Mad Hedge Technology Letter

March 26, 2019

Fiat Lux

Featured Trade:

(PINTEREST COMES OUT)

(PINS), (FB), (AAPL), (GOOGL), (AMZN)

Mad Hedge Technology Letter

March 26, 2019

Fiat Lux

Featured Trade:

(PINTEREST COMES OUT)

(PINS), (FB), (AAPL), (GOOGL), (AMZN)

The Facebook (FB) of digital images is on deck and has filed to go public.

I'll give you the skinny on it.

Pinterest (PINS) has slightly different lingo - they call digital images pins, a collection of pins, a pinboard, and the users that post pins are pinners.

Aside from this little creative wrinkle, Pinterest does little to help flow my creative juices.

That's not to say they are a bad company, in fact, it's quite refreshing that on the financial side of the equation, Pinterest is a solid financial enterprise.

They make money and aren't going to burn through their cash reserves anytime soon.

This should give some peace of mind to potential investors looking at snapping up shares of Pinterest.

Even though they are not a bad company, I cannot promote them as a firm revolutionizing technology in the way we know it, they certainly don’t, and never will, at least at the current pace of innovation.

Pinterest derives almost 100% of its revenue from digital ads à la Facebook, they do not sell anything and much like Facebook, the user is the product by way of mining private data and selling them over to third-party ad agencies who subsequently sell targeted ads on Pinterest’s platform.

As I read through Pinterest’s S-1 filing with the SEC, an overwhelming portion of the content is reserved for the litany of regulatory risks that serving digital ads, curating others' content, and the international risks that pose to Pinterest growth story.

As with most tech growth stories, this particular narrative must orbit around the strength of incessantly growing its domestic and international user base.

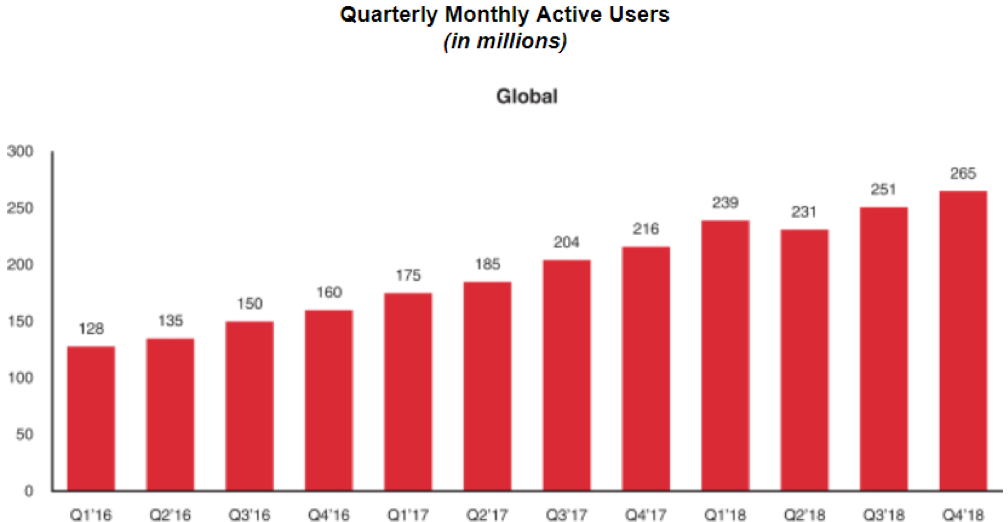

I surmise that part of the reason they desire to go public is because of the 265 million in global quarterly monthly users have reached the high watermark.

Therefore, this calculated risk of going public is entirely justified as the cash out for the venture capitalist and private owners that invested in this company as a burgeoning toddler.

Or the owners see catastrophic downside from the regulatory landscape which has been increasingly volatile in the past few quarters and wish to get out as soon as they can.

Let's make no mistake about this, Pinterest does not control its own destiny, and their success will be based upon external factors that they cannot control.

Some of these factors have already reared their ugly head, the most relevant example was when Google (GOOGL) changed its image search algorithm which disrupted Pinterest’s image function.

This was an example of third-party content originators clamping down on their willingness to allow Pinterest to populate content on their proprietary platform, and the lack of availability of content or the decreasing nature of it will sting the hope of increasing web traffic on Pinterest going forward.

