Mad Hedge Technology Letter

May 2, 2019

Fiat Lux

Featured Trade:

(APPLE’S HOME RUN)

(AAPL), (CRM), (GOOGL)

Mad Hedge Technology Letter

May 2, 2019

Fiat Lux

Featured Trade:

(APPLE’S HOME RUN)

(AAPL), (CRM), (GOOGL)

The company that Steve Jobs built is an earnings thoroughbred with money growing out of their ears.

Apple’s earnings report was real confirmation that Apple’s pivot into a services company is overshadowing its drop in iPhone revenue.

They even elevated forward guidance for next quarter.

Being an economic bellwether that it is, the earnings success could point to more bullish momentum for not only the tech sector but the broader market.

The tech strength showing up in the squiggly figures of the sector’s earnings report indicates that the expected earnings recession will be more of a pause rather than a dip that was first expected.

The next bout of bullish strength that permeates through the market will take many tech stocks to higher highs.

The numbers backed up this premise with Q2 2018 revenue from the services category comprising 20% of total revenue in Q2 2019—a rubber stamp of confidence that this isn’t a false dawn after service sales only comprised of 16% of total revenue the prior year.

The death of the smartphone is upon us with most people who can afford a premium one already using one as we speak with no intentions for a quick refresh.

Apple’s strategy of selling expensive iPhones to Chinese nationals is over with iPhone sales getting slaughtered by 17% to about $31 billion—an accelerated decline for a product that has been hamstrung by smartphone rivals in China offering better phones for lower prices.

The $11.5 billion from its services division and the end result of registering revenue in the high end of its $55-59 billion projection for the quarter is a stark shift from the underperformance of 2018 when Chinese iPhones sales were so bad that they stopped reporting the segment altogether.

The $58 billion of quarterly revenue was still a drop of 5% YOY which included $31 billion in iPhone sales, a shell of its former self when they generated $37.5 billion in iPhone sales the same quarter in 2018.

The disruption in handing off the baton to the services brigade caused outsized ructions inside the company causing the stock to plummet 20% last winter.

Wearables put the cherry on top of the sundae expanding at a rate close to 50% during the quarter with AirPods and Apple Watch leading the charge as best sellers.

Apple plans to inject $75 billion on share repurchases and it also approved a 75-cent dividend per share, a 5% increase.

These repurchases could boost Apple’s stock by up to 7% per year offering investors another compelling reason to hold this stock long-term.

The upgraded dimensions of Apple’s business model could finally give investors peace of mind as they wean themselves from Chinese iPhone sales.

Moving forward, the relationship between American tech and the Chinese consumer will be contentious at best, and battling with Huawei on its turf is not a sensible strategy.

Highlighting this weakness were the Greater Chinese revenue registering only $10.2 billion in sales, down from the Q2 2018 tally of $13 billion.

On the positive side, the Chinese weakness is already baked into the pastry ceding way for the services narrative to move to the forefront.

Generating more incremental revenue from its existing base of 1.4 billion Apple accounts is the order of the day.

I initially believed Apple would make major headway in the services segment and foresaw services composing about 25% of total revenue.

However, I didn’t believe they would be able to achieve this for a few years, and the surprise to investors is the velocity of change to the upside in its services business.

Adding the new magazine subscription for $9.99 to its platform is another feather in their cap even though it doesn’t transform the industry.

