Mad Hedge Technology Letter

August 7, 2019

Fiat Lux

Featured Trade:

(CORD-CUTTING IS ACCELERATING)

(DIS), (T), (NFLX), (CMCSA)

Mad Hedge Technology Letter

August 7, 2019

Fiat Lux

Featured Trade:

(CORD-CUTTING IS ACCELERATING)

(DIS), (T), (NFLX), (CMCSA)

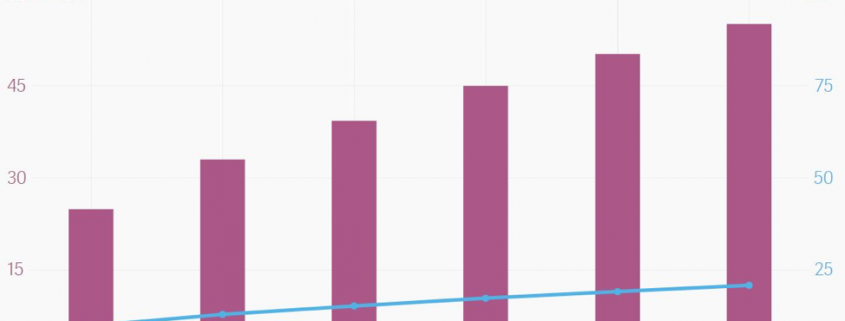

Cord-cutting is picking up steam – that is the last thing traditional media want to hear.

There are several foundational themes that this newsletter has glued onto readers' foreheads.

The generational pivot to cloud-based media is one of them.

It’s easy to denominate this phenomenon down to Netflix (NFLX) but in 2019, this trend is so much more than Netflix.

E-marketer published a survey showing that cord-cutters will surpass 20% of all U.S. adults by the end of 2019.

The rapid demise of traditional television has been equally as mind-numbing with the 100.5 million subscribers in 2014 turning into 86.5 million subscribers today.

Comcast (CMCSA) has tried to buck the trend by homing in on fast broadband internet, but that strategy can only go so far.

Disney (DIS), WarnerMedia, and NBCUniversal Disney have really gotten their ducks in a row and are on the verge of launching their own unique streaming services.

Disney's service entails a 3-segment strategy bringing in Hulu and ESPN Plus to the Disney fold.

The Disney service will revolve around family content at its core so don’t expect Game of Thrones lookalikes.

WarnerMedia's hopes to cash in on its HBO brand while peppering it with original series and programming from Warner Bros. and DC.

Disney will be able to lean on family brands of Marvel, Star Wars, and Pixar, and newly acquired National Geographic.

Marvel Cinematic Universe is a growth asset pumping out more than $22 billion at the box office across 23 movies.

Disney Plus will also have a solid collection of Disney films to play with, which could make it indispensable to parents and comes with no ads making it even more appealing to kids.

Disney will also deploy some mix of bundles to diversify its offerings and personalize services for viewers who do not want its entire lineup of content.

The soon-to-be HBO Max will implement HBO original content along with WarnerMedia brands like Warner Bros., DC Entertainment, TBS, TNT, and CNN.

HBO Max will have a treasure trove of old Warner Bros. movies and TV shows, like "Friends" and "The Fresh Prince of Bel Air," that has played extremely well on Netflix.

HBO will get those titles back at the end of 2019.

HBO has also tied up with BBC Studios to stream "Doctor Who."

"You should assume that HBO Max will have live elements," said Randall Stephenson, chairman and CEO of AT&T, on the company's second quarter conference call.

This roughly translates into HBO Max snapping up live sports and music events to complement scripted content.

This is something that Netflix has shied away from and live events are best monetized through live ads.

The last big label service to go into effect is NBC’s yet to be named streaming service.

NBCUniversal will have the luxury of offering their cable subscribers a chance to pivot to an in-house online streaming service making the move seamless.

At first, the 21 million US cable-TV subscribers will receive the streaming content for free.

