I love doing presentations to small businesses on my free time, partly to stay in touch with the pulse of the Davids who have the unenviable task of fighting uphill against the Goliaths.

It’s bad enough that the tech giants have scaled locally turning one’s local playground into a disadvantage.

The presentation is aptly titled "Content is King... But Only Through One’s Ownership" where the same parallels are explored and unpacked for my audience.

Proprietary Content – must be yours and you must own it on your own turf - your blog, your vlog, your app, and so on, it goes for everything.

Repurposing content on other platforms as a supplement to your own is one thing, but the moment you adopt an enemy platform as your main platform, that’s your coup de grâce.

SMEs (small businesses enterprise) believe it’s plausible to work with the higher ups, but don’t forget they have every incentive to cut you off from the fountain of youth.

One could say the best skill big tech has today is undermining their competition.

Facebook doesn’t allow posting content that criticizes Facebook, have you ever wondered why?

Website innovation has grinded to a halt because of the PageRank algorithm from Google, everybody is making websites the same, a top nav, descriptive text, a smattering of images and a handful of other elements arranged similarly.

Google’s algorithms and the self-regulating nature of their ecosystem have perverted the chance to have a unique online experience.

Most internet users have probably discovered that most websites don’t work well and the execution of them is lousy.

Many companies are not contributing enough resources to build out their site properly, or just don’t have the cash to fund it or a mix of the two.

About 95% of customer service calls originate from the company’s webpage because of payment problems, disfunction, misleading content, or simply because the website is down.

Ask any small business and they will tell you they deal with their domain being down for hours at a time because of some unknown server problem.

Not only is capitalism only working for a small group of Americans, but so are websites, such as massive companies like Amazon.com who have worked wonders with its e-commerce site.

Because the internet and namely websites are the key to building businesses, Silicon Valley is now using the concept of websites and their position as de-facto moderators to prevent others from developing proper websites, killing off the competition.

Alphabet is notorious for ranking their own products at the top of page one of any Google search.

Amazon has followed the same practice by sticking their in-house brands at the top of any Amazon search on Amazon.com.

And remember that none of this can be called “antitrust” because these borderline tactics offer consumers lower prices but that is only because consumers are brainwashed to believe Amazon offers the lowest price.

What if the same products are available for half of Amazon’s in-house brands, would Amazon volunteer to post their in-house brands on the second page, the graveyard of search results?

I would guess no.

Websites used to give businesses a chance, remember in the mid-90s when a website of any ilk was impressive as if someone was walking on water.

What can we expect next?

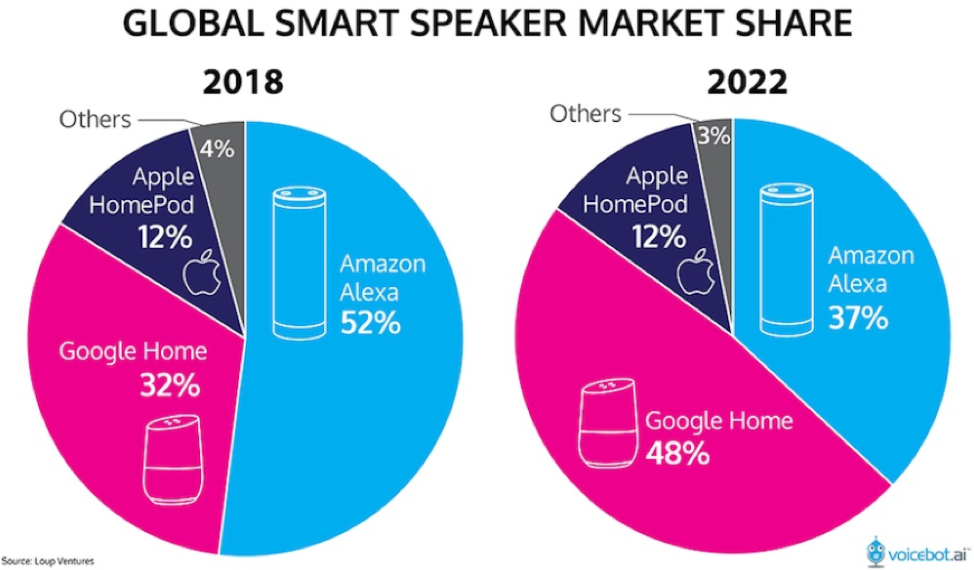

Amazon, Google, and Apple are taking their shows to artificial intelligence voice platforms.

SMEs could at least throw hail marys on standard internet searches with visual screens, but once content migrates over to voice platforms owned by Silicon Valley, then its game, set, and match.