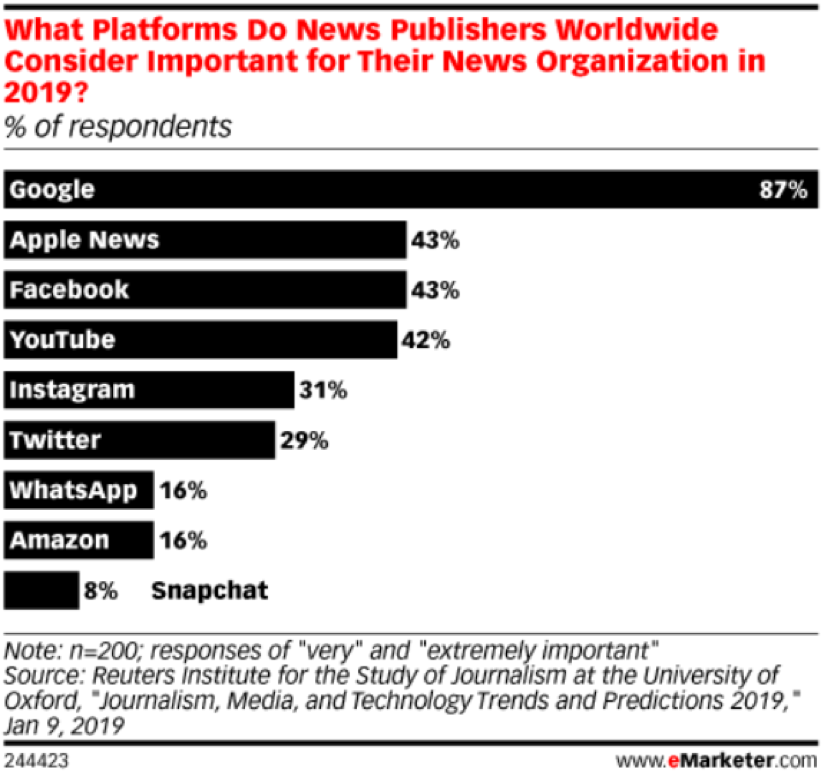

Respondents to emarketer.com made it widely known that Apple as a platform was the second most important platform for news publishers behind Google offering a great opportunity to carve out more income from their new news app.

Apple is still in dire need of attractive video options for its content basket and assets on the market are plenty from live sports, shows, movies, and video games.

My money would be on Cook to prefer video games as a viable growth driver because it resonates deeply with younger audiences from abroad and avoids the polarity of controversial content which societies are increasingly sensitive to.

Another option would be to dive headfirst into the enterprise software business moving towards a Salesforce (CRM) model selecting cloud companies à la carte to integrate into a business cloud.

Many Apple device holders already wield their devices for their own online businesses, and this would represent a solid growth driver if they could make their services more business-friendly.

What can we expect moving forward?

In short, less iPhone sales and more service revenue as a proportion of total revenue.

If Apple can carefully choreograph its downshift of iPhones sales that doesn’t destroy overall revenue and profitability, they will successfully manage in transforming the company into a hybrid service company.

I believe that Apple’s services will contribute around 30% of total revenue by 2020 and this is a big deal that will buoy the stock.

Ultimately, these are happier times for Apple as their bet on services isn’t getting bogged down, eclipsing expectations, and will cement their status as a sure-fire $1 trillion market cap company.

Bravo!

Mad Hedge Technology Letter

April 24, 2019

Fiat Lux

Featured Trade:

(WHO BEAT WHOM IN THE APPLE/QUALCOMM BATTLE)

(QCOM), (INTC), (AAPL)

The 5G bonanza is slithering towards us in a slow yet predictable motion – that was the takeaway from Apple finally conceding that its bargaining positioning was weaker than initially thought.

Apple made amends with chipmaker Qualcomm (QCOM) in the nick of time, let me explain.

Qualcomm is the leader of 5G chip technology, and the two firms decided on a six-year pact that will allow Qualcomm to sell patent licensing to Apple while becoming a crucial supplier of 5G modems to the new iPhone that will roll-out to consumers in the back half of 2020.

Envisioning this 2 for 1 special a few weeks ago was impossible as the brouhaha spilled over into the national media with top executives exchanging barbs.

Qualcomm, to its credit, stayed steadfast on its position and was the bigger winner of the spat.

The rapid reaction in the stock price has vindicated Qualcomm’s initial reluctance to make a cut-price deal with Apple.

The new contract locks in Apple at around $9 per phone in licensing fees, almost double what many analysts were predicting.

Apple also paid a one-time fee of the backlog of patent usage from the past two years that many specialists estimate to be in the $6 billion range.

Qualcomm has previously stated that Apple owes them $7 billion from the kerfuffle and Apple’s refusal to pay stemmed from their belief that Qualcomm was “double dipping” – a claim based on Qualcomm charging a fee for each iPhone using its patents as well as a fee for the technology itself which Apple felt extortionate.

Ultimately, the jousting wasn’t worth the trouble as the best-case scenario of Apple saving $1 billion in patent fees was overshadowed by the opportunity cost which was significantly higher.