Some of the assets that will trot out on the NBC platform are "The Office," because NBC is removing it from Netflix for 2021.

As cord-cutters hasten their move to streaming, this trio of loaded content-creating firms will benefit as long as they maintain a high quality of content and the pipeline to please fidgety consumers.

Mad Hedge Technology Letter

July 26, 2019

Fiat Lux

Featured Trade:

(WHY 3D PRINTING WILL BOOST THE AIRPLANE INDUSTRY),

(SSYS), (ETSY), (MSFT), (BA), (NFLX), (GE), (LMT)

If you need a new investment idea – here’s one.

3D printing.

Yes, the same 3D printing that was once considered a raging but hopeless fad.

A lot has changed since then.

Early adopters were largely cut down at the knees as they tried to traverse the rocky terrain from a niche market to going full out mainstream.

The teething pains echo bitcoin which was the fad of 2017, on the contrary, this technology it is built on is rock solid, yet the path to sustainability is littered with corpses.

Production complications and the lack of specialists in the industry meant that problems were rampant and nurturing an industry from scratch is harder than you think.

It is time to stand up and take notice of 3D printing, this time it is here to stay.

Certain tech companies love this technology.

Etsy (ETSY) e-commerce participants gravitate towards 3D printing because it gets firms from paper to the real world in a fraction of the time.

The cost of production doesn’t change whether you’re producing one item or a million because of the economies of scale.

The previous 3D printing bonanza was a frenzy and this corner of tech became known for the use of buzzwords representing the potential to reinvent the world.

With lofty expectations, there was a natural disappointment when outsiders understood growing pains were part of the critical evolution instead of a direct route to profits.

The initial goal was to democratize production which sounds eerily similar to bitcoins mantra of democratizing money.

The way to do this was to make it simple to produce whatever one wishes.

That would assume that the general public could pick up professional production 3D printing skills on arrival.

That was wishful thinking.

The truth was that applying 3D printers was time-draining and aggravating.

Issues cropped up like faulty first-generation hardware or software -problems that overwhelmed newbies.

Then if everything was going smoothly on that front, there was the larger issue of realizing it’s just a lot harder to design specific things than initially thought without a deep working knowledge of computer-aided software (CAD) design.

Most people know how to throw a football, but that doesn’t mean that most people can wake up one day in their pajamas and convince themselves they will be the next starting quarterback to lead an NFL team to the Super Bowl.

The high-quality 3D printing designs were reserved for authentic professionals that could put together complicated designs.

The move to compiling a comprehensive library will help spur on the 3D printing revolution while upping the foundational skill base.

Then there is the fact that 3D printing technology is a lot better now than it once was, and the printing technology has come down in price making it more affordable for the masses.

These trends will propel broad-based adoption and as the printing process standardizes, more products can rely on this technology from scratch.

The holy grail of 3D printing would be 3D printing on demand like Netflix (NFLX), but imagine this on-demand 3D printing would function to personalize a physical product on the spot.

Think of a hungry customer walking into a restaurant and not even looking at a menu because one sentence would be enough to trigger specific models in the database that could conjure up the design for the meal.

This would involve integrating artificial intelligence into 3D printing and the production process would quicken to minutes, even seconds.

At some point, crafting the perfect meal or designing a personalized Tuscan villa could take minutes.

The 3D printing industry is reaching an inflection point where the advancement of the technology, expertise, and an updated production process are brewing together at the perfect time.

