Mad Hedge Technology Letter

April 26, 2018

Fiat Lux

Featured Trade:

(THE SMALL AI PLAY YOU'VE NEVER HEARD OF),

(BOX), (GOOGL), (MSFT), (AMZN), (IBM)

Mad Hedge Technology Letter

April 26, 2018

Fiat Lux

Featured Trade:

(THE SMALL AI PLAY YOU'VE NEVER HEARD OF),

(BOX), (GOOGL), (MSFT), (AMZN), (IBM)

The cloud segment of technology is hotter than hot, and as this sector starts to trade at a big premium, investors will have to look further down the chain of command to find a reasonable deal.

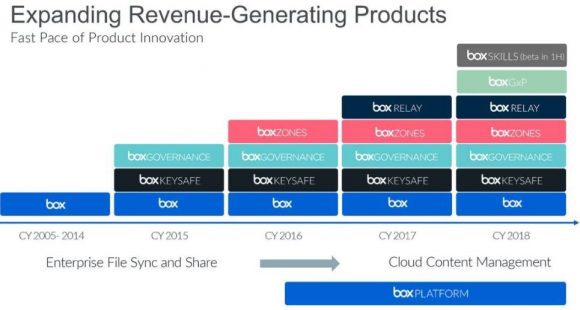

An up-and-coming cloud service Box (BOX) has gone undiscovered and is in position to seize a larger share of the cloud market moving forward.

The firm is led by CEO Aaron Levie who dropped out of my old alma mater USC in 2005 to start a cloud company with acting CFO and childhood friend Dylan Smith.

Last quarter was record-setting for Box, and it had a number of significant six- and seven-digit deals. Keep in mind Box's revenues are paltry compared to the behemoths that run this industry.

The platform has seen gradual success from all corners of the business world with various businesses from insurance claims processors to wealth advisors who use Box as a back-end platform.

Health care is another industry deploying the Box platform to aid and develop cloud services for patients.

In a general sense, the beauty of the cloud is the propensity to adapt to any company that is willing to go digital.

Even though many legacy companies are not natively digital, the cloud can twist and contort to fit the customers' needs.

Levie raised some compelling arguments for the continued tech momentum stating that imminent regulation in Europe through General Data Protection Regulation (GDPR) will act as a "broader tailwind in compliance and security efforts."

Box also announced a "readiness (GDPR) package" revealing that tech companies have been planning for the regulation overhaul up to 18 months in advance.

Even though mass media sensationalism would lead investors to believe the threat of regulation is about to blindside this whole sector, the unrest has been bubbling up for quite some time allowing tech companies ample time to get their houses in order.

Box actually sees the genesis of GDPR as a critical part of the cloud adoption process.

As dinosaur systems become outdated, a sense of safety reinforced by strong cybersecurity protection, strong privacy rules, and content compliance will nudge companies to head for the cloud like a drunk sailor to a pub.

Legacy platforms are the most susceptible to cyber-criminals and rogue hackers.

The analog defense is no match for sophisticated cyber-espionage, and GDPR will be another "driving force" behind the macro-migration shift to the cloud, just based on the security aspect alone.

Another pearl of wisdom offered by Box is that the bulk of clients requiring cloud products are integrating Microsoft Office 365.

This software acts as a lynchpin to any cloud service.

I must confess that I am writing this story on Microsoft Office 365 now, and most businesses cannot function without the dizzying array of Excel, PowerPoint, and Word.

Box has a strong relationship with Microsoft and has incisive insight into the synergies the cloud industry spins off.

The integration of Office 365 has complemented the Azure cloud with tighter cohesiveness.

The school of thought is the collective cloud industry is a $50 billion per year market and growing, offering smaller firms healthy growth levers to advance at the same time that the Microsofts (MSFT) and Amazons (AMZN) overperform.

At the Sohn Investment Conference in New York, Chamath Palihapitiya, a venture capitalist and former Facebook executive, extolled Box as a great way to play Artificial Intelligence (AI).

The shares spiked almost 13% upon his adulation.

A recent completed survey showed 66% of business leaders feel the pace of digitization must pick up in their own offices.

The speed of innovation is something that keeps most CEOs up at night. Wake up tomorrow and it is possible their core products could be outdated or disrupted by a new Amazon threat.