For instance, a local business such as Joe’s Furniture Moving Business who, with the internet and visual screens, is searchable through search engines and can be even located on Google Maps with a concrete address.

Once we migrate the lions share of content to voice platforms over the next 15 years, Google Home, Apple HomePod, or Amazon Alexa could easily choose to remove Joe’s Furniture Moving Business information because they make more money offering you information of a moving service they own or have a stake in.

The advent of 5G will refine the voice technology and enhance the machine learning techniques needed to complete the migration of content.

Once the world crosses an inflection point where the technology and volume of content on smart speakers outweigh the hassle to use a keyboard or mobile screen, this effectively makes these smart speaker manufacture Gods of the World because they will own the voice-based internet.

They will be the gatekeepers of all global information, business, and development in the world and we will need to satisfy their algorithms to get our own content uploaded on their voice platforms.

And because of the nature of voice, users cannot see what else is out there, users will only hear what these companies tell us offering an outsized opportunity to manipulate the user experience generating more dollars for these powerful platforms.

By the end of 2019, 74 million Americans will be using smart speakers, giving these smart speaker firms adequate data to fine tune their products.

Eventually, all Americans will be forced to use it or will not be able to function, similar to the effects of a laptop, email, and smartphone combination now.

Once these voice platforms become ubiquitous, websites will be deemed irrelevant – consumers will simply have a choice of Google Home, Amazon Alexa, and Apple HomePod and blindly trust what they tell you is in your best interests.

Pick your poison.

That’s right, users won’t control content in about 15 years, a scary thought, and now you understand why these companies will even give their voice A.I. platforms for free if they have to and probably will in the future.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/smart-speakers.png483566Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-11 01:06:362019-07-10 21:51:06The Means to a Frightening End

YouTube has to be the online streaming asset of the year even relegating Netflix (NFLX) to the minor leagues – I’ll tell you why.

India is the new China.

Netflix’s growth strategy is intertwined with India and the management has been extraordinarily vocal about their interests there.

The Indian online streaming renaissance isn’t just fueling Netflix’s rise. In fact, YouTube and its free platform are performing miracles along the Ganges River.

How big is YouTube in India?

YouTube already has 245 million monthly active users in India penetrating 85% of the country’s internet population making India one of its best-performing markets.

The company says more than 60% of its streaming hours in India come from outside the six metros, meaning YouTube has captured the hearts and minds of the rural population who cannot afford to pay for online content.

KPMG forecasts India’s online streaming audience to surpass 550 million by 2023 and YouTube will capture 70% of the 550 million audience.

How did YouTube manage to do this?

First, the content is free with ads allowing rural Indians to join in.

Second, local Indians became hooked on Alphabet’s YouTube with Alphabet (GOOGL) taking an already brilliant platform and supercharged it by tailoring it to popular local influencers that are joining in droves inciting a massive network effect.

Effectively, YouTube attracted these influencers with eye-popping audiences to create organic and original content without the $8 billion Netflix planned content budget in 2019.

YouTube was able to do this by borrowing the Instagram format but transferring it to a more effective video platform model.

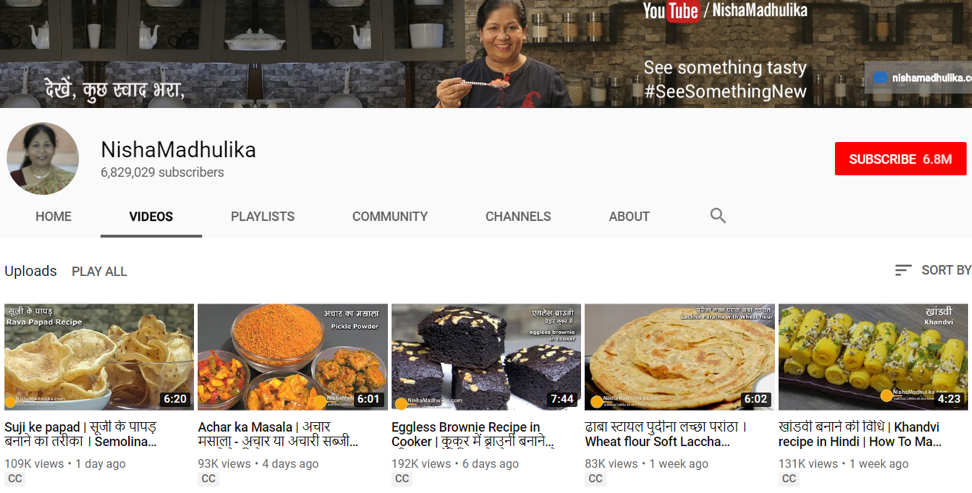

Take for instance Nisha Madhulika whose channel has blossomed into one of the most popular Hindi language-based online cooking channels on the internet.