The updated terms see a substantial improvement for Qualcomm over the $7.50 per phone that Apple was paying before.

The end of the saga smells of desperation on CEO of Apple Tim Cook’s behalf, realizing that time was ticking down and competitors such as Huawei have already launched 5G-supported phones.

Apple is, in fact, late to the party and one of the main root causes was the logjam with Qualcomm.

If Apple didn’t come to terms with Qualcomm, suppliers and designers wouldn’t have enough time or supply to prepare to meet the fall 2020 deadline causing Apple to delay the new iPhone.

The worst-case scenario that became a realistic threat was that the new iPhone wouldn’t have been ready until 2021 – Apple shares would have dropped 20% in a heartbeat if this played out.

Avoiding this doomsday scenario is a massive bullish signal for Apple shares and brings forward revenue demand into 2020.

The new iPhone with ironically Qualcomm’s 5G modem technology is also the selling point for iPhone lovers to upgrade to a newer and faster iPhone iteration.

It’s a headscratcher that Tim Cook played his cards in the way that he did, another misstep in a long record of fumbles in the red zone.

Inevitably, scrunching up the production schedule heaps loads of pressure on the existing engineering teams to produce a flawless iPhone.

Apple simply couldn’t wait any longer and CEO of Qualcomm Steven Mollenkopf understood that, leading me to solely blame Tim Cook for this calculated error.

Where do the chips lie after this recent shakeout?

First, this piece of news is demonstrably bullish for Qualcomm and its business model while backloading around $6 billion or so in revenue onto its balance sheet.

In short, Qualcomm hit it out of the park and set itself up for the upcoming insatiable demand for 5G chips while publicly demonstrating they are best in show for 5G infrastructure equipment.

It might turn out to be Qualcomm’s best day in the history of the company and one that employees will never forget inside its headquarters.

This will embolden Qualcomm in the future to fight for the revenue that is rightfully theirs and they won’t be frightened by bigger sharks attempting to persuade them that they should receive a lesser share of the pie.

For Mollenkopf, this is his crowning moment and a pathway to another big-time job, the one day grabbing of the spoils has elevated his reputation.

Apple is a minor winner because of the adequate supply of chips that Qualcomm will provide that guarantees Apple’s engineers clarity instead of dragging itself deeper into a courtroom battle with a company that supplies an integral component to their iPhone.

Hours after the news hit the press, Intel (INTC) waived the white flag issuing a short response admitting they are exiting the 5G smartphone business, a bitter pill to swallow for a legacy company finding it difficult to stay with the big boys.

And if you remember, Intel was initially thought to be the one to provide memory to the 5G smartphone but now that notion is dead as a doornail.

Intel will hope they can capture a fair share of the 5G PC business to make up for the lost opportunity, but as consumers migrate away from PCs, shareholders could sense Intel could be left holding the bag.

Qualcomm has strengthened its stranglehold on the 5G smartphone modem market in an industry that will morph into a worldwide addressable market of $20 billion by 2025.

Even though Huawei just announced they would be willing to sell their 5G chips to Apple, Huawei and South Korea’s Samsung mainly produce chips for their in-house branded smartphones and shun feeding competitors like Apple who require the same chips.

Apple hoped to create some leveraging power to get a better 5G chip deal and loosen the jaws that gave Qualcomm a powerful position over Apple, but Intel quitting this segment left Apple with a series of bad choices and they chose the lesser of the evils.

What does this boil down to?

Qualcomm outmuscled Intel producing faster and better performing chips that supported longer battery life.

Qualcomm simply has better engineering talent.

Intel had an uphill battle in the first place, but it is clear they cut their losses because the writing was on the wall leaving Qualcomm to reap all the benefits.

Global Market Comments

April 23, 2019

Fiat Lux

Featured Trade:

(LAS VEGAS MAY 9 GLOBAL STRAGEGY LUNCHEON)

(APRIL 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(FXI), (RWM), (IWM), (VXXB), (VIX), (QCOM), (AAPL), (GM), (TSLA), (FCX), (COPX), (GLD), (NFLX), (AMZN), (DIS)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader April 17 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What will the market do after the Muller report is out?

A: Absolutely nothing—this has been a total nonmarket event from the very beginning. Even if Trump gets impeached, Pence will continue with the same kinds of policies.