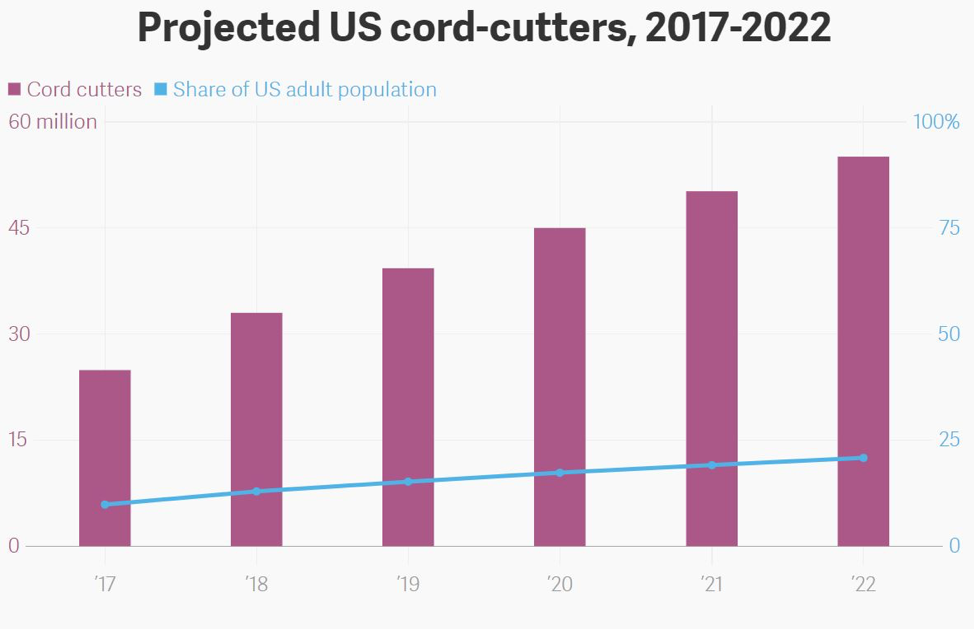

The company at the forefront of this phenomenon is Stratasys (SSYS).

Stratasys produces in-office prototypes and direct digital manufacturing systems for automotive, aerospace, industrial, recreational, electronic, medical and consumer products.

And when I talk about real pros who have the intellectual property to whip out a complex CAD-based 3D design, I am specifically talking about Stratasys who have been in this business since the industry was in infancy.

And if you add in the integration of cloud software, 3D printing would dovetail nicely with it.

All the elements are in place to fuel this industry into the mainstream.

Take for example airplanes made by Boeing (BA) and Airbus, 3D printer-designed parts comprise only 0.1% of the actual plane now.

It is estimated that 3D printed design parts could consist up to 20% of the overall plane.

These massive airline manufacturers like Boeing (BA) have profit margins of around 15% to 20%, and carving out more 3D printer-designed parts to integrate into the main design will boost profit margins to up to 50%.

The development of the 3D printing process into aerospace technology is happening fast with Boeing inking a five-year collaboration agreement with Swiss technology and engineering group Oerlikon to develop standard processes and materials for metal 3D printing.

Any combat pilot knows who Oerlikon is because they are famed for building ultra-highspeed machines to shoot down, you guessed it, airplanes and missiles.

They will collaborate to use the data resulting from their agreement to support the creation of a standard titanium 3D printing processes.

Only last November, GE announced that GE’s Aviation’s GEnx-2B aircraft engine for the Boeing 747-8 will apply a 3D printed bracket approved by the Federal Aviation Administration (FAA) for the engine, replacing a traditionally manufactured power door opening system (PDOS) bracket.

With the positive revelations that the (FAA) is supporting the adoption of 3D printing-based designs, GE is preparing to begin imminent mass production of the 3D printed brackets at its Auburn, Alabama facility.

Eric Gatlin, general manager of GE Aviation’s additive integrated product team gushed that “It’s the first project we took from design to production in less than ten months.”

Defense companies are also dipping their toe into the water with aerospace company Lockheed Martin (LMT), the world’s largest defense contractor, winning a $5.8 million contract with the Office of Naval Research to help further develop 3D printing for the aerospace industry.

They will partner up to investigate the use of artificial intelligence in training robots to independently oversee the 3D printing of complex aerospace components.

3D printed designs have the potential to crash the cost of making big-ticket items from cars to nuclear plants while substantially shortening the manufacturing process.

Further emphasis on cornering the North America aerospace market could cement this stock as a no-brainer buy of 2019 as the (FAA) embraces more of the technology opening up the addressable market for the active participants.

