Mad Hedge Technology Letter

April 8, 2019

Fiat Lux

Featured Trade:

(THE BATTLE FOR COFFEE IN CHINA)

(SBUX), (MSFT), (AAPL), (IBM)

Mad Hedge Technology Letter

April 8, 2019

Fiat Lux

Featured Trade:

(THE BATTLE FOR COFFEE IN CHINA)

(SBUX), (MSFT), (AAPL), (IBM)

If you ask me what you should sample at a Starbucks in China - I would say nothing.

Starbucks has become successful on the back of selling bad tasting coffee to the Chinese.

Even more peculiar, the CEO of Starbucks Kevin Johnson has been captaining the ship since 2017.

After watching Johnson's interview with Bloomberg, I fully believe he is not adequately prepared for what the future beholds.

Let me explain why.

Johnson started at IBM (IBM) in the 80s as an engineer, but he hasn't been an engineer for the last 20 odd years.

In the early 2000s, he became a salesman at Microsoft (MSFT), and his interview revealed that he is still a salesman at heart.

He continued to refer back to his engineering background, yet the know-how he accumulated in the 80s at IBM has little relevance to the “move fast and break things” environment of today.

Johnson was groomed under the tutelage of Microsoft’s Steve Ballmer at Microsoft, a salesman, who almost sunk Microsoft during his tenure.

Anyone who trained under Steve Ballmer is someone that would need to walk across fiery embers to prove his or her viability.

The interview with Bloomberg felt like an inauthentic marketing video, with Johnson regurgitating salesman rhetoric with little substance.

As Starbucks shreds the bear story of naysayers to make new all-time highs, there are serious icebergs ahead because of disruptive technological start-ups.

Starbucks has relied on emerging markets as its growth engine inaugurating 612 stores in China last year, and another 600 will come online before 2022.

Selling bad coffee to Chinese will be more difficult going forward.

The prominent tea drinking nation had no idea what good coffee tasted like 10 years ago.

Even recently, many Chinese thought instant coffee packaged in those convenient stick-shaped packets was high-grade coffee.

The last five years has seen an unmitigated onslaught of Chinese international tourism mainly flowing to Europe, Canada, Australia, and America.

Not only did Chinese shop until their panties dropped, but they began to become more inclined to understand culinary and cultural aspects of foreign cultures like, for instance, how good coffee should taste among other cultural trappings.

Five years ago, Chinese also went to Starbucks to sample the coffee. Now, they go to Starbucks because the interiors are comfortable making it a plausible place for an impromptu business meeting in a downtown or business district location.

Let’s remember that Starbucks could never crack the Italian market because teaching Italians how to make coffee doesn’t sell in Italy.

It took until last September to open the first Starbucks in the cultural center of Milan, Italy, and I can tell you that it’s not a regular, cookie cutter Starbucks.

The Milan Starbucks is billed as a “Reserve Roastery” with marble finishes contributed from the supplier that up until now was only used to build the famed Duomo of Milan and buildings in the surrounding Piazza.

To say this Starbucks is posh is an understatement.

The 25,000-square-foot coffee shop delivers small-batch roastings of exotic coffees from more than 30 countries, and artisanal food from the local culinary rock star, Rocco Princi.

In fact, Starbucks built it into a four-star restaurant with expensive cocktails and the whole shebang.

Understandably, the average revenue per user (ARPU) at the Italian roastery earns 400% more than the average American Starbucks shop.

This is what Starbucks had to do to get their first footprint into Italy, while coffee know-how isn’t up to that level in China, differentiating variables will be harder to discover moving forward as Chinese customers look to handcrafted, artisanal options demanding a superior customer experience.

The generic Starbucks in China sells mediocre black coffee made from inferior beans for $5 per cup, a far cry from the reserve roastery in Milan.

If you get into the creamier, frothy types of drinks, then price points shoot up to $6 or $7.

Meet the current tech disruptor of coffee business in China, Luckin Coffee headed by Chinese tech entrepreneur Qian Zhiya.