Q: If we are so close to the peak, when do we go short?

A: It’s simple: markets can remain irrational longer than you can remain liquid. Those shorts are expensive. As long as global excess liquidity continues pouring into the U.S., you’ll not want to short anything. I think what we’ll see is a market that slowly grinds upward until it’s extremely overbought.

Q: China (FXI) is showing some economic strength. Will this last?

A: Probably, yes. China was first to stimulate their economy and to stimulate it the most. The delayed effect is kicking in now. If we do get a resolution of the trade war, you want to buy China, not the U.S.

Q: Are commodities expected to be strong?

A: Yes, China stimulating their economy and they are the world’s largest consumer commodities.

Q: When is the ProShares Short Russell 2000 ETF (RWM) actionable?

A: Probably very soon. You really do see the double top forming in the Russell 2000 (IWM), and if we don’t get any movement in the next day or two, it will also start to roll over. The Russell 2000 is the canary in the coal mine for the main market. Even if the main market continues to grind up on small volume the (IWM) will go nowhere.

Q: Why do you recommend buying the iPath Series B S&P 500 VIX Short Term Futures ETN (VXXB) instead of the Volatility Index (VIX)?

A: The VIX doesn’t have an actual ETF behind it, so you have to buy either options on the futures or a derivative ETF. The (VXXB), which has recently been renamed, is an actual ETF which does have a huge amount of time decay built into it, so it’s easier for people to trade. You don’t need an option for futures qualification on your brokerage account to buy the (VXXB) which most people don’t have—it’s just a straight ETF.

Q: So much of the market cap is based on revenues outside the U.S., or GDP making things look more expensive than they actually are. What are your thoughts on this?

A: That is true; the U.S. GDP is somewhat out of date and we as stock traders don’t buy the GDP, we buy individual stocks. Mad Hedge Fund Trader in particular only focuses on the 5% or so—stocks that are absolutely leading the market—and the rest of the 95% is absolutely irrelevant. That 95% is what makes up most of the GDP. A lot of people have actually been caught in the GDP trap this year, expecting a terrible GDP number in Q1 and staying out of the market because of that when, in fact, their individual stocks have been going up 50%. So, that’s something to be careful of.

Q: Is it time to jump into Qualcomm (QCOM)?

A: Probably, yes, on the dip. It’s already had a nice 46% pop so it’s a little late now. The battle with Apple (AAPL) was overhanging that stock for years.

Q: Will Trump next slap tariffs on German autos and what will that do to American shares? Should I buy General Motors (GM)?

A: Absolutely not; if we do slap tariffs on German autos, Europe will retaliate against every U.S. carmaker and that would be disastrous for us. We already know that trade wars are bad news for stocks. Industry-specific trade wars are pure poison. So, you don't want to buy the U.S. car industry on a European trade war. In fact, you don’t want to buy anything. The European trade war might be the cause of the summer correction. Destroying the economies of your largest customers is always bad for business.

Q: How much debt can the global economy keep taking on before a crash?

A: Apparently, it’s a lot more with interest rates at these ridiculously low levels. We’re in uncharted territory now. We really don't know how much more it can take, but we know it’s more because interest rates are so low. With every new borrowing, the global economy is making itself increasingly sensitive to any interest rate increases. This is a policy you should enact only at bear market bottoms, not bull market tops. It is borrowing economic growth from futures year which we may not have.

Q: Is the worst over for Tesla (TSLA) or do you think car sales will get worse?

A: I think car sales will get better, but it may take several months to see the actual production numbers. In the meantime, the burden of proof is on Tesla. Any other surprises on that stock could see us break to a new 2 year low—that's why I don’t want to touch it. They’ve lately been adopting policies that one normally associates with imminent recessions, like closing most of their store and getting rid of customer support staff.

Q: Is 2019 a “sell in May and go away” type year?

A: It’s really looking like a great “Sell in May” is setting up. What’s helping is that we’ve gone up in a straight line practically every day this year. Also, in the first 4 months of the year, your allocations for equities are done. We have about 6 months of dead territory to cover from May onward— narrow trading ranges or severe drops. That, by the way, is also the perfect environment for deep-in-the-money put spreads, which we plan to be setting up soon.

