Global Market Comments

February 4, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or FROM PANIC TO EUPHORIA),

(SPY), (TLT), (AAPL), (GLD),

Global Market Comments

February 4, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or FROM PANIC TO EUPHORIA),

(SPY), (TLT), (AAPL), (GLD),

What a difference a month makes!

In a mere 31 days, we lurched from the worst December in history to the best January in 30 years. Traders have gone from lining up to jump off the Golden Gate Bridge to ordering Dom Perignon Champaign on Market Street.

However, not everything is as it appears. The suicide prevention hotline on the bridge has been broken for years, and you can now pick up Dom Perignon at Costco for only $120 a bottle.

Clearly, investors are enjoying the show but are keeping one eye on the exit. Perhaps that’s why gold (GLD) hit an 8-month high as nervous investors Hoover up a downside hedge against their long positions.

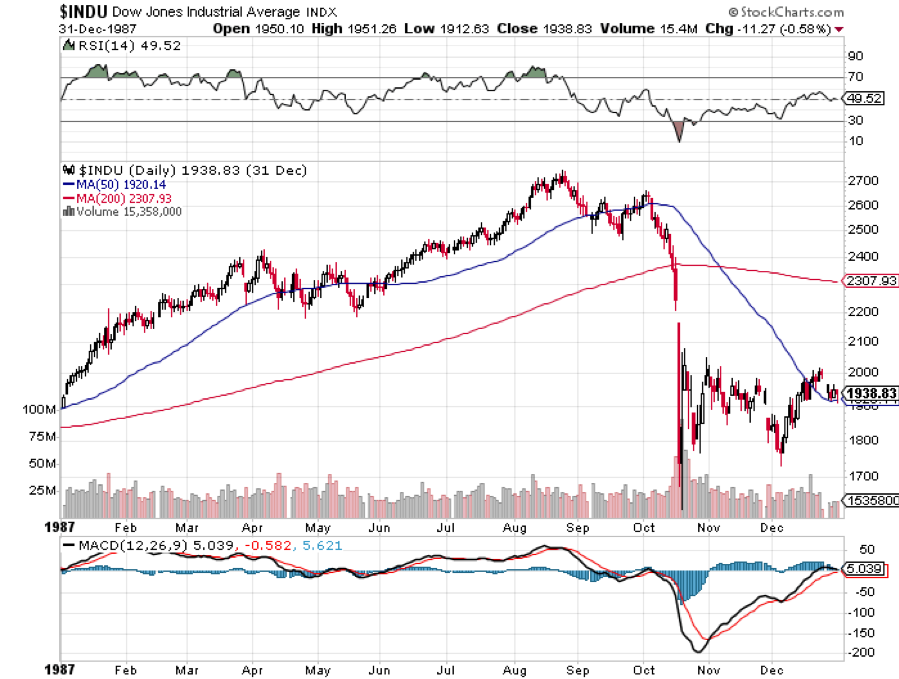

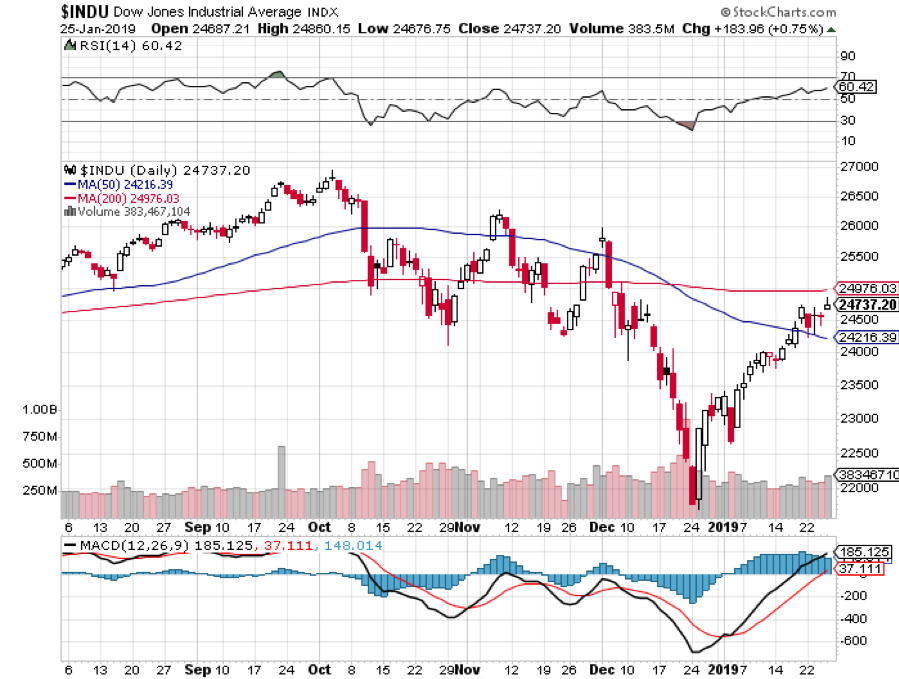

In fact, it has been the best January since 1987, with a ferocious start. The problem with that analogy is that I remember what followed that year (see chart below). After a robust first nine months of the year, the Dow Average (INDU) broke the 50-day moving average. It looked like just another minor correction and a buying opportunity.