Pinterest has clearly disclosed in its IPO filing that they are reliant on crawling third-party search engine services for third-party photos, this content is curated into their platform and credited to the original user.

I would classify this type of technology as unimpressively low grade and Pinterest will be susceptible to many more possible disruptions in the future.

In layman terms, if the stars do not align, Pinterest will be the first to feel it, and strategically speaking, this is a poor position to strategically operate from.

If Pinterest cannot serve the specific content that incites the tastes of pinners, this could destroy retention and engagement rates leading to a damaging downdraft of ad revenue.

Pinterest's feeble business model will certainly call for new investments in and around more innovative parts of technology.

What we have seen most successful technology companies flirt with are full-fledged recurring revenue models, and bluntly, Pinterest does not have one.

The likes of Microsoft, Amazon, Google, and Apple have pivoted hard towards this subscription model proving they can have their own cake and eat it too.

Funnily enough, Pinterest pays AWS, Amazon’s cloud arm, an extraordinary amount of money to store the pins or digital images on AWS Cloud platform to the tune of almost $800 million per year showing how beneficial it is to be on the other side of the equation.

Pinterest does benefit from a robust brand reputation and its footprint in America is quite large.

However, one group of potential customers have clearly been left out in the cold - Males.

The firm has been famous for being the go-to image platform for young mothers and generally speaking, American women born in the 1980s.

According to data analytics, it appears that content that males gravitate towards is not present on the platform and will need to be addressed going forward to grow users.

Another crucial problem that must be addressed is the lack of domestic growth in the user base.

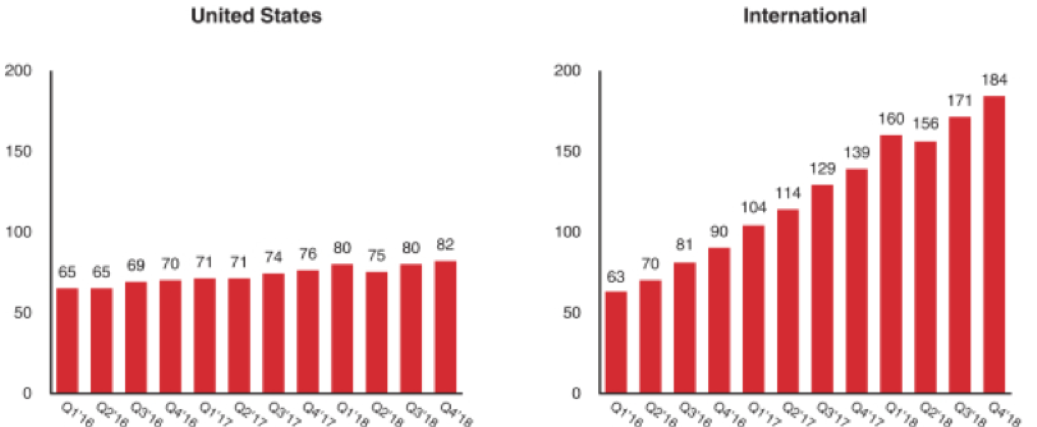

In Q1 2018, Pinterest achieved 80 million monthly active users, however, fast forward to Q4 in 2018 and the number had barely inched up to 82 million monthly active users.

From Q1 to Q2, there was a dramatic deceleration in the number of monthly active users falling by 5 million to 75 million monthly active users.

The company blamed this on Facebook changing their password security causing users who rely on Facebook passwords and username entrance data to be temporarily stonewalled from entering Pinterest.

Millions decided to avoid the hassle and just stop using Pinterest because they were unable to enter the platform, causing major carnage to Pinterest’s ad-supported revenue model because of the hemorrhaging usership.

Unfortunately, bigger platforms such as Facebook and Google are not responsible to telegraph these structural changes in policy to Pinterest which means that this type of loss of usership could be a bi-annual or annual exercise in damage control.

Losing 10% of your user base based on someone else’s systemic changes is a bitter pill to swallow.

Investors must ask themselves why a premium search engine like Google search want to allow Pinterest to continue to curate its images for ad revenue effectively skimming off of Google’s top line?

