“Staving off death is a thing that you have to work at…If living things don’t actively work to prevent it, they would eventually merge with their surroundings and cease to exist as autonomous beings. That is what happens when they die.”

This is a quote from Richard Dawkins, which Jeff Bezos wrote to Amazon (AMZN) shareholders in his farewell letter. Needless to say, death and decay seem to be at the forefront of his mind these days.

That’s why it comes as no surprise that the founder of Blue Origin and, of course, Amazon (as well as Elon Musk’s favorite punching bag) has launched a company comprising renowned scientists and globally respected executives to realize his dream of developing immortality technology.

The company, called Altos Labs, is basically an anti-aging venture. While many people would probably mock the idea, this seemingly impossible wild concept has notable names backing it.

Bezos is not the only investor putting his money on this project.

Russian billionaire Yuri Milner, whose wealth expanded thanks to his strategic funding of Facebook (FB), along with Russian email service Mail.ru (MLRYY) and Russian social networking site VK, is also part of the mission.

In fact, the company was officially conceived in Yuri’s house in Palo Alto in the Los Altos hills, leading to the name Altos Labs. (Given that “Los Altos” means “the heights” in Spanish, they probably used it as a double entendre for Altos Labs’ goals.)

In addition to Yuri and Bezos, there are several other backers of Altos Labs.

While they aren’t specifically named, the mere fact that the startup has generated the most funding of virtually any biotechnology business at $3 billion is quite telling of how much faith investors have on this project.

And they wouldn’t be wrong.

Its remarkable roster of executives includes experts from GlaxoSmithKline (GSK), Roche’s (RHHBY) Genentech, and the National Cancer Institute.

Altos Labs not only has wealthy backers and esteemed executives on its board, it also has Nobel Prize-winning scientists working on its goals.

The highest-profile scientist they have is Shinya Yamanaka, who received the Nobel Prize in 2012 for his stem cell research.

His work, which focuses on cell “reprogramming,” can reverse the development of cells towards that of stem cells. In a nutshell, Yamanaka is working on a “backward aging” technology.

Part of the board is Juan Carlos Izpisúa Belmonte, who specializes in developing techniques to switch cells from one type to another.

He gained notoriety when he experimented on creating hybridized human and monkey embryos using Yamanaka’s technology.

Another member of Altos’ board is Jennifer Doudna, who shared the 2015 Breakthrough Prize with Yamanaka and later won the 2020 Nobel Prize for her co-discovery of CRISPR genome editing.

Although it’s a startup, the company will have offices in the San Francisco Bay Area, San Diego, Cambridge in the UK, and even Japan.

Admittedly, most of the details about the project are still under wraps. But insiders say that Bezos and his crew seek to become the “Bell Labs” of biology.

The oversimplified explanation of its goal is that Altos Labs plans to reverse diseases, effectively regenerating new cells to help the body perform optimally.

Basically, they seek to come up with a biological reprogramming technology that can rejuvenate the cells and eventually revitalize human beings.

They target cells under pressure, including those with genetic abnormalities, suffering from injuries, or aging.

Using their reprogramming technology, they aim to create medications that can deliver one-time treatments for these conditions. Ultimately, these efforts will lead to a prolonged human life.

Further clarifying their mission, Altos explained that their goal is to extend “health span” and that boosting any longevity initiative would simply be considered an “accidental consequence.”

Inasmuch as Alto Labs is an exciting venture, it isn’t the first in the field. This startup joins the ranks of Calico Labs, which was launched in 2013 and funded by one of Google’s (GOOGL) co-founders, Larry Page.

Other startups working on reprogramming technology are Life Biosciences, Turn Biotechnologies, AgeX Therapeutics, and Shift Bioscience.

The quest to defeat death is a mission as old as time.

In response to this challenge, Alto Labs has put together an impressively pedigreed bunch.

Moreover, a solid and established connection is seen between aging clocks and reprogramming technology—all of which Alto Labs already have access to due to its roster of executives and scientists.

While the technology feels so farfetched, industry experts believe it holds indisputable and repeatable results.

These were already seen in laboratory experiments. However, these have only succeeded so far when applied to individual cells.