The market ended up plunging 42% in weeks including a terrifying 20% capitulation swan dive on the last day. I tried actually to buy the stock at the close that day. The clerk just burst into tears and threw the handset on the floor. I didn’t get filled. Since the tape was running two hours late, NOBODY got filled on any orders entered after 12:00 PM.

It doesn’t help that markets have been rising in the face of a collapsing earnings picture. Look at the chart below and you’ll see that after peaking out at an annualized 26% a year ago in the wake the passage of the new tax bill, earnings have been rolling over like the Bismarck on their way to zero.

If you own stocks anywhere in the world, this chart should have made the hair on the back of your neck stand up. It’s almost as if the tax bill was delivering the OPPOSITE of its intended outcome.

How multiple expansion will we get in the face of fading earnings? How about none? How about negative!

A totally red-hot January Nonfarm payroll Report on Friday at 304,000 confirmed that the economy was still alive and well, at least on a trailing basis. Headline Unemployment Rate rose to 4.0%.

The Labor Department said that the government shutdown had no impact on the numbers because federal employees were furloughed and not unemployed. Tomato, tomahto.

However, 175,000 workers were laid off in the private sector and that is why the Unemployment Rate ticked up to a multi-month high. Noise from the shutdown is going to be affecting all data for months.

That’s also why part-time workers jumped 500,000 in January. A lot of federal employees started working as Uber drivers and pizza delivery guys to put food on the table without a paycheck.

Further confusing matters was the fact that December was revised down by 90,000.

Leisure & Hospitality led the way with 74,000 new jobs, followed by Construction with 52,000 and Health Care by 42,000 jobs.

The shutdown is over, but how much did it cost us? Standard & Poor’s says $6 billion but the restart costs will be greater. More recent estimates run as high as $11 billion.

Weekly Jobless Claims were up a stunning 53,000, to 253,000, an 18-month high. While government workers can’t claim, their private subcontractors can, hence the massive shutdown-driven jump.

Bitcoin hits a new one-year low at $3,400. Some $400 billion has gone to money Heaven since 2017. Only $113 billion in market capitalization remains. I told you it was a Ponzi scheme. US coal production hits a 39-year low as it is steadily replaced by natural gas and solar. Could there be a connection? Talk about data mining.

Earnings were mixed, with some companies coming out hero’s, others as goats.

Apple (AAPL) slightly beat expectations with revenues at $84.31 billion versus $83.97 billion expected, and earnings at $4.18 per share versus $4.17 expected. Guidance going forward is very cautious of a slowing China.

Good thing I saw the ambush coming and covered my short two days ago. A penny beat is the most managed earnings I have ever seen. To warn about earnings and then surprise to the upside is classic Tim Cook.

December Pending Home Sales cratered, down 2.2% in December and 9.8% YOY. Despite the dramatically lower mortgage interest rates, buyers fled the crashing stock market.

“PATIENCE” is still the order of the day at the Federal Reserve with its Open Market Committee Meeting ordering no interest rate rise. It was a trifecta for the doves. The free pass for stocks continues. That’s why I covered all my shorts starting from last week. Even a blind squirrel occasionally finds an acorn.

Tesla reported another profit for the second consecutive quarter, and the company is about to reach escape velocity. Model 3 production in 2019 is to reach 75% of the total output and we can expect a new pickup truck. A second factory in Shanghai will take the “3” to over a half million units a year. That $35,000 Tesla is just over the horizon.

Why are all major companies reporting good earnings but cautious guidance? Are they reading the newspapers, or do they know something we don’t? Not a great sign of a continuing bull market. Sell the next capitulation top.

This week was a classic example of how the harder I work, the luckier I get, and I have been working pretty hard lately.

I came out of a near money Apple (AAPL) put spread at cost, then rolled into a far money put spread just before the stock sold off. That little maneuver made me $1,030 in two days.

Then, I spotted a perfect “head and shoulders” top in the bond market set up by a three-point rally in the (TLT). When the red hot January Nonfarm Payroll report printed the next day at 5:30 AM PCT, bonds immediately gave back a full point.

It was all enough to boost my performance to a new all-time high after a hiatus of two months. Those who recently signed up for my service must think that I am some kind of freakin' genius! They’ll learn the truth soon enough.