Q: Is it time to buy Freeport McMoRan (FCX) in to play both oil and copper?

A: Yes. They’re both being driven by the same thing: China demand. China is the world’s largest new buyer of both of these resources. But you’re late in the cycle, so use dips and choose your entry points cautiously. (FCX) is not an oil play. It is only a copper (COPX) and gold (GLD) play.

Q: Are you still against Bitcoin?

A: There are simply too many better trading and investment options to focus on than Bitcoin. Bitcoin is like buying a lottery ticket—you’re 10 times more likely to get struck by lightning than you are to win.

Q: Are there any LEAPS put to buy right now?

A: You never buy a Long-Term Equity Appreciation Securities (LEAPS) at market tops. You only buy these long-term bull option plays at really severe market selloffs like we had in November/December. Otherwise, you’ll get your head handed to you.

Q: What is your outlook on U.S. dollar and gold?

A: U.S. dollar should be decreasing on its lower interest rates but everyone else is lowering their rates faster than us, so that's why it’s staying high. Eventually, I expect it to go down but not yet. Gold will be weak as long as we’re on a global “RISK ON” environment, which could last another month.

Q: Is Netflix (NFLX) a buy here, after the earnings report?

A: Yes, but don't buy on the pop, buy on the dip. They have a huge head start over rivals Amazon (AMZN) and Walt Disney (DIS) and the overall market is growing fast enough to accommodate everyone.

Q: Will wages keep going up in 2019?

A: Yes, but technology is destroying jobs faster than inflation can raise wages so they won’t increase much—pennies rather than dollars.

Q: How about buying a big pullback?

A: If we get one, it would be in the spring or summer. I would buy a big pullback as long as the U.S. is hyper-stimulating its economy and flooding the world with excess liquidity. You wouldn't want to bet against that. We may not see the beginning of the true bear market for another year. Any pullbacks before that will just be corrections in a broader bull market.

Good Luck and Good Trading

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

Mad Hedge Technology Letter

April 18, 2019

Fiat Lux

Featured Trade:

(NETFLIX’S WORST NIGHTMARE)

(NFLX), (DIS), (FB), (AAPL)

Netflix came out with earnings yesterday and revealed guidance that many industry analysts were dreading.

It appears that Netflix’s relative subscriber growth rate has reached the high-water mark for now.

Competition is rapidly encroaching Netflix’s moat.

In a letter to shareholders, management opined revealing that they do not “anticipate these new entrants will materially affect our growth.”

I am quite bothered by this statement because one would have to be blind, deaf, and dumb to believe that Disney (DIS) or Apple’s (AAPL) new products will not take away meaningful eyeballs from Netflix.

These companies are all competing in the same sphere – digital entertainment.

Papering over the cracks with wishy washy rhetoric was not something I was doing backflips over.

Netflix’s management knew this earnings report had nothing to do with results because everyone wanted to reassess how bad the new entrants would make life for Netflix.

Disney has the content to inflict major damage to Netflix’s business model.

The mere existence of Disney as a rival weakens Netflix’s narrative substantially in two ways.

First, Disney’s entrance into the online streaming game means Netflix will not have a chance to raise subscription prices for the short to medium term.

The last price hike was done in the nick of time and even though management mentioned it followed through “as expected,” losing this financial lever gives Netflix less ammunition going forward and caps EPS growth potential.

Second, another dispiriting factor is the premium for retaining and acquiring original content will skyrocket with more firms jockeying for the same finite amount of actors, producers, directors, and writers.

This particular premium cannot be quantified but firms might try to bid up the cost of certain talent just so the other guy has to foot a bigger bill, this is done in professional sports all the time.

Firms might even take actors off the table with exclusive contracts just to frustrate the supply of content generators.

Uncertainty perpetuates with the future cost of content unable to be baked into the casserole yet, and represents severe downside risk to a stock which trots out an expensive PE ratio of 133.

Growth, growth, and more growth – that is what Netflix has groomed investors to obsess on with the caveat of major strings attached.

This model is highly effective in a vacuum when there are no other players that can erode market share.

Delivering on growth justifies heavy cash burn, and to Netflix’s credit, they have fully delivered in spades.

The strings attached come in the form of steep losses in order to create top of the line content.