That is the world we live in now.

Only 42% of CIOs admitted they have a digital strategy. And of those digital strategies, they are mostly digital second or third, not digital first, blueprints.

In the same PricewaterhouseCoopers (PwC) survey, companies conceded that only 40% of IT teams are able to pursue the newest innovations with adopting specific operational needs in mind.

The micro-environment harbors the same bullishness as the macro-factors.

Box is hitting all the right notes.

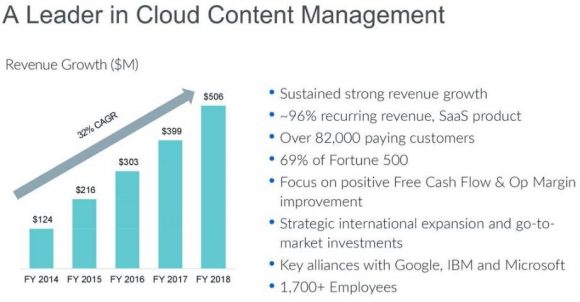

Revenue is advancing at a 24% per year clip, and annual revenue surpassed the half a billion mark.

Box has indicated it expects to cross the $1 billion annual revenue threshold sometime in mid- to late 2021, giving the company more than three years to double revenue.

Recent reports support Box's growth trajectory.

About 60% of revenue derives from firms that employ more than 2,000 workers, highlighting Box's propensity to emphasize enterprise cloud development instead of small individual users.

Working with larger companies gives Box the opportunity to cross-sell more powerful add-ons, delivering a net expansion rate of 14%.

Migrating to a new cloud platform is incredibly sticky boosting retention rates. Box's churn rate is flourishing with a best of breed 4% per year. The key to expediting cloud success is quickening its pace of new product rollout.

Box attempts to give exactly what customers need with a spate of new concoctions.

Box GxP is a new product calibrated around life science companies. The Box GxP compliance is up to date with FDA regulations. And, Box has the ability to retire legacy ECM (Enterprise Content Management) systems.

This new service has experienced solid traction around the world as we head toward a world where legacy software becomes obsolete.

The second new offering is Box Skills, still in beta mode, which is a part of Box's artificial intelligence strategy.

Box is platform neutral allowing in-house architecture to support partnerships with Google, Microsoft, Amazon, and IBM to nail down third-party cloud tools that Box customers need.

Box Skills is a framework that brings the best machine learning innovation to content securely stored in Box.

This is managed through artificial intelligence, which automatically contextualizes images through detection protocols. Text recognition is automated for the benefit of the user, too.

Audio intelligence renders text transcripts and detects topics that can be searched in Box to locate an audio file by words or topic.

Video intelligence offers transcription, topic detection, and facial recognition allowing users to jump around video files in a non-linear fashion.

Palihapitiya effectively gave Box a free commercial to the tech investing world. His bull thesis for Box squarely centers around its AI innovations, specifically Box Skills.

The last new service to market is Box Transform, which is the advanced consulting arm of Box.

The goal of Transform is to arrange a concierge-like Box advisor that can help companies accelerate digital transformation throughout an organization while unlocking efficiencies and productivity for employees.

This service originated from Box's consulting advanced professional services team and will give Box another growth lever. Companies such as Red Hat and Intel have made the consultant- and support-side of the business a robust part of their organizations.

Impeding growth is the cutthroat competition in this space with Amazon, Microsoft, and Google (GOOGL).

However, margins remain strong at 75.5% last quarter, and Box expects margins to slightly dip around 74% this year.

Box has found a warm welcome for its newer products, deriving almost 70% of its new deals from fresh cloud offerings.

Partners are also a big source of new deals comprising more than half the deals over $100,000.

Specifically, IBM (IBM) made up a swath of its larger deals. In a sense, competitors are not really competitors.

They are frenemies. They compete against each other yet innovate and do deals together.

The core growth is supplemented by existing customers that are the best source of extra marginal revenue.

In short, once firms are firmly lodged on a platform, they buy everything on that platform.

Enter a supermarket, and odds are if goods are purchased, the receipt will be from the entered supermarket.

Box is entirely leveraged toward mid-sized and large enterprise business. That is where it makes its money.

The emphasis on large players boosts the ACV (Average Contract Value), which is regarded as a sacrosanct metric for Box.