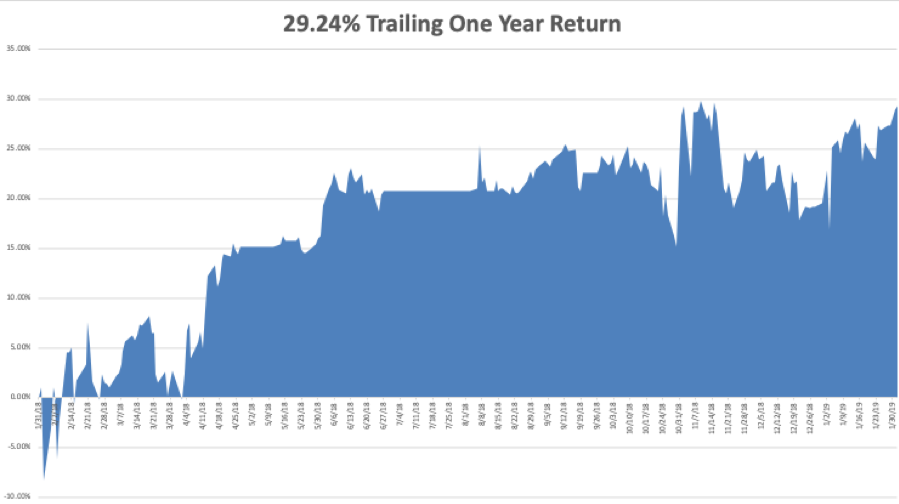

My January and 2019 year-to-date return soared to +9.66%, boosting my trailing one-year return back up to +29.24%. The is my hottest start to a New Year in a decade. Sometimes you have to make a sacrifice to the trading gods to get rewarded and that is what December was all about.

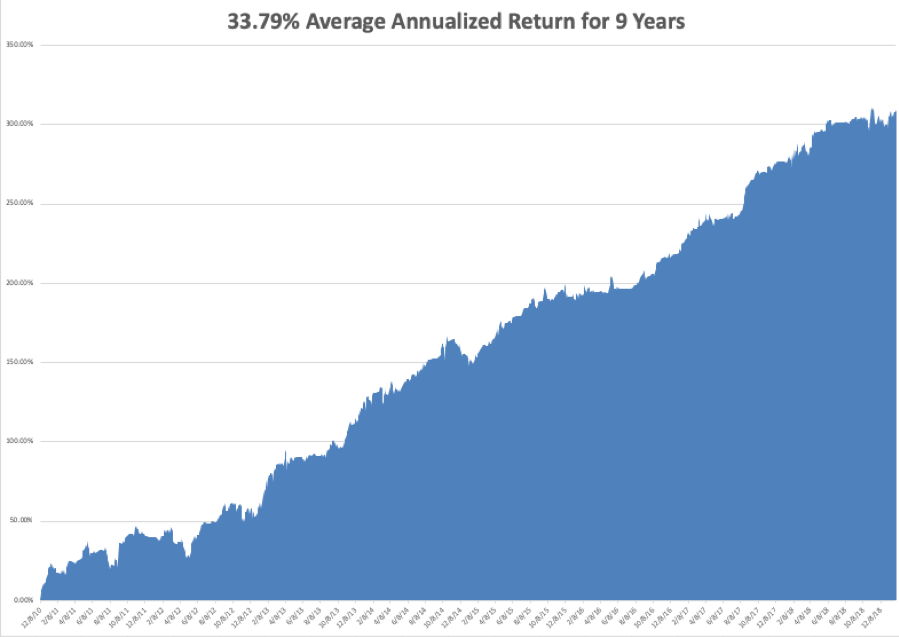

My nine-year return climbed up to +309.80%, a new pinnacle. The average annualized return revived to +33.79%.

I am now 80% in cash, short the bond market, and short Apple.

The upcoming week is still iffy on the data front because of the government shutdown. Some government data may be delayed and other completely missing. Private sources will continue reporting on schedule. All of the data will be completely skewed for at least the next three months. You can count on the shutdown to dominate all media until it is over.

Jobs data will be the big events over the coming five days along with some important housing numbers. We also have several heavies reporting earnings.

On Monday, February 4 at 10:00 AM, we get the much delayed December Factory Orders. Alphabet (GOOGL) reports.

On Tuesday, February 5, 10:00 AM EST, we learn the January ISM Non-Manufacturing Index.

On Wednesday, February 6 at 8:30 AM EST, the November Trade Balance is published.

Thursday, February 7 at 8:30 AM EST, we get Weekly Jobless Claims. December Consumer Credit follows at 9:30 AM and should be a humdinger. Intercontinental Exchange (ICE) reports.

On Friday, February 8, at 10:00 AM EST, Wholesale Inventories are out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’ll be sitting down with a case of Modelo Negro and a big bag of Cheetos to watch the commercials during the Super Bowl with my family. (My dad played for USC Varsity in 1948). I never forgave the Rams for defecting from Los Angeles, and Boston is too far away to care about.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 31, 2019

Fiat Lux

Featured Trade:

(MARKET GETS A FREE PASS FROM THE FED),

(SPY), ($INDU), (TLT), (GLD), (FXE), (UUP),

(APPLE SEIZES VICTORY FROM THE JAWS OF DEFEAT),

(AAPL)

Mad Hedge Technology Letter

January 31, 2019

Fiat Lux

Featured Trade:

(APPLE SEIZES VICTORY FROM THE JAWS OF DEFEAT),

(AAPL)

After an almost 40% swan dive, Apple has found solid footing at these levels for the time being. 40% seems to be the magic number. Declines ALWAYS end at 40% with Apple.

About time!