Planning to revise down annual cash flow from $3 billion to $3.5 billion in 2019 will serve as a litmus test to whether investors are ready to shoulder the extra losses in the near term.

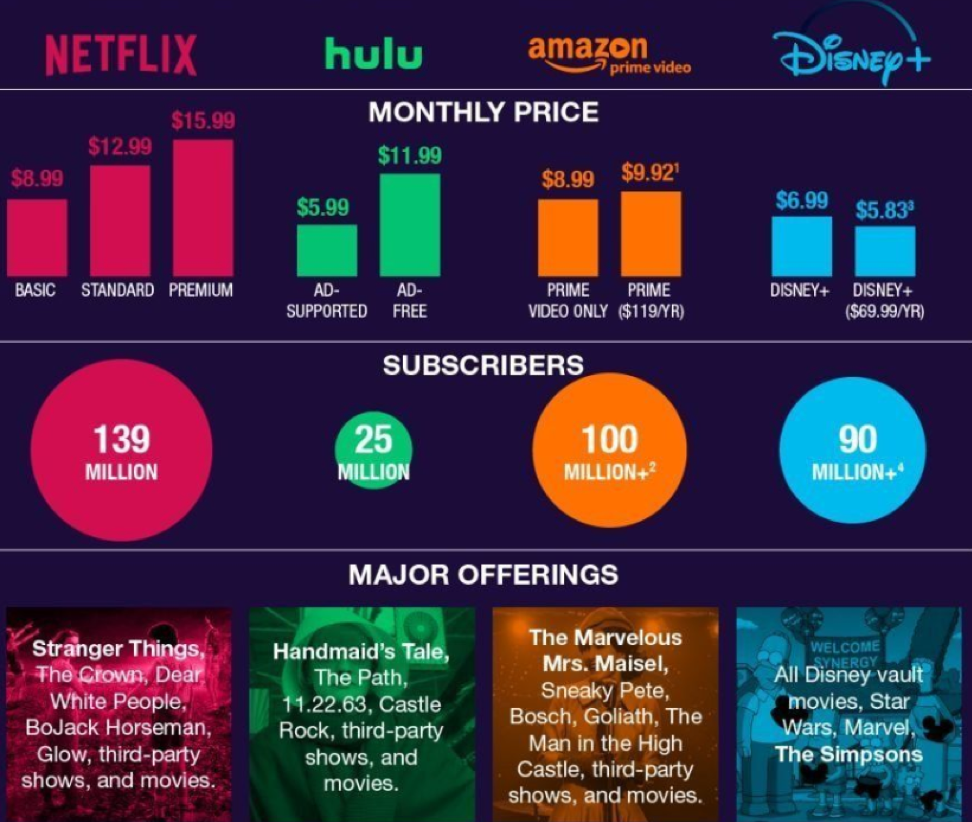

I found it compelling that Disney Plus will debut at $6.99 per month – add that to the price of Netflix’s standard package of $12.99 and you get a shade under $20.

Disney hopes to dictate spending habits by psychologically grouping Disney and Netflix for both at under $20.

The result of breaching the $20 threshold might push customers into ditching Netflix and sticking with the $6.99 Disney subscription.

Then there is the thorny issue of Netflix’s growth – the quality and trajectory of it.

The firm issued poor guidance for next quarter projecting total paid net adds of 5.0m, representing -8% YOY with only 300,000 adds in the US and 4.7m for the international segment.

Alarm bells should be sounding in the halls when the most lucrative segment is estimated to decelerate by 8% YOY.

Domestic subscriptions deliver higher margins bumping up the average revenue per user (ARPU).

Contrast this with Netflix’s basic Indian package costing $7.27 or 500 rupees and a mobile package of $3.63 or 250 rupees.

In my opinion, domestically decelerating in the high single digits does not justify the additional annual cash burn of half a billion dollars even if you accumulate millions of more Indian adds at lower price points.

This leads me to surmise that the quality of growth is beginning to slip, and Netflix appears to be running into the same type of quagmire Facebook (FB) is facing.

These models are grappling with stagnating or slowing North American growth and an emerging market solution isn’t the panacea.

The Netflix Indian packages are actually considered expensive by local standards meaning that Netflix’s won’t be able to crowbar in price hikes like they did in America.