The technology can gather a cell from an 80-year-old and, via in vitro, reverse this age by as much as 40 years.

If this succeeds, Altos is poised to lead and dominate the “immortality” industry — a sector projected to be worth $600 billion by 2025 — soon.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-03-03 16:00:172022-03-07 21:39:05Cheating Death: Are We Getting Closer to Immortality?

I believe there is a good chance that this creation of Jeff Bezos will see its shares double over the next five years.

Amazon, is in effect, taking over the world.

Jeff Bezos, born Jeff Jorgensen, is the son of an itinerant alcoholic circus clown and a low-level secretary in Albuquerque, New Mexico. When he was three, his father abandoned the family. His mother remarried a Cuban refugee, Miguel Bezos, who eventually became a chemical engineer for Exxon.

I have known Jeff Bezos for so long he had hair when we first met in the 1980s. He was a quantitative researcher in the bond department at Morgan Stanley, and I was the head of international trading.

Bezos was then recruited by the cutting-edge quantitative hedge fund, D.E. Shaw, which was making fortunes at the time, but nobody knew how. When I heard in 1994 that he left his certain success there to start an online bookstore, I thought he’d suffered a nervous breakdown, common in our industry.

Bezos incorporated his company in Washington state later that year, initially calling it “Cadabra” and then “Relentess.com.” He finally chose “Amazon” as the first interesting word that appeared in the dictionary, suggesting a river of endless supply. When I learned that Bezos would call his start-up “Amazon,” I thought he’d gone completely nuts.

Bezos funded his start-up with a $300,000 investment from his parents who he promised stood a 75% chance of losing their entire investment. But then his parents had already spent a lifetime running Bezos through a series of programs for gifted children, so they had the necessary confidence.

It was a classic garage start-up with three employees based in scenic Bellevue, Washington. The hours were long with all of the initial effort going into programming the initial site. To save money, Bezos bought second-hand pine doors which he placed on sawhorses, which stood in for proper desks.

Bezos initially considered 20 different industries to disrupt, including CDs and computer software. He quickly concluded that books were the ripest for disruption, as they were cheap, globally traded, and offered millions of titles.

When Amazon.com was finally launched in 1995, the day was spent fixing software bugs on the site, and the night wrapping and shipping the 50 or so orders a day. Growth was hyperbolic from the get-go, with sales reaching $20,000 a week by the end of the second month.

An early problem was obtaining supplies of books when wholesalers refused to offer him credit or deliver books on time. Eventually, he would ask suppliers to keep a copy of every book in existence at their own expense, which could ship within 24 hours.

Venture capital rounds followed, eventually raising $200 million. Early participants all became billionaires, gaining returns of 10,000-fold or more, including his trusting parents. There is one guy out there who missed becoming a billionaire because he didn’t check his voicemail often enough, which invited him into the initial funding round.

Bezos put the money to work, launching into a hiring binge of epic proportions. “Send us your freaks,” Bezos told the recruiting agencies, looking for the tattooed and the heavily pierced who were willing to work in shipping late at night for low wages. Keeping costs rock bottom was always an essential part of the Amazon formula.

Bezos used his new capital to raid Walmart (WMT) for its senior distribution staff, for which it was later sued.

Amazon rode on the coattails of the Dotcom Boom to go public on NASDAQ on May 15, 1997 at $18 a share. The shares quickly rocketed to an astonishing $105, and in 1999 Jeff Bezos became Time Magazine’s “Man of the Year.”

Unfortunately, the company committed many of the mistakes common to inexperienced managements with too much cash on their hands. It blew $200 million on acquisitions that, for the most part, failed. Those include such losers as Pets.com and Drugstore.com. But Bezos’s philosophy has always been to try everything and fail them quickly, thus enabling Amazon to evolve 100 times faster than any other.

Amazon went into the Dotcom crash with tons of money on its hands, thus enabling it to survive the long funding drought that followed. Thousands of other competitors failed. Amazon shares plunged to $5.

But the company kept on making money. Sales soared by 50% a month, eventually topping $1 billion by 2001. The media noticed Wall Street took note. The company moved from the garage to a warehouse to a decrepit office building in downtown Seattle.