It’s been an erratic last few months for the company that Steve Jobs built and this last earnings report will go a long way to somewhat stabilize the short-term share price.

The miniscule earnings beat telegraphs to investors that the bad news has been sucked out.

That is what Tim Cook wants the investor community to think.

But is he right?

I would argue that the bad news is over for the short-term but could rear its ugly head again later – it all rides on China’s shoulders.

Let’s take a look at the numbers.

Chinese revenue was down 27% YOY locking in $13.17 billion in quarterly revenue compared to $17.96 billion the prior year.

There is no two ways about this – it’s an awful number and a hurtful manifestation of the Chinese economy decelerating.

The unrelenting pressure of the geopolitical trade war has handcuffed Beijing’s drive to deleverage its balance sheet and steer its economy to a more consumption-supportive model.

China is lamentably back to its traditional ways - the old economy - infusing $2.2 trillion into its balance sheet along with cutting the reserve ratio for state banks hoping to incite economic growth.

Positive short-term catalyst but negative long-term consequences.

This is why I urged Apple lovers to stay away from this stock earlier because of the uncertainty of its current strategic position.

It makes no sense to place an indirect on the current Washington administration navigating a China soft landing.

As it stands, most of Apple’s supply chain is in China and moving it out will be done in piecemeal which is happening behind the scenes and will cause massive job loss in China further hurting the Chinese economy.

The ratcheting up of tensions signals the untenable end of American tech supply chains in China and no new foreign investment will pour into China.

Maybe even never.

I wholeheartedly blame CEO of Apple Tim Cook for not foreseeing this development.

That is what he is paid to do.

Then there is the issue of iPhone sales in China.

Chinese citizens aren’t buying iPhones because of three reasons.

The cohort of wealthy Chinese who can afford a $1,000 iPhone might think twice if they want to be seen outside with a product from a country that is becoming adversarial. Apple has incurred hard-to-quantify brand damage to its once pristine brand in a land that once worshipped the company.

The refresh cycle has elongated because Apple manufactures great smartphones and iPhone holders are waiting it out on the sidelines two or even three iterations down the road to upgrade because that is when they can unearth the relative value of the product.

Lastly, local Chinese smartphone markers have greatly enhanced their products because of a function of time and borrowed Western technology. It is now possible to buy a smartphone that offers around 80% of performance and functionality of an iPhone but for less than half the price.

The customers on the fence who once viewed iPhones as a must-buy are now migrating to the local Chinese competitor because they are a relatively good deal.

I can surmise that these three headwinds are just beginning and will become more entrenched over time.

If the trade war becomes worse, the brand damage will accelerate. iPhones are becoming incrementally better which will delay new iPhone upgrades unless something revolutionary comes out that requires customers to upgrade to be a part of the new technology.

And sadly, Chinese competition is catching up quicker than Apple can innovate and that will not stop.

However, the silver lining is that the worst-case scenario won’t happen in the next quarter and the market won’t get wind of this until the second half of the year.

Instead of a meaningful sell-off because of this earnings report, Cook chose to front-run the weakness by reporting the hideous performance at the beginning of January.

Cook knew he needed to come clean with the negative news and the reformulated projections that were re-laid a few weeks ago were the same ones that Apple barely beat by one cent on the bottom line by posting EPS of $4.18 and marginally on the top line by $420 million.

I am in no way saying that this was a great earnings report – it wasn’t.

Apple mainly delivered on the mediocrity that they discussed a few weeks ago lowering the bar to the point where it would be a failure of epic proportions if Apple couldn’t beat significantly revised down earnings.

Then the outlook for the next quarter wasn’t as bad as people thought, but that doesn’t mean it was good.

When you start playing the game of not as bad as the market thought – it is a slippery slope to head down and halfway to the CEO getting sacked down the road.

I mentioned before that the macro headwinds came 2 years too early for Cook and pegging 60% of company revenue to a smartphone which has trended towards mass commoditization is a bad bet.

Cook has been painstakingly slow rewriting Apple as a service company which is his current get-out-of-jail-free card dangling in front of him like a juicy carrot.

iPhone gross margin is now 34.3% which is lower than the other Apple products whose margins are 38%.

Their flagship product isn’t as profitable on a per-unit basis as it once was highlighting the necessity for refreshing the product lines with not just new iterations but game-changing products.

The type of products that Steve Jobs used to mushroom popularity would suffice.

Gross margins will continue to come down as the smartphone market is saturated and customers won’t buy iPhones now unless they receive a drastic price reduction.

The result is that Apple no longer publishes iPhone unit sales to conceal the worst number for their most important and volume-heavy product.

A little too late if you tell me and irresponsible to investor transparency if you ask me.

Apple Pay, Apple Music, and iCloud storage eclipsed $10.9 billion demonstrating a 19% YOY increase.

This shows that this company still has strengths, but don’t forget that services are still less than 15% of total revenue even though they are the fastest growth part of their portfolio.

Cook isn’t doing enough to supercharge the content and services at Apple.

The top line number was $84.3 billion, a 5% YOY decline in revenue – a YOY decline hasn’t happened in 18 years and this is deeply troublesome.