The amount of data created in 2017 was more data created in the past 5,000 years. In the next five years, data volume with grow by 800%.

Box has continually positioned itself as the firm that can extract a staggering amount of unrealized value locked away in the nooks and crannies of legacy models.

Box is a great long-term hold as these diminutive cloud assets become more valuable by the day.

_________________________________________________________________________________________________

Quote of the Day

"Television won't be able to hold onto any market it captures after the first six months. People will soon get tired of staring at a plywood box every night." - said Darryl F. Zanuck, co-founder of Twentieth Century-Fox Film Corp.

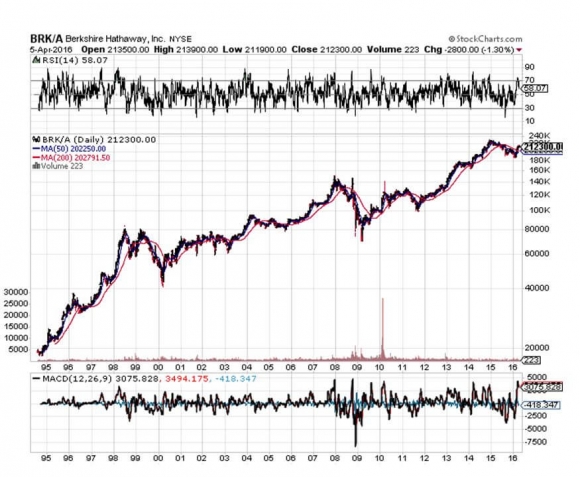

Sometime in the early 1970?s, a friend of mine said I should take a look at a stock named Berkshire Hathaway (BRKA) run by a young stud named Warren Buffett.

I thought, ?Why the hell should I invest in a company that makes sheets??

After all, the American textile industry was in the middle of a long trek toward extinction that began in the 1920?s, and was only briefly interrupted by the hyper prosperity of WWII. The industry?s travails were simply an outcome of ever rising US standards of living, which pushed wages, and therefore costs, up.

It turns out that Warren Buffett made a lot more than sheets. However, he is not a young stud anymore, just an old one, like me.

Since then, Warren?s annual letter to investors has been an absolute ?must read? for me when it is published every spring.

It has been edited for the past half century by my friend, Carol Loomis, who just retired after a 60-year career with Fortune magazine. (I never wrote for them because their freelance rates were lousy).

Witty, insightful, and downright funny, I view it as a cross between a Harvard Business School seminar and a Berkeley anti establishment demonstration. You will find me lifting from it my ?Quotes of the Day? for the daily newsletter over the next several issues. There are some real zingers.

And what a year it has been!

Berkshire?s gain in net worth was $18.3 billion, which increased the share value by 8.3%, and today, the market capitalization stands at an impressive $343.4 billion. (Sorry Warren, but I clocked 30% last year, eat your heart out).

The shares are not for small timers, as one now costs $214,801, and no, they don?t sell half shares. This compares to a 1965 per share market value of $23.80, and is why the media are always going gaga over Warren Buffett.

If you?re lazy and don?t want to do the math, that works out to a compound annualized return of an eye popping 21.6%. This is why guessing what Warren is going to do next has become a major cottage industry (Progressive Insurance anyone?).

Warren brought in these numbers despite the fact that its largest non-insurance subsidiary, the old Burlington Northern Santa Fe Railroad (BNSF) suffered an awful year.

Extensive upgrades under construction and terrible winter weather disrupted service, causing the railroad to lose market share to rival Union Pacific (UNP).

I was kind of pissed when Warren bought BNSF in 2009 for a blockbuster $44 billion, as it was long my favorite trading vehicles for the sector. Since then, its book value has doubled. Typical Warren.

Buffett plans to fix the railroad?s current problems with $6 billion in new capital investment this year, one of the largest single capital investments in American history. Warren isn?t doing anything small these days.

Buffett also got a hickey from his investment in UK supermarket chain Tesco, which ran up a $444 million loss for Berkshire in 2014. Warren admits he was too slow in getting out of the shares, a rare move for the Oracle of Omaha, who rarely sells anything (which avoids capital gains taxes).

Warren increased his investment in all of his ?Big Four? holdings, American Express (AXP), Coca-Cola (KO), IBM (IBM), and Wells Fargo (WFC).

