Mad Hedge Technology Letter

January 17, 2019

Fiat Lux

Featured Trade:

(WHY FINTECH IS EATING THE BANKS’ LUNCH),

(WFC), (JPM), (BAC), (C), (GS), (XLF), (PYPL), (SQ), (SPOT), (FINX), (INTU)

Mad Hedge Technology Letter

January 17, 2019

Fiat Lux

Featured Trade:

(WHY FINTECH IS EATING THE BANKS’ LUNCH),

(WFC), (JPM), (BAC), (C), (GS), (XLF), (PYPL), (SQ), (SPOT), (FINX), (INTU)

Going into January 2018, the big banks were highlighted as the pocket of the equity market that would most likely benefit from a rising rate environment which in turn boosts net interest margins (NIM).

Fast forward a year and take a look at the charts of Bank of America (BAC), Citibank (C), JP Morgan (JPM), Goldman Sachs (GS), and Morgan Stanley (GS), and each one of these mainstay banking institutions are down between 10%-20% from January 2018.

Take a look at the Financial Select Sector SPDR ETF (XLF) that backs up my point.

And that was after a recent 10% move up at the turn of the calendar year.

As much as it pains me to say it, bloated American banks have been completely caught off-guard by the mesmerizing phenomenon that is FinTech.

Banking is the latest cohort of analog business to get torpedoes by the brash tech start-up culture.

This is another fitting example of what will happen when you fail to evolve and overstep your business capabilities allowing technology to move into the gaps of weakness.

Let me give you one example.

I was most recently in Tokyo, Japan and was out of cash in a country that cash is king.

Japan has gone a long way to promoting a cashless society, but some things like a classic sushi dinner outside the old Tsukiji Fish Market can’t always be paid by credit card.

I found an ATM to pull out a few hundred dollars’ worth of Japanese yen.

It was already bad enough that the December 2018 sell-off meant a huge rush into the safe haven currency of the Japanese Yen.

The Yen moved from 114 per $1 down to 107 in one month.

That was the beginning of the bad news.

I whipped out my Wells Fargo debit card to withdraw enough cash and the fees accrued were nonsensical.

Not only was I charged a $5 fixed fee for using a non-Wells Fargo ATM, but Wells Fargo also charged me 3% of the total amount of the transaction amount.

Then I was hit on the other side with the Japanese ATM slamming another $5 fixed fee on top of that for a non-Japanese ATM withdrawal.

For just a small withdrawal of a few hundred dollars, I was hit with a $20 fee just to receive my money in paper form.

Paper money is on their way to being artifacts.

This type of price gouging of banking fees is the next bastion of tech disruption and that is what the market is telling us with traditional banks getting hammered while a strong economy and record profits can’t entice investors to pour money into these stocks.

FinTech will do what most revolutionary technology does, create an enhanced user experience for cheaper prices to the consumers and wipe the greedy traditional competition that was laughing all the way to the bank.

The best example that most people can relate to on a daily basis is the transportation industry that was turned on its head by ride-sharing mavericks Uber and Lyft.

But don’t ask yellow cab drivers how they think about these tech companies.

Highlighting the strong aversion to traditional banking business is Slack, the workplace chat app, who will follow in the footsteps of online music streaming platform Spotify (SPOT) by going public this year without doing a traditional IPO.

What does this mean for the traditional banks?

Less revenue.

Slack will list directly and will set its own market for the sale of shares instead of leaning on an investment bank to stabilize the share price.

Recent tech IPOs such as Apptio, Nutanix and Twilio all paid 7% of the proceeds of their offering to the underwriting banks resulting in hundreds of millions of dollars in revenue.

Directly listings will cut that fee down to $10-20 million, a far cry from what was once status quo and a historical revenue generation machine for Wall Street.

This also layers nicely with my general theme of brokers of all types whether banking, transportation, or in the real estate market gradually be rooted out by technology.

In the world of pervasive technology and free information thanks to Google search, brokers have never before added less value than they do today.

Slowly but surely, this trend will systematically roam throughout the economic landscape culling new victims.

And then there are the actual FinTech companies who are vying to replace the traditional banks with leaner tech models saving money by avoiding costly brick and mortar branches that dot American suburbs.

PayPal (PYPL) has been around forever, but it is in the early stages of ramping up growth.

That doesn’t mean they have a weak balance sheet and their large embedded customer base approaching 250 million users has the network effect most smaller FinTech players lack.

PayPal is directly absorbing market share from the big banks as they have rolled out debit cards and other products that work well for millennials.

They are the owners of Venmo, the super-charged peer-to-peer payment app wildly popular amongst the youth.

Shares of PayPal’s have risen over 200% in the past 2 years and as you guessed, they don’t charge those ridiculous fees that banks do.

Wells Fargo and Bank of America charge a $12 monthly fee for balances that dip below $1,500 at the end of any business day.

Your account at PayPal can have a balance of 0 and there will never be any charge whatsoever.

Then there is the most innovative FinTech company Square who recently locked in a new lease at the Uptown Station in Downtown Oakland expanding their office space by 365,000 square feet for over 2,000 employees.