Let me explain why Cook is the center of the problem.

The underlying issue is Cook doesn’t know what product should be next for Apple.

Apple dabbled with the Apple TV which didn’t pan out.

Then the autonomous vehicle unit just closed down sacking 200 employees.

And the content side of it hasn’t been developed fast enough relative to the slowing down of iPhone sales which is why you can blame Cook for being reactive instead of proactive.

It’s not like he can claim that his head was in the sand and couldn’t take note of what Netflix was doing and had gotten into that original content game sooner.

The hesitation is exactly what worries me with Cook. Cook is a great operations guy and can take an existing product, beef up margins, shave down expenses, streamline execution and boost top and bottom line profits.

Cook is being painfully exposed now that he is out of his comfort zone and must aggressively move in a direction that doesn’t have a red carpet laid out for him.

Even though the pre-earnings red flag raised many questions, Cook only satisfied these red flags on a short-term basis and Apple still needs to reconfigure its product roadmap for the long term.

If Cook plans to milk more out of the iPhone story, Apple becomes a sell the rallies stock, but the market will give the benefit of the doubt to Apple for a quarter or so.

The 800-pound gorilla in the room is the Chinese economy which could go into a hard landing if the stimulus fails to deliver economic respite or if the trade war tensions are exacerbated.

At the bare minimum, the waterfall of downgrades should be over for the time being, but this will come to the fore in a quarter or so when Apple will need to shine light on its plans moving forward.

I wouldn’t bet the ranch on Cook being innovative.

It looks like Apple will start to trade in a range.

It’s hard to believe any bad news superseding what came out at the beginning of this month in the short-term, but at the same time, there are no idiosyncratic catalysts to cause this stock to bullishly break out.

We are at an inflection point in Cook’s career and he is finding out that it's not as easy to be Apple as it used to, and mammoth decisions are on the horizon that must be addressed or possibly become the next IBM.

If you ask me, I’ve been calling on Apple to replace Cook for a while with Jack Dorsey as the signal caller, I still believe this is the only way to stay in the heavyweight division of tech titans five years from now.

Such is the competitive nature of the tech landscape these days.

Mad Hedge Technology Letter

January 29, 2019

Fiat Lux

Featured Trade:

(WHATS BEHIND THE NVIDIA MELTDOWN),

(QRVO), (MU), (SWKS), (NVDA), (AMD), (INTC), (AAPL), (AMZN), (GOOGL), (MSFT), (FB)

Great company – lousy time to be this great company.

That is the least I can say for GPU chip company Nvidia (NVDA) who issued a cataclysmic earnings alert figuring it was better to spill the negative news now to start the healing process earlier.

This stock is a great long-term hold because they are the best of breed in an industry fueled by a secular tailwind in GPUs.

But this doesn’t mean they will be gifted any freebies in the short term and, sad to say, they have been dragged, kicking and screaming, into the heart of the trade skirmish along with Apple (AAPL) and buddy Intel (INTC) amongst others.

The best thing a tech company can have going for them right now is to have no China exposure, that is why I am bullish on software companies such as PayPal, Twilio, and Microsoft.

I called the chip disaster back in summer of 2018 recommending to stay away like the plague.

The climate has worsened since then and like I recently said – don’t buy the dead cat bounce in chips because the bad news isn’t baked into the story yet or at least not fully baked.

It’s actually a blessing in disguise if banned in China if you are firms such as Facebook (FB), Google (GOOGL), and Amazon (AMZN).

I recently noted that a material end to this trade war could be decades away and the tech world is already being reconfigured around the monopoly board as we speak with this in mind.

Where do things stand?

The US administration took a scalp when Chinese communist backed DRAM chip maker Fujian Jinhua effectively shuttered its doors.

Victory in a minor battle will likely embolden the US administration into continuing its aggressive stance if it is working.

If you forgot who Fujian Jinhua was… they are the Chinese chip company who were indicted by the U.S. Justice Department for stealing intellectual property (IP) from Boise-based chip behemoth Micron (MU).

The way they allegedly stole the information was by poaching Taiwanese chip engineers who would divulge the secrets to the Chinese company buttressing China in pursuing their hellbent goal of being able to domestically supply enough quality chips in order to stop buying American chips in the future.

Officially, China hopes to ramp up its self-sufficiency ratio in the semiconductor industry to at least 70% by 2025 which dovetails nicely with the broader goal of Chinese tech hegemony.

Fujian Jinhua was classified as a strategically important firm to the Chinese state and knocking the wind out of their sails will have a reverberating effect around the Chinese tech sector and will deter Taiwanese chip engineers to act as a go-between.

According to a research note by Zhongtai Securities, Jinhua’s new plant was expected to have flooded the market with 60,000 chips per month and generate annual revenue of $1.2 billion directly competing with Micron with their own technology borrowed from Micron themselves.

Jinhua’s overall goal was to support a monthly manufacturing target of 240,000 chips spoiling Chinese tech companies with a healthy new stream of state-subsidized allotment of chips needed to keep costs down and build the gadgets and gizmos of the future.