As you have seen, Google has hijacked many of these types of business initiatives by taking on these opportunities themselves, dismantling the choke points, and going in for the kill.

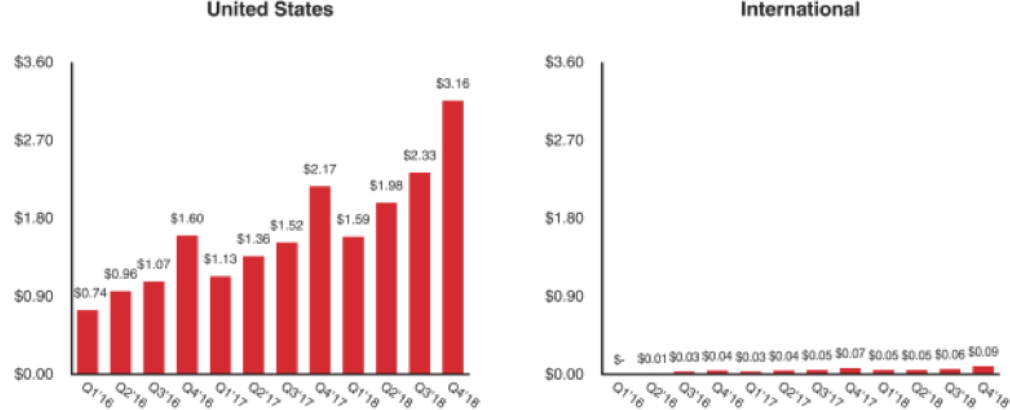

The main avenue of user expansion is its international audience, and sadly, the average revenue per international user is a paltry $0.09. This number was up sequentially from the prior quarter which was $0.06.

If you compare the revenue per user with America, then it's easy to understand why the company wants to go public now.

Management presided over a sequential increase of American revenue per user from $2.33 to $3.16 in the prior quarter and the same growth will be hard to maintain and replicate spurring the higher-ups to cash out.

International growth is staring down a barrel of a gun with restricted access by governments who do not allow this type of service in their countries such as China, India, Kazakhstan, and Turkey.

The impact of these broad-based bans decodes into Europe being the only possible answer to user growth in revenue terms and total usership.

To state that Pinterest is confronted by widespread global risk is an understatement.

However, the low-hanging fruit would be squeezing more revenue out of the American user and I would guess that the ceiling would be around $7 per user in the near-term.

If management hopes to eclipse the $7 per American user, they will have to migrate into more data generative strategies such as video.

Mad Hedge Technology Letter

March 25, 2019

Fiat Lux

Featured Trade:

(APPLE’S BIG PUSH INTO SERVICES)

(AAPL), (GS), (NFLX), (GOOGL), (ROKU)

The future of Apple (AAPL) has arrived.

Apple has endured a tumultuous last six months, but the company and the stock have turned the page on the back of the anticipation of the new Apple streaming service that Apple plans to introduce next week at an Apple event.

The company also recently announced a partnership with Goldman Sachs (GS) to launch an Apple-branded credit card.

In the deal, Goldman Sachs will pay Apple for each consumer credit card that is issued.

These new initiatives indicate that Apple is doing its utmost to wean itself from hardware sales.

Effectively, Apple's over-reliance on hardware sales was the reason for its catastrophic winter of 2018 when Apple shares fell off a cliff trending lower by almost 35%.

This new Apple is finally here to save the day and will demonstrate the high-quality of engineering the company possesses to roll out such a momentous service.

Frankly speaking, Apple needs this badly.

They were awkwardly wrong-footed when Chinese consumers in unison stopped buying iPhones destroying sales targets that heaped bad news onto a bad situation.

I never thought that Apple could pivot this quickly.

Apple's move into online streaming has huge ramifications to competing companies such as Roku (ROKU).

In 2018, I was an unmitigated bull on this streaming platform that aggregates online streaming channels such a Sling TV, Hulu, Netflix and charges digital advertisers to promote their products on the platform through digital ads.

I believe this trade is no more and Roku will be negatively impacted by Apple’s ambitious move into online streaming.

What we do know about the service is that channels such as Starz and HBO will be subscription-based channels that device owners will need to pay a monthly fee and Apple will collect an affiliate commission on these sales.