Square is led by one of the best tech CEOs in Silicon Valley Jack Dorsey.

Not only is the company madly innovative looking to pounce on any pocket of opportunity they observe, but they are extremely diversified in their offerings by selling point of sale (POS) systems and offering an online catering service called Caviar.

They also offer software for Square register for payroll services, large restaurants, analytics, location management, employee management, invoices, and Square capital that provides small loans to businesses and many more.

On average, each customer pays for 3.4 Square software services that are an incredible boon for their software-as-a-service (SaaS) portfolio.

An accelerating recurring revenue stream is the holy grail of software business models and companies who execute this model like Microsoft (MSFT) and Salesforce (CRM) are at the apex of their industry.

The problem with trading this stock is that it is mind-numbingly volatile. Shares sold off 40% in the December 2018 meltdown, but before that, the shares doubled twice in the past two years.

Therefore, I do not promote trading Square short-term unless you have a highly resistant stomach for elevated volatility.

This is a buy and hold stock for the long-term.

And that was only just two companies that are busy redrawing the demarcation lines.

There are others that are following in the same direction as PayPal and Square based in Europe.

French startup Shine is a company building an alternative to traditional bank accounts for freelancers working in France.

First, download the app.

The company will guide you through the simple process — you need to take a photo of your ID and fill out a form.

It almost feels like signing up to a social network and not an app that will store your money.

You can send and receive money from your Shine account just like in any banking app.

After registering, you receive a debit card.

You can temporarily lock the card or disable some features in the app, such as ATM withdrawals and online payments.

Since all these companies are software thoroughbreds, improvement to the platform is swift making the products more efficient and attractive.

There are other European mobile banks that are at the head of the innovation curve namely Revolut and N26.

Revolut, in just 6 months, raised its valuation from $350 million to $1.7 billion in a dazzling display of growth.

Revolut’s core product is a payment card that celebrates low fees when spending abroad—but even more, the company has swiftly added more and more additional financial services, from insurance to cryptocurrency trading and current accounts.

Remember my little anecdote of being price-gouged in Tokyo by Wells Fargo, here would be the solution.

Order a Revolut debit card, the card will come in the mail for a small fee.

Customers then can link a simple checking account to the Revolut debit card ala PayPal.

Why do this?

Because a customer armed with a Revolut debit card linked to a bank account can use the card globally and not be charged any fees.

It would be the same as going down to your local Albertson’s and buying a six-pack, there are no international or hidden fees.

There are no foreign transaction fees and the exchange rate is always the mid-market rate and not some manipulated rate that rips you off.

Ironically enough, the premise behind founding this online bank was exactly that, the originators were tired of meandering around Europe and getting hammered in every which way by inflexible banks who could care less about the user experience.

Revolut’s founder, Nikolay Storonsky, has doubled down on the firm’s growth prospects by claiming to reach the goal of 100 million customers by 2023 and a succession of new features.

To say this business has been wildly popular in Europe is an understatement and the American version just came out and is ready to go.

Since December 2018, Revolut won a specialized banking license from the European Central Bank, facilitated by the Bank of Lithuania which allows them to accept deposits and offer consumer credit products.

N26, a German like-minded online bank, echo the same principles as Revolut and eclipsed them as the most valuable FinTech startup with a $2.7 Billion Valuation.

N26 will come to America sometime in the spring and already boast 2.3 million users.

They execute in five languages across 24 countries with 700 staff, most recently launching in the U.K. last October with a high-profile marketing blitz across the capital.

Most of their revenue is subscription-based paying homage to the time-tested recurring revenue theme that I have harped on since the inception of the Mad Hedge Technology Letter.

And possibly the best part of their growth is that the average age of their customer is 31 which could be the beginning of a beautiful financial relationship that lasts a lifetime.

N26’s basic current account is free, while “Black” and “Metal” cards include higher ATM withdrawal limits overseas and benefits such as travel insurance and WeWork membership for a monthly fee.

Sad to say but Bank of America, Wells Fargo, and the others just can’t compete with the velocity of the new offerings let alone the software-backed talent.

We are at an inflection point in the banking system and there will be carnage to the hills, may I even say another Lehman moment for one of these stale business models.

Online banking is here to stay, and the momentum is only picking up steam.

If you want to take the easy way out, then buy the Global X FinTech ETF (FINX) with an assortment of companies exposed to FinTech such as PayPal, Square, and Intuit (INTU).

The death of cash is sooner than you think.

This year is the year of FinTech and I’m not afraid to say it.

Mad Hedge Technology Letter

January 2, 2019

Fiat Lux

Featured Trade:

(THE FANGS' PATH TO ONLINE BANKING),

(SQ), (V), (MA), (AXP), (JPM)

Yu'e Bao or "leftover treasure" in English has caught the attention of more than 400 million Chinese investors.

This money market fund has exponentially grown into a $250 billion fund by the end of 2017, and is now the largest money market fund in the world!

This product isn't offered by Bank of China or another giant state-owned bank or financial enterprise, but Alibaba's (BABA) Ant Financial (gotta love those Chinese names).

Assets under management are up 100% YOY and it now accounts for a quarter of China's money-market mutual fund industry in just one fund.