Her impressive resume spans from COO of Shenzhou, a car rental app and website, to Co-founder of UCAR, a ride-hailing service spun off from Shenzhou.

During the Bloomberg interview, Kevin Johnson bragged that Starbucks is opening a new Chinese Starbucks every 15 hours.

He forgot to mention Starbucks' local competitor opens a new Luckin Coffee every 8 hours amounting to about 3 per day.

Luckin Coffee's plan is to open 1,950 more stores in the next 18 months.

This has the inklings of a dogfight down to zero with a local upstart, and ask how that turned out for Facebook, Google, or even Amazon in China.

Every FANG except Apple (AAPL) cease to exist in China now, and brewing bad coffee doesn’t create the positive network effect that Apple has in China, effectively delivering an additional 4 million ancillary jobs connected to the iOS system.

The entrenched nature of Apple in China means they cannot be removed without catastrophic job losses to local Chinese triggering massive social unrest.

In the case of Starbucks, every location that folds, employees can walk across the street to join a Luckin Coffee franchise, such is an environment in a zero-sum game.

Qian envisions coffee shops like a tech empire because of her background, and has earmarked fresh capital for product R&D, technology innovation, and business development.

Luckin is hellbent on capturing young office workers with its locations, delivery services, and low prices, operating a no-frills type of Starbucks alternative.

They have undercut Starbucks pricing by offering the same cup of Americano $5 coffee for $3.15.

How about their expansion plans?

Locations will explode to 4,500 by the end of 2019 which will eclipse the number of Chinese Starbucks in mid-2019.

The company has relied on technology, over half of the locations lack physical seating, shrinking space by way of applying kiosk structures as a coffee preparation station before customers access delivery orders through the smartphone app.

Digital payments are common via WeChat or Luckin’s own “coffee wallet,” and over 70% of digital customers are under 30.

Luckin's strategy is a far cry from the plush sofas of Starbucks' home away from home strategy. Distinctively, Luckin does not want customers to lounge around and talk business.

The rise of Luckin Coffee coincides with hamstringing Starbucks' comparable-store sales growth rising just 1%, with a 2% decline in transactions, down from 6% sales growth the prior Q1.

CFO Patrick Grismer did what CEO Kevin Johnson could not, admitting, “we have to acknowledge that competition is intensifying.”

Luckin Coffee burned through more than $100 million in cash in 2018, and like the prototypical tech company, will burn more cash to intensify competition with Starbucks.

I predict they will head further into deeper coffee discounts to snatch market share.

Other possible pain points for Starbucks that Qian could exploit are more subsidized deliveries which could continue for another “3-5 years” but could be extended if need be.

Qian is content with her model, stating she is “in no rush to make a profit,” signaling convenient access to a trove of generous debt instruments.

The best-case scenario in 2019 is that Starbucks' profit margins shrink or stagnate in China, the worst case, they lose significant Chinese market share and tier 1 city franchises continue to cannibalize revenue.

Starbucks' golden years in China are over and you can thank technology for offering a model to compete with them.

If Starbucks' shares continue moving up, it won’t be for much longer.

Global Market Comments

April 3, 2019

Fiat Lux

Featured Trade:

(WHO WILL BE THE NEXT FANG?)

(FB), (AMZN), (NFLX), (GOOGL), (AAPL),

(BABA), (TSLA), (WMT), (MSFT),

(IBM), (VZ), (T), (CMCSA), (TWX)

FANGS, FANGS, FANGS! Can’t live with them but can’t live without them either.

I know you’re all dying to get into the next FANG on the ground floor, for to do so means capturing a potential 100-fold return, or more.

I know because I’ve done it four times. The split adjusted average cost of my Apple shares is only 25 cents compared to today’s $174, so you can understand my keen interest. My average on Tesla is $16.50.

Uncover a new FANG and the riches will accrue rapidly. Facebook (FB), Amazon AMZN), Netflix (NFLX), and Alphabet (GOOGL) didn’t exist 25 years ago. Apple (AAPL) is relatively long in the tooth at 40 years. And now all four are in a race to become the world’s first trillion-dollar company.