As it stands, Stratasys is the industry leader in this field, and placing best of breed tech companies into your portfolio will put you in better position to weather the squalls of the capricious tech sector.

The company is still relatively unknown even though it has been around for ages.

Stratasys is a company to put on your radar and remember this space as the 3D printing market blossoms.

It’s nonetheless still a speculative punt but a compelling part of the tech industry.

Mad Hedge Technology Letter

July 5, 2019

Fiat Lux

Featured Trade:

(THE BALL IS IN NETFLIX’S COURT)

(NFLX), (DIS), (AAPL), (IQ), (KHC)

Being as volatile as it is, investors are afforded ample opportunity to get into one of the premium tech stocks in the land Netflix (NFLX).

Chasing this one higher is a dangerous thought, as habitual 30% dips is part and parcel of being attached to this supreme online streaming stock.

December of 2018 gave you that sinking feeling when Netflix dropped off a cliff dipping to $260 but spiking after the turn of the year as the Fed swiveled on a dime to save the equity market from implosion.

Let’s make no bones about it, the long-term narrative for Netflix is intact as it’s ever been.

The company simply makes a great product, period, and systematically taps endless demand.

What many cable companies don’t understand is that you cannot make a high-quality film product that wedges in annoying commercials and equally as obnoxious, dictate the window of time in which they should watch the content.

Optionality is value and Netflix has this spot on.

I know many Millennial consumers that would rather jump off a building than subject themselves to commercials.

These factors erode the quality of the product just as if an employer would dictate to one of his or her employees that wanted to take a vacation to Africa.

But the vacation to Africa would have some strings attached.

He or she would only be able to visit at the height of summer in 120-degree Fahrenheit weather while every activity he or she chose to do, would be pre-empted by numerous advertisements that he or she must be shown.

Consumers don’t need these sideshows anymore; the world has developed away from these models and corporates have lost this control.

The loss of corporate control of the consumers is because the internet gives consumers millions of different options at the tip of their fingers.

Tapping into the optionality and the habits that revolve around it is paramount to corporate America.

This is the same reason why big box food companies like Kraft Heinz (KHC) is getting smacked around, consumers have better options and are more aware of them because of technology.

Another example of corporate miscalculation comes in the form of supply chains being redirected from China to South East Asia.

It was clear as day that during my time in China that companies were making a terrible mistake going into China in the first place.

This shows how many corporates are dragged down by a lack of vision and do an awful job of anticipating paradigm shifts that are becoming more common because of the accelerating rate of change of the corporate climate, weather, technology, rule of law, and human migration.

Netflix is effectively blocked from China and China has its own Netflix called iQIYI (IQ), they had no chance from the beginning like Google, Amazon, Facebook, and the many other American tech firms.

Netflix’s business model now has scale working for them and growth numbers will be the main recipients going forward if they focus on high quality content.

That means expect high pay packages to the best media talent in the world.

They can afford to pay a tier 1 actor $50 million per movie because the data buttresses this strategy.

At the same time, Netflix is crushing competition by hoarding the talent with extraordinary pay packages while allowing these highly paid specialists 100% creative control over what they do.

Who would want to work for a company that paid more than double and whose management gave them free reign on creative decisions?

Sounds like an artist’s dream and it’s exactly that for actors like Will Smith who have signed onto Netflix’s project.

I would even suggest that Netflix needs to overpay actors just for the reason of taking them off the market for competitors.

This truly is the lucrative golden age for actors, producers, and directors who are the top 1% of their craft, but for everyone else, it’s a hard slog.

This usually means becoming a tier 1 actor before the migration to online streaming happened.

The picture I am painting is that Netflix’s success and future prospects aren’t about Disney or other competitors, but entirely about them.

He who has the most chips at the table with the best cards is in best position to win and the same goes for Netflix.

The rest of the bunch like Apple (AAPL) and Disney who are late to the party will be feeding off the rest of what Netflix cannot exploit and that’s the best-case scenario.