These inflows coincide with the sudden migration into mobile payments. Common folks are comfortable with investing their life savings in these short-term instruments with a too-big-to-fail, larger-than-life firm such as Alibaba.

Yu'e Bao derives its funds from Alipay users, Alibaba's digital third-party platform, that allows consumers to pay for everything in life from theater tickets to utility bills.

Service is unified on a holistic graphic interface. Users can easily divert cash into this fund with a few screen taps on their app. Yu'e Bao's ROI offers a seven-day annualized yield of 4.02%, down from the introductory annualized rate of 6.9% around the launch in 2013.

Yu'e Bao's short-term yield outmuscles the 1.5% interest rate on one-year Chinese bank deposits and the 3.6% yield on 10-year Chinese government debt.

Weak banking regulation has spawned a mammoth FinTech (financial technology) industry in the Middle Kingdom. Only one yuan (16 cents) is enough to create an account and considerable retail flow has rushed in.

China has catapulted ahead of the rest of the world emerging as the leader of global FinTech innovation. The pace, sophistication, and scale of development of China's FinTech have surpassed the level in any other of the developed countries.

The country's digital metamorphosis has enhanced e-commerce, payment systems, and connected logistical services. The Chinese discretionary spender for the past decade has been the deepest and most reliable lever of global growth.

Mobile third-party payments in China, 90% cornered by Tencent's WeChat and Alibaba's Alipay, are estimated to reach a lofty $6 trillion in revenue by 2019, more than 50 times that of the U.S.

These omnipresent payment systems are now deeply embedded into the fabric of Chinese society. It's common to witness homeless people on Shanghai subways waving around a scannable image for WeChat or Alipay money transfers instead of asking for physical cash.

Even in rural farmlands, shabby convenience stores prioritize digital currency and sometimes don't accept paper currency at all. Yes, China is beating the U.S. to a cashless society.

Digitization is changing the competitive balance, and global banks must embrace large-scale disruption caused by big tech platforms.

Banks in China regard these companies as potential collaborators resulting in a net positive long-term infusion of enhanced products and services.

Agreements have been forged between the Bank of China and Tencent, and the China Construction Bank has linked up with Alibaba.

China has incorporated the technical power of A.I. (artificial intelligence) and machine learning into its FinTech platforms at every opportunity. Robo-advisors are also making inroads creating a bespoke financial program for the individual.

This trend has so far failed to go viral in America where individuals still prefer plastic cards or even paper cash. E-commerce clocked in a paltry 9.1% of total U.S. retail sales in the third quarter of 2017.

Even though most of us have our heads buried deep in our smartphone virtual world, Americans are still programmed to whip out debit or credit cards at every opportunity.

Chinese who visit America carp endlessly about America's archaic payment system.

Ultimately, American payment systems are ripe for digital disruption.

The American consumer will ultimately cause severe damage to MasterCard (MA), Visa (V), and American Express (AXP) which are happy with the current status quo.

The lack of innovation in the US FinTech sector is a failure in the otherwise fabulous technological leadership of the US. American smartphones should already be a fertile digital wallet, not just a niche market.

Savvy Jack Dorsey even invented a firm based on this inefficiency exploiting the lack of proficiency in domestic FinTech with Square (SQ).

And a vital reason the stock has gone parabolic this year is because of the brisk execution and the long runway ahead in this industry.

American big tech will gradually utilize China's FinTech model and extrapolate it with "American personality." It is much more of a two-way street now than before with cutting-edge ideas flowing both ways.

The next leg up after digital wallet penetration of FinTech is money market funds on tech platforms. In effect, the Chinese innovation of this industry has allowed more variations of potential financing for the ambitious Chinese, and the same trends will gradually appear on Yankee shores.

Ironically enough, Amazon's (AMZN) land grab strategy is more prevalent in China as artificially low financing and juicier scale justify this strategy.

The scaling premium also explains why corporate China's early adopter advantage is so effective because not many countries boast a 1.3-billion-person consumer market.

Soon, Americans will wake up to the reality that American FinTech must advance or foreign firms will rush in.

Mediocrity is not good enough.

iPhones and Android consumers could direct savings into tech money market funds with compounding yield all on a single digital platform.

Tech companies could deploy some of the repatriated cash to invest in some fledgling FinTech expertise to smoothly execute this new endeavor.

Consequently, a successfully created money market fund on a tech platform would enlarge the already substantial cash hoard these firms possess. Not only will the large tech companies flourish, but the big will get absolutely massive.

The determining factor is financial regulation. Capitol Hill has drawn a large swath of mighty Silicon Valley tech titans to testify because they are stepping on too many toes lately.

A scheme to hijack the digital payments market and dominate the mutual fund industry will cause unyielding push back in Washington especially when the Amazon death star continues pillaging select industries of their choosing and eliminating brick-and-mortar jobs by the millions.

J.P. Morgan (JPM) which has the largest institutional money market fund in the country and retail stalwarts such as BlackRock and Vanguard will be sweating profusely too if mega tech starts probing around its turf.

Alibaba is also coming for its bacon with the failed purchase of payment transfer service MoneyGram International (MGI) temporarily shutting out Jack Ma from a foothold in the American payment system industry.