One thing is certain. The path to FANGdom is shortening. It took Apple four decades to get where it is today, Facebook did it in one. As Steve Jobs used to tell me when he was running both Apple and Pixar, “These overnight successes can take a long time.”

There is also no assurance that once a FANG always a FANG. In my lifetime, I have seen far too many Dow Average components once considered unassailable crash and burn, like Eastman Kodak (KODK), General Electric (GE), General Motors (GM), Sears (SHLD), Bethlehem Steel, and IBM (IBM).

I established in an earlier piece that there are eight essential attributes of a FANG, product differentiation, visionary capital, global reach, likeability, vertical integration, artificial intelligence, accelerant, and geography.

We are really in a “What have you done for me lately” world. That goes for me too. All that said, I shall run through a short list for you of the future FANG candidates we know about today.

Alibaba (BABA)

Alibaba is an amalgamation of the Chinese equivalents of Amazon, PayPal, and Google all sewn together. It accounts for a staggering 63% of all Chinese online commerce and is still growing like crazy. Some 54% of all packages shipped in China originate from Alibaba.

The juggernaut has over half billion active users, and another half billion placing orders through mobile phones. It is a master of AI and B2B commerce. There is nothing else like it in the world.

However, it does have some obvious shortcomings. Its brand is almost unknown in the US. It has a huge problem with fakes sold through their sites.

It also has an ownership structure for foreign investors that is byzantine, to say the least. It is a contractual right to a share of profits funneled through a PO box in the Cayman Island. The SEC is interested, to say the least.

We also don’t know to what extent founder Jack Ma has sold his soul to the Beijing government. It’s probably a lot. That could be a problem if souring trade relations between the US and the Middle Kingdom get worse, a certainty with the current administration.

Tesla (TSLA)

Before you bet on a new startup breaking into the Detroit Big Three, go watch the movie “Tucker” first. Spoiler Alert: It ends in tears.

Still, Tesla (TSLA) has just passed the 270,000 mark in the number of cars manufacturered. Tucker only got to 50.

Having led my readers into the stock after the IPO at $16.50, I am already pretty happy with this company. Owning three of their cars helps too (two totaled). But Tesla still has a long way to go.

It all boils down to the success of the $35,000, 200-mile range Tesla 3 for which it already has 500,000 orders. So far so good.

It’s all about scale. If it can produce these cars in sufficient numbers, it will take over the world and easily become the next FANG. If it can’t, it won’t. It’s that simple.

To say that a lot is already built into the share price would be an understatement. Tesla now trades at ten times revenues compared to 0.5 for Ford (F) and (General Motors (GM). That’s a relative overvaluation of 20:1.

Any of a dozen competing electric car models could scale up with a discount model before they do, such as the similarly priced GM Bolt. But with a ten-year lead in the technology, I doubt it.

It isn’t just cars that will anoint Tesla with FANG sainthood. The firm already has a major presence in rooftop solar cell installation through Solar City, utility sized solar plants, industrial scale battery plants, and is just entering commercial trucks. Consider these all seeds for FANGdom.

One thing is certain. Without Tesla, there wouldn’t be s single mass-market electric car on the road today.

For that, we can already say thanks.

Uber

In the blink of an eye, ride sharing service Uber has become essential for globe-trotting travelers such as myself.

Its 2 million drivers completely disrupted the traditional taxi model for local transportation which remains unchanged since the days of horses and buggies.

That has created the first $75 billion of enterprise value. It’s what’s next that could make the company so interesting.

It is taking the lead in autonomous driving. It could also replace FeDex, UPS, DHL, and the US post office by offering same day deliveries at a fraction of the overnight cost.

It is already doing this now with Uber Foods which offers immediate delivery of takeouts (click here if you want lunch by the time you finish reading this piece.)

UberCopters anyone? Yes, it’s already being offered in France and Brazil.