Her channel has over 6.8 subscribers, yet, accumulating subscribers is one thing, and making money is another.

Past videos that were posted around 2-3 weeks ago have views between 200,000 to 400,000.

These influencers build up revenue by displaying 3rd party ads generated by Alphabet.

A general rule of thumb is that for every 1 million view, ad revenue collected is around $2,000.

Therefore, Nisha and fellow YouTubers with massive audiences are incentivized to pump out high-quality content in high volume.

Scrolling through her numbers, Nisha appears to average around $700 of revenue per video.

She sprinkles in the occasional viral video that garners 1.5 million views which would earn her a tidy $3,000 for a single video.

Not bad and that is before any of the possible marketing opportunities are quantified.

As long as she focuses on the quality of the videos, she can consistently earn $700 per video, then she can do more by partnering with affiliates to sell 3rd party products and receive a commission that is trackable through the links she leaves at the bottom of her videos.

Nisha’s video business works like this, her channel entails producing 3-5 short videos per week producing around 9-11 million views per month adding up to between $18,000-$22,000 in revenue per month.

Remember that while she is accumulating views for newly posted videos, there are still viewers rummaging through her older content demonstrating the beauty of the network effect.

Older videos in Nisha’s case usually add an extra $3,000-$5,000 per month to the bottom line in pure profit.

Many influencers curate, edit, design, and film the content themselves, or subcontract these jobs for a cheap fee.

An influencer could run their YouTube channel for less than $100 per month minus the fees for the equipment.

YouTube has created a powerful platform for content creators to monetize their original content and give them incentives to stick around and build a business.

Netflix has more of a mercenary model where they contract highly paid actors to contribute a finite amount of content for a fee.

YouTube’s model penetrates to the heart of the average person with regular people instead of propping up overpaid Hollywood actors like Netflix.

In many cases, YouTube’s influencers offer live, raw, and personal access, and the data suggests that live, unscripted content are one of the most monetizable types of content on the market due to its original nature and unpredictability.

That is why live sports like the NFL and NBA are easy to sell, monetize, and in great demand.

I do believe that Netflix has a great product but overpaying for Hollywood’s best talent is not sustainable because the cost-benefit ratio isn’t worth it, which is why Netflix is raising customer prices to monetize the quality of streaming content better.

With other big tech players coming into the market, it will push up the costs for Hollywood talent putting more short-term pressure on their financial model.

Even if Netflix does get the right actors to provide content, they do have their fair share of bad movies.

YouTube’s performance in India will be hard to compete with, even harder when they avoid expensive mistakes, a bad video is simply glossed over and ignored.

Netflix is in the midst of testing a mobile-only Indian subscription package for around $3.64 per month, or 250 Indian rupees, to respond to YouTube’s godlike presence there.

Remember that most rural Indians do not have access to hardware such as computers, laptops, or tablets, and run their lives with cheap Chinese smartphones from Oppo and Vivo.

If you thought $3.64 was a cheap streaming package, then Amazon (AMZN) takes it one step further by offering Amazon prime video for $1.88 per month or 129 Indian rupees.

I like Netflix’s product and the narrative is still intact, but I adore and love YouTube’s transformation that has caught many of us by surprise.

This massive shift wouldn’t be possible without Google’s army of best of breed ad tech.

Even more poignant, YouTube takes direct to consumers to a rawer entry point enhancing the special experience.

The problem with Hollywood talent is that reformulating them onto Netflix’s platform brings them closer to the audience to a certain degree, but not like Nisha’s cooking channel where she can speak directly to the viewer and even interact with her audience in the comment section.

YouTube has mastered this relationship between content creator and audience, and no matter how many times I watch Will Smith’s Bright, I can’t expect him to reply to my comments.

Well, there’s not even a comment section on Netflix’s platform.

In short, Netflix’s Indian strategy is incomplete and I predict that YouTube will extend its lead there because the scalability is well-suited for the Indian rural audience who have little or no discretionary income.

The freemium model wins out again.

Affixing a Netflix grade streaming asset to Alphabet’s booming digital ad business is a match made in heaven.

Buy Alphabet on the dip – YouTube’s outperformance in 2019 will surpass expectations and carry Alphabet shares to new all-time highs this calendar year.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/youtube.png493972Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-03 08:06:492019-04-03 08:21:24YouTube’s Big Move Into India

FANGS, FANGS, FANGS! Can’t live with them but can’t live without them either.