And if the Chinese aren't let in, there will be others sniffing around for the bacon, too.

The momentum for these financial instruments is robust as FinTech integrates deeper into consumer life. The global cash glut from a decade of cheap financing is causing profit-hungry investors to starve for high-yield vehicles.

The stability and clean balance sheets of tech giants give them ample chance to successfully execute. So, why can't they also become banks? Would you buy an Apple, Amazon, or Google money market fund if they offered a 4% to 7% annualized yield?

I believe most Americans would.

Global Market Comments

October 15, 2018

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or OUR HARD LANDING BACK ON EARTH),

(SPY), (QQQ), (TLT), (VIX), (VXX), (MSFT), (JPM), (AAPL),

(DECODING THE GREENBACK),

(DUMPING THE OLD ASSET ALLOCATION RULES)

Truth be told, it’s the really boring, sedentary, go-nowhere markets that drive me nuts, cause me to tear my hair out, and urge me on to an early retirement.

The week started with such promise.

Sunday night I witnessed the first Space X landing of a rocket in California which I could clearly see from the top of Berkeley’s Grizzly Peak some 250 miles away. It was fascinating to see four separate jets steer the spacecraft earthward.

Financial markets had a different landing in mind, the hard kind, if not a crash.

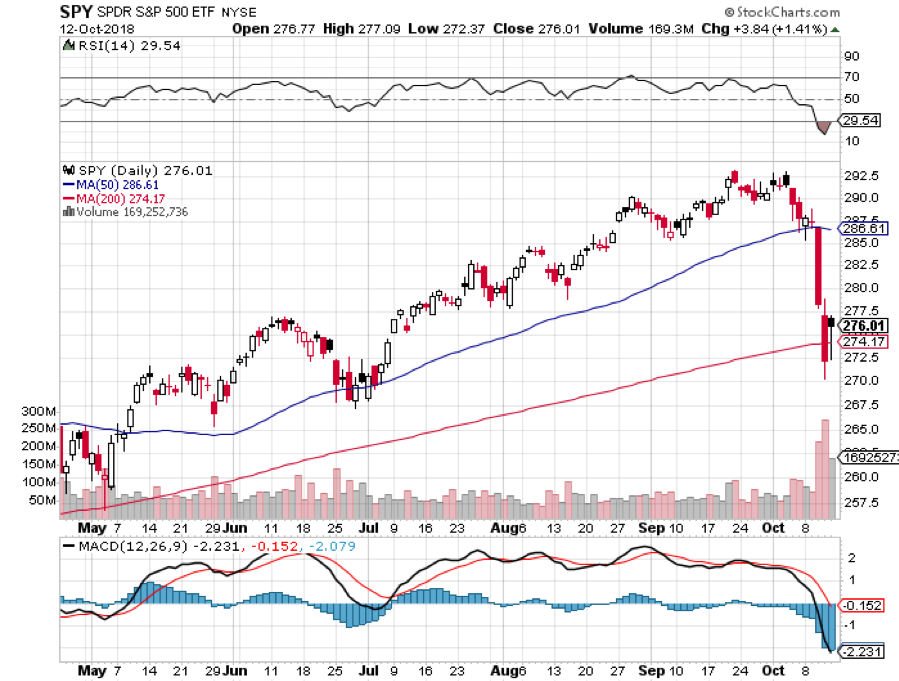

I absolutely love the market we had last week which saw the third biggest down day in history, volatility explode, and $2.6 trillion in stock market capitalization vaporize.

I had to blink when I saw NASDAQ (QQQ) down an incredible 350 points in one day. My Mad Hedge Market Timing Index hit an all-time low at 4.

No wonder insider selling hit $10.3 billion in August, another record. Maybe they know something we don’t.

Chinese Gamer Tencent Postponed their US IPO. It seems they noticed that market conditions had become unfavorable. I know investment bankers hate passing on an opportunity to ring the cash register. I used to be one.

There is no better feeling than being 100% cash going into one of these crashes and then having panicked investors puke their best quality positions to me at a market bottom.

On Thursday, I backed up the truck and issued four perfectly timed Trade Alerts, picking up Microsoft (MSFT), Apple (AAPL), and the S&P 500 (SPY), and covering my short position in the bond market (TLT).

In fact, I believe I had my best week of the year even though I only added modestly to my annual return. Look at the charts below and you’ll see that I suffered a 9% drawdown during the February meltdown. Maybe I’m getting wiser as I get older? One can only hope.

This time, I managed to limit my loss to a modest 2.5% and am nearly unchanged on the month despite the Dow Average at one point nearly giving up all its gains for 2018. This is also against a horrific backdrop of hedge fund performance that is now showing losses for 2018.

The Volatility Index (VIX) made a move for the ages, at one point kissing the $29 handle, up from $11 two weeks ago. During the 600-point swoosh down on Thursday, I couldn’t get any of my staff on the phone. The entire company was logged into their personal trading accounts, buying puts on the iPath S&P 500 VIX Short-Term Futures ETN (VXX) as fast as they could.