Amazon moved beyond books to compact disc sales in 1999. Electronics and toys followed. At its New York toy announcement, Bezos realized that the company actually had no toys on hand. So, he ordered an employee to max out his credit card cleaning out the local Hammacher Schlemmer just to obtain some convincing props.

A pattern emerged. As Bezos entered a new industry, he originally offered to run the online commerce for the leading firm. This happened with Circuit City, Borders, and Toys “R” Us. The firms then offered to take over Amazon, but Bezos wasn’t selling.

In the end, Amazon came to dominate every field it entered. Please note that all three of the abovementioned firms no longer exist, thanks to extreme price competition from Amazon.

Amazon had a great subsidy in the early years as it did not charge state sales tax. As of 2011, it only charged sales tax in five states. That game is now over, with Amazon now collecting sales taxes in all 45 states that have them.

Amazon Web Services originally started out to manage the firm’s own website. It has since grown into a major profit center. Full disclosure: Mad Hedge Fund Trader is a customer.

Amazon entered the hardware business with the launch of its e-reader Kindle in 2007. The Amazon Echo smart speaker followed in. This is despite news stories that it records family conversations and randomly laughs.

Amazon Studios started in 2010, run by a former Disney executive, pumping out a series of high-grade film productions. In 2017, it became the first streaming studio to win an Oscar with Manchester by the Sea with Jeff Bezos visibly in the audience at the Hollywood awards ceremony.

Its acquisitions policy also became much more astute, picking up audio book company Audible.com, shoe seller Zappos, Whole Foods, and most recently PillPack. Since its inception, Amazon has purchased more than 86 outside companies. Make that 89 with MGM Entertainment.

Sometimes, Amazon’s acquisition tactics are so predatory they would make John D. Rockefeller blush. It decided to get into the discount diaper business in 2010, and offered to buy Diapers.com, which was doing business under the name of “Quidsi.” The company refused, so Amazon began offering its own diapers for sale 30% cheaper for a loss. Diapers.com was driven to the wall and caved, selling out for $545 million. Diaper prices then popped back up to their original level.

Welcome to online commerce.

At the end of 2021, Amazon boasted some one million employees worldwide. In fact, it has been the largest single job creator in the United States for the past decade. Also, this year, it disclosed the number of Amazon Prime members at 100 million, then raised the price from $120 to $139 a year, thus creating an instant $2 billion in profit.

The company’s ability to instantly create profit like this is breathtaking. And this will make you cry.

So, what’s on the menu for Amazon? There is a lot of new ground to pioneer.

1) Health Care is the big one, accounting for $3 trillion, or 17% of U.S. GDP, but where Amazon has just scratched the surface. Its recent $1 billion purchase of PillPack signals a new focus on the area. Who knows? The hyper-competition Bezos always brings to a new market would solve the American health care crisis, which is largely cost-driven. Bezos can oust middlemen like no one else.

2) Food is the great untouched market for online commerce, which accounts for 20% of total U.S. retail spending, but sees only 2% take place online. Essentially, this is a distribution problem, and you have to accomplish this within the prevailing subterranean 1% profit margins in the industry. Books don’t need to be frozen or shipped fresh. Walmart (WMT) will be target No. 1, which currently gets 56% of its sales from groceries. Amazon took a leap up the learnings curve with its $13.7 billion purchase of Whole Foods (WFC) in 2017. What will follow will be interesting.

3) Banking is another ripe area for “Amazonification,” where excessive fees are rampant. It would be easy for the company to accelerate the process through buying a major bank that already had licenses in all 50 states. Amazon is already working the credit card angle.

4) Overnight Delivery is a natural, as Amazon is already the largest shipper in the U.S., sending out more than 1 million packages a day. The company has a nascent effort here, already acquiring several aircraft to cover its most heavily trafficked routes. Expect FedEx (FDX), UPS (UPS), DHL, and the United States Post Office to get severely disrupted.

5) Clothing-Amazon has already surpassed Walmart this year as the largest clothing retailer. The company has already launched 76 private labels, with half of them in the fashion area, such as Clifton Heritage (color and printed shirts), Buttoned Down (100% cotton shirts), and Goodthreads (casual shirts) as well as subscription services for all of the above.