I know you’re all dying to get into the next FANG on the ground floor, for to do so means capturing a potential 100-fold return, or more.

I know because I’ve done it four times. The split adjusted average cost of my Apple shares is only 25 cents compared to today’s $174, so you can understand my keen interest. My average on Tesla is $16.50.

Uncover a new FANG and the riches will accrue rapidly. Facebook (FB), Amazon AMZN), Netflix (NFLX), and Alphabet (GOOGL) didn’t exist 25 years ago. Apple (AAPL) is relatively long in the tooth at 40 years. And now all four are in a race to become the world’s first trillion-dollar company.

One thing is certain. The path to FANGdom is shortening. It took Apple four decades to get where it is today, Facebook did it in one. As Steve Jobs used to tell me when he was running both Apple and Pixar, “These overnight successes can take a long time.”

There is also no assurance that once a FANG always a FANG. In my lifetime, I have seen far too many Dow Average components once considered unassailable crash and burn, like Eastman Kodak (KODK), General Electric (GE), General Motors (GM), Sears (SHLD), Bethlehem Steel, and IBM (IBM).

I established in an earlier piece that there are eight essential attributes of a FANG, product differentiation, visionary capital, global reach, likeability, vertical integration, artificial intelligence, accelerant, and geography.

We are really in a “What have you done for me lately” world. That goes for me too. All that said, I shall run through a short list for you of the future FANG candidates we know about today.

Alibaba (BABA)

Alibaba is an amalgamation of the Chinese equivalents of Amazon, PayPal, and Google all sewn together. It accounts for a staggering 63% of all Chinese online commerce and is still growing like crazy. Some 54% of all packages shipped in China originate from Alibaba.

The juggernaut has over half billion active users, and another half billion placing orders through mobile phones. It is a master of AI and B2B commerce. There is nothing else like it in the world.

However, it does have some obvious shortcomings. Its brand is almost unknown in the US. It has a huge problem with fakes sold through their sites.

It also has an ownership structure for foreign investors that is byzantine, to say the least. It is a contractual right to a share of profits funneled through a PO box in the Cayman Island. The SEC is interested, to say the least.

We also don’t know to what extent founder Jack Ma has sold his soul to the Beijing government. It’s probably a lot. That could be a problem if souring trade relations between the US and the Middle Kingdom get worse, a certainty with the current administration.

Tesla (TSLA)

Before you bet on a new startup breaking into the Detroit Big Three, go watch the movie “Tucker” first. Spoiler Alert: It ends in tears.

Still, Tesla (TSLA) has just passed the 270,000 mark in the number of cars manufacturered. Tucker only got to 50.

Having led my readers into the stock after the IPO at $16.50, I am already pretty happy with this company. Owning three of their cars helps too (two totaled). But Tesla still has a long way to go.

It all boils down to the success of the $35,000, 200-mile range Tesla 3 for which it already has 500,000 orders. So far so good.

It’s all about scale. If it can produce these cars in sufficient numbers, it will take over the world and easily become the next FANG. If it can’t, it won’t. It’s that simple.

To say that a lot is already built into the share price would be an understatement. Tesla now trades at ten times revenues compared to 0.5 for Ford (F) and (General Motors (GM). That’s a relative overvaluation of 20:1.

Any of a dozen competing electric car models could scale up with a discount model before they do, such as the similarly priced GM Bolt. But with a ten-year lead in the technology, I doubt it.

It isn’t just cars that will anoint Tesla with FANG sainthood. The firm already has a major presence in rooftop solar cell installation through Solar City, utility sized solar plants, industrial scale battery plants, and is just entering commercial trucks. Consider these all seeds for FANGdom.

One thing is certain. Without Tesla, there wouldn’t be s single mass-market electric car on the road today.

For that, we can already say thanks.

Uber

In the blink of an eye, ride sharing service Uber has become essential for globe-trotting travelers such as myself.

Its 2 million drivers completely disrupted the traditional taxi model for local transportation which remains unchanged since the days of horses and buggies.

That has created the first $75 billion of enterprise value. It’s what’s next that could make the company so interesting.

It is taking the lead in autonomous driving. It could also replace FeDex, UPS, DHL, and the US post office by offering same day deliveries at a fraction of the overnight cost.

It is already doing this now with Uber Foods which offers immediate delivery of takeouts (click here if you want lunch by the time you finish reading this piece.)

UberCopters anyone? Yes, it’s already being offered in France and Brazil.