Uber has the potential to be so much more if it can just outlive its initial growing pains.

It is a classic case of the founder being a terrible manager, as Travis Kalanick has lurched from one controversy to the next. The board finally decided he should spend much time on his new custom built 350-foot boat.

Its “bro” culture is notorious, even in Silicon Valley.

It is also getting enormous pushback from regulators everywhere protecting entrenched local interests. It has lost its license in London, the only place in the world that offered a decent taxi service pre-Uber. Its drivers are getting beaten up in Paris.

However, if it takes advantage of only a few of the doors open to it, status as a FANG beckons.

Walmart (WMT)

A few years ago, I was heavily criticized for pointing out that half the employees at my local Walmart (WMT) were missing their front teeth. They have since received a $2 an hour's pay raise, but the teeth are still missing. They don’t earn enough money to get them fixed.

The company is the epitome of bricks and mortar in a digital world with 12,000 stores in 28 countries. It is the largest private employer in the US, with 1.4 million workers, mostly earning minimum wage.

The Walmart customer is the very definition of the term “late adopter.” Many are there only because unlike Amazon, Wal-Mart accepts cash and Food Stamps.

Still, if Walmart can, in any way, crack the online nut, it would be a turbocharger for growth. It moved in this direction with the acquisition of Jet.com for $3 billion, a cutting-edge e-commerce firm based in Hoboken, NJ.

However, this remains a work in progress. Online sales account for only 4% of Walmart’s total. But they could only be a few good hires at the top away from success.

Microsoft (MSFT)

Talk about going from being the 800-pound gorilla to an 80 pound one, and then back to 800 pounds.

I don’t know why Microsoft (MSFT) lost its way for 15 years, but it did. Blame Bill Gates’s retirement from active management and his replacement by his co-founder Steve Ballmer.

Since Ballmer’s departure in 2014, the performance of the share price has been meteoric, rising by some 125% over the past two years.

You can thank the new CEO Satya Nadella who brought new vitality to the job and has done a complete 180, taking Microsoft belatedly into the cloud.

Microsoft was never one to take lightly. Windows still powers 90% of the world’s PCs. No company can function without its Office suite of applications (Word, Excel, and PowerPoint). SQL Server and Visual Studio are everywhere.

That’s all great if you want to be a public utility, which Microsoft shareholders don’t.

LinkedIn, the social media platform for professionals, could be monetized to a far greater degree. However, specialization does come at the cost of scalability.

It seems that the future is for Microsoft to go head to head against next door neighbor Amazon (AMZN) for the cloud services market while simultaneously duking it out with Alphabet (GOOGL).

My bet is that all three win.

Airbnb

This is another new app that has immeasurably changed my life for the better. Instead of cramming myself into a hotel suite with a wildly overpriced minibar for $600 a night, I get a whole house for $300 anywhere in the world, with a new local best friend along with it.

Overnight, Airbnb has become the world’s largest hotel chain without actually owning a single hotel. At its latest funding round in 2017, it was valued at $31 billion.

The really tricky part here is for the firm to balance out supply and demand in every city in the world at the same time. It is also not a model that lends itself to vertical integration. But who knows? Maybe priority deals with established hotels are to come.

This is another firm that is battling local regulation, that great barrier to technological innovation. None other than its home town of San Francisco now has strict licensing requirements for renters, a 30 day annual limitation, and a $1,000 a day fine for offenders.

The downtowns of many tourist meccas like Florence, Italy and Paris, France have been completely taken over by Airbnb customers, driving rents up and locals out.

IBM (IBM)

There was a time in my life when IBM was so omnipresent we thought like the Great Pyramids of Egypt it would be there forever. How times change. Even Oracle of Omaha Warren Buffet became so discouraged that he recently dumped the last of his entire five-decade long position.

A recent 20 consecutive quarters of declining profits certainly hasn’t helped Big Blue’s case. It is one of the only big technology companies whose share price has gone virtually nowhere for the past two years.

IBM’s problem is that it stuck with hardware for too long. An entrenched bureaucracy delayed its entry into services and the cloud, the highest growth areas of technology.