6) Furniture is currently the fastest growing category at Amazon. Customers can use an Amazon tool to design virtual rooms to see where new items and colors will fit best.

7) Event Ticketing firms like StubHub and Ticketmaster are among the most despised companies in the U.S., so they are great disruption candidates. Amazon has already started in the U.K., and a takeover of one of the above would ease its entry into the U.S.

If only SOME of these new business ventures succeed, they have the potential to DOUBLE Amazon’s shares from current levels, taking its market capitalization up to $3.2 trillion. Perhaps this explains why institutional investors continue to pour into the shares.

Whatever happened to Bezos’s real father, Ted Jorgensen?

He was discovered by an enterprising journalist in 2012 running a bicycle shop in Glendale, Arizona. He had long ago sobered up and remarried. He had no idea who Jeff Bezos was. Ted Jorgensen died in 2015.

Bezos never took the time to meet him. Too busy running Amazon, I guess. Worth over $300 billion, Bezos is now the second richest man in the world after Elon Musk.

Second Richest Man in the World

https://www.madhedgefundtrader.com/wp-content/uploads/2022/02/2nd-richest.png316560Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-02-25 09:02:362022-02-25 12:07:39Why Amazon is Beating All

Yes, these are two sovereign currencies, the lira and the hryvnia, that have absolutely lost any credibility whatsoever.

We forget that there are many of these banana republics out there that might as well adopt some sort of alternative currency.

El Salvador anointed Bitcoin their national currency and now that isn’t as bizarre as it first seemed.

Americans sometimes forget that the pandemic ripped through emerging nations like a hot knife through butter and there were no stimuli or handouts, let alone handouts for corporations, and there has never been a longer queue for U.S. green cards.

Well, Russia is on Ukraine’s doorstep and the threat of it crowding the Ukraine border means that no foreign capital or investment will penetrate Ukraine for the foreseeable future.

Every Ukrainian under 40 years old is now making a mad dash for higher ground to the European Union or if they can, the United States, United Kingdom, or Canada.

The Ukrainian hryvnia has lost 10% of its value in a few days and this could be a beginning of a much bigger collapse in purchasing power for Ukrainians who don’t leave.

It could trigger a vicious cycle all the way to zero where like a hot potato, Ukrainian citizens try to rid themselves of local currency as fast as possible.

Like I said, there are others out there, pretty much every ex-Soviet republic not in the European Union of the likes of Georgia, Kazakhstan, Moldova, Azerbaijan, and Armenia of the South Caucasus.

When you add up the population of the likes of Uzbekistan and such, then that totals roughly 130 million people.

These 130 million people, like El Salvadoreans, would be foolish not to adopt Bitcoin if they can’t secure US dollars.

For people who haven’t traveled to these esoteric places, US dollars are in high demand and hard to find and families hold on to them for dear life.

So if the choices are Bitcoin or worthless paper, then between those two, the decision is rather straightforward.

Ukrainians are slowly coming to the realization that these are their options.

Don’t think that any one of these similar countries is immune to political strife or war either.

Georgia has already given up a sliver of their country to Russia already.

And in an incredible set of events, the Government of Ukraine has passed a law that legalizes Bitcoin and other cryptocurrencies.

The law grants legal status to virtual assets. The law not only grants users the right to operate cryptocurrencies but also defines the clear rights and duties of all market participants.

The Ukraine’s government also approved the law on cloud services as a whole. The bill’s goal is to create conditions for the processing and protection of data when using cloud computing technology, as well as providing cloud services and determining the specifics of public authorities’ use of cloud services, as well as more efficient use of public resources through the introduction of new technologies.

The new law will expedite the entry in Ukraine of the world’s top cloud service providers – Microsoft (MSFT), Amazon Web Services (AMZN), and Google (GOOGL) Cloud – and encourage the construction of data centers.

The Ministry of Digital Development has previously said that it planned to expand the market for “virtual assets.”

Virtual assets are divided into two categories in the draught law: secured and unsecured virtual assets.

A secured VA is an asset that verifies property or non-property rights, such as the right of claim on other objects like stable coins, and is secured by fiat currency, securities, or any sort of offline asset.