On the positive side, Netflix did beat Q1 estimates with paid net adds up 9.6 million with 1.74m in the US and 7.86m internationally, up 16% YOY.

Netflix was able to reach revenue of $4.5B, a company record mostly due to the $2 price hike during the quarter in America.

The letter to shareholders simplifies Netflix’s tactics to investors explaining, “For 20 years, we’ve had the same strategy: when we please our members, they watch more and we grow more.”

What this letter doesn’t tell you is that Disney and the looming battle with Netflix will reshape the online streaming landscape.

In simple economics, an increase of supply caps demand, and don’t get sidetracked by the smoke and mirrors, Disney and Netflix are absolutely fighting for the same eyeballs no matter how much Netflix plays this down.

To highlight an example of how these two are directly competing against each other – let’s take the cast of Monica, Chandler, Rachel, Ross, Joey, and Phoebe – in the hit series Friends.

Netflix acquired the broadcasting rights from Warner Bros, who owns Disney, and it was the most popular show on Netflix.

Warner Bros, knowing that Disney were on the verge of rolling out an online streaming product, renewed Netflix for 2019 at $80 million.

Not only were they hand feeding the enemy in broad daylight, but they handicapped their new products as it is about to debut.

Whoever made that decision must go into the hall of shame of boneheaded online content decisions.

Once 2020 rolls around, Disney will finally be able to slap Friends on Disney Plus where it belongs, and the streaming wars will heat up to a fever pitch.

Ultimately, when Netflix brushes off reality proclaiming that if they please viewers with the same strategy, then everything will be hunky-dory, then I would say they are being disingenuous.

The online streaming industry has started to become more complex by the minute and the “same strategy” that worked wonders in a vacuum before must evolve with the times.

At $360, I would short Netflix in the short to medium term until they prove the headwinds are a blip.

If it goes up to $400, it’s a screaming short because accelerating cash burn, poor guidance, decelerating domestic net adds, and a jolt of new competition aren’t the catalysts that will take shares above the heavenly lands of $400, let alone $450.

Netflix is still a fantastic company though – I’m an avid viewer.

Mad Hedge Technology Letter

April 11, 2019

Fiat Lux

Featured Trade:

(THE MEANS TO A FRIGHTENING END)

(AMZN), (FB), (GOOGL), (AAPL)

Death of websites.

I love doing presentations to small businesses on my free time, partly to stay in touch with the pulse of the Davids who have the unenviable task of fighting uphill against the Goliaths.

It’s bad enough that the tech giants have scaled locally turning one’s local playground into a disadvantage.

The presentation is aptly titled "Content is King... But Only Through One’s Ownership" where the same parallels are explored and unpacked for my audience.

Proprietary Content – must be yours and you must own it on your own turf - your blog, your vlog, your app, and so on, it goes for everything.

Repurposing content on other platforms as a supplement to your own is one thing, but the moment you adopt an enemy platform as your main platform, that’s your coup de grâce.

SMEs (small businesses enterprise) believe it’s plausible to work with the higher ups, but don’t forget they have every incentive to cut you off from the fountain of youth.

One could say the best skill big tech has today is undermining their competition.

Facebook doesn’t allow posting content that criticizes Facebook, have you ever wondered why?

Website innovation has grinded to a halt because of the PageRank algorithm from Google, everybody is making websites the same, a top nav, descriptive text, a smattering of images and a handful of other elements arranged similarly.

Google’s algorithms and the self-regulating nature of their ecosystem have perverted the chance to have a unique online experience.

Most internet users have probably discovered that most websites don’t work well and the execution of them is lousy.

Many companies are not contributing enough resources to build out their site properly, or just don’t have the cash to fund it or a mix of the two.

About 95% of customer service calls originate from the company’s webpage because of payment problems, disfunction, misleading content, or simply because the website is down.

Ask any small business and they will tell you they deal with their domain being down for hours at a time because of some unknown server problem.

Not only is capitalism only working for a small group of Americans, but so are websites, such as massive companies like Amazon.com who have worked wonders with its e-commerce site.

Because the internet and namely websites are the key to building businesses, Silicon Valley is now using the concept of websites and their position as de-facto moderators to prevent others from developing proper websites, killing off the competition.

Alphabet is notorious for ranking their own products at the top of page one of any Google search.