Which leads me to believe that the bottom is near. Earnings and valuation support start kicking in big time at these levels, and the blackout period for company share buybacks started ending with the bank earnings last Friday.

When you take a $1 trillion buyer out of the market, it has a huge effect no matter how strong the fundamentals are. Start buying those dips. Their return is similarly eventful. I’ve already started to invest my 95% cash position.

Further eroding confidence was the president’s statement that the Federal Reserve is crazy. So, now we know the president appoints crazy people to the most important financial positions in the country. White House control of interest rates ahead of elections. Why didn’t I think of that?

Sparking the Friday melt-up was a statement by JP Morgan (JPM) CEO Jamie Diamond saying that a 40-basis point rise in rates is no big deal. The bull market is on. His earnings beat all expectations.

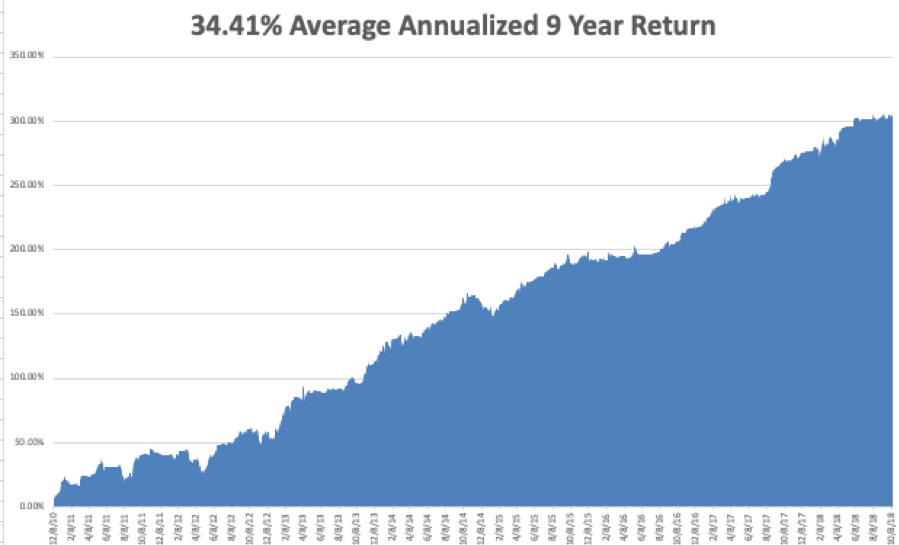

My 2018 year-to-date performance has bounced back to 27.56%, and my trailing one-year return stands at 35.87%. October is almost flat at -0.84%. Most people will take that in these horrific conditions.

My nine-year return appreciated to 304.03%. The average annualized return stands at 34.41%.

This coming week will be pretty sedentary on the data front.

Monday, October 15 at 8:30 AM brings us September Retail Sales.

On Tuesday, October 16 at 9:15 AM, September Industrial Production is announced.

On Wednesday, October 17 at 8:30 AM, September Housing Starts are published.

Thursday, October 18 at 8:30, we get Weekly Jobless Claims. At 10:00 we learne the September Index of Leading Economic Indicators.

On Friday, October 19, at 10:00 AM, the September Housing Starts are out. The Baker-Hughes Rig Count follows at 1:00 PM.

As for me, I will spend this week on my Southeastern US roadshow, giving strategy luncheons in Savannah, GA, Atlanta, GA, Miami, FL, and Houston, TX. I love meeting my readers mano a mano who are often a source of my best trading ideas. It looks like I’ll miss Hurricane Michael by three days.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 28, 2018

Fiat Lux

Featured Trade:

(WHAT WILL TRIGGER THE NEXT BEAR MARKET?)

(JPM), (SNE), (TLT), (ELD), (AMZN),

(WEDNESDAY, OCTOBER 17, 2018, HOUSTON

GLOBAL STRATEGY LUNCHEON)

To paraphrase Leo Tolstoy in Anna Karenina, all bull markets are alike; each bear market takes place for its own particular reasons.

Now that the wreckage of the past financial crises is firmly in our rearview mirror, it is time for us to start pondering the causes of the next one. I’ll give you a hint: It will all boil down to excessive debt…again.

Global quantitative easing has been going on for a decade now, keeping interest rates far too low for too long. The unintended consequences will be legion, and the day of atonement may be a lot closer than you think.

The 1991 bear market was prompted by the Savings & Loan Crisis, where too many unsophisticated financial institutions in a newly unregulated world dreadfully mismatched asset and liabilities.

Every time I drive by a former Home Savings and Loan branch, with its unmistakable quilt decorations and accents, I remember those frightful days. Back then, when I looked at buying a home in San Francisco, the seller burst into tears when the price I offered would have generated a negative equity bill due for him.

The 2000 Dotcom crash can easily be explained by the monstrous amounts of debt provided to stock speculators. The 2008 crash was produced by massive, unregulated, and largely unknown lending to the housing sector through complex derivatives that virtually no one understood, especially the buyers.

So, here we are in 2018 nearly a decade out of the last crisis. Potential disasters are lurking everywhere under the surface while blinder constrained investors blithely power ahead. Once they metastasize, they rapidly feed into each other, creating a domino effect. They always do.