In addition, Berkshire owns options on Bank of America (BAC) stock, which have a current exercise value of $12.5 billion (purchased the day after the Mad Hedge Fund Trader issued a Trade Alert on said stock for an instant 300% gain on the options).

The secret to understanding Buffett picks over the years is that cash flow is king.

This means that he has never participated in the many technology booms over the decades, or fads of any other description, for that matter.

He says this is because he will never buy a business he doesn?t intrinsically understand, and they didn?t offer computer programming as an elective in high school during the Great Depression.

No doubt this has lowered his potential returns, but with the benefit of much lower volatility.

That makes his position in (IBM) a bit of a mystery, the worst performing Dow stock of the past two years. I would much rather own Apple (AAPL) myself, which also boasts great cash flow, and even a dividend these days (with a 1.50% yield).

Warren will be the first to admit that even he makes mistakes, sometimes, disastrous ones. He cites his worst one ever as a perfect example, his purchase of Dexter Shoes for $433 million in 1993. This was right before China entered the shoe business as a major competitor.

Not only did the company quickly go under, he exponentially compounded the error through buying the firm with an exchange of Berkshire Hathaway stock, which is now worth a staggering $5.7 billion.

Ouch, and ouch again!

Warren has also been mostly missing in action on the international front, believing that the mother load of investment opportunities runs through the US, and that its best days lie ahead. I believe the same.

Still, he has dipped his toe in foreign waters from time to time, and I was sometimes quick to jump on his coattails. A favorite of mine was his purchase of 10% of Chinese electric car factory BYD (BYDDF) in 2009, where I have captured a few doubles over the years.

Buffett expounds at great length the attractions of the insurance industry, which today remains the core of his business. For payment of a premium up front, the buyers of insurance policies receive a mere promise to perform in the future, sometimes as much as a half century off.

In the meantime, Warren can invest the money any way he wants. The model has been a real printing press for Buffett since he took over his first insurer in 1951, GEICO.

Much of the letter promotes the upcoming shareholders annual meeting, known as the ?Woodstock of Capitalism?.

There, the conglomerate?s many products will be for sale, including, Justin Boots (I have a pair), the gecko from GEICO (which insures my Tesla S-1), and See?s Candies (a Christmas addiction, love the peanut brittle!).

There, visitors can try their hand at Ping-Pong against Ariel Hsing, a 2012 American Olympic Team member, after Bill Gates and Buffett wear her down first.

They can try their hand against a national bridge champion (don?t play for money). And then there is the newspaper-throwing contest (Buffett?s first gainful employment).

Some 40,000 descend on remote Omaha for the firm?s annual event. All flights to the city are booked well in advance, with fares up to triple normal rates.

Hotels sell out too, and many now charge three-day minimums (after Warren, what is there to do in Omaha for two more days other than to visit PayPal?s technical support?). Buffett recommends Airbnb as a low budget option (for the single shareholders?).

I was amazed to learn that Berkshire files a wrist breaking 24,100-page Federal tax return (and I thought mine was bad!). Add to this a mind numbing 3,400 separate state tax returns.

Overall, Berkshire holdings account for more than 3% of the total US gross domestic product, but a far lesser share of the government?s total tax revenues, thanks to careful planning.

Buffett ends his letter by advertising for new acquisitions and listing his criteria. They include:

(1) ?Large purchases (at least $75 million of pre-tax earnings unless the business will fit into one of our existing units),

(2) ?Demonstrated consistent earning power (future projections are of no interest to us, nor are ?turnaround? situations),

(3) ?Businesses earning good returns on equity while employing little or no debt,

(4) Managemen

t in place (we can?t supply it),

(5) Simple businesses (if there?s lots of technology, we won?t understand it),

(6) An offering price (we don?t want to waste our time or that of the seller by talking, even preliminarily, about a transaction when price is unknown).

Let me know if you have any offers.

To read the entire history of Warren Buffett?s prescient letters, please click here: http://www.berkshirehathaway.com/letters/letters.htm.

Corporate earnings are up big! Great!

Buy!

No wait!

The economy is going down the toilet!

Sell! Buy! Sell! Buy! Sell!

Help!

Anyone would be forgiven for thinking that the stock market has become bipolar.