Uber has the potential to be so much more if it can just outlive its initial growing pains.

It is a classic case of the founder being a terrible manager, as Travis Kalanick has lurched from one controversy to the next. The board finally decided he should spend much time on his new custom built 350-foot boat.

Its “bro” culture is notorious, even in Silicon Valley.

It is also getting enormous pushback from regulators everywhere protecting entrenched local interests. It has lost its license in London, the only place in the world that offered a decent taxi service pre-Uber. Its drivers are getting beaten up in Paris.

However, if it takes advantage of only a few of the doors open to it, status as a FANG beckons.

Walmart (WMT)

A few years ago, I was heavily criticized for pointing out that half the employees at my local Walmart (WMT) were missing their front teeth. They have since received a $2 an hour's pay raise, but the teeth are still missing. They don’t earn enough money to get them fixed.

The company is the epitome of bricks and mortar in a digital world with 12,000 stores in 28 countries. It is the largest private employer in the US, with 1.4 million workers, mostly earning minimum wage.

The Walmart customer is the very definition of the term “late adopter.” Many are there only because unlike Amazon, Wal-Mart accepts cash and Food Stamps.

Still, if Walmart can, in any way, crack the online nut, it would be a turbocharger for growth. It moved in this direction with the acquisition of Jet.com for $3 billion, a cutting-edge e-commerce firm based in Hoboken, NJ.

However, this remains a work in progress. Online sales account for only 4% of Walmart’s total. But they could only be a few good hires at the top away from success.

Microsoft (MSFT)

Talk about going from being the 800-pound gorilla to an 80 pound one, and then back to 800 pounds.

I don’t know why Microsoft (MSFT) lost its way for 15 years, but it did. Blame Bill Gates’s retirement from active management and his replacement by his co-founder Steve Ballmer.

Since Ballmer’s departure in 2014, the performance of the share price has been meteoric, rising by some 125% over the past two years.

You can thank the new CEO Satya Nadella who brought new vitality to the job and has done a complete 180, taking Microsoft belatedly into the cloud.

Microsoft was never one to take lightly. Windows still powers 90% of the world’s PCs. No company can function without its Office suite of applications (Word, Excel, and PowerPoint). SQL Server and Visual Studio are everywhere.

That’s all great if you want to be a public utility, which Microsoft shareholders don’t.

LinkedIn, the social media platform for professionals, could be monetized to a far greater degree. However, specialization does come at the cost of scalability.

It seems that the future is for Microsoft to go head to head against next door neighbor Amazon (AMZN) for the cloud services market while simultaneously duking it out with Alphabet (GOOGL).

My bet is that all three win.

Airbnb

This is another new app that has immeasurably changed my life for the better. Instead of cramming myself into a hotel suite with a wildly overpriced minibar for $600 a night, I get a whole house for $300 anywhere in the world, with a new local best friend along with it.

Overnight, Airbnb has become the world’s largest hotel chain without actually owning a single hotel. At its latest funding round in 2017, it was valued at $31 billion.

The really tricky part here is for the firm to balance out supply and demand in every city in the world at the same time. It is also not a model that lends itself to vertical integration. But who knows? Maybe priority deals with established hotels are to come.

This is another firm that is battling local regulation, that great barrier to technological innovation. None other than its home town of San Francisco now has strict licensing requirements for renters, a 30 day annual limitation, and a $1,000 a day fine for offenders.

The downtowns of many tourist meccas like Florence, Italy and Paris, France have been completely taken over by Airbnb customers, driving rents up and locals out.

IBM (IBM)

There was a time in my life when IBM was so omnipresent we thought like the Great Pyramids of Egypt it would be there forever. How times change. Even Oracle of Omaha Warren Buffet became so discouraged that he recently dumped the last of his entire five-decade long position.

A recent 20 consecutive quarters of declining profits certainly hasn’t helped Big Blue’s case. It is one of the only big technology companies whose share price has gone virtually nowhere for the past two years.

IBM’s problem is that it stuck with hardware for too long. An entrenched bureaucracy delayed its entry into services and the cloud, the highest growth areas of technology.

Still, with some $80 billion in annual revenues, IBM is not to be dismissed. Its brand value is still immense. It still maintains a market capitalization of $144 billion.

And it has a new toy, Watson, the supercomputer named after the company’s founder, which has great promise, but until now has remained largely an advertising ploy.

If IBM can reinvent itself and get back into the game, it has FANG potential. But for the time being, investors are unimpressed and sitting on their hands.