Still, with some $80 billion in annual revenues, IBM is not to be dismissed. Its brand value is still immense. It still maintains a market capitalization of $144 billion.

And it has a new toy, Watson, the supercomputer named after the company’s founder, which has great promise, but until now has remained largely an advertising ploy.

If IBM can reinvent itself and get back into the game, it has FANG potential. But for the time being, investors are unimpressed and sitting on their hands.

The Big Telecom Companies

My final entrant in the FANGstakes would be any combination of the four top telecommunication companies, Verizon (VZ), AT&T (T), Comcast (CMCSA), and Time Warner (TWX), which now control a near monopoly in the US.

There is a reason why the administration is blocking the AT&T/Time Warner merger, and it is not because these companies are consistently cited in polls as the most despised in America. They are trying to stop the creation of another hostile FANG.

Still, if any of the big four can somehow get together, the consequences would be enormous. Ownership of the pipes through which the modern economy courses bestows great power on these firms.

And Then….

There is one more FANG possibility that I haven’t mentioned. Somewhere, someplace, there is a pimple-faced kid in a dorm room thinking up a brand-new technology or business model that will take the world by storm and create the next FANG.

Call me crazy, but I have been watching this happen for my entire life.

I want to thank my friend, Scott Galloway, of New York University’s Stern School of Business, for some of the concepts in this piece. His book, “The Four” is a must read for the serious tech investor.

Creating the Next FANG?

Mad Hedge Technology Letter

March 12, 2019

Fiat Lux

Featured Trade:

(FIREEYE’S LAST LINE OF DEFENSE),

(FEYE), (MSFT), (AMZN), (GOOGL), (ORCL), (EFX), (IBM)

A potential cataclysmic threat potentially wreaking havoc to our financial system is no other than cybercrime – that is one of the few gems that Fed Chair Jerome Powell delivered to the American public in a historic interview with 60 Minutes this past weekend.

Powell has even gone on record before claiming that Congress should do “as much as possible (against cybercrime), and then double it.”

The Fed Chair clearly has intelligence that retail investors wish they could get their hands on.

Digital nefarious attacks have been all the rage resulting in public blowups at Equifax (EFX) and North Korea’s state-sponsored hack on International Business Machines Corporation (IBM) just to name a few.

At the bare minimum, this means that cybersecurity solution companies will be the recipients of a gloriously expanding addressable market.

Powell’s testimony to the public was timely as it provides the impetus for investors to look at cybersecurity firms that will actively forge ahead and protect domestic business from these lurking threats.

Considering a long-term investment in FireEye Inc. (FEYE) at these beaten down prices could unearth value.

For all the digital novices, FireEye offers cybersecurity solutions allowing organizations to pre-emptively plan, prevent, respond to, and remediate cyber-attacks.

It offers vector-specific appliance, virtual appliance, and a smorgasbord of cloud-based solutions to detect and thwart indistinguishable cyber-attacks.

The company deploys threat detection and preventative methods including network security products, email security solutions, and endpoint security solutions.

And when you marry this up with my 2019 underlying thesis of the year of the enterprise software subscription, this company is on the verge of a breakout.

Last year was a year full of milestones for the company with the firm achieving non-GAAP profitability for the full year for the first time and generating positive operating and free cash flow for the full year.

The company was able to attract new business by adding over 1,100 new customers.

The cloud is where the company is betting all their chips and crafting the optimal subscription-as-a-service (SaaS) product is the engine that will propel the company’s shares higher.

The heart of their cloud initiative relies on Helix - a comprehensive detection and response platform designed to simplify, integrate and automate security operations.

This intelligence-led approach fuses innovative security technologies, nation-grade FireEye Threat Intelligence and world-renowned expertise from FireEye Mandiant into FireEye Helix.

By enhancing the endpoint products and email protection, sales of both products exploded higher by double digits YOY as FireEye successfully displaced incumbent vendors and legacy technology to the delight of shareholders.