For the most part, it was unforeseen that the US administration had the gall and calculative nous to combat the nurtured Chinese state tech sector.

However, I will say, it makes sense to pick off the Chinese tech space now before they stop needing American chips at all in 5-7 years and when all remnants of leverage disappear.

The short-term pain will be felt in the American chip tech sector which is evident with the horrid news Nvidia reported and the aftermath seen in the price action of the stock.

Nvidia expects top line revenue to shrink by $500 million or half a billion – it’s been a while since I saw such a massive cut in forecasts.

Half of revenue comes from the Middle Kingdom and expect huge downgrades from Apple on its earnings report too.

If this didn’t scare you, what will?

These short-term headwinds are worth it to the American tech sector as a whole.

To eventually ward off a future existential crisis when Chinese GPU companies start offering outside business actionable high quality chips curated with borrowed technology, funded by artificially low debt, and for half the price is worth its weight in gold.

The same story is playing out with Huawei around the globe but at the largest scale possible.

This is what happens when the foreign tech sector is up against companies who have access to unlimited state loans and is part of wider communist state policy to take over foundational technology globally.

I will also emphasize that the Chinese communist party has a seat on every board at any notable Chinese tech company influencing decisions at the top even more than the upper management.

If upper management stopped paying heed to the communist voice at the table, they would be out of business in a jiffy.

Therefore, Huawei founder Ren Zhengfei standing at a podium promulgating a scenario where Huawei is operating freely from the government is what dreams are made of.

It’s not a prognosis rooted in reality.

The communist party are overlords breathing down the neck of Huawei after any material decisions that can affect the company and subsequently the government’s position in the interconnected world.

The China blue print essentially entails a pan-Amazon strategy emphasizing large volume – low cost strategy.

Amazon was successful because investors would throw money at the company until it scaled up and wiped the competition away in one fell swoop.

Amazon is on a destructive path bludgeoning every American second-tier mall reshaping the economic world.

The unintended consequences have been profound with the ultimate spoils falling at the feet of CEO and Founder of Amazon Jeff Bezos, his phalanx of employees as well as Amazon stockholders which are mostly comprised of wealthy investors.

Well, Chairman Xi Jinping and the Chinese communist party are attempting to Amazon the American tech sector and the broader American economy.

The American economy could potentially become the second-tier mall in this analogy and the game playing out is an existential crisis for the likes of Advanced Micro Devices (AMD), Nvidia, Micron, Intel and the who’s who of semiconductor chips.

If stocks reacted on a 30-year timeframe, Nvidia would be up 15% today instead of reaching a trading day nadir of 17%.

What is happening behind the scenes?

American tech companies are moving supply chains or planning to move supply chains out of China.

This is an epochal manifestation of the larger trade war and a decisive development in the eyes of the American administration.

In fact, many industry analysts understand a logjam of failed trade solutions as a bonus to the Chinese.

However, I would argue the complete opposite.

Yes, the Chinese are waiting out the current administration to deal with a new one that might be more lenient.

But that will take another two years and publicly listed companies grappling with the performance of quarterly earnings don’t have two years like the Chinese communist party.

And who knows, the next administration might even seize the baton from the current administration and clamp down even more.

Be careful what you wish for.

Taiwanese company and biggest iPhone assembler Foxconn Technology Group is discussing plans to move production away from China to India.

India is a democratic country, the biggest democracy in Asia, and is a staunch ally of the United States.

CEOs of Google (GOOGL) and Microsoft (MSFT), some of Silicon Valley heavyweights, are from India and American tech companies have been making generational tech investments in India recently.

Warren Buffet even invested $300 million in an Indian FinTech company Paytm.

When you read stories about India being the new China, well it’s happening faster than anyone thought and on a scale that nobody thought, and the underlying catalyst is the overarching trade war fueling this quick migration.

Apple is already constructing low grade iPhones in India in the state of Karnataka since 2017, and these were the first iPhones made in India.

They won’t be the last either.

Wistron, major Taiwanese original design manufacturer, has since started producing the iPhone 6S model there as well.

And it is no surprise that China and its artificially priced smartphones have undercut Samsung and Apple in India grabbing the market share lead.

This is happening all over the emerging world.

And don’t forget if U.S. President Donald Trump revisits banning American chip companies supply channels to Chinese telecom company ZTE. That would be 70,000 Chinese jobs out the window in a nanosecond.

The current administration has drier powder than you think and this would hasten the deceleration of the Chinese economy and also move forward the American recession into 2019 boding negative for tech shares.

Therefore, I would recommend balancing out a trading portfolio with overweights and underweights because it is obvious that tech stocks won’t be coupled to a gondola trajectory to the peak of the summit this year.

It’s a stockpickers market this year with visible losers and winners.

And if China does get their way in the tech war, American chip companies will eventually become worthless squeezed out by mainland competition brought down by their own technology full circle.

They are first on the chopping board because their overreliance on Chinese revenue streams for the bulk of sales.