Apple needs to supplement its original content strategy with periphery deals because Apple just doesn’t have the volume to offer consumers a comprehensive streaming product like Netflix.

Only $1 billion on original content has been spent, and this content will be free for device owners who have Apple IDs.

Apple's original content budget is 1/9 of Netflix annual original content budget.

My guess is that Apple wants to take stock of the streaming product on a smaller scale, run the data analytics and make some tough strategic decisions before launching this service in a full-blown way.

It's easier to clean up a $1 billion mess than a $9 billion mess, but knowing Apple and its hallmarks of precise execution, I'd be shocked if they make a boondoggle out of this.

Transforming the company from a hardware to a software company will be the long-lasting legacy of Tim Cook.

The first stage of implementation will see Apple seeking for a mainstay show that can ingrain the service into the public's consciousness.

Netflix was a great example, showing that hit shows such as House of Cards can make or break an ecosystem and keep it extremely sticky ensuring viewers will stay inside a walled pay garden.

Apple hopes to convince traditional media giants such as the Wall Street Journal to place content on Apple's platform, but there has already been blowback from companies like the New York Times who referenced Netflix’s demolition of traditional video content as a crucial reason to avoid placing original content on big tech platforms.

Netflix understands how they blew up other media companies and don’t expect them to be on Apple’s streaming service.

They wouldn’t be caught dead on it.

Tim Cook will have to run this race without the wind of Netflix’s sails at their back.

Netflix has great content, and that content will never leave the Netflix platform come hell or high water.

Apple is just starting with a $1 billion content budget, but I believe that will mushroom between $4 to $5 billion next year, and double again in 2021 to take advantage of the positive network effect.

Apple has every incentive to manufacture original content if third-party original content is not willing to place content on Apple's platform due to fear of cannibalization or loss of control.

Ultimately, Apple is up against Netflix in the long run and Apple has a serious shot at competing because of the embedment of 1 billion users already inside of Apple's iOS ecosystem that can easily be converted into Apple streaming service customers.

If you haven't noticed lately, Silicon Valley's big tech companies are all migrating into service-related SaaS products with Alphabet (GOOGL) announcing a new gaming product that will bypass traditional consoles and operate through the Google Chrome browser.

Even Walmart (WMT) announced its own solution to gaming with a new cloud-based gaming service.

I envision Apple traversing into the gaming environment too and using this new streaming service as a fulcrum to launch this gaming product on Apple TV in the future.

The big just keep getting bigger and are nimble enough to go where internet users spend their time and money whether it's sports, gaming, or shopping.

Apple is no longer the iPhone company.

I have said numerous times that Apple's pivot to software was about a year too late.

The announcement next week would have been more conducive to supporting Apple’s stock price if it was announced the same time last year, but better late than never.

Moving forward, Apple shares should be a great buy and hold investment vehicle.

Expect many more cloud-based services under the umbrella of the Apple brand.

This is just the beginning.

Mad Hedge Technology Letter

March 21, 2019

Fiat Lux

Featured Trade:

(THE ALPHABET NO-BRAINER)

(GOOGL)

Buy Alphabet (GOOGL).

That is the obvious takeaway from the European Union disciplining Alphabet.

EU regulators levied a $1.7 billion fine because of breaches of anti-trust law.

It’s the third time the company has been caught out over unfair practices, but let's be honest about it, the internet is a dirty game and rife with firms cutting corners wherever they can get an edge.

Google search is incentivized to thwart third-party companies hoping to carve out ad revenue on the back of Google's assets.

I commend the EU for stepping up and scolding these big tech companies when stateside they have been allowed to run riot doing whatever they please.

It's gotten to the point where these companies are larger than governments themselves and hold enough power to crush small countries in its wake.

The pitiful thing about this whole ordeal is that it shows how little sway governments hold on these monster tech companies now.

Not only are they too big to fail, but too big to regulate.

Google will keep doing what it does, raking in ad revenue because of the stranglehold they have on global eyeballs.

So let’s diagnose this for what it is - a slight slap on the wrist.

There will be many more fines down the road, but who cares, Alphabet will just cut them a check.

A fine of $1.7 billion is chump change if you consider they pulled in over $32 billion in digital advertising last quarter alone.