As a result, the firm’s pipeline of opportunities continues to build.

As for network security, FireEye plans to extend the reach of their market-leading advanced threat protection capabilities further into the cloud with protection specifically aimed for cloud heavyweights Microsoft (MSFT) Azure, Amazon Web Services (AWS), Google (GOOGL) and Oracle (ORCL) Cloud.

They are collaborating with these major cloud providers on hybrid solutions that integrate seamlessly with their technologies so FireEye solutions will easily snap into a customer's cloud deployments.

Cloud subscriptions and managed services were the ultimate breakout performer highlighting the successful outsized pivot to (SaaS) revenue.

This segment increased 31% sequentially and 12% YOY, highlighting underlined strength in the segments of managed defense, standalone threat intelligence, Helix subscriptions, and cloud email solution.

The furious growth was achieved even though Q4 2017 billings included a $10 million plus transaction and if this deal is excluded, cloud subscriptions and managed services would have grown more than 30% YOY in Q4 2017 demonstrating the hard bias to the cloud has been highly instrumental to its success.

Recurring billings expanded 12% YOY, a small bump in acceleration from 11% in Q3, but if you remove that big deal in Q4 '17, recurring billings grew over 20% YOY in Q4 2018.

The growing chorus of product satisfaction can be found in the customer retention rate of 90%.

Transaction volume was at record levels for both deals greater than $1 million and transactions less than $1 million, signaling not only that customer renewals are expanding, but also explosion of new revenue streams captured by FireEye is aiding the top line.

This story is all about the recurring revenue and I expect that narrative to perpetuate throughout 2019 as an overarching theme to the strength of the firm’s revenue drivers.

The 10% billings growth last quarter paints a more honest trajectory of the true growth proposition for FireEye.

I believe the 6%-to-7% revenue guide for fiscal 2019 is down to the accounting technicals manifesting in the appliance revenue that is fading from the overall story.

The solid billings growth underpinning the overall business meshing with diligent expense control is conjuring up a massive amount of operating leverage.

Shares are undervalued and offer an attractive risk versus reward proposition.

If the company delivers on its core growth outlook, which I fully expect them to do plus more, shares should climb over $20 barring any broad-based market meltdowns.

I am bullish FireEye and urge readers to wait for shares to settle before putting new money to work.

Corporate earnings are up big! Great!

Buy!

No, wait!

The economy is going down the toilet!

Sell!

Buy! Sell! Buy! Sell!

Help!

Anyone would be forgiven for thinking that the stock market has become bipolar.

According to the Commerce Department’s Bureau of Economic Analysis, the answer is that corporate profits account for only a small part of the economy.

Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly or are too small to have much of an impact.

Wages and salaries are in a three-decade-long decline. Interest and investment income are falling because of the ultra-low level of interest rates. Farm incomes are at a decade low, thanks to the China trade war, but are a tiny proportion of the total, and agricultural prices have been in a seven-year bear market.

Income from non-farm unincorporated business, mostly small business, is unimpressive.

It gets more complicated than that.

A disproportionate share of corporate profits is being earned overseas.

So, multinationals with a big foreign presence, like Apple (AAPL), Intel (INTC), Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes.

They really get to have their cake and eat it too. Many of their business activities are contributing to foreign GDPs, like China’s, far more than they are here.

Those with large domestic businesses, like retailers, earn less but pay more in tax as they lack the offshore entities in which to park them.

The message here is to not put all your faith in the headlines but to look at the numbers behind the numbers.

Caveat emptor. Buyer beware.

Mad Hedge Technology Letter

February 7, 2019

Fiat Lux

Featured Trade:

(THE DEATH OF THE COLLEGE DEGREE),

(GOOGL), (IBM), (AAPL), (BABA), (BIDU)

If you’re an educator not at a top 25 American university, you might want to stop reading right now.

Disruption.

You’re either on the right or wrong side of it.

I’ve detailed numerous subsets of the economy and society that have been transformed by sharp shifts in technological innovation.