All other sorts of cryptocurrencies and crypto-based assets, such as non-stable coins like Bitcoin, non-fungible tokens, and so on, are classified as unsecured VAs.

Therefore, it’s not surprising to find out in the latest data that adoption into Bitcoin and other crypto in Ukraine has skyrocketed.

Non-profit donors looking for donations are also being paid via Bitcoin.

The rapid legislation of course would not have occurred if not for the Russian situation, but either way, adoption is adoption and add another 50 million or so Ukrainians to Bitcoin’s growth story.

Eventually, Africa and South America will join the adoption phase as they also preside over rapidly depreciating fiat currency.

I’m shocked that Argentina hasn’t ventured this way yet, put them down for the next country in the crypto queue.

Even if Bitcoin is suffering a bout of weakness due to exogenous shocks, the long-term price trajectory is well above $100,000.

https://www.madhedgefundtrader.com/wp-content/uploads/2022/02/bitcoin-feb1722.png434994Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-02-17 16:02:432022-02-17 18:06:19Another 130 Million People Jump on the Crypto Wagon

Happy and newly enriched followers of the Mad Hedge Fund Trader Alert Service have the good fortune to own a record ten deep in-the-money options positions that expire on Friday, February 18 at the stock market close in three days.

I have to admit that I traded like a Wildman this month, pedal to the metal, and 100% invested. This will take our 2022 year-to-date performance to over 24%. I like to think that is the end result of my 53 years investment in researching trading strategies.

Sometimes overconfidence works.

It is therefore time to explain to the newbies how to best maximize their profits.

These involve the:

Risk On

World is Getting Better

(TLT) 2/$149-$152 put spread 10.00% (TLT) 2/$147-$150 put spread 10.00% (TLT) 3/$150-$153 put spread 10.00% (BRKB) 2/$270-$280 call spread 10.00% (TSLA) 2/$600-$650 call spread 10.00%

Risk Off

World is Getting Worse

(MSFT) 2/$340-$350 put spread -10.00% (SPY) 2/$465-$475 put spread -10.00% (SPY) 3/$470-$480 put spread -10.00% (AMZN) 2/$3400-$3500 put spread -10.00% (TLT) 3/$127-$130 call spread -10.00%

Total Net Position 0.00%

Total Aggregate Position 100.00%

Provided that we don’t have another 2,000-point move down in the market in the next three days, these positions should expire at their maximum profit points.

So far, so good.

I’ll do the math for you on our deepest in-the-money position, the Tesla (TSLA) February 18 $600-$650 vertical bull call spread, which 50% in the money from its lower strike price which I almost certainly will run into expiration. Your profit can be calculated as follows:

Profit: $50.00 expiration value - $43.00 cost = $7.00 net profit

(2 contacts X 100 contracts per option X $7.00 profit per option)

= $1,400 or 16.28% in 15 trading days.

Many of you have already emailed me asking what to do with these winning positions.

The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck, and pat yourself on the back for a job well done.

You don’t have to do anything.

Your broker (are they still called that?) will automatically use your long position to cover your short position, canceling out the total holdings.

The entire profit will be credited to your account on Monday morning February 21 and the margin freed up.

Some firms charge you a modest $10 or $15 fee for performing this service.

If you don’t see the cash show up in your account on Monday, get on the blower immediately and make your broker find it.

Although the expiration process is now supposed to be fully automated, occasionally machines do make mistakes. Better to sort out any confusion before losses ensue.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. You can probably unload them pennies below their maximum expiration value.

Keep in mind that the liquidity in the options market understandably disappears, and the spreads substantially widen, when a security has only hours, or minutes until expiration on Friday, February 18. So, if you plan to exit, do so well before the final expiration at the Friday market close.

This is known in the trade as the “expiration risk.”

One way or the other, I’m sure you’ll do OK, as long as I am looking over your shoulder, as I will be, always. Think of me as your trading guardian angel.

I am going to hang back and wait for good entry points before jumping back in. It’s all about keeping that “Buy low, sell high” thing going.

I’m looking to cherry-pick my new positions going into the next month-end.

Take your winnings and go out and buy yourself a well-earned dinner. Just make sure it’s take-out. I want you to stick around.