Emerging Market Debt

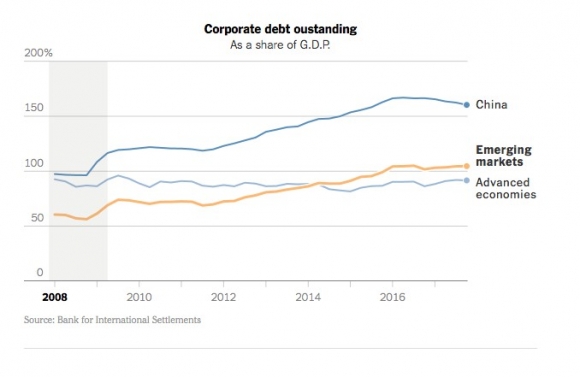

Lacking domestic capital markets with any real depth, companies in emerging economies prefer to borrow in U.S. dollars. When the dollar is weak that’s great because it means liabilities on the balance sheet shrink when brought back into the home currency. When the greenback is strong, the opposite happens. Dollar debt can grow so large that it can wipe out a company’s total equity.

This is already happening in a major way in Turkey, where the lira has plunged 50% in the past year, effectively doubling their debt. And once it starts, a global contagion kicks in as all emerging companies become suspect. This is not a small problem. Emerging market debt has rocketed from 55% to 105% of GDP since 2008.

The Rise of Junk Borrowers

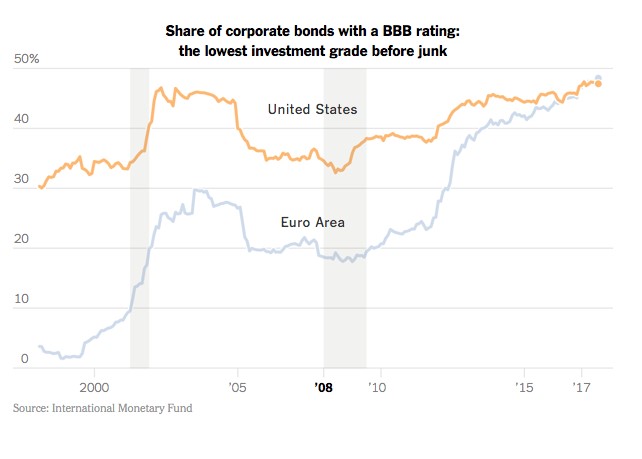

In recent years there has been a massive expansion in borrowing by marginal credits. This is taking place because fixed income investors are willing to accept a large increase in the amount of risk for only a small marginal rise in interest rates.

There is now $1.4 trillion in low grade BBB bonds outstanding, with one-third of this one downgrade away from junk. There has also been a dramatic rise in “covenant lite” issuance, which minimizes the rights of bond holders in the event of default. When the next round of trouble arrives, you can expect this market to shut down completely, as it did in 2008.

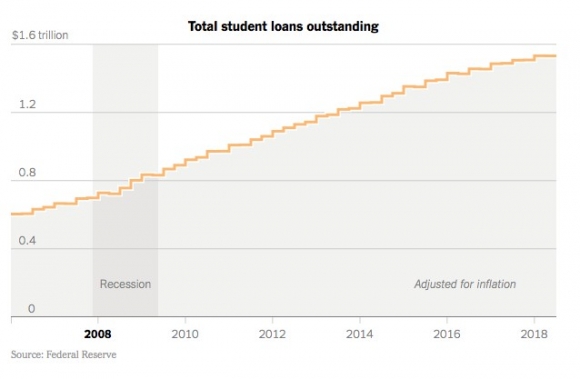

Student Loans

These have been the sharpest rising form of borrowing over the past decade, doubling to $1.5 trillion. Some 10% are now in default. This acts as a major drag on the economy as heavily indebted students don’t borrow, buy homes or cars, or really participate in the economy in any way, banned by lowly FICO scores. This is why millennials in general have been slow to enter the housing market for the first time.

Shadow Banking

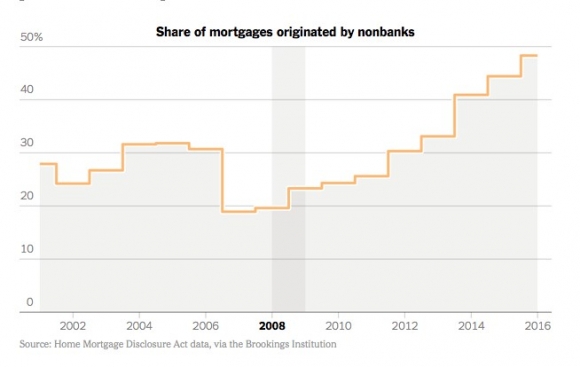

Would you like to know today’s equivalent of subprime the lending that took the financial system down in 2008? That would be shadow banking, or off the books, unreported lending by hedge funds, private equity funds, and mortgage companies. Again, this is all in pursuit of high interest rates in a low interest rate world.

Yes, liars’ loans are back, just not to the extent we saw 10 years ago…yet. I’m waiting for my cleaning lady to get offered a great refi package again, just as she was in the run-up to the last crisis. How many of these loans are out there? No one has any idea, especially the Fed. As a result, nearly 50% of all mortgage lending is now from unregulated nonbank sources.