According to the Commerce Department?s Bureau of Economic Analysis, the answer is that corporate profits accounts for only a small part of the economy.

Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly, or are too small to have much of an impact.

Wages and salaries are in a three decade long decline. Interest and investment income is falling, because of the ultra low level of interest rates. Farm incomes are up, but are a tiny proportion of the total. Income from non-farm unincorporated business, mostly small business, is unimpressive.

It gets more complicated than that.

A disproportionate share of corporate profits is being earned overseas. So multinationals with a big foreign presence, like Apple (AAPL), Intel (INTC), Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes.

They really get to have their cake, and eat it too. Many of their business activities are contributing to foreign GDP?s, like China?s, more than they are here. Those with large domestic businesses, like retailers, earn less, but pay more in tax, as they lack the offshore entities in which to park them.

The message here is to not put all your faith in the headlines, but to look at the numbers behind the numbers. Those who bought in anticipation of good corporate profits last month, got those earnings, and then got slaughtered in the marketplace.

Caveat emptor. Buyer beware.

While driving back from Lake Tahoe last weekend, I received a call from a dear friend who was in a very foul mood. He had bailed on all his equity holdings at the end of last year, fully expecting a market crash in the New Year.

Despite market volatility doubling, multinationals getting crushed by the weak euro and the Federal Reserve now signaling its first interest rate rise in a decade, here we are with the major stock indexes sitting at all time highs.

Why the hell are stocks still going up?

I paused for a moment as a kid driving a souped up Honda weaved into my lane of Interstate 80, cutting me off. Then I gave him my response, which I summarize below:

1) There is nothing else to buy. Complain all you want, but US equities are now one of the world?s highest yielding securities, with a lofty 2% dividend. That compares to one third of European debt offering negative rates and US Treasuries at 1.90%.

2) Oil prices have yet to bottom and the windfall cost savings are only just being felt around the world.

3) While the weak euro is definitely eating into large multinational earnings, we are probably approaching the end of the move. The cure for a weak euro is a weak euro. The worst may be behind for US exporters.

4) What follows a collapse in European economic growth? A European recovery, powered by a weak currency. This is why China has been on fire, which exports more to Europe than anywhere else.

5) What follows a Japanese economic collapse? A recovery there too, as hyper accelerating QE feeds into the main economy. Japanese stocks are now among the worlds cheapest. This is why the Nikkei Average hit a new 15-year high over the weekend, giving me yet another winning Trade Alert.

6) While the next move in interest rates will certainly be up, it is not going to move the needle on corporate P&L?s for a long time. We might see a ?% hike and then done, and that probably won?t happen until 2016. In a deflationary world, there is no room for more. At least, that?s what Janet tells me.

This will make absolutely no difference to the large number of corporates, like Apple (AAPL), that don?t borrow at all.

7) Technology everywhere is accelerating at an immeasurable pace, causing profits to do likewise. You see this in biotech, where blockbuster new drugs are being announced almost weekly.

See the new Alzheimer?s cure announced last week? It involves extracting the cells from the brains of alert 95 year olds, cloning them and then injecting them into early stage Alzheimer?s patients. The success rate has been 70%. That one alone could be worth $5 billion.

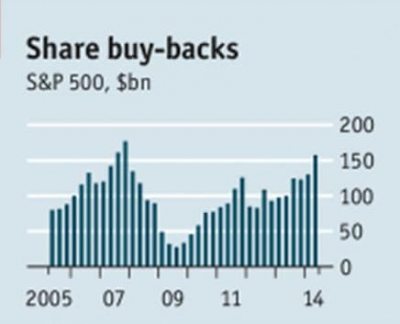

8) US companies are still massive buyers of their own stock, over $170 billion worth in 2014. This has created a free put option for investors for the most aggressive companies, like Apple (AAPL), IBM (IBM), Exxon (XOM), Wells Fargo (WFC), and Intel (INTC), the top five repurchasers. They have nothing else to buy either.