The Big Telecom Companies

My final entrant in the FANGstakes would be any combination of the four top telecommunication companies, Verizon (VZ), AT&T (T), Comcast (CMCSA), and Time Warner (TWX), which now control a near monopoly in the US.

There is a reason why the administration is blocking the AT&T/Time Warner merger, and it is not because these companies are consistently cited in polls as the most despised in America. They are trying to stop the creation of another hostile FANG.

Still, if any of the big four can somehow get together, the consequences would be enormous. Ownership of the pipes through which the modern economy courses bestows great power on these firms.

And Then….

There is one more FANG possibility that I haven’t mentioned. Somewhere, someplace, there is a pimple-faced kid in a dorm room thinking up a brand-new technology or business model that will take the world by storm and create the next FANG.

Call me crazy, but I have been watching this happen for my entire life.

I want to thank my friend, Scott Galloway, of New York University’s Stern School of Business, for some of the concepts in this piece. His book, “The Four” is a must read for the serious tech investor.

Creating the Next FANG?

https://www.madhedgefundtrader.com/wp-content/uploads/2018/02/tech-guys.jpg368550Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2019-04-03 01:06:312019-04-02 17:47:43Who Will Be the Next FANG?

Don’t get caught up in the cesspool of digital ads inundating your life.

I’ll teach you how to take back control of your life and even mess with these data thieves.

No need to thank me.

One of the most frequented complaints I hear today is the overflowing number of digital ads people are faced with that make you want to pull your hair out.

If you want to play your part in taking back your internet freedom, then read on.

The internet ad business is a world that borders subterfuge.

The high stakes environment is perpetuated by none other than Silicon Valley and specifically the tech heavyweights that wield capital dominating the data sphere.

Even though it sounds remarkably cliché, data is truly the new oil.

You would be surprised how many internet operations are based on the back of you, the user, and the data you generate.

Take Lyft (LYFT).

They are forced to tap the digital marketing world to attract qualified drivers.

Not only does Lyft spend ad dollars on driver recruitment, but they must spend to grow the number of passengers.

The rider base, as a result, synthetically grows which is directly attributable to paid marketing initiatives.

Lyft lays out on a platter the ways they attempt to generate new passengers and drivers, essentially becoming market makers, and it’s a mind-boggling long list including:

“referrals, affiliate programs, free or discount trials, partnerships, display advertising, television, billboards, radio, video, content, direct mail, social media, email, hiring and classified advertisement websites, mobile “push” communications, search engine optimization and keyword search campaigns.”

Even if there is only a 20% chance of breaking even, these unicorns are incentivized to lose others' money translating into poor quality growth or initiate high-risk strategies or carry out a combination of the two.

Sales and marketing costs in the year ending Dec 2018 came in at $296.6 million, meaning that over 37% of overall costs to Lyft were attributed to this one segment.

If that wasn’t bad enough, Alphabet affiliated company CapitalG took in $41.4 million, $74.4 million, and $92.4 million of ad-related services in 2016, 2017, 2018 laughing all the way to the bank.

Not only do Alphabet have a 5% stake in Lyft, but they are incentivized to bump up Lyft’s search engine optimization ranking to the top because they’ll benefit through asset appreciation if the company flourishes.

The process is rigged so what can we do about it?

Seizing control of your life and personal data first centers on installing a different browser other than a Google-based product to diversify the data out of Alphabet’s (GOOGL) iron grip.

I have chosen to use the browser called Brave, based on the Chromium web browser, it comes preinstalled with an ad blocker and disables web trackers, and most importantly, works well.

Make sure to import your passwords and bookmarks from your prior browser to ensure a smooth transition.

Once you are armed with a browser with a functioning ad-blocker, notice how the ad-less experience enhances your browser experience.

Try out YouTube.com, notice that ads don’t pop up in the beginning or middle of your viewing session and they do not even prompt you to disable them.

To understand which websites are hellbent on grabbing your digital ad dollar, then you will visit the odd website such as CNBC’s live TV feed which forces the user to disable the ad blocker which can be done at the top.

As much as CEO of Facebook (FB) Mark Zuckerberg has been vilified for his ad practices, he does not force users to disable ad blockers to use his platform to his credit which indicates that most users really have no idea about this stuff.

Seeking Alpha, the internet financial new site, is one of the worst eggs in the dozen, full out blocking users from even viewing the main homepage if you are accessing it with a VPN (virtual private network).

If you do access Seeking Alpha with an ad blocker, every page you click prompts an annoying reminder to “white list” the site which is polite verbiage for don’t block us or we will prevent you from using us.

Awareness and actionable methods to take back your internet freedom and personal data are vital to the health and longevity of the internet.