Amazon has followed the same practice by sticking their in-house brands at the top of any Amazon search on Amazon.com.

And remember that none of this can be called “antitrust” because these borderline tactics offer consumers lower prices but that is only because consumers are brainwashed to believe Amazon offers the lowest price.

What if the same products are available for half of Amazon’s in-house brands, would Amazon volunteer to post their in-house brands on the second page, the graveyard of search results?

I would guess no.

Websites used to give businesses a chance, remember in the mid-90s when a website of any ilk was impressive as if someone was walking on water.

What can we expect next?

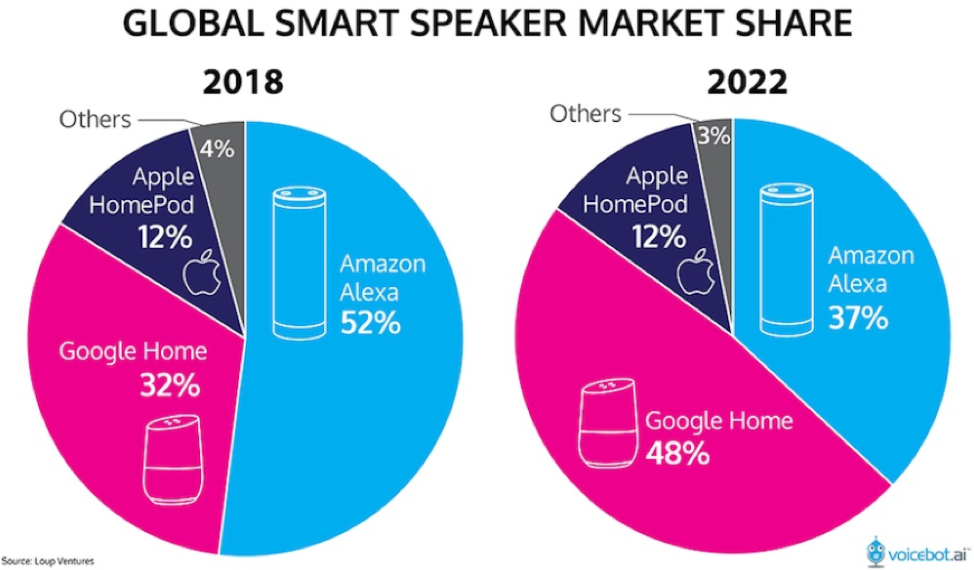

Amazon, Google, and Apple are taking their shows to artificial intelligence voice platforms.

SMEs could at least throw hail marys on standard internet searches with visual screens, but once content migrates over to voice platforms owned by Silicon Valley, then its game, set, and match.

For instance, a local business such as Joe’s Furniture Moving Business who, with the internet and visual screens, is searchable through search engines and can be even located on Google Maps with a concrete address.

Once we migrate the lions share of content to voice platforms over the next 15 years, Google Home, Apple HomePod, or Amazon Alexa could easily choose to remove Joe’s Furniture Moving Business information because they make more money offering you information of a moving service they own or have a stake in.

The advent of 5G will refine the voice technology and enhance the machine learning techniques needed to complete the migration of content.

Once the world crosses an inflection point where the technology and volume of content on smart speakers outweigh the hassle to use a keyboard or mobile screen, this effectively makes these smart speaker manufacture Gods of the World because they will own the voice-based internet.

They will be the gatekeepers of all global information, business, and development in the world and we will need to satisfy their algorithms to get our own content uploaded on their voice platforms.

And because of the nature of voice, users cannot see what else is out there, users will only hear what these companies tell us offering an outsized opportunity to manipulate the user experience generating more dollars for these powerful platforms.

By the end of 2019, 74 million Americans will be using smart speakers, giving these smart speaker firms adequate data to fine tune their products.

Eventually, all Americans will be forced to use it or will not be able to function, similar to the effects of a laptop, email, and smartphone combination now.

Once these voice platforms become ubiquitous, websites will be deemed irrelevant – consumers will simply have a choice of Google Home, Amazon Alexa, and Apple HomePod and blindly trust what they tell you is in your best interests.

Pick your poison.

That’s right, users won’t control content in about 15 years, a scary thought, and now you understand why these companies will even give their voice A.I. platforms for free if they have to and probably will in the future.