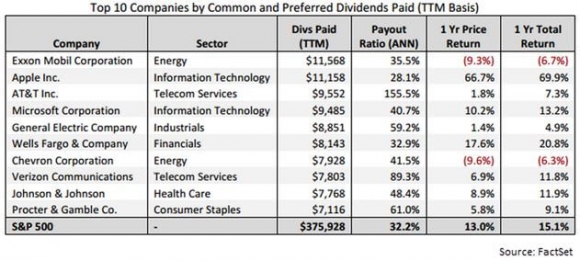

They are jacking up dividend payouts at a frenetic pace as well and are expected to return more than $430 billion in payouts this year (see chart below).

9) Oil will bottom in the coming quarter, if it hasn?t done so already. This will make the entire energy sector the ?BUY? of the century, dragging the indexes up as well. Have you noticed that Conoco Phillips (COP), Warren Buffets favorite oil company, now sports a stunning 4.70% dividend?

10) Ditto for the banks, which were dragged down by falling interest for most of 2015. Reverse that trade this year, and you have another major impetus to drive stock indexes higher.

My friend was somewhat set back, dazzled, and non-plussed by my long-term overt bullishness. He asked me if I could think on anything that might trigger a new bear market, or at least a major correction.

I told him to forget anything international. There is no foreign development that could damage the US economy in any meaningful way. No one cares.

On he other hand, I could think of a lot of possible scenarios that could be hugely beneficial for US stocks, like a peace deal with Iran, which would chop oil prices by another half.

The traditional causes of recessions, oil price and interest rate spikes, are nowhere on the horizon. In fact, the prices for these two commodities, energy and money, are headed lower and not higher, another deflationary symptom.

Then something occurred to me. Share prices have been going up for too long and need some kind of rest, weeks or possibly months. At a 17 multiple American stocks are not the bargain they were 6 years ago when they sold for 10X earnings. Those were the only thing I could think of.

But then those are the arguments for shifting money out of the US and into Europe, Japan, and China, which is what the entire world seems to be doing right now.

I have joined them as well, which is why my Trade Alert followers are long the Wisdom Tree Japan Hedged Equity ETF (DXJ) (click here for ?The Bull Case for Japanese Stocks?).

With that, I told my friend I had to hang up, as another kid driving a souped up Shelby Cobra GT 500, obviously stolen, was weaving back an forth in front of me requiring my attention.

Whatever happened to driver?s ed?

I am writing this to you from the ancient city of Bodrum on the southwest coast of Turkey. Coming here, I had to set my watch ahead ten hours, then back 3,000 years.

As I sit here on my balcony, a flotilla of yachts, both large and small, motor by with the Greek island of Kos hovering in the background in the haze. Smoke from the gurgling water pipes below waft in my direction.

The carnage in Syria goes on 400 miles to my east and worse in Iraq another 300 miles in the distance. The security forces are on a nervous alert and machine guns held by jumpy, sweating teenagers are everywhere. My five star hotel is eerily vacant, even though it is peak season, but the service is great.

Despite these ominous signs, I am happy to report that the industry beating performance of the Mad Hedge Fund Trader?s Trade Alert Service has punched through to a new all time high.

The total return for my followers so far in 2014 has reached 19.74%, compared to a far more feeble 1.4% for the Dow Average during the same period. June came in at a robust 4.32%.

I managed to pull this off during some of the most difficult trading conditions in market history. Turnover across all asset classes is hitting decade lows (see chart below), and volatility has crashed through the floor. Most of the rest of the hedge fund industry is getting destroyed.

The three and a half year return is now at an amazing 142.24%, compared to a far more modest increase for the Dow Average during the same period of only 36%.

That brings my averaged annualized return up to 39.7%. Not bad in this zero interest rate world. It appears better to reach for capital gains than the paltry yields out there.

This has been the profit since my groundbreaking trade mentoring service was first launched in 2010. Thousands of followers now earn a full time living solely from my Trade Alerts, a development of which I am immensely proud of.

Like most of the industry, I expected May and June to be poor months for risk assets. The market has had a tremendous run over the last two years, and the spring historically heralds a period of seasonal weakness.

Wrong!

One of the toughest things to do in this business is to admit you blew it, and then execute an immediate risk reversal in your portfolio.

In the end, the failure of the market to fall meant that it could only go up. We got additional help from month end window dressing, calming events in the Ukraine, and a 7:1 share split at Apple.

Another particularly vexing challenge is that the principal market driver has shifted from economics to geopolitics. The global economic recovery continues, but at a pace so modest that it hardly moves the needle on the volatility front.