Instead of enriching these few Silicon Valley bullies, change your browser to an independent service, install an ad-blocker, and lastly buy a VPN.

A VPN is a software that circumvents geographical restrictions by connecting to servers in different countries effectively masking your computer’s IP address location.

This can have many different applications such as during my summer vacations in Switzerland, I can access all the US-based internet services that would require my IP address to originate from a domestic American location.

A VPN is also important in minimizing the chances of cyber threats and offers extra layers of security.

Chinese internet users often access international websites that are habitually censored through VPN software getting access to the west’s treasure trove of professional knowledge.

In many cases, a small Chinese company wielding a VPN is the difference between success and failure.

VPN software is the Chinese communist party’s worst enemy which is why they forced Apple to remove them from Apple’s app store recently.

My go-to VPN is Astrill. To visit their website, please click here.

Knowledge is power.

The masking of a computer’s geographical location will stymy digital ad crawlers diluting ad data forcing them to revalue the digital ad tools they use to charge exorbitant amounts to analog companies to digitally advertise destroying ad revenue.

I see this as a positive development as the unintended consequences of these digital ad creatures have toxified the internet for the naive user with many digital companies resorting to perverse tactics that beget even more perverse marketing tactics.

The slew of new tech IPOs is offering us inside knowledge into how enslaved tech companies are to the likes of Alphabet and Facebook digital ad apparatus.

To shake them off our tails, users on mass need to alter how they use the internet to protect from being pickpocketed in broad daylight.

Once revenue begins to suffer, they will have to act more reasonably to the betterment of the internet which we all share as a communal good.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/astrill.png443552Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-02 08:06:522019-04-02 08:36:22How to Get Control of Your Life

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR THE INMATES ARE RUNNING THE ASYLUM)

(SPY), (TLT), (FCX), (DIS), (TSLA), (IWM), (AAPL),

(GOOGL), (MSFT), (PYPL), (AMZN)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-01 08:07:292019-04-01 08:12:16April 1, 2019

I have decided to run for president next year. If you wondered why my content has been slacking off lately, it’s because I’ve been hard at work writing the Mueller Report. Oh, and the Dow Average will reach 100,000 by December.

Ha! Gotcha! April fool.

Still, looking at the market action last week, you really have to wonder if the inmates have seized control of the asylum when the average rose four of five days. These are people who are buying stocks at a decade high, with collapsing earnings, and the rest of the world falling into recession.

However, there is a method to their madness. Interest rates across every maturity in Europe and Japan turned negative last week. Suddenly both US stocks AND bonds looked like the bargain of the century, but only if you were foreign. An avalanche of cash into the US followed triggering an explosive move up in the bond market. For the first time in three years, I was not short.

And here’s the interesting part. It could continue for months.

In the meantime, investors have been grappling with a number that will be the most important print of the year. The first look at Q1 2019 GDP will be published on April 23, and it is widely expected to be awful, at less than a 1% annual rate. It will include the effects of the record 34-day government shutdown as well as the horrendous weather and flooding of last winter.

So, on the one hand, you have a stock market that is simultaneously being propped up by enormous cash flows and held back by a weakening economy and earnings and profit-taking from the best quarterly start in ten years. It all adds up to a market that could go absolutely nowhere.

And I just so happen to have the perfect portfolio for such a market. These are the precise conditions where deep in-the-money call and put option spreads absolutely prosper. When everything is going nowhere, spreads always expire at their maximum profit points.

The global easing trend is accelerating as central banks rush to head off the next global recession. Expect interest rates to drop to levels you once thought impossible.

The global bond short covering panic continues, with ten-year US Treasury yields dropping to an eye-popping 2.33%. Slowing global growth is to blame. Did I hear the word “refi”?

Foreign investors poured into the US bond market, driving ten-year US Treasury yields down to 2.33%. When everyone else in the world has negative yields, our bonds become the best paying in the world.

Q4 GDP final report came in at 2.2% as expected, down a third from Q3. Expect that figure to more than halve in Q1 2019. Put on your hard hat.

The Mueller Report gave Trump a clean bill of health, at least on the collusion issue. But it opened up a dozen other lines of investigation that will continue for years. It’s definitely a “RISK ON” development.

US Existing Home sales jumped 11.8% in January. Low mortgage interest rates are finally kicking in with the 30-year fixed at 4.23%. This is a one hit wonder, not the beginning of a new trend. But interest rates are going lower.

New Home Sales were up 4.9% to 667,000 units in February in a rare positive data point. Could low interest rates finally be kicking in? Still, avoid homebuilders.