Well done, and on to the next trade.

You Can’t Do Enough Research

https://www.madhedgefundtrader.com/wp-content/uploads/2019/09/john-and-girls.png322345Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-02-15 09:02:012022-02-15 15:58:03How to Handle the Friday February 18 Options Expiration

The market finally found something worse than inflation to rattle it: WWIII.

I’m not expecting my call-up papers from the Marine Corps anytime soon. After all, there isn’t a war that is about to happen. In any case, if the defense of the nation relies upon me as a pilot, we are in big trouble.

The market clearly thought otherwise last week, when the Dow swooned 1,200 points in two days. The Friday close was a dog’s breakfast.

It gets worse.

The collapse sets up a perfect “head and shoulders” top which the hedge fund community has been gunning for all year. That beckons eventual lows that will finally bring us into decent LEAPS territory, especially if the Volatility Index (VIX) leaps over $40.

Biden actually has a pretty good strategy going in the Ukraine. By announcing the time and date of the Russian invasion in advance, he boxes Putin into a corner, forcing him to put up or shut up.

It's really all one big chess game, with the two countries attempting to each gain maximum security advantages at minimum cost. Putin would love the Ukraine if he could get it. So did Hitler, Napoleon, and Genghis Khan before him.

Biden hopes to make the price so high it’s not worth it. After all, Hitler, Napoleon, and Genghis Khan didn’t come to good endings.

It’s really meaningless to fight this battle when modern national borders are rapidly dissolving anyway. Modern borders are increasingly being drawn by operating systems, apps, and security suites rather than lines on a map.

Of course, bonds were discounting a completely different scenario, that of peace, prosperity, and booming economies that demand more capital at higher interest rates. Fed members are now playing a game of competitive hawkishness, talking interest rates up and bond prices down.

It all sounds like a great short bond environment to me, which is why I have been running a triple short position since the beginning of the year. The best is yet to come.

So we flipped from being long everything in 2021 to short the works in 2022. That’s just the way markets work now. So, if you can’t stand the heat, get out of the kitchen.

Fed Now Pushing a Half-Point Hike, tanking the markets, and could deliver 100 basis points by July. Competitive hawkishness has broken out at the Fed. Looks like a bond short will be the trade of the year. Who knew? (You did).

Core CPI Comes in Hot at 7.5%, the highest since 1982, and hotter than expected. The news finally took bond prices to new multi-year lows and ten-year yields to 2.0%. One-third of this number is rent, which is rising at a record rate. Wages are up an eye-popping 5% YOY. Used car prices were up massively. Stocks took it on the news. It’s going to get worse before it gets better. The chances of a 50-basis point hike in March.

Real Yields Turn Positive, for the first time in a decade, at least for 30-year US treasury bonds. That is the real inflation-adjusted yield for TIPS, or Treasury Inflation-Protected Securities, which now yield 0.08%. Expect real yields to soar from here. Yes, positive returns for bonds at last!

JGB Yields Approach Five Year High, at 0.25%, so will the Bank of Japan be forced to raise rates for the first time in 21 years to come in line with the market. Quantitative Easing is also ending. Gee, do you think zero rates have worked? It's all part of an accelerating trend for more expensive global money.

Pfizer Hauls in $32 Billion From Covid, and another $22 billion for its antiviral Paxlovid. Still, the stock market is a “What have you done for me lately,” and the shares are off 20% since December.

NVIDIA Cancels ARM Purchase, ending its $66 billion attempt to buy market share. UK regulatory opposition was the issue. Buy (NVDA) on dips. The best-run company in the market has just suffered a 40% selloff.

GM to Ramp Up EV Production Sixfold This Year. Electric Escalade SUVs and trucks are the top priority. But while saying is one thing, doing is another. No mention has been made of how they will obtain the extra chips and batteries. Avoid (GM) a never-ending font of disappointment.

Weekly Jobless Claims Prints at 223,000, well above the post-pandemic low of 188,000 in December. Continuing Claims post at 1,621,000.