But the one industry that has stealthily moved into the heart and center of technological disruption is education.

For centuries, universities and higher learning institutions had a stranglehold on critical information required to successfully perform in the cutting-edge knowledge economy of those times.

Then on September 15, 1997, a mere 21 years ago, Google search launched its free services to the world and grabbed the monopoly of information away from the college system.

This website effectively caused the cost of information to crater to zero and its free website is ranked #1 as of February 2019 with over 4.5 billion monthly active users.

The ensuing 21 years has been a renaissance in the ability to distribute information propelled by this one platform, and the result is that billions have the ability to study and read up on what they want and when they want.

The ability to learn for free combined with a tight labor market is a promising landscape for job seekers, with analysts forecasting more opportunities for professionals without a degree.

Job-search site Glassdoor amassed a list of various employers no longer bound by requiring applicants to possess a 4-year bachelor’s degree.

These firms aren’t your second-rate companies either made up of gold standard workplaces such as Google, Apple, and IBM.

In 2017, IBM's vice president of talent Joanna Daley confided that about 15% of IBM’s new hires don't have a four-year bachelor qualification.

She emphasizes hands-on experience through coding boot camp or industry-related vocational classes as explicit criteria to get hired.

This development bodes poorly for the future of universities and boosts the prospects of alternative education.

Online college offers working adults ample flexibility in furthering their education.

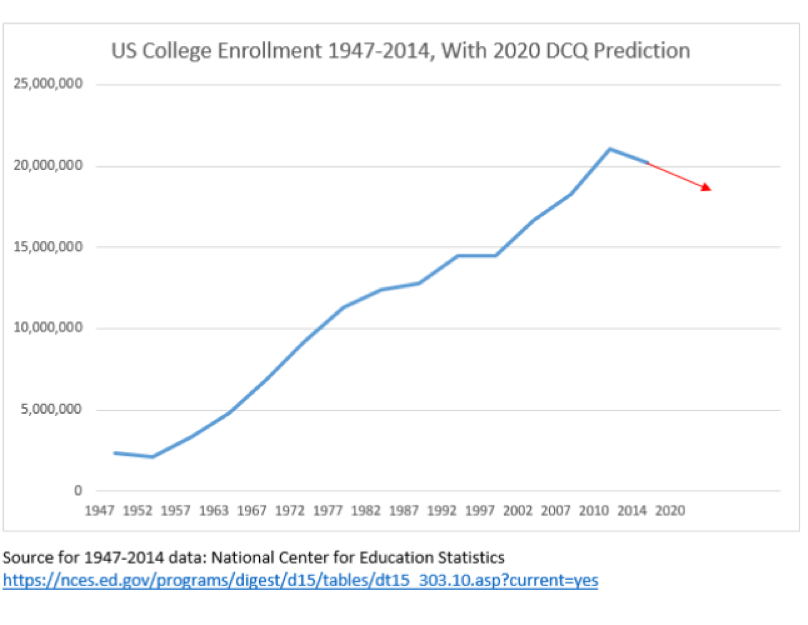

According to the most recent federal statistics from 2016, roughly one out of every three, or 6.3 million college students learned online.

Even though online courses are becoming more widespread, the best and brightest aren’t attending these schools.

However, it did hijack the marginal student that was on the fence for a 4-year university and brought them into the orbit of for-profit online courses and the revenues that came with it.

That was the first stage of online forces imposing financial pressure on the education marketplace.

Now analysts are discovering the second major trend with higher rated students opting out of the university system altogether.

In many cases, a 4-year university degree is a bad value proposition.

Why is that?

Costs.

In a capitalistic economy that lives and dies by the mantra of buy low and sell high – universities seem to be getting sold short lately.

The exorbitant costs to obtain a 4-year degree has led to an outsized student debt bubble and removed the mystique of this once treasured qualification.

A growing chorus of bipartisan voices has pigeonholed student debt as a major problem across the country.

In the previous presidential election, Democratic candidate Bernie Sanders called this situation “outrageous” as national student debt has spiraled out of control to the amount of $1.5 trillion.