Google was penalized for initially forcing websites to sign exclusivity contracts promising flourishing websites not to work with other search engines.

In 2009, Google upped the ante by paying off these popular third-party websites to not allow alternative search engines to display their website in searches.

Expectedly, these websites lapped up the extra revenue and had no complaints.

The last thing a dominant website wants to do is to irate Google who they are reliant on for the bulk of revenue.

Protecting your customers and shielding them from outside competition is nothing new.

This sort of business practice has been going on since the beginning of time.

Google has no incentive to change its business model to accommodate EU law because retrospective fines of this paltry amount will not force them to substantially transform their ad business.

Heftier fines could come its way in the EU as the Europeans are intent on tackling digital privacy, but the push hardly disrupts Google and the direction they are headed in.

The Android platform and Google's bundle of apps are monopolies that command 80% of the European market share on consumer devices.

Google claims that it stopped this illegal, underhanded practice in 2016. However, in the bigger scheme of things, Google will, by default, benefit naturally from the strategic position they hold in the tech ecosystem.

Therefore, this convoluted regulatory cat-and-mouse game with the European Commission will continue because at the end of the day, Google's positive network effect becomes stronger with age and assets under its umbrella of services are inclined to possess an advantage over companies that aren't linked with Google in a financially incentivized way.

This issue seeps deeper with Stadia, Google’s new attempt at revolutionizing gaming with native cloud-based gaming.

If Google directly connects with gamers via Google Chrome and is incentivized to push in-house gaming ad revenue through this platform, then why would Google search ever allow outside consumers to be able to find relevant search results about other gaming companies if they aren’t profiting directly.

It's a conflict of interest that Google will find itself knee-deep in.

For your information, Stadia will initially only be available on Google Chrome and on Android devices, you’re out of luck if you use Safari.

And what if a company such as Nintendo wants to post ads on Google Stadia via Google Chrome, can Google just say no because they don’t want to feed the enemy?

Google is on record for saying that it will give companies a fair shot to market different search engines and even give more clout to third-party shopping networks.

But by no means does this mean Google will voluntarily give up their cash cow.

Any change would be ornamental at best, and at the worst, Google would just stonewall the initiative and kick the can down the road eventually hoping the EU fine will be less than the last one.

For any small company, this would be disastrous, but Google is no peon.

Shares rose on the news of the EU fine as investors cheered from the sidelines that this chapter in Google's penalties and fines ledger is temporarily over.

It's funny to say that a $1.7 billion fine effectively meant Google came away from the situation unscathed, but that is where we are at with this type of company at this point in history.

This year is shaping up to be an overly positive year for Alphabet as they venture into gaming and have an interesting mix of high growth divisions such as YouTube.

They have even started to sell its self-driving sensors through its Waymo division.

I almost feel my spine tingle as I say this, but Google might be the most innovative company of 2019 following in the footsteps of Amazon’s innovative rampage in 2018.

Alphabet can't stay out of the news and being berated for being too dominant in Europe is a problem that many smaller companies wish they could have.

In the short-term, I initiated a bullish call on Google and shares have run up quite significantly since that call.

Wait for a pullback to locate an entry point, but I can't imagine shares going back under $1,000 in 2019 unless there is some type of catastrophic black swan event that roils the broader market.

Mad Hedge Technology Letter

March 20, 2019

Fiat Lux

Featured Trade:

(LYFT), (UBER), (GRUB), (POSTMATES), (DOORDASH), (GOOGL)

The imminent launch of the Lyft IPO is telling investors that the next era of technology is upon us.

Does that mean that you should go out and buy Lyft shares as soon as they hit the market?

Yes and no.

30 million shares are up for grabs and the price of the IPO appears to be pinpointed between $62 and $68.

Even though this company is a huge cash burning enterprise, the fact is that they have been catching up to industry leader Uber and snatching away market share from the incumbent.

It was only in January 2017 that Lyft had accumulated 27% of the domestic market share, and in the recent filing for the IPO, that number had exploded to 39%.

If Lyft can start to gnaw into Uber's lead even more, shares will be prime to rise beyond the likely $62 to $68 level.

Let's remember that one of the main reasons for Uber giving up ground in this 2-way race is because of the toxic work environment embroiling many of the upper management and the subsequent damage to its broad-based public image.