Among these companies that could go bust are Broadcom (AVGO), Qualcomm (QCOM), Qorvo (QRVO), Skyworks Solutions (SWKS) and as you expected Micron and Nvidia who are one of the main protagonists in this story.

Global Market Comments

January 28, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or IT’S FINALLY OVER)

(SPY), (TLT), (FXE), (MSFT), (AAPL),

(PG), (F), (LRCX), (AMD), (XLNX)

Last week, I was too busy to cook dinner for my brood, so I ordered a pizza delivery. When an older man showed up with our dinner, I told the kids to tip him double. After all, he might be an unpaid federal air traffic controller.

It is a good thing I work late on Friday afternoon because that's when the government shutdown ended after 35 days. The bad news? The government stops getting paid again in only 18 more days. If you have to travel, you better do it quick as the open window may be short.

The most valuable thing we learned from all of this is that the weak point in America is the airline transportation system which relies on 4,000 flights to get the country’s business done.

Having once owned a European air charter company, I could have told you as much was coming. Every nut, bolt, and screw that goes into a US registered aircraft has to be inspected by the federal government. They are painted yellow when viewed which is called “yellow tagging”. No inspection, no screw. No screw, no airplane. No airplane, no flight. No flight, no economy. I can’t tell you how many times I have seen a $30 million aircraft grounded by a failed 50-cent part.

And here’s what most investors don’t get. We lost 75 basis points in GDP growth from the shutdown. We may lose another 75 basis points restarting. And if you lose 1.50% from a post-Christmas period that is normally weak anyway, Q1 GDP may well come in negative. Hello recession!

We won’t know for sure until the first advanced estimate of Q1 GDP from the US Department of Commerce’s Bureau of Economic Analysis is published on April 26. That’s when the sushi will hit the fan. That, by the way, is perilously close for the May 10 prediction of the end of the entire ten-year bull market.

How did investors fare during the shutdown? We clocked the best January in 32 years with the Dow Average up 7.55%. Maybe the government should stay closed all the time!

It is not like the government shutdown, the fading Chinese trade talks, and the arrest of the president’s pal were the only things happening last week.

A slowing China is freaking out investors everywhere. Even if a trade deal is cut tomorrow, it may not be enough to pull the economy out of a downward death spiral. Look out below! A 6.6% growth rate for 2018 is the slowest in 30 years.

Existing Home Sales were down a disastrous 6.4%, in December and 10% YOY, the worst read since 2012. The government shutdown is made closings nearly impossible.

The EC’s Mario Draghi said there would be no euro rate rises until 2020 and the US bond market took off like a rocket. Another point or two and we’ll be in short selling territory again. Don’t count on Europe to pull us out of the next recession. Whoever came up with the idea of putting an Italian in charge of Europe’s finances anyway? Like that was such a great idea.

Procter & Gamble (PG) beat with an upside earnings surprise. It must be all those people buying soap to wash their hands of our political system. But Ford (F) disappointed, dragged down by weak foreign earnings. The weakest big car company to get into electric cars is really starting to suffer. The last of the buggy whip makers is taking a swan dive

The semis have bottomed in the wake of spectacular earnings reports from (LRCX), (AMD), and (XLNX). The great artificial intelligence play is back in action after a severe spanking. I never had any doubt they would come back. Now for an entry point.

Farmers are leaving crops to rot in the field as the trade war with China destroys prices and the Mexicans needed to harvest them are trapped at the border. There’s got to be an easier way to earn a living. Avoid the ags and all ag plays. Short tofu stocks!

Investors are now sitting on pins and needles wondering if we get a repeat of the horrific February of 2018, or whether so far great earnings reports will drive us to higher highs. Earnings tail off right when the next government shutdown is supposed to start so our lives will be interesting, to say the least.

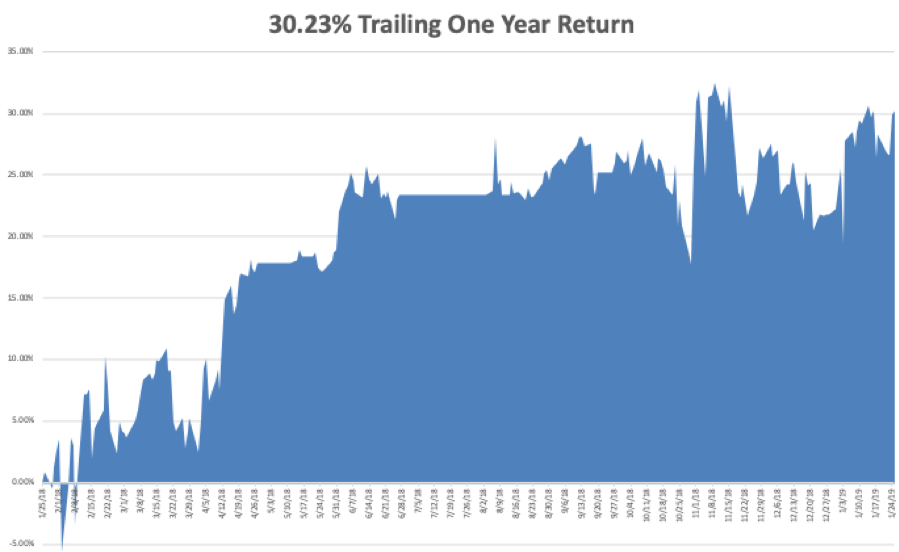

My January and 2019 year to date return soared to +7.24%, boosting my trailing one-year return back up to +30.23%.