Apple (AAPL) announced its new streaming service, Apple TV Plus, and the stock fell on a “sell the news” drop. Roku is included in the package so buy (ROKU). The Apple offering is weak enough to allow plenty of room for Disney to launch its own streaming service Disney Plus at the end of this year. Prepare for an onslaught of princesses. Buy (DIS) too.

Home price appreciation hit a four-year low with the S&P Case Shiller National Home Price Index growing only 4.2% YOY in January, down from 4.6% the previous month. Las Vegas, Phoenix, and Minneapolis are still showing the biggest gains while San Francisco and Seattle are seeing the biggest price drops. Avoid homebuilders (ITB).

Lyft (LYFT) priced at $72 a share, the top end of expectations, valuing the company at an eye popping $25 billion at the end of the day. Never mind that the company is losing money hand over fist, it’s all about potential. The tech IPO bubble top has started!

The Mad Hedge Fund Trader was up on the week with time decay in our combed 13 positions our best friend. The quarter end window dressing was kind to us.

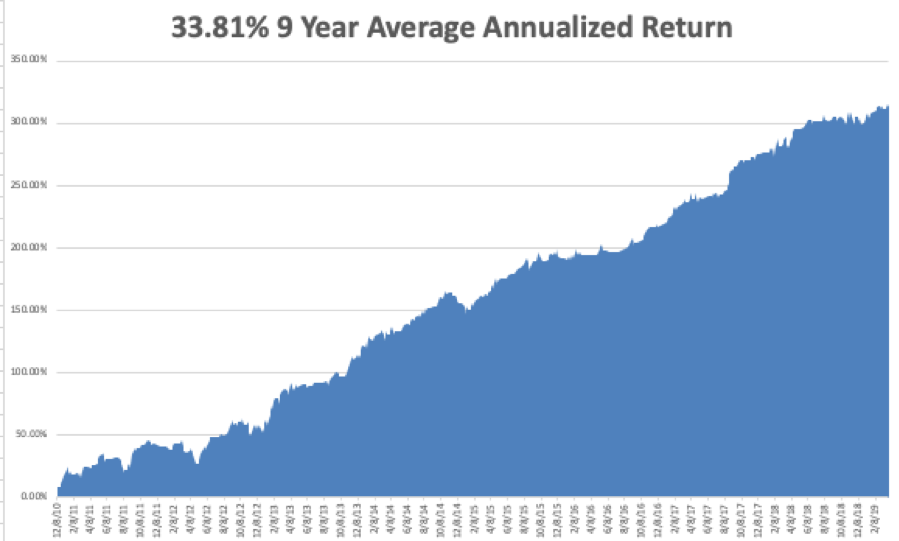

March turned positive in a final burst, up 1.78%. My 2019 year to date return retreated to +15.49%, boosting my trailing one-year return back up to +35.16%.

My nine-year return recovered to +315.56%, a new all-time high.The average annualized return appreciated to +33.81%. I am now 45% in cash, 30% long and 25% short, and my entire portfolio expires at the April 18 option expiration day in 9 trading days. I took generous profits on my positions in copper miner Freeport McMoRan (FCX) right when it bounced off the 200-day moving average.

The Mad Hedge Technology Letter maintained long positions in Microsoft (MSFT), Alphabet (GOOGL), and PayPal (PYPL), and Amazon (AMZN), which are clearly going to new highs.

It’s jobs week again with the usual trifecta of employment reports. Last month was a disaster, so this month will be interesting.

On Monday, April 1 at 8:30 AM, February Retail Sales are published.

On Tuesday, April 2, 8:30 AM EST, we learn February Durable Goods.

On Wednesday, April 3 at 8:15 AM, the ADP Employment Report comes out for private hiring.

On Thursday, April 4 at 8:30 AM EST, the Weekly Jobless Claims are announced.

On Friday, April 5 at 8:30 AM, we obtain the big number of the week, the February Nonfarm Payroll Report.

The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I’m going to use a rare spell of good weather to drive up to Lake Tahoe and start the planning work on my October 25-26 Mad Hedge Lake Tahoe Conference. Half the dinner tickets sold out on the first day, so you better get moving now.

Maybe it’s something I said? To learn more about the conference, please click here. I’ll see you there.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-04-01 08:06:362019-04-01 08:12:28The Market Outlook for the Week Ahead, or The Inmates are Running the Asylum

(FINDING A NEW FANG), (FB), (AAPL), (NFLX), (GOOGL), (TSLA), (BABA)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-03-29 09:07:252019-03-29 10:51:56March 29, 2019

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.