The Outlier

Remember when Sony (SNE) was almost put out of business by a hack attack from North Korea? What if they had done this to JP Morgan (JPM)? That would have created a chain reaction of defaults throughout the financial system that would have been impossible to stop. When this happened in 2008, it took the Fed three months to reopen markets such as commercial paper. If big bankers need a reason to lie awake at night, this is it.

I’m not saying that markets can’t go higher before they go lower. In fact, I dove back into Amazon (AMZN) only this morning.

However, as an Australian farmer told me on my last trip down under, “Be careful when you cross the field, mate. Deadly snakes abound.” Add up all the above and it will turn into a giant headache for investors everywhere.

Mad Hedge Technology Letter

September 6, 2018

Fiat Lux

Featured Trade:

(THE SMART PLAYS IN FINTECH),

(SQ), (PYPL), (JPM), (COF), (WFC), (BAC),

(MGI), (GRUB), (BABA), (NFLX)

Fintech is all the rage now, and it’s time for investors to grab a piece of the action.

The tech sectors’ stellar performance in 2018 is a little taste of things to come as every industry forcibly pushes toward software and artificial intelligence to enhance products and services.

Bull markets don’t die of old age and some of these tech stalwarts are truly defying gravity.

The fintech sector is no exception.

Square (SQ) led by tech visionary Jack Dorsey has been a favorite of the Mad Hedge Technology Letter practically from the newsletter’s inception.

But another company has caught my eye that most of you already know about – PayPal (PYPL).

PayPal, a digital payments company, has extraordinary core drivers and a splendid growth trajectory.

Its arsenal of services includes digital wallets, money transfers, P2P payments, and credit cards.

It also has Venmo.

Venmo, a digital payment app, is the strongest growth lever in PayPal’s umbrella of assets right now, and was the first meaningful digital payment app in America.

It was established by Andrew Kortina and Iqram Magdon-Ismail, who were roommates at the University of Pennsylvania, and the company was bought out by PayPal for $800 million in 2014, marking a new chapter in PayPal’s evolution.

Funny enough, Venmo’s original use was to buy mp3 formatted songs via email in 2009.

Venmo is wildly popular with tech savvy millennials. A brief survey conducted illustrates how fashionable Venmo is by recording higher user statistics than Apple Pay.

The app is commonly used for ordering pizza through Uber Eats or Grubhub (GRUB), or even shelling out for monthly rent.

If you want to stir up your imagination even more, Venmo has a prominent social feed where users can view other Venmo users’ purchases.

Financial models suggest Venmo could contribute $300 million to the PayPal top line in 2021. If Venmo executes perfectly, revenue could surpass the $1 billion mark in 2021, with much higher operating margins than PayPal’s core products.

Even though management declines to speak specifically about Venmo, the dialogue in the earnings call usually provides some color into what is going on underneath the hood.

Xoom, a digital remittance distributor app with offices in San Francisco and Guatemala City owned by PayPal, along with Venmo grew payment volume by 50% YOY, surging to $33 billion annually.

Of that $33 billion in volume, $19 billion was contributed by Venmo and Xoom chipped in with $14 billion.

More than 60,000 new merchants joined PayPal’s array of platforms, adding up to more than 19.5 million total merchants.

All in all, PayPal locked in $3.86 billion of sales last quarter, which was a 23% YOY jump in revenue, at a time where widespread acceptance of fintech platforms is brisk.

PayPal raised its end-of-year forecast and rewarded shareholders with authorization of a $10 billion buyback.

Upward margin expansion, expanding market share, multiple revenue stream, and untapped pricing power is the recipe to PayPal’s meteoric rise.

PayPal’s share price has climbed higher from a base of $73 at the beginning of the year to an all-time high of more than $90.

Offering more proof fintech is alive and kicking is Jack Dorsey’s Square’s dizzying rise of more than 200% YOY in its share price.

The company is exceeding all revenue growth expectations and is poised to ramp up subscription revenue.

As with the Venmo app, Square’s Cash app has unrealized potential and will be one of the outperforming profit drivers going forward.

Square hopes to be the one-stop-shop for all types of digital payment needs including consumer finance, equity purchases, possibly international transfers, and cryptocurrency.

All of this is happening amid a robust secular story that could have seen traditional banks swept into the dustbin of history.

Rewind a few years ago, perusing the data about the movement to digital payments must have frightened the living daylights out of the executives from major Wall Street mainstays.

Digital wallets assertive migration into mainstream money payment services could have detached traditional banks’ core businesses.

Slogging your way to a physical bank to put in a wire transfer was not appealing.

Archaic methods of business are painful to see, and traditional banks were still operating this way as of 2015.

Time is money and technology has crashed the traditional waiting time to almost zero.

The way these tech companies operate is simple.

They compete to hire a hoard of advanced computer developers or shortcut the process using the time-honored tradition of poaching the competition’s best talent.

Then snatch market share at all costs and grow like crazy.

Banks badly needed introducing some functions to their array of services such as linking with third-party payment APIs to facilitate online payments and enabling cross-platform digital payments.