Foreclosures are Soaring now that the pandemic relief is over. They were up 29% in January, double YOY levels. Florida leads in this troubled category. The numbers would be higher save for enormous rises in home prices which permit cash out refis.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

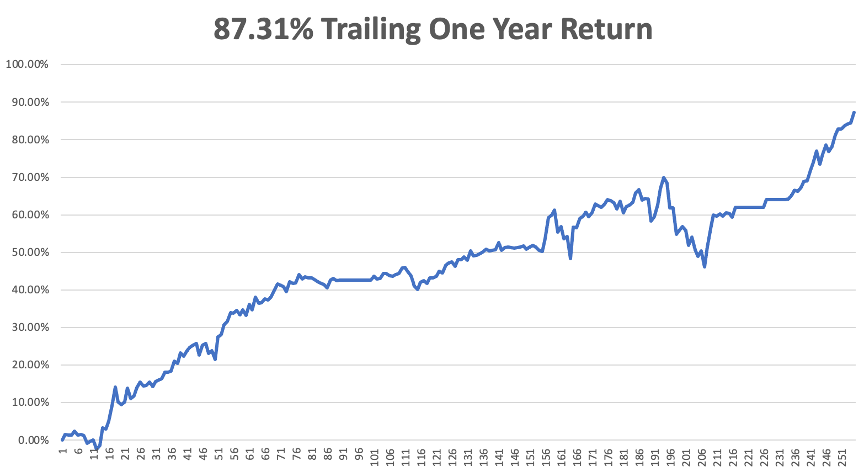

With near record volatility fading fast, my February month to date performance rocketed to a blistering 8.71% in only nine days. My 2022 year-to-date performance has exploded to an unbelievable 23.30%. The Dow Average is down -4.3% so far in 2022. It is the great outperformance on an index since Mad Hedge Fund Trader started 14 years ago.

With 30 trade alerts issued so far in 2022, there was too much going on to describe here. Check your inboxes.

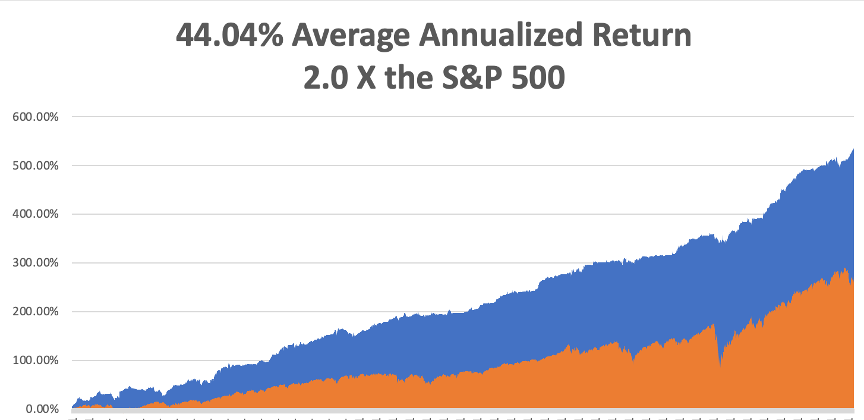

That brings my 13-year total return to 535.86%, some 2.00 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 44.04% for the first time. How long it will keep rising I have no idea, but as long as it is, I’m not complaining. When you’re hot, you have to be maximum aggressive.

We need to keep an eye on the number of US Coronavirus cases at 78 million and rising quickly and deaths topping 919,000, which you can find here.

On Monday, February 14 at 8:00 AM EST, US Consumer Inflation Expectations are out.

On Tuesday, February 15 at 8:30 AM, the New York Empire State Manufacturing Index is printed. On Wednesday, February 16 at 8:30 AM, US Retail Sales for January are announced.

On Thursday, February 17 at 8:30 AM, Weekly Jobless Claims are published. Housing Starts and Building Permits for January are announced. On Friday, February 18 at 7:00 AM, Existing Home Sales for January are disclosed. At 2:00 PM, the Baker Hughes Oil Rig Count are out.

As for me, I made the most unlikely of entries into journalism 50 years ago, thanks to basketball, Mensa, and the kindness of complete strangers.

Struggling as a part-time English teacher in Tokyo for Toyota, Sony, and Meiji Shipping, I noticed one day in the Japan Times an ad for a Mensa meeting, the organization for geniuses.

