Social unrest will have NO material effect on tech shares moving forward.

Some investors expected the Nasdaq (COMPQ) index to roll over big time, throttled by a national insurrection. Anti-police-violence protests, some becoming riots, have broken out in more than 60 cities.

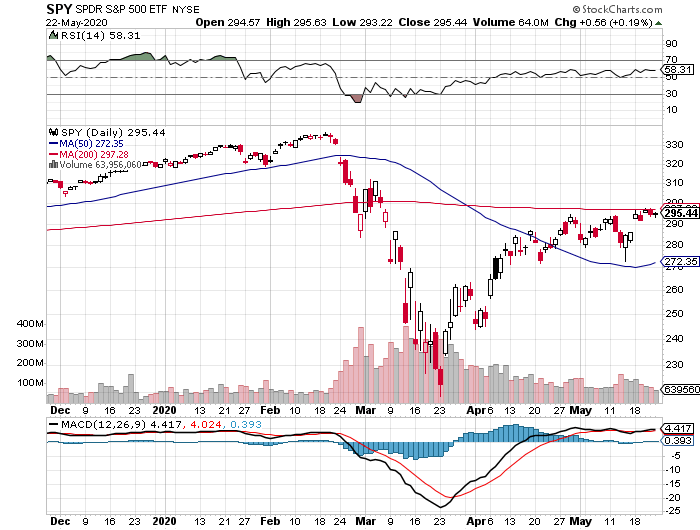

However, it appears to be another false negative for the Nasdaq as it motors upwards acting on the momentum of outperformance during the coronavirus.

One thing that the coronavirus pandemic, as well as protests, have taught investors is the unwavering faith in technology’s strength will continue powering the overall market rebound.

Any social unrest will not stop tech shares because they simply don’t subtract from their revenue models.

This will perpetuate into the rest of 2020 and beyond.

Much of the public reaction from big tech has been paying some form of lip service about the national situation being untenable followed up with a small donation.

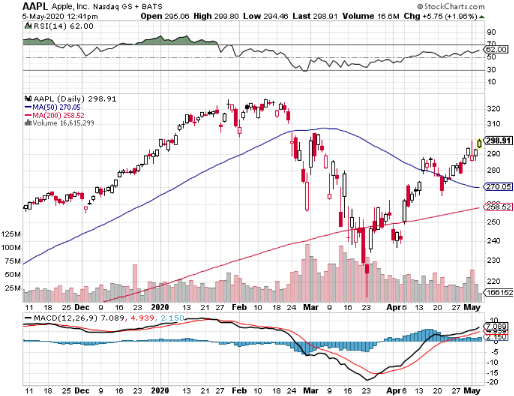

Apple (AAPL) says it's making donations to various groups including the Equal Justice Initiative, a non-profit organization based in Montgomery, Alabama that provides legal representation to marginalized communities.

To read more about big tech’s donations, click here.

Aside from some PR formalities, it will be business as usual after things settle down.

Apple might suffer some slight inconveniences of having some stores looted, but that doesn’t mean consumers can’t buy products online.

Tech companies simply contort to fit the new paradigm and that is what they are best at doing.

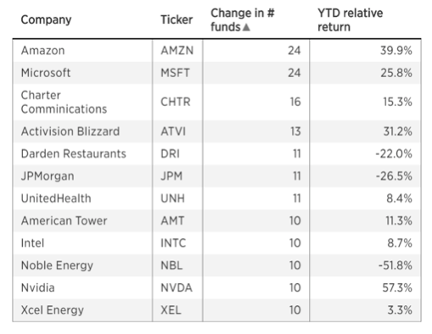

Apple has charged hard into the digital service as a subscription world that has served Amazon, Apple, Google (GOOGL), and Microsoft (MSFT) so well.

To read more about the robust performance of software stocks, please click here.

Many of these tech companies don’t need a physical presence to drive forward earnings, revenue models, and widen their competitive advantages.

That’s the beauty of it and their brands are so entrenched that it doesn’t matter what happens in the outside world at this point.

It’s true that a few tech companies might have to scale back or modify operations until the storm subsides but not at a great scale that will worry investors.

Amazon is reducing deliveries and changing delivery routes in some areas affected by the protests.

Big tech dodged a bullet with the majority of the financial burden falling on the shoulders of big-box retailers like Walmart (WMT) and Target (TGT) and city center-located businesses.

Walmart closed hundreds of stores one hour early on Sunday, but most are slated to reopen. Nordstrom (JWN) temporarily closed all its stores on Sunday.

Amazon (AMZN)-owned Whole Foods are often located in neighborhoods that are perceived likely to escape the bulk of the turmoil.

The events of the last few days will have significant side effects on the normalcy of society or the new normal of it.

Combined with the pandemic, consumers will opt for more spacious housing options in less concentrated areas of the U.S.

The social unrest once again delivers the goodies into the hands of e-commerce as people will be less inclined to leave their house to consume.

A stock that really sticks out during all of this is the leader in interconnected data centers Equinix (EQIX) because of the explosion of data being consumed from the stay-at-home revolution.

Sadly, the price of tech share does not account for life quality which is part of the reason we see stocks lurching higher.

By the time all the different crises, including coronavirus and protests, are snuffed out, we could be in a world where the only strong companies left are technology, "big tech".

They have an insurmountable lead at this point with guns still blazing.

When you add the windfall of trillions in cash the Fed has pumped out and unwittingly diverted into tech shares recently, it is hard to envision ANY scenario in which the Nasdaq will be down a year from now.

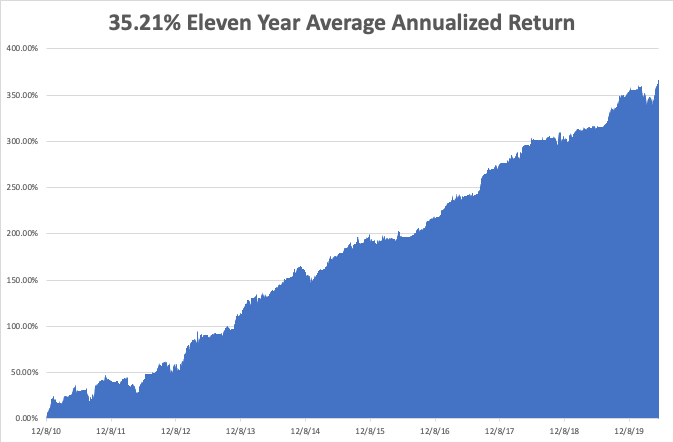

I am bullish on the Nasdaq index and even more bullish on big tech.

Even the supposed “rotation” to value has only meant that tech shares haven’t gone down.

A dip now in tech shares means shares dip for two hours before resurging.

Why would anyone want to sell the best and highest growth industry in the public markets with unlimited revenue-generating potential?