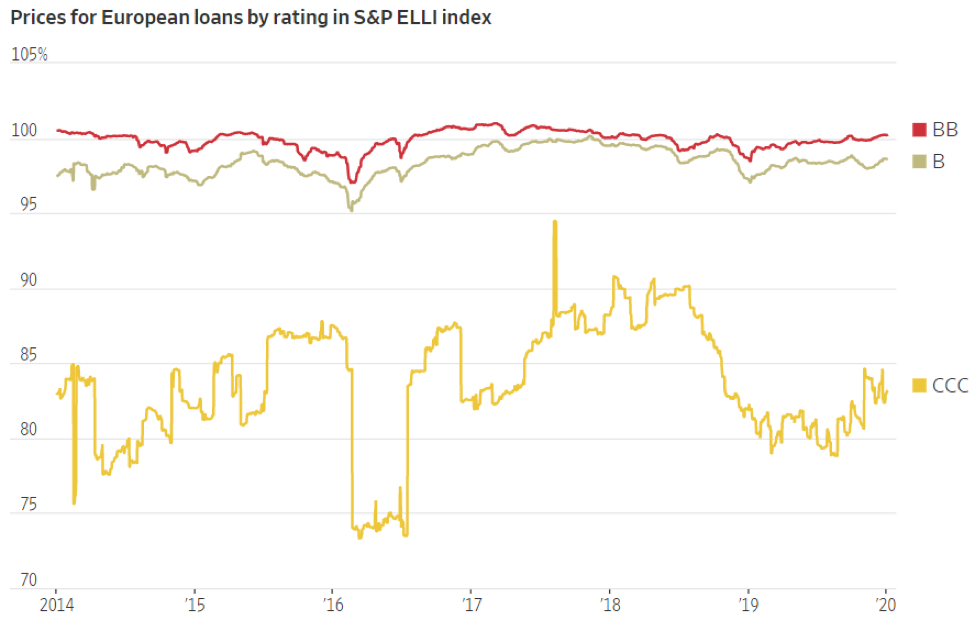

The worrying development for 2020 is that poorer-rated tech corporations won’t have the same access to cheap debt as they did in 2018 or even 2019.

The chapter of loose credit is about to close stymying loss-making tech companies who thought they could use subsidies to achieve success.

The prices of CCC-rated European bonds have declined immensely in the past year showing investors' lack of appetite for the riskier part of the corporate debt market.

Venture capitalists aren’t going to foot the bill for the next big thing in Silicon Valley at this point in the economic cycle unless the unit economics are too good to be true.

The story of 2020 will be the intensification between the haves and have nots in tech.

This is the case of the market putting a premium on time-honored tech brands and bulletproof balance sheets that they have cultivated.

On a broader level, the Fed who has presided over a $600 billion expansion in their balance sheet in the last four months offers yet another tailwind to tech shares in the short-term.

The Fed’s decision in the last few months to re-start large-scale asset purchases will help keep a foot under tech shares in early 2020 and responds like a de facto QE.

If you thought 2019 was a bad year for Uber and Lyft, then wait until this year plays itself out.

The gig economy stocks are in the direct firing line with nowhere to run and other non-sensical profit models will find it costly to search for debt alternatives in which to service their visions.

If the tech sector does become a war of attrition between the FANGs staving off one another by acquiring inorganic growth, then marginal tech players will get squeezed because they don’t have the capital bazookas to compete with the likes of Facebook (FB) and Google (GOOGL).

This is the year that we could see a slew of fringe tech companies go bust as debt markets sour on false narratives of future profits and equity markets turn against them.

The feast versus famine theme is also aligned with 5G, with many of the same cast of characters such as Apple, Alphabet posed to usurp revenue when this new technology finally becomes pervasive in consumer culture.

The Apple refresh cycle will dust off its playbook for another blockbuster rollout later this year when Apple debuts its much-awaited 5G phone.

Much of the share appreciate in Apple of late can be attributed to the anticipation of the new iPhone and the fresh infusion of revenue that branches off from it.

The applications that result from the new 5G Apple phone is seen as a luscious force multiplier to many 3rd party companies as well.

Chip stocks will be counted on as the ones lifting the tech foundations and just looking at shares in China, demonstrations of frothiness are running wild throughout their markets.

The Chinese government, to counteract the trade war, has been on a mission to flood its tech sector with unlimited capital as a catchup mechanism to overcome its inferior domestic chip industry.

Will Semiconductor, a supplier of integrated circuit products for telecommunications and electronics for cars, delivered a 390% performance in 2019 ranking it as the best performer in the Chinese stock market.

Luxshare Precision Industry and GoerTek, suppliers of consumer electronics products supplying Apple, and GigaDevice Semiconductor, producing flash chips, weren’t too shabby either each eclipsing at least 193% last year.

Even though 5G construction isn’t fully operational, I can attest that revenue creation for the companies involved are in full swing.

Investors must narrow their pickings to the biggest and financially resilient; this is not the time to expose oneself to the ugly trepidations of the mood-sensitive tech market.

For investors who can balance the delicate relationship of risk and surgical maneuvering, this year will end positive.

Mad Hedge Technology Letter

December 30, 2019

Fiat Lux

Featured Trade:

(TECH TALENT PUTS THEIR FOOT DOWN ),

(EA), (ADBE), (TSLA), (GOOGL), (TWTR)

Global Market Comments

December 30, 2019

Fiat Lux

Featured Trade:

(WILL SYNBIO SAVE OR DESTROY THE WORLD?),

(XLV), (XPH), (XBI), (IMB), (GOOG), (AAPL), (CSCO), (BIIB)

Mad Hedge Technology Letter

December 27, 2018

Fiat Lux

Featured Trade:

(WHY YOU CANNOT NEGLECT THE CLOUD)

(AMZN), (MSFT), (GOOGL), (AAPL), (CRM), (ZS)

Global Market Comments

December 27, 2019

Fiat Lux

SPECIAL ISSUE ABOUT THE FAR FUTURE

Featured Trade:

(PEAKING INTO THE FUTURE WITH RAY KURZWEIL),

(GOOG), (INTC), (AAPL), (TXN),