I joined and, after a few meetings, was invited to give a presentation on the subject of my choice at the next meeting. Since I had just obtained a degree in Biochemistry from UCLA, I spoke on the effects of THC (tetra hydro cannabinol) on the human brain. The meeting was exceptionally well attended by detectives from the Tokyo Police Department, as THC was then highly illegal.

At the end of the meeting, famed Australian journalist Murray Sayle approached me and said he could get me into the Foreign Correspondents Club of Japan. The big attraction was access to the Club’s substantial English language library.

Except for a few well-worn Playboy magazines coming out of the local US Air Force bases, there were almost no English language publications in Japan in those days.

So I joined as a corporate member at 22, the youngest of the 2,000-man club, eating lunch daily with the foreign correspondents on the 20th floor of the Yurakcho Denki Building in central Tokyo. It was just across the street from General Douglas MacArthur’s WWII occupation headquarters.

Many correspondents were holdovers from WWII and had fought their way to Japan on the long island-hopping campaign. Once in Tokyo, they never left, were treated like visiting royalty, paid well, and besieged by beautiful women.

At 6’4” it was only weeks before I was recruited for the club’s basketball team. We played the team from the US Embassy Marine Corps guard, which regularly kicked our butts every week. After all, they had nothing to do all day but play basketball. But they also gave us access to the Tokyo PX where you could get a bottle of Johnny Walker Red for $3.00, versus the local retail price of $100.00.

I managed to eventually get a job at Dai Nana Securities to teach English to the sales staff there. The first oil shock had just taken place and the sole buyers of shares in the world were all in the Middle East.

After two weeks of trying, I met with the president of the company, Mr. Saito, and told him his staff would never learn English. They just lacked the language gene. But if he taught me the stock business, I would sell the shares for him.

He said OK.

Thus, I ensued on a crash course on securities analysis, relying heavily on the firm’s only copies of the 1934 book, Securities Analysis by Benjamin Graham, and his 1949 tome, The Intelligent Investor. I still have a copy of the first research report I wrote on electric tool maker Makita.

It wasn’t long before I became the top salesman at Dai Nana, eventually selling up to 5% holdings in the top 200 Japanese companies to the Saudi Arabia Monetary Authority, the Kuwait Investment Authority, and the Abu Dhabi Investment Authority.

Then the stock market crashed. I lost my job. So, I started asking around the Press Club if anyone had any work. I was broke and nearly homeless.

At the time, most of the correspondents had just returned from covering the Vietnam War. In Japan, they wanted to cover politics, geisha girls, and Emperor Hirohito. Business was at the very bottom of the list. Besides, no one cared what happened in Japan anyway.

It turned out that all the members of the Press Club basketball team were business journalists. There was Mike Tharpe from the Wall Street Journal, Tracy Dalby from the New York Times, and Richard Hanson from the Associated Press, all NCAA college athletes.

Then one team member, The Economist correspondent, Doug Ramsey, asked me if I could write a story about the Japanese steel industry, which was then aggressively dumping product in the US, killing American jobs and creating a political firestorm. Using my stock market contacts, I spent a week diligently researching the subject.

The editors in London loved the story and said they’d take two a week at $75 each. Then the Financial Times heard about me and said they’d also take two a week. All of a sudden, I had a full-time job paying the princely sum of $1,200 a month!

I eventually built up a global syndicate of 40 business publications in ten countries. By 26, I was earning $100,000 a year and published several books. At my peak I accounted for about half of all business news coming out of Japan, along with stringer jobs with the British Broadcasting Corp. in London and NBC in New York.

This was all from a person whose only “C” in college was in English. Officially, I didn’t know how to write back then.

Officially, I still don’t.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/02/foreign-correspondent-ID.png544864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-02-14 10:02:272022-02-14 15:49:04The Market Outlook for the Week Ahead, or Welcome to WWIII

Mad Hedge Technology Letter February 9, 2022 Fiat Lux

Featured Trade:

(THE TELEHEALTH TRADE GETS CROWDED) (TDOC), (AMZN)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-02-09 16:04:042022-02-09 16:31:56February 9, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.