If you wanted the definition of a public relations disaster, Uber was the poster boy.

Story after story leaked detailing payment problems to Uber drivers, a huge data leak revealing millions of lost personal information, and even a crude video of the founder berating a driver went viral.

There might be no Cinderella ending for this ride-hailing operation as litigious time bombs stemming from an aggressive high-risk, high-reward strategy skirting local taxi laws have flaunted the feeling of corporate invincibility in the face of government.

Being the first of its kind to hit the market, I do believe the demand will outstrip the supply.

There is a scarcity value at play here that cannot be quantified.

And an initial pop from the low-to-mid $60 range to about $80 is a real possibility in the short-term.

However, expect any robust price action to be met with rip-roaring volatility, meaning there is a legitimate chance that shares will consolidate back to $50 before they head up to $100.

Some of my favorite picks have echoed this same price action with fintech juggernaut Square (SQ) and streaming platform Roku (ROKU) mimicking heart-stopping price action with 10% moves up or down on any given day.

This doesn't mean that these are bad companies, but they do become harder to trade when entry points and exit points become harder to navigate around because of the extreme beta attached to the package.

The big winner of this IPO is ultimately self-driving technology.

Let's not skirt around the issue - Lyft loses a lot of money and so does Uber and that needs to stop.

It has been customary for tech companies to go public in order for the initial venture capitalists to cash out so they can rotate capital into different appreciating assets.

When companies are on the verge of ex-growth, maintaining the same growth trajectory becomes almost impossible without even more incremental cash burn relative to sales.

This leads to an even more arduous pursuit of revenue acceleration with stopgap solutions calling for riskier strategies.

What this means for Lyft is that they will need to double down on their self-driving technology because they are incentivized to do so, otherwise face an existential crisis down the road.

The most exorbitant cost for Uber and Lyft is by far employing, servicing, and paying out the drivers that shuttle around passengers.

I cannot envision these companies becoming profitable unless they find a way to eliminate the human driver and automate the driving function.

I will say that Uber benefitting from the Uber Eats business has been a high margin bump to the top line.

Yet, food delivery is not the main engine that will spur on these IPO darlings.

This part of the business is getting more saturated with margins getting chopped down every day.

What food delivery mainstays like Doordash and GrubHub don't have, is the proprietary self-driving technology that at some point will be present in every vehicle in the United States and the world.

What we are seeing now is a race to perfect, optimize, and implement this technology in order to further license it out to food delivery operations and other logistic heavy business that focus on the last mile.

The licensing portion out of self-driving technology will become a massive revenue driver eclipsing anything that the actual ride-hailing revenue from passengers can inject.

Well, that is at least the hope.

And because Lyft going public might force the company to remove the subsidies provided to the lift operators, this could translate into higher costs per unit.

The pathway is a no-brainer – Lyft needs self-driving technology more than the technology needs them.

And even though Google is head and shoulders the industry leader with Waymo, Lyft and Uber don't have a world-famous search engine that they can fall back on if the sushi hits the fan.

I believe Lyft passengers will have to pay more for rides in the future because of the demand for meeting short-term targets incentivizing management to raise fares.

Going public first will allow them to set the industry standards before Uber can participate in the discussion gifting a tactical advantage to Lyft.

That is why Uber is attempting to go public as fast as possible because every day that Lyft is a public company is every day that they can push their unique narrative and standardize what is a nascent industry that never existed 20 years ago with their new capital.

If high risk is your cup of tea, then buy shares when you get the first crack at it, otherwise, take a backseat with a bag of popcorn and watch history unfold.

This trade is not for the faint of heart and until we can get some more color on the business model and the ability or not of management to meet quarterly or annual expectations, there will be many moving parts with cumbersome guesswork involved.

To read up on Lyft’s IPO filing on the SEC website, please click here.

Mad Hedge Technology Letter

March 19, 2019

Fiat Lux

Featured Trade:

(GOOGLE’S AGGRESSIVE MOVE INTO GAMING),

(GOOGL), (AAPL), (FB), (NFLX), (MSFT) (EA), (TTWO), (ATVI)

The saturation of tech is upon us.

That is the takeaway from Google’s (GOOGL) hard pivot into gaming.