Other functions such as establishing modern peer-to-peer payment systems or adopting QR code technology that are wildly popular in East Asia could enhance optionality as well.

These are several instruments they could have amalgamated into their arsenal of fintech technology that could have freshened up these dinosaur institutions.

Harmonizing banking tasks with mobile functionality was fast coming and would be the standard.

Anyone not on board would sink like the Titanic.

Ultimately, banking institutions needed to up their game and acquire one of these digital wallet processors or watch from the sidelines.

They chose the former when a consortium called Early Warning Services (EWS) jointly created by behemoth American banks, including JPMorgan Chase & Co. (JPM), Capital One (COF), Bank of America (BAC), and Wells Fargo (WFC) to “prevent fraud and reduce detection risk” made a game-changing decision.

(EWS) acquired digital payment app Zelle in 2016, and this was its aggressive response to Square Cash and PayPal’s Venmo.

Results have been nothing short of breathtaking.

Leveraging the embedded base of existing banking relationships, Zelle took off like a scalded chimp and never looked back.

In a blink of an eye, Zelle had already signed up more than 30 banks and over 100 financial institutions to its platform.

Banks couldn’t bear being left out of the fintech party.

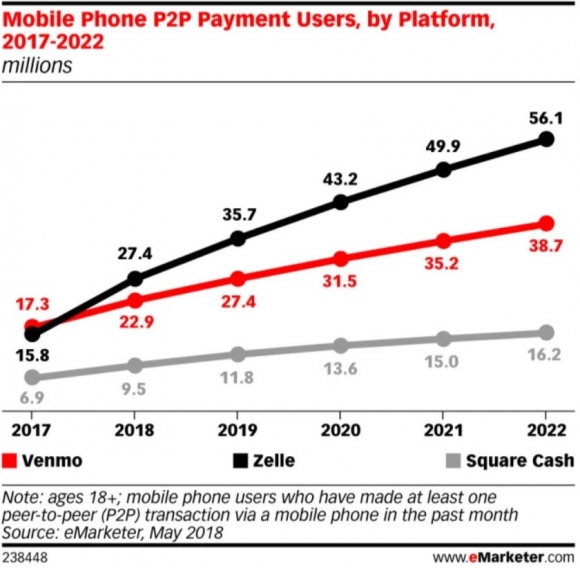

With hearty conviction, Zelle is signing up users at a pace of 100,000 per day, and the volume of payments in 2017 eclipsed $75 billion.

Zelle projects to expand more than 73% in 2018, integrating 27.4 million new accounts in the U.S., head and shoulders above Venmo’s 22.9 million and Square Cash due to add 9.5 million more users.

Make no bones about it, Zelle was in prime position to convert existing relationships into digital converts. The banks that do not have an interest in Zelle have an uphill climb to stay relevant.

The United States is rather late to this secular growth story. That being said, already 57% of Americans have used a mobile wallet at least once in their lives.

Innovative ideas bring supporters galore and even more adoptees.

That is why the strong pivot into technological enhanced ideas bear unlimited fruit.

Using a mobile platform to just open an app then send funds within a split second with minimal costs is appealing for the Netflix (NFLX) crazed generation that can hardly get off the couch.

Ironically, it’s those in the emerging parts of the world leading this fintech revolution by skipping the traditional banking experience completely and downloading digital wallet apps on their mobile devices.

It’s entirely realistic that some fresh-faced youth have never been present at a physical banking branch before in India or China.

Download an app and your fiscal life commences. Period.

The volume of funds passing through the arteries of Chinese digital wallet apps surpassed $15 trillion in 2017.

And by 2021, 79.3% of the Chinese population are projected to use digital wallets as their main source of splurging Chinese yuan.

America lags a country mile behind China, but the Chinese progress has offered American tech companies a crystal-clear blueprint to springboard digital payment initiatives.

Chinese state banks are already starting to become marginalized, and the Wall Street banks are not immune to the same fate.

Devoid of a digital strategy will be a death knell to certain banking institutions.

Compare the pace of adoption and some must question why American adoption is tardy to a fault.

Highlighting the lackadaisical pace of American fintech integration was Alibaba’s (BABA) smash-and-grab attempt at MoneyGram International Inc. (MGI), as it sought to gain a foothold into the American fintech market.

The attempt was rebuffed by the federal government.

The nascent state of the digital payment world in America must alarm Silicon Valley experts. And the run-up in Square and PayPal includes calculated bets that these two standouts will leapfrog into the future with guns blazing along with Zelle.

The parabolic nature of Square’s mystifying gap up means that a moderate pullback is warranted to put capital to work in this name.

Investors should wait for a timely entry point into PayPal as well.

These two stocks have overextended themselves.

As the fintech pie extrapolates, there will be multiple victors, and these victors are already taking shape in the form of Zelle, PayPal, and Square.

![]()

________________________________________________________________________________________________

Quote of the Day

“In the not-too-distant future, commerce is just going to be commerce. It won't be online commerce or offline commerce. It's just going to be commerce. And that will happen because of the phone,” – said CEO of PayPal Dan Schulman.