Disney should be able to have moderate success with its array of great movie, television, and sports content.

I’d be surprised if Disney failed because they possess the ingredients to concoct a delicious cocktail.

Apple has a harder proposition because of the lack of entertainment value in their content. They are still tied to the hardware sales and much of the service sales come from their app store and servicing the hardware.

But Apple does have money, and a lot of it to throw at the problem, but I don’t believe CEO of Apple Tim Cook is the right man to navigate through the travails of the online content world. He’s an operations guy and has never proved anything more than that.

Netflix still has substantial opportunity to grow its brand and the runway is long.

The demand for watching great original movies and television programs without commercials whenever consumers want is still in the first innings.

Even though Disney will remove some non-original content from Netflix’s platform, the content spend on a massive pipeline of new projects will more than fill the void left by Disney’s content.

In fact, Netflix should thank Disney for all those years that Disney allowed them to build their brand through 3rd party premium content like the television program Friends.

I believe Netflix does not need 3rd party content anymore, that is how much Netflix has bolted ahead in the past few years.

The company has introduced price hikes with its 4K premium package going from $14 to $16 per month.

But Netflix is still underpricing itself to the consumer to grab market share, and there is still pricing headway in the future if the company wants it.

In the coming months, Netflix plans to offer more detailed reporting on its metrics and the transparency will give investors even more insight into why this company is brilliant.

I believe the numbers will show that Netflix is absolutely killing it.

As for the trading, Netflix has settled in a range of $320 to $380 and any dips to the $340 range should be quite appetizing.

Add incrementally and use any large dip to drop your cost basis.

Stand aside if you cannot handle heightened volatility.

Mad Hedge Technology Letter

July 1, 2019

Fiat Lux

Featured Trade:

(THE DEATH OF HARDWARE)

(AAPL), (CRM), (NFLX), (HUAWEI)

Apple’s Chief Design Officer Jony Ive, the British industrial designer who made Apple (AAPL) products beautiful, is on his way out.

What else could the man do?

Jonathan Paul Ive was born in Chingford, London in 2967 to a silversmith who lectured at Middlesex Polytechnic.

He pursed automotive design at Newcastle Polytechnic, now named University of Northumbria at Newcastle, and graduated with a BA in industrial design in 1989.

His student successes harvested him the RSA Student Design Award which gifted him a stipend for an exploratory trip to the United States.

Palo Alto, California was his ultimate destination where he befriended various design experts including Robert Brunner—a designer who ran a small consultancy firm that would later join Apple Computers.

Ive signed onto product design agency Roberts Weaver Group following his studies demonstrating his typical attention to detail that he became renowned for.

London startup design agency called Tangerine came calling and Ive used his talents to design microwave ovens, toilets, drills and toothbrushes.

Ive slammed into confict with management at Tangerine who believed his ideas were too modern and exorbitant.

Apple later decided to partner with Tangerine on the basis of some of Ive’s former Silicon Valley friends like Robert Brunner delivering Ive to the forefront of Apple design products where he started hatching his plan to be the ultimate designer at Apple.

The rest is history as Ive went on to produce memorable consumer product designs such as the iMac, iPod, iPhone, and iPad.

His last burst of creativity was applied to produce the Apple Watch which was an overwhelming success.

He will now take his show independent but still collaborate with Apple as his main client.

The new design firm will be called LoveFrom.

This announcement isn’t a shocker and certainly, he really had one foot out of the door ever since the passing of Former Co-Founder Steve Jobs in 2011 put him on less solid footing.

If you remember, Apple had a secret corridor constructed between Jobs' and Ive’s office epitomizing how closely they collaborated on product development as well as how good of friends they were.

Current CEO of Apple Tim Cook is the exact opposite of what Steve Jobs represented and part of the reason why Apple has lacked that game-changing new product resulting in a reduced share price.

Steve Jobs was a visionary and the person to transform his ideas into physical form was Jony Ive.

You could argue that part of Jony Ive succumbed with Steve Jobs as well as his parabolic career trajectory.

That’s what all those lines of people camping overnight in front of Apple stores was about.

The cult of Apple was at its peak around 2012 where Apple sold the most iPhones and was miles ahead of competition.

Fast forward 7 years and Tim Cook has allowed the relative competition to catch up and even overtake Apple in numerous metrics.

I would argue that Tim Cook was a dependent stop gap to Steve Jobs but the lack of vision in a position where visionaries are rewarded has been Apple’s Achilles heel.

Surely, Apple could have hired an Elon Musk after Tim Cook steadied the rutter.

The results have been monetary success, milking the famed iPhone business for what it’s worth plus more, but missing the boat on premium content.

They could have bought Netflix (NFLX) while it was less potent with the glut of cash in reserve, or they could have penetrated the enterprise business with acquiring Salesforce (CRM) at an earlier stage.

And during this period, Chinese phone makers caught up big time with Huawei now offering a better and cheaper iPhone alternative.

What Jony Ive was leaving the headquarters of Apple represents is the death of hardware.

Out with the old and in the new, and the new is software and the direction Apple is doubling down on.

Apple's services of iTunes, the App Store, the Mac App Store, Apple Music, Apple Pay, and AppleCare, has become Apple’s “new” business.

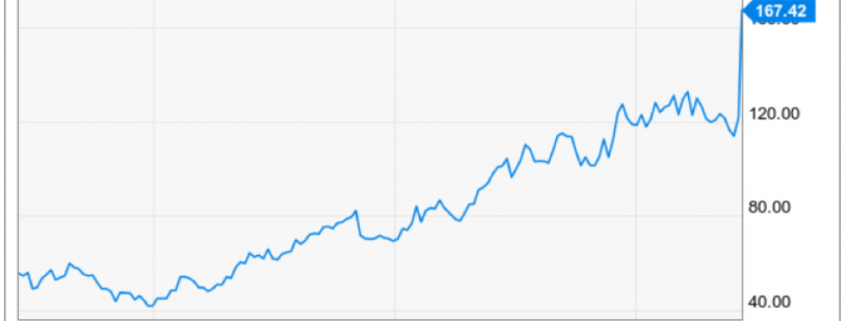

Apple's services segment did sales of $11.5 billion in revenue, up from the $9.9 billion services earned in the second quarter of 2018.

A new all-time record was set for services revenue this quarter.

Apple Pay is available in 30 markets and expect to go live in 40 markets by the end of 2019.

Apple now boasts 390 million paid subscriptions across all of its services, an increase of 30 million sequentially and by 2020, Apple will pass half a million paid subscriptions.

Apple hopes to penetrate further into the magazine business with Apple News+, a $9.99 per month service that offers unlimited access to more than 200 magazines.

Apple plans to surpass $14 billion in services revenue per quarter by 2020.

This is what Apple is doing now and the sad fact is that Ive and his special skills do not fit seamlessly into the main growth drivers of the company anymore.

Software engineers are being cherrypicked left, right, and center as Apple avoids making any big capital investments aside from leasing new buildings to install an army of fresh programmers.

Apple reported $11.45 billion in services revenue topped analysts’ expectations of $11.37 billion.

Apple also reported services margins of 63.8% for the quarter.

Services now accounts for about 20% of Apple’s revenue, up from 16% a year earlier and 13% in the first quarter.

I will give Tim Cook credit for recovering from the 20% drop in Apple’s shares, better late than never.

Now Apple is in the process of shifting up to 30% of their supply chain from China to South East Asia to de-risk from the Middle Kingdom.

Mad Hedge Technology Letter

June 11, 2019

Fiat Lux

Featured Trade:

(BIG TECH’S FEEDING FRENZY)

(CRM), (DATA), (GOOGL), (NFLX)

The start of the cloud consolidation is upon us.

The cloud kings, in order to stay ahead of the competition, are resorting to acquiring growth through M&A.

We are still in the sweet part of the growth phase with companies showing they can pull off a mid-20% annual growth rate.

Salesforce (CRM), the leader in client relationships management platforms, took this cue to add to its army of software cloud options by snapping up Tableau (DATA).

What does Tableau do?

Tableau software takes the inputs of raw data and transforms it into easily decipherable dashboards and diagrams.

The company has been expanding its product line to include data cleanup and machine learning tools, enabling it to compete in the wider data-warehousing business.

It has more than 86,000 customers, including Verizon Communications Inc. and Netflix (NFLX).

Let me remind you why big data companies are the golden goose of the technology industry and why they are intrinsic to the fortunes of tech companies.

The idea of big data has been around for years; most organizations now are acutely aware that if they capture all the data that flows into their businesses, they can apply data analytics and generate value creation by making the best strategic decisions suggested from the underlying data.

If upper management hasn’t figured this out yet, they are probably out of business by now.

Let’s roll back to the 1950s, decades before anyone coined the term “big data,” businesses were using rudimentary analytics, basically numbers in a spreadsheet that were manually registered, to unearth paradigm shifts and market opportunities in their industry.

The smorgasbord of goodies that big data analytics offer the world is legendary.

Speed and efficiency are at the top of the list.

Whereas a few years ago, collecting vital information that could be used for future decisions took pace much slower than today.

Identifying insights for immediate actionable business implementation is happening in real time now.

This new mode of execution and organization offers firms an outsized competitive edge they could only dream of.

Harnessing data and utilizing it in the best way in order to monetize its business model is now the norm.

The end result is repeatedly higher trending profits and better customer experience.

Companies and its expenses were also reaping the rewards of this new model with major cost reduction.

Big data technologies can expect significant cost advantages when it comes to storing large amounts of data – plus they can identify more efficient ways of doing business.

Companies now have the pulse of the market and demonstrate the ability to gauge customer needs and satisfaction allowing the company to identify new markets.

This, in turn, has firms often migrating into completely different parts of the economy.

Salesforce’s deal with Tableau isn’t the first and won’t be the last cloud deal.

This is just the beginning.

The decision comes after Google (GOOGL) agreed to buy Looker Data Sciences Inc. for $2.6 billion last week, a move to expand Google’s offerings for managing data in the cloud.

I envision Google wading further into the enterprise software waters as they attempt to relieve their reliance on Search as the primary money maker.

Acquiring the best software then spreading its application through its other assets would be a great initiative too.

For example, creating an enterprise service for YouTube channels and charging YouTube creators a fee to operate a cloud-based product that specializes in optimizing their YouTube channel would be a compelling idea.

There are a million different machinations that Google could elect for, and letting the genie out of the bottle in a good way will do wonders.

After all, global spending on technologies and services that enable digital transformation will surpass $2 trillion in 2022 serving up a long and wide runway for companies that can hunker down and carve out premium enterprise software on the cloud.

As for Salesforce, the stock sold off on anxiety that Salesforce is overreaching to add growth.

There is definitely some truth behind this weakness.

Could this be the end for Salesforce’s growth supercycle?

Salesforce is a pure software growth strategy and the stock has gone nowhere trading sideways for the past 6 months.

Make no bones about it, Salesforce absolutely overpaid for Tableau and even announced that its second headquarter will be stationed in Seattle, a stone’s throw from the headquarter of Tableau.

Founder and Co-CEO of Salesforce Marc Benioff is betting the ranch on data analytics and hopes the subsequent synergies will result in cost savings, better cloud products, a resurgence in revenue growth while wielding a first-rate army of software engineers.

As for now, even the tech market is single-handedly propped up by the Fed who have signaled even more dovish monetary policy.

Wait to read the tea leaves on whether these new additions to Salesforce will meaningfully result in growth or not.

For the time being, Salesforce and tech remain in a precarious position whipsawing because of Trump’s high-risk geopolitical strategy and the Fed attempting to cushion any economic blows from an administration hellbent on tariffs.