The goal of their new gaming service is to become the Netflix (NFLX) of gaming allowing gamers to skip purchasing third-party consoles and playing games directly from an Android-based Google device.

Middlemen in the broad economy are getting killed and this is the beginning.

What we are really seeing is a last-ditch effort to protect gaming consoles - these devices will become extinct in less than 20 years boding ill for companies such as Sony and Nintendo

The cloud is still all the rage and companies such as Microsoft (MSFT), Alphabet (GOOGL), and Apple (AAPL) have the natural infrastructure in place to offer cloud-based gaming solutions.

Phenomenon such as internet game Fortnite have shown that consoles are outdated and relying on the cloud as a fulcrum to extract gaming revenue by way of add-ons and in-game enhancements will be the way forward

Another key takeaway from this development is that passive investment is dead, even more so in tech, where these big tech companies are starting to bleed over into each other's territory.

This dispersion will create opportunity and pockets of weakness.

I blame this on a lack of innovation with companies still trying to extract as much as they can from the current smartphone-based status quo which has pretty much run its course.

Technology is itching for something revolutionary and we still have no idea what that new idea or device will be.

The rollout of 5G is promising and companies will need some time to adapt to this super-fast connection speed.

In either case, I can tell you the revolution won’t include foldable smartphones.

In 2018, the gaming industry flourished on accelerating momentum by registering over $136 billion in sales, and the revenue growth rate is already about 15% and increasing.

Naturally, companies such as Amazon and Google want a piece of this action and are hellbent on making inroads in the gaming environment such as Amazon's ownership of Twitch, which is a game streaming service where viewers can watch live tournament-style competitions proving extremely popular with Generation Z.

I applaud this move by Google because they already have proved they can execute on certain mature assets such as YouTube which has become the Netflix replacement of 2019.

Doubling down in the gaming sector would be a bonus as they search a second accelerating revenue driver that will dovetail nicely with the overperformance in YouTube this year.

It’s even possible that YouTube could be modified to support live stream gaming, certainly various synergistic dynamics are at play here.

Even if they fail - it's worth the risk.

Revenue extraction will be painful for certain companies like Facebook (FB) in this new environment, who has seen a horde of top executives abort after the company drastically changed directions, believing the company is on a suicide mission to fines and more regulatory penalties.

I've mentioned in the past that Facebook no longer commands the same type of employee brand recognition they once cultivated.

Facebook will find a tougher time to find the right people they need to execute their private chat plan, by linking the likes of WhatsApp, Instagram, and Facebook Messenger.

This is a high-risk high-reward proposition that could end up with Facebook's co-founder Mark Zuckerberg in tears if regulators give him the cold shoulder, and that is why many executives who are risk-adverse want to cash in now because they sink with the Titanic.

Not only are gaming assets becoming saturated, but the general online streaming environment is attracting a tsunami of supply all at one time.

Online content is already veering into the same type of pricing structures that cable offered traditional customers.

Investors will have to ask themselves, how much will the average consumer spend in content-based entertainment per month?

My guess is not more than $100 per month.

The saturation will cause tech companies to become even more draconian.

Be prepared for some more epic in-fighting until a new gateway of internet monetization opens up.

There has never been a better time to be a tactical and active investor in tech.

The Fang trade has splintered off with each company facing unpredictable futures.

Unearthing value will become more difficult because these traditional bellwether tech stocks have decoupled and aren't going straight up anymore.

Those zigs and zags will still be buttressed by a secular tailwind of the migration to digital, but there are certain winners and losers that will result of this.

Apple announcing a new streaming product is proof that these Silicon Valley tech firms are desperate for new profit drivers as the woodchips that fuel the fire start to run noticeably short on supply.

At the bare minimum, this looks disastrous for the traditional gaming companies of Electronic Arts (EA), Take-Two Interactive (TTWO), and Activision (ATVI) whose shares have been effectively shelved due to the Fortnite revolution.

EA has fought back with their own Fortnite lookalike called Apex Legends which showed a Fortnite-like trajectory sucking in 10 million players in the first 72 hours.

The stock exploded 16%, signaling this is the new way forward for gaming companies.

As a whole, these traditional gaming studios simply don’t have the firepower to compete with the big boys, let alone possess a strong cloud infrastructure.