This has been a terrible commercial for the younger generations to follow in the footsteps of the indebted Millennial generation.

And with Generation Z tech savvy at building stand-alone firms buttressed by Instagram and YouTube platforms, why go to college anymore?

Or to nail one of those jobs developing iPhones in Cupertino, why not take a few coder boot camps and self-develop a portfolio impressive enough to score an Apple interview?

The bottom line is that there are workarounds for a fraction of the price.

And because tech firms have outpaced analog companies in salaries and hiring for the past two decades, there is an outsized bias on compiling technical skills that will lead a candidate down a path to a salary of over $100,000 quicker than a 4-year degree can.

Not many other industries can claim the same.

The cracks are beginning to reveal themselves in the overall university apparatus.

Universities had years of record revenue that they reinvested into the system to enhance programs, staff, buildings, stadiums, and infrastructure.

The financial catalyst was the rise of the Chinese college student.

The latest statistics nailed the number of Chinese nationals in America studying for 4-year degrees at over half a million.

Many of those were trained up with engineering-related degrees and bolted back home to find jobs at Baidu (BIDU), Tencent, or Alibaba (BABA) powering Chinese Inc.

However, the drop off in demographics from young Chinese and Americans are forcing universities to fight for a shallower pool of candidates with less attractive degrees relative to the value of degrees of past generations.

The second-tier universities are hardest hit with examples galore.

Alcorn State University in Mississippi saw a dramatic 69.45% decrease in applications in 2018 and its rural location didn’t help either.

Alabama State University is feeling the pinch with a 33.06% drop in application in recent years.

If you thought the University of New Orleans was clawing its way back to relevancy after Hurricane Katrina, you are mistaken with its 38.23% drop in applications.

Military schools haven’t been spared either with applications to The United States Air Force Academy crashing 28.12% over the past ten years.

A confluence of deadly trends is about to beset the university system and schools will likely go bust.

Technology is giving a reason for students to bypass the system while also speeding up the financial timebombs many universities are about to confront.

Then we must ask ourselves, will universities even exist in the future?

Probably, but perhaps just the top 25 elite schools that are still worth the high costs.

Mad Hedge Technology Letter

November 1, 2018

Fiat Lux

Featured Trade:

(LOOK AT ZENDESK FOR YOUR NEXT TEN BAGGER)

(ZEN), (RHT), (AMZN), (MSFT), (CRM), (IBM), (SNAP)

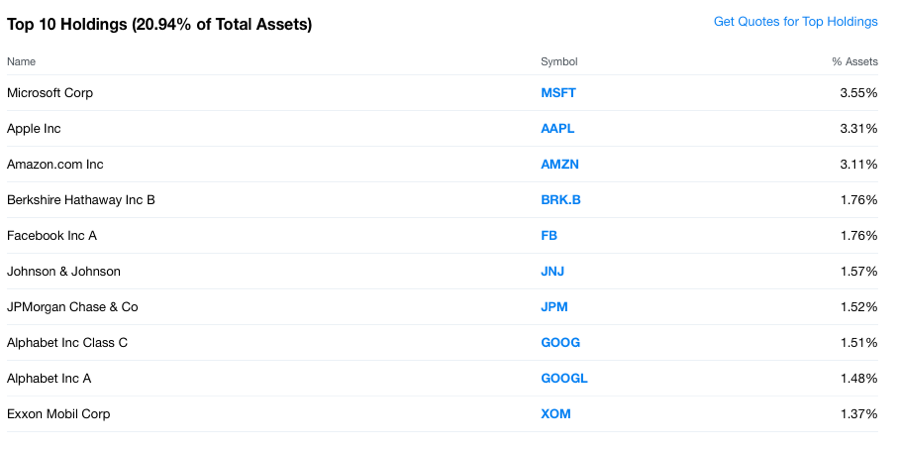

S&P Top 10 Holdings 3-4-2019

S&P Top 10 Holdings 3-4-2019