The world is waiting to see whether the US can deliver a second half GDP growth rate of 4% per annum?.. or not.

In the meantime, a megalomaniac in Russia and terrorists in the Middle East are determining the short-term direction of asset prices. No hedge fund trader has any edge here, so calls on the coming price action are little more than educated guesses and wishing.

Good luck outperforming in that environment!

I played June predominantly from the long side, accumulating a basket of positions in old technology and traditional industrial names like IBM (IBM), Google (GOOGL), Caterpillar (CAT), and Microsoft (MSFT). I then opportunistically laid out hedging shorts in the S&P 500 (SPY) and the Treasury bond market (TLT).

As the market has tortuously ground up, I have whittled back my portfolio. I figured out that the way to make money trading in this market was not to trade, to ignore the day-to-day counter trend moves.

As a result, almost every day in June was profitable for my followers.

Quite a few were able to move fast enough to cash in on the move. To read the plaudits yourself, please go to my Testimonials Page . They are all real, and new ones come in almost every day.

My esteemed colleague, Mad Day Trader Jim Parker, was no slouch either, dodging in an out of the raindrops to make money on an intraday basis.

What would you expect with a combined 85 years of market experience between the two of us? Followers are laughing all the way to the bank.

Don?t forget that Jim clocked an amazing 2013 with a staggering 374% trading profit. That was just for an eight-month year!

The Opening Bell with Jim Parker, a quickie but insightful webinar giving followers an instant snapshot of the market opening every day, has been an overwhelming success. Many customers have already reported dramatic improvements in their trading results.

Watch this space, because the crack team at Mad Hedge Fund Trader has more new products and services cooking in the oven. You?ll hear about them as soon as they are out of beta testing.

Our business is booming, so I am plowing profits back in to enhance our added value for you. Next out will be the Mad Hedge Fund Trader Channel on YouTube that will enable me to post videos from my frequent travels around the world.

The coming year promises to deliver a harvest of new trading opportunities. The big driver will be a global synchronized recovery that promises to drive markets into the stratosphere by the end of 2014.

Global Trading Dispatch, my highly innovative and successful trade-mentoring program, earned a net return for readers of 40.17% in 2011, 14.87% in 2012, and 67.45% in 2013.

Our flagship product,?Mad Hedge Fund Trader PRO, costs $4,500 a year. It includes my Global Trading Dispatch?(my trade alert service and daily newsletter). You get a real-time trading portfolio, an enormous research database, and live biweekly strategy webinars. You also get Jim Parker?s?Mad Day Trader?service and?The Opening Bell with Jim Parker.

To subscribe, please go to my website at?www.madhedgefundtrader.com, find the?Global Trading Dispatch??or ?Mad Hedge Fund Trader PRO??box on the right, and click on the blue??SUBSCRIBE NOW??button.

Corporate earnings are up big! Great! Buy! No wait! The economy is going down the toilet! Sell! Buy! Sell! Buy! Sell! Help! Anyone would be forgiven for thinking that the stock market has become bipolar. According to the Commerce Department?s Bureau of Economic Analysis, the answer is that corporate profits account for only a small part of the economy. Using the income method of calculating GDP, corporate profits account for only 15% of the reported GDP figure. The remaining components are doing poorly, or are too small to have much of an impact. Wages and salaries are in a three decade long decline. Interest and investment income is falling, because of the low level of interest rates and the collapse of the housing market. Farm incomes are up, but are a small proportion of the total. Income from non-farm unincorporated business, mostly small business, is unimpressive. It gets more complicated than that. A disproportionate share of corporate profits are being earned overseas. So multinationals with a big foreign presence, like Intel, Oracle (ORCL), Caterpillar (CAT), and IBM (IBM), have the most rapidly growing profits and pay the least amount in taxes. They really get to have their cake, and eat it too. Many of their business activities are contributing to foreign GDP?s, like China?s, more than they are here. Those with large domestic businesses, like retailers, earn less, but pay more in tax, as they lack the offshore entities in which to park them. The message here is to not put all your faith in the headlines, but to look at the numbers behind the numbers. Those who bought in anticipation of good corporate profits last month, got those earnings, and then got slaughtered in the marketplace. Caveat emptor. Buyer beware.