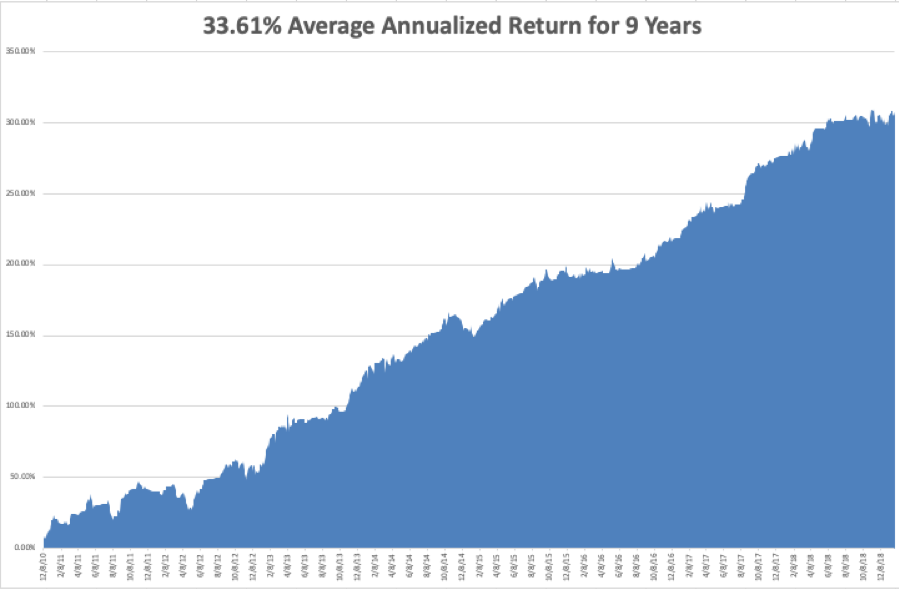

My nine-year return climbed up to +308.14%, a mere 1.72% short of a new all time high. The average annualized return revived to +33.61%.

I have been dancing in between the raindrops using rallies to take profits on longs and big dips to cover shorts.

I started out the week using the 4 1/2 point plunge in the bond market (TLT) to cover the last of my shorts there, bring in a whopper of a $1,680 profit in only 13 trading days. To quote the Terminator (whose girlfriend I once dated, the Terminatrix), I’ll be back.”

I used the big 500-point swoon in the Dow on Monday to come out of my (SPY) short at cost. An unfortunate comment on interest rates by the European Central Bank forced me to stop out of my long in the Euro (FXE), also at cost.

That has whittled my portfolio down to only two positions, a long in Microsoft (MSFT) and a short in Apple (AAPL). As a pairs trade you could probably run this position for years. I am now 80% in cash.

The goal is to go 100% into cash into the February option expiration in 14 trading days, wait for a big breakout, and then fade it. Essentially, I am waiting for the market to tell me what to do. That will enable me to bank double-digit profits for the start of 2019, the best in a decade.

The upcoming week is very iffy on the data front because of the government shutdown. Some government data may be delayed and other completely missing. Private sources will continue reporting on schedule. All of the data will be completely skewed for at least the next three months. You can count on the shutdown to dominate all media until it is over.

Jobs data will be the big events over the coming five days along with some important housing numbers. We also have several heavies reporting earnings.

On Monday, January 28 at 8:30 AM EST, we get the Chicago Fed National Activity Index.

On Tuesday, January 29, 9:00 AM EST, the Case Shiller National Home Price Index for November is released. The ever important Apple (AAPL) earnings are out after the close, along with Juniper Networks (JNPR).

On Wednesday, January 30 at 8:15 AM EST, the ADP Private Employment Report is announced. Pending Home Sales for December follows. Boeing Aircraft (BA) and Facebook (FB), and PayPal (PYPL) announce.

Thursday, January 31 at 8:30 AM EST, we get Weekly Jobless Claims. We also get the all-important Consumer Spending Index for December. Amazon (AMZN) and General Electric (GE) announce.

On Friday, February 1 at 8:30 AM EST, the January NonFarm Payroll Report hits the tape.

The Baker-Hughes Rig Count follows at 1:00 PM. Schlumberger (SLB) announces earnings. Home Sales is released. AbbVie Inc (ABBV) and DR Horton (DHI) report.

As for me, I will be celebrating my birthday. Believe me, lighting 67 candles creates a real bonfire. I received the best birthday card ever from my daughter which I have copied below

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

January 24, 2019

Fiat Lux

Featured Trade:

(FROM THE FRONT LINES OF THE TRADE WAR),

(AAPL), (AVGO), (QCOM), (TLT),

(HOW THE MAD HEDGE MARKET TIMING ALGORITHM TRIPLED MY